| FEES AND EXPENSES | LOCATION IN PROSPECTUS | |

| Charges for Early Withdrawals | If you fully surrender your Policy within the first 10 years of Policy issue or any Basic Life Coverage Layer added to the Policy (each Basic Life Coverage Layer will have its own 10-year period from the date it went into effect) you will be assessed a surrender charge of up to a maximum of 5.722% ($57.22) per $1,000 of Basic Face Amount plus any face amount added at Policy issue by the Annual Renewable Term Rider. This charge will vary based on the individual characteristics of the Insured and other options chosen. For example, if you fully surrender your Policy within the first 10 years of Policy issue, you could pay a surrender charge up to $5,722 on a $100,000 of Basic Face Amount. | Fee Tables Surrendering Your Policy |

| Transaction Charges | In addition to Surrender Charges, you may also be charged for other transactions. These other charges may include charges for each premium paid, withdrawal charges for partial withdrawals, transfer fees for transfers among the Investment Options, fees for Illustration requests, unscheduled face amount increases for certain riders, and for requests to increase | Fee Tables Deductions From Your Premiums |

| FEES AND EXPENSES | LOCATION IN PROSPECTUS | |||

| or exercise certain benefits under an optional rider. | Making Withdrawals | |||

| Ongoing Fees and Expenses (annual charges) | In addition to Surrender Charges and transaction charges, an investment in the Policy is subject to certain ongoing fees and expenses, including fees and expenses covering the cost of insurance under the Policy, administrative charges, asset charges, Coverage charges, interest on any Policy loans, and the cost of optional benefits available under the Policy. Certain fees and expenses are set based on characteristics of the Insured (e.g. age, sex, and rating classification). Please review the Policy Specifications page of your Policy for rates applicable to your Policy. You will also bear expenses associated with the Funds you choose under the Policy, as shown in the following table: | Fee Tables Monthly Deductions Appendix: Funds Available Under the Policy | ||

| ANNUAL FEE | MINIMUM | MAXIMUM | ||

| Variable Investment Options (Fund fees and expenses) | 0.09%1 | 1.10%1 | ||

1 As a percentage of Fund net assets.

If you fully surrender your Policy within the first 10 years of Policy issue or any Basic Life Coverage Layer added to the Policy (each Basic Life Coverage Layer will have its own 10-year period from the date it went into effect) you will be assessed a surrender charge of up to a maximum of 5.722% ($57.22) per $1,000 of Basic Face Amount plus any face amount added at Policy issue by the Annual Renewable Term Rider. This charge will vary based on the individual characteristics of the Insured and other options chosen.

For example, if you fully surrender your Policy within the first 10 years of Policy issue, you could pay a surrender charge up to $5,722 on a $100,000 of Basic Face Amount.

Fee Tables

Surrendering Your Policy

In addition to Surrender Charges, you may also be charged for other transactions. These other charges may include charges for each premium paid, withdrawal charges for partial withdrawals, transfer fees for transfers among the Investment Options, fees for Illustration requests, unscheduled face amount increases for certain riders, and for requests to increase

Fee Tables

Deductions From Your Premiums

or exercise certain benefits under an optional rider.Making Withdrawals

In addition to Surrender Charges and transaction charges, an investment in the Policy is subject to certain ongoing fees and expenses, including fees and expenses covering the cost of insurance under the Policy, administrative charges, asset charges, Coverage charges, interest on any Policy loans, and the cost of optional benefits available under the Policy. Certain fees and expenses are set based on characteristics of the Insured (e.g. age, sex, and rating classification). Please review the Policy Specifications page of your Policy for rates applicable to your Policy.

You will also bear expenses associated with the Funds you choose under the Policy, as shown in the following table:

Fee Tables

Monthly Deductions

Appendix: Funds Available Under the Policy

ANNUAL FEE

MINIMUM

MAXIMUM

Variable Investment Options (Fund fees and expenses)

0.09%1

1.10%1

1 As a percentage of Fund net assets.

| RISKS | LOCATION IN PROSPECTUS | |

| Risk of Loss | You can lose money by investing in the Policy, including loss of principal and any prior earnings. | Principal Risks of Investing in the Policy |

| Not a Short-Term Investment | This Policy is not a short-term investment and is not appropriate for an investor who needs ready access to cash. The Policy is designed to provide a Death Benefit. This Policy may not be the right kind of policy if you plan to withdraw money or surrender your Policy for short-term needs. Withdrawals are not allowed in the first Policy Year. Surrender charges apply for up to 10 years after Policy issue and each Basic Life Coverage Layer added to the Policy. A surrender and withdrawal may be subject to negative tax consequences. If there is a reduction in the Face Amount of a Basic Life Coverage layer, including decreases due to withdrawals, the surrender charge for the effected Basic Life Coverage Layer will not change. | Principal Risks of Investing in the Policy Surrendering Your Policy |

| Risks Associated with Investment Options | An investment in this Policy is subject to the risk of poor investment performance and can vary depending on the performance of the Investment Options available under the Policy (e.g. Funds). Each Investment Option (including any Fixed Option or Indexed Fixed Option) will have its own unique risks. The Fixed Options and Indexed Fixed Options are not registered with the SEC. You should review, working with your financial professional, the Investment Options before making an investment decision. | Principal Risks of Investing in the Policy Investment Options - Fixed Options Investment Options - Indexed Fixed Options Appendix: Funds Available Under the Policy |

| Insurance Company Risks | Investment in the Policy is subject to the risks related to us, and any obligations (including any Fixed Option or Indexed Fixed Option), guarantees, or benefits are subject to our claims-paying ability. If we experience financial distress, we may not be able to meet our obligations to you. More information about us, including our financial strength ratings, is available upon request by calling us at (800) 347-7787 or visiting our website at www.PacificLife.com. | Principal Risks of Investing in the Policy About Pacific Life |

| Policy Lapse | Your Policy remains In Force as long as you have sufficient Net Accumulated Value to cover your Policy’s Monthly Deductions of Policy charges. Insufficient premium payments, poor investment performance, withdrawals, and unpaid loans or loan interest may cause your Policy to lapse – which means no Death Benefit will be paid. There are costs associated with reinstating a lapsed Policy and there is no guarantee that a reinstatement will be approved. | Principal Risks of Investing in the Policy Lapsing and Reinstatement |

Not all Investment Options may be available through your financial professional.

Transfers between Investment Options are generally limited to 25 each calendar year. Any transfers to or from the Fixed Account or Fixed LT Account will be counted towards the 25 allowed each calendar year unless part of a transfer program (for example, the first year transfer service) or the transfer is from the Fixed Account to an Indexed Fixed Option. Transfers to or from a Variable Investment Option cannot be made before the seventh calendar day following the last transfer to or from the same Variable Investment Option. Additional Fund transfer restrictions apply. There is a $25 fee per transfer in excess of 12 transfers per Policy Year. We do not currently impose this charge.

Under the Fixed Options, there are frequency, amount and/or percentage limits on the amount that may be transferred into or out of the Fixed Options. These limits are significantly more restrictive than those that apply to transfers into or out of the Variable Investment Options. It may take several Policy Years to transfer your Accumulated Value out of either of the Fixed Options to the Variable Investment Options. Additional Fixed Option transfer restrictions apply.

Under the Indexed Fixed Options, once a Segment is created, you cannot transfer out of a Segment until the end of the Segment Term. Money may be transferred from a Segment for withdrawals and Standard Policy Loans, however, if the withdrawal or loan was not part of a systematic distribution program, you will not be able to transfer into an Indexed Fixed Option for a 12-month period. Additional Indexed Fixed Option transfer restrictions apply.

Certain Funds may stop accepting additional investments into their Fund or may liquidate a Fund. In addition, if a Fund determines that excessive trading has occurred, they may limit your ability to continue to invest in their Fund for a certain period of time.

We reserve the right to remove, close to new investment, or substitute Funds as Investment Options. We reserve the right to add, remove, or change Fixed Options, Indexed Fixed Options, and Variable Investment Options.

Certain Investment Options described in this Prospectus may not be available depending on the broker-dealer through which the Policy is sold.

Transferring Among Investment Options and Market-Timing Restrictions

Transfer Services

Loans

Indexed Fixed Options

Appendix: Funds Available Under the Policy

Appendix: Financial Intermediary Variations

We offer several optional benefits in the form of a rider to the Policy. These riders can only be selected at Policy issue, may have an additional charge and could be subject to conditions to exercise or underwriting. Your selection of certain optional Riders may result in restrictions on some Policy benefits. Not all riders are available in every state. We may stop offering an optional benefit at any time for new Policy purchases. If you purchased the Flexible Duration No-Lapse Guarantee Rider, at initial purchase and during the entire time that you own this Rider, you must allocate 100% of the Accumulated Value among the allowable Investment Options as indicated under the APPENDIX: FUNDS AVAILABLE UNDER THIS POLICY – Allowable Investment Options section in this prospectus.

Certain Policy features and benefits described in this Prospectus may vary or may not be available depending on the broker-dealer through which your Policy was sold.

Optional Riders and Benefits

Appendix: Funds Available Under the Policy

Appendix: Financial Intermediary Variations

Consult with a tax professional to determine the tax implications of an investment in and payments received under the Policy. Withdrawals may be subject to ordinary income tax and may be subject to tax penalties. Tax consequences for loans and withdrawals generally differ. There is no additional tax benefit to you if the Policy is purchased through a tax-qualified plan.

Variable Life Insurance and Your Taxes

Some financial professionals may receive compensation for selling this Policy to you in the form of commissions, additional cash compensation, and non-cash compensation. We may also provide additional payments in the form of cash, other special compensation or reimbursement of expenses to the financial professional’s selling broker dealer. These financial professionals may have a financial incentive to offer or recommend this Policy over another investment.

Distribution Arrangements

Some financial professionals may have a financial incentive to offer you a new policy in place of the one you already own.

You should only exchange your policy if you determine, after comparing the features, fees, and risks of both policies, that it is preferable for you to purchase the new policy rather than continue to own the existing policy.

Policy Exchanges

Distribution Arrangements

FEE TABLES

The following tables describe the fees and expenses that you will pay when buying, owning, and surrendering or making withdrawals from the Policy. Please refer to your Policy Specifications page for information about the specific fees you will pay each year based on the options you have elected.

The first table describes the fees and expenses that you will pay at the time you buy the Policy, surrender or make withdrawals from the Policy, or transfer Accumulated Value between Investment Options.

| TRANSACTION FEES | ||

| CHARGE | WHEN CHARGE IS DEDUCTED | AMOUNT DEDUCTED |

| Maximum Sales Charge Imposed on Premiums (Load) | ||

| Basic premium load | Upon receipt of premium4 | 6.90% of basic premium |

| Surplus premium load | Upon receipt of premium that exceeds the Premium band amount4 | 20.00% of surplus premium |

| Internal premium load | Upon receipt of a replacement or conversion of a policy you have with us4 | 6.90% of internal premium |

| Maximum Surrender Charge1 | Upon full surrender of the Policy a Surrender Charge applies for 10 years from each Basic Life Coverage Layer2. | $57.22 per $1,000 of Basic Face Amount plus at issue Annual Renewable Term Rider Face Amount |

| Withdrawal charge (including any withdrawals under the Automated Income Program)3 | Upon partial withdrawal of Accumulated Value | $25 per withdrawal |

| Transfer fees3 | Upon transfer of Accumulated Value between Investment Options | $25 per transfer in excess of 12 per Policy Year |

| Illustration request3 | Upon request of Policy Illustration in excess of 1 per year | $25 per request |

| Annual Renewable Term Rider (Unscheduled Face Amount increase)3 | Upon effective date of requested Face Amount increase | $100 per request |

| Annual Renewable Term Rider – Additional Insured3 | Upon effective date of the addition of a covered person | $100 per request |

| Terminal Illness Rider Processing Charge3 | Upon approval of specific request | $100 per request |

| Overloan Protection 3 Rider | ||

| Minimum and Maximum guaranteed charge | At exercise of benefit | 1.12%–4.52% of Accumulated Value on date of exercise5 |

| Charge for a representative Insured | Maximum guaranteed charge for a male standard non-smoker or standard non tobacco who exercises the Rider at Age 85 is 2.97% of Accumulated Value on date of exercise6 | |

1 The Surrender Charge is based on the Age and Risk Class of the Insured, the Face Amount of the effected Coverage Layer(s), as well as the Death Benefit Option you choose. If there is a reduction in the Face Amount of a Basic Life Coverage Layer, including decreases due to withdrawals, the Surrender Charge for the effected Basic Life Coverage Layer will not change. The Surrender Charge reduces to $0 after 10 years from the effective date of each Coverage Layer. The Surrender Charge shown in the table may not be typical of the Surrender Charge you will pay. Ask your life insurance producer for information on this charge for your Policy. The Surrender Charge for your Policy will be stated in the Policy Specifications.

2 While there is no surrender charge on Annual Renewable Term Rider Coverage, the at-issue Annual Renewable Term Rider Coverage layer Face Amount is used in the calculation of the initial surrender charge. Each Basic Face Amount increase will have a corresponding Surrender Charge related to the amount of the increase and will be apply for 10 years from Coverage Layer issue. Annual Renewable Term Rider Face Amount increases will not have a corresponding Surrender Charge.

3 We currently do not impose this charge.

4 If an internal transfer occurs between two variable universal life policies you have with us in connection with a transfer or exchange offer by Pacific Life or Pacific Select Distributors, LLC (our distributor), including pursuant to a conversion or split option rider, the amount transferred will not incur any Premium Load (which includes basic, surplus, and internal premium loads). Premium loads will apply (basic and surplus) on new Policy for additional premium added at issue or after the initial premium paid. In addition, the internal transfer will not incur a Surrender Charge on any amount transferred from the old policy to purchase the new policy. Any Surrender Charge applicable to the new policy will continue to apply under the terms of the new policy.

5 The charge to exercise the Overloan Protection 3 Rider is shown as a table in your Policy Specifications. The charge varies by the Insured’s sex, Risk Class and Age at the time the Rider is exercised. For more information on this Rider, see the WITHDRAWALS, SURRENDERS AND LOANS – Overloan Protection 3 Rider section in this prospectus.

6 Charges shown for the representative Insured may not be typical of the charges you will pay.

We offer different underwriting methods such as guaranteed issue, simplified issue, or regular issue. The cost of insurance rates is generally higher if guaranteed issue or simplified issue are used, than if the Policy is issued through regular underwriting. As a result, a healthy individual who uses regular issue for the Policy may be subject to lower cost of insurance rates than if the individual uses guaranteed or simplified issue.

The next table describes the fees and expenses that you will pay periodically during the time you own the Policy, not including Fund fees and expenses.

| PERIODIC CHARGES OTHER THAN FUND OPERATING EXPENSES | ||

| CHARGE | WHEN CHARGE IS DEDUCTED | AMOUNT DEDUCTED |

| Base Policy Charges: | ||

| Cost of Insurance1,2 | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Net Amount At Risk |

| Minimum and Maximum current charge | $0.01–$83.34 per $1,000 of Net Amount At Risk | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 Current charge during Policy Year 1 is $0.08 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | |

| Administrative charge1 | ||

| Maximum guaranteed and current charge | Monthly Payment Date | $10.00 |

| Asset charge1 | ||

| Maximum guaranteed charge Current charge | Monthly Payment Date | Maximum guaranteed charge is 0.36% annually (0.03% monthly) of unloaned Accumulated Value Current charge is 0.15% annually (0.0125% monthly) of unloaned Accumulated Value |

| Indexed Fixed Option charge1 Maximum guaranteed charge Current charge | Monthly Payment Date | Maximum guaranteed charge is 3% annually (0.25% monthly) of Accumulated Value allocated to the 1-Year High Cap Plus Indexed Account) Current charge is 3% annually (0.25% monthly) of Accumulated Value allocated to the 1-Year High Cap Plus Indexed Account) |

| Coverage charge1,4 | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date, beginning on effective date of each Basic Life Coverage Layer | $24.50 per Policy8 plus $0.12–$11.62 per $1,000 of Basic Life Coverage Layer |

| Minimum and Maximum current charges | $24.50 per Policy8 plus $0.00–$5.25 per $1,000 of Basic Life Coverage Layer, multiplied by a Coverage Charge Factor of 0% to 100% | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $24.50 per Policy9 plus $0.88 per $1,000 of Basic Life Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue, with Death Benefit Option A3. Current charge during Policy Year 1 is $24.50 per Policy9 plus $0.80 per $1,000 of Basic Life Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue, with Death Benefit Option A3 | |

| Optional Benefit Charges7: | ||

| Standard Loan interest charge | ||

| Maximum guaranteed and current charge | Policy Anniversary | 2.25% of Policy’s Standard Loan Account balance annually5 |

| Alternate Loan Rider 2 Interest charge | ||

| Maximum guaranteed charge | Policy Anniversary | Maximum guaranteed rate is 7.50% (0.625% monthly) of the Alternate Loan Value balance annually6 |

| Annual Renewable Term Rider | ||

| Cost of Insurance1,2 | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Net Amount At Risk |

| Minimum and Maximum current charges | $0.01–$83.34 per $1,000 of Net Amount At Risk | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker who is Age 45 at Policy issue3 | |

| Current charge during Policy Year 1 is $0.08 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Coverage charge1,4,9 | ||

| Minimum and Maximum guaranteed charge Minimum and Maximum current charges | Monthly Payment Date | $0.13–$12.20 per $1,000 of Rider Coverage Layer $0.00–$1.73 per $1,000 of Rider Coverage Layer |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.93 per $1,000 of Rider Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue with Death Benefit Option A3 Current charge during Policy Year 1 is $0.09 per $1,000 of Rider Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue with Death Benefit Option A3 | |

| Flexible Duration No-Lapse Guarantee Rider | ||

| Minimum and Maximum guaranteed charge Minimum and Maximum current charge | Monthly Payment Date | $0.01–$0.33 per $1,000 of Net Amount of Risk $0.01–$0.33 per $1,000 of Net Amount of Risk |

| Charge for a representative Insured | Maximum guaranteed and current charge is $0.03 per $1,000 of Net Amount At Risk at the end of Policy Year 1 for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | |

| Scheduled Annual Renewable Term Rider | ||

| Cost of Insurance1,2 | ||

| Minimum and Maximum guaranteed charge Minimum and Maximum current charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Net Amount At Risk $0.01–$83.34 per $1,000 of Net Amount At Risk |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker who is Age 45 at Policy issue3 | |

| Current charge during Policy Year 1 is $0.03 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Coverage charge1,4 Minimum and Maximum guaranteed charge Minimum and Maximum current charges | $0.13–$12.20 per $1,000 of Rider Coverage Layer The current Coverage charge for this Rider is $0.00 | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.93 per $1,000 of Rider Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue with Death Benefit Option A3 | |

| Annual Renewable Term Rider–Additional Insured | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Rider Face Amount |

| Minimum and Maximum current charge | $0.01–$83.34 per $1,000 of Rider Face Amount | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.12 per |

| $1,000 of Rider Face Amount for a female standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Current charge during Policy Year 1 is $0.03 per $1,000 of Rider Face Amount for a female standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Premier LTC Rider | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.02–$1.87 per $1,000 of LTC Net Amount At Risk |

| Minimum and Maximum current charge | $0.01–$1.15 per $1,000 of LTC Net Amount At Risk | |

| Charge for a representative Insured | Maximum guaranteed charge is $0.20 per $1,000 of LTC NAR for a male, who is Age 45 at Policy Issue3 Current charge is $0.07 per $1,000 of LTC NAR for a single male, who is Age 45 at Policy Issue with a 2.0% benefit3 |

1 The charge is not deducted on and after your Policy’s Monthly Deduction End Date.

2 Cost of insurance rates apply uniformly to all members of the same Class and vary based on Age, sex, and Risk Class of the Insured. The cost of insurance charges shown in the table may not be typical of the charges you will pay. Your Policy Specifications will indicate the guaranteed cost of insurance charge applicable to your Policy, and more detailed information concerning your cost of insurance charges is available on request from your life insurance producer or us. Also, before you purchase the Policy, you may request personalized Illustrations. Cost of insurance rates for your Policy will be stated in the Policy Specifications and calculated using the Net Amount At Risk.

3 Charges shown for the representative Insured may not be typical of the charges you will pay.

4 The Coverage charge rate is based on the Age, sex, and Risk Class of the Insured on the Policy Date or date Rider is effective. It also varies with the Death Benefit Option you choose. Each Coverage Layer will have a corresponding Coverage charge related to the amount of the increase, based on the Age and Risk Class of the Insured at the time of the increase. A decrease in Face Amount will not decrease the applicable Coverage charge for any Coverage Layer. . If there is a reduction in the Face Amount of a Basic Life Coverage Layer, including decreases for any withdrawals, the Coverage charge for the effected Basic Life Coverage Layer will not change. For the current Coverage charge, we use a Coverage Charge Factor which may reduce the amount charged and varies by Policy duration. Ask your life insurance producer for information regarding this charge for your Policy. The Coverage charge for your Policy and the Coverage charge schedule will be stated in the Policy Specifications.

5 In addition to the Standard Loan interest charge, the Standard Loan Account Value that is used to secure Standard Policy Debt will be credited interest at a minimum of 2.00% to help offset the Standard Loan interest charge of 2.25%. Standard Loan interest on the Standard Loan Account and Standard Policy Debt accrues daily and any Standard Loan interest that has accrued is due on each Policy Anniversary. Any unpaid Standard Loan interest on each Policy Anniversary will be added to the Standard Loan Account. On each Policy Anniversary, we transfer the excess of the Standard Policy Debt over Standard Loan Account Value from the Investment Options to the Standard Loan Account. If the Standard Loan Account Value is greater than Standard Policy Debt, then such excess is transferred from the Standard Loan Account to the Variable Options or the Fixed Account on a proportionate basis according to your most recent allocation instructions.

6 There is no credited interest on the Alternate Loan Value balance (the amount used to secure the alternate loan); the amount to secure the loan remains in eligible Indexed Accounts (also called Designated Accounts).

7 Riders are described under the OPTIONAL RIDERS AND BENEFITS section in this prospectus. Rider charges are based on the Age and Risk Class (the Overloan Protection 3 Rider also uses sex as a factor) of the person Insured under the Rider on the effective date of the Rider. Ask your life insurance producer for information on optional Rider charges for your Policy. The charges for any optional benefit Riders you add to your Policy will be stated in the Policy Specifications.

8 This charge ($24.50 per Policy) applies to the initial Basic Life Coverage Layer only and is not assessed against any additional Basic Life Coverage Layer.

9 A decrease in Face Amount will not decrease its Coverage charge because the Coverage charge is based on the Coverage Layer at issue and the charge is used to recover the expense of issuing the insurance coverage.

The next item shows the minimum and maximum total operating expenses charged by the Fund that you pay periodically during the time that you own the Policy. A complete list of Funds available under the Policy, including their annual expenses, may be found at the back of this document in the APPENDIX: FUNDS AVAILABLE UNDER THE POLICY.

Annual Fund Expenses

| Minimum | Maximum | |||

| Expenses that are deducted from Fund assets, including management fees, distribution and/or service (12b-1) fees, and other expenses. | 0.09% | 1.10% |

| TRANSACTION FEES | ||

| CHARGE | WHEN CHARGE IS DEDUCTED | AMOUNT DEDUCTED |

| Maximum Sales Charge Imposed on Premiums (Load) | ||

| Basic premium load | Upon receipt of premium4 | 6.90% of basic premium |

| Surplus premium load | Upon receipt of premium that exceeds the Premium band amount4 | 20.00% of surplus premium |

| Internal premium load | Upon receipt of a replacement or conversion of a policy you have with us4 | 6.90% of internal premium |

| Maximum Surrender Charge1 | Upon full surrender of the Policy a Surrender Charge applies for 10 years from each Basic Life Coverage Layer2. | $57.22 per $1,000 of Basic Face Amount plus at issue Annual Renewable Term Rider Face Amount |

| Withdrawal charge (including any withdrawals under the Automated Income Program)3 | Upon partial withdrawal of Accumulated Value | $25 per withdrawal |

| Transfer fees3 | Upon transfer of Accumulated Value between Investment Options | $25 per transfer in excess of 12 per Policy Year |

| Illustration request3 | Upon request of Policy Illustration in excess of 1 per year | $25 per request |

| Annual Renewable Term Rider (Unscheduled Face Amount increase)3 | Upon effective date of requested Face Amount increase | $100 per request |

| Annual Renewable Term Rider – Additional Insured3 | Upon effective date of the addition of a covered person | $100 per request |

| Terminal Illness Rider Processing Charge3 | Upon approval of specific request | $100 per request |

| Overloan Protection 3 Rider | ||

| Minimum and Maximum guaranteed charge | At exercise of benefit | 1.12%–4.52% of Accumulated Value on date of exercise5 |

| Charge for a representative Insured | Maximum guaranteed charge for a male standard non-smoker or standard non tobacco who exercises the Rider at Age 85 is 2.97% of Accumulated Value on date of exercise6 | |

1 The Surrender Charge is based on the Age and Risk Class of the Insured, the Face Amount of the effected Coverage Layer(s), as well as the Death Benefit Option you choose. If there is a reduction in the Face Amount of a Basic Life Coverage Layer, including decreases due to withdrawals, the Surrender Charge for the effected Basic Life Coverage Layer will not change. The Surrender Charge reduces to $0 after 10 years from the effective date of each Coverage Layer. The Surrender Charge shown in the table may not be typical of the Surrender Charge you will pay. Ask your life insurance producer for information on this charge for your Policy. The Surrender Charge for your Policy will be stated in the Policy Specifications.

2 While there is no surrender charge on Annual Renewable Term Rider Coverage, the at-issue Annual Renewable Term Rider Coverage layer Face Amount is used in the calculation of the initial surrender charge. Each Basic Face Amount increase will have a corresponding Surrender Charge related to the amount of the increase and will be apply for 10 years from Coverage Layer issue. Annual Renewable Term Rider Face Amount increases will not have a corresponding Surrender Charge.

3 We currently do not impose this charge.

4 If an internal transfer occurs between two variable universal life policies you have with us in connection with a transfer or exchange offer by Pacific Life or Pacific Select Distributors, LLC (our distributor), including pursuant to a conversion or split option rider, the amount transferred will not incur any Premium Load (which includes basic, surplus, and internal premium loads). Premium loads will apply (basic and surplus) on new Policy for additional premium added at issue or after the initial premium paid. In addition, the internal transfer will not incur a Surrender Charge on any amount transferred from the old policy to purchase the new policy. Any Surrender Charge applicable to the new policy will continue to apply under the terms of the new policy.

5 The charge to exercise the Overloan Protection 3 Rider is shown as a table in your Policy Specifications. The charge varies by the Insured’s sex, Risk Class and Age at the time the Rider is exercised. For more information on this Rider, see the WITHDRAWALS, SURRENDERS AND LOANS – Overloan Protection 3 Rider section in this prospectus.

6 Charges shown for the representative Insured may not be typical of the charges you will pay.

| PERIODIC CHARGES OTHER THAN FUND OPERATING EXPENSES | ||

| CHARGE | WHEN CHARGE IS DEDUCTED | AMOUNT DEDUCTED |

| Base Policy Charges: | ||

| Cost of Insurance1,2 | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Net Amount At Risk |

| Minimum and Maximum current charge | $0.01–$83.34 per $1,000 of Net Amount At Risk | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 Current charge during Policy Year 1 is $0.08 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | |

| Administrative charge1 | ||

| Maximum guaranteed and current charge | Monthly Payment Date | $10.00 |

| Asset charge1 | ||

| Maximum guaranteed charge Current charge | Monthly Payment Date | Maximum guaranteed charge is 0.36% annually (0.03% monthly) of unloaned Accumulated Value Current charge is 0.15% annually (0.0125% monthly) of unloaned Accumulated Value |

| Indexed Fixed Option charge1 Maximum guaranteed charge Current charge | Monthly Payment Date | Maximum guaranteed charge is 3% annually (0.25% monthly) of Accumulated Value allocated to the 1-Year High Cap Plus Indexed Account) Current charge is 3% annually (0.25% monthly) of Accumulated Value allocated to the 1-Year High Cap Plus Indexed Account) |

| Coverage charge1,4 | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date, beginning on effective date of each Basic Life Coverage Layer | $24.50 per Policy8 plus $0.12–$11.62 per $1,000 of Basic Life Coverage Layer |

| Minimum and Maximum current charges | $24.50 per Policy8 plus $0.00–$5.25 per $1,000 of Basic Life Coverage Layer, multiplied by a Coverage Charge Factor of 0% to 100% | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $24.50 per Policy9 plus $0.88 per $1,000 of Basic Life Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue, with Death Benefit Option A3. Current charge during Policy Year 1 is $24.50 per Policy9 plus $0.80 per $1,000 of Basic Life Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue, with Death Benefit Option A3 | |

| Optional Benefit Charges7: | ||

| Standard Loan interest charge | ||

| Maximum guaranteed and current charge | Policy Anniversary | 2.25% of Policy’s Standard Loan Account balance annually5 |

| Alternate Loan Rider 2 Interest charge | ||

| Maximum guaranteed charge | Policy Anniversary | Maximum guaranteed rate is 7.50% (0.625% monthly) of the Alternate Loan Value balance annually6 |

| Annual Renewable Term Rider | ||

| Cost of Insurance1,2 | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Net Amount At Risk |

| Minimum and Maximum current charges | $0.01–$83.34 per $1,000 of Net Amount At Risk | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker who is Age 45 at Policy issue3 | |

| Current charge during Policy Year 1 is $0.08 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Coverage charge1,4,9 | ||

| Minimum and Maximum guaranteed charge Minimum and Maximum current charges | Monthly Payment Date | $0.13–$12.20 per $1,000 of Rider Coverage Layer $0.00–$1.73 per $1,000 of Rider Coverage Layer |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.93 per $1,000 of Rider Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue with Death Benefit Option A3 Current charge during Policy Year 1 is $0.09 per $1,000 of Rider Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue with Death Benefit Option A3 | |

| Flexible Duration No-Lapse Guarantee Rider | ||

| Minimum and Maximum guaranteed charge Minimum and Maximum current charge | Monthly Payment Date | $0.01–$0.33 per $1,000 of Net Amount of Risk $0.01–$0.33 per $1,000 of Net Amount of Risk |

| Charge for a representative Insured | Maximum guaranteed and current charge is $0.03 per $1,000 of Net Amount At Risk at the end of Policy Year 1 for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | |

| Scheduled Annual Renewable Term Rider | ||

| Cost of Insurance1,2 | ||

| Minimum and Maximum guaranteed charge Minimum and Maximum current charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Net Amount At Risk $0.01–$83.34 per $1,000 of Net Amount At Risk |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker who is Age 45 at Policy issue3 | |

| Current charge during Policy Year 1 is $0.03 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Coverage charge1,4 Minimum and Maximum guaranteed charge Minimum and Maximum current charges | $0.13–$12.20 per $1,000 of Rider Coverage Layer The current Coverage charge for this Rider is $0.00 | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.93 per $1,000 of Rider Coverage Layer for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue with Death Benefit Option A3 | |

| Annual Renewable Term Rider–Additional Insured | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.01–$83.34 per $1,000 of Rider Face Amount |

| Minimum and Maximum current charge | $0.01–$83.34 per $1,000 of Rider Face Amount | |

| Charge for a representative Insured | Maximum guaranteed charge during Policy Year 1 is $0.12 per |

| $1,000 of Rider Face Amount for a female standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Current charge during Policy Year 1 is $0.03 per $1,000 of Rider Face Amount for a female standard non-smoker or standard non tobacco who is Age 45 at Policy issue3 | ||

| Premier LTC Rider | ||

| Minimum and Maximum guaranteed charge | Monthly Payment Date | $0.02–$1.87 per $1,000 of LTC Net Amount At Risk |

| Minimum and Maximum current charge | $0.01–$1.15 per $1,000 of LTC Net Amount At Risk | |

| Charge for a representative Insured | Maximum guaranteed charge is $0.20 per $1,000 of LTC NAR for a male, who is Age 45 at Policy Issue3 Current charge is $0.07 per $1,000 of LTC NAR for a single male, who is Age 45 at Policy Issue with a 2.0% benefit3 |

1 The charge is not deducted on and after your Policy’s Monthly Deduction End Date.

2 Cost of insurance rates apply uniformly to all members of the same Class and vary based on Age, sex, and Risk Class of the Insured. The cost of insurance charges shown in the table may not be typical of the charges you will pay. Your Policy Specifications will indicate the guaranteed cost of insurance charge applicable to your Policy, and more detailed information concerning your cost of insurance charges is available on request from your life insurance producer or us. Also, before you purchase the Policy, you may request personalized Illustrations. Cost of insurance rates for your Policy will be stated in the Policy Specifications and calculated using the Net Amount At Risk.

3 Charges shown for the representative Insured may not be typical of the charges you will pay.

4 The Coverage charge rate is based on the Age, sex, and Risk Class of the Insured on the Policy Date or date Rider is effective. It also varies with the Death Benefit Option you choose. Each Coverage Layer will have a corresponding Coverage charge related to the amount of the increase, based on the Age and Risk Class of the Insured at the time of the increase. A decrease in Face Amount will not decrease the applicable Coverage charge for any Coverage Layer. . If there is a reduction in the Face Amount of a Basic Life Coverage Layer, including decreases for any withdrawals, the Coverage charge for the effected Basic Life Coverage Layer will not change. For the current Coverage charge, we use a Coverage Charge Factor which may reduce the amount charged and varies by Policy duration. Ask your life insurance producer for information regarding this charge for your Policy. The Coverage charge for your Policy and the Coverage charge schedule will be stated in the Policy Specifications.

5 In addition to the Standard Loan interest charge, the Standard Loan Account Value that is used to secure Standard Policy Debt will be credited interest at a minimum of 2.00% to help offset the Standard Loan interest charge of 2.25%. Standard Loan interest on the Standard Loan Account and Standard Policy Debt accrues daily and any Standard Loan interest that has accrued is due on each Policy Anniversary. Any unpaid Standard Loan interest on each Policy Anniversary will be added to the Standard Loan Account. On each Policy Anniversary, we transfer the excess of the Standard Policy Debt over Standard Loan Account Value from the Investment Options to the Standard Loan Account. If the Standard Loan Account Value is greater than Standard Policy Debt, then such excess is transferred from the Standard Loan Account to the Variable Options or the Fixed Account on a proportionate basis according to your most recent allocation instructions.

6 There is no credited interest on the Alternate Loan Value balance (the amount used to secure the alternate loan); the amount to secure the loan remains in eligible Indexed Accounts (also called Designated Accounts).

7 Riders are described under the OPTIONAL RIDERS AND BENEFITS section in this prospectus. Rider charges are based on the Age and Risk Class (the Overloan Protection 3 Rider also uses sex as a factor) of the person Insured under the Rider on the effective date of the Rider. Ask your life insurance producer for information on optional Rider charges for your Policy. The charges for any optional benefit Riders you add to your Policy will be stated in the Policy Specifications.

8 This charge ($24.50 per Policy) applies to the initial Basic Life Coverage Layer only and is not assessed against any additional Basic Life Coverage Layer.

9 A decrease in Face Amount will not decrease its Coverage charge because the Coverage charge is based on the Coverage Layer at issue and the charge is used to recover the expense of issuing the insurance coverage.

Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue3

Current charge during Policy Year 1 is $0.08 per $1,000 of Net Amount At Risk for a male standard non-smoker or standard non tobacco who is Age 45 at Policy issue1 The charge is not deducted on and after your Policy’s Monthly Deduction End Date.

2 Cost of insurance rates apply uniformly to all members of the same Class and vary based on Age, sex, and Risk Class of the Insured. The cost of insurance charges shown in the table may not be typical of the charges you will pay. Your Policy Specifications will indicate the guaranteed cost of insurance charge applicable to your Policy, and more detailed information concerning your cost of insurance charges is available on request from your life insurance producer or us. Also, before you purchase the Policy, you may request personalized Illustrations. Cost of insurance rates for your Policy will be stated in the Policy Specifications and calculated using the Net Amount At Risk.

3 Charges shown for the representative Insured may not be typical of the charges you will pay.

4 The Coverage charge rate is based on the Age, sex, and Risk Class of the Insured on the Policy Date or date Rider is effective. It also varies with the Death Benefit Option you choose. Each Coverage Layer will have a corresponding Coverage charge related to the amount of the increase, based on the Age and Risk Class of the Insured at the time of the increase. A decrease in Face Amount will not decrease the applicable Coverage charge for any Coverage Layer. . If there is a reduction in the Face Amount of a Basic Life Coverage Layer, including decreases for any withdrawals, the Coverage charge for the effected Basic Life Coverage Layer will not change. For the current Coverage charge, we use a Coverage Charge Factor which may reduce the amount charged and varies by Policy duration. Ask your life insurance producer for information regarding this charge for your Policy. The Coverage charge for your Policy and the Coverage charge schedule will be stated in the Policy Specifications.

5 In addition to the Standard Loan interest charge, the Standard Loan Account Value that is used to secure Standard Policy Debt will be credited interest at a minimum of 2.00% to help offset the Standard Loan interest charge of 2.25%. Standard Loan interest on the Standard Loan Account and Standard Policy Debt accrues daily and any Standard Loan interest that has accrued is due on each Policy Anniversary. Any unpaid Standard Loan interest on each Policy Anniversary will be added to the Standard Loan Account. On each Policy Anniversary, we transfer the excess of the Standard Policy Debt over Standard Loan Account Value from the Investment Options to the Standard Loan Account. If the Standard Loan Account Value is greater than Standard Policy Debt, then such excess is transferred from the Standard Loan Account to the Variable Options or the Fixed Account on a proportionate basis according to your most recent allocation instructions.

6 There is no credited interest on the Alternate Loan Value balance (the amount used to secure the alternate loan); the amount to secure the loan remains in eligible Indexed Accounts (also called Designated Accounts).

7 Riders are described under the OPTIONAL RIDERS AND BENEFITS section in this prospectus. Rider charges are based on the Age and Risk Class (the Overloan Protection 3 Rider also uses sex as a factor) of the person Insured under the Rider on the effective date of the Rider. Ask your life insurance producer for information on optional Rider charges for your Policy. The charges for any optional benefit Riders you add to your Policy will be stated in the Policy Specifications.

8 This charge ($24.50 per Policy) applies to the initial Basic Life Coverage Layer only and is not assessed against any additional Basic Life Coverage Layer.

9 A decrease in Face Amount will not decrease its Coverage charge because the Coverage charge is based on the Coverage Layer at issue and the charge is used to recover the expense of issuing the insurance coverage.

Annual Fund Expenses

| Minimum | Maximum | |||

| Expenses that are deducted from Fund assets, including management fees, distribution and/or service (12b-1) fees, and other expenses. | 0.09% | 1.10% |

PRINCIPAL RISKS OF INVESTING IN THE POLICY

Risk of Loss

You can lose money by investing in this Policy, including loss of principal and any prior earnings. The Policy is not a deposit or obligation of, or guaranteed or endorsed by any bank. It is not federally insured by the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board, or any other government agency.

Unsuitable as Short-Term Savings Vehicle (Surrender and Withdrawal Risk)

This Policy is not a short-term investment and is not appropriate for an investor who needs ready access to cash. The Policy is designed to provide a death benefit. The Policy may be inappropriate for you if you do not have the financial ability to keep it in force for a substantial period of time.

This Policy may not be the right kind of policy if you plan to withdraw money or surrender your Policy for short-term needs. A surrender will terminate the Policy and all of its benefits. Withdrawals cannot be taken until after first year of the Policy and may be subject to withdrawal charges. A withdrawal will reduce your Accumulated Value and may significantly reduce the value of the Death Benefit or benefit riders under the Policy, potentially by more than the amount withdrawn, and could even terminate a benefit rider. Withdrawals may also significantly increase the risk of lapse.

Surrender charges reduce the Cash Surrender Value of your Policy. Surrender charges apply for up to 10 years after Policy issue and each Basic Life Coverage Layer added to the Policy. A surrender and withdrawal may be subject to negative tax consequences. If there is a reduction in the Face Amount of a Basic Life Coverage layer, including decreases due to withdrawals, the surrender charge for the effected Basic Life Coverage Layer will not change.

Please discuss your insurance needs and financial objectives with your financial professional. Together you can decide if the Policy is right for you. We are a variable life insurance policy provider. We are not a fiduciary and therefore do not give advice or make recommendations regarding insurance or investment products.

Policy Lapse

Your Policy remains In Force as long as you have sufficient Net Accumulated Value to cover your Policy’s Monthly Deductions of Policy charges. Insufficient premium payments, fees and expenses, poor investment performance, withdrawals, and unpaid loans or loan interest may cause your Policy to lapse – which means no Death Benefit or other benefits will be paid. There are costs associated with reinstating a lapsed Policy. There is no guarantee that your Policy will not lapse even if you pay your planned premium. You should consider a periodic review of your coverage with your financial professional.

Before your Policy lapses, there is a Grace Period. The Grace Period gives you 61 days to pay enough additional premium to keep your Policy In Force and to prevent your Policy from lapsing. The 61-day period begins on the date we send notice that your Policy’s Accumulated Value less any Total Policy Debt is not enough to pay the total monthly charge.

The Policy may be eligible for the Short-Term No-Lapse Guarantee Rider that may help prevent the Policy from Lapsing. See the Short-Term No-Lapse Guarantee Rider in the OTHER BENEFITS AVAILABLE UNDER THE POLICY section in this prospectus.

If the Policy lapses, you have three years from the end of the Grace Period to apply for reinstatement. Evidence of insurability is required when you apply for reinstatement and there is no guarantee that reinstatement will be approved. The costs associated with reinstating a lapsed Policy include sufficient net premium to:

● cover all due and unpaid monthly deductions and loan interest charges that accrued during the Grace Period;

● keep the Policy in force for three months after the date of reinstatement, and

● cover any negative accumulated value if there was a policy loan or other outstanding debt at the time of lapse.

If the Policy is reinstated, the same Risk Class in use at the time of lapse will apply to the reinstated Policy.

Limitations on Access to Accumulated Value through Withdrawals

Withdrawals under the Policy are available starting on the first Policy Anniversary. Each withdrawal must be at least $200. We will not accept a withdrawal request if the withdrawal will cause the Policy to become a Modified Endowment Contract (MEC), unless you have told us In Writing that you desire to have your Policy become a MEC. See the Tax Implications section below for additional information on MECs.

Risks Associated with Variable Investment Options

You should consider the Policy’s Investment Options as well as its costs. Your investment is subject to the risk of poor investment performance and can vary depending on the performance of the Variable Investment Options you have chosen. Each Variable Investment Option will have its own unique risks. The value of each Variable Investment Option will fluctuate with the value of the investments it holds, and returns are not guaranteed. You can lose money by investing in the Policy, including loss of principal. You bear the risk of any Variable Investment Options you choose. You should read each Fund prospectus carefully before investing. You can obtain a Fund prospectus by contacting your financial professional or by visiting https://pacificlife.onlineprospectus.net/pacificlife/products/. No assurance can be given that a Fund will achieve its investment objectives.

Risks Associated with Policy Loans

When you borrow money from your Policy, we use your Policy’s Accumulated Value as security. You pay interest, which accrues at the Loan Account Charge Interest Rate, on the amount you borrow. Accrued interest is due on your Policy Anniversary. The Accumulated Value set aside to secure your loan is transferred to a Loan Account which earns interest daily at the Loan Account Credit Interest Rate. Taking out a loan, whether or not you repay it, will affect the growth of your Policy’s Accumulated Value since the amount used to secure the loan will not participate in the investment experience of the Investment Options, will not be available to pay any Policy charges, may increase the risk of the Policy lapsing, and could reduce the amount of the Death Benefit.

Risks Associated with Fixed Options

Under the Fixed Options, there are frequency, amount and/or percentage limits on how much may be transferred from the Fixed Options. These limits are significantly more restrictive than those that apply to transfers out of the Variable Investment Options and it may take several Policy Years to transfer your Accumulated Value out of either of the Fixed Options to Variable Investment Options. Such restrictions on transfers from the Fixed Options may prevent you from reallocating your Accumulated Value at the times and in the amounts that you desire and may result in lower investment performance than if you allocated to Variable Investment Options. See the YOUR INVESTMENT OPTIONS – Transferring Among Investment Options and Market-timing Restrictions section in this prospectus. We declare the annual interest rate for the Fixed Options at our discretion, subject to a guaranteed minimum interest rate. You bear the risk that we will not declare an interest rate greater than the guaranteed minimum.

Risks Associated with Indexed Fixed Options

The value of the Segments in each of the Indexed Fixed Options is based on the way we credit interest to a Segment. We add interest using Segment Index Interest which, in part, is based on any positive change in an external index. There is no guarantee that Segment Indexed Interest will be greater than zero, but it will never be negative. If the underlying Index remains level or declines over a prolonged period of time and we have not credited Segment Index Interest, you may need to increase premium payments to prevent the Policy from lapsing.

Once a Segment is created, you cannot transfer Accumulated Value out of that Segment until the end of the Segment Term. Money may be transferred out for withdrawals and Standard Policy Loans, however, a Lockout Period will apply if the withdrawal or Standard Loan is not part of a Systematic Distribution Program.

We manage our obligation to credit Segment Indexed Interest in part by purchasing call options on the Index and by prospectively adjusting the Participation Rate, Segment Adjustment Factor, and/or Growth Cap (or Indexed Threshold Rate for the 1-Year No Cap Indexed Account) on future Segments to reflect changes in the costs of purchasing such call options (the price of call options varies with market conditions). In certain cases, we may reduce the Participation Rate, Segment Adjustment Factor or the Growth Cap or increase the Indexed Threshold Rate for a future Segment. If we do so, the amount of the Segment Indexed Interest which you may otherwise have received would be reduced. However, we will not change any rates, caps or thresholds below any guaranteed rates.

There is no guarantee that the Index described in this Prospectus will be available during the entire time you own your Policy. If the Index is discontinued or we are unable to utilize it, we may substitute a successor index of our choosing. If we do so, the performance of the new index would differ from the Index. This, in turn, may affect the Segment Indexed Interest you earn. There is no guarantee that we will offer the Indexed Accounts during the entire time you own your Policy. We may discontinue offering one (or more) of the Indexed Accounts at any time. If we discontinue an Indexed Account, you may transfer Indexed Accumulated Value to any other available Indexed Account or to the Fixed Options consistent with your Policy’s investment and transfer restrictions at Segment Maturity. If you do not do so, your Indexed Accumulated Value will be reallocated to the Fixed Account.

An allocation to the Indexed Fixed Options is not equivalent to investing in the underlying stocks comprising the Index. You will have no ownership rights in the underlying stocks comprising the Index, such as voting rights, dividend payments, or other distributions. Also, we are not affiliated with the Index or the underlying stocks comprising the Index. Consequently, the Index and the issuers of the underlying stocks comprising the Index have no involvement with the Policy. The Index is a price return index and the performance of the Index does not include income from any dividends or other distributions paid by the Index’s component companies. If dividends and other distributions were included, the Index performance would be higher. For more information on “investor control” see the VARIABLE LIFE INSURANCE AND YOUR TAXES section in this prospectus and also the SAI.

Insurance Company Risks

Investment in the Policy is subject to the risks related to us, and any obligations (including under any Fixed Options or Indexed Fixed Options), guarantees, or benefits are backed by our claims paying ability and financial strength. You must look to our strength with regard to such guarantees.

Tax Implications

We believe the Policy meets the statutory definition of life insurance for federal income tax purposes. We do not know whether the current treatment of life insurance policies under current federal income tax, estate, or gift tax laws will continue. We also do not know if the current interpretations of the laws by the IRS or the courts will remain the same. Also, future legislation may adversely change the tax treatment of life insurance policies.

Death benefits from a life insurance policy may generally be excluded from income under the Tax Code. Also, you generally are not subject to taxation on any increase in the Accumulated Value until it is withdrawn. You may be subject to income tax if you take withdrawals or surrender your Policy, or if your Policy lapses and you have not repaid any outstanding Total Policy Debt. If your Policy becomes a MEC, distributions you receive beginning on the date the Policy becomes a MEC may be subject to tax and a 10% penalty.

Cybersecurity and Business Continuity Risks

Our business relies heavily on the effective operation of our computer systems and networks, as well as those of our business partners and service providers. Consequently, we are potentially susceptible to operational and information security risks associated with the technologies, processes and procedures designed to protect networks, systems, computers, programs and information from cyber-attacks, operational failure, AI misuse, damage or unauthorized access. These risks include but are not limited to, theft, loss, misuse, corruption and destruction of information maintained online or digitally, denial of service on websites and other operational failures, and unauthorized disclosure of confidential, proprietary and customer information. Cyber-attacks affecting us, any third-party administrator, the underlying Funds, intermediaries, and other affiliated or third-party service providers may adversely affect us and your Policy Accumulated Value. For instance, cyber-attacks or operational incidents may interfere with Contract transaction processing, including the processing of orders from our website or with the underlying Funds; impact our ability to calculate Accumulated Unit Values, Subaccount Unit Values or an underlying Fund to calculate a net asset value; cause the disclosure and possible destruction of confidential, proprietary and customer information; impede order processing; subject us and/or our service providers and intermediaries to regulatory fines, litigation, loss of business, financial losses and reputational damage. Cybersecurity risks may also impact the issuers of securities in which the underlying Funds invest, which may cause the Funds underlying your Policy to lose value. The digitalization, increased information availability, use of new and constantly evolving technologies, the increased sophistication and severity of cyber campaigns, and the heightened geopolitical risk and tension, continue to pose new and significant cybersecurity and operational risks and threats. While measures and controls have been adopted and are periodically reviewed and updated to mitigate cybersecurity and operational risks, there can be no guarantee or assurance that we, the underlying Funds, or our service providers will not suffer losses affecting your Policy due to cyber-attacks, operational incidents, misuse of AI, or information security breaches in the future.

We are also exposed to risks related to natural and man-made disasters or other events, including (but not limited to) earthquakes, fires, floods, storms, epidemics and pandemics (such as COVID-19), geopolitical tensions, armed conflicts, wars, terrorist acts, civil unrest, malicious acts and/or other events that could adversely affect our ability to conduct business. The risks from such events are common to all insurers. To mitigate such risks, we have business continuity plans in place that include remote workforces, remote system and telecommunication accessibility, and other plans to ensure availability of critical resources and business continuity during an event. Such events can also have an adverse impact on financial markets, U.S. and global economies, service providers, and Fund performance for the funds available through your Policy. There can be no assurance that we, the Funds, or our service providers will avoid such adverse impacts due to such events and some events may be beyond control and cannot be fully mitigated or foreseen.

DEATH BENEFITS

The Death Benefit

We will pay Death Benefit Proceeds to your Beneficiary after the Insured dies while the Policy is still In Force. Your Beneficiary generally will not have to pay federal income tax on the portion of any Death Benefit Proceeds that are payable as a lump sum at death. Some Riders and settlement options may affect how the Death Benefit Proceeds are paid, see the OPTIONAL RIDERS AND BENEFITS section in this prospectus for more details.

Your Policy’s Death Benefit depends on three choices you must make:

● The Total Face Amount

● The Death Benefit Option

● The Death Benefit Qualification Test

The Policy’s Death Benefit is the higher of:

1. The Death Benefit calculated under the Death Benefit Option in effect; or

2. The Minimum Death Benefit according to the Death Benefit Qualification Test that applies to your Policy.

Certain Riders may impact the Policy’s Death Benefit, see the OPTIONAL RIDERS AND BENEFITS section in this prospectus.

Withdrawals and Policy Loans may impact the Policy’s Death Benefit, see the WITHDRAWALS, SURRENDERS AND LOANS section in this prospectus for more details.

The Total Face Amount

The Face Amount of your Policy and any Rider providing Coverage on the Insured is used to determine the Death Benefit as well as certain Policy charges, including the cost of insurance, Coverage charge and Surrender Charges.

Your Policy’s Total Face Amount is made up of one or more of the following types of Coverage:

1. Basic Face Amount – the Face Amount under the Policy

2. Face Amount under the Annual Renewable Term Rider (ART)

3. Face Amount under the Scheduled Annual Renewable Term Rider (S-ART)

Your Policy must have a Basic Face Amount. You may also select S-ART and ART Coverage at Policy issue. These riders are described in Optional Riders and Benefits.

Each type of Face Amount you select creates a Coverage Layer. Your Policy’s initial amount of insurance Coverage, which you select in your application, is its initial Face Amount. The Policy’s Total Face Amount is the sum of the Face Amounts of all Coverage Layers. The Coverage Layers you select in your application are effective on the Policy Date. You will find your Policy’s Total Face Amount, which includes any increases or decreases, in the Policy Specifications in your Policy.

If you request an increase in Face Amount, a new Coverage Layer will be created, with its own Coverage Layer Date and Policy charges.

If you request a decrease in Face Amount, the Coverage charge will not change and the cost of insurance charge may decrease since the Face Amount decrease may affect the Net Amount At Risk. No surrender charges are imposed on a Face Amount decrease.

Changing the Face Amount

You can increase or decrease your Policy’s Face Amount as long as we approve it. If you change the Face Amount, we will send you a Supplemental Schedule of Coverage for benefits and premiums.

● You can change the Face Amount as long as the Insured is alive.

● You must send us your Written Request while your Policy is In Force.

● Unless you request otherwise, the change will become effective on the first Monthly Payment Date on or after we receive and approve your request.

● Changing the Total Face Amount can affect the Net Amount At Risk, which affects the cost of insurance charge. An increase in the Face Amount may increase the cost of insurance charge, while a decrease may decrease the charge.

● If your Policy’s Death Benefit is equal to the Minimum Death Benefit, and the Net Amount At Risk is more than three times the Death Benefit on the Policy Date, we may reduce the Death Benefit by requiring you to make a withdrawal from your Policy. If we require you to make a withdrawal, the withdrawal may be taxable. Please turn to the WITHDRAWALS, SURRENDERS AND LOANS section in this prospectus for information about making withdrawals.

● We will refuse your request to make the Basic Face Amount less than $1,000.00.

Requesting an Increase in Face Amount

You may request an increase in the Face Amount under the Policy or ART rider. Each increase will create a new Coverage Layer.

Here are some additional things you should know about requesting an increase in the Face Amount under the Policy:

● The Insured must be Age 90 or younger at the time of the increase.

● You must give us satisfactory Evidence of Insurability.

● Each increase you make to the Face Amount must be a minimum of $25,000.

● Each increase in Face Amount may have an associated cost of insurance rate, Coverage charge and may have a Surrender Charge. Any cost or charge changes will take effect on the next Monthly Payment Date after the Face Amount increase is applied to the Policy. Any increase under the Annual Renewable Term Rider will not have a corresponding Surrender Charge.

● There is a $100 charge for any unscheduled increases in Face Amount under the ART rider. Currently, we are not imposing the $100 charge.

● We reserve the right to limit Face Amount increases to one per Policy Year.

● A requested increase in Face Amount will terminate the Flexible Duration No-Lapse Guarantee Rider. See the OPTIONAL RIDERS AND BENEFITS – Flexible Duration No-Lapse Guarantee Rider section in this prospectus.

Term Increases in Face Amount

Your Policy may be issued with the Scheduled Annual Renewable Term Rider (S-ART). Under this rider there may be scheduled annual renewable term insurance coverage increases in Face Amount, under the S-ART Rider. In this Rider, a scheduled increase is referred to as a Term Increase. All Term Increases will be shown in the Policy Specifications. Future Term Increases will not require future medical underwriting, but may in some instances require financial underwriting. Financial underwriting generally includes a review of the Insureds earned income and net worth in relation to the amount of life insurance coverage requested.

A Term Increase in S-ART Coverage will increase the Face Amount of the existing Coverage Layer.

There is a cost of insurance charge associated with each such Term Increase that has gone into effect and continues to be in effect. Such cost of insurance charge is part of the Monthly Deduction for the Policy and is calculated the same as that for other Coverage Layers, subject to maximum cost of insurance Rates that are the same as those applicable to the initial Coverage Layer. The monthly Cost of Insurance Rates are shown in the Policy Specifications. There is also a guaranteed Coverage charge associated with each Term Increase. The guaranteed Coverage charge is based on the current S-ART Face Amount. There is no surrender charge associated with a Term Increase.

Other Increases in Face Amount

The Policy’s Face Amount may increase under the Policy, the S-ART Rider or the ART Rider when you request a change in Death Benefit Option. In this case, we will increase the Face Amount of the most recently issued Coverage Layer. If there are Basic, S-ART and ART Coverage Layers with the same Coverage Layer Date, we will increase the ART first, then the S-ART, and finally the Basic Face Amount.

Requesting a Decrease in Total Face Amount

You may request a decrease in the Policy’s Total Face Amount. A decrease in the Total Face Amount is subject to the following limits:

● We do not allow decreases during the first Policy Year

● You may only request one decrease per Policy Year

● The Policy’s Basic Face Amount must be at least $1,000 following a decrease. We can refuse your request if the change in Face Amount would mean that your Policy no longer qualifies as Life Insurance under the Code

● Unless you have told us otherwise In Writing, any request for a decrease will not take effect if the Policy would be classified as a Modified Endowment Contract under the Code.

Decreasing the Total Face Amount may affect your Policy’s tax status. To ensure your Policy continues to qualify as life insurance, we might be required:

● To return part of your premium payments to you if you have chosen the Guideline Premium Test, or

● To make distributions from the Accumulated Value, which may be taxable. For more information, please see the VARIABLE LIFE INSURANCE AND YOUR TAXES section in this prospectus.

We can refuse your request if the amount of any distributions would exceed the Net Cash Surrender Value under the Policy.

If there is a decrease in Total Face Amount, the Coverage charge will not change and the cost of insurance charge may decrease since the Face Amount decrease may affect the Net Amount At Risk. No surrender charge is imposed on a Face Amount decrease.

Processing of Decreases

Decreasing the Total Face Amount, whether as a result of your request or as a result of a withdrawal or change in Death Benefit Option, will reduce the Face Amount of the Coverage Layers.

We will apply any decrease in the Face Amount to eligible Coverage Layers to the most recent eligible increases you made to the Face Amount first and then to the Initial Face Amount.

If more than one Coverage Layer has the same Coverage Layer Date, we will first reduce the Face Amount of any S-ART Rider Coverage Layer first, then any ART Rider Coverage Layer, then the Basic Face Amount of any Policy Coverage Layer.

If you elected an accelerated death benefit rider, any accelerated Death Benefit payments made under a rider will decrease the Total Face Amount. You can find specific information about this decrease in the applicable rider description which can be found in the OPTIONAL RIDERS AND BENEFITS section in this prospectus.

Death Benefit Options

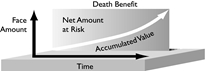

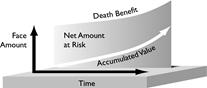

The Policy offers three Death Benefit Options, Options A, B, and C. The Death Benefit Option you choose will generally depend on which is more important to you: the amount of the Death Benefit, Cost of Insurance Charges or the Accumulated Value of your Policy.

Death Benefit Option A provides a Death Benefit equal to the Total Face Amount of the Policy. Additional premiums and Investment Option performance do not change the Total Face Amount, except in limited circumstances to ensure that the Policy qualifies as life insurance under the Code. However, additional premiums and positive Investment Option performance will increase the Accumulated Value and decrease the Net Amount At Risk which may, in turn, reduce Cost of Insurance charges. Withdrawals may reduce the Total Face Amount depending on the timing, withdrawal amount and withdrawal frequency during a Policy year.

Death Benefit Option B provides a Death Benefit equal to the Total Face Amount of the Policy plus the Accumulated Value. Additional premiums and positive Investment Option performance will increase the Death Benefit. However, since the Death Benefit under this option is based, in part, on the Accumulated Value, Policy charges and negative Investment Option performance may decrease the Death Benefit. Cost of Insurance charges are generally higher than Death Benefit Option A. Withdrawals do not reduce the Total Face Amount, but they do reduce the Accumulated Value which will in turn reduce the Death Benefit.

Death Benefit Option C provides a death benefit equal to the Total Face Amount of the Policy plus the total premiums paid, minus any withdrawal or distributions that reduce the Accumulated Value. The more premiums you pay and the less you withdraw, the larger the Death Benefit, subject to the Option C Death Benefit Limit. However, while taking withdrawals does not reduce the Total Face Amount, it does increase the sum of the withdrawals, which has the effect of reducing the Death Benefit. Cost of Insurance charges are generally higher than Death Benefit Option A.

Below is a chart that compares each Death Benefit Option based on features you may want to consider.

|

Feature |

Death Benefit Option A |

Death Benefit Option B |

Death Benefit Option C |

|

Death Benefit |

Equal to Total Face Amount |

Equal to Total Face Amount plus Accumulated Value |

Equal to Total Face Amount plus total premiums paid less any withdrawals or distributions that impact your Accumulated Value subject to the Option C Death Benefit Limit. |

|

Cost of Insurance |

Generally, higher Accumulated Values will decrease the Net Amount At Risk. This may in turn reduce Cost of Insurance charges. Cost of Insurance charges are generally lower than Death Benefit Option B and C. |

Generally, higher Accumulated Values will have no impact on the Net Amount At Risk. Cost of Insurance charges are generally higher than Death Benefit Option A. |

Generally, higher Accumulated Values will decrease the Net Amount At Risk, but premium payments will increase your Net Amount At Risk. Cost of Insurance charges are generally higher than Death Benefit Option A. |

|

Accumulated Value |

The Accumulated Value has no impact on your Death Benefit except to ensure that the Policy qualifies as life insurance under the Code (see the Minimum Death Benefit in the Death Benefits – Death Benefit Qualification Test section in this prospectus). However, your Cost of Insurance Charges are generally lower than Death Benefit Option B and C. Lower |

The higher your Accumulated Value, the higher the Death Benefit. However, your Cost of Insurance Charges are generally higher than Death Benefit Option A and higher Cost of Insurance Charges can lead to lower Accumulated Values. |

The Accumulated Value has no impact on your Death Benefit except to ensure that the Policy qualifies as life insurance under the Code (see the Minimum Death Benefit in the Death Benefits – Death Benefit Qualification Test section in this prospectus). However, your Cost of Insurance Charges are generally higher than Death Benefit Option A |

|

Cost of Insurance charges can lead to higher Accumulated Values. |

and higher Cost of Insurance Charges can lead to lower Accumulated Values. | ||

|

Impact of Withdrawals |

May reduce Total Face Amount and if it does, there will be a reduction in the Death Benefit. |

Does not reduce Total Face Amount. But it does reduce the Accumulated Value which will in turn reduce the Death Benefit. |