N-4

Dec. 31, 2025

USD ($)

Years

|

Important Information You Should Consider About the Contract

|

|||

|

Fees, Expenses, and Adjustments

|

|||

|

Are there Charges or Adjustments for Early Withdrawals?

|

Yes.

Surrender Charges: If you withdraw money from the Contract within 6 years following your last Purchase Payment, you may be assessed a surrender charge. The maximum surrender charge is 8.0% of the Purchase Payment, and a surrender charge may be assessed up to 6 years after the last Purchase Payment. If you make an early withdrawal, you could pay a surrender charge of up to $8,000 on a $100,000 withdrawal. Losses from surrender charges will be greater if there are also negative Interim Value adjustments, taxes, or tax penalties. Interim Value Adjustments: If all or a portion of Account Value is removed from an Index Strategy before the end of the Index Strategy Term, we will apply an Interim Value adjustment, which may be negative. In extreme circumstances, you could lose up to 100% of your investment in an Index Strategy due to a negative Interim Value adjustment. For example, if you allocate $100,000 to an Index Strategy with a 3-year Strategy Term and later make a withdrawal before the 3 years have ended, you could lose your $100,000 investment. Losses from negative Interim Value adjustments will be greater if you also have to pay a surrender charge, taxes, or tax penalties. An Interim Value adjustment will apply upon any withdrawal, death benefit payment, transfer, Annuitization, or surrender that occurs during an Index Strategy Term other than on the Index Strategy Start Date or Index Strategy End Date. For more information on surrender charges and Interim Value adjustments, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus. |

||

|

Are there Transaction Charges?

|

Yes.

In addition to surrender charges and Interim Value adjustments, you may be charged for additional copies of reports. For more information, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus. |

||

|

Important Information You Should Consider About the Contract

|

|||

|

Fees, Expenses, and Adjustments

|

|||

|

Are there Ongoing Fees and Expenses?

|

Yes.

The table below describes the fees and expenses that you may pay each year, depending on the investment options you choose. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have elected. There is an implicit ongoing fee on the Index Strategies to the extent that an Index Strategy’s Cap Rate, Spread, Participation Rate, or Step Rate, as applicable, limit the positive Index Return used in calculating the Index Credit that may be applied to an Index Strategy at the end of an Index Strategy Term. This means that your returns may be lower than the Index Return. In return for accepting this limit on Index gains, you will receive some protection from Index losses. This implicit ongoing fee is not reflected in the tables below. |

||

|

Annual Fee

|

Minimum

|

Maximum

|

|

|

Base Contract Fees

|

1.20%(1)

|

1.30%(1)

|

|

|

Portfolio Company fees and expenses

|

0.57%

|

1.25%

|

|

|

Optional benefits available for an additional charge

(for a single optional benefit, if elected) |

None.

|

None.

|

|

|

(1) Insurance Charge: a percentage of the net assets of the Variable Option. For Purchase Payments equal to or greater than $1,000,000 the charge will be 1.20%.

|

|||

|

Because your Contract is customizable, the choices you make affect how much you will pay. To help you understand the cost of owning your Contract, the following table shows the lowest and highest cost you could pay each year, based on current charges. This estimate assumes that you do not take withdrawals from the Contract, which could add surrender charges and negative Interim Value adjustments that substantially increase costs.

|

|||

|

Lowest Annual Cost

$1,912 |

Highest Annual Cost

$2,601 |

|

|

|

Assumes:

|

Assumes:

|

|

|

|

For more information on ongoing fees and expenses, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus.

|

|||

Are there Charges or Adjustments for Early Withdrawals?

Yes.

Surrender Charges: If you withdraw money from the Contract within 6 years following your last Purchase Payment, you may be assessed a surrender charge. The maximum surrender charge is 8.0% of the Purchase Payment, and a surrender charge may be assessed up to 6 years after the last Purchase Payment. If you make an early withdrawal, you could pay a surrender charge of up to $8,000 on a $100,000 withdrawal. Losses from surrender charges will be greater if there are also negative Interim Value adjustments, taxes, or tax penalties.

Interim Value Adjustments: If all or a portion of Account Value is removed from an Index Strategy before the end of the Index Strategy Term, we will apply an Interim Value adjustment, which may be negative. In extreme circumstances, you could lose up to 100% of your investment in an Index Strategy due to a negative Interim Value adjustment. For example, if you allocate $100,000 to an Index Strategy with a 3-year Strategy Term and later make a withdrawal before the 3 years have ended, you could lose your $100,000 investment. Losses from negative Interim Value adjustments will be greater if you also have to pay a surrender charge, taxes, or tax penalties. An Interim Value adjustment will apply upon any withdrawal, death benefit payment, transfer, Annuitization, or surrender that occurs during an Index Strategy Term other than on the Index Strategy Start Date or Index Strategy End Date.

For more information on surrender charges and Interim Value adjustments, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus.

Surrender Charges: If you withdraw money from the Contract within 6 years following your last Purchase Payment, you may be assessed a surrender charge. The maximum surrender charge is 8.0% of the Purchase Payment, and a surrender charge may be assessed up to 6 years after the last Purchase Payment. If you make an early withdrawal, you could pay a surrender charge of up to $8,000 on a $100,000 withdrawal. Losses from surrender charges will be greater if there are also negative Interim Value adjustments, taxes, or tax penalties.

Interim Value Adjustments: If all or a portion of Account Value is removed from an Index Strategy before the end of the Index Strategy Term, we will apply an Interim Value adjustment, which may be negative. In extreme circumstances, you could lose up to 100% of your investment in an Index Strategy due to a negative Interim Value adjustment. For example, if you allocate $100,000 to an Index Strategy with a 3-year Strategy Term and later make a withdrawal before the 3 years have ended, you could lose your $100,000 investment. Losses from negative Interim Value adjustments will be greater if you also have to pay a surrender charge, taxes, or tax penalties. An Interim Value adjustment will apply upon any withdrawal, death benefit payment, transfer, Annuitization, or surrender that occurs during an Index Strategy Term other than on the Index Strategy Start Date or Index Strategy End Date.

For more information on surrender charges and Interim Value adjustments, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus.

Are there Transaction Charges?

Yes.

In addition to surrender charges and Interim Value adjustments, you may be charged for additional copies of reports. For more information, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus.

In addition to surrender charges and Interim Value adjustments, you may be charged for additional copies of reports. For more information, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus.

Are there Ongoing Fees and Expenses?

Yes.

The table below describes the fees and expenses that you may pay each year, depending on the investment options you choose. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have elected.

There is an implicit ongoing fee on the Index Strategies to the extent that an Index Strategy’s Cap Rate, Spread, Participation Rate, or Step Rate, as applicable, limit the positive Index Return used in calculating the Index Credit that may be applied to an Index Strategy at the end of an Index Strategy Term. This means that your returns may be lower than the Index Return. In return for accepting this limit on Index gains, you will receive some protection from Index losses. This implicit ongoing fee is not reflected in the tables below.

The table below describes the fees and expenses that you may pay each year, depending on the investment options you choose. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have elected.

There is an implicit ongoing fee on the Index Strategies to the extent that an Index Strategy’s Cap Rate, Spread, Participation Rate, or Step Rate, as applicable, limit the positive Index Return used in calculating the Index Credit that may be applied to an Index Strategy at the end of an Index Strategy Term. This means that your returns may be lower than the Index Return. In return for accepting this limit on Index gains, you will receive some protection from Index losses. This implicit ongoing fee is not reflected in the tables below.

Annual Fee

Minimum

Maximum

Base Contract Fees

1.20%(1)

1.30%(1)

Portfolio Company fees and expenses

0.57%

1.25%

Optional benefits available for an additional charge

(for a single optional benefit, if elected)

(for a single optional benefit, if elected)

None.

None.

(1) Insurance Charge: a percentage of the net assets of the Variable Option. For Purchase Payments equal to or greater than $1,000,000 the charge will be 1.20%.

Because your Contract is customizable, the choices you make affect how much you will pay. To help you understand the cost of owning your Contract, the following table shows the lowest and highest cost you could pay each year, based on current charges. This estimate assumes that you do not take withdrawals from the Contract, which could add surrender charges and negative Interim Value adjustments that substantially increase costs.

Lowest Annual Cost

$1,912

$1,912

Highest Annual Cost

$2,601

$2,601

Assumes:

-

Investment of $100,000

-

5% annual appreciation

-

Least expensive Portfolio fees and

expenses

-

No optional benefits

-

No sales charges

-

No subsequent Purchase Payments, transfers or withdrawals

Assumes:

-

Investment of $100,000

-

5% annual appreciation

-

Most expensive combination of optional benefits and Portfolio fees and expenses

-

No sales charges

-

No subsequent Purchase Payments, transfers or withdrawals

For more information on ongoing fees and expenses, please refer to the “Fee Table” and “Charges and Adjustments” sections of this prospectus.

Risks

Is there a Risk of Loss from Poor Performance?

Yes.

You can lose money by investing in the Contract. Under an Index Strategy, the maximum amount of loss that you could experience from negative Index performance at the end of an Index Strategy Term, after taking into account the current limits on Index loss provided under the Contract, is: 95% loss for a 5% Buffer; 90% loss for a 10% Buffer; 85% loss for a 15% Buffer; 80% loss for a 20% Buffer; 70% loss for a 30% Buffer; or 0% loss for a 100% Buffer.

The Company does not guarantee that the Contract will always offer Index Strategies that limit Index losses, which would mean a risk of loss of the entire amount invested.

For more information on the risk of loss, please refer to the “Principal Risks of Investing in the Contract” section of this prospectus.

You can lose money by investing in the Contract. Under an Index Strategy, the maximum amount of loss that you could experience from negative Index performance at the end of an Index Strategy Term, after taking into account the current limits on Index loss provided under the Contract, is: 95% loss for a 5% Buffer; 90% loss for a 10% Buffer; 85% loss for a 15% Buffer; 80% loss for a 20% Buffer; 70% loss for a 30% Buffer; or 0% loss for a 100% Buffer.

The Company does not guarantee that the Contract will always offer Index Strategies that limit Index losses, which would mean a risk of loss of the entire amount invested.

For more information on the risk of loss, please refer to the “Principal Risks of Investing in the Contract” section of this prospectus.

Is this a Short-Term Investment?

No.

The Contract is not a short-term investment and is not appropriate for an investor who needs ready access to cash. The Contract is designed to provide benefits on a long-term basis. Because of the long-term nature of the Contract, you should consider whether the Contract is consistent with your financial situation and objectives.

Amounts withdrawn from the Contract may result in surrender charges, taxes and tax penalties. In addition, removing amounts from an Index Strategy prior to the Index Strategy End Date may result in a negative Interim Value adjustment and loss of positive Index performance.

Removing a portion of amounts in an Index Strategy prior to the Index Strategy End Date will also result in an immediate reduction to your Index Strategy Base. The Index Strategy Base will be proportionately reduced, and the proportionate reduction could be greater than the amount removed. Reductions to your Index Strategy Base will result in lower Interim Values for the remainder of the Index Strategy Term and less positive Index Credit (if any) on the Index Strategy End Date.

At the end of an Index Strategy Term, amounts in the matured Index Strategy will be reallocated, withdrawn or otherwise processed according to your instructions. You must provide instructions for reallocation by the Index Anniversary Date corresponding to the Index Strategy End Date. In the absence of instructions, if the same Index Strategy is available, amounts in the matured Index Strategy will be automatically re-invested in the same Index Strategy for a new Index Strategy Term. During the Savings Stage, if the same Index Strategy is no longer available, amounts in the matured Index Strategy will be automatically transferred to the Holding Account, and the amount may be transferred into another Index Strategy on the next Index Anniversary Date.

For more information on the short-term investment risks, please refer to the “Principal Risks of Investing in the Contract”,“Charges and Adjustments” and “General Description of Contracts - Transfer and Reallocation Guidelines” sections of this prospectus.

The Contract is not a short-term investment and is not appropriate for an investor who needs ready access to cash. The Contract is designed to provide benefits on a long-term basis. Because of the long-term nature of the Contract, you should consider whether the Contract is consistent with your financial situation and objectives.

Amounts withdrawn from the Contract may result in surrender charges, taxes and tax penalties. In addition, removing amounts from an Index Strategy prior to the Index Strategy End Date may result in a negative Interim Value adjustment and loss of positive Index performance.

Removing a portion of amounts in an Index Strategy prior to the Index Strategy End Date will also result in an immediate reduction to your Index Strategy Base. The Index Strategy Base will be proportionately reduced, and the proportionate reduction could be greater than the amount removed. Reductions to your Index Strategy Base will result in lower Interim Values for the remainder of the Index Strategy Term and less positive Index Credit (if any) on the Index Strategy End Date.

At the end of an Index Strategy Term, amounts in the matured Index Strategy will be reallocated, withdrawn or otherwise processed according to your instructions. You must provide instructions for reallocation by the Index Anniversary Date corresponding to the Index Strategy End Date. In the absence of instructions, if the same Index Strategy is available, amounts in the matured Index Strategy will be automatically re-invested in the same Index Strategy for a new Index Strategy Term. During the Savings Stage, if the same Index Strategy is no longer available, amounts in the matured Index Strategy will be automatically transferred to the Holding Account, and the amount may be transferred into another Index Strategy on the next Index Anniversary Date.

For more information on the short-term investment risks, please refer to the “Principal Risks of Investing in the Contract”,“Charges and Adjustments” and “General Description of Contracts - Transfer and Reallocation Guidelines” sections of this prospectus.

What are the Risks Associated with the Investment Options?

An investment in the Contract is subject to the risk of poor investment performance and can vary depending on the performance of the investment options available under the Contract, including the Index Strategies, and the Variable Options. Each investment option has its own unique risks. You should review the investment options before making an investment decision.

For the Index Strategies:

For the Index Strategies:

-

The Cap Rate, Spread, Participation Rate or Step Rate, as applicable, may limit positive Index Credits (i.e., limited upside). This may result in you earning less than the Index Return. For example:

-

Point-to-Point with Cap Index Strategy. Assuming a Cap Rate of 5% and an Index Return of 10% (which is greater than the Cap Rate), we will apply a 5% Index Credit at the end of the Index Strategy Term.

-

Enhanced Cap Rate Index Strategy. Assuming a Spread of 2%, Cap Rate of 15% and Index Return of 18% (which is greater than the Cap Rate plus the Spread), we will apply a 15% Index Credit at the end of the Index Strategy Term. If the Index Return is instead 10% (which is less than the Cap Rate plus the Spread), we will deduct the Spread from the Index Return and apply an 8% Index Credit at the end of the Index Strategy Term. If the Index Return is instead 1% (which is greater than zero but less than the Spread), the Index Credit would be 0%.

-

Step Rate Plus Index Strategy. Assume the Step Rate is 4% and the Participation Rate is 60%. If the Index Return is 5%, we will apply the Step Rate to calculate the Index Credit because the Step Rate (4%) is greater than the Index Return multiplied by the Participation Rate (5% x 60% = 3%). The Index Credit at the end of the Index Strategy Term will be 4%. If the Index Return is instead 10%, we will apply the Participation Rate rather than the Step Rate because the Index Return multiplied by the Participation Rate (10% x 60% = 6%) will be greater than the Step Rate (4%). The Index Credit at the end of the Index Strategy Term will be 6%.

-

Dual Directional Index Strategy. Assuming a Cap Rate of 4% and an Index Return of 8% (which is greater than the Cap Rate), we will apply a 4% Index Credit at the end of the Index Strategy Term.

-

The Buffer may limit negative Index Credits (i.e., limited protection in the case of market decline). For example, if the Index Return is -25% and the Buffer is 10%, we will apply a -15% Index Credit (the amount of negative Index Return that exceeds the Buffer) at the end of the Index Strategy Term.

-

There may be losses due to surrender charges, negative Interim Value adjustments, and taxes and tax penalties.

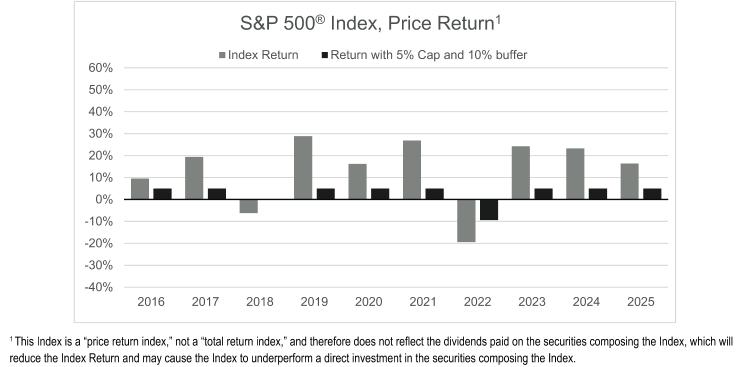

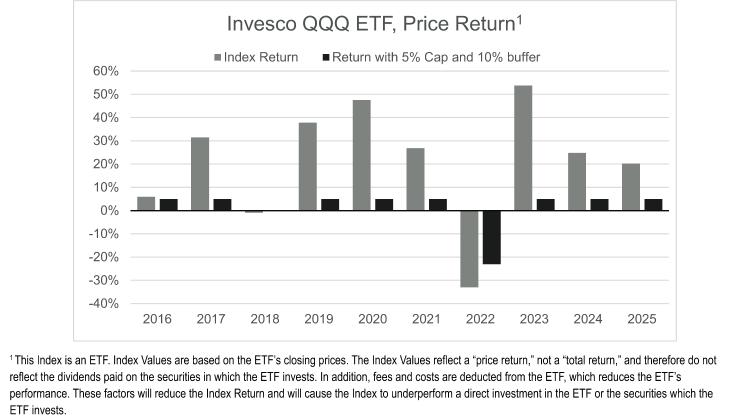

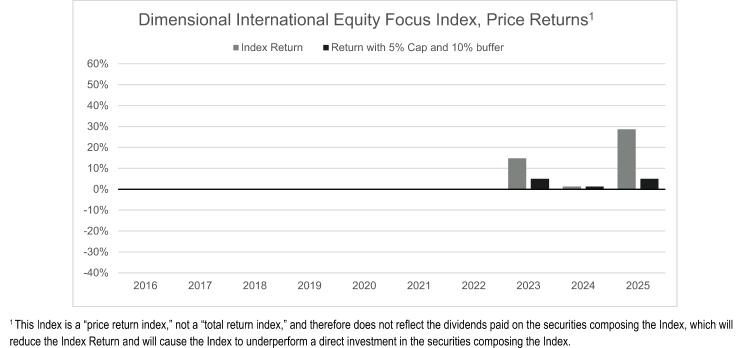

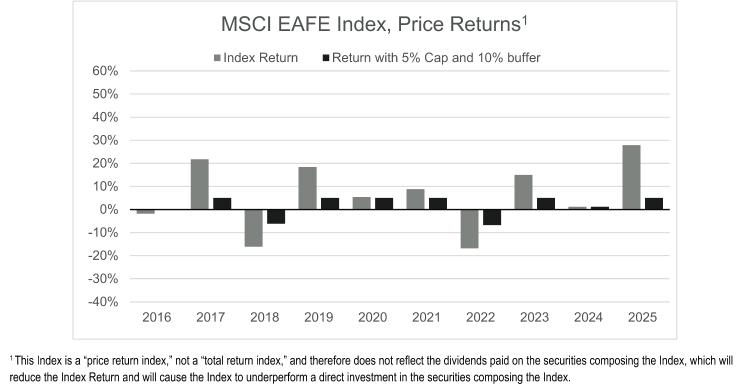

Index performance is on a “price return” basis, not a “total return” basis, and therefore does not reflect dividends paid on the securities composing the Index. In addition, if the Index is an exchange-traded fund (ETF), the ETF deducts fees and costs that reduce Index performance. These factors will reduce the Index Return and may cause the Index to underperform a direct investment in the securities composing the Index.

For more information on the risks associated with investment options, please refer to the “Principal Risks of Investing in the Contract” and “Appendix A” sections of this prospectus.

What are the Risks Related to the Insurance Company?

An investment in the Contract is subject to the risks related to the Company. Any obligations (including under the Index Strategies), guarantees, or benefits are subject to the claims-paying ability of the Company. More information about the Company, including its financial strength ratings, is available upon request. Such requests can be made toll-free at 1-888-PRU-2888.

For more information on the insurance company risks, please refer to the “Principal Risks of Investing in the Contract” section of this prospectus.

For more information on the insurance company risks, please refer to the “Principal Risks of Investing in the Contract” section of this prospectus.

Yes.

There are restrictions that may limit the investment options that you may choose, and there are limitations on the transfer of Account Value among investment options.

There are restrictions that may limit the investment options that you may choose, and there are limitations on the transfer of Account Value among investment options.

-

Account Value may be transferred to an Index Strategy, or among Index Strategies, only on an Index Strategy End Date.

-

Account Value in the Variable Option may be transferred to an Index Strategy only on an Index Anniversary Date.

-

During the Savings Stage, Account Value transferred from an Index Strategy to the Variable Option prior to the Index Strategy End Date will result in an Interim Value adjustment, which may be negative.

-

During the Income Stage, no Index Strategies are available other than the 1-year Point-to-Point with Cap, 1-year Dual Directional, 1-year Step Rate Plus, and 1-year Enhanced Cap Rate* Index Strategies. The Variable Options are not available during the Income Stage. We reserve the right to:

-

Remove or substitute Portfolios and close the Variable Option;

-

Add or remove Index Strategies (there is no guarantee that any Index Strategy will be available in the future);

-

Change the features of an Index Strategy from one Index Strategy Term to the next, including the Index, Cap Rate, Spread, Participation Rate, Step Rate, and Buffer, as applicable, subject to any minimum guarantees; and

-

Substitute the Index of an Index Strategy during its Index Strategy Term.

We may impose limitations on an investment professional’s or investment advisor’s ability to request financial transactions on your behalf.

*Enhanced Cap Rate Index Strategies are only available on annuities with an Application Sign Date on or after July 1, 2024.

Certain Investment Options may not be available through certain financial intermediaries. See Appendix F, “Financial Intermediary Variations’” and the Cover Page of this prospectus for additional information.

For more information on investment and transfer restrictions, please refer to the “Principal Risks of Investing in the Contract”, “Investment Options”, “General Description of Contracts – Transfer and Reallocation Guidelines”, “What are the Separate Accounts”, “Financial Professional Permission to Forward Transaction Instructions”, and “Appendix A” sections of this prospectus.

*Enhanced Cap Rate Index Strategies are only available on annuities with an Application Sign Date on or after July 1, 2024.

Certain Investment Options may not be available through certain financial intermediaries. See Appendix F, “Financial Intermediary Variations’” and the Cover Page of this prospectus for additional information.

For more information on investment and transfer restrictions, please refer to the “Principal Risks of Investing in the Contract”, “Investment Options”, “General Description of Contracts – Transfer and Reallocation Guidelines”, “What are the Separate Accounts”, “Financial Professional Permission to Forward Transaction Instructions”, and “Appendix A” sections of this prospectus.

Certain Contract Benefits may not be available through certain financial intermediaries. See, Appendix F, “Financial Intermediary Variations” and the Cover Page of this prospectus for additional information.

You should consult with a tax professional to determine the tax implications of an investment in and payments received under the Contract. There is no additional tax benefit if you purchase the Contract through a tax-qualified plan or individual retirement account (IRA). Withdrawals will be subject to ordinary income tax, and may be subject to a 10% additional tax for distributions taken prior to age 59½.

For more information on tax implications, please refer to the “Taxes” section of this prospectus.

For more information on tax implications, please refer to the “Taxes” section of this prospectus.

Investment professionals may receive compensation for selling the Contract to investors and may have a financial incentive to offer or recommend the Contract over another investment. This compensation is paid in the form of commissions, based on the amount of your investment in the Contract.

For more information on investment professional compensation, please refer to the Statement of Additional Information.

For more information on investment professional compensation, please refer to the Statement of Additional Information.

Some investment professionals may have a financial incentive to offer you a Contract in place of the one you already own. You should only exchange your contract if you determine after comparing the features, fees, and risks of both contracts, and any fees or penalties to terminate the existing contract, that it is preferable to purchase the new contract, rather than continue to own your existing contract.

For more information on exchanges, please refer to the Statement of Additional Information.

For more information on exchanges, please refer to the Statement of Additional Information.

FEE TABLE

The following tables describe the fees, expenses, and adjustments that you will pay when buying, owning, and surrendering or making withdrawals from an Investment Option or from the Contract. Please refer to your Annuity specifications page for information about the specific fees you will pay each year based on the options you have elected.

The first table describes the fees and expenses that you will pay at the time that you buy the Annuity, surrender or make withdrawals from an Investment Option or from the Annuity, or transfer Account Value between Investment Options, where applicable. State premium taxes may also be deducted. These fees and charges are described in more detail within this prospectus in the "Charges and Adjustments" section.

|

Transaction Expenses

|

Maximum

|

|

Sales Charge Imposed on Purchases

|

None

|

|

Deferred Sales Charge (as a percentage of each Purchase Payment)1

|

7.00%

|

|

Transfer Fee

|

None

|

|

Additional Copies of Reports

|

$50

|

|

|

Age of Purchase Payment Being Withdrawn*

|

Percentage Applied Against Purchase Payment being Withdrawn

|

|

|

|

Less than 1 year old

|

7.0%

|

|

|

|

1 year old or older but not yet 2 years old

|

7.0%

|

|

|

|

2 years old or older but not yet 3 years old

|

6.0%

|

|

|

|

3 years old or older but not yet 4 years old

|

5.0%

|

|

|

|

4 years old or older but not yet 5 years old

|

4.0%

|

|

|

|

5 years old or older but not yet 6 years old

|

3.0%

|

|

|

|

6 years old or older

|

0.0%

|

|

|

Transaction Expenses

|

Maximum

|

|

Sales Charge Imposed on Purchases

|

None

|

|

Deferred Sales Charge (as a percentage applied against Purchase Payment being withdrawn)1

|

8.00%

|

|

Transfer Fee

|

None

|

|

Additional Copies of Reports

|

$50

|

|

|

Age of Purchase Payment Being Withdrawn*

|

Percentage Applied Against Purchase Payment being Withdrawn

|

|

|

|

Less than 1 year old

|

8.0%

|

|

|

|

1 year old or older but not yet 2 years old

|

8.0%

|

|

|

|

2 years old or older but not yet 3 years old

|

7.0%

|

|

|

|

3 years old or older but not yet 4 years old

|

6.0%

|

|

|

|

4 years old or older but not yet 5 years old

|

5.0%

|

|

|

|

5 years old or older but not yet 6 years old

|

4.0%

|

|

|

|

6 years old or older

|

0.0%

|

|

The next table describes the adjustments, in addition to any transaction expenses, that apply if all or a portion of the Account Value is removed from an Index Strategy before the expiration of an Index Strategy Term.

|

Adjustments

|

Maximum

|

|

Interim Value Adjustment Maximum Potential Loss (as a percentage of your investment in an Index Strategy)1

|

100%

|

The next table describes the maximum fees and expenses that you will pay each year during the time that you own the Contract (not including Portfolio fees and expenses). Your current fees and expenses may be less than the maximum.

|

Annual Contract Expenses

|

Current

|

Maximum

|

|

Base Contract1,2

|

1.30%3

|

1.30%

|

|

In addition to the fees described above, we limit the amount you can earn on the Index Strategies. This means your Index Credit may be lower than the Index Return. In return for accepting this limit on Index gains, you will receive some protection from Index losses.

|

The next item shows the minimum and maximum total operating expenses charged by the Portfolios that you may pay periodically during the time that you own the Annuity. Expenses may change over time and may be higher or lower in the future. More information about the Portfolios, including their annual expenses, may be found in "Appendix A" of this prospectus.

|

Annual Portfolio Expenses

|

||

|

(expenses that are deducted from Portfolio assets, including management fees, distribution and/or service (12b-1) fees, and other expenses)

|

Minimum

|

Maximum

|

|

0.57%

|

1.25%

|

|

|

Adjustments

|

Maximum

|

|

Interim Value Adjustment Maximum Potential Loss (as a percentage of your investment in an Index Strategy)1

|

100%

|

|

Annual Contract Expenses

|

Current

|

Maximum

|

|

Base Contract1,2

|

1.30%3

|

1.30%

|

|

Annual Portfolio Expenses

|

||

|

(expenses that are deducted from Portfolio assets, including management fees, distribution and/or service (12b-1) fees, and other expenses)

|

Minimum

|

Maximum

|

|

0.57%

|

1.25%

|

|

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT

The risks identified below are the principal risks of investing in the Annuity. The Annuity may be subject to additional risks other than those identified and described in this prospectus.

Risk of Loss: You could lose money by investing in the Annuity, including your principal investment. An investment in the Annuity is not a deposit with a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Buffer Risk: You take the investment risk for amounts allocated to one or more Index Strategies since the Index Credit is based upon the performance of the associated Index. You could lose a significant amount of money if the Index declines in value. We limit the negative Index Return used in calculating Index Credit applied to an Index Strategy at the end of its Index Strategy Term through a Buffer. The Buffer is the amount of protected negative Index Return. Any negative Index Return in excess of the Buffer reduces the Account Value allocated to the Index Strategy (i.e., the protection from negative Index performance is limited). You bear the risk of the negative Index Return in excess of the Buffer you choose. In the case of a multi-year Index Strategy Term, losses are measured over the entire Index Strategy Term from the Index Strategy Start Date to the Index Strategy End Date and may exceed the Buffer levels associated with the Index Strategy. Sustained negative Index Returns may result in zero or negative Index Credits over multiple Index Strategy Terms.

Under an Index Strategy, the maximum amount of loss that you could experience from negative Index performance at the end of an Index Strategy Term, after taking into account the current limits on Index loss provided under the Annuity, is: 95% loss for a 5% Buffer; 90% loss for a 10% Buffer; 85% loss for a 15% Buffer; 80% loss for a 20% Buffer; 70% loss for a 30% Buffer or 0% loss for a 100% Buffer. The Company does not guarantee that the Annuity will always offer Index Strategies that limit Index losses, which would mean risk of loss of the entire amount invested.

Cap Rate Risk: If you elect a Point-to-Point with Cap Rate or Enhanced Cap Rate Index Strategy, a positive Index Credit may be limited by the applicable Cap Rate, which means that your Index Credit could be lower than the Index Return. The Cap Rate exists for the full term of the Index Strategy. Cap Rates, upon renewal, may be higher or lower than the initial Cap Rate but will never be less than the Guaranteed Minimum Cap Rate. Renewal Cap Rates may differ from the Cap Rates used for new Annuity contracts or for other Annuity contracts issued at different times. No Index Strategy guarantees a positive Index Credit.

If you elect a Dual Directional Index Strategy, a positive Index Return may be limited by the applicable Cap Rate. However, if the Index Return is negative and is within or equal to the Buffer, then the Index Credit would not be limited by the applicable Cap Rate. Cap Rates for the Dual Directional Index Strategy will be equal to or lower than the Cap Rate in the Point to Point with Cap Rate Index Strategy. Cap Rates will never be less than the Guaranteed Minimum Cap Rates. The Guaranteed Minimum Cap Rate equals 1.00% for a one-year Index Strategy Term, 5.00% for a three-year Index Strategy Term and 10.00% for a six-year Index Strategy Term. Cap Rates for new Index Strategy Terms are declared at our discretion, subject to applicable guarantees. You bear the risk that we will not declare a Cap Rate above the Guaranteed Minimum Cap Rate.

Step Rate Plus Risk: If you elect a Step Rate Plus Index Strategy, a positive Index Credit may be limited by the applicable Step Rate or Participation Rate, which means that your Index Credit could be lower than the Index Return. The Step Rate and Participation Rate exist for the full term of the Index Strategy. Step Rates and Participation Rates, upon renewal, may be higher or lower than the initial Step Rate or Participation Rate but will never be less than the Guaranteed Minimum Step Rate and Guaranteed Minimum Participation Rate, respectively. Renewal Step Rates or Participation Rates may differ from the Step Rates or Participation Rates used for new Annuity contracts or for other Annuity contracts issued at different times. No Index Strategy guarantees a positive Index Credit.

For Step Rate Plus Index Strategies, the Guaranteed Minimum Step Rate equals 1% and the Guaranteed Minimum Participation Rate equals 60%. Step Rates and Participation Rates for new Index Strategy Terms are declared at our discretion, subject to applicable guarantees. You bear the risk that we will not declare a Step Rate or Participation Rate above the guaranteed minimum

Tiered Participation Rate Risk: If you elect a Tiered Participation Rate Index Strategy, a positive Index Credit will be calculated using the applicable 1st Tier Participation Rate, 2nd Tier Participation Rate, and Tier Level. If the Index Return does not exceed the Tier Level, the 2nd Tier Participation Rate will not apply to any portion of the Index Return. The 1st Tier Participation Rate, 2nd Tier Participation Rate, and Tier Level exist for the full term of the Index Strategy. Participation Rates and Tier Levels, upon renewal, may be higher or lower than the initial Participation Rates or Tier Level but will never be less than the Guaranteed Minimum Participation Rate or Guaranteed Maximum Tier Level, respectively. Renewal Participation Rates and Tier Levels may differ from the Participation Rates and Tier Levels used for new Annuity contracts or for other Annuity contracts issued at different times. No Index Strategy guarantees a positive Index Credit.

For Tiered Participation Rate Index Strategies, the Guaranteed Minimum Participation Rate equals 100% and the Guaranteed Maximum Tier Level equals 35%. Participation Rates for new Index Strategy Terms are declared at our discretion, subject to applicable guarantees. You bear the risk that we will not declare a Participation Rate above the guaranteed minimum, or a Tier Level below the guaranteed maximum.

Risks Associated with the Indices: Because the S&P 500® Index, MSCI EAFE Index, Invesco QQQ ETF, iShares Russell 2000 ETF, AB 500 Plus Index and Dimensional International Equity Focus Index are each comprised of a collection of equity securities, in each case the value of the component securities is subject to market risk, or the risk that market fluctuations may cause the value of the component securities to go up or down, sometimes rapidly and unpredictably. Market fluctuations can result from disasters and other events, such as storms, earthquakes, fires, outbreaks of infectious diseases (such as COVID -19), utility failures, terrorist acts, political and social developments, and military and governmental actions. In addition, the

value of equity securities may increase or decline for reasons directly related to the issuers of the securities. Equity markets are subject to the risk that the value of the securities may fall due to general market and economic conditions. Market volatility may exist with these Indices, which means that the value of the Indices can change dramatically over a short period of time in either direction. When you allocate to an Index Strategy that is linked to the performance of one of the Indices, you are not investing in the Index or in the securities composing the Index.

Each Index is subject to additional risks, including the following:

|

●

|

The S&P 500® Index is subject to risks associated with large-capitalization U.S. companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges and may not be able to attain the high growth rate of successful smaller companies.

|

|

●

|

The MSCI EAFE Index is subject to risks associated with foreign securities, including emerging markets. International investing involves special risks not found in domestic investing, including political and social differences and currency fluctuations due to economic decisions. Foreign markets can be more volatile than U.S. markets, and emerging markets can be riskier than investing in well-established foreign markets. The risks associated with investing on a worldwide basis include differences in the regulation of financial data and reporting, currency exchange differences, as well as economic and political systems differences. The Index is also subject to risks associated with large-capitalization companies (as described above) and mid-capitalization companies. Generally, the securities of mid-capitalization companies can be more volatile and riskier than the securities of large-capitalization companies.

|

|

●

|

The Invesco QQQ ETF is subject to risks associated with large-capitalization companies and foreign securities (each as described above). In addition, to the extent that the Index is comprised of securities issued by companies in a particular sector, those securities may not perform as well as the securities of companies in other sectors or the market as a whole.

|

|

●

|

The AB 500 Index is subject to risks associated with large-capitalization U.S. companies and foreign securities, including emerging markets (each as described above).

|

|

●

|

The Dimensional International Equity Focus Index is subject to risks associated with foreign securities, including emerging markets (as described above).

|

|

●

|

The iShares Russell 2000 ETF is subject to risks associated with small-capitalization companies. Generally, the securities of small-capitalization companies are more volatile and riskier than the securities of large-capitalization companies.

|

When you allocate to an Index Strategy that is linked to the performance of an ETF you are not investing in the ETF. Index-based ETFs seek to track the investment results of a specific market index. Due to a variety of factors, including the fees and expenses associated with an ETF, an ETF’s performance may not fully replicate or may, in certain circumstances, diverge significantly from the performance of the underlying index. This potential divergence between the ETF and the specific market index is known as tracking error. Although we believe that we will be viewed as the owner of the Index Strategy for tax purposes, there is no legal guidance to indicate how the IRS might view access to an ETF linked Index Strategy coupled with frequent transfers among investment options.

Index performance is on a “price return” basis, not a “total return” basis, and therefore does not reflect dividends paid on the securities composing the Index. Also, if the Index is an ETF, the ETF deducts fees and costs that reduce Index performance. These factors will reduce the Index Return and may cause the Index to underperform a direct investment in the securities composing the Index.

When you allocate to an Index Strategy that is linked to the performance of one of the Indices, you will not have voting rights or rights to receive dividends or other distributions that direct holders of the securities comprising the Indices have.

Early Withdrawal Risk: The Annuity is not a short-term investment vehicle and is not an appropriate investment for an investor who needs ready access to cash. The Annuity is designed to provide benefits on a long-term basis Because of the long-term nature of the Annuity, you should consider whether the Annuity is consistent with your financial situation and objectives. In extreme circumstances, the maximum potential loss resulting from a negative Interim Value adjustment is 100% of the amount invested in an Index Strategy.

Withdrawals under the Annuity, including partial withdrawals and a full surrender, may be subject to significant risk. Withdrawals during the first six Annuity Years may result in surrender charges. Surrender charges do not apply to withdrawals of the Free Withdrawal Amount or RMD withdrawals. However, even when surrender charges do not apply, withdrawals may be subject to negative Interim Value adjustments and negative tax consequences.

An Interim Value adjustment will apply to any withdrawal that occurs during an Index Strategy Term other than on the Index Strategy Start Date or Index Strategy End Date. Similarly, an Interim Value adjustment will apply to a death benefit payment, transfer, or Annuitization during an Index Strategy Term other than on the Index Strategy Start Date or Index Strategy End Date. A negative Interim Value adjustment will result in loss, which could be significant. See “Interim Value Risk” below. In extreme circumstances, you could lose up to 100% of your investment in an Index Strategy due to a negative Interim Value adjustment.

If a portion of Account Value allocated to an Index Strategy is withdrawn or otherwise removed prior to the Index Strategy End Date, there will be an immediate reduction to your Index Strategy Base. The reduction will be in a proportion equal to the reduction in your Interim Value. The proportional reduction could be larger than the dollar amount withdrawn or otherwise removed from the Index Strategy. Reductions to your Index Strategy Base will negatively impact your Interim Values for the remainder of the Index Strategy Term and will result in a lower positive Index Credit (if any) on the Index Strategy End Date.

Withdrawals may significantly reduce the Death Benefit, perhaps by more than the amount withdrawn. If you set up scheduled withdrawals, your exposure to these risks will repeat as long as the scheduled withdrawals continue.

Cyber Security and Business Continuity Risk: With the increasing use of technology and computer systems in general and, in particular, the Internet to conduct necessary business functions, the Company is susceptible to operational, information security and related risks. These risks, which are often collectively referred to as “cyber security” risks, may include deliberate or malicious attacks, as well as unintentional events and occurrences. These risks are heightened by our offering of increasingly complex products, such as those that feature automatic asset transfer or reallocation strategies, and by our employment

of complex investment, trading and hedging programs. Cyber security is generally defined as the technology, operations and related protocol surrounding and protecting a user’s computer hardware, network, systems and applications and the data transmitted and stored therewith. These measures ensure the reliability of a user’s systems, as well as the security, availability, integrity, and confidentiality of data assets.

of complex investment, trading and hedging programs. Cyber security is generally defined as the technology, operations and related protocol surrounding and protecting a user’s computer hardware, network, systems and applications and the data transmitted and stored therewith. These measures ensure the reliability of a user’s systems, as well as the security, availability, integrity, and confidentiality of data assets.

Deliberate cyber attacks can include, but are not limited to, gaining unauthorized access (including physical break-ins) to computer systems in order to misappropriate and/or disclose sensitive or confidential information; deleting, corrupting or modifying data; and causing operational disruptions. Cyber attacks may also be carried out in a manner that does not require gaining unauthorized access, such as causing

denial-of-service attacks on websites (in order to prevent access to computer networks). In addition to deliberate breaches engineered by external actors, cyber security risks can also result from the conduct of malicious, exploited or careless insiders, whose actions may result in the destruction, release or disclosure of confidential or proprietary information stored on an organization’s systems.

denial-of-service attacks on websites (in order to prevent access to computer networks). In addition to deliberate breaches engineered by external actors, cyber security risks can also result from the conduct of malicious, exploited or careless insiders, whose actions may result in the destruction, release or disclosure of confidential or proprietary information stored on an organization’s systems.

The Company is also subject to risks related to disasters and other events, such as storms, earthquakes, fires, outbreaks of infectious diseases (such as COVID-19), utility failures, terrorist acts, political and social developments, and military and governmental actions. These risks are often collectively referred to as “business continuity” risks. These events could adversely affect the Company and our ability to conduct business and process transactions. Although the Company has business continuity plans, it is possible that the plans may not operate as intended or required and that the Company may not be able to provide required services, process transactions, deliver documents or calculate values. It is also possible that service levels may decline as a result of such events.

Cyber security events, disasters and similar events, whether deliberate or unintentional, that could impact the Company and Contract owners could arise not only in connection with our own administration of the Annuity, but also with entities operating the Annuity’s Portfolios and with third-party service providers. Cyber security and other events affecting any of the entities involved with the offering and administration of the Annuity may cause significant disruptions in the business operations related to the Annuity. Potential impacts may include, but are not limited to, potential financial losses under the Annuity, your inability to conduct transactions under the Annuity and/or with respect to a Portfolio, an inability to calculate unit values with respect to the Annuity and/or the net asset value (“NAV”) with respect to a Portfolio, and disclosures of your personal or confidential account information.

In addition to direct impacts to you, cyber security and other events described above may result in adverse impacts to the Company, including regulatory inquiries, regulatory proceedings, regulatory and/or legal and litigation costs, and reputational damage. Costs incurred by the Company may include reimbursement and other expenses, including the costs of litigation and litigation settlements and additional compliance costs. Considerable expenses also may be incurred by the Company in enhancing and upgrading computer systems and systems security following a cyber security failure or responding to a disaster or similar event. The rapid proliferation of technologies, as well as the increased sophistication and activities of organized crime, hackers, terrorists, and others continue to pose new and significant cyber security threats. In addition, the global spread of COVID-19 has caused the Company and its service providers to implement business continuity plans, including

widespread use of work-from-home arrangements. Although the Company, our service providers, and the Portfolios offered under the Annuity may have established business continuity plans and risk management systems to mitigate risks, there can be no guarantee or assurance that such plans or systems will be effective, or that all risks that exist, or may develop in the future, have been completely anticipated and identified or can be protected against. Furthermore, the Company cannot control or assure the efficacy of the cyber security and business continuity plans and systems implemented by third-party service providers, the Portfolios, and the issuers in which the Portfolios invest.

widespread use of work-from-home arrangements. Although the Company, our service providers, and the Portfolios offered under the Annuity may have established business continuity plans and risk management systems to mitigate risks, there can be no guarantee or assurance that such plans or systems will be effective, or that all risks that exist, or may develop in the future, have been completely anticipated and identified or can be protected against. Furthermore, the Company cannot control or assure the efficacy of the cyber security and business continuity plans and systems implemented by third-party service providers, the Portfolios, and the issuers in which the Portfolios invest.

The military invasion of Ukraine initiated by Russia in February 2022 and the resulting response by the United States and other countries have led to economic disruptions, as well as increased volatility and uncertainty in the financial markets. It is not possible to predict the ultimate duration and scope of the conflict, or the future impact on U.S. and global economies and financial markets. The performance of the Index(es) may be adversely affected.

Artificial Intelligence Risk: In addition to the cyber security risks described above, the development, adoption and use of AI, including generative artificial intelligence (“Generative AI”), by us and by third parties on whom we rely may increase existing operational risks or create new operational risks that we are not currently anticipating. AI technologies offer potential benefits in areas such as customer service personalization and process automation, and we expect to use AI and Generative AI to help deliver products and services and support critical functions. We also expect third parties on whom we rely to do the same. There are significant risks involved in developing and deploying AI, and there can be no assurance that its use will enhance our products or services or be beneficial to our business, including our efficiency or profitability. The risk that AI and Generative AI may be misused is increased by the relative newness of the technology, the speed at which it is being adopted, and the lack of laws, regulations or standards governing its use. Such misuse could expose the Company to legal or regulatory risk, damage customer relationships or cause reputational harm. Further, our ability to continue to develop and efficiently deploy AI technologies depends on access to specific third-party equipment and other physical infrastructure, such as processing hardware and network capacity, the availability and pricing of which is difficult to control, especially in a highly competitive environment. Our competitors may also adopt AI or Generative AI more quickly or more effectively than we do, which could cause competitive harm. Because the Generative AI technology is so new, some of the potential risks of Generative AI are currently unknowable.

Interim Value Risk: To determine the Interim Value, we apply a formula which does not reflect the actual performance of the applicable Index, but rather a determination of the value of hypothetical underlying investments at the time of the Interim Value calculation. This amount could be more or less than if you had held the Index Strategy for the full Index Strategy Term. It also means that you could have a negative performance, even if the value of the Index

has increased at the time of the calculation. All withdrawals from an Index Strategy, including death benefit payments, transfers, annuitization, and surrenders paid before the Index Strategy End Date will be based on the Interim Value. Withdrawals and partial transfers before an Index Strategy End Date could have adverse impacts even if the value of the Index has increased at the time of the calculation because an early withdrawal will not allow you to participate in the Index Return for the Index Strategy Term with your entire Index Strategy Base. If you withdraw or transfer a portion out of an Index Strategy, the withdrawal or transfer will cause an immediate reduction to your Index Strategy Base in a proportion equal to the reduction in your Interim Value. A proportional reduction may be larger than the dollar amount of your withdrawal or transfer even if the value of the Index has increased. See “Withdrawal Risk” above for additional information.

Risks Associated with a Performance Lock: If a Performance Lock is executed:

|

●

|

You will no longer participate in Index Strategy performance, positive or negative, for the remainder of the existing Index Strategy Term for the “locked” Index Strategy.

|

|

●

|

You will not receive Index Credit on any “locked” Index Strategy on the Index Strategy End Date. As a result, you may receive less than the full Index Credit, or less than the full protection of the Buffer, than you would have received if you waited for us to apply the Index Credit on the Index Strategy End Date.

|

|

●

|

We use the Performance Lock Value calculated at the end of the current Valuation Day on the Performance Lock Date to execute your Performance Lock. This means you will not be able to determine in advance your Performance Lock Value, and it may be higher or lower than it was at the point in time you requested a manual Performance Lock, or that your Index Strategy reached its target for an automatic Performance Lock.

|

|

●

|

If a Performance Lock is executed when your Performance Lock Value has declined, you will lock in any loss. It is possible that you would have realized less of a loss or no loss if the Performance Lock occurred at a later time, or if the Index Strategy was not “locked.”

|

|

●

|

We will not provide advice or notify you regarding whether you should exercise a Performance Lock or the optimal time for doing so. We will not warn you if you exercise a Performance Lock at a sub-optimal time. We are not responsible for any losses related to your decision whether or not to exercise a Performance Lock.

|

Transfer Risk: The Annuity imposes significant limitations on the transfer of Account Value among investment options. Account Value may be transferred to an Index Strategy, or among Index Strategies, only on an Index Strategy End Date. Account Value in the Variable Option may be transferred to an Index Strategy only on an Index Anniversary Date. These limitations restrict your ability to reallocate Account Value in reaction to changes in market conditions.

Account Value in the Variable Option may be transferred to an Index Strategy only on an Index Anniversary Date. You may have to wait up to one year before you have an opportunity to transfer Account Value from the Variable Option to the Index Strategies. If you fail to request a transfer from the Variable Options on an Index Anniversary Date, the next transfer opportunity will be in one year on the next Index Anniversary Date.

During the Savings Stage, the Annuity permits transfers of Account Value from an Index Strategy to the Variable Options prior to the Index Strategy End Date. Any such transfer will be based on the Interim Value of the Index Strategy (an “Interim Value Transfer”) and will therefore be subject to an Interim Value adjustment. If you perform an Interim Value Transfer, and the Interim Value adjustment is negative, you will experience a loss, which could be significant. The Index Strategy’s Buffer, Cap Rate, Spread, Participation Rate(s), or Step Rate, as applicable, will not apply. There will be no Index Credit applied to amounts removed from an Index Strategy prior to the Index Strategy End Date. At the time you request an Interim Value Transfer, you will not know the applicable Interim Value because Interim Value is calculated at the end of a Valuation Day. The Interim Value applicable to the Interim Value Transfer could be lower than you anticipated. During the Income Stage, Interim Value Transfers are not permitted. Account Value in an Index Strategy may be transferred to the Variable Options only on an Index Strategy End Date.

Availability of Index Strategies will vary over time

Before allocating to an Index Strategy, you should determine the Index Strategies, Buffers, Cap Rates, Spreads, Participation Rates and Step Rates available to you. We reserve the right to change the Indices, Buffers, and limits on Index Gains at any time for new Strategy Terms, subject to applicable guarantees. We reserve the right to add or remove Index Strategies. There is no guarantee that an Index Strategy will be available in the future. You should make sure the Index Strategies you select are appropriate for your investment goals. During the Income Stage, we will limit the Index Strategy allocation options available.

Reallocation of Index Strategies

At the end of an Index Strategy Term for an Index Strategy, the amount allocated to that Index Strategy will be reallocated based upon your instructions we received in Good Order, or if none has been received in Good Order, automatically renew into the same Index Strategy unless the Index Strategy End Date would be after the Maximum Annuity Date. During the Saving Stage, if the same Index Strategy is no longer available, the amount will be transferred into the Holding Account, and the amount may be transferred into another Index Strategy on the next Index Anniversary Date. During the Income Stage, if the current Index Strategy is no longer available and we have no additional instructions, we will automatically transfer these amounts into the Index Strategy with, in order of priority, the shortest Strategy Term, the highest Buffer, and the lowest Cap Rate. You must provide instructions for reallocation by the Index Anniversary Date.

Substitution of an Index

We have the right to substitute a comparable index prior to the Index Strategy End Date if any Index is discontinued or if the calculation of an Index is substantially changed (such as a material change in the formula or method of calculating the Index). We would attempt to choose a substitute index that has a similar investment objective and risk profile to the replaced index and would notify you of any such substitutions. Upon substitution of an Index, we will calculate your Index Return on the replaced Index up until the date of substitution and the substitute Index from the date of substitution to the Index Strategy End Date. An Index substitution will not change your Index Strategy. The performance of the new Index may not be as good as the one that it substituted and as a result your Index Return may have been better if there had been no substitution. When we notify you of any substitution of an Index, we will also inform you of the potential impacts to your Index Credit. *Enhanced Cap Rate Index Strategies are only available on annuities with an Application Sign Date on or after July 1, 2024.

Risks of Investing in Variable Options: You take all the investment risk for amounts allocated to the Variable Options, which invest in the Portfolios. If the Variable Options increase in value, then your Account Value goes up; if it decreases in value, your Account Value goes down. How much your Account Value goes up or down depends on the performance of the Portfolios. We do not guarantee the investment results of any Portfolio. An investment in the Annuity is subject to the risk of poor investment performance, and the value of your investment can vary depending on the performance of the Portfolios, which has its own unique risks. We reserve the right to remove or substitute the Portfolios and close the Variable Options to new investment. The Variable Options are not available during the Income Stage.

Insurance Company Risk: No company other than us has any legal responsibility to pay amounts that we owe under the Annuity. You should look to our financial strength for our claims-paying ability. Amounts allocated to the Index Strategies are held in a non-registered, non-insulated Index Strategies Separate Account. These assets are subject to the claims of our creditors and the benefits provided under the Index Strategies are subject to our claims paying ability. The Company is also subject to risks related to disasters and other events, such as storms, earthquakes, fires, outbreaks of infectious diseases (such as COVID-19), utility failures, terrorist acts, political and social developments, and military and governmental actions. These risks are often collectively referred to as “business continuity” risks. These events could adversely affect the Company and our ability to conduct business and process transactions. Although the Company has business continuity plans, it is possible that the plans may not operate as intended or required and that the Company may not be able to provide required services, process transactions, deliver documents or calculate values. It is also possible that service levels may decline

as a result of such events.

as a result of such events.

Possible Adverse Tax Consequences: The tax considerations associated with the Annuity vary and can be complicated. The tax considerations discussed in this prospectus are general in nature and describe only federal income tax law (not state, local, foreign or other federal tax laws). Before making a Purchase Payment or taking other action related to your Annuity, you should consult with a qualified tax advisor for complete information and advice. For example, distributions from your Annuity are generally subject to ordinary income taxation on the amount of any investment gain unless the distribution qualifies as a non-taxable exchange or transfer. In addition, if you take a distribution prior to the taxpayer’s age 59½, you may be subject to a 10% additional tax in addition to ordinary income taxes on any gain.

Index Strategies Separate Account

Assets supporting the Index Strategies are held in a non-insulated, non-registered, and non-unitized Index Strategies Separate Account established under Arizona law. These assets are subject to the claims of our creditors and the benefits provided under the Index Strategies are subject to our claims paying ability.

An Owner does not have any interest in or claim on the assets in the Index Strategies Separate Account. In addition, neither an Owner nor amounts allocated to the Index Strategies participate in the performance of the assets held in the Index Strategies Separate Account.

We are not obligated to invest according to specific guidelines or strategies except as may be required by Arizona and other state insurance laws. The Index Strategies Separate Account is not registered with the SEC under the Investment Company Act.

The General Account: Our general obligations and any guaranteed benefits under the Annuity are supported by our General Account and are subject to our claims paying ability. Assets supporting annuity payments are held in the General Account. Assets in the General Account are not segregated for the exclusive benefit of any particular contract or obligation. General Account assets are also available to our general creditors and for conducting routine business activities, such as the payment of salaries, rent and other ordinary business expenses. The General Account is subject to regulation and supervision by the Arizona Department of Insurance and to the insurance laws and regulations of all jurisdictions where we are authorized to do business.

INVESTMENT OPTIONS

Index-Linked Options

The Contract currently offers multiple Index Strategies. For each Index Strategy, we will credit positive or negative interest (i.e., Index Credit) at the end of the Index Strategy Term to amounts allocated to the Index Strategy based, in part, on the performance of the Index. An investment in an Index Strategy is not an investment in the Index or in any Index fund. You could lose a significant amount of money if the Index declines in value. You could also lose a significant amount of money due to an Interim Value adjustment, if amounts are removed from an Index Strategy prior to the end of the Index Strategy Term.

The Index Credit is the amount you receive on an Index Strategy End Date based on the Index Return and the type of Index Strategy. The Index Credit may be positive or negative, which means you can lose principal and prior earnings. We do not guarantee the Index Credits for the Index Strategies. There is a risk of loss of your investment because the Index Strategy will be credited the negative Index Return in excess of the level of protection you selected through the Buffers.

We currently offer the following Index Strategies: Point-to-Point with Cap, Enhanced Cap Rate, Tiered Participation Rate, Step Rate Plus and Dual Directional. These Index Strategies are explained below. Information regarding the features of each currently offered Index Strategy, including (i) its name, (ii) a brief statement describing the assets that the Index seeks to track, (iii) its Index Strategy Term, (iv) its crediting methodology, (v) its current limit on Index loss, and (vi) its minimum limit on Index gain, is available in “Appendix A".

We can add or remove Index Strategies and change the features of an Index Strategy from one Strategy Term to the next, including the Index and the current limits on Index gains and losses (subject to any applicable guarantees). Not all Index Strategies will be available with all Indices, Buffers, and in all available Index Strategy Terms. As a result of economic market conditions, or utilization of the Index Strategies, we reserve the right to add and remove Index Strategies at any time, subject to regulatory requirements and approvals. Additions or removals would be effective with any newly issued contracts or upon reallocation for any existing contract holders. Removals would not impact existing contract holders currently allocated to an Index Strategy prior to the Index Strategy End Date. You will receive a Reallocation Notice 30 days prior to your Index Anniversary Date. You must provide instructions for reallocation (by any method allowable) by the Index Anniversary Date. The reallocation will be processed on the Index Anniversary Date. You will be able to make reallocation selections via mail, phone, or through online access. For currently available Options please see our website at www.prudential.com/flexguard-rates.

The minimum amount required to allocate to any Index Strategy, upon the Index Effective Date or at the time of renewal into a new Index Strategy is $2,000. In the event that the Account Value allocated to an Index Strategy falls below $2,000 and is not combined with reallocations from other Index Strategies on an Index Anniversary Date to meet the $2,000 minimum, these funds will automatically be renewed into the same Index Strategy. There is no maximum amount that can be allocated to an Index Strategy. If the same Index Strategy is no longer available, the funds associated with the closed Index Strategy will be transferred to the Holding Account, where they may be allocated among the Variable Options or into another Index Strategy on the next Index Anniversary Date.

Index Strategy Term

The Index Strategy Term is the time period allocated to each Index Strategy. The term begins on the Index Strategy Start Date and ends on the Index Strategy End Date. Index Strategy Terms of 1, 3, and 6 years are available and may vary based on the Index Strategy and whether you are in the Savings Stage or the Income Stage of the Benefit. The Index Strategy Start Date begins on the day you allocate funds to any Index Strategy, known as the Index Effective Date. The annual anniversary of this date is the Index Anniversary Date and will not change for the life of your Contract. You may only allocate to an Index Strategy on an Index Anniversary Date.

Before selecting an Index Strategy for investment, you should consider in consultation with your Financial Professional which Strategy Term lengths may be appropriate for you based on your liquidity needs, investment time horizon, and financial goals. Investing in Index Strategies with shorter Strategy Terms will provide more opportunities for Index Credits, transferring Account Value, and withdrawing or otherwise removing amounts without an Interim Value adjustment. However, assuming the same Index and Buffer, Index Strategies with shorter Strategy Terms generally tend to have less potential for Index gains. Conversely, investing in Index Strategies with longer Strategy Terms will provide fewer opportunities for Index Credits, transferring Account Value, and withdrawing or otherwise removing amounts without an Interim Value adjustment; however, assuming the same Index and Buffer, Index Strategies with longer Strategy Terms generally tend to have more potential for Index gains.

Amounts must remain in an Index Strategy until the end of its Index Strategy Term to be credited with Index Credit and to avoid a possible Interim Value adjustment, in addition to potential surrender charges and tax consequences. An Interim Value adjustment will apply upon any withdrawal, death benefit payment, transfer, Annuitization, Benefit charge or surrender that occurs during an Index Strategy Term other than on the Index Strategy Start Date or Index Strategy End Date. An Interim Value adjustment may be positive, negative or equal to zero. A negative Interim Value adjustment will result in loss. See the “Charges and Adjustments” section of this prospectus for additional information.

Index Return

We calculate the Index Return for every Index Strategy on a point-to-point basis. The Index Return will be the percentage change in the Index Value from the Index Strategy Start Date to the Index Strategy End Date. The Index Return is then used to determine the Index Credit for an Index Strategy. The Index Return is calculated by taking the Index Value on the Index Strategy End Date, minus the Index Value on the Index Strategy Start Date, and then dividing the result by the Index Value on the Index Strategy Start Date.

Examples:

| (1) | Negative Index Return Index Value at Index Strategy Start Date: 1569 Index Value on Index Strategy End Date: 1333 Index Return: -15% ((1333-1569)/1569) |

| (2) | Positive Index Return Index Value at Index Strategy Start Date: 1569 Index Value on Index Strategy End Date: 1726 Index Return: 10% ((1726-1569)/1569) |

Because we calculate the Index Return by comparing the value of the Index between two specific points in time, the Index Return may be negative or flat for the Index Strategy Term as a whole (including a multi-year Strategy Term) even if the Index performed positively for certain periods of time during the Index Strategy Term.

Each Index Strategy references an Index that determines the Index Return used to compute the Index Credit. When you allocate to an Index Strategy that is linked to the performance of one of the Indices, you are not investing in the Index. We currently offer Index Strategies based on the following securities indices:

|

S&P 500® Index, Price Return (SPX): The S&P 500® Index is comprised of 500 stocks considered representative of the overall market and is exclusive of dividends. An index is unmanaged and not available for direct investment.

|

|

MSCI EAFE Index, Price Return (MXEA): The MSCI EAFE Index measures the equity market performance of 22 developed market country indices located in Europe, Australasia and the Far East and is exclusive of dividends. An index is unmanaged and not available for direct investment.

|

|

Invesco QQQ ETF, Price Return (QQQ): The Invesco QQQ ETF is an exchange-traded fund that seeks to track the investment results of the NASDAQ-100 Index®. The Index includes the 100 largest non-financial companies listed on the Nasdaq® based on market cap.

|

|

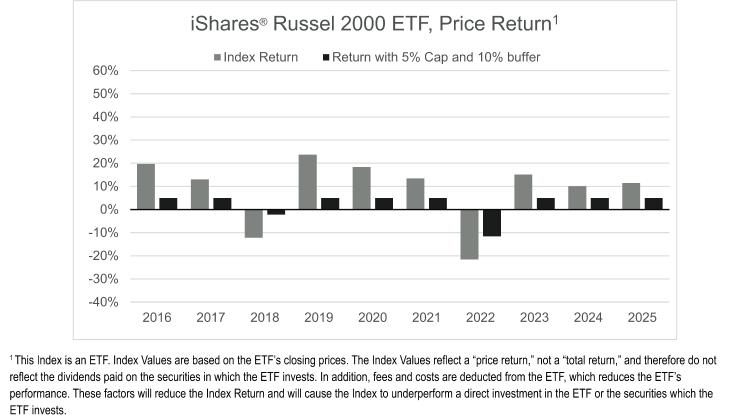

iShares® Russell 2000 ETF, Price Return (IWM): The iShares® Russell 2000 ETF seeks to track the investment results of the Russell® 2000 Index, an index composed of small-capitalization U.S. equities. The Russell® 2000 Index measures the performance of the small capitalization sector of the U.S. equity market, as defined by FTSE Russell.

|

|

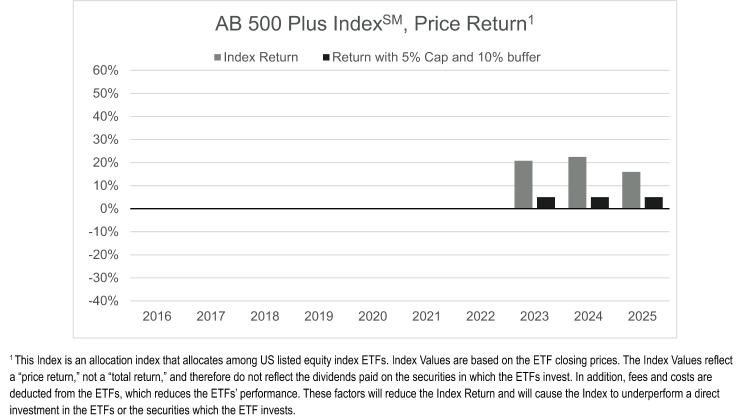

AB 500 Plus IndexSM, Price Return (ABUSPLS): The AB 500 Plus IndexSM is a rules based, allocation index that utilizes the SPDR® S&P 500® ETF Trust as its default allocation. The Index will tactically reallocate to additional US listed equity index ETFs: Invesco QQQ TrustSM, SERIES 1 ETF, iShares® Russell 2000 ETF, Shares® MSCI EAFE ETF, and iShares® MSCI Emerging Markets ETF when our proprietary positioning signals indicate that those other equity index ETFs have a higher expected return potential than the default allocation. At all times, the Index is fully allocated to equity index ETFs, with a significant allocation to equity index ETFs that track US listed companies. By following proprietary positioning signals, the Index aims to maintain significant exposure to the SPDR® S&P 500® ETF Trust, while providing differentiated returns through a tactical reallocation process.

|

|

The rules for calculating the AB 500 Plus IndexSM include an annual 0.75% reduction, which accrues daily, meaning that a small portion of that reduction is included in the published Index Value each day. The reduction is included to aid in setting the cap and participation rates and/or buffer levels of the Index Strategy with which the Index is used.

|

When you allocate to an Index Strategy that is linked to the performance of an ETF you are not investing in the ETF. Index-based ETFs seek to track the investment results of a specific market index. Due to a variety of factors, including the fees and expenses associated with an ETF, an ETF’s performance may not fully replicate or may, in certain circumstances, diverge significantly from the performance of the underlying index. This potential divergence between the ETF and the specific market index is known as tracking error. Although we believe that we will be viewed as the owner of the Index Strategy for tax purposes, there is no legal guidance to indicate how the IRS might view access to an ETF linked Index Strategy coupled with frequent transfers among investment options.