Table of Contents. | ||||||||

| Section | Page | ||||

| Corporate Data: | |||||

| Consolidated Financial Results: | |||||

| Portfolio Data: | |||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 2 |  | ||||||

Investor Company Summary. | ||||||||

| Executive Management Team | ||||||||

| Laura Clark | Chief Executive Officer, Director | |||||||

| John Nahas | Chief Operating Officer | |||||||

| Michael Fitzmaurice | Chief Financial Officer | |||||||

David E. Lanzer | General Counsel and Corporate Secretary | |||||||

| Board of Directors | ||||||||

| Tyler H. Rose | Chairman | |||||||

Laura Clark | Chief Executive Officer, Director | |||||||

| Robert L. Antin | Director | |||||||

| Michael S. Frankel | Director | |||||||

| Diana J. Ingram | Director | |||||||

| Angela L. Kleiman | Director | |||||||

| Debra L. Morris | Director | |||||||

David P. Stockert | Director | |||||||

| Howard Schwimmer | Director | |||||||

| Investor Relations Information | ||||||||

Mikayla Lynch | ||||||||

Director, Investor Relations and Capital Markets | ||||||||

mlynch@rexfordindustrial.com | ||||||||

| Equity Research Coverage | ||||||||||||||||||||||||||||||||

| BofA Securities | Samir Khanal | (646) 855-1497 | Green Street Advisors | Vince Tibone | (949) 640-8780 | |||||||||||||||||||||||||||

| Barclays | Brendan Lynch | (212) 526-9428 | J.P. Morgan Securities | Michael Mueller | (212) 622-6689 | |||||||||||||||||||||||||||

| BMO Capital Markets | John Kim | (212) 885-4115 | Jefferies LLC | Jonathan Petersen | (212) 284-1705 | |||||||||||||||||||||||||||

| BNP Paribas Exane | Nate Crossett | (646) 342-1588 | Mizuho Securities USA | Vikram Malhotra | (212) 282-3827 | |||||||||||||||||||||||||||

Cantor Fitzgerald | Richard Anderson | (929) 441-6927 | Robert W. Baird & Co. | Nicholas Thillman | (414) 298-5053 | |||||||||||||||||||||||||||

| Citigroup Investment Research | Craig Mailman | (212) 816-4471 | Scotiabank | Greg McGinniss | (212) 225-6906 | |||||||||||||||||||||||||||

| Colliers Securities | Barry Oxford | (203) 961-6573 | Truist Securities | Anthony Hau | (212) 303-4176 | |||||||||||||||||||||||||||

Deutsche Bank | Omotayo Okusanya | (212) 250-9284 | Wells Fargo Securities | Blaine Heck | (443) 263-6529 | |||||||||||||||||||||||||||

Evercore ISI | Michael Griffin | (212) 446-9462 | Wolfe Research | Andrew Rosivach | (646) 582-9250 | |||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 3 | | ||||||

Company Overview. | ||||||||

| For the Quarter Ended March 31, 2026 | ||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 4 | | ||||||

Highlights - Consolidated Financial Results. | ||||||||

| Quarterly Results | (in millions) | |||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 5 | | ||||||

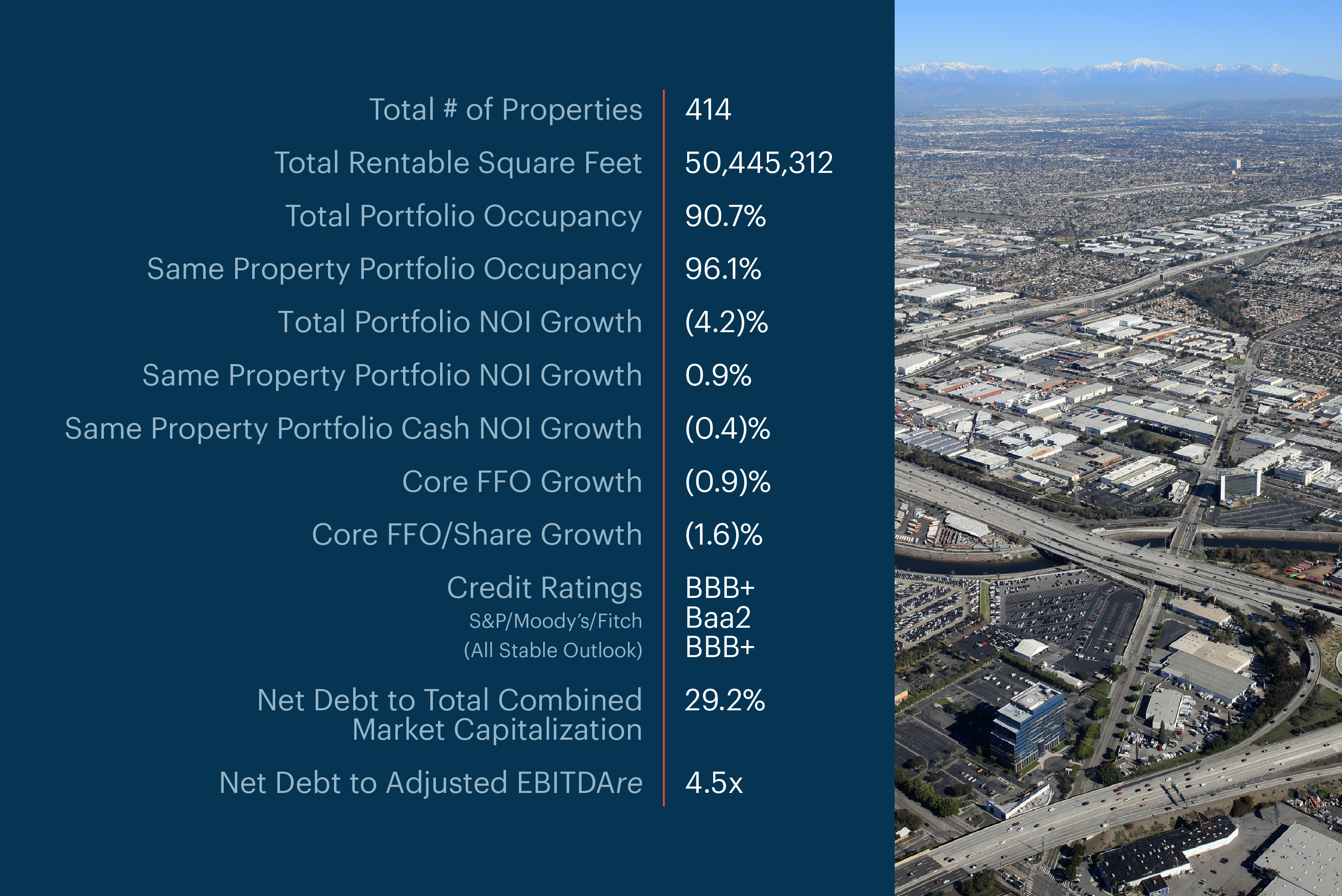

Financial and Portfolio Highlights and Capitalization Data.(1) | ||||||||

| (in thousands except share and per share data and portfolio statistics) | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||

| Financial Results: | |||||||||||||||||||||||||||||

| Total rental income | $ | 242,141 | $ | 243,230 | $ | 246,757 | $ | 241,568 | $ | 248,821 | |||||||||||||||||||

| Net income (loss) | $ | 94,562 | $ | (67,735) | $ | 93,056 | $ | 120,394 | $ | 74,048 | |||||||||||||||||||

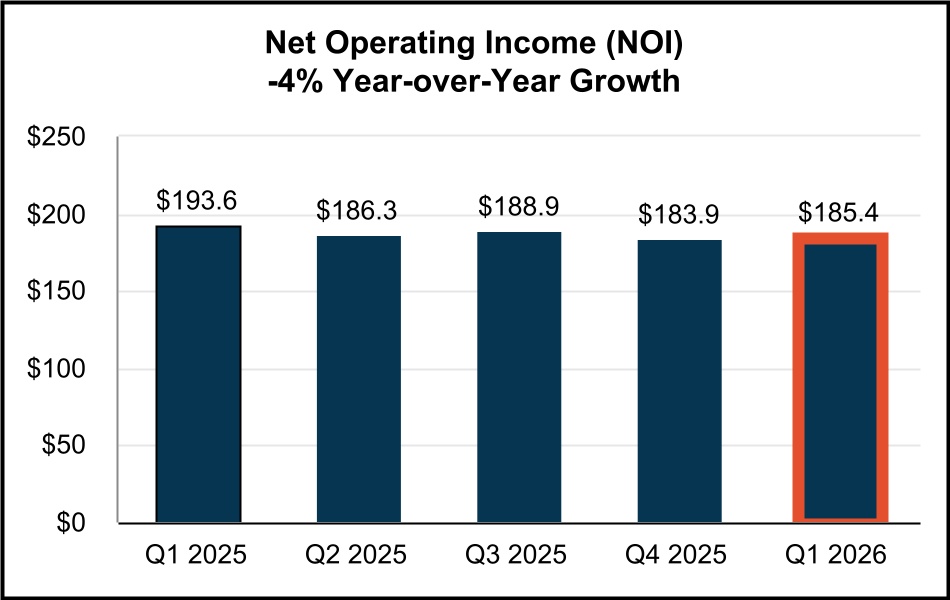

| Net Operating Income (NOI) | $ | 185,378 | $ | 183,943 | $ | 188,878 | $ | 186,270 | $ | 193,560 | |||||||||||||||||||

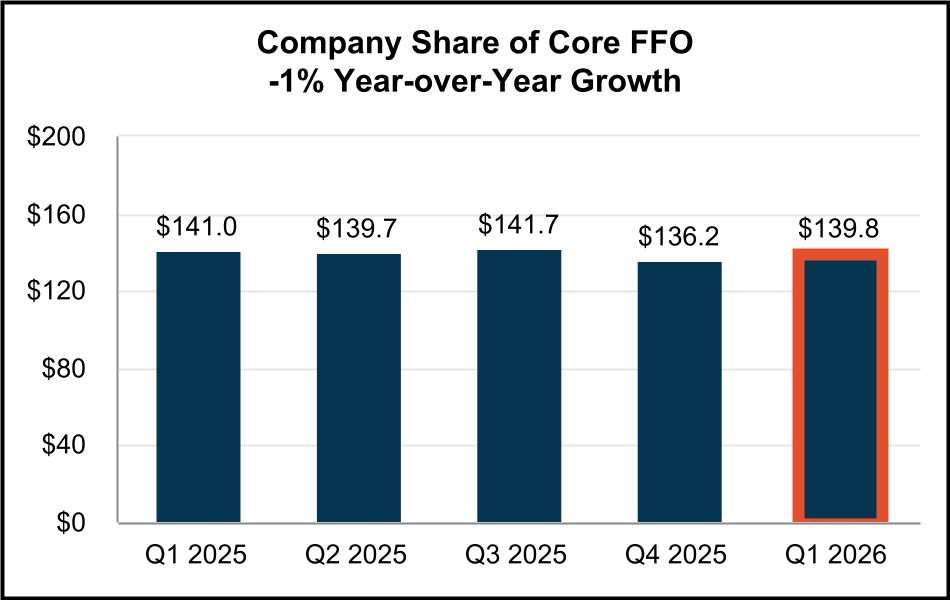

| Company share of Core FFO | $ | 139,758 | $ | 136,182 | $ | 141,700 | $ | 139,709 | $ | 141,023 | |||||||||||||||||||

| Company share of Core FFO per common share - diluted | $ | 0.61 | $ | 0.59 | $ | 0.60 | $ | 0.59 | $ | 0.62 | |||||||||||||||||||

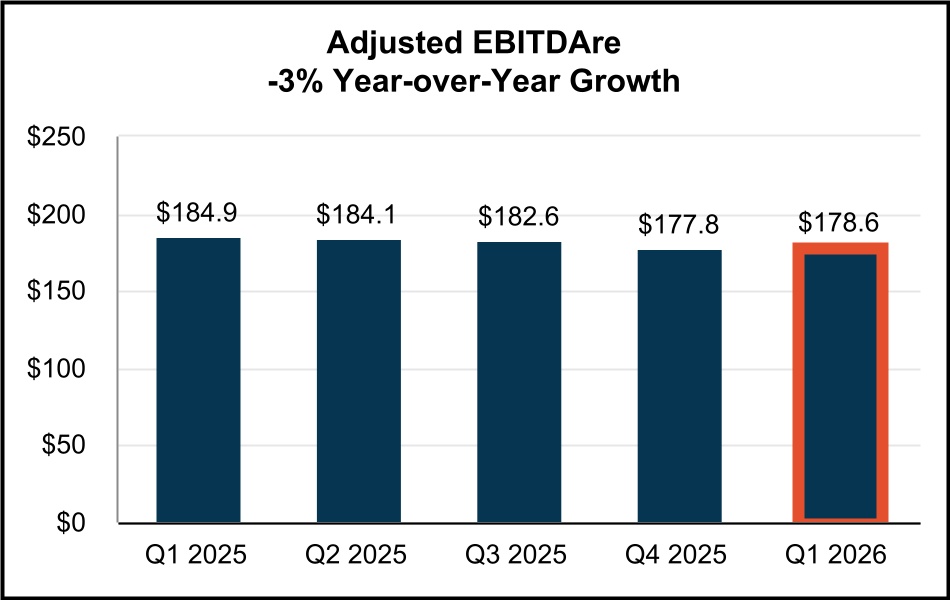

Adjusted EBITDAre | $ | 178,557 | $ | 177,808 | $ | 182,624 | $ | 184,111 | $ | 184,859 | |||||||||||||||||||

| Dividend declared per common share | $ | 0.4350 | $ | 0.4300 | $ | 0.4300 | $ | 0.4300 | $ | 0.4300 | |||||||||||||||||||

| Portfolio Statistics: | |||||||||||||||||||||||||||||

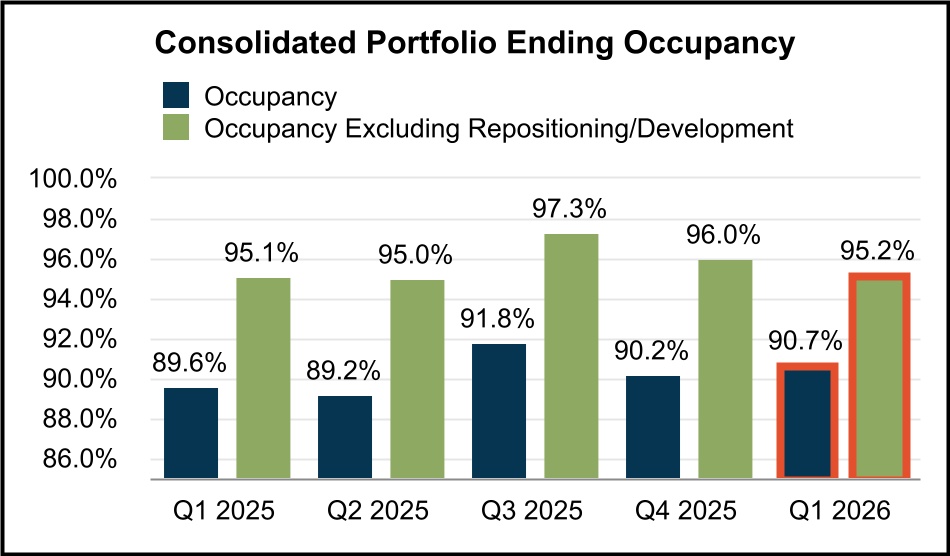

| Portfolio rentable square feet (“RSF”) | 50,445,312 | 51,161,188 | 50,850,824 | 51,021,897 | 50,952,137 | ||||||||||||||||||||||||

| Ending occupancy | 90.7% | 90.2% | 91.8% | 89.2% | 89.6% | ||||||||||||||||||||||||

| Ending occupancy excluding repositioning/development | 95.2% | 96.0% | 97.3% | 95.0% | 95.1% | ||||||||||||||||||||||||

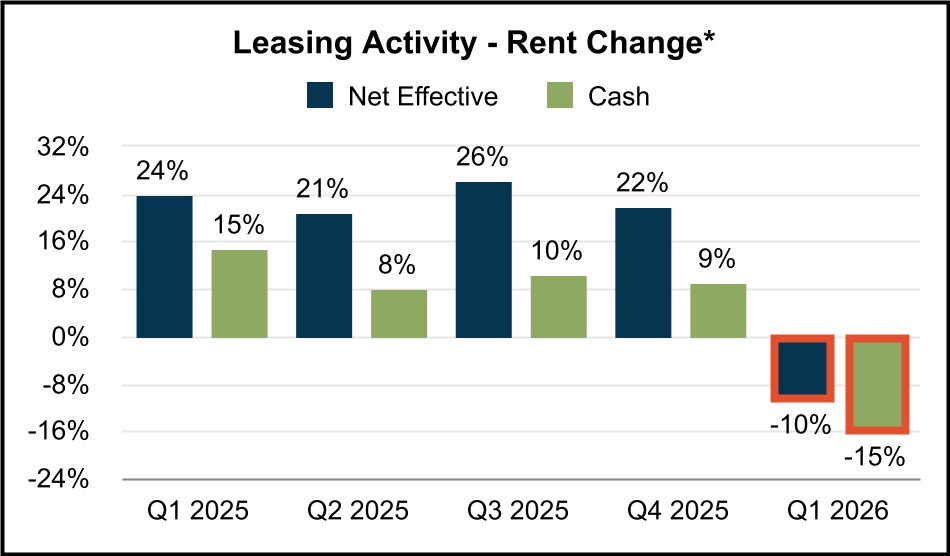

Net Effective Rent Change(2) | (10.0)% | 22.0% | 26.1% | 20.9% | 23.8% | ||||||||||||||||||||||||

Cash Rent Change(2) | (15.4)% | 9.0% | 10.3% | 8.1% | 14.7% | ||||||||||||||||||||||||

| Same Property Portfolio Performance: | |||||||||||||||||||||||||||||

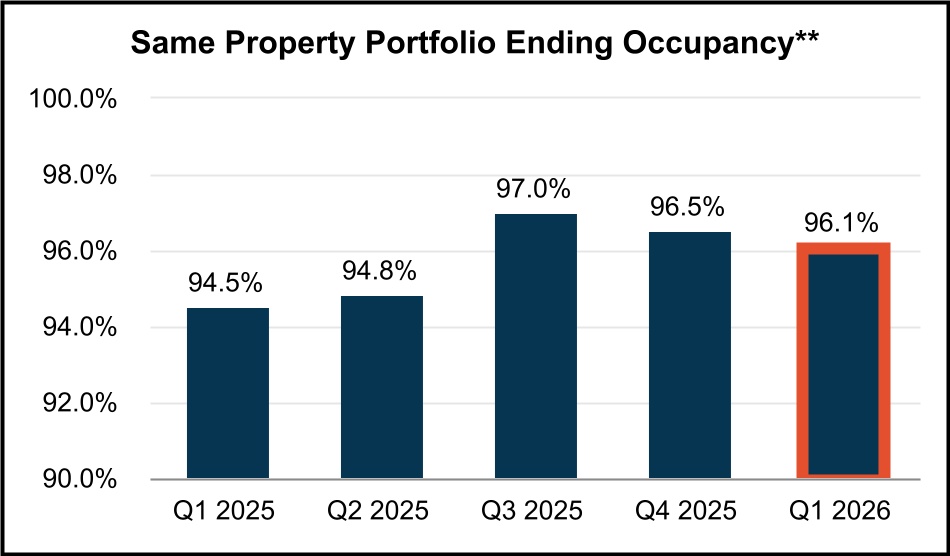

Same Property Portfolio ending occupancy(3) | 96.1% | 96.5% | 97.0% | 94.8% | 94.5% | ||||||||||||||||||||||||

Same Property Portfolio NOI growth(4) | 0.9% | ||||||||||||||||||||||||||||

Same Property Portfolio Cash NOI growth(4) | -0.4% | ||||||||||||||||||||||||||||

| Capitalization: | |||||||||||||||||||||||||||||

Total shares and units issued and outstanding at period end(5) | 233,127,293 | 238,245,286 | 240,452,878 | 244,334,274 | 244,310,773 | ||||||||||||||||||||||||

| Series B and C Preferred Stock and Series 3 CPOP Units | $ | 173,250 | $ | 173,250 | $ | 173,250 | $ | 173,250 | $ | 173,250 | |||||||||||||||||||

| Total equity market capitalization | $ | 7,803,506 | $ | 9,398,107 | $ | 10,058,268 | $ | 8,864,220 | $ | 9,738,017 | |||||||||||||||||||

| Total consolidated debt | $ | 3,271,720 | $ | 3,278,649 | $ | 3,278,896 | $ | 3,379,141 | $ | 3,379,383 | |||||||||||||||||||

| Total combined market capitalization (net debt plus equity) | $ | 11,023,512 | $ | 12,510,978 | $ | 13,088,208 | $ | 11,812,244 | $ | 12,612,821 | |||||||||||||||||||

| Ratios: | |||||||||||||||||||||||||||||

| Net debt to total combined market capitalization | 29.2% | 24.9% | 23.2% | 25.0% | 22.8% | ||||||||||||||||||||||||

Net debt to Adjusted EBITDAre (quarterly results annualized) | 4.5x | 4.4x | 4.1x | 4.0x | 3.9x | ||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 6 | | ||||||

Guidance. | ||||||||

| As of March 31, 2026 | ||||||||

Q1 2026 Updated Guidance | Initial 2026 Guidance | YTD Results as of March 31, 2026 | |||||||||||||||||||||

| Earnings | |||||||||||||||||||||||

Net Income Attributable to Common Stockholders per diluted share(1)(2) | $1.22 - $1.27 | $1.15 - $1.20 | $0.38 | ||||||||||||||||||||

Company share of Core FFO per diluted share(1)(2) | $2.37 - $2.42 | $2.35 - $2.40 | $0.61 | ||||||||||||||||||||

Same Property Portfolio(3) | |||||||||||||||||||||||

| Same Property Portfolio NOI Growth - Net Effective | (2.0)% - (1.0)% | (2.5)% - (1.5)% | 0.9% | ||||||||||||||||||||

| Same Property Portfolio NOI Growth - Cash | (1.5)% - (0.5)% | (2.0)% - (1.0)% | (0.4)% | ||||||||||||||||||||

| Average Same Property Portfolio Occupancy (Full Year) | 95.1% - 95.6% | 94.8% - 95.3% | 96.3% | ||||||||||||||||||||

| Capital Allocation | |||||||||||||||||||||||

| Dispositions | $400M - $500M | $400M - $500M | $127M | ||||||||||||||||||||

Repositioning/Development Annualized Stabilized Cash NOI(4) | $16M - $18M | $19M - $21M | $3M | ||||||||||||||||||||

| Repositioning/Development Starts (SF) | 1.2M | 1.1M | —M | ||||||||||||||||||||

| Repositioning/Development Starts (Total Estimated Project Costs) | $160M - $170M | $140M - $150M | $—M | ||||||||||||||||||||

| Other Assumptions | |||||||||||||||||||||||

| General and Administrative Expenses | +/-$60M | +/-$60M | $14.9M | ||||||||||||||||||||

| Interest Expense | +/-$112M | +/-$112M | $26.6M | ||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 7 | | ||||||

Guidance (Continued). | ||||||||

| As of March 31, 2026 | ||||||||

| Earnings Components | Range ($ per share) | Notes | ||||||||||||||||||

Initial 2026 Core FFO Per Diluted Share Guidance | $2.35 | $2.40 | ||||||||||||||||||

Same Property Portfolio NOI Growth - Net Effective | 0.01 | 0.01 | Increased 50 bps at the midpoint to (2.0)% - (1.0)%, driven by stronger 1Q leasing activity | |||||||||||||||||

Repositioning/Development NOI, Net | (0.01) | (0.01) | Projected rent commencement timing extended | |||||||||||||||||

Dispositions, Net of Capital Recycling of Proceeds | 0.02 | 0.02 | Higher than projected accretion from share repurchases | |||||||||||||||||

Net General & Administrative Expenses | — | — | Guidance unchanged at +/-$60M | |||||||||||||||||

| Net Interest Expense | — | — | Guidance unchanged at +/-$112M | |||||||||||||||||

Current 2026 Core FFO Per Diluted Share Guidance | $2.37 | $2.42 | ||||||||||||||||||

| Core FFO Per Diluted Share Annual Growth | (1.3)% | 0.8% | ||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 8 | | ||||||

Consolidated Balance Sheets. | ||||||||

| (unaudited and in thousands) | ||||||||

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||

| ASSETS | |||||||||||||||||||||||||||||

| Land | $ | 7,562,694 | $ | 7,689,921 | $ | 7,774,737 | $ | 7,787,021 | $ | 7,797,744 | |||||||||||||||||||

| Buildings and improvements | 4,821,492 | 4,677,318 | 4,607,202 | 4,594,494 | 4,573,881 | ||||||||||||||||||||||||

| Tenant improvements | 205,656 | 198,161 | 194,405 | 186,429 | 181,632 | ||||||||||||||||||||||||

| Furniture, fixtures, and equipment | 132 | 132 | 132 | 132 | 132 | ||||||||||||||||||||||||

| Construction in progress | 327,029 | 451,109 | 475,072 | 431,807 | 386,719 | ||||||||||||||||||||||||

| Total real estate held for investment | 12,917,003 | 13,016,641 | 13,051,548 | 12,999,883 | 12,940,108 | ||||||||||||||||||||||||

| Accumulated depreciation | (1,219,932) | (1,165,792) | (1,119,746) | (1,070,684) | (1,021,151) | ||||||||||||||||||||||||

| Investments in real estate, net | 11,697,071 | 11,850,849 | 11,931,802 | 11,929,199 | 11,918,957 | ||||||||||||||||||||||||

| Cash and cash equivalents | 51,714 | 165,778 | 248,956 | 431,117 | 504,579 | ||||||||||||||||||||||||

| Restricted cash | — | — | 65,464 | 130,071 | 50,105 | ||||||||||||||||||||||||

| Loan receivable, net | 123,819 | 123,704 | 123,589 | 123,474 | 123,359 | ||||||||||||||||||||||||

| Rents and other receivables, net | 11,962 | 13,958 | 15,727 | 12,861 | 17,622 | ||||||||||||||||||||||||

| Deferred rent receivable, net | 205,398 | 190,376 | 181,439 | 173,691 | 166,893 | ||||||||||||||||||||||||

| Deferred leasing costs, net | 92,022 | 87,745 | 82,227 | 71,482 | 70,404 | ||||||||||||||||||||||||

| Deferred loan costs, net | 6,382 | 6,886 | 7,391 | 7,892 | 1,642 | ||||||||||||||||||||||||

Acquired lease intangible assets, net(1) | 130,045 | 140,627 | 154,931 | 169,036 | 182,444 | ||||||||||||||||||||||||

Acquired indefinite-lived intangible asset | 5,156 | 5,156 | 5,156 | 5,156 | 5,156 | ||||||||||||||||||||||||

Interest rate swap assets | 4,562 | 2,025 | 2,804 | 3,586 | 5,580 | ||||||||||||||||||||||||

| Other assets | 20,500 | 25,609 | 31,522 | 15,765 | 20,730 | ||||||||||||||||||||||||

Assets associated with real estate held for sale, net(2) | 48,761 | — | — | 6,282 | 18,386 | ||||||||||||||||||||||||

| Total Assets | $ | 12,397,392 | $ | 12,612,713 | $ | 12,851,008 | $ | 13,079,612 | $ | 13,085,857 | |||||||||||||||||||

| LIABILITIES & EQUITY | |||||||||||||||||||||||||||||

| Liabilities | |||||||||||||||||||||||||||||

| Notes payable | $ | 3,247,451 | $ | 3,251,909 | $ | 3,249,733 | $ | 3,347,575 | $ | 3,348,060 | |||||||||||||||||||

| Interest rate swap liability | 9 | 829 | 1,626 | 667 | — | ||||||||||||||||||||||||

| Accounts payable, accrued expenses and other liabilities | 125,007 | 120,849 | 153,558 | 124,814 | 141,999 | ||||||||||||||||||||||||

| Dividends and distributions payable | 102,418 | 103,399 | 103,913 | 105,594 | 105,285 | ||||||||||||||||||||||||

Acquired lease intangible liabilities, net(3) | 110,914 | 116,487 | 122,870 | 129,683 | 136,661 | ||||||||||||||||||||||||

| Tenant security deposits | 95,219 | 92,444 | 91,835 | 90,757 | 90,050 | ||||||||||||||||||||||||

Tenant prepaid rents | 82,186 | 88,777 | 85,114 | 85,494 | 88,822 | ||||||||||||||||||||||||

Liabilities associated with real estate held for sale(2) | 482 | — | — | 4 | 234 | ||||||||||||||||||||||||

| Total Liabilities | 3,763,686 | 3,774,694 | 3,808,649 | 3,884,588 | 3,911,111 | ||||||||||||||||||||||||

| Equity | |||||||||||||||||||||||||||||

| Series B preferred stock, net ($75,000 liquidation preference) | 72,443 | 72,443 | 72,443 | 72,443 | 72,443 | ||||||||||||||||||||||||

| Series C preferred stock, net ($86,250 liquidation preference) | 83,233 | 83,233 | 83,233 | 83,233 | 83,233 | ||||||||||||||||||||||||

| Preferred stock | 155,676 | 155,676 | 155,676 | 155,676 | 155,676 | ||||||||||||||||||||||||

| Common stock | 2,263 | 2,316 | 2,328 | 2,367 | 2,362 | ||||||||||||||||||||||||

| Additional paid in capital | 8,745,875 | 8,945,123 | 8,993,439 | 9,140,264 | 9,116,069 | ||||||||||||||||||||||||

| Cumulative distributions in excess of earnings | (651,692) | (642,130) | (474,813) | (462,309) | (474,550) | ||||||||||||||||||||||||

| Accumulated other comprehensive income (loss) | 2,887 | (422) | (515) | 1,092 | 3,582 | ||||||||||||||||||||||||

| Total stockholders’ equity | 8,255,009 | 8,460,563 | 8,676,115 | 8,837,090 | 8,803,139 | ||||||||||||||||||||||||

| Noncontrolling interests | 378,697 | 377,456 | 366,244 | 357,934 | 371,607 | ||||||||||||||||||||||||

| Total Equity | 8,633,706 | 8,838,019 | 9,042,359 | 9,195,024 | 9,174,746 | ||||||||||||||||||||||||

| Total Liabilities and Equity | $ | 12,397,392 | $ | 12,612,713 | $ | 12,851,008 | $ | 13,079,612 | $ | 13,085,857 | |||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 9 | | ||||||

Consolidated Statements of Operations. | ||||||||

| Quarterly Results | (unaudited and in thousands, except share and per share data) | |||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

| Revenues | |||||||||||||||||||||||||||||

Rental income(1) | $ | 242,141 | $ | 243,230 | $ | 246,757 | $ | 241,568 | $ | 248,821 | |||||||||||||||||||

| Management and leasing services | — | 197 | 118 | 132 | 142 | ||||||||||||||||||||||||

| Interest income | 2,937 | 4,670 | 6,367 | 7,807 | 3,324 | ||||||||||||||||||||||||

| Total Revenues | 245,078 | 248,097 | 253,242 | 249,507 | 252,287 | ||||||||||||||||||||||||

| Operating Expenses | |||||||||||||||||||||||||||||

| Property expenses | 56,763 | 59,287 | 57,879 | 55,298 | 55,261 | ||||||||||||||||||||||||

| General and administrative | 14,925 | 19,199 | 20,037 | 19,752 | 19,868 | ||||||||||||||||||||||||

| Depreciation and amortization | 72,933 | 76,819 | 81,172 | 71,188 | 86,740 | ||||||||||||||||||||||||

| Total Operating Expenses | 144,621 | 155,305 | 159,088 | 146,238 | 161,869 | ||||||||||||||||||||||||

| Other (Expenses) Income | |||||||||||||||||||||||||||||

Other income | 1,350 | — | — | — | — | ||||||||||||||||||||||||

| Other expenses | (102) | (65,910) | (4,218) | (244) | (2,239) | ||||||||||||||||||||||||

| Interest expense | (26,600) | (25,451) | (25,463) | (26,701) | (27,288) | ||||||||||||||||||||||||

| Impairment of real estate | (6,824) | (89,097) | — | — | — | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | — | — | — | (291) | — | ||||||||||||||||||||||||

| Gains on sale of real estate | 26,281 | 19,931 | 28,583 | 44,361 | 13,157 | ||||||||||||||||||||||||

| Total Other (Expenses) Income | (5,895) | (160,527) | (1,098) | 17,125 | (16,370) | ||||||||||||||||||||||||

| Net Income (Loss) | 94,562 | (67,735) | 93,056 | 120,394 | 74,048 | ||||||||||||||||||||||||

| Less: net (income) loss attributable to noncontrolling interests | (3,375) | 2,312 | (3,137) | (4,060) | (2,849) | ||||||||||||||||||||||||

| Net income (loss) attributable to Rexford Industrial Realty, Inc. | 91,187 | (65,423) | 89,919 | 116,334 | 71,199 | ||||||||||||||||||||||||

| Less: preferred stock dividends | (2,314) | (2,315) | (2,314) | (2,315) | (2,314) | ||||||||||||||||||||||||

| Less: earnings allocated to participating securities | (1,008) | (952) | (519) | (592) | (539) | ||||||||||||||||||||||||

| Net income (loss) attributable to common stockholders | $ | 87,865 | $ | (68,690) | $ | 87,086 | $ | 113,427 | $ | 68,346 | |||||||||||||||||||

| Earnings per Common Share | |||||||||||||||||||||||||||||

| Net income (loss) attributable to common stockholders per share - basic | $ | 0.38 | $ | (0.30) | $ | 0.37 | $ | 0.48 | $ | 0.30 | |||||||||||||||||||

| Net income (loss) attributable to common stockholders per share - diluted | $ | 0.38 | $ | (0.30) | $ | 0.37 | $ | 0.48 | $ | 0.30 | |||||||||||||||||||

| Weighted average shares outstanding - basic | 228,312,419 | 231,758,110 | 234,586,980 | 236,098,831 | 227,395,984 | ||||||||||||||||||||||||

| Weighted average shares outstanding - diluted | 228,312,419 | 232,050,966 | 234,586,980 | 236,098,831 | 227,395,984 | ||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 10 | | ||||||

Consolidated Statements of Operations. | ||||||||

| Quarterly Results (continued) | (unaudited and in thousands, except share and per share data) | |||||||

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Revenues | |||||||||||

| Rental income | $ | 242,141 | $ | 248,821 | |||||||

| Management and leasing services | — | 142 | |||||||||

| Interest income | 2,937 | 3,324 | |||||||||

| Total Revenues | 245,078 | 252,287 | |||||||||

| Operating Expenses | |||||||||||

| Property expenses | 56,763 | 55,261 | |||||||||

| General and administrative | 14,925 | 19,868 | |||||||||

| Depreciation and amortization | 72,933 | 86,740 | |||||||||

| Total Operating Expenses | 144,621 | 161,869 | |||||||||

| Other (Expenses) Income | |||||||||||

| Other income | 1,350 | — | |||||||||

| Other expenses | (102) | (2,239) | |||||||||

| Interest expense | (26,600) | (27,288) | |||||||||

Impairment of real estate | (6,824) | — | |||||||||

| Gains on sale of real estate | 26,281 | 13,157 | |||||||||

| Total Other (Expenses) Income | (5,895) | (16,370) | |||||||||

| Net Income | 94,562 | 74,048 | |||||||||

| Less: net income attributable to noncontrolling interests | (3,375) | (2,849) | |||||||||

| Net income attributable to Rexford Industrial Realty, Inc. | 91,187 | 71,199 | |||||||||

| Less: preferred stock dividends | (2,314) | (2,314) | |||||||||

| Less: earnings allocated to participating securities | (1,008) | (539) | |||||||||

| Net income attributable to common stockholders | $ | 87,865 | $ | 68,346 | |||||||

| Net income attributable to common stockholders per share – basic | $ | 0.38 | $ | 0.30 | |||||||

| Net income attributable to common stockholders per share – diluted | $ | 0.38 | $ | 0.30 | |||||||

| Weighted-average shares of common stock outstanding – basic | 228,312,419 | 227,395,984 | |||||||||

| Weighted-average shares of common stock outstanding – diluted | 228,312,419 | 227,395,984 | |||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 11 | | ||||||

Non-GAAP FFO and Core FFO Reconciliations.(1) | ||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||

Net Income (Loss) | $ | 94,562 | $ | (67,735) | $ | 93,056 | $ | 120,394 | $ | 74,048 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Depreciation and amortization | 72,933 | 76,819 | 81,172 | 71,188 | 86,740 | ||||||||||||||||||||||||

Impairment of real estate(2) | 6,824 | 89,097 | — | — | — | ||||||||||||||||||||||||

| Gains on sale of real estate | (26,281) | (19,931) | (28,583) | (44,361) | (13,157) | ||||||||||||||||||||||||

NAREIT Defined Funds From Operations (FFO) | 148,038 | 78,250 | 145,645 | 147,221 | 147,631 | ||||||||||||||||||||||||

| Less: preferred stock dividends | (2,314) | (2,315) | (2,314) | (2,315) | (2,314) | ||||||||||||||||||||||||

Less: FFO attributable to noncontrolling interests(3) | (5,282) | (2,688) | (4,906) | (4,962) | (5,394) | ||||||||||||||||||||||||

Less: FFO attributable to participating securities(4) | (1,434) | (953) | (713) | (728) | (750) | ||||||||||||||||||||||||

| Company share of FFO | $ | 139,008 | $ | 72,294 | $ | 137,712 | $ | 139,216 | $ | 139,173 | |||||||||||||||||||

| Company share of FFO per common share‐basic | $ | 0.61 | $ | 0.31 | $ | 0.59 | $ | 0.59 | $ | 0.61 | |||||||||||||||||||

| Company share of FFO per common share‐diluted | $ | 0.61 | $ | 0.31 | $ | 0.59 | $ | 0.59 | $ | 0.61 | |||||||||||||||||||

| FFO | $ | 148,038 | $ | 78,250 | $ | 145,645 | $ | 147,221 | $ | 147,631 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

Acquisition expenses(5) | — | 10 | 161 | 23 | 79 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | — | — | — | 291 | — | ||||||||||||||||||||||||

Non-capitalizable demolition costs(5) | — | — | — | — | 365 | ||||||||||||||||||||||||

Co-CEO transition costs(5)(6) | — | 60,223 | — | — | — | ||||||||||||||||||||||||

Severance costs(5)(7) | — | — | 2,728 | 199 | 1,483 | ||||||||||||||||||||||||

Other nonrecurring expenses(5)(8) | 62 | 5,605 | 1,259 | — | — | ||||||||||||||||||||||||

| Core FFO | 148,100 | 144,088 | 149,793 | 147,734 | 149,558 | ||||||||||||||||||||||||

| Less: preferred stock dividends | (2,314) | (2,315) | (2,314) | (2,315) | (2,314) | ||||||||||||||||||||||||

Less: Core FFO attributable to noncontrolling interests(3) | (5,284) | (4,943) | (5,045) | (4,979) | (5,461) | ||||||||||||||||||||||||

Less: Core FFO attributable to participating securities(4)(9) | (744) | (648) | (734) | (731) | (760) | ||||||||||||||||||||||||

| Company share of Core FFO | $ | 139,758 | $ | 136,182 | $ | 141,700 | $ | 139,709 | $ | 141,023 | |||||||||||||||||||

| Company share of Core FFO per common share‐basic | $ | 0.61 | $ | 0.59 | $ | 0.60 | $ | 0.59 | $ | 0.62 | |||||||||||||||||||

| Company share of Core FFO per common share‐diluted | $ | 0.61 | $ | 0.59 | $ | 0.60 | $ | 0.59 | $ | 0.62 | |||||||||||||||||||

| Weighted-average shares outstanding-basic | 228,312,419 | 231,758,110 | 234,586,980 | 236,098,831 | 227,395,984 | ||||||||||||||||||||||||

Weighted-average shares outstanding-diluted | 228,312,419 | 232,050,966 | 234,586,980 | 236,098,831 | 227,395,984 | ||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 12 | | ||||||

Non-GAAP FFO and Core FFO Reconciliations.(1) | ||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

Net Income | $ | 94,562 | $ | 74,048 | |||||||

| Adjustments: | |||||||||||

| Depreciation and amortization | 72,933 | 86,740 | |||||||||

Impairment of real estate(2) | 6,824 | — | |||||||||

| Gains on sale of real estate | (26,281) | (13,157) | |||||||||

| Funds From Operations (FFO) | 148,038 | 147,631 | |||||||||

| Less: preferred stock dividends | (2,314) | (2,314) | |||||||||

| Less: FFO attributable to noncontrolling interests | (5,282) | (5,394) | |||||||||

| Less: FFO attributable to participating securities | (1,434) | (750) | |||||||||

| Company share of FFO | $ | 139,008 | $ | 139,173 | |||||||

| Company share of FFO per common share‐basic | $ | 0.61 | $ | 0.61 | |||||||

| Company share of FFO per common share‐diluted | $ | 0.61 | $ | 0.61 | |||||||

| FFO | $ | 148,038 | $ | 147,631 | |||||||

| Adjustments: | |||||||||||

Acquisition expenses(3) | — | 79 | |||||||||

Non-capitalizable demolition costs(3) | — | 365 | |||||||||

Severance costs(3)(4) | — | 1,483 | |||||||||

Other nonrecurring expenses(3)(5) | 62 | — | |||||||||

| Core FFO | 148,100 | 149,558 | |||||||||

| Less: preferred stock dividends | (2,314) | (2,314) | |||||||||

| Less: Core FFO attributable to noncontrolling interests | (5,284) | (5,461) | |||||||||

| Less: Core FFO attributable to participating securities | (744) | (760) | |||||||||

| Company share of Core FFO | $ | 139,758 | $ | 141,023 | |||||||

| Company share of Core FFO per common share‐basic | $ | 0.61 | $ | 0.62 | |||||||

| Company share of Core FFO per common share‐diluted | $ | 0.61 | $ | 0.62 | |||||||

| Weighted-average shares outstanding-basic | 228,312,419 | 227,395,984 | |||||||||

| Weighted-average shares outstanding-diluted | 228,312,419 | 227,395,984 | |||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 13 | | ||||||

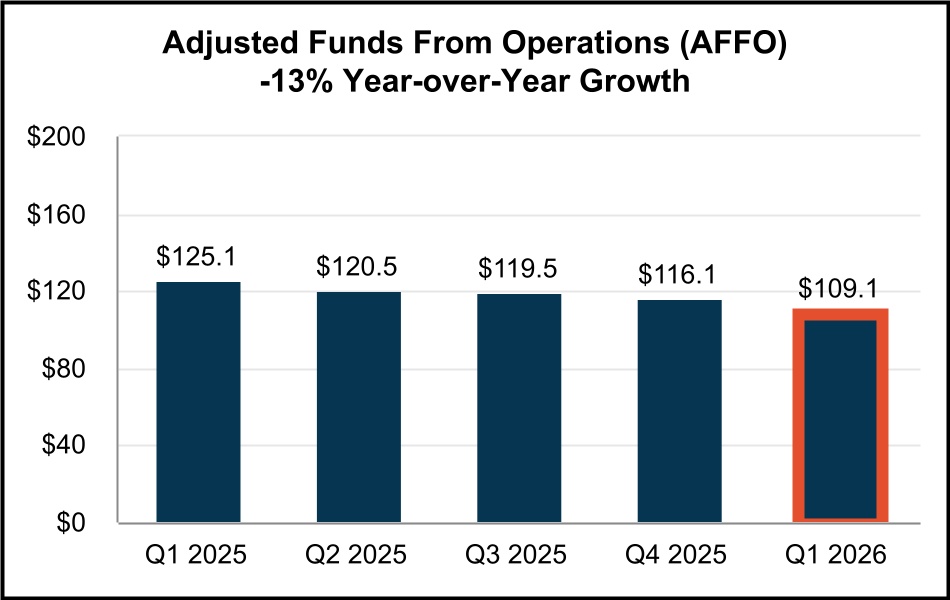

Non-GAAP AFFO Reconciliation.(1) | ||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||

Funds From Operations(2) | $ | 148,038 | $ | 78,250 | $ | 145,645 | $ | 147,221 | $ | 147,631 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Amortization of deferred financing costs | 1,334 | 1,333 | 1,340 | 1,255 | 1,134 | ||||||||||||||||||||||||

| Non-cash stock compensation | 4,063 | 8,537 | 10,485 | 10,091 | 9,699 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | — | — | — | 291 | — | ||||||||||||||||||||||||

| Amortization related to termination/settlement of interest rate derivatives | 77 | 78 | 78 | 76 | 77 | ||||||||||||||||||||||||

| Note payable (discount) premium amortization, net | 1,641 | 1,616 | 1,597 | 1,579 | 1,560 | ||||||||||||||||||||||||

| Non-capitalizable demolition costs | — | — | — | — | 365 | ||||||||||||||||||||||||

Co-CEO transition costs | — | 60,223 | — | — | — | ||||||||||||||||||||||||

| Severance costs | — | — | 2,728 | 199 | 1,483 | ||||||||||||||||||||||||

Other nonrecurring expenses | 62 | 5,605 | 1,259 | — | — | ||||||||||||||||||||||||

| Deduct: | |||||||||||||||||||||||||||||

| Preferred stock dividends | (2,314) | (2,315) | (2,314) | (2,315) | (2,314) | ||||||||||||||||||||||||

Straight line rental revenue adjustment(3) | (15,136) | (9,073) | (8,164) | (6,918) | (5,517) | ||||||||||||||||||||||||

| Above/(below) market lease revenue adjustments | (4,647) | (4,129) | (5,254) | (5,788) | (9,186) | ||||||||||||||||||||||||

Capitalized payments(4) | (13,203) | (14,814) | (15,756) | (14,368) | (13,321) | ||||||||||||||||||||||||

| Accretion of net loan origination fees | (115) | (115) | (115) | (115) | (115) | ||||||||||||||||||||||||

Recurring capital expenditures(5) | (2,314) | (2,566) | (3,563) | (5,887) | (1,311) | ||||||||||||||||||||||||

2nd generation tenant improvements(6) | (185) | (179) | (460) | (663) | (162) | ||||||||||||||||||||||||

2nd generation leasing commissions(7) | (8,193) | (6,324) | (8,007) | (4,162) | (4,879) | ||||||||||||||||||||||||

| Adjusted Funds From Operations (AFFO) | $ | 109,108 | $ | 116,127 | $ | 119,499 | $ | 120,496 | $ | 125,144 | |||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 14 | | ||||||

Statement of Operations Reconciliations - NOI, Cash NOI, EBITDAre and Adjusted EBITDAre.(1) | ||||||||

| (unaudited and in thousands) | ||||||||

| NOI and Cash NOI | |||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

Rental income(2)(3)(4) | $ | 242,141 | $ | 243,230 | $ | 246,757 | $ | 241,568 | $ | 248,821 | |||||||||||||||||||

| Less: Property expenses | 56,763 | 59,287 | 57,879 | 55,298 | 55,261 | ||||||||||||||||||||||||

| Net Operating Income (NOI) | $ | 185,378 | $ | 183,943 | $ | 188,878 | $ | 186,270 | $ | 193,560 | |||||||||||||||||||

Above/(below) market lease revenue adjustments | (4,647) | (4,129) | (5,254) | (5,788) | (9,186) | ||||||||||||||||||||||||

| Straight line rental revenue adjustment | (15,136) | (9,073) | (8,164) | (6,918) | (5,517) | ||||||||||||||||||||||||

| Cash NOI | $ | 165,595 | $ | 170,741 | $ | 175,460 | $ | 173,564 | $ | 178,857 | |||||||||||||||||||

EBITDAre and Adjusted EBITDAre | |||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

Net income (loss) | $ | 94,562 | $ | (67,735) | $ | 93,056 | $ | 120,394 | $ | 74,048 | |||||||||||||||||||

| Interest expense | 26,600 | 25,451 | 25,463 | 26,701 | 27,288 | ||||||||||||||||||||||||

| Depreciation and amortization | 72,933 | 76,819 | 81,172 | 71,188 | 86,740 | ||||||||||||||||||||||||

Impairment of real estate | 6,824 | 89,097 | — | — | — | ||||||||||||||||||||||||

| Gains on sale of real estate | (26,281) | (19,931) | (28,583) | (44,361) | (13,157) | ||||||||||||||||||||||||

EBITDAre | $ | 174,638 | $ | 103,701 | $ | 171,108 | $ | 173,922 | $ | 174,919 | |||||||||||||||||||

| Stock-based compensation amortization | 4,063 | 8,537 | 10,485 | 10,091 | 9,699 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | — | — | — | 291 | — | ||||||||||||||||||||||||

| Acquisition expenses | — | 10 | 161 | 23 | 79 | ||||||||||||||||||||||||

Co-CEO transition costs | — | 60,223 | — | — | — | ||||||||||||||||||||||||

Other nonrecurring expenses | 62 | 5,605 | 1,259 | — | — | ||||||||||||||||||||||||

Pro forma effect of dispositions(5) | (206) | (268) | (389) | (216) | 162 | ||||||||||||||||||||||||

Adjusted EBITDAre | $ | 178,557 | $ | 177,808 | $ | 182,624 | $ | 184,111 | $ | 184,859 | |||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 15 | | ||||||

Same Property Portfolio Performance.(1) | ||||||||

| (unaudited and dollars in thousands) | ||||||||

| Same Property Portfolio: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of properties | 342 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Square Feet | 41,727,325 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Same Property Portfolio NOI and Cash NOI: | ||||||||||||||||||||||||||

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| 2026 | 2025 | $ Change | % Change | |||||||||||||||||||||||

Rental income(2)(3)(4) | $ | 211,391 | $ | 207,919 | $ | 3,472 | 1.7% | |||||||||||||||||||

| Property expenses | 47,304 | 45,350 | 1,954 | 4.3% | ||||||||||||||||||||||

| Same Property Portfolio NOI | $ | 164,087 | $ | 162,569 | $ | 1,518 | 0.9% | (4) | ||||||||||||||||||

Straight-line rental revenue adjustment | (9,971) | (7,454) | (2,517) | 33.8% | ||||||||||||||||||||||

Above/(below) market lease revenue adjustments | (4,171) | (4,572) | 401 | (8.8)% | ||||||||||||||||||||||

| Same Property Portfolio Cash NOI | $ | 149,945 | $ | 150,543 | $ | (598) | (0.4)% | (4) | ||||||||||||||||||

| Same Property Portfolio Occupancy: | |||||||||||||||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||||||||||||||

| 2026 | 2025 | Year-over-Year Change (basis points) | Three Months Ended December 31, 2025(5) | Sequential Change (basis points) | |||||||||||||||||||||||||

Quarterly Weighted Average Occupancy:(5) | |||||||||||||||||||||||||||||

| Los Angeles County | 96.9% | 93.2% | 370 bps | 96.7% | 20 bps | ||||||||||||||||||||||||

| Orange County | 96.4% | 97.4% | (100) bps | 98.0% | (160) bps | ||||||||||||||||||||||||

| Riverside / San Bernardino County | 95.1% | 97.3% | (220) bps | 96.7% | (160) bps | ||||||||||||||||||||||||

| San Diego County | 97.7% | 97.9% | (20) bps | 98.1% | (40) bps | ||||||||||||||||||||||||

| Ventura County | 94.6% | 91.3% | 330 bps | 94.6% | — bps | ||||||||||||||||||||||||

| Quarterly Weighted Average Occupancy | 96.3% | 94.7% | 160 bps | 96.8% | (50) bps | ||||||||||||||||||||||||

| Ending Occupancy: | 96.1% | 94.5% | 160 bps | 96.5% | (40) bps | ||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 16 | | ||||||

Capitalization Summary. | ||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Capitalization as of March 31, 2026 | ||||||||

| Description | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

Common shares outstanding(1) | 224,521,552 | 229,957,058 | 232,297,172 | 236,151,829 | 235,610,472 | ||||||||||||||||||||||||

Operating partnership units outstanding(2) | 8,605,741 | 8,288,228 | 8,155,706 | 8,182,445 | 8,700,301 | ||||||||||||||||||||||||

| Total shares and units outstanding at period end | 233,127,293 | 238,245,286 | 240,452,878 | 244,334,274 | 244,310,773 | ||||||||||||||||||||||||

| Share price at end of quarter | $ | 32.73 | $ | 38.72 | $ | 41.11 | $ | 35.57 | $ | 39.15 | |||||||||||||||||||

| Common Stock and Operating Partnership Units - Capitalization | $ | 7,630,256 | $ | 9,224,857 | $ | 9,885,018 | $ | 8,690,970 | $ | 9,564,767 | |||||||||||||||||||

Series B and C Cumulative Redeemable Preferred Stock(3) | $ | 161,250 | $ | 161,250 | $ | 161,250 | $ | 161,250 | $ | 161,250 | |||||||||||||||||||

3.00% Series 3 Cumulative Redeemable Convertible Preferred Units(4) | 12,000 | 12,000 | 12,000 | 12,000 | 12,000 | ||||||||||||||||||||||||

| Preferred Equity | $ | 173,250 | $ | 173,250 | $ | 173,250 | $ | 173,250 | $ | 173,250 | |||||||||||||||||||

| Total Equity Market Capitalization | $ | 7,803,506 | $ | 9,398,107 | $ | 10,058,268 | $ | 8,864,220 | $ | 9,738,017 | |||||||||||||||||||

| Total Debt | $ | 3,271,720 | $ | 3,278,649 | $ | 3,278,896 | $ | 3,379,141 | $ | 3,379,383 | |||||||||||||||||||

| Less: Cash and cash equivalents | (51,714) | (165,778) | (248,956) | (431,117) | (504,579) | ||||||||||||||||||||||||

| Net Debt | $ | 3,220,006 | $ | 3,112,871 | $ | 3,029,940 | $ | 2,948,024 | $ | 2,874,804 | |||||||||||||||||||

| Total Combined Market Capitalization (Net Debt plus Equity) | $ | 11,023,512 | $ | 12,510,978 | $ | 13,088,208 | $ | 11,812,244 | $ | 12,612,821 | |||||||||||||||||||

| Net debt to total combined market capitalization | 29.2 | % | 24.9 | % | 23.2 | % | 25.0 | % | 22.8 | % | |||||||||||||||||||

Net debt to Adjusted EBITDAre (quarterly results annualized)(5) | 4.5x | 4.4x | 4.1x | 4.0x | 3.9x | ||||||||||||||||||||||||

Net debt & preferred equity to Adjusted EBITDAre (quarterly results annualized)(5) | 4.8x | 4.6x | 4.4x | 4.2x | 4.1x | ||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 17 | | ||||||

Debt Summary. | ||||||||

| (unaudited and dollars in thousands) | ||||||||

| Debt Detail: | ||||||||||||||||||||||||||

| As of March 31, 2026 | ||||||||||||||||||||||||||

| Debt Description | Maturity Date | Stated Interest Rate | Effective Interest Rate(1) | Principal Balance(2) | ||||||||||||||||||||||

| Unsecured Debt: | ||||||||||||||||||||||||||

$1.25 Billion Revolving Credit Facility(3) | 5/30/2029(4) | SOFR+0.685%(5) | 4.365% | $ | — | |||||||||||||||||||||

$575M Exchangeable 2027 Senior Notes(6) | 3/15/2027 | 4.375% | 4.375% | 575,000 | ||||||||||||||||||||||

| $300M Term Loan Facility | 5/26/2027 | SOFR+0.76%(5) | 3.577%(7) | 300,000 | ||||||||||||||||||||||

| $125M Senior Notes | 7/13/2027 | 3.930% | 3.930% | 125,000 | ||||||||||||||||||||||

| $300M Senior Notes | 6/15/2028 | 5.000% | 5.000% | 300,000 | ||||||||||||||||||||||

$575M Exchangeable 2029 Senior Notes(6) | 3/15/2029 | 4.125% | 4.125% | 575,000 | ||||||||||||||||||||||

| $25M Series 2019A Senior Notes | 7/16/2029 | 3.880% | 3.880% | 25,000 | ||||||||||||||||||||||

| $400M Senior Notes | 12/1/2030 | 2.125% | 2.125% | 400,000 | ||||||||||||||||||||||

| $400M Term Loan Facility | 5/30/2030 | SOFR+0.76%(5) | 4.174%(8) | 400,000 | ||||||||||||||||||||||

| $400M Senior Notes - Green Bond | 9/1/2031 | 2.150% | 2.150% | 400,000 | ||||||||||||||||||||||

| $75M Series 2019B Senior Notes | 7/16/2034 | 4.030% | 4.030% | 75,000 | ||||||||||||||||||||||

| Secured Debt: | ||||||||||||||||||||||||||

| $60M Term Loan Facility | 10/27/2026(9) | SOFR+1.250%(9) | 5.060%(10) | 60,000 | ||||||||||||||||||||||

| 13943-13955 Balboa Boulevard | 7/1/2027 | 3.930% | 3.930% | 13,712 | ||||||||||||||||||||||

| 2205 126th Street | 12/1/2027 | 3.910% | 3.910% | 5,200 | ||||||||||||||||||||||

| 2410-2420 Santa Fe Avenue | 1/1/2028 | 3.700% | 3.700% | 10,300 | ||||||||||||||||||||||

| 11832-11954 La Cienega Boulevard | 7/1/2028 | 4.260% | 4.260% | 3,667 | ||||||||||||||||||||||

| 1100-1170 Gilbert Street (Gilbert/La Palma) | 3/1/2031 | 5.125% | 5.125% | 1,268 | ||||||||||||||||||||||

| 7817 Woodley Avenue | 8/1/2039 | 4.140% | 4.140% | 2,573 | ||||||||||||||||||||||

| Total Debt | 3.723% | $ | 3,271,720 | |||||||||||||||||||||||

Debt Composition: | ||||||||||||||||||||||||||||||||

| Category | Weighted Average Term Remaining (yrs) | Stated Interest Rate | Effective Interest Rate | Balance | % of Total | |||||||||||||||||||||||||||

| Fixed | 3.0 | 3.723% (See Table Above) | 3.723% | $ | 3,271,720 | 100% | ||||||||||||||||||||||||||

| Variable | — | — | —% | $ | — | 0% | ||||||||||||||||||||||||||

| Secured | 1.3 | 4.639% | $ | 96,720 | 3% | |||||||||||||||||||||||||||

| Unsecured | 3.1 | 3.695% | $ | 3,175,000 | 97% | |||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 18 | | ||||||

Debt Summary (Continued). | ||||||||

| (unaudited and dollars in thousands) | ||||||||

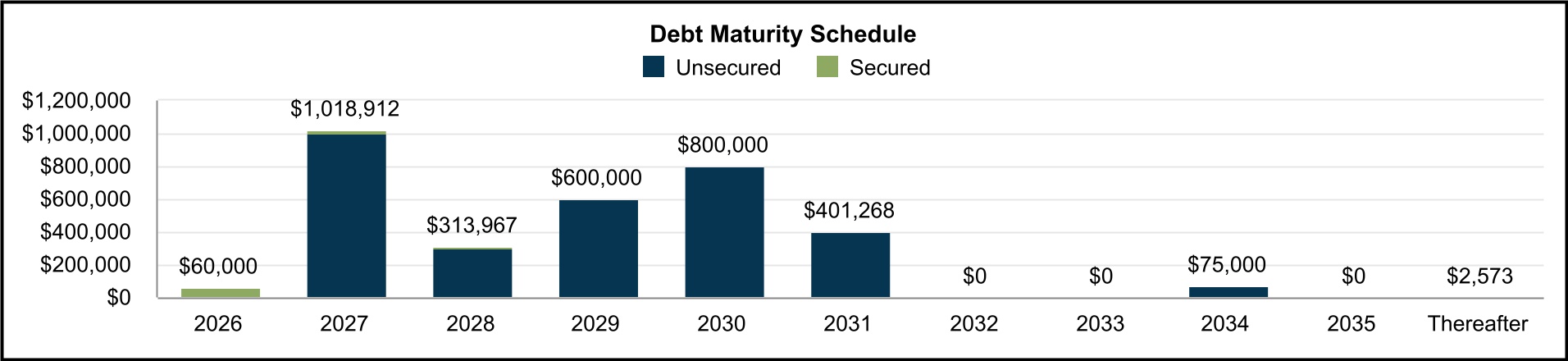

Debt Maturity Schedule(11): | ||||||||||||||||||||||||||||||||

| Year | Secured | Unsecured | Total | % Total | Effective Interest Rate(1) | |||||||||||||||||||||||||||

| 2026 | $ | 60,000 | $ | — | $ | 60,000 | 2 | % | 5.060 | % | ||||||||||||||||||||||

| 2027 | 18,912 | 1,000,000 | 1,018,912 | 31 | % | 4.077 | % | |||||||||||||||||||||||||

| 2028 | 13,967 | 300,000 | 313,967 | 10 | % | 4.949 | % | |||||||||||||||||||||||||

| 2029 | — | 600,000 | 600,000 | 18 | % | 4.115 | % | |||||||||||||||||||||||||

| 2030 | — | 800,000 | 800,000 | 25 | % | 3.149 | % | |||||||||||||||||||||||||

| 2031 | 1,268 | 400,000 | 401,268 | 12 | % | 2.159 | % | |||||||||||||||||||||||||

| 2032 | — | — | — | — | % | — | % | |||||||||||||||||||||||||

| 2033 | — | — | — | — | % | — | % | |||||||||||||||||||||||||

| 2034 | — | 75,000 | 75,000 | 2 | % | 4.030 | % | |||||||||||||||||||||||||

| 2035 | — | — | — | — | % | — | % | |||||||||||||||||||||||||

| Thereafter | 2,573 | — | 2,573 | — | % | 4.140 | % | |||||||||||||||||||||||||

| Total | $ | 96,720 | $ | 3,175,000 | $ | 3,271,720 | 100 | % | 3.723 | % | ||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 19 | | ||||||

Operations. | ||||||||

| Quarterly Results | ||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 20 | | ||||||

Portfolio Overview. | ||||||||

| At March 31, 2026 | (unaudited results) | |||||||

| Consolidated Portfolio: | ||||||||

| Rentable Square Feet | Ending Occupancy % | In-Place ABR(3) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Market | # of Properties | Same Property Portfolio | Non-Same Property Portfolio | Total Portfolio | Same Property Portfolio | Non-Same Property Portfolio | Total Portfolio(1) | Total Portfolio Excluding Repo/Redev(2) | Total (in 000’s) | Per Square Foot | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Central LA | 20 | 2,834,219 | 384,729 | 3,218,948 | 97.7 | % | 83.1 | % | 95.9 | % | 97.9 | % | $ | 42,773 | $13.85 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Greater San Fernando Valley | 73 | 5,694,646 | 1,336,692 | 7,031,338 | 97.4 | % | 54.0 | % | 89.2 | % | 93.1 | % | 110,791 | $17.67 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Mid-Counties | 39 | 3,106,841 | 1,749,456 | 4,856,297 | 96.1 | % | 84.0 | % | 91.7 | % | 95.7 | % | 78,100 | $17.53 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| San Gabriel Valley | 45 | 4,790,522 | 1,339,164 | 6,129,686 | 93.7 | % | 33.8 | % | 80.6 | % | 92.9 | % | 67,143 | $13.59 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| South Bay | 81 | 6,555,953 | 1,216,128 | 7,772,081 | 97.9 | % | 71.3 | % | 93.7 | % | 97.9 | % | 174,059 | $23.89 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Los Angeles County | 258 | 22,982,181 | 6,026,169 | 29,008,350 | 96.6 | % | 63.6 | % | 89.8 | % | 95.4 | % | 472,866 | $18.16 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| North Orange County | 24 | 1,919,265 | 621,985 | 2,541,250 | 92.5 | % | 61.8 | % | 85.0 | % | 93.7 | % | 40,841 | $18.92 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| OC Airport | 8 | 1,042,362 | — | 1,042,362 | 100.0 | % | — | % | 100.0 | % | 100.0 | % | 21,138 | $20.28 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| South Orange County | 9 | 482,919 | 46,642 | 529,561 | 100.0 | % | 56.6 | % | 96.2 | % | 100.0 | % | 8,979 | $17.63 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| West Orange County | 10 | 1,288,838 | — | 1,288,838 | 98.4 | % | — | % | 98.4 | % | 98.4 | % | 22,013 | $17.35 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Orange County | 51 | 4,733,384 | 668,627 | 5,402,011 | 96.5 | % | 61.4 | % | 92.2 | % | 96.8 | % | 92,971 | $18.67 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Inland Empire East | 1 | 33,258 | — | 33,258 | 100.0 | % | — | % | 100.0 | % | 100.0 | % | 682 | $20.52 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Inland Empire West | 52 | 9,034,990 | 489,396 | 9,524,386 | 94.2 | % | 35.7 | % | 91.2 | % | 93.8 | % | 135,489 | $15.60 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Riverside / San Bernardino County | 53 | 9,068,248 | 489,396 | 9,557,644 | 94.2 | % | 35.7 | % | 91.2 | % | 93.8 | % | 136,171 | $15.62 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Central San Diego | 21 | 1,417,060 | 511,105 | 1,928,165 | 97.5 | % | 53.3 | % | 85.8 | % | 93.7 | % | 40,468 | $24.47 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| North County San Diego | 13 | 1,042,142 | 280,876 | 1,323,018 | 97.4 | % | 100.0 | % | 97.9 | % | 98.7 | % | 20,238 | $15.62 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| San Diego County | 34 | 2,459,202 | 791,981 | 3,251,183 | 97.5 | % | 69.8 | % | 90.7 | % | 95.9 | % | 60,706 | $20.58 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Ventura | 18 | 2,484,310 | 741,814 | 3,226,124 | 95.5 | % | 91.1 | % | 94.5 | % | 95.3 | % | 43,416 | $14.24 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Ventura County | 18 | 2,484,310 | 741,814 | 3,226,124 | 95.5 | % | 91.1 | % | 94.5 | % | 95.3 | % | 43,416 | $14.24 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| CONSOLIDATED TOTAL / WTD AVG | 414 | 41,727,325 | 8,717,987 | 50,445,312 | 96.1 | % | 64.8 | % | 90.7 | % | 95.2 | % | $ | 806,130 | $17.63 | (4) | |||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 21 | | ||||||

Executed Leasing Statistics and Trends. | ||||||||

| (unaudited results) | ||||||||

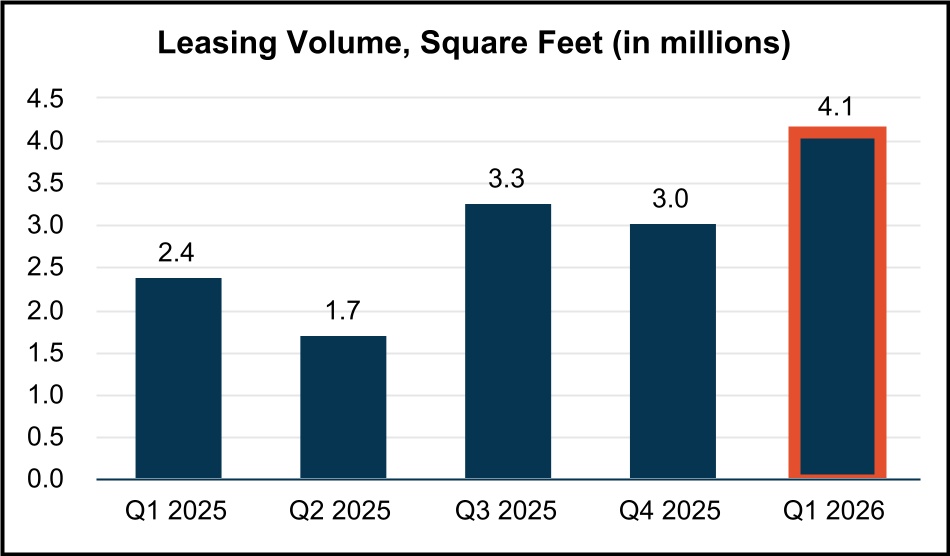

| Executed Leasing Activity and Weighted Average New / Renewal Leasing Spreads: | ||||||||

| Three Months Ended | ||||||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | ||||||||||||||||||||||||||||

| Leasing Spreads: | ||||||||||||||||||||||||||||||||

Net Effective Rent Change | (10.0) | % | 22.0 | % | 26.1 | % | 20.9 | % | 23.8 | % | ||||||||||||||||||||||

Cash Rent Change | (15.4) | % | 9.0 | % | 10.3 | % | 8.1 | % | 14.7 | % | ||||||||||||||||||||||

Leasing Activity (Building SF):(1) | ||||||||||||||||||||||||||||||||

| New leases | 1,296,230 | 1,574,816 | 2,361,131 | 678,727 | 882,403 | |||||||||||||||||||||||||||

| Renewal leases | 2,829,822 | 1,464,751 | 904,014 | 1,020,266 | 1,511,946 | |||||||||||||||||||||||||||

| Total leasing activity | 4,126,052 | 3,039,567 | 3,265,145 | 1,698,993 | 2,394,349 | |||||||||||||||||||||||||||

| Total expiring leases | (4,638,894) | (3,551,170) | (1,734,790) | (1,786,814) | (3,102,514) | |||||||||||||||||||||||||||

Expiring leases - placed into repositioning/development | 152,417 | 957,493 | 418,878 | 304,776 | 833,218 | |||||||||||||||||||||||||||

Net absorption(2) | (360,425) | 445,890 | 1,949,233 | 216,955 | 125,053 | |||||||||||||||||||||||||||

Retention rate(3) | 64 | % | 61 | % | 72 | % | 69 | % | 68 | % | ||||||||||||||||||||||

Retention + Backfill rate(4) | 79 | % | 70 | % | 77 | % | 74 | % | 82 | % | ||||||||||||||||||||||

Executed Leasing Activity and Change in Annual Rental Rates and Turnover Costs for Current Quarter Leases:(5) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Effective Rent | Cash Rent | Turnover Costs(6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| First Quarter 2026 | # Leases Signed | SF of Leasing | Wtd. Avg. Lease Term (Years) | Current Lease | Prior Lease | Rent Change | Current Lease | Prior Lease | Rent Change | Wtd. Avg. Abatement (Months) | Tenant Improvements per SF | Leasing Commissions per SF | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New | 59 | 1,296,230 | 4.1 | $16.16 | $17.70 | (8.7)% | $16.46 | $18.88 | (12.8)% | 3.5 | $3.24 | $3.40 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Renewal | 85 | 2,829,822 | 3.0 | $15.13 | $16.87 | (10.3)% | $15.30 | $18.20 | (15.9)% | 2.0 | $0.37 | $1.90 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total / Wtd. Average | 144 | 4,126,052 | 3.4 | $15.30 | $17.01 | (10.0)% | $15.49 | $18.31 | (15.4)% | 2.2 | $0.86 | $2.15 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Excluding Tireco, Inc. Lease Extension: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Renewal(7) | 84 | 1,727,982 | 2.9 | $15.38 | $13.76 | 11.8% | $15.18 | $14.73 | 3.0% | 1.3 | $0.63 | $1.46 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total / Wtd. Average(7) | 143 | 3,024,212 | 3.4 | $15.58 | $14.76 | 5.5% | $15.50 | $15.78 | (1.8)% | 1.8 | $1.30 | $1.95 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 22 | | ||||||

Leasing Statistics (Continued). | ||||||||

| (unaudited results) | ||||||||

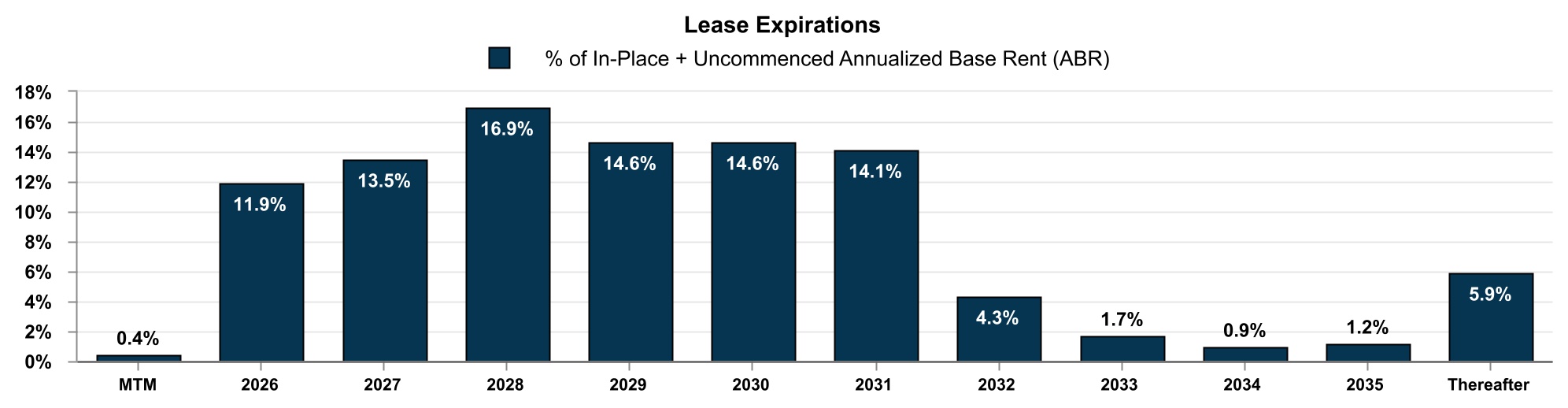

| Lease Expiration Schedule as of March 31, 2026: | ||||||||

| Year of Lease Expiration | # of Leases Expiring | Total Rentable Square Feet | In-Place + Uncommenced ABR (in thousands) | In-Place + Uncommenced ABR per SF | ||||||||||||||||||||||

| Available | — | 2,018,812 | $ | — | $— | |||||||||||||||||||||

Repositioning/Development(1) | — | 2,367,663 | — | $— | ||||||||||||||||||||||

| MTM Tenants | 11 | 177,759 | 3,081 | $17.33 | ||||||||||||||||||||||

| 2026 | 275 | 5,325,060 | 96,674 | $18.15 | ||||||||||||||||||||||

| 2027 | 360 | 6,455,107 | 109,436 | $16.95 | ||||||||||||||||||||||

| 2028 | 297 | 7,116,599 | 137,161 | $19.27 | ||||||||||||||||||||||

| 2029 | 251 | 6,560,423 | 118,418 | $18.05 | ||||||||||||||||||||||

| 2030 | 141 | 7,032,333 | 118,134 | $16.80 | ||||||||||||||||||||||

| 2031 | 117 | 7,801,768 | 114,570 | $14.69 | ||||||||||||||||||||||

| 2032 | 32 | 1,772,969 | 35,270 | $19.89 | ||||||||||||||||||||||

| 2033 | 16 | 785,478 | 14,124 | $17.98 | ||||||||||||||||||||||

| 2034 | 7 | 355,445 | 6,992 | $19.67 | ||||||||||||||||||||||

| 2035 | 8 | 462,072 | 9,634 | $20.85 | ||||||||||||||||||||||

| Thereafter | 36 | 2,213,824 | 47,687 | $21.54 | ||||||||||||||||||||||

| Total Portfolio | 1,551 | 50,445,312 | $ | 811,181 | $17.61(2) | |||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 23 | | ||||||

Top Tenants and Lease Segmentation. | ||||||||

| (unaudited results) | ||||||||

Top 20 Tenants as of March 31, 2026 | ||||||||

| Tenant | Submarket | Leased Rentable SF | In-Place + Uncommenced ABR (in 000’s)(1) | % of In-Place + Uncommenced ABR(1) | In-Place + Uncommenced ABR per SF(1) | Lease Expiration | ||||||||||||||||||||||||||||||||

Tireco, Inc.(2) | Inland Empire West | 1,101,840 | $20,021 | 2.5% | $18.17 | 4/30/2030(2) | ||||||||||||||||||||||||||||||||

| Zenith Energy West Coast Terminals LLC | South Bay | —(3) | $11,909 | 1.5% | $3.41(3) | 9/29/2041 | ||||||||||||||||||||||||||||||||

| IBY, LLC | San Gabriel Valley | 1,178,021 | $11,531 | 1.4% | $9.79 | 4/5/2031(4) | ||||||||||||||||||||||||||||||||

| Cubic Corporation | Central San Diego | 315,227 | $11,443 | 1.4% | $36.30 | 3/31/2038 | ||||||||||||||||||||||||||||||||

| Federal Express Corporation | Multiple Submarkets(5) | 527,861 | $10,986 | 1.3% | $20.81 | 11/30/2032(5) | ||||||||||||||||||||||||||||||||

| L3 Technologies, Inc. | South Bay | 461,431 | $9,537 | 1.2% | $20.67 | 9/30/2031 | ||||||||||||||||||||||||||||||||

| GXO Logistics Supply Chain, Inc. | Mid-Counties | 411,034 | $9,076 | 1.1% | $22.08 | 11/30/2028 | ||||||||||||||||||||||||||||||||

| The Hertz Corporation | South Bay | 38,680(6) | $8,922 | 1.1% | $11.14(6) | 10/31/2026 | ||||||||||||||||||||||||||||||||

| Best Buy Stores, L.P. | Inland Empire West | 501,649 | $8,871 | 1.1% | $17.68 | 6/30/2029 | ||||||||||||||||||||||||||||||||

| Orora Packaging Solutions | Multiple Submarkets(7) | 476,065 | $8,150 | 1.0% | $17.12 | 9/30/2028(7) | ||||||||||||||||||||||||||||||||

| Top 10 Tenants | 5,011,808 | $110,446 | 13.6% | |||||||||||||||||||||||||||||||||||

| Top 11 - 20 Tenants | 3,804,158 | $52,162 | 6.4% | |||||||||||||||||||||||||||||||||||

| Total Top 20 Tenants | 8,815,966 | $162,608 | 20.0% | |||||||||||||||||||||||||||||||||||

| Lease Segmentation by Size: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Square Feet | Number of Leases | Leased Building/Land Rentable SF | Building/Land Rentable SF | Leased % | Leased % Excl. Repo/Redev | In-Place + Uncommenced ABR (in 000’s)(1) | % of In-Place + Uncommenced ABR(1) | In-Place + Uncommenced ABR per SF(1) | |||||||||||||||||||||||||||||||||||||||||||||

| Building: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| <4,999 | 528 | 1,317,282 | 1,423,356 | 92.5% | 92.8% | $ | 26,537 | 3.3% | $20.15 | ||||||||||||||||||||||||||||||||||||||||||||

| 5,000 - 9,999 | 214 | 1,526,542 | 1,706,427 | 89.5% | 91.0% | 30,018 | 3.7% | $19.66 | |||||||||||||||||||||||||||||||||||||||||||||

| 10,000 - 24,999 | 319 | 5,208,997 | 5,730,610 | 90.9% | 93.7% | 99,532 | 12.3% | $19.11 | |||||||||||||||||||||||||||||||||||||||||||||

| 25,000 - 49,999 | 180 | 6,541,759 | 7,260,587 | 90.1% | 94.2% | 118,436 | 14.6% | $18.10 | |||||||||||||||||||||||||||||||||||||||||||||

| 50,000 - 99,999 | 118 | 8,482,118 | 9,714,581 | 87.3% | 96.4% | 150,593 | 18.5% | $17.75 | |||||||||||||||||||||||||||||||||||||||||||||

| >100,000 | 120 | 22,783,920 | 24,396,789 | 93.4% | 97.1% | 341,724 | 42.1% | $15.00 | |||||||||||||||||||||||||||||||||||||||||||||

| Building Subtotal / Wtd. Avg. | 1,479 | 45,860,618 | (2) | 50,232,350 | (2) | 91.3% | (2) | 95.8% | (2) | $ | 766,840 | 94.5% | $16.72 | ||||||||||||||||||||||||||||||||||||||||

Land/IOS(3) | 22 | 7,664,817 | (4) | 8,263,593 | (4) | 92.8% | (4) | 41,368 | 5.1% | $5.40 | (4) | ||||||||||||||||||||||||||||||||||||||||||

Other(3) | 50 | 2,973 | 0.4% | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | 1,551 | $ | 811,181 | 100.0% | |||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 24 | | ||||||

Capital Expenditure Summary. | ||||||||

| (unaudited results, in thousands, except square feet and per square foot data) | ||||||||

| Three months ended March 31, 2026 | ||||||||

| Year to Date | ||||||||||||||||||||

| Total | SF(1) | PSF | ||||||||||||||||||

| Tenant Improvements: | ||||||||||||||||||||

| New Leases – 1st Generation | $ | 148 | 44,052 | $ | 3.36 | |||||||||||||||

| New Leases – 2nd Generation | 50 | 136,065 | $ | 0.37 | ||||||||||||||||

| Renewals | 135 | 365,392 | $ | 0.37 | ||||||||||||||||

| Total Tenant Improvements | $ | 333 | ||||||||||||||||||

| Leasing Commissions & Lease Costs: | ||||||||||||||||||||

| New Leases – 1st Generation | $ | 2,174 | 526,129 | $ | 4.13 | |||||||||||||||

| New Leases – 2nd Generation | 3,931 | 758,090 | $ | 5.19 | ||||||||||||||||

| Renewals | 4,262 | 2,236,364 | $ | 1.91 | ||||||||||||||||

| Total Leasing Commissions & Lease Costs | $ | 10,367 | ||||||||||||||||||

| Total Recurring Capex | $ | 2,314 | 50,708,486 | $ | 0.05 | |||||||||||||||

| Recurring Capex % of NOI | 1.2 | % | ||||||||||||||||||

| Recurring Capex % of Rental Income | 1.0 | % | ||||||||||||||||||

| Nonrecurring Capex: | ||||||||||||||||||||

Repositioning and Development in Process(2) | $ | 29,483 | ||||||||||||||||||

Unit Renovation(3) | 7,933 | |||||||||||||||||||

Other(4) | 2,451 | |||||||||||||||||||

| Total Nonrecurring Capex | $ | 39,867 | 30,061,253 | $ | 1.33 | |||||||||||||||

Other Capitalized Costs(5) | $ | 13,858 | ||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 25 | | ||||||

Properties and Space Under Repositioning/Development.(1) | ||||||||

| As of March 31, 2026 | (unaudited results, $ in millions) | |||||||

1Q 2026 Stabilizations | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

RSF(2) | Purch. Price(1) | Proj. Project Costs(1) | Proj. Total Invest.(1) | Proj. Remaining Costs | Construction Period(1) | Property Leased | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Property | Submarket | Repositioning/ Development | Start | Complete | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

1Q 2026 Stabilizations | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12118 Bloomfield Avenue | Mid-Counties | Development | 107,045 | $ | 16.7 | $ | 20.0 | $ | 36.7 | $ | — | 4Q-22 | 1Q-25 | 100% | ||||||||||||||||||||||||||||||||||||||||||||||||

1315 Storm Parkway(3) | South Bay | Repositioning | 37,844 | 8.5 | 3.4 | 11.9 | 0.3 | 2Q-24 | 4Q-24 | 100% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total/Weighted Average Stabilized | 144,889 | $ | 25.2 | $ | 23.4 | $ | 48.6 | $ | 0.3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

Stabilized | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repositioning | Development | Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Actual Cash NOI: 1Q 2026 ($M) | $— | $(0.1) | $(0.1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Annualized Stabilized Cash NOI ($M) | $0.7 | $1.9 | $2.6 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Estimated Stabilized Return on Cost | 5.9% | 5.2% | 5.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 26 | | ||||||

Properties and Space Under Repositioning/Development (Continued).(1) | ||||||||

| As of March 31, 2026 | (unaudited results, $ in millions) | |||||||

Lease-Up | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Repositioning/ Development | RSF(2) | Purch. Price(1) | Est. Project Costs(1) | Est. Total Invest.(1) | Est. Remaining Costs | Construction Period | Property Leased | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Property | Submarket | Start | Complete | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Lease-Up | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

9615 Norwalk Boulevard | Mid-Counties | Development | 201,571 | $ | 9.6 | $ | 49.9 | $ | 59.5 | $ | 1.8 | 3Q-21 | 4Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||

3211-3233 Mission Oaks Blvd.(4) | Ventura | Development | 116,852 | 40.7 | 26.2 | 66.9 | 0.2 | 2Q-22 | 1Q-25 | 83% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

4416 Azusa Canyon Road | San Gabriel Valley | Development | 129,830 | 12.3 | 21.4 | 33.7 | 1.7 | 4Q-22 | 2Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

15010 Don Julian Road | San Gabriel Valley | Development | 219,690 | 22.9 | 37.6 | 60.5 | 2.9 | 1Q-23 | 4Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

12772 San Fernando Road(5) | Greater San Fernando Valley | Development | 143,529 | 22.1 | 22.6 | 44.7 | 1.3 | 3Q-23 | 1Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

19900 Plummer Street(5) | Greater San Fernando Valley | Development | 79,539 | 15.5 | 15.6 | 31.1 | 1.3 | 3Q-23 | 1Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

1500 Raymond Avenue(5) | North Orange County | Development | 136,218 | 46.1 | 22.4 | 68.5 | 1.1 | 4Q-23 | 1Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

19301 Santa Fe Avenue | South Bay | Repositioning | LAND | 14.7 | 5.7 | 20.4 | 0.4 | 2Q-24 | 3Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

14955 Salt Lake Avenue | San Gabriel Valley | Repositioning | 45,205 | 10.9 | 3.7 | 14.6 | 0.5 | 4Q-24 | 3Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

8985 Crestmar Point | Central San Diego | Repositioning | 53,395 | 8.1 | 5.7 | 13.8 | 0.7 | 4Q-24 | 3Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

9455 Cabot Drive | Central San Diego | Repositioning | 97,510 | 12.2 | 8.2 | 20.4 | 1.2 | 2Q-25 | 4Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

1175 Aviation Place | Greater San Fernando Valley | Repositioning | 93,202 | 17.9 | 3.9 | 21.8 | 0.8 | 3Q-25 | 4Q-25 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Total/Weighted Average Lease-Up | 1,316,541 | $ | 233.0 | $ | 222.9 | $ | 455.9 | $ | 13.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 27 | | ||||||

Properties and Space Under Repositioning/Development (Continued).(1) | ||||||||

| As of March 31, 2026 | (unaudited results, $ in millions) | |||||||

Under Construction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Repositioning/Development | RSF(2) | Purch. Price(1) | Est. Project Costs(1) | Est. Total Invest.(1) | Est. Remaining Costs | Construction Period | Property Leased | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Property | Submarket | Start | Complete | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Under Construction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

14940 Proctor Road | San Gabriel Valley | Development | 160,094 | $ | 28.8 | $ | 26.1 | $ | 54.9 | $ | 2.6 | 4Q-24 | 2Q-26 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||

| 11234 Rush Street | San Gabriel Valley | Development | 101,728 | 12.6 | 21.6 | 34.2 | 3.0 | 4Q-24 | 3Q-26 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

3680-3880 Voyager Street (3547-3555 Voyager Street) | South Bay | Development | 67,734 | 21.1 | 18.9 | 40.0 | 7.3 | 1Q-25 | 3Q-26 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5235 Hunter Avenue | North Orange County | Development | 121,288 | 11.4 | 20.2 | 31.6 | 4.3 | 1Q-25 | 2Q-26 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 7815 Van Nuys Boulevard | Greater San Fernando Valley | Development | 78,904 | 25.6 | 16.0 | 41.6 | 7.2 | 2Q-25 | 4Q-26 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

14400 Figueroa Street (Figueroa & Rosecrans) | South Bay | Repositioning | 56,771 | 61.4 | 16.8 | 78.2 | 13.4 | 3Q-25 | 1Q-27 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 950 West 190th Street | South Bay | Development | 196,900 | 41.5 | 31.3 | 72.8 | 29.4 | 4Q-25 | 4Q-27 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 9323 Balboa Avenue | Central San Diego | Development | 177,551 | 27.1 | 26.3 | 53.4 | 23.9 | 4Q-25 | 2Q-27 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 24935-24955 Avenue Kearny | Greater San Fernando Valley | Repositioning | 66,130 | 5.8 | 3.8 | 9.6 | 1.4 | 4Q-25 | 2Q-26 | —% | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Total/Weighted Average Under Construction | 1,027,100 | $ | 235.3 | $ | 181.0 | $ | 416.3 | $ | 92.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

Total/Weighted Average Lease-Up/Under Construction | 2,343,641 | $ | 468.3 | $ | 403.9 | $ | 872.2 | $ | 106.4 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

Lease-Up/Under Construction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repositioning | Development | Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Actual Cash NOI: 1Q 2026 ($M) | $0.3 | $1.2 | $1.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Annualized Stabilized Cash NOI ($M) | $9 - $10 | $38 - $42 | $47 - $51 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Estimated Stabilized Return on Cost | 5.0% - 5.5% | 5.5% - 6.0% | 5.5% - 6.0% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 28 | | ||||||

Properties and Space Under Repositioning/Development (Continued).(1) | ||||||||

| As of March 31, 2026 | (unaudited results, $ in millions) | |||||||

Near-Term Potential Future Repositioning and Development | ||||||||||||||||||||||||||

| Property | Submarket | Repositioning/ Development | Projected RSF(7) | Estimated Construction Start | Purchase Price ($M) | Lease Expiration Date | Actual Cash NOI 1Q 2026 ($M) | Project Description | ||||||||||||||||||

| 16425 Gale Avenue | SG Valley | Development | 325,800 | 2Q-26 | $26.3 | Vacant | $— | Development of an existing 1970s vintage industrial building acquired in 2016. The project will deliver a modern, Class A demisable cross-dock industrial building. | ||||||||||||||||||

9400-9500 Santa Fe Springs Road(6) | Mid-Counties | Repositioning | 184,270 | 2Q-26 | $210.0 | 05/31/26 | $0.6 | Functionality and quality upgrades including new office, additional power capacity and sprinkler upgrade. | ||||||||||||||||||

| 3100 Fujita Street | South Bay | Repositioning | 91,516 | 3Q-26 | $14.2 | Vacant | $— | Repositioning of an existing 1970s vintage, functionally-limited industrial building acquired in 2018 through a sale leaseback. | ||||||||||||||||||

9000 Airport Boulevard | South Bay | Development | 418,000 | 4Q-26 | $144.3 | 10/31/26 | $2.2 | 18 acres of industrially-zoned land acquired through a sale leaseback for planned development. Following lease expiration, the project will deliver a rare, Class-A industrial campus. | ||||||||||||||||||

4181 Ruffin Road | Central San Diego | Development | 220,943 | 4Q-26 | $36.0 | 10/31/26 | $0.0 | Development of a modern Class A industrial building with highly competitive functionality in a premier location. | ||||||||||||||||||

| Total Future Repositioning/Development | 1,240,529 | $430.8 | $2.8 | |||||||||||||||||||||||

| Repositioning | Development | Total | ||||||||||||||||||||||||

| Projected RSF | 275,786 | 964,743 | 1,240,529 | |||||||||||||||||||||||

Projected Project Costs ($M) | $20 - $22 | $140 - $148 | $160 - $170 | |||||||||||||||||||||||

Actual Cash NOI: 1Q 2026(7) ($M) | $0.6 | $2.2 | $2.8 | |||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 29 | | ||||||

Properties and Space Under Repositioning/Development (Continued).(1) | |||||||||||

| As of March 31, 2026 | (unaudited results, in thousands, except square feet) | ||||||||||

| Current Year Stabilized Repositioning/Development | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Property (Submarket) | RSF | Stabilized Period | Stabilized Return on Cost | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12118 Bloomfield Avenue | 107,045 | 1Q-26 | 5.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||

1315 Storm Parkway(3) | 37,844 | 1Q-26 | 5.9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 30 | | ||||||

Current Year Investments and Dispositions Summary. | ||||||||||||||||||||||||||||||||||||||

| As of March 31, 2026 | (unaudited results) | |||||||||||||||||||||||||||||||||||||

| 2026 Current Period Dispositions | ||||||||||||||||||||||||||||||||||||||

| Disposition Date | Property Address | Submarket | Asset Type | Rentable Square Feet | Gross Proceeds ($M) | Realized NOI Contribution in the Quarter of Sale ($M) | ||||||||||||||||||||||||||||||||

| 2/6/2026 | 14005 Live Oak Avenue | Los Angeles - San Gabriel Valley | Development | — | $ | 14.50 | $ | — | ||||||||||||||||||||||||||||||

| 2/24/2026 | 18250 Euclid Street | Orange County Airport | Operating | 62,838 | $ | 26.71 | $ | 0.1 | ||||||||||||||||||||||||||||||

| 3/17/2026 | 29010 Avenue Paine | Los Angeles - Greater San Fernando Valley | Operating | 100,157 | $ | 31.00 | $ | 0.2 | ||||||||||||||||||||||||||||||

| 3/18/2026 | 13700-13738 Slover Avenue | San Bernardino - Inland Empire West | Operating | 17,862 | $ | 14.48 | $ | (0.1) | ||||||||||||||||||||||||||||||

| 3/25/2026 | 600-708 Vermont Avenue | North Orange County | Development | 133,836 | $ | 40.70 | $ | — | ||||||||||||||||||||||||||||||

Total 2026 Dispositions through March 31, 2026 | 314,693 | $ | 127.39 | |||||||||||||||||||||||||||||||||||

| 2026 Subsequent Period Dispositions | ||||||||||||||||||||||||||||||||||||||

| 4/16/2026 | 423-424 Berry Way | North Orange County | Development | 101,380 | $ | 16.51 | N/A | |||||||||||||||||||||||||||||||

Total Year To Date 2026 Dispositions | 416,073 | $ | 143.90 | |||||||||||||||||||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 31 | | ||||||

Net Asset Value Components. | ||||||||

| As of March 31, 2026 | (unaudited and in thousands, except share data) | |||||||

| Net Operating Income | ||||||||

Pro Forma Net Operating Income (NOI)(1) | Three Months Ended Mar 31, 2026 | |||||||

| Total operating rental income | $242,141 | |||||||

| Property operating expenses | (56,763) | |||||||

Pro forma effect of uncommenced leases(2) | 1,076 | |||||||

Pro forma effect of dispositions(3) | (206) | |||||||

Pro forma NOI effect of significant properties classified as current, lease-up, and stabilized repositioning and development(4) | 11,547 | |||||||

| Pro Forma NOI | 197,795 | |||||||

Above/(below) market lease revenue adjustments | (4,647) | |||||||

| Straight line rental revenue adjustment | (15,136) | |||||||

| Pro Forma Cash NOI | $178,012 | |||||||

| Balance Sheet Items | ||||||||

| Other assets and liabilities | March 31, 2026 | |||||||

| Cash and cash equivalents | $51,714 | |||||||

| Loan receivable, net | 123,819 | |||||||

| Rents and other receivables, net | 11,962 | |||||||

| Other assets | 20,500 | |||||||

| Accounts payable, accrued expenses and other liabilities | (125,007) | |||||||

| Dividends payable | (102,418) | |||||||

| Tenant security deposits | (95,219) | |||||||

| Prepaid rents | (82,186) | |||||||

Estimated remaining cost to complete repositioning/development projects(5) | (106,813) | |||||||

| Total other assets and liabilities | $(303,648) | |||||||

| Debt and Shares Outstanding | ||||||||

Total consolidated debt(6) | $3,271,720 | |||||||

| Preferred stock/units - liquidation preference | $173,250 | |||||||

Common shares outstanding(7) | 224,521,552 | |||||||

Operating partnership units outstanding(8) | 8,605,741 | |||||||

| Total common shares and operating partnership units outstanding | 233,127,293 | |||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 32 | | ||||||

Notes and Definitions. | ||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 33 | | ||||||

Notes and Definitions. | ||||||||

| March 31, 2026 | |||||||||||||||||

| Current Period Covenant | Revolver, $300M & $400M Term Loan Facilities | Senior Notes ($125M, $25M, $75M) | |||||||||||||||

| Maximum Leverage Ratio | less than 60% | 24.2% | 27.7% | ||||||||||||||

| Maximum Secured Leverage Ratio | less than 45% | 0.7% | N/A | ||||||||||||||

| Maximum Secured Leverage Ratio | less than 40% | N/A | 0.8% | ||||||||||||||

| Maximum Secured Recourse Debt | less than 15% | N/A | —% | ||||||||||||||

| Minimum Tangible Net Worth | $7,266,909 | N/A | $9,829,351 | ||||||||||||||

| Minimum Fixed Charge Coverage Ratio | at least 1.50 to 1.00 | 5.34 to 1.0 | 5.30 to 1.00 | ||||||||||||||

| Unencumbered Leverage Ratio | less than 60% | 25.0% | 28.9% | ||||||||||||||

| Unencumbered Interest Coverage Ratio | at least 1.75 to 1.00 | 5.97 to 1.00 | 5.97 to 1.00 | ||||||||||||||

| March 31, 2026 | |||||||||||

| Current Period Covenant | Senior Notes ($400M due 2030 & $400M due 2031) | ||||||||||

| Maximum Debt to Total Asset Ratio | less than 60% | 24.1% | |||||||||

| Maximum Secured Debt to Total Asset Ratio | less than 40% | 0.7% | |||||||||

| Minimum Debt Service Coverage Ratio | at least 1.50 to 1.00 | 5.21 to 1.00 | |||||||||

| Minimum Unencumbered Assets to Unsecured Debt Ratio | at least 1.50 to 1.00 | 4.21 to 1.00 | |||||||||

For the Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

EBITDAre | $ | 174,638 | $ | 103,701 | $ | 171,108 | $ | 173,922 | $ | 174,919 | |||||||||||||||||||

Above/(below) market lease revenue adjustments | (4,647) | (4,129) | (5,254) | (5,788) | (9,186) | ||||||||||||||||||||||||

Non-cash stock compensation | 4,063 | 8,537 | 10,485 | 10,091 | 9,699 | ||||||||||||||||||||||||

Co-CEO transition costs | — | 60,223 | — | — | — | ||||||||||||||||||||||||

Debt extinguishment and modification expenses | — | — | — | 291 | — | ||||||||||||||||||||||||

Straight line rental revenue adj. | (15,136) | (9,073) | (8,164) | (6,918) | (5,517) | ||||||||||||||||||||||||

Capitalized payments | (5,851) | (6,013) | (6,516) | (5,304) | (5,091) | ||||||||||||||||||||||||

| Accretion of net loan origination fees | (115) | (115) | (115) | (115) | (115) | ||||||||||||||||||||||||

Recurring capital expenditures | (2,314) | (2,566) | (3,563) | (5,887) | (1,311) | ||||||||||||||||||||||||

| 2nd gen. tenant improvements | (185) | (179) | (460) | (663) | (162) | ||||||||||||||||||||||||

| 2nd gen. leasing commissions | (8,193) | (6,324) | (8,007) | (4,162) | (4,879) | ||||||||||||||||||||||||

| Cash flow for fixed charge coverage calculation | $ | 142,260 | $ | 144,062 | $ | 149,514 | $ | 155,467 | $ | 158,357 | |||||||||||||||||||

| Cash interest expense calculation detail: | |||||||||||||||||||||||||||||

| Interest expense | 26,600 | 25,451 | 25,463 | 26,701 | 27,288 | ||||||||||||||||||||||||

| Capitalized interest | 7,352 | 8,801 | 9,240 | 9,064 | 8,230 | ||||||||||||||||||||||||

| Note payable premium amort. | (1,641) | (1,616) | (1,597) | (1,579) | (1,560) | ||||||||||||||||||||||||

| Amort. of deferred financing costs | (1,334) | (1,333) | (1,340) | (1,255) | (1,134) | ||||||||||||||||||||||||

| Amort. of swap term fees & t-locks | (77) | (78) | (78) | (76) | (77) | ||||||||||||||||||||||||

| Cash interest expense | 30,900 | 31,225 | 31,688 | 32,855 | 32,747 | ||||||||||||||||||||||||

| Scheduled principal payments | 215 | 247 | 244 | 242 | 230 | ||||||||||||||||||||||||

| Preferred stock/unit dividends | 2,404 | 2,405 | 2,404 | 2,405 | 2,695 | ||||||||||||||||||||||||

| Fixed charges | $ | 33,519 | $ | 33,877 | $ | 34,336 | $ | 35,502 | $ | 35,672 | |||||||||||||||||||

| Fixed Charge Coverage Ratio | 4.2 | x | 4.3 | x | 4.4 | x | 4.4 | x | 4.4 | x | |||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 34 | | ||||||

Notes and Definitions. | ||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 35 | | ||||||

Notes and Definitions. | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

| Rental revenue (before collectability adjustment) | $ | 202,658 | $ | 201,454 | $ | 203,217 | $ | 199,839 | $ | 208,394 | |||||||||||||||||||

| Tenant reimbursements | 41,728 | 43,793 | 42,612 | 41,403 | 41,856 | ||||||||||||||||||||||||

| Other income | 486 | 598 | 915 | 467 | 874 | ||||||||||||||||||||||||

| Increase (reduction) in revenue due to change in collectability assessment | (2,731) | (2,615) | 13 | (141) | (2,303) | ||||||||||||||||||||||||

| Rental income | $ | 242,141 | $ | 243,230 | $ | 246,757 | $ | 241,568 | $ | 248,821 | |||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

| # of Properties | 342 | 287 | 288 | 289 | 292 | ||||||||||||||||||||||||

| Square Feet | 41,727,325 | 37,466,856 | 37,916,326 | 37,991,248 | 38,380,256 | ||||||||||||||||||||||||

| Ending Occupancy | 96.1 | % | 96.5 | % | 96.8 | % | 96.1 | % | 95.7 | % | |||||||||||||||||||

| SPP NOI growth | 0.9 | % | 0.4 | % | 1.9 | % | 1.1 | % | 0.7 | % | |||||||||||||||||||

| SPP Cash NOI growth | (0.4) | % | 2.8 | % | 5.5 | % | 3.9 | % | 5.0 | % | |||||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| 2026 | 2025 | $ Change | % Change | ||||||||||||||||||||

| Rental revenue | $ | 175,232 | $ | 171,506 | $ | 3,726 | 2.2% | ||||||||||||||||

| Tenant reimbursements | 35,740 | 35,709 | 31 | 0.1% | |||||||||||||||||||

| Other income | 419 | 704 | (285) | (40.5)% | |||||||||||||||||||

| Rental income | $ | 211,391 | $ | 207,919 | $ | 3,472 | 1.7% | ||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | |||||||||||||||||||||||||

Net Income (Loss) | $ | 94,562 | $ | (67,735) | $ | 93,056 | $ | 120,394 | $ | 74,048 | |||||||||||||||||||

| General and administrative | 14,925 | 19,199 | 20,037 | 19,752 | 19,868 | ||||||||||||||||||||||||

| Depreciation & amortization | 72,933 | 76,819 | 81,172 | 71,188 | 86,740 | ||||||||||||||||||||||||

| Other expenses | 102 | 65,910 | 4,218 | 244 | 2,239 | ||||||||||||||||||||||||

| Interest expense | 26,600 | 25,451 | 25,463 | 26,701 | 27,288 | ||||||||||||||||||||||||

Debt extinguishment and modification expenses | — | — | — | 291 | — | ||||||||||||||||||||||||

| Management & leasing services | — | (197) | (118) | (132) | (142) | ||||||||||||||||||||||||

| Other income | (1,350) | — | — | — | — | ||||||||||||||||||||||||

| Interest income | (2,937) | (4,670) | (6,367) | (7,807) | (3,324) | ||||||||||||||||||||||||

Impairment of real estate | 6,824 | 89,097 | — | — | — | ||||||||||||||||||||||||

| Gains on sale of real estate | (26,281) | (19,931) | (28,583) | (44,361) | (13,157) | ||||||||||||||||||||||||

| NOI | $ | 185,378 | $ | 183,943 | $ | 188,878 | $ | 186,270 | $ | 193,560 | |||||||||||||||||||

| S/L rental revenue adj. | (15,136) | (9,073) | (8,164) | (6,918) | (5,517) | ||||||||||||||||||||||||

Above/(below) market lease revenue adjustments | (4,647) | (4,129) | (5,254) | (5,788) | (9,186) | ||||||||||||||||||||||||

| Cash NOI | $ | 165,595 | $ | 170,741 | $ | 175,460 | $ | 173,564 | $ | 178,857 | |||||||||||||||||||

First Quarter 2026 Supplemental Financial Reporting Package | Page 36 | | ||||||

Notes and Definitions. | ||||||||

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

Net income | $ | 94,562 | $ | 74,048 | |||||||

| General and administrative | 14,925 | 19,868 | |||||||||

| Depreciation and amortization | 72,933 | 86,740 | |||||||||

| Other expenses | 102 | 2,239 | |||||||||

| Interest expense | 26,600 | 27,288 | |||||||||