Entity | | Interest in Securities/Other Consideration to be Received | | Price Paid or to be Paid or Consideration Provided |

Sponsor | 2,800,000 MLAC Class B Ordinary Shares, of which 1,600,000 Sponsor Earnout Shares shall be held in escrow and shall vest and be released from escrow, in the amounts specified below, upon Pubco meeting the milestones specified below: | $25,000 paid to purchase the 7,187,500 MLAC Class B Ordinary Shares (of which 4,387,500 shares will be forfeited upon the Closing). | ||

(i)Upon the occurrence of Triggering Event I, 533,333 Sponsor Earnout Shares shall be released from the escrow account to the Sponsor; | ||||

(ii)Upon the occurrence of Triggering Event II, 533,333 Sponsor Earnout Shares shall be released from the escrow account to the Sponsor; and | ||||

(iii)Upon the occurrence of Triggering Event III, 533,334 Sponsor Earnout Shares shall be released from the escrow account to the Sponsor. | ||||

Sponsor | Additional MLAC Class A Ordinary Shares and/or cash | Amounts outstanding at the Closing under any MLAC Working Capital Loan will be repaid, at the lender’s option, in either cash or by the issuance of MLAC Class A Ordinary Shares at $10.00 per share. |

This summary highlights selected information from this proxy statement/prospectus and does not contain all the information that is important to you. You should carefully read this entire proxy statement/prospectus, including the Business Combination Agreement attached as Annex A to this proxy statement/prospectus as well as the other Annexes attached to the proxy statement/prospectus.

The Parties

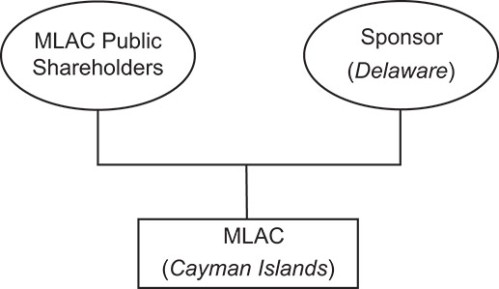

MLAC

MLAC is a blank check company incorporated in the Cayman Islands as an exempted company with limited liability on June 14, 2024. MLAC was incorporated for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses or entities. The MLAC Class A Ordinary Shares, MLAC Units and MLAC Share Rights are currently listed on The Nasdaq Global Market under the symbols “MLAC,” “MLACU” and “MLACR,” respectively.

MLAC completed the MLAC IPO of 23,000,000 MLAC Class A Ordinary Shares on December 16, 2024, generating gross proceeds to MLAC of $230,000,000. Simultaneously with the closing of the MLAC IPO, MLAC completed the sale to the Sponsor and BTIG of 805,000 MLAC Private Placement Shares at a purchase price of $10.00 per MLAC Private Placement Shares in the MLAC Private Placement, generating gross proceeds to MLAC of $8,050,000. Following the closing of the MLAC IPO, a total of $231,150,000, comprised of the net proceeds from the MLAC IPO and the MLAC Private Placement, was placed in the Trust Account. As of December 31, 2025, the Trust Account balance was approximately $241.2 million. Since the MLAC IPO, MLAC’s activity has been limited to efforts toward locating and completing a suitable business combination.

The mailing address of MLAC’s principal executive office is 930 Tahoe Blvd STE 802 PMB 45, Incline Village, NV 89451, and its telephone number is (775) 204-1489. Prior to the consummation of the Business Combination, MLAC will effect the Domestication, pursuant to which MLAC will transfer by way of continuation to and become a Delaware corporation, and at least two hours after the Domestication, MLAC Merger Sub will merge with and into MLAC, with MLAC continuing as the surviving company and a wholly- owned subsidiary of Pubco.

Pubco

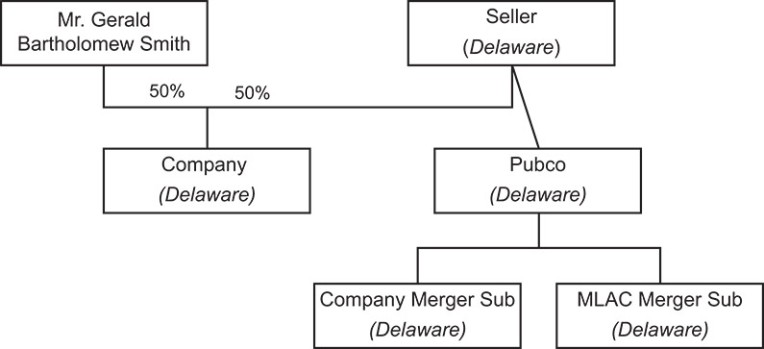

Pubco was incorporated as a corporation organized under the laws of Delaware on September 22, 2025, solely for the purpose of effectuating the Business Combination described herein. It currently owns no material assets and does not presently operate any business.

Following the Closing, it will be an operating company engaged in a number of businesses focused on AVAX. Following the Closing, Pubco will engage in the following principal activities: (i) the targeted accumulation of AVAX; (ii) tailored treasury management geared towards staking yield and other asset management levers intended to compound AVAX per share over time and (iii) the further ecosystem integration, including the potential provision of Avalanche-focused infrastructure, such as the operation of validator nodes, L1 activation and other corporate development activities, to expand exposure to Avalanche.

On September 25, 2025, Pubco issued one thousand (1,000) shares of common stock to Seller for nominal consideration. These shares represent all shares in the capital of Pubco that are currently issued and outstanding and, at the Company Merger Effective Time and by virtue of the Mergers, will be automatically canceled and extinguished without any conversion thereof or payment therefor. For descriptions of Pubco securities, see “Description of Pubco Securities.”

Prior to the consummation of the Business Combination, (i) the directors of Pubco are Mr. Robert Hadick and Mr. Gerald Bartholomew Smith; (ii) the officers are Mr. Gerald Bartholomew Smith (President) and Ms. Laine Mihalchick Moljo (Secretary) and (iii) the sole shareholder of Pubco is Seller.

The mailing address of Pubco’s registered office is 251, Little Falls Drive, Wilmington, County of New Castle, 19808, State of Delaware. Immediately prior to the consummation of the Business Combination, Pubco’s mailing address will be 413 W 14th Street, Floor 2, PMB 4633, New York, State of New York, 10014.

MLAC Merger Sub

MLAC Merger Sub was incorporated in Delaware on September 26, 2025 solely for the purpose of effectuating the Business Combination described herein. MLAC Merger Sub has no material assets and does not operate any business.

Prior to the consummation of the Business Combination, the sole director of MLAC Merger Sub is Gerald Bartholomew Smith and the sole shareholder of MLAC Merger Sub is Pubco. In connection with the consummation of the Business Combination, MLAC Merger Sub will merge with and into MLAC, with MLAC continuing as the surviving company and a wholly-owned subsidiary of Pubco, and the MLAC shareholders will receive one share of Pubco Class A Stock for each MLAC Class A Ordinary Share held by such shareholder. Each holder of MLAC Rights receiving one share of Pubco Class A Stock in exchange for every ten (10) MLAC Rights held by such holder.

The mailing address of MLAC Merger Sub’s registered office is 251, Little Falls Drive, Wilmington, County of New Castle, 19808, State of Delaware.

Company Merger Sub

Company Merger Sub was incorporated as a limited liability company organized under the laws of Delaware on September 26, 2025, solely for the purpose of effectuating the Business Combination described herein. Company Merger Sub has no material assets and does not operate any business.

Prior to the consummation of the Business Combination, the sole member of Company Merger Sub is Pubco. In connection with the consummation of the Business Combination, Company Merger Sub will merge with and into the Company, with the Company continuing as the surviving company and a wholly owned subsidiary of Pubco.

The mailing address of Company Merger Sub’s registered office is 251, Little Falls Drive, Wilmington, County of New Castle, 19808, State of Delaware.

Company

The Company is a newly formed company that will be focused exclusively on AVAX-related business lines. The Company was formed as a Delaware limited liability company on August 20, 2025, solely for the purpose of effectuating the Business Combination described herein.

On October 1, 2025, (i) the Company Unit Investors, in accordance with the provisions of the Company Unit Subscription Agreements agreed to purchase, payable in cash, USDC or AVAX, and the Company agreed to issue and sell, approximately $216 million worth of Company Units; and (ii) the Funds, in accordance with the provisions of the Contribution Agreement, performed the Dragonfly Contribution and received as consideration a total number of 5,805,638 Company Units.

Prior to the consummation of the Business Combination, the members are Seller, Mr. Gerald Bartholomew Smith, and the Company Unit Investors.

In connection with the consummation of the Business Combination, Company Merger Sub will merge with and into the Company, with the Company continuing as the surviving company and a wholly owned subsidiary of Pubco.

The registered office of the Company is 251 Little Falls Drive, Wilmington, County of New Castle, Delaware 19808 and the telephone number is 800-927-9800.

For more information about the Company, see “Information Related to the Company.”

Seller

Seller was incorporated as a limited liability company organized under the laws of Delaware on July 18, 2018.

At the date hereof, the sole manager of Seller is Haseeb Ahmad Qureshi, and the sole member of Seller is Dragonfly Management Limited.

Transactions

The Business Combination Agreement

On October 1, 2025, MLAC, Pubco, the Pubco Subsidiaries, the Company and Seller entered into the Business Combination Agreement. On January 13, 2026, and on March 17, 2026, MLAC, Pubco, the Pubco Subsidiaries, the Company, Seller Related Parties and Astral entered amendments to the Business Combination Agreement, in each case effective as of October 1, 2025.

Astral is a Delaware limited partnership whose general partner is Astral Horizon GP, LLC. The limited partners of Astral are certain senior managers and employees of the Seller and the general partners of the DVs. Astral Horizon GP, LLC is managed by some of the same individuals who serve as the managers of the general partners of the DVs. Accordingly, Astral is a related party to the Seller Related Parties by virtue of common management and overlapping ownership among their respective principals. The 4,000,000 newly issued Pubco Class A Stock Astral is entitled to receive as additional consideration for the Company Merger (the “Additional Merger Consideration Shares”) are being issued to Astral in consideration for advisory and strategic services provided by Astral’s limited partners in connection with the structuring and execution of the Business Combination and the establishment of Pubco. Such services included, but were not limited to:

(i) | Executive Recruitment: Astral’s limited partners assisted in identifying, evaluating, and recruiting the Chief Executive Officer of Pubco; and |

(ii) | Tax and Corporate Structuring Advisory: Astral’s limited partners provided strategic advice regarding aspects of the tax and corporate structuring of the Business Combination and post-Closing operations of Pubco. |

Consequently, (i) on January 13, 2026, the Parties entered into the First Amendment to the Business Combination Agreement, pursuant to which, inter alia, the 4,000,000 Additional Merger Consideration Shares (i.e., the 2,000,000 Astral Post-Closing Shares and the 2,000,000 Astral Earnout Shares) will be issued, on the Company Merger Effective Date, to Astral (the Astral Earnout Shares being held in escrow for the Escrow Period only to be released in accordance with the Astral Escrow Agreement), and (ii) on March 17, 2026, the Parties entered into the Second Amendment to the Business Combination Agreement, pursuant to which the issuance by Pubco to Astral of the 2,000,000 Astral Post-Closing Shares will occur on the thirtieth (30th) calendar day following the Closing Date, rather than on the Company Merger Effective Date.

Pursuant to the Business Combination Agreement, and subject to the terms and conditions set forth therein, (a) prior to the Closing, MLAC will effect the Domestication, pursuant to which MLAC will transfer by way of continuation to and become a Delaware corporation, (b) at least two hours after the Domestication, the MLAC Merger will be completed, pursuant to which MLAC Merger Sub will merge with and into MLAC, with MLAC continuing as the surviving company and a wholly owned subsidiary of Pubco and with MLAC Shareholders receiving one (1) share of Pubco Class A Stock for each MLAC Class A Ordinary Share held by such MLAC Shareholder, and with each holder of MLAC Rights receiving one (1) share of Pubco Class A Stock in exchange for every ten (10) MLAC Rights held by such holder, and (c) the Company Merger will be completed, pursuant to which Company Merger Sub will merge with and into the Company, with the Company continuing as the surviving company, and with (i) each Company Member other than Seller Related Parties receiving one (1) share of Pubco Class A Stock for each Company Unit held immediately prior to the effective time of the Company Merger, (ii) Seller Related Parties receiving one (1) share of Pubco Class A Stock and one (1) share of Pubco Class B Stock for each Company Unit held and (iii) Astral receiving the Additional Merger Consideration Shares, as follows: (i) 2,000,000 shares of Pubco Class A Stock (the “Astral Escrow Shares”) will be issued at the Company Merger Effective Time and deposited into an escrow account with the Trustee (or another escrow agent reasonably acceptable to Seller and Pubco) (the “Astral Escrow Account”), and (ii) 2,000,000 shares of Pubco Class A Stock (the “Astral Post-Closing Shares”) will be issued and deposited into Astral’s security account on the thirtieth (30th) calendar day following the Closing Date, rather than on the Company Merger Effective Date.

The Astral Escrow Shares will be released in tranches, all as provided in the Business Combination Agreement and the escrow agreement that will be entered into by and between Seller, Pubco and the escrow agent in a form to be mutually agreed upon by the parties prior to the Closing (the “Astral Escrow Agreement”). In particular, the Astral Escrow Shares will (i) vest and be released to

Astral upon the achievement of one or more Triggering Events (as defined under the Business Combination Agreement) or the occurrence of a Change in Control, and/or (ii) be transferred to Pubco in the event that, within the earn out period ending on the fifth (5th) anniversary of the Closing Date, all of the Triggering Events have not been achieved by Pubco and a Change in Control has not occured.

In particular, pursuant to the Business Combination Agreement the Astral Earnout Shares will vest and be released from the Astral Escrow Account to Astral, in the amounts specified below, upon Pubco meeting the following price milestones: (i) on the last day of any twenty (20) consecutive trading day period after the Closing Date in which the VWAP of the Pubco Class A Stock is greater than or equal to $13.00 per share (“Triggering Event I”), 666,667 shares of Pubco Class A Stock; (ii) on the last day of any twenty (20) consecutive trading day period after the Closing Date in which the VWAP of the Pubco Class A Stock is greater than or equal to $15.00 per share (“Triggering Event II”), 666,667 shares of Pubco Class A Stock; and (iii) on the last day of any twenty (20) consecutive trading day period after the Closing Date in which the VWAP of the Pubco Class A Stock is greater than or equal to $17.00 per share (“Triggering Event III,” and together with Triggering Event I and Triggering Event II, the “Triggering Events” and each a “Triggering Event”), 666,666 shares of Pubco Class A Stock.

For more information about the Business Combination Agreement, please see the section entitled “The Business Combination Proposal — The Business Combination Agreement.” A copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A.

Related Agreements

Contribution Agreement

Concurrently with the execution of the Business Combination Agreement, Seller, the Company, Pubco, the Foundation entered into the Contribution Agreement, pursuant to which, on the date of the Business Combination Agreement, (i) the Foundation agreed to perform the Foundation Transaction on the terms and subject to the conditions set forth in the Token Sale Agreement and (ii) Seller agreed to perform the Dragonfly Contribution by contributing, directly or indirectly through the Funds, 1,960,040 AVAX tokens to the Company in exchange for 5,805,638 Company Units.

In addition to the above, the Contribution Agreement also contains certain covenants of the parties, including inter alia:

(i)Outreach and Management. Seller has agreed to identify and engage potential acquisition targets, additional Advisory Board members, co-asset managers, and prospective management team members for the Company. In addition, the parties have identified Mr. Gerald Bartholomew Smith as the Chief Executive Officer of the Company.

(ii)Exclusivity and the Company’s Right of First Refusal. For a period of eighteen (18) months commencing on the date of the Business Combination Agreement, (a) the Foundation agreed not to directly or indirectly enter into any binding agreement to enter into a “Competing Transaction” (as defined in the Contribution Agreement); and (b) the Company will have a right of first refusal with respect to any proposed sale, that is not a Competing Transaction, by the Foundation of AVAX in one single transaction or a series of related transactions (other than any sales to a bona fide person or entity entering into an arrangement with a Foundation entity to acquire or utilize AVAX in connection with a strategic, business or operational purpose, not, to purchase AVAX primarily for investment, capital markets related or market making purposes) with an aggregate value exceeding $75 million at a price representing a discount greater than 30% (based on the then-current/weighted 30-day trailing market price of AVAX), subject to specified notice, timing, acceptance procedures, and specific exemptions. This right of first refusal will terminate automatically if the Company fails to list on a U.S. national securities exchange by April 30, 2026, with at least $300 million in AVAX assets and $100 million in cash or cash equivalents.

(iii)Board Representation. For a period of five (5) years following the Closing Date (period that may be extended upon the occurrence of certain conditions), the Foundation will be entitled to designate one (1) individual for appointment to the board of directors of Pubco.

(iv)Foundation Right of First Refusal. For a period of five (5) years commencing on the date of the Business Combination Agreement, the Foundation will have a right of first refusal with respect to any proposed sale by the Company of Foundation

Tokens in one or more related transactions with an aggregate value exceeding $1 million, subject to specified notice, timing and acceptance procedures.

(v)Tokenization. The Company and Pubco have agreed that any issuance, sale or distribution of crypto assets relating to their respective shares, assets or any network, protocol or application developed by or on their behalf will be conducted exclusively on the Avalanche Network.

The Contribution Agreement may be terminated prior to the Closing as follows: (a) by the mutual written consent of Seller, the Company, Pubco, the Foundation; or (b) by the Foundation, if the Transaction fails to close or Pubco fails to list on a U.S. national stock exchange by September 30, 2026, in each case with assets of at least $300 million in AVAX plus $100 million in cash or cash equivalents. If the Business Combination Agreement is terminated, the Contribution Agreement shall automatically terminate.

If the Contribution Agreement is terminated, it and the Token Sale Agreement will become void and of no further force and effect, and the Foundation AVAX sold by the Foundation to the Company under the Foundation Transaction and the AVAX contributed by the Funds to the Company under the Dragonfly Contribution will be returned to the Foundation and the Funds, respectively, in the same form in which they were sold or contributed, and any consideration received by the Foundation or the Funds will be returned to the Company.

For more information about the Contribution Agreement, please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Contribution Agreement.” A copy of the Contribution Agreement is attached to this proxy statement/prospectus as Annex E.

Token Sale Agreement

Concurrently with the execution of the Business Combination Agreement, the Company, Pubco, Avalanche BVI and Avalanche Cayman entered into the Token Sale Agreement, pursuant to which, on the date of the Business Combination Agreement, the Foundation agreed to perform the Foundation Transaction by selling $200 million of AVAX tokens on a pre-discount basis to the Company in exchange for, at a 60% discount, $50 million in cash or USDC and $30 million in the form of up to 3,000,000 Pubco Class A Stock.

For more information about the Token Sale Agreement, please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Token Sale Agreement.” A copy of the Token Sale Agreement is attached to this proxy statement/prospectus as Annex D.

Astral Escrow Agreement

In accordance with the provisions of the Business Combination Agreement, at Closing Astral, Pubco and the Seller shall enter into the Astral Escrow Agreement with Continental Transfer & Trust Company, as escrow agent. The Astral Escrow Agreement will set forth the terms and conditions of the Astral Escrow Account.

Pursuant to the Astral Escrow Agreement, Astral will deposit, at Closing, in the Astral Escrow Account 2,000,000 of the 4,000,000 Pubco Class A Stock issued to Astral as Astral Earnout Shares and will manage the Astral Escrow Account and release, in one or more tranches, the Astral Earnout Shares to Astral and/or Pubco in accordance with the provisions of the Business Combination Agreement.

For more information about the Astral Escrow Agreement, please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Astral Escrow Agreement.”

Sponsor Escrow Agreement

In accordance with the provisions of the Sponsor Support Agreement, at Closing the Sponsor, Pubco and the Seller shall enter into the Sponsor Escrow Agreement with Continental Stock Transfer & Trust Company, as escrow agent. The Sponsor Escrow Agreement will set forth the terms and conditions of the Sponsor Escrow Account.

Pursuant to the Sponsor Escrow Agreement, the Sponsor will deposit, at Closing, in the Sponsor Escrow Account 1,600,000 of the 2,800,000 Pubco Class A Stock issued to Sponsor as Sponsor Earnout Shares and will manage the Sponsor Escrow Account and release, in one or more tranches, the Sponsor Earnout Shares to the Sponsor and/or Pubco in accordance with the provisions of the Sponsor Support Agreement.

The Sponsor Escrow Shares will be released in tranches, all as provided in the Sponsor Support Agreement (as described below) and the Sponsor Escrow Agreement. In particular, the Sponsor Escrow Shares will (i) vest and be released to Sponsor upon the achievement of one or more Triggering Events (as defined below) or the occurrence of a Change in Control, and/or (ii) be transferred to Pubco in the event that, within the earn out period ending on the fifth (5th) anniversary of the Closing Date, all of the Triggering Events have not been achieved by Pubco and a Change in Control has not occured.

For more information about the Sponsor Escrow Agreement, please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Sponsor Escrow Agreement.”

Sponsor Support Agreement

Concurrently with the execution of the Business Combination Agreement, MLAC, Sponsor and Pubco entered into the Sponsor Support Agreement, pursuant to which, among other things, the Sponsor agreed (i) to vote its MLAC Ordinary Shares in favor of the Business Combination Agreement and the Transactions and each of the MLAC Shareholder Approval Matters, (ii) to vote its MLAC Ordinary Shares against (a) any Acquisition Proposal, (b) any merger, consolidation, combination, sale of substantial assets, reorganization, recapitalization, dissolution, liquidation or winding up of or by MLAC (other than the Transactions), (c) any change in the business of MLAC and (d) any proposal, action or agreement involving MLAC that would or would reasonably be expected to jeopardize the Transactions, (iii) to comply with the restrictions imposed by the Insider Letter, including the restrictions on transfer and redemption of MLAC Ordinary Shares in connection with the Transactions, (iv) subject to and conditioned upon the consummation of the MLAC Merger, to waive any anti-dilution rights that would otherwise result in the MLAC Class B Ordinary Shares held by Sponsor converting into MLAC Class A Ordinary Shares on a greater than one-for- one basis, (v) to deliver to MLAC for cancellation 495,000 MLAC Private Placement Shares and 4,387,500 MLAC Founder Shares immediately prior to the MLAC Merger Effective Time, (vi) to effect certain security cancellations and deposit 1,600,000 Pubco Class A Stock issued to it at Closing into escrow in connection with the Closing (the “Sponsor Escrow Shares”) and (vii) subject to and effective as of the Closing, to irrevocably and unconditionally release and waive any and all claims it may have against MLAC, Pubco and the Company or their respective Affiliates arising on or prior to the Closing, subject to customary carve-outs.

Pursuant to the Sponsor Support Agreement the Sponsor Earnout Shares will vest and be released from the Sponsor Escrow Account to the Sponsor in the amounts specified as follows: (i) upon the occurrence of Triggering Event I, 533,333 shares of Pubco Class A Stock; (ii) upon the occurrence of Triggering Event II, 533,333 shares of Pubco Class A Stock; and (iii) upon the occurrence of Triggering Event III, 533,334 shares of Pubco Class A Stock.

Further, pursuant to the Sponsor Support Agreement, the parties agreed that prior to the Closing they would enter into an amendment to the Insider Letter, to amend certain terms relating to transfer restrictions applicable to the shares held by the Sponsor.

For more information about the Sponsor Support Agreement, please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Sponsor Support Agreement.”

Company Unit Subscription Agreements

Concurrently with the execution of the Business Combination Agreement, Pubco, the Company and MLAC entered into the Company Unit Subscription Agreements with the Company Unit Investors, pursuant to which the Company Unit Investors agreed to purchase, payable in cash, USDC or AVAX (or a combination of cash, USDC and/or AVAX), and the Company agreed to issue and sell, approximately $216 million worth of Company Units at the Per Unit Price, upon the terms and subject to the conditions set forth therein. Company Unit Investors received a number of Company Units equal to (a) if the Company Unit Investor elected to purchase Company Units by contributing AVAX, the Stated AVAX Amount multiplied by the Applicable Signing AVAX Price, or (b) if the Company Unit Investor elected to purchase the Company Units by contributing cash or USDC, the Stated Dollar Amount or the Stated USDC Amount (as applicable) divided by the Per Unit Price. For more information about the Company Unit Subscription Agreements,

please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — The Company Unit Subscription Agreements.”

Lock-Up Agreement

Concurrently with the Closing, (i) MLAC, Sponsor, and the MLAC Insiders will enter into with Pubco the Sponsor Lock-Up Agreement and (ii) the Funds, Astral as well as certain other holders of shares of Pubco Stock will also enter into with Pubco Seller Lock-Up Agreements in substantially the same form as the Sponsor Lock-Up Agreement, pursuant to which, in each case, such parties will agree that the shares of Pubco Class A Stock received by them in connection with the Business Combination, amounting to approximately 10,605,638 shares of Pubco Class A Stock, and any other securities convertible into or exercisable or exchangeable for Pubco Stock, will be subject to transfer restrictions, subject to certain customary exceptions.

Under the Lock-Up Agreements, the above-mentioned shares will be subject to transfer restrictions until the earlier of (i) the Anniversary Release (i.e., 180 days following the date of the Closing); provided, that if the VWAP of Pubco Class A Stock equals or exceeds $12.50 per share for any 20 consecutive trading days following the Closing, the Anniversary Release will be deemed to occur at 11:59 p.m. New York City time on such 20th consecutive trading day, and (ii) the date on which Pubco consummates a liquidation, merger, capital stock exchange, reorganization or other similar transaction that results in all Pubco shareholders having the right to exchange their shares of Pubco Stock for cash, securities or other property.

For more information about the Lock-Up Agreements please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Lock-Up Agreements.” Copy of the form Lock-Up Agreements is attached to the Business Combination Agreement under Exhibit D.

Amended and Restated Registration Rights Agreement

Concurrently with the Closing, Pubco, MLAC, the Sponsor, Seller, the Foundation and certain securityholders shall enter into an amended and restated registration rights agreement, which will add Pubco as a party (the “Amended and Restated Registration Rights Agreement”), and which provides for customary demand registration rights, piggyback registration rights and shelf registration rights for the benefit of the holders of Pubco Stock named therein, including the Sponsor, Seller and the Foundation subject to customary cutbacks and issuer suspension rights. The Amended and Restated Registration Rights Agreement also includes customary provisions relating to underwriting participation, registration expenses, indemnification and coordination of sales in underwritten offerings, and will become effective upon the Closing and will supersede MLAC’s existing registration rights agreement in its entirety. Pubco estimates that up to approximately 15,605,638 shares of Pubco Class A Stock will be subject to registration rights pursuant to the Amended and Restated Registration Rights Agreement immediately following the Closing, representing approximately 25% of the total issued and outstanding shares of Pubco Class A Stock following the Transactions, and assuming, among other things, that no Public Shareholders exercise redemption rights with respect to their Public Shares upon completion of the Business Combination, that no shares of Pubco Class A Stock are issued pursuant to the Incentive Plan and that no Adjustment Units are issued pursuant to the Company Unit Subscription Agreements.

Agreements with PJT and Barclays

Pursuant to the Private Placement Engagement Letter, AVAT engaged PJT and Barclays to provide certain capital markets advisory services and to act as exclusive placement agents for the Company Unit Subscription. Pursuant to the Private Placement Engagement Letter, for the services provided thereto, PJT and Barclays will receive a cash fee at the Closing which is equal to 5.5% of the aggregate gross cash proceeds from the sale of equity or equity-linked securities of AVAT to institutional accounts, with such placement fee split equally between PJT and Barclays. Additionally, if the Company sells any equity or equity-linked securities of AVAT (or securities of the same or a similar class) within twelve (12) months following any termination of the Private Placement Engagement Letter, then the Company will pay to PJT and Barclays a fee at the closing that is equal to the fee which would have been payable to PJT and Barclays if the closing occurred during the term of the appointment. PJT and Barclays are entitled to be indemnified by AVAT pursuant to certain customary indemnity provisions under the Private Placement Engagement Letter.

Pursuant to the Financial Advisor Engagement Letter, AVAT engaged PJT to act as its exclusive financial advisor in connection with the Business Combination, and PJT agreed to perform customary financial advisory services. For its services under the Financial Advisor Engagement Letter, PJT will receive a customary advisory fee payable in cash promptly at, and conditional upon, the Closing.

PJT is entitled to be indemnified by AVAT pursuant to certain customary indemnity provisions under the Financial Advisor Engagement Letter.

For more information about the Agreements with PJT and Barclays, please see the section entitled “The Business Combination Proposal — Other Transaction Agreements — Agreements with PJT and Barclays”

Merger Consideration

As consideration for the Company Merger:

(1) | each Company Member other than Seller Related Parties shall be entitled to receive from Pubco one (1) share of Pubco Class A Stock for each Company Unit held by such Company Member immediately prior to the Company Merger Effective Time; |

(2) | each Seller Related Party shall be entitled to receive from Pubco, for each Company Unit held by such Seller Related Party immediately prior to the Company Merger Effective Time: |

| • | one (1) share of Pubco Class A Stock; and |

| • | one (1) share of Pubco Class B Stock; |

(3) | Astral shall be entitled to receive 4,000,000 newly issued Pubco Class A Stock as Additional Merger Consideration Shares, out of which (i) 2,000,000 shares of Pubco Class A Stock will be deposited, upon the Closing, into the Astral Escrow Account, and will be released in tranches, all as provided in the Business Combination Agreement and the Astral Escrow Agreement, and (ii) 2,000,000 shares of Pubco Class A Stock will and delivered on the thirtieth (30th) calendar day following the Closing Date; and |

(4) | all of the issued and outstanding Company Merger Sub Membership Interests shall be converted into an equal number of shares of common stock of the Company Surviving Subsidiary (i.e., the Company). |

At the Company Merger Effective Time and by virtue of the Mergers, all of the shares of Pubco Stock issued and outstanding immediately prior to the MLAC Merger Effective Time shall be automatically canceled and extinguished without any conversion thereof or payment therefor.

For more information about the Astral Earnout Shares please see the section entitled “The Business Combination Proposal — Business Combination Agreement.”

By virtue of the MLAC Merger:

(1) | immediately prior to the MLAC Merger Effective Time, (i) each MLAC Unit issued and outstanding immediately prior to the MLAC Merger Effective Time, that has not been forfeited in accordance with the Sponsor Support Agreement, shall be automatically subject to the Unit Separation with the holder thereof being deemed to hold one (1) MLAC Class A Ordinary Share and one (1) MLAC Right; and (ii) the MLAC Class A Ordinary Shares (other than the shares in respect of which its holder has validly exercised its right of redemption) and MLAC Right underlying the MLAC Unit held or deemed to be held following the Unit Separation shall be converted in accordance with the applicable terms of limbs (2)(i) and (2)(ii) respectively; |

(2) | at the MLAC Merger Effective Time: |

(i) | each issued and outstanding MLAC Right shall be automatically converted into the number of shares of Pubco Class A Stock that would have been received by the holder thereof if the MLAC Right had been converted upon the consummation of a Business Combination in accordance with MLAC’s Organizational Documents, the MLAC IPO Prospectus and the MLAC Rights Agreement into MLAC Class A Ordinary Shares, but for such purposes treating it as if (a) such Business Combination had occurred immediately prior to the MLAC Merger Effective Time and (b) the MLAC |

Class A Ordinary Shares issued upon conversion of the MLAC Rights had then automatically been converted into shares of Pubco Class A Stock in accordance with the provisions of limb (2)(ii). At the MLAC Merger Effective Time, the MLAC Rights shall cease to be outstanding and shall automatically be canceled and retired and shall cease to exist;

(ii) | each issued and outstanding MLAC Class A Ordinary Share (other than (x) treasury shares and (y) shares in respect of which its holder has validly exercised its right of redemption) shall be converted automatically into one (1) share of Pubco Class A Stock, following which all such MLAC Class A Ordinary Shares (other than the treasury shares) shall cease to be outstanding and shall automatically be canceled and shall cease to exist; |

(iii) | each MLAC Class B Ordinary Share issued and outstanding immediately prior to the MLAC Merger Effective Time that has not been forfeited in accordance with the Sponsor Support Agreement (other than treasury shares) shall be converted automatically into one (1) share of Pubco Class A Stock, following which all such MLAC Class B Ordinary Shares shall cease to be outstanding and shall automatically be canceled and shall cease to exist. |

(iv) | Pursuant to the Sponsor Support Agreement 1,600,000 of the 2,800,000 shares of Pubco Class A Stock issued to the Sponsor in exchange for the 2,800,000 MLAC Class B Ordinary Share held by the Sponsor shall be deposited, upon the Closing, into an escrow account with Continental Stock Transfer and Trust Company, and will be released in tranches, all as provided in the Sponsor Support Agreement and the Sponsor Escrow Agreement. For more information about the Sponsor Earnout Shares please see the section entitled “The Business Combination Proposal — Other Transaction Agreement — Sponsor Support Agreement”; and |

(v) | each issued and outstanding MLAC Merger Sub Membership Interest shall be converted into an equal number of ordinary shares, par value $0.0001, of the MLAC Surviving Subsidiary,with the same rights, powers and privileges as the shares so converted and shall constitute the only outstanding share capital of the MLAC Surviving Subsidiary. |

At the MLAC Merger Effective Time, each issued and outstanding Public Share in respect of which the holder thereof has validly exercised redemption rights pursuant to and in accordance with the MLAC Memorandum and Articles will be canceled, and those MLAC Shareholders will only have the right to receive a pro rata share of the redemption amount.

If there are any MLAC Ordinary Shares that are owned by MLAC as treasury shares, such treasury shares will be automatically canceled without any conversion thereof or payment therefor.

For illustrative purposes, based on funds in the Trust Account of approximately $241.2 million as of December 31, 2025 and $244.0 million as of April 27, 2026, the estimated per share redemption prices would have been approximately $10.49 per share and $10.61 per share, respectively (including interest earned on the funds held in the Trust Account but less taxes payable). As of December 31, 2025 and April 24, 2026, approximately 36.5% and 0.1%, respectively, of the AVAX holdings of AVAT were unlocked and unstaked, available to be liquidated as needed to fund transaction or other operating expenses.

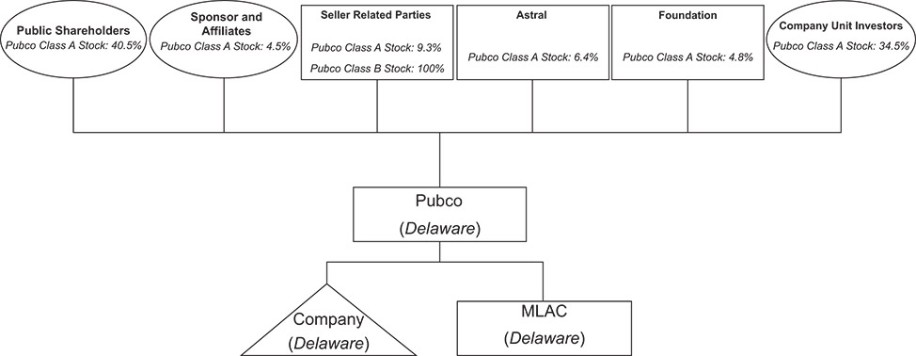

Ownership of Pubco After the Transactions

Upon the completion of the Business Combination, and assuming, among other things, that no Public Shareholders exercise redemption rights with respect to their Public Shares upon completion of the Business Combination, (i) Public Shareholders (including MLAC Right Holders) will own approximately 41.8% of the issued and outstanding shares of Pubco Class A Stock, (ii) the Company Unit Investors will own approximately 35.7% of the issued and outstanding shares of Pubco Class A Stock, (iii) the Sponsor and its Affiliates will own approximately 4.6% of the issued and outstanding shares of Pubco Class A Stock, out of which the Sponsor Earnout Shares will represent approximately 2.6% of the issued and outstanding shares of Pubco Class A Stock, (iv) Seller Related Parties will own approximately 9.6% of the issued and outstanding shares of Pubco Class A Stock and 100% of the issued and outstanding shares of Pubco Class B Stock, (v) Astral will own approximately 3.3% of the issued and outstanding shares of Pubco Class A Stock, out of which the Astral Post-Closing Shares will represent approximately 3.3% of the issued and outstanding shares of Pubco Class A Stock and (vi) the Foundation will own approximately 5.0% of the issued and outstanding shares of Pubco Class A Stock. Each holder of shares of Pubco Class A Stock will have no voting rights, except (i) as required by the DGCL or (ii) on any matter that adversely affects them relative to holders of any other class of stock of Pubco, until all shares of Pubco Class B Stock are canceled. Once all shares of Pubco Class B Stock are canceled, holders of Pubco Class A Stock will acquire full voting rights. Each holder of shares of Pubco Class B Stock will be entitled to one vote for each share of Pubco Class B Stock held of record by such

holder on all matters on which stockholders are generally entitled to vote. See “Risk Factors — Seller, whose interests may conflict with yours, can individually exercise significant influence over Pubco. You will have no voting rights of Pubco Class A Stock except as required by the DGCL and the concentrated ownership of Pubco Stock may prevent you and other shareholders from influencing significant decisions in the very limited circumstances in which the DGCL will give you the right to vote and may prevent or discourage unsolicited acquisition proposals or offers for Pubco Stock, and that may adversely affect the trading price of Pubco Class A Stock.”

If any of the Public Shareholders exercise their redemption rights, the percentage of the issued and outstanding shares of Pubco Class A Stock held by the Public Shareholders will decrease and the percentages of issued and outstanding shares of Pubco Class A Stock held by the Company Unit Investors, the Sponsor, Seller Related Parties, Astral, and the Foundation each increase relative to the percentage held if none of the Public Shares are redeemed unless the Class A Pubco Stock cease to be nonvoting securities, in which case, the Foundation’s percentage ownership will decrease relative to the percentage held if none of the Public Shares are redeemed and the Foundation will receive a number of pre-funded warrants convertible into Pubco Class A Stock in accordance with the Token Sale Agreement, the Contribution Agreement and the Foundation warrant agreement so that its beneficial ownership in Pubco does not exceed the Maximum Percentage.

The tables below illustrate varying beneficial ownership levels in Pubco immediately upon Closing, assuming No Redemptions by Public Shareholders, 25% Redemptions by Public Shareholders (5,727,000 MLAC Class A Ordinary Shares are redeemed by Public Shareholders), 50% Redemptions by Public Shareholders (11,452,023 MLAC Class A Ordinary Shares are redeemed by Public Shareholders), 75% Redemptions by Public Shareholders (17,178,034 MLAC Class A Ordinary Shares are redeemed by Public Shareholders) and Maximum Redemptions by Public Shareholders (22,904,656 MLAC Class A Ordinary Shares are redeemed by Public Shareholders). If any of these assumptions are not correct, these percentages will be different.

Potential ownership of issued and outstanding shares of Pubco Class A Stock upon Closing:

| No Redemptions | | 25% Redemptions | | 50% Redemptions | | 75% Redemptions | | Maximum Redemptions | |||||||||||

Pubco Stockholders | | Shares | | % | | Shares | | % | | Shares | | % | | Shares | | % | | Shares | | % |

Public Shareholders(1) |

| 25,300,000 |

| 41.8 |

| 19,573,629 |

| 35.7 |

| 13,847,258 |

| 28.3 |

| 8,120,887 |

| 18.8 |

| 2,394,516 |

| 6.4 |

Company Unit Investors(2) |

| 21,563,032 |

| 35.7 |

| 21,563,032 |

| 39.4 |

| 21,563,032 |

| 44.0 |

| 21,563,032 |

| 49.8 |

| 21,563,032 |

| 57.3 |

Sponsor and Affiliates(3) |

| 2,800,000 |

| 4.6 |

| 2,800,000 |

| 5.1 |

| 2,800,000 |

| 5.7 |

| 2,800,000 |

| 6.5 |

| 2,800,000 |

| 7.5 |

Seller Related Parties(2)(4) |

| 5,805,638 |

| 9.6 |

| 5,805,638 |

| 10.6 |

| 5,805,638 |

| 11.8 |

| 5,805,638 |

| 13.4 |

| 5,805,638 |

| 15.5 |

Astral(5) |

| 2,000,000 |

| 3.3 |

| 2,000,000 |

| 3.7 |

| 2,000,000 |

| 4.1 |

| 2,000,000 |

| 4.6 |

| 2,000,000 |

| 5.3 |

Foundation(6) |

| 3,000,000 |

| 5.0 |

| 3,000,000 |

| 5.5 |

| 3,000,000 |

| 6.1 |

| 3,000,000 |

| 6.9 |

| 3,000,000 |

| 8.0 |

Total | 60,468,670 | 100.0 | 54,742,299 | 100.0 | 49,015,928 | 100.0 | 43,289,557 | 100.0 | 37,563,186 | 100.0 | ||||||||||

(1) | Includes 2,300,000 MLAC Right Holder shares. |

(2) | Assumes each Company Unit will be redeemed for one share of Pubco Class A Stock and no issuance of Adjustment Units. |

(3) | Includes the 1,600,000 Sponsor Earnout Shares. |

(4) | Includes 2,547,252 Company Units issued to Dragonfly Ventures L.P. and 3,258,386 Company Units issued to Dragonfly Ventures II, L.P. |

(5) | Includes the 2,000,000 Astral Post-Closing Shares. Does not include the Astral Earnout Shares, which will be held in escrow for the Escrow Period and may only be released to Astral upon the achievement of certain Triggering Events in accordance with the Astral Escrow Agreement. |

(6) | Up to 3,000,000 of Pubco Class A stock will be issued to the Foundation to the Foundation pursuant to the Foundation Transaction. In the event the Pubco Class A Stock cease to be nonvoting securities, the Foundation will forfeit a number of its Pubco Class A Stock and will receive from Pubco a number of pre-funded warrants convertible into Pubco Class A Stock prior to the time the Pubco Class A Stock cease to be nonvoting securities so that the Foundation’s beneficial ownership in Pubco does not exceed the Maximum Percentage. |

All of the relative percentages above are for illustrative purposes only and are based upon certain assumptions as described in the section entitled “Beneficial Ownership of Securities” and as described above. Should one or more of the assumptions prove incorrect, actual ownership percentages may vary materially from those described in this proxy statement/prospectus as anticipated, believed, estimated, expected or intended. See “Unaudited Pro Forma Condensed Combined Financial Information.”

Dilution

Dilution per share to Public Shareholders is determined by MLAC’s NTBV per share, as adjusted, while excluding the Business Combination, while giving effect to material probable or consummated transactions and other material effects on NTBV per share, from the Public Shareholders as set forth as follows under five redemption scenarios.

The following table illustrates NTBV per share and the change in NTBV per share, as adjusted, following the Closing, but excluding the other effects of the Business Combination, while giving effect to probable or consummated transactions that are material and other material effects on NTBV per share. These are presented in relation to the offering price per Public Share in the MLAC IPO as set forth as follows under the five redemption scenarios:

Assuming | Assuming | Assuming | Assuming | Assuming | |||||||||||

No | 25% | 50% | 75% | Maximum | |||||||||||

| Redemptions | | Redemptions | | Redemptions | | Redemptions | | Redemptions | ||||||

Public Shares |

| 23,000,000 |

| 17,273,629 |

| 11,547,258 |

| 5,820,887 |

| 94,516 | |||||

MLAC Founder Shares |

| 7,187,500 |

| 7,187,500 |

| 7,187,500 |

| 7,187,500 |

| 7,187,500 | |||||

MLAC Private Placement Shares |

| 495,000 |

| 495,000 |

| 495,000 |

| 495,000 |

| 495,000 | |||||

MLAC Representative Private Placement Shares |

| 310,000 |

| 310,000 |

| 310,000 |

| 310,000 |

| 310,000 | |||||

Total MLAC Ordinary Shares outstanding as of December 31, 2025 |

| 30,992,500 |

| 25,266,129 |

| 19,539,758 |

| 13,813,387 |

| 8,087,016 | |||||

NTBV(1) as of December 31, 2025 |

| (734,770) |

| (734,770) |

| (734,770) |

| (734,770) |

| (734,770) | |||||

Adjusted for: |

| |

| |

| |

| |

| | |||||

MLAC shares underlying public rights |

| 2,300,000 |

| 2,300,000 |

| 2,300,000 |

| 2,300,000 |

| 2,300,000 | |||||

MLAC Private Placement Shares to be surrendered by the Sponsor |

| (495,000) |

| (495,000) |

| (495,000) |

| (495,000) |

| (495,000) | |||||

MLAC Private Placement Shares to be surrendered by BTIG |

| (310,000) |

| (310,000) |

| (310,000) |

| (310,000) |

| (310,000) | |||||

MLAC Class B Ordinary Shares to be surrendered by the Sponsor |

| (4,387,500) |

| (4,387,500) |

| (4,387,500) |

| (4,387,500) |

| (4,387,500) | |||||

Total MLAC Ordinary Shares outstanding as of December 31, 2025, as adjusted |

| 28,100,000 |

| 22,373,629 |

| 16,647,258 |

| 10,920,887 |

| 5,194,516 | |||||

NTBV as of December 31, 2025(1) |

| (734,770) |

| (734,770) |

| (734,770) |

| (734,770) |

| (734,770) | |||||

Adjusted for(2): |

| |

| |

| |

| |

| | |||||

Reclassification of MLAC Class A Ordinary Shares subject to redemption to equity |

| 243,344,159 |

| 182,758,118 |

| 121,172,078 |

| 61,586,037 |

| 1,000,000 | |||||

Transaction expenses to be paid by MLAC |

| (1,325,978) |

| (1,325,978) |

| (1,325,978) |

| (1,325,978) |

| (1,325,978) | |||||

NTBV as of December 31, 2025, as adjusted |

| 241,283,411 |

| 180,697,370 |

| 120,111,330 |

| 59,525,289 |

| (1,060,748) | |||||

NTBV per share as of December 31, 2025, as adjusted | $ | 8.59 | $ | 8.08 | $ | 7.22 | $ | 5.45 | $ | (0.20) | |||||

Dilution(3) | $ | 1.41 | $ | 1.92 | $ | 2.78 | $ | 4.55 | $ | 10.20 | |||||

(1) | NTBV is calculated as total assets minus total liabilities and MLAC Class A Ordinary Shares subject to redemption as of December 31, 2025. |

(2) | NTBV is adjusted for (i) payments from the Trust Account at different levels of redemptions to Public Shareholders at the $10.55 per share redemption price as of February 28, 2026; (ii) transaction costs that have not been recorded on MLAC’s financial statements as of December 31, 2025; and (iii) the portion of the deferred underwriter fee to be forfeited by BTIG, which will have an impact on the calculation of NTBV upon the Closing. |

(3) | Dilution is calculated by subtracting the NTBV per share as of December 31, 2025, as adjusted, from the $10.00 MLAC IPO per share price for the Public Shares. |

MLAC issued the Public Shares in the MLAC IPO at $10.00 per share. After giving effect to the issuance of the 23,000,000 Public Shares in the MLAC IPO and the 310,000 MLAC Private Placement Shares issued to BTIG in the MLAC Private Placement, which remain issued and outstanding, there were 23,310,000 MLAC Class A Ordinary Shares issued and outstanding.

In connection with the Business Combination, assuming its consummation in accordance with the Business Combination Agreement, immediately after the Closing, Pubco is expected to have outstanding 60,468,670 shares of Pubco Class A Stock, including (i) 3,000,000 Pubco Class A Stock to be issued to the Foundation pursuant to the Foundation Transaction, (ii) 5,805,638 Pubco Class A Stock to be issued to the Seller Related Parties pursuant to the Seller Related Parties receiving one share of Pubco Class A Stock for each Company Unit held, (iii) 2,000,000 Pubco Class A Stock to be issued to Astral as additional consideration for the Company Merger, (iv) 2,800,000 Pubco Class A Stock to be issued to the Sponsor and Affiliates in exchange for MLAC Founder Shares, (v) 25,300,000 Pubco Class A Stock to be issued pursuant to each Public Shareholder receiving one (1) share of Pubco Class A Stock for each MLAC Class A Ordinary Share held by such shareholder, including 2,300,000 shares underlying the MLAC Public Rights, and (vi) 21,563,032 shares of Pubco Class A Stock to be issued in connection with the Company Unit Investors receiving one share of Pubco Class A Stock for each Company Unit held immediately prior to the effective time of the Company Merger. These shares outstanding also assume, among other things, that no shares of Pubco Class A Stock are issued pursuant to the Incentive Plan and that no Adjustment Units are issued pursuant to the Company Unit Subscription Agreements. The tabular disclosure includes presentations of information at various illustrative redemption levels consistent with the “No Redemptions,” “25% Redemptions,” “50% Redemptions,” “75% Redemptions” and “Maximum Redemptions” scenarios further described in the section of this proxy statement/prospectus entitled “Unaudited Pro Forma Condensed Combined Financial Information.”

For purposes of Item 1604(c)(1) of Regulation S-K, Pubco would have 60,468,670 total shares of Pubco Class A Stock outstanding immediately after giving effect to the Business Combination under the “No Redemptions” scenario based on the assumptions set forth in the preceding paragraph and as further described above. Where there are no redemptions of Public Shares prior to the Closing, MLAC valuation is based on the $10.00 issuance price per Public Share in the MLAC IPO and is therefore calculated as $10.00 (MLAC per share MLAC IPO price) multiplied by 60,468,670 shares, or $604,686,700. The following table illustrates the valuation at the $10.00 issuance price per share in the MLAC IPO for each redemption scenario:

Assuming | Assuming | Assuming | Assuming | Assuming | |||||||||||

No | 25% | 50% | 75% | Maximum | |||||||||||

| Redemptions | | Redemptions | | Redemptions | | Redemptions | | Redemptions | ||||||

Public Shares outstanding post Business Combination |

| 25,300,000 |

| 19,573,629 |

| 13,847,258 |

| 8,120,887 |

| 2,394,516 | |||||

Company Unit Investor shares outstanding post Business Combination(1) |

| 21,563,032 |

| 21,563,032 |

| 21,563,032 |

| 21,563,032 |

| 21,563,032 | |||||

Sponsor and Affiliates shares outstanding post Business Combination(2) |

| 2,800,000 |

| 2,800,000 |

| 2,800,000 |

| 2,800,000 |

| 2,800,000 | |||||

Seller Related Parties shares outstanding post Business Combination(3) |

| 5,805,638 |

| 5,805,638 |

| 5,805,638 |

| 5,805,638 |

| 5,805,638 | |||||

Astral shares outstanding post Business Combination(4) |

| 2,000,000 |

| 2,000,000 |

| 2,000,000 |

| 2,000,000 |

| 2,000,000 | |||||

Foundation shares outstanding post Business Combination(5) |

| 3,000,000 |

| 3,000,000 |

| 3,000,000 |

| 3,000,000 |

| 3,000,000 | |||||

Total shares outstanding post Business Combination |

| 60,468,670 |

| 54,742,299 |

| 49,015,928 |

| 43,289,557 |

| 37,563,186 | |||||

Total valuation based on $10.00 issuance price per share in the MLAC IPO | $ | 604,686,700 | $ | 547,422,990 | $ | 490,159,280 | $ | 432,895,570 | $ | 375,631,860 | |||||

(1) | Assumes each Company Unit will be redeemed for one share of Pubco Class A Stock and no issuance of Adjustment Units. |

(2) | Includes 2,800,000 MLAC Founder Shares (including the 1,600,000 Sponsor Earnout Shares) (after accounting for the surrender of 4,387,500 MLAC Founder Shares by the Sponsor, the surrender of 495,000 Private Placement Shares held by the Sponsor, and the surrender of 310,000 Private Placement Shares held by BTIG). |

(3) | Includes the 2,547,252 Company Units issued to Dragonfly Ventures L.P., 3,258,386 Company Units issued to Dragonfly Ventures II, L.P. |

(4) | Includes the 2,000,000 Astral Post-Closing Shares. Does not include the Astral Earnout Shares, which will be held in escrow for the Escrow Period and may only be released to Astral upon the achievement of certain Triggering Events in accordance with the Astral Escrow Agreement. |

(5) | Up to 3,000,000 of Pubco Class A stock will be issued to the Foundation to the Foundation pursuant to the Foundation Transaction. In the event the Pubco Class A Stock cease to be nonvoting securities, the Foundation will forfeit a number of its Pubco Class A Stock and will receive from Pubco a number of pre-funded warrants convertible into Pubco Class A Stock prior to the time the Pubco Class A Stock cease to be nonvoting securities so that the Foundation’s beneficial ownership in Pubco does not exceed the Maximum Percentage. |

The foregoing required disclosure is not a guarantee that the trading price of Pubco Class A Stock will not be below the offering price in the MLAC IPO, nor is the required disclosure a guarantee that Pubco will attain any of the levels of valuation presented.

The above discussion and table are based on 30,992,500 MLAC Ordinary Shares outstanding on December 31, 2025.

The above discussion and table also exclude potential dilutive effects associated with future issuances or grants of equity or equity-linked securities by Pubco pursuant to the Incentive Plan expected to be adopted in connection with the Closing and that no Adjustment Units are issued.

The aforementioned equity issuances are not the only sources of potential dilution to the relative ownership percentage associated with shares of Pubco Class A Stock held by non-redeeming Public Shareholders after the Closing; any additional equity and equity-linked issuances by Pubco may result in additional dilution to Public Shareholders’ percentage ownership in Pubco, potentially significantly, and may have other effects, as described above and as further described in the “Risk Factors” section of this proxy statement/prospectus.

All of the relative percentages above are for illustrative purposes only and are based upon certain assumptions as described above. Should one or more of the assumptions prove incorrect, actual ownership percentages may vary materially from those described in this proxy statement/prospectus as anticipated, believed, estimated, expected or intended. See “Unaudited Pro Forma Condensed Combined Financial Information.”

Organizational Structure

Prior to the Transactions

The following simplified diagrams illustrate the ownership structures of MLAC, Pubco and the Company before the consummation of the Transactions:

MLAC

Pubco, the Pubco Subsidiaries and the Company

Following the Transactions

The following simplified diagram illustrates the ownership structure of Pubco following the consummation of the Transactions. The percentage ownerships of shares of Pubco Class A Stock and Pubco Class B Stock are presented assuming, among other things, that no Public Shareholders exercise redemption rights with respect to their Public Shares upon completion of the Business Combination:

Board of Directors and Executive Officers of Pubco Following the Transactions

As of the date of this proxy statement/prospectus, the directors of Pubco are Robert Hadick and Gerald Bartholomew Smith. Effective as of Closing, the current directors of Pubco will remain as directors of Pubco.

Effective as of the Closing, the Pubco Board will consist of one (1) or more members, each of whom shall be a natural person.

In addition to the current directors of Pubco who will remain as directors of Pubco, the following individuals will be nominated for election to the Pubco Board immediately following Closing:

a)Paul Grinberg

b)Sarkees John Nahas

All members of the Pubco Board shall be elected for a one-year term and may be re-elected for successive terms.

Immediately following Closing, the executive officers of Pubco will be as follows:

Name | | Age | | Position |

Gerald Bartholomew Smith | 49 | Chief Executive Officer, Director | ||

Laine Mihalchick Moljo | 40 | Chief Operating Officer | ||

Sean Ostrower | 40 | Chief Financial Officer |

For more information, see the sections of this proxy statement/prospectus entitled “Management of Pubco Following the Business Combination.”

Date, Time and Place of the Extraordinary General Meeting in lieu of an Annual General Meeting of MLAC Shareholders

The Meeting will be held on , 2026 at , Eastern Time, at 1345 Avenue of the Americas, New York, NY 10105 and virtually via live webcast on the Internet at https://www.cstproxy.com/mountainlakeacquisition/2026. You will be able to attend, vote your shares and submit questions during the Meeting via a live webcast available at https://www.cstproxy.com/mountainlakeacquisition/2026.

You or your proxyholder will be able to attend and vote at the Meeting by visiting https://www.cstproxy.com/mountainlakeacquisition/2026 and using a control number assigned by CST. To register and receive access to the Meeting, registered shareholders and beneficial owners (those holding shares through a stock brokerage account or by a bank or other holder of record) will need to follow the instructions applicable to them provided in this proxy statement/prospectus. You will need the voter control number included on your proxy card in order to be able to vote your shares or submit questions during the Meeting. If you do not have a voter control number, you will be able to listen to the Meeting only and you will not be able to vote or submit questions during the Meeting.

Voting Power; Record Date

MLAC Shareholders will be entitled to vote or direct votes to be cast at the Meeting if they owned MLAC Ordinary Shares at the close of business on , 2026, which is the Record Date for the Meeting. MLAC Shareholders are entitled to one vote at the Meeting for each MLAC Ordinary Share held as of the Record Date. If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or nominee, you should contact your broker, bank or nominee to ensure that votes related to the shares you beneficially own are properly counted. In this regard, you must provide the broker, bank or nominee with instructions on how to vote your shares or, if you wish to attend the Meeting and vote, obtain a proxy from your broker, bank or nominee.

As of the close of business on the Record Date, there were 30,992,500 MLAC Ordinary Shares issued and outstanding, consisting of 23,805,000 MLAC Class A Ordinary Shares and 7,187,500 MLAC Class B Ordinary Shares. Of these shares, 23,000,000 were Public Shares.

Quorum and Vote of MLAC Shareholders

A quorum of MLAC Shareholders is necessary to hold a valid meeting. A quorum for the Meeting consists of the holders of one-third of the then issued and outstanding MLAC Ordinary Shares (whether in person or by proxy). As of the Record Date, MLAC Shareholders holding 10,330,834 MLAC Ordinary Shares would be required to achieve a quorum at the Meeting without the MLAC Ordinary Shares held by the Sponsor. In addition to the MLAC Ordinary Shares held by the Sponsor, which represent approximately 24.8% of the issued and outstanding MLAC Ordinary Shares, MLAC will need MLAC Shareholders holding 2,648,334 MLAC Ordinary Shares, or 11.5%, of the 23,000,000 Public Shares represented in person or by proxy at the Meeting to hold a valid quorum.

To pass, each of the Business Combination Proposal, the Nasdaq Proposal, the Director Election Proposal and the Adjournment Proposal requires an ordinary resolution of MLAC Shareholders, which requires the affirmative vote of a simple majority of the votes cast by, or on behalf of, the MLAC Shareholders as, being entitled to do so, vote in person or, where proxies are allowed, by proxy at the Meeting (assuming the presence of a quorum). To pass, the Merger Proposal requires a special resolution of MLAC Shareholders, which requires the affirmative vote of at least two-thirds of the votes cast by, or on behalf of, the MLAC Shareholders as, being entitled to do so, vote in person or, where proxies are allowed, by proxy at the Meeting (assuming the presence of a quorum). MLAC Shareholders are also being asked to approve by way of ordinary resolutions, on a non-binding advisory basis, each of the Domestication and Organizational Documents Proposals. Although the MLAC Board is asking MLAC Shareholders to approve each of the Domestication and Organizational Documents Proposals on the non-binding advisory basis, regardless of the outcome of the non-binding advisory vote on each of the Domestication and Organizational Documents Proposals, the Amended and Restated Pubco Charter and Pubco’s Amended and Restated Bylaws will take effect upon the Closing if the Business Combination Proposal and the Merger Proposal are approved.

Assuming a quorum is established, an MLAC Shareholder’s failure to vote by proxy or to vote in person (including virtually) at the Meeting will have no effect on the Proposals. Abstentions and broker non-votes, while considered present for the purposes of establishing a quorum, are not treated as votes cast and will have no effect on any of the Proposals.

The Sponsor has agreed to vote its 7,682,500 MLAC Ordinary Shares, representing 24.8% of the issued and outstanding MLAC Ordinary Shares, in favor of each of the Proposals. As a result, with respect to each Proposal that require approval of MLAC Shareholders by an ordinary resolution, in addition to the Sponsor’s MLAC Ordinary Shares, MLAC would need only 7,813,751, or 34.0%, of the 23,000,000 Public Shares (assuming all issued and outstanding MLAC Ordinary Shares are voted at the Meeting), and would not need any of the 23,000,000 Public Shares (assuming a minimum number of MLAC Ordinary Shares to achieve a quorum are voted at the Meeting), to be voted in favor of such Proposals in order to have such Proposals approved. With respect to each Proposal that requires approval of MLAC Shareholders by a special resolution, in addition to the Sponsor’s MLAC Ordinary Shares, MLAC would need only 12,979,167, or 56.4%, of the 23,000,000 Public Shares (assuming all issued and outstanding MLAC Ordinary Shares are voted at the Meeting), and would not need any of the 23,000,000 Public Shares (assuming a minimum number of MLAC Ordinary Shares to achieve a quorum are voted at the Meeting), to be voted in favor of such Proposals in order to have such Proposals approved.

Redemption Rights

Pursuant to the MLAC Memorandum and Articles, Public Shareholders may elect to have their Public Shares redeemed for cash at the applicable redemption price per share equal to the quotient obtained by dividing (a) the aggregate amount on deposit in the Trust Account as of two (2) business days prior to the Closing, including interest (net of taxes payable), by (b) the total number of the then issued and outstanding Public Shares. As of the date of this proxy statement/prospectus, based on funds in the Trust Account of approximately $244.0 million as of April 27, 2026, this would have amounted to approximately $10.61 per share (including interest earned on the funds held in the Trust Account but less taxes payable). Public Shareholders may exercise redemption rights whether or not they are holders as of the Record Date and whether or not such shares are voted at the Meeting and whether they vote for or against the Business Combination Proposal. Notwithstanding the foregoing, the MLAC Memorandum and Articles provides that a Public Shareholder, together with any affiliate of such shareholder or any other person with whom such shareholder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will be restricted from redeeming its shares with respect to more than 15% of the Public Shares in the aggregate, without the prior consent of MLAC.

If a Public Shareholder exercises its redemption rights, then such Public Shareholder will be exchanging its Public Shares for cash and will not receive shares of Pubco Class A Stock upon consummation of the Business Combination. Such a Public Shareholder will be entitled to receive cash for its Public Shares only if it properly demands redemption and delivers its shares (either physically or electronically) to CST in accordance with the procedures described herein. See the section titled “Extraordinary General Meeting of MLAC Shareholders — Redemption Rights” for the procedures to be followed if you wish to redeem your Public Shares for cash. In connection with the MLAC IPO, the Sponsor and its Affiliates agreed to waive any redemption rights with respect to any MLAC Ordinary Shares held by them in connection with the completion of the Business Combination. Such waivers are standard in transactions of this type and the Sponsor and its Affiliates did not receive separate consideration for the waiver.

Appraisal Rights

MLAC Shareholders do not have appraisal rights in connection with the Business Combination under the DGCL or the Cayman Act.

In addition, Public Shareholders are still entitled to exercise the rights of redemption as detailed in this proxy statement/prospectus and the redemption proceeds payable to Public Shareholders who exercise such redemption rights will represent the fair value of those shares. For a discussion about the Public Shareholders’ redemption rights, please see “Extraordinary General Meeting of MLAC Shareholders — Redemption Rights.”

Proxy Solicitation

Proxies may be solicited by mail, telephone or in person. MLAC has engaged Sodali & Co as the proxy solicitor to assist in the solicitation of proxies. If an MLAC Shareholder grants a proxy, it may still vote its shares itself if it revokes its proxy before the Meeting. An MLAC Shareholder may also change its vote by entering a new vote by Internet or telephone, submitting a later-dated proxy or attending and voting, virtually via the live webcast or in person, during the Meeting as described in the section of this proxy statement/prospectus titled “Extraordinary General Meeting of MLAC Shareholders — Revoking Your Proxy.”

Interests of the Sponsor and its Affiliates in the Business Combination

When Public Shareholders consider the recommendation of the MLAC Board in favor of approval of the Business Combination and other Proposals, Public Shareholders should keep in mind that the Sponsor and its Affiliates have interests in the Proposals that are different from or in addition to (and which may conflict with), the interests of a Public Shareholder as an MLAC Shareholder. These interests include, among other things:

| • | the Sponsor paid $25,000 for the 7,187,500 MLAC Class B Ordinary Shares. Of these amounts, contemporaneously with the consummation of the Business Combination, the Sponsor shall submit for cancellation 4,387,500 MLAC Class B Ordinary Shares, as a result, the Sponsor will retain the Retained Sponsor Shares. If the Business Combination or another MLAC initial business combination is not consummated by June 16, 2026 (or such other date as approved by the MLAC Shareholders), MLAC will cease all operations except for the purpose of winding up. In such event, the 2,800,000 Retained Sponsor Shares held by the Sponsor (or any permitted distributees thereof, as applicable) will be worthless because the holders thereof entered into an agreement waiving entitlement to participate in any redemption or liquidating distributions with respect to such shares. Neither the Sponsor nor any other person received any compensation in exchange for this agreement to waive redemption and liquidation rights. Pursuant to terms of the Insider Letter and the Sponsor Lock-Up Agreement, the Retained Sponsor Shares are subject to a lock-up whereby, subject to certain limited exceptions, the Retained Sponsor Shares are not transferable until the earlier of (A) the Anniversary Release; provided that, if the VWAP of the shares of Pubco Class A Stock equals or exceeds $12.50 per share for any 20 consecutive trading days after Closing, then the Anniversary Release will be deemed to occur at 11:59 p.m. (New York City time) on such 20th consecutive trading day, or (B) subsequent to MLAC’s initial business combination, the date on which Pubco consummates a transaction which results in all of its shareholders having the right to exchange their shares for cash, securities or other properties. (The Sponsor may, on or before the Closing of the Business Combination, distribute some or all of the Retained Sponsor Shares held by it and such distributed Retained Sponsor Shares may be released from lock-up restrictions in connection with applicable stock exchange listing requirements.) In this regard, while the Retained Sponsor Shares are not the same as the MLAC Class A Ordinary Shares, are subject to certain restrictions that are not applicable to the MLAC Class A Ordinary Shares, and may become worthless if MLAC does not complete a business combination by June 16, 2026 (or such other date as approved by the MLAC Shareholders), the aggregate value of the 2,800,000 Retained Sponsor Shares owned by the Sponsor is estimated to be approximately $29.59 million, assuming the per share value of the Retained Sponsor Shares is the same as the $10.57 closing price of the MLAC Class A Ordinary Shares on Nasdaq on April 24, 2026; |

| • | the Sponsor has agreed that the 1,600,000 shares of Pubco Class A Stock to be issued to the Sponsor (of the total 2,800,000 Retained Sponsor Shares it will hold), will be held in escrow during the Earnout Period, subject to early release upon certain price-based Triggering Events. Additionally, any Retained Sponsor Shares that are released from escrow shall not be sold or transferred until the Anniversary Release; |

| • | the 495,000 MLAC Private Placement Shares held by the Sponsor (or any permitted distributees thereof, as applicable) will be forfeited immediately prior to the closing pursuant to the Sponsor Support Agreement. The Sponsor purchased the MLAC Private Placement Shares at an aggregate purchase price of $4,950,000, or $10.00 per unit, in the Private Placement consummated simultaneously with the MLAC IPO. The aggregate value of the 495,000 MLAC Private Placement Shares held by the Sponsor is estimated to be approximately $5.23 million, assuming the per unit value of the MLAC Private Placement Shares is the same as the $10.57 closing price of the MLAC Class Ordinary Shares on Nasdaq on April 24, 2026; |

| • | if the proposed Business Combination is consummated, immediately after the Closing the Sponsor and its Affiliates are anticipated to hold 4.9% of the outstanding shares of Pubco Common Stock, based on the assumptions set forth in the section of this proxy statement/prospectus entitled “Share Calculations and Ownership Percentages”, which also incorporate relevant assumptions further described in the section of this proxy statement/prospectus entitled “Unaudited Pro Forma Condensed Combined Financial Information” and “Beneficial Ownership of Securities” and assuming, among other assumptions further described in aforementioned sections of this proxy statement/ prospectus, no redemptions of Public Shares and no conversion of public share rights or private share rights prior to or in connection with the proposed Business Combination; |

| • | based on the difference in the effective purchase price of $0.003 per share paid for the MLAC Class B Ordinary Shares, as compared to the purchase price of $10.00 per Unit sold in the MLAC IPO, the Sponsor and its members may earn a positive |

| rate of return even if the share price of Pubco after the Closing falls below the price initially paid for the MLAC Units in the MLAC IPO and the unredeeming unaffiliated Public Shareholders experience a negative rate of return following the Closing of the Business Combination; |

| • | if, prior to the Closing, the Sponsor provides working capital loans to MLAC, up to $1,500,000 of which may be convertible into MLAC Private Placement Shares at the option of the Sponsor, such loans may not be repaid if no business combination is consummated and MLAC is forced to liquidate; provided, however, that, as of the date of this proxy statement/prospectus, there are no such working capital loans outstanding; |

| • | unless MLAC consummates an initial business combination, it is possible that MLAC’s officers, directors and the Sponsor may not receive reimbursement for out-of-pocket expenses incurred by them, to the extent that such expenses exceed the amount of available funds not deposited in the Trust Account (provided, however, that, as of the date of this proxy statement/prospectus, MLAC’s officers and directors have not incurred (nor are any of them expecting to incur) out-of-pocket expenses exceeding such funds available to MLAC for reimbursement thereof, but provided, further, that if any such expenses are incurred prior to consummation of the Business Combination, MLAC’s officers, directors and the Sponsor may not receive reimbursement therefor if the proposed Business Combination is not consummated); |

| • | if the Trust Account is liquidated, including in the event MLAC is unable to complete an initial business combination by June 16, 2026 (or such other date as approved by the MLAC Shareholders), the Sponsor has agreed that it will be liable to MLAC, if and to the extent any claims by a third party for services rendered or products sold to MLAC (except for MLAC’s independent auditors) or a prospective target business with which MLAC has entered into a written letter of intent, confidentiality or similar agreement or business combination agreement, reduce the amount of funds in the Trust Account to below the lesser of (i) $10.05 per public share and (ii) the actual amount per public share held in the Trust Account as of the date of the liquidation of the Trust Account, if less than $10.05 per share due to reductions in the value of the trust assets less taxes payable, provided, however, that such liability will not apply to any claims by a third party or prospective target business that executed a waiver of any and all rights to the monies held in the Trust Account (whether or not such waiver is enforceable), nor will it apply to any claims under MLAC’s indemnity of the underwriters of the MLAC IPO against certain liabilities, including liabilities under the Securities Act; |