Accounting policies

Dec. 31, 2025

The material accounting policies applied in the preparation of these consolidated financial statements are set out below. Where an

accounting policy is specific to a note, the policy is described in the note to which it relates. These policies have been consistently applied

to all the periods presented.

1.1 Reporting entity

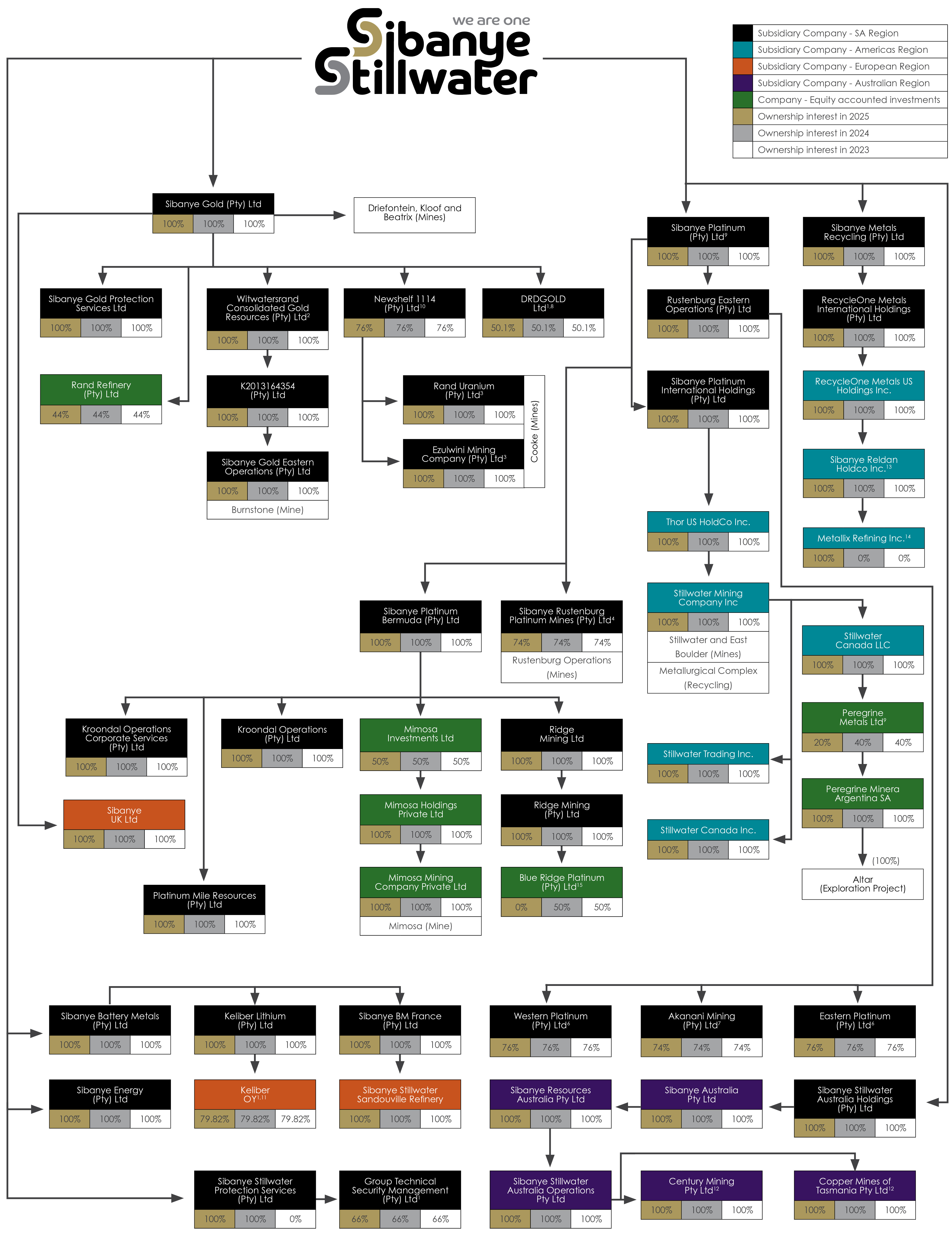

Sibanye Stillwater Limited (the Company) and its subsidiaries (together referred to as the Group or Sibanye-Stillwater) is a multinational

mining and metals processing Group with a diverse portfolio of mining and processing operations, projects and investments across five

continents. The Group is also one of the foremost global recyclers of PGM autocatalysts and has interests in leading mine tailings

retreatment operations. Sibanye-Stillwater has established itself as one of the world’s largest primary producers of platinum, palladium and

rhodium and is also a top tier gold producer. It also produces and refines iridium and ruthenium, nickel, chrome, copper and cobalt. The

Group also built and diversified its asset portfolio into battery metals and green metals mining and processing, and increased its presence in

the circular economy by growing and diversifying its recycling and tailings reprocessing operations globally. Domiciled in South Africa,

Sibanye-Stillwater currently owns and operates a portfolio of high-quality operations and projects, which are grouped into four regions,

namely, Southern Africa (SA region), Americas, Europe and Australia.

The SA region houses the gold and PGM operations and projects located in South Africa and Zimbabwe. The underground and surface

gold mining operations in South Africa are the Driefontein, Kloof and Cooke operations in the West Witwatersrand (West Wits) region,

DRDGOLD Limited (DRDGOLD) with a surface tailings treatment plant in the East of Johannesburg in Gauteng and in the West Wits, and the

Beatrix operation in the southern Free State. Sibanye-Stillwater also owns and manages significant gold extraction and processing facilities

where ore is treated and beneficiated to produce gold doré. In addition, several organic projects currently underway are aimed at

sustaining these gold mining operations into the long term. Burnstone is a shallow developmental stage gold mine and processing

operation located in the South Rand Goldfield of the Witwatersrand Basin in the Mpumalanga province, and comprises two established

shaft complexes, a carbon-in-leach gold processing plant, tailings storage facility and related surface infrastructure and mining rights. In

line with the Group's capital allocation framework, it was decided to delay the Burnstone project, which is currently under care-and-

maintenance. The Southern Free State project is an advanced exploration stage project that includes the Bloemhoek, De Bron-Merriespruit,

Robijn and Hakkies areas. It is located adjacent to the Beatrix operation in the Free State province.

Beatrix, a conventional mining operation, comprises two operating vertical shafts and one metallurgical plant mining the Beatrix/VS5 reef,

the Aandenk/Kalkoenkrans reef as well as some historical surface rock dump material. During 2024, the Group agreed to sell the Beatrix 4

shaft which includes the Beisa uranium project. Driefontein is an established mine consisting of four operating vertical shaft complexes and

one metallurgical plant mining three different reefs as well as some historical surface rock dump material. Kloof is also an ongoing mine with

two operating vertical shaft complexes. Four reefs are extracted at Kloof, together with the mining of some historical surface rock dump

material. The Cooke underground operations consist of four vertical shafts, which currently are under care-and-maintenance. The surface

mining section, known as Randfontein Surface Operations, mines historical surface tailings facilities and surface rock dumps, processing

them at the Cooke and Ezulwini metallurgical plants.

The PGM assets in the SA region are the Kroondal operation, the Rustenburg operation (SRPM), the Marikana operation (Marikana) and the

tailings retreatment entity, Platinum Mile in the North West Province, and Mimosa (50%) in Zimbabwe. Marikana currently has five

contributing shafts namely K3, K4 (commenced production in 2023), Rowland, Saffy and E3 and the ore mined at the Marikana operations

is processed through four of the eight concentrators on site. The PGM concentrate produced is dispatched to the smelter where a sulphide-

rich matte is produced for further processing at the base metal refinery (BMR). At the BMR, base metals are removed and the resulting

PGM-rich product is sent to the precious metal refinery (PMR) for final treatment. Marikana therefore sells refined metals to customers. In

addition to underground operations, there is one tailings retreatment operation (Bulk Tailings Treatment (BTT) plant), which transitioned from

hydraulic remining to mechanical remining of a dormant tailings storage facility during the period and the tailings are retreated at the BTT

plant for the recovery of coarse chrome and PGMs.

The Rustenburg operation comprise of three operating vertical shafts (Siphumelele 1, Khuseleka 1 and Thembelani 1), two declines at

Bathopele, a concentrating plant at the Waterval UG2 concentrator and a chrome recovery plant, the Western Limb tailings retreatment

plant and related surface infrastructure and assets. In addition, remining operations are carried out on one dormant tailings storage facility

(Waterval West dam). Fresh ore is processed through the Waterval UG2 concentrator. Tailings are treated at the Western Limb Tailings

Retreatment Plant, Platinum Mile and at the Chrome retreatment plant where a saleable chromite concentrate is recovered. Tailings from

the Rustenburg operation are piped to Platinum Mile for further beneficiation and recovery of chrome and PGMs. The tailings from Platinum

Mile are pumped to an active tailings storage facility for final disposal. The Rustenburg operation has a tolling agreement with a third party

and currently sells refined metals as well as PGM concentrate to customers. In addition, Platinum Mile successfully commissioned a coarse

chrome recovery plant in 2023.

Kroondal, which now forms part of and reported under the Rustenburg operation, comprises of four operating decline shafts. Fresh ore is

processed at Kroondal through two concentrator plants (K1 and K2). Tailings from the K1 and K2 plants are piped to three adjacent tailings

storage facilities and at a fourth tailings storage facility at Marikana. Platinum Mile is a tailings retreatment facility located on the

Rustenburg lease area adjacent to our Kroondal operations. This facility recovers PGMs and chrome from the live tailings at our Rustenburg

operations. Kroondal and Platinum Mile currently only sells PGM concentrate and chrome to customers.

The US region houses the PGM operations located in the US and exploration-stage projects located in Canada and Argentina. The US PGM

operations include the East Boulder and Stillwater mining operations (including the Blitz project) in Montana. The assets in Montana also

include the Metallurgical complex in Columbus, Montana. This complex houses the smelter, BMR and an analytical laboratory which

produces a PGM-rich filter cake that is further refined by a third-party precious metal refinery. These processing and metallurgical facilities

are also used to process recycled material such as spent autocatalytic convertors and petroleum refinery catalysts. The US region also

includes the Reldan Group of Companies (Reldan) (see note 16.2) which is a precious metals recycling group with facilities in Pennsylvania,

USA, as well as Mexico and India, processing primarily e-scrap to produce both green precious and base metals. Also included in the US

region is the newly acquired Metallix Refining (Metallix) which produces recycled precious metals, including gold, silver and PGMs, primarily

from industrial waste streams. It operates two processing and recycling operations in Greenville, North Carolina. Metallix has a global

customer base, which it services from the United Kingdom and South Korea, in addition to its customers in the United States (US).

Keliber, a Finnish mining and battery chemical company, owns the Keliber project, an advanced lithium hydroxide project located in the

Kaustinen region of Finland. Since the Sibanye-Stillwater Board of Directors approved the Keliber project and the immediate construction of

the Keliber Lithium Refinery in 2022, construction activities thereof have continued successfully after commencing in March 2023. Similarly,

the earthworks and selected infrastructure works commenced at the Päiväneva concentrator site in late 2023. Once developed, the

Keliber project will sustainably produce battery-grade lithium hydroxide. Following a detailed multidisciplinary assessment of various project

start up scenarios for Keliber during H2 2025, Sibanye-Stillwater and its partner, Finnish Minerals Group, agreed that a staged startup for the

Keliber lithium project was the most responsible approach, as staged commissioning of the mine, concentrator, and refinery reduces ramp-

up risk by prioritising operational readiness in the mining and concentrating stages before determining the appropriate timing for refinery

commissioning. The first stage of the project start up began during Q1 2026. The Group holds a 79.82% shareholding interest in Keliber. In

2022, the Group also acquired French mining group Eramet SA's Sandouville hydrometallurgical nickel processing facilities near Le Havre,

France's second largest industrial port. Sandouville's production was severely hampered by plant availability in 2023 and in 2025, the

production of nickel cathodes at the Sandouville nickel refinery ceased. The pre-feasibility study to assess the potential conversion of the

Sandouville plant to produce pCAM (the GalliCam project) is underway. The study will continue into 2026, with a decision on progressing on

the project to be evaluated by the end of H1 2026.

The Group's green metals investments also include the acquisition of a 100% stake in the Australian based entity, New Century Resources

Limited (Century), which owns a zinc tailings retreatment operation. The Group has also exercised an option to acquire a 100%

shareholding in Copper Mines of Tasmania Proprietary Limited, who owns the Mt Lyell Copper Mine in Australia .

1.2 Basis of preparation

The consolidated financial statements for the year ended 31 December 2025 have been prepared on a going concern basis in

accordance with IFRS Accounting Standards, as issued by the International Accounting Standards Board (IASB), the South African Institute

of Chartered Accountants Financial Reporting Guides issued by the Accounting Practices Committee and Financial Reporting

Pronouncements issued by the Financial Reporting Standards Council, as well as the requirements of the South African Companies Act and

JSE Listings Requirements. The consolidated financial statements have been prepared under the historical cost convention, except for

certain financial assets and financial liabilities (including derivative instruments) which are measured at fair value through profit or loss or

other comprehensive income.

Standards, interpretations and amendments to published standards effective for the year ended 31 December 2025

During the financial year, the following amendments to standards applicable to the Group became effective and had no material impact

on the Group’s consolidated financial statements:

Pronouncement | Details of amendments | Effective date1 |

Lack of Exchangeability (Amendments to IAS 21) | Under IAS 21 The Effects of Changes in Foreign Exchange Rates (IAS 21), a spot exchange rate is used when translating a foreign currency transaction. In some rare circumstances, it is possible that one currency cannot be exchanged into another. Consequently, market participants are unable to buy and sell currency to meet their needs at the official exchange rate and turn instead to unofficial, parallel markets. The IASB amended IAS 21 to clarify when a currency is exchangeable to another currency and how a spot rate can be estimated when a currency lacks exchangeability. This amendment is applicable to the Group's investment in Mimosa (domiciled in Zimbabwe), however no material impact was identified. | 1 January 2025 |

Amendments to Illustrative Examples on IFRS 7, IFRS 18, IAS 1, IAS 8, IAS 36 and IAS 37- Disclosures about Uncertainties in the Financial Statements | These amendments include examples illustrating how an entity applies the requirements in IFRS Accounting Standards to disclose the effects of uncertainties in its financial statements. The examples do not add to or change requirements in IFRS Accounting Standards and therefore there are no transition requirements. | The examples do not have an effective date, but may be considered for December 2025 year-ends. |

1Effective date refers to annual period beginning on or after the effective date

Standards, interpretations and amendments to published standards which are not yet effective

Certain new standards, amendments and interpretations to existing standards have been published that apply to the accounting periods

beginning on or after 1 January 2026 but have not been early adopted by the Group. The standards, amendments and interpretations that

are applicable to the Group are:

Pronouncement | Details of amendments | Effective date1 |

Amendments to the classification and measurement of financial instruments (Amendments to IFRS 9 Financial Instruments (IFRS 9) and IFRS 7 Financial Instruments: Disclosures (IFRS 7))2 | The amendments provide guidance on the classification of financial assets with contingent features. Under IFRS 9, it was unclear whether the contractual cash flows of some financial assets with ESG-linked features represented the solely payments of principal and interest (SPPI) criterion, which is a condition for measurement at amortised cost. The amendments apply to all contingent features, not just ESG-linked features and introduce an additional SPPI test for financial assets with contingent features that are not related directly to a change in basic lending risks or costs. The amendments also include additional disclosures for all financial assets and financial liabilities that have certain contingent features that are not related directly to a change in basic lending risks or costs, and are not measured at fair value through profit or loss. The amendments to IFRS 9 also clarifies when a financial asset and financial liability is recognised and derecognised and provides an exception for certain financial liabilities settled using an electronic payment system. The exception allows for financial liabilities to be derecognised before the settlement date if certain criteria are met. | 1 January 2026 |

Annual improvements to IFRS Accounting Standards (Amendments to IFRS 7, IFRS 9, IFRS 10 Consolidated Financial Statements, and IAS 7 Statement of Cash Flows)2 | The IASB published annual improvements to IFRS Accounting Standards relating to various standards applied by the Group in the consolidated financial statements. The amendments are primarily clarifications, internal referencing updates and editorial changes to IFRS Accounting Standards. | 1 January 2026 |

Contracts Referencing Nature-dependent Electricity (Amendments to IFRS 9 and IFRS 7)2 | The amendments address challenges in contracts referencing nature-dependent electricity, referred to as renewable power purchase agreements (PPAs). The amendments include the own-use exemption for purchasers in PPAs and hedge accounting requirements for purchasers and sellers in PPAs. To apply the own-use exemption to a PPA, IFRS 9 currently requires the contract to be for receipt of electricity in line with the entity’s expected purchase or usage requirements. The amendments allow an entity to apply the own-use exemption to PPAs if the entity is, and expects to be, a net-purchaser of electricity for the contract period. | 1 January 2026 |

IFRS 18 Presentation and Disclosure in Financial Statements (IFRS 18) | IFRS 18 was issued to address the need for more relevant information in financial statements. IFRS 18 will have no impact on net profit, however it will change how the Group's results are presented on the consolidated income statement and information disclosed in the notes to the consolidated financial statements. This also includes disclosure of certain non-GAAP measures, which will form part of the audited consolidated financial statements. IFRS 18 introduces a more structured income statement such as a newly defined subtotal for operating profit and a requirement for entities to allocate all income and expenses between three new distinct categories based on the entity’s main business activities (operating, investing, and financing activities). IFRS 18 also requires entities to analyse their operating expenses directly on the income statement, which is either by nature, by function or using a mixed presentation. IFRS 18 also requires entities to report some of their non-GAAP measures in the financial statements. It introduces a narrow definition for management performance measures (MPM) and requires MPMs to be a subtotal of income and expenses that is used in public communications outside of the financial statements and reflective of management’s view of financial performance of an entity as a whole. Management is in the process of assessing the potential impact on the Group's consolidated financial statements. | 1 January 2027 |

1Effective date refers to annual period beginning on or after said date

2No material impact expected

Significant accounting judgements and estimates

The preparation of the consolidated financial statements requires the Group’s management to make estimates and assumptions that

affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated

financial statements, and the reported amounts of revenues and expenses during the reporting period. The determination of estimates

requires the exercise of judgement based on various assumptions and other factors such as historical experience, current and expected

economic conditions, and in some cases valuation techniques. Actual results could differ from those estimates.

For material accounting policies that are subject to significant judgement, estimates and assumptions, see the following notes to the

consolidated financial statements:

Accounting policy | Note to the consolidated financial statements |

Unconsolidated structured entities | 1 - Consolidation |

Revenue | 3 - Revenue |

Cash-settled share-based payment obligation | 6 - Share-based payments |

Royalties, mining and income tax, and deferred tax | 11 - Royalties, mining and income tax, and deferred tax |

Property, plant and equipment | 14 - Property, plant and equipment |

Business combinations | 16 - Acquisitions |

Goodwill | 17 - Goodwill and other intangibles |

Equity-accounted investments | 18 - Equity-accounted investments |

Other investments | 19 - Other investments |

Other receivables and other payables | 21 - Other receivables and other payables |

Inventories | 22 - Inventories |

Borrowings and derivative financial instrument | 27 - Borrowings and derivative financial instrument |

Environmental rehabilitation obligation | 29 - Environmental rehabilitation obligation and other provisions |

Occupational healthcare obligation | 30 - Occupational healthcare obligation |

Deferred revenue | 31 - Deferred revenue |

Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of

future events that are believed to be reasonable under the circumstances.

The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities

within the financial period are discussed under the relevant note of the item affected.

1.3 Consolidation

1The NCI in the statement of changes in equity at 31 December 2025, relates to the attributable share of accumulated profits of DRDGOLD, Group Technical Security

Management Proprietary Limited (GTSM) and Keliber OY (see note 26)

2Witwatersrand Consolidated Gold Resources Proprietary Limited (Wits Gold) has ceded and pledged its shares in K2013164354 Proprietary Limited (K2013) (a dormant

entity) and K2013 has ceded and pledged it shares in Sibanye Gold Eastern Operations Proprietary Limited (SGEO) in favour of the lenders of the Burnstone Debt (see note

27.6)

3Rand Uranium Proprietary Limited (Rand Uranium) and Ezulwini Mining Company Proprietary Limited (Ezulwini) together own a number of underground and surface mining

operations

4A 26% stake in Sibanye Rustenburg Platinum Mines Proprietary Limited (SRPM) was acquired through Newshelf 1335 Proprietary Limited (B-BBEE SPV) in terms of the

Rustenburg operation transaction, The shareholders of B-BBEE SPV are Rustenburg Mine Employees Trust (30.4%), Rustenburg Mine Community Development Trust (24.8%),

Bakgatla-Ba-Kgafela Investment Holdings (24.8%) and Siyanda Resources Proprietary Limited (20.0%). The Rustenburg Mine Employees Trust and the Rustenburg Mine

Community Development Trust are controlled and consolidated by Sibanye-Stillwater and cash-settled share-based payment obligations amounting to R986 million and

R804 million, respectively, are eliminated upon consolidation. During H2 2023, the sale transaction between Rustenburg Platinum Mines Limited (subsidiary of Anglo

Platinum Mines Limited) and SRPM became effective, which resulted in SRPM assuming full ownership of Kroondal. Following the intercompany transfer of the Kroondal

operations to SRPM in 2025, Kroondal is reported as part of the Rustenburg operation

5The Group has no current or contractual obligation to provide financial support to any of its structured entities

6Sibanye-Stillwater recognises no NCI in Western Platinum Proprietary Limited (WPL) and Eastern Platinum Proprietary Limited (EPL). The shareholding of Lonplats Employee

Share Ownership Trust (Employee Trust) (3.8%,) the Bapo Ba Mogale Local Economic Development Trust (Bapo Trust) (0.9%) and Lonplats Marikana Community

Development Trust (Community Trust) (0.9%) (together Marikana Trusts) is not considered since these trusts are controlled and consolidated by Sibanye-Stillwater. Cash-

settled share-based payment obligations amounting to R905 million relating to the Marikana Trusts are eliminated upon consolidation. In addition, as a result of the

Marikana broad-based black economic empowerment (B-BBEE) transaction (see note 6.4), the equity interests of shareholders in WPL and EPL, including all non-

controlling shareholders, were replaced with the right to receive dividends. As a result, the effective shareholding interests were replaced by a share-based payment

obligation and dividend obligation for entities not forming part of the Group (see note 6.4 and 21.2)

7Sibanye-Stillwater recognises no NCI in Akanani on a similar basis as described for WPL and EPL below (see footnote 6 above), since a revised shareholders' agreement

replaced the equity interests with a right to receive dividends

8The effective shareholding at 31 December 2025 was 50.10% (2024: 50.23% and 2023: 50.28%) after considering treasury shares held by DRDGOLD and new share issues

and subscriptions during 2025 (see note 26.1)

9At 31 December 2025, the Group had a 20% legal interest in Peregrine Metals Limited (Peregrine), as a result of completion of the Initial Earn-in arrangement of 80% by

Aldebaran Resources Inc. (Aldebaran) during 2025 (see note 18.3)

10The Group has a 76% legal interest in the Newshelf 1114 Proprietary Limited (Newshelf 1114) group and the NCI can acquire a further 2% legal shareholding once they

have implemented the necessary funding structure. However, no accounting NCI is recognised, since the NCI’s vendor loan financing exceeds their proportionate

interest in Newshelf 1114 and therefore no effective shareholding exists

11The Group has an effective shareholding of 79.82% (2024: 79.82%, 2023: 79.82%) in Keliber OY at 31 December 2025. Keliber Oy is incorporated in Finland

12The Group acquired a 100% shareholding in the Century on 10 May 2023 and also exercised its option to acquire a 100% shareholding in Copper Mines of Tasmania

Proprietary Limited which owns the Mt Lyell copper mine

13The Group, through Sibanye Reldan Holdco Inc., acquired a 100% shareholding in the Reldan Group of Companies (Reldan) on 15 March 2024 (see note 16.2)

14The Group, through Sibanye Reldan Holdco Inc., acquired a 100% shareholding in Metallix Refining (Metallix) on 4 September 2025 (see note 16.1)

15During 2025, the Group disposed of its interest in Blue Ridge Platinum (Proprietary) Limited

Subsidiaries

Subsidiaries are all entities over which the Group exercises control. The Group controls an entity when it is exposed to, or has rights to,

variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries

are consolidated from the date on which control is obtained by the Group until the date on which control ceases. Control is reassessed if

facts and circumstances indicate that there are changes to one or more of the elements of control.

Inter-company transactions, balances and unrealised gains or losses on transactions between Group companies are eliminated on

consolidation. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by

the Group.

Unconsolidated structured entities

In assessing whether the Group controls a special purpose vehicle (SPV), significant judgements include the extent of the Group's

involvement in the setup and design of the power purchase agreement (PPA) including decisions related to the underlying infrastructure,

whether there is any financial recourse to the Group in relation to financing the SPV or any project-related risk, as well as terms and

conditions of any options to acquire the underlying power generating infrastructure.

During 2023, the Group entered into two substantially similar wind energy power purchase agreements. The PPA is a 89-megawatt (MW)

project entered into by Sibanye Energy Proprietary Limited (Sibanye Energy). This clean energy will be generated by the Castle Wind Farm

(Castle), located near the town of De Aar in the Northern Cape province of South Africa, and will supply the SA operations via a wheeling

agreement with Eskom. Under the terms of the 15-year PPA, Castle is funded, built, and operated by a project consortium. The Group has

an option to acquire the project company or plant at the end of the 15-year PPA in exchange for an additional payment incorporated into

the energy tariff as well as a nominal exercise price. Alternatively, the PPA can be extended for an additional period of five years,

whereafter it can be further extended for a period agreed between the parties. Other than in the event of default on electricity payments

to be made by the Group, there is no recourse to the Group for funding or project-related risk. Castle became operational during Q1 2025.

The Group will pay for all electricity produced based on a pre-determined tariff, adjusted for inflation over the term of the PPA. The

arrangement does not contain any fixed or minimum payments.

The second PPA is the Witberg wind energy project, located near Matjiesfontein in the Western Cape province with a contracted capacity

of 103MW (Witberg), also entered into by Sibanye Energy. The terms of the Witberg PPA are similar to Castle. Witberg will also supply the SA

operations via a wheeling agreement with Eskom. The project cost will be fully funded by Red Rocket, a South African Independent Power

Producer developing the project, together with its lenders. Similar to the Castle project, the Group committed to a 15-year PPA and also

has a purchase option on the same terms as the Castle project. There is also no recourse to the Group, except in the event of electricity

payment default. When Witberg becomes operational, the Group will also pay a pre-determined tariff for electricity produced, adjusted

for inflation over the term of the PPA. Similar to Castle, there are no fixed or minimum payments.

During 2024, Sibanye-Stillwater concluded an additional 140MW wind energy project, the Umsinde Emoyeni Wind Farm, located on the

border between the Northern Cape Province and the Western Cape Province near Murraysburg, South Africa. Commercial operation is

scheduled for Q4 2026. The project will supply Sibanye-Stillwater’s SA operations utilising the national grid through a secured wheeling

agreement with Eskom. Under the terms of a -year PPA with Sibanye-Stillwater, the project will be fully funded by a project

consortium which will build, own and operate the project. The arrangement does not contain any fixed or minimum payments and the

Group does not have an option to purchase the wind farm.

The Group holds no shareholding or voting interest in the project companies and did not provide a guarantee for any of the obligations of

these companies towards their shareholders or funders. Management concluded that the Group does not control the project companies

under IFRS 10 Consolidated Financial Statements (IFRS 10) since it does not have power over the relevant activities as contemplated in IFRS

10. At the reporting date, there were no assets or liabilities recognised by the Group relating to the project companies and no financial or

other support had been provided. There is also no intention to provide financial or other support to the project companies, other than

payment of the electricity tariff in future periods when electricity is produced.

Transactions with shareholders

Transactions with owners in the capacity as equity participants are not recognised in profit or loss, but instead are recognised in equity with

a corresponding change in assets or liabilities. Changes in a parent’s ownership interest in a subsidiary that does not result in the parent

losing control of the subsidiary are equity transactions.

1.4 Foreign currencies

Functional and presentation currency

Items included in the financial statements of each of the Group’s entities are measured using the currency of the primary economic

environment in which the entity operates (the functional currency). The consolidated financial statements are presented in South African

rand (SA rand), which is the Group’s presentation currency.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the

transactions. Monetary assets and liabilities are translated into the functional currency at each reporting date. Foreign exchange gains and

losses resulting from the settlement of such transactions and from the translation of monetary assets and liabilities denominated in foreign

currencies, are recognised in profit or loss.

Foreign operations

The results and financial position of all the Group entities that have a functional currency different from the presentation currency are

translated into the presentation currency as follows:

•Assets and liabilities are translated at the exchange rate ruling at the reporting date. Equity items are translated at historical rates. The

income and expenses are translated at the average exchange rate for the year, unless this average is not a reasonable approximation

of the rates prevailing on the transaction dates, in which case these items are translated at the rate prevailing on the date of the

transaction. Exchange differences on translation are accounted for in other comprehensive income and accumulated in the foreign

currency translation reserve (FCTR) in the consolidated statement of changes in equity. These differences are recognised in profit or loss

upon realisation of the underlying operation

•Exchange differences arising from the translation of the net investment in foreign operations, which includes certain long-term

borrowings (i.e. the reporting entity’s interest in the net assets of that operation), are taken to other comprehensive income. When a

foreign operation is sold, exchange differences that were recorded in other comprehensive income are recognised in profit or loss as

part of the gain or loss on disposal. If the Group disposes of part of its interest in a subsidiary but retains control, then the relevant

proportion of the cumulative amount is reattributed to NCI. When the Group disposes of only part of an associate or joint venture while

retaining significant influence or joint control, the relevant proportion of the cumulative amount is reclassified to profit or loss. If a

company in the Group repays a portion of long-term borrowings forming part of a net investment in foreign operations, amounts

previously recorded in other comprehensive income are only recognised in profit or loss upon disposal of the relevant operation. These

amounts are reclassified to profit or loss through OCI, consistent with where the amounts were previously included

•Goodwill and fair value adjustments arising on the acquisition of a foreign operation are treated as assets and liabilities of the foreign

operation and are translated at each reporting date at the closing rate

1.5 Assets and associated liabilities classified as held for sale

During H2 2024, the Group agreed to sell the Beatrix 4 shaft which forms part of the Beatrix gold operations and includes the Beisa uranium

project, to Neo Energy Metals Plc. (Neo Energy). The transaction will allow the Beisa project to be developed by Neo Energy, while Sibanye-

Stillwater will retain exposure to future uranium production. The Beatrix 4 shaft was placed on care and maintenance by Sibanye-Stillwater

in 2023 primarily due to declining gold reserves and a depressed uranium price, which has subsequently recovered. The transaction

includes total consideration of R500 million, comprising R250 million cash and R250 million in newly issued shares in Neo Energy (equalling

approximately 40% shareholding in Neo Energy at the time of signing the sale agreement). The transaction was subject to certain

outstanding conditions precedent at the reporting date, however the assets and liabilities associated with the transaction were classified as

held for sale in accordance with the requirements of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations (IFRS 5). Neo

Energy will assume responsibility for all Beatrix 4 shaft rehabilitation and environmental liabilities, which amounts to a carrying value of

R480 million (2024: R451 million) at 31 December 2025. Property, plant and equipment of R30 million (2024: R30 million) relating to the Beatrix

4 shaft disposal, which is measured at the lower of its carrying value and fair value less cost to sell, is included in assets held for sale at 31

December 2025 and 31 December 2024.

During H1 2025, following the Group's decision to withdraw from the Rhyolite Ridge joint venture agreement, it was decided to sell its

investment in ioneer Limited (ioneer). The Group held 145,862,742 shares in ioneer representing 6.19% of their share capital. At 30 June 2025,

the investment (R164 million) was classified as held for sale in accordance with the requirements of IFRS 5. The sale of ioneer was effective

during H2 2025 with the proceeds on the sale amounting to R186 million. The initial fair value of the investment was R1,134 million when it

was acquired.

During H1 2025, DRDGOLD decided to sell its 50.25% share in Stellar, a renewable energy company developing a solar plant in Limpopo,

South Africa. The decision was based on DRDGOLD's decision to focus on its core operating activities. DRDGOLD's investment in Stellar was

classified as held for sale in accordance with the requirements of IFRS 5. Property, plant and equipment and capital prepayments of

R105 million and other net assets of R6 million was included in assets held for sale. The sale of Stellar was effective during H2 2025 with the

proceeds on the sale amounting to R132 million. At 31 December 2025, no other assets are classified as assets held for sale (2024:

R40 million).