Q1 2026: double-digit sales and business EPS growth

Paris, April 23, 2026

Q1 sales growth of 13.6% at CER1 and business earnings per share (EPS)2 of €1.88

•Pharma launches sales increased by 49.6%, reaching €1.2 billion, driven primarily by Ayvakit, ALTUVIIIO, and Sarclisa

•Dupixent sales increased by 30.8% to €4.2 billion, a strong start to 2026

•Vaccines sales increased by 2.1% to €1.3 billion, benefiting from Heplisav-B

•Research and Development expenses reached €1.7 billion, up by 1.5%

•Selling and general expenses reached €2.3 billion, up by 11.6%, mainly due to the effect of recent acquisitions

•Business EPS was €1.88, up by 14.0% at CER; 5.0% at actual exchange rates; IFRS EPS €1.34

Pipeline progress

•Five regulatory approvals, all in immunology

•Positive pipeline readouts: venglustat in the rare disease GD3 (phase 3) and lunsekimig in respiratory diseases (phase 2)

•Two regulatory submission acceptances, one phase 3 study start, four regulatory designations (breakthrough, orphan)

Capital allocation

•Completion of the Dynavax acquisition

•Completion of €921 million of the €1 billion share buyback programme

Other major developments

•25-year partnership with WHO3 in sleeping sickness: positive CHMP recommendation paves the way in Africa for acoziborole, the first single-dose oral treatment co-developed with DNDi4

Guidance affirmed

•In 2026, sales are expected to grow by a high single-digit percentage at CER. Business EPS at CER is expected to grow slightly faster than sales (before share buyback), delivering profitable growth.5

Olivier Charmeil, interim Chief Executive Officer: “We had a strong start to 2026 with double-digit sales and business EPS growth. Sales increased by 13.6%, supported by Pharma launches and recent acquisitions. Dupixent sales were above the €4 billion quarterly mark again and grew by 30.8%. Business EPS was up by 14.0%, reflecting a measured growth of 7.0% in total operating expenses. We obtained five regulatory approvals, all in immunology, achieved one positive phase 3 study readout for venglustat in rare diseases, and reported encouraging phase 2 data for lunsekimig in respiratory diseases. We reiterate our guidance for 2026: we continue to expect sales to grow by a high single-digit percentage and business EPS to grow slightly faster than sales, at constant exchange rates, delivering profitable growth. We are looking forward to welcoming Belén Garijo as the new CEO of Sanofi from next month.”

| | | | | | | | | | | | | | |

| Q1 2026 | Change | Change

at CER | | | |

| Net sales | €10,509 | m | +6.2 | % | +13.6 | % | | | |

| IFRS net income | €1,614m | -13.8 | % | — | | | | |

| IFRS EPS | €1.34 | -11.8 | % | — | | | | |

| Free cash flow6 | €1,054 | m | +2.4 | % | — | | | | |

| Business operating income | €2,967 | m | +2.2 | % | +10.9 | % | | | |

| Business net income | €2,264 | m | +2.4 | % | +11.1 | % | | | |

| Business EPS | €1.88 | | +5.0 | % | +14.0 | % | | | |

1 Changes in net sales are at constant exchange rates (CER) unless stated otherwise (definition in Appendix 8).

2 To facilitate an understanding of operational performance, Sanofi comments on the business net income, a non-IFRS financial measure (definition in

Appendix 8). The income statement is in Appendix 3 and a reconciliation of IFRS net income to business net income is in Appendix 4.

3 World Health Organization.

4 Drugs for Neglected Diseases initiative.

5 Applying April 2026 average currency exchange rates, the currency impacts are estimated at c.-2% on sales and at c.-3% on business EPS.

6 Free cash flow is a non-IFRS financial measure (definition in Appendix 8).

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 1 |

Q1 2026 summary

A conference call and webcast for investors and analysts will begin at 13:00 CEST with details on sanofi.com, including slides.

The performance shown in this press release covers the three-month period to March 31, 2026 (the quarter or Q1 2026) compared to the three-month period to March 31, 2025 (Q1 2025). All percentage changes in sales in this press release are at CER, unless otherwise mentioned.

In Q1 2026, sales were €10,509 million and increased by 13.6%. Exchange rate movements had a negative effect of 7.4 percentage points (pp); therefore, at actual exchange rates, sales increased by 6.2%. The divestments of medicines/portfolio streamlining had a negative impact of 0.4pp on sales growth.

Sales by geography

| | | | | | | | | | |

Net sales (€ million) | Q1 2026 | Change

at CER | | |

| United States | 5,289 | | +26.2 | % | | |

| Europe | 2,163 | | +5.9 | % | | |

| Rest of World | 3,057 | | +0.2 | % | | |

| of which China | 649 | | -2.1 | % | | |

US sales were €5,289 million and increased by 26.2%. The growth was driven by Dupixent, pharma launches, and newly acquired Heplisav-B in vaccines, partly offset by older haemophilia and other medicines, and all vaccines except polio/pertussis/hib (PPH).

Europe sales were €2,163 million and increased by 5.9%. The growth was primarily driven by demand for Dupixent, pharma launches, and all vaccines except PPH, partly offset by lower sales of legacy medicines, including Lovenox, others, and industrial.

Rest of World sales were €3,057 million and increased by 0.2%. The performance was led by demand for Dupixent and launches, including Beyfortus, and by meningitis, travel, and endemic vaccines. This was almost fully offset by lower sales of many legacy medicines, flu, and PPH vaccines. China sales were €649 million and decreased by 2.1% in a broadly stable market. Sales were supported by Dupixent that returned to growth after a 2025 price adjustment, by the three launch medicines available in China (Rezurock, Sarclisa, and Myqorzo), and by insulins. This was more than offset by lower sales of legacy medicines, including Lovenox, and by a significant decline in PPH vaccines due to a decline in childbirths in China.

Business operating income

In Q1 2026, business operating income (BOI) was €2,967 million and increased by 10.9% (2.2% at actual exchange rates) from €2,902 million in Q1 2025. The ratio of BOI to net sales was 28.6% and decreased by 0.7pp (28.2% at actual exchange rates, down by 1.1pp). The decrease was mainly driven by a high increase in other operating expenses (up by 62.4%), principally from higher Regeneron profit sharing, partly offset by higher business gross profit (up by 14.4%) and lower growth in R&D expenses (up by 1.5%).

Business development

Business development, including strategic investments in external innovation is an integral part of Sanofi’s efforts to access optionality for promising scientific developments to contribute to pipeline replenishment.

On February 10, Sanofi announced the completion of the $2.2 billion acquisition of Dynavax Technologies Corporation (Dynavax). The acquisition included a US-marketed adult hepatitis B vaccine (Heplisav-B), consolidated in sales from the day of closing, which is differentiated by its two-dose regimen over one month. The acquisition also included Dynavax’s shingles vaccine candidate (Z-1018), which is currently in phase 1/2 studies, and added to the Sanofi pipeline, as well as additional vaccine pipeline projects. This acquisition augments Sanofi’s presence in adult immunisation by bringing together Dynavax’s vaccines with Sanofi’s global scale, development capabilities, and commercial reach.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 2 |

Biopharma segment

Pharma

Comments on sales performance are provided for all launch medicines and established medicines with sales of minimum €100 million per quarter.

Launches

| | | | | | | | | | |

Net sales (€ million) | Q1 2026 | Change

at CER | | |

| ALTUVIIIO | 325 | | +42.2 | % | | |

Nexviazyme/Nexviadyme | 208 | | +13.3 | % | | |

| Ayvakit | 177 | | — | % | | |

| Sarclisa | 167 | | +30.1 | % | | |

| Rezurock | 133 | | +11.5 | % | | |

| Cablivi | 68 | | +9.0 | % | | |

| Xenpozyme | 63 | | +17.9 | % | | |

| Tzield/Teizeild | 14 | | +36.4 | % | | |

| Wayrilz | 10 | | — | % | | |

| Qfitlia | 5 | | — | % | | |

| Myqorzo | 1 | | — | % | | |

| Total | 1,171 | | +49.6 | % | | |

ALTUVIIIO (haemophilia A) sales were €325 million of which 83% was in the US, making it the largest factor medicine in the market. Growth continues to be driven by patients switching from shorter half-life and legacy factor medicines, including Eloctate, and some patients from non-factor treatments. Rest of World sales were €54 million, approaching 20% of total sales, and benefited from launches in Japan and Taiwan. The haemophilia A factor medicine franchise sales (ALTUVIIIO and Eloctate combined) were €383 million and increased by 31.5%, primarily driven by ALTUVIIIO’s strong performance and launches, while Eloctate contributed €58 million and declined by 7.1%.

Nexviazyme/Nexviadyme (Pompe disease) sales were €208 million and increased by 13.3%, driven by Europe (+20.3%) where patients are still switching from Myozyme/Lumizyme. In the US (+11.1%), most patients already switched. The Pompe disease franchise sales (Nexviazyme/Nexviadyme and Myozyme/Lumizyme combined) were €320 million and increased by 2.4%.

Ayvakit (systemic mastocytosis) sales were €177 million. Sales were split between the US (€154 million), Europe (€22 million), and Rest of World (€1 million) with continued growth in the number of patients treated. Higher government rebates as a result of the originator Blueprint becoming part of Sanofi had a negative impact on US sales. On a market pro-forma basis, sales reached $206.7 million, an increase of 38.4% from $149.4 million in Q1 2025. Without the higher US rebates, sales growth would have been c.10pp higher. Sanofi does not hold marketing rights in China but receives a royalty on sales by CStone Pharmaceuticals.

Sarclisa (multiple myeloma) sales were €167 million and increased by 30.1%, supported by high growth in Europe (+29.3%), mainly from increased use in earlier lines of treatment, including front-line transplant-ineligible patients and Rest of World (+70.6%), partly also from favourable contract business.

Rezurock (chronic graft-versus-host disease) sales were €133 million and increased by 11.5%, driven by strong growth (+144.4%) in Rest of World, mainly China. Sales in the US were €106 million and increased by 3.5%. Sales in Europe were €7 million (-22.2%).

Cablivi (acquired thrombotic thrombocytopenic purpura) sales were €68 million and increased by 9.0%, driven by more patients being treated in the US (where sales increased by 19.4%), and in Europe (+4.0%). Sales in Rest of World were €3 million (-33.3%).

Xenpozyme (acid sphingomyelinase deficiency) sales were €63 million and increased by 17.9%, driven by Rest of World (+111.1%).

Tzield/Teizeild (delay onset of type 1 diabetes) sales were €14 million, of which €11 million in the US, and increased by 36.4%. Launches in Europe (sales of €2 million) and Rest of World (€1 million) have started.

Wayrilz (immune thrombocytopenia) sales were €10 million, all in the US, following approval in August 2025.

Qfitlia (haemophilia A and B) sales were €5 million, all in the US, following approval in March 2025.

Myqorzo (obstructive hypertrophic cardiomyopathy) sales were €1 million, all in China, following approval in January 2026.

Immunology

| | | | | | | | | | |

Net sales (€ million) | Q1 2026 | Change

at CER | | |

| Dupixent | 4,170 | | +30.8 | % | | |

| Kevzara | 124 | | +20.7 | % | | |

Dupixent (atopic dermatitis (AD), asthma, chronic rhinosinusitis with nasal polyposis (CRSwNP), eosinophilic esophagitis, prurigo nodularis (PN), chronic spontaneous urticaria (CSU), chronic obstructive pulmonary disease (COPD), bullous pemphigoid (BP), and allergic fungal rhinosinusitis (AFRS)) sales were €4,170 million and increased by 30.8%. Global sales were driven by strong volume growth across approved indications and Dupixent retained a leading market position across its disease areas. US sales were €3,023 million and increased by 35.9%, partly driven by a low basis of comparison due to high gross-to-net price

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 3 |

adjustments in Q1 2025. Adjusting for the basis of comparison, sales growth was largely driven by volume demand. In Europe, sales were €563 million and increased by 22.4%, reflecting growth across approved indications and consistent growth in the larger markets Germany, France, and Italy. In Rest of World, sales were €584 million and increased by 14.9%, mainly driven by Brazil, Canada, China, and Japan.

Kevzara (rheumatoid arthritis, other rheumatological indications) sales were €124 million and increased by 20.7%. With most sales in the US (€85 million), growth of 39.7% was mainly driven by increased use in polymyalgia rheumatica, approved in 2024.

Other main medicines

| | | | | | | | | | |

Net sales (€ million) | Q1 2026 | Change

at CER | | |

| Lantus | 419 | | -0.7 | % | | |

| Toujeo | 375 | | +10.5 | % | | |

| Fabrazyme | 265 | | +7.6 | % | | |

| Plavix | 224 | | -3.3 | % | | |

| Cerezyme | 186 | | +1.1 | % | | |

| Lovenox | 184 | | -22.3 | % | | |

| Praluent | 153 | | +17.7 | % | | |

| Thymoglobulin | 120 | | +6.6 | % | | |

| Alprolix | 119 | | -17.5 | % | | |

| Myozyme/Lumizyme | 112 | | -13.3 | % | | |

| Aprovel | 104 | | -0.9 | % | | |

Lantus sales were €419 million and decreased by 0.7%. US sales were €183 million and increased by 4.1% from volume growth, partly offset by gross-to-net movements. The benefit of windfall sales from the unavailability of competing medicines is still expected to subside in 2026. Combined sales in Europe and Rest of World decreased by 4.3% due to growth in Toujeo sales.

Toujeo sales were €375 million and increased by 10.5%, driven mainly by the US (+19.7%) and Europe (+9.8%). Toujeo continued to experience solid volume growth and an increase in market share.

Fabrazyme sales were €265 million and increased by 7.6%, driven by Rest of World (+18.8%) and supported by growth in patient numbers in the US and Europe.

Plavix sales were €224 million and decreased by 3.3%, driven by lower Rest of World sales (majority of sales, €203 million, -2.7%).

Cerezyme sales were €186 million and broadly stable (+1.1%), with growth in Europe (+8.5%) partly offset by lower sales in the US (-2.1%) and Rest of World (-2.4%). The Gaucher disease franchise sales (Cerezyme and Cerdelga combined) were €275 million and increased by 3.6%.

Lovenox sales were €184 million and decreased by 22.3%, from lower sales in Europe (-20.9%) and Rest of World (-24.8%), driven by the sustained impact of biosimilars.

Praluent sales were €153 million and increased by 17.7% from higher sales in Europe (€131 million, +28.4%).

Thymoglobulin sales were €120 million and increased by 6.6% as sales advanced in Rest of World (+10.5%) and the US (+6.8%).

Alprolix sales were €119 million and decreased by 17.5%, driven by lower sales to the collaborator Swedish Orphan Biovitrum (Rest of World sales, €17 million, -43.8%) and market dynamics in the US (sales of €102 million, -10.9%).

Myozyme/Lumizyme sales were €112 million and decreased by 13.3% driven by patients switching to Nexviazyme/Nexviadyme.

Aprovel sales were €104 million and broadly stable (-0.9%), with sales mainly in Rest of World (€87 million, +1.1%).

Vaccines

| | | | | | | | | | |

Net sales (€ million) | Q1 2026 | Change

at CER | | |

| Polio/pertussis/hib primary vaccines and boosters, incl. Heplisav-B | 664 | | +4.2 | % | | |

| Beyfortus | 284 | | +2.8 | % | | |

| Meningitis, travel, and endemic | 278 | | -2.0 | % | | |

| Influenza, COVID-19 | 67 | | -4.1 | % | | |

| Total | 1,293 | | +2.1 | % | | |

Vaccines sales were €1,293 million and increased by 2.1% driven by the newly acquired Heplisav-B and higher sales of Beyfortus.

Polio/pertussis/hib (PPH) primary and booster vaccines, including Heplisav-B sales were €664 million and increased by 4.2%. Sales in the US (€229 million, +47.4%) benefited from the inclusion of newly acquired Heplisav-B while sales in Rest of World (€337 million, -13.1%) were impacted by lower demand from a decline in childbirths, including in China.

Beyfortus sales were €284 million and increased by 2.8%. Sales in the US (-21.5%) were impacted by a high basis of comparison due to an inventory increase in Q1 2025 as well as competition. Sales in Europe (+2.6%) and Rest of World (+14.2%) benefited from the expanded geographical availability; Beyfortus now protects babies in more than 45 countries worldwide.

Meningitis, travel, and endemic vaccines sales were €278 million and decreased by 2.0% driven by lower sales in the US (€128 million, -17.5%) partly offset by better performance in Europe (€60 million, +30.4%) and Rest of World (€90 million, +11.8%).

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 4 |

Influenza, COVID-19 vaccines sales were €67 million and decreased by 4.1%. While flu sales in the US and Europe reflected the normal seasonal pattern, sales in Rest of World (€31 million, -25.0%) were impacted by lower uptake in the Southern Hemisphere partly offset by Nuvaxovid sales reaching €16 million, mainly in Europe.

Business operating income

In Q1 2026, Biopharma BOI was €2,955 million and increased by 10.8% (2.1% at actual exchange rates) from €2,893 million in Q1 2025. The ratio of BOI to net sales was 28.5% and decreased by 0.7pp (28.1% at actual exchange rates, down by 1.1pp). The decrease was mainly driven by a high increase in other operating expenses (up by 62.5%), principally from higher Regeneron profit sharing, partly offset by higher business gross profit (up by 13.9%) and lower growth in R&D expenses (up by 1.4%).

Pipeline update

Sanofi has 77 projects in a pipeline across three main areas (Immunology, Rare diseases, and Vaccines) and selectively in the disease areas of Neurology and Oncology, including 40 potential new medicines and vaccines. The following section highlights significant developments in the late- and mid-stage pipeline since the prior results press release.

Highlights

| | | | | |

| Regulatory approvals | Dupixent – CSU children (EU)

Dupixent – BP (JP)

Dupixent – AFRS (US)

Rezurock – cGVHD, 3L (EU)

Tzield - T1D, stage 2, delay onset of stage 3, children (US) |

| Regulatory submission acceptances | Fluzone HD/Efluelda – flu 50y+ (US, EU) |

| Phase 3 data readouts | venglustat – GD3 – primary endpoint met

venglustat – FD – primary endpoint not met |

| Phase 3 study starts | frexalimab – kidney transplant |

| Regulatory designations | Wayrilz – wAIHA – breakthrough therapy (US) Wayrilz – wAIHA – orphan (JP) Wayrilz – IgG4-RD – orphan (JP) venglustat – GD3 – breakthrough therapy (US) |

The list of all pipeline changes is available from the Q1 2026 results investor presentation, pipeline appendix.

Immunology

Dupixent (dupilumab)

•The European Commission (EC) approved Dupixent for the treatment of moderate-to-severe CSU in children aged two to 11 years with inadequate response to histamine-1 antihistamines (H1AH) and who are naïve to anti-immunoglobulin E therapy. This expands the previous approval in the EU for adults and adolescents aged 12 years and older with CSU, a chronic, inflammatory skin disease that causes sudden and debilitating hives and recurring itch. The approval was supported by data from the LIBERTY-CUPID clinical study programme, including two phase 3 studies, Study A and Study C (clinical study identifier: NCT04180488), in which children aged six to 11 years participated, and the single-arm, CUPIDKids phase 3 study (clinical study identifier: NCT05526521) in children aged two to 11 years with CSU. In the US, a supplemental biologics license application (sBLA) has been accepted for review seeking approval for Dupixent in certain children aged two to 11 years with CSU. The US Food and Drug Administration (FDA) decision is expected later in April 2026. Dupixent is approved for CSU in certain adults and adolescents in several jurisdictions including the US, the EU, and Japan.

•The Ministry of Health, Labour and Welfare (MHLW) in Japan granted marketing and manufacturing authorisation for Dupixent for the treatment of adults with moderate-to-severe BP. The approval in Japan was based on data from the LIBERTY-BP-ADEPT phase 2/3 study (clinical study identifier: NCT04206553), which evaluated Dupixent in adults with moderate-to-severe BP. Patients were randomised to receive 300 mg (n=53) or placebo (n=53) added to standard-of-care oral corticosteroids. In addition to BP, Dupixent is approved in Japan in AD, asthma, CRSwNP, PN, CSU, and COPD.

•The FDA approved Dupixent for the treatment of adult and paediatric patients aged six years and older with AFRS who have a history of sino-nasal surgery. The FDA evaluated Dupixent under priority review, which is reserved for medicines that have the potential to provide significant improvements in the treatment, diagnosis, or prevention of serious conditions. The approval expands the coverage of sino-nasal diseases to now include AFRS, alongside CRSwNP. The approval was supported by the LIBERTY-AFRS-AIMS phase 3 study (clinical study identifier: NCT04684524), in which 62 adults and children aged six years and older were randomised to receive an age- and weight-based dose of 200 or 300 mg every two or four weeks (n=33) or placebo (n=29).

Rezurock (belumosudil)

The EC granted a conditional marketing authorisation for Rezurock for the treatment of chronic graft-versus-host disease (cGVHD) in adults and in children aged 12 years and older with a body weight of at least 40 kg. The medicine is to be used when other treatment options provide limited clinical benefit, are not suitable, or have been exhausted. The conditional marketing authorisation is contingent on completion of a confirmatory, randomised, controlled study. This follows the positive opinion by the European Medicines Agency (EMA)’s Committee for Medicinal Products for Human Use (CHMP) in January. The approval is based on safety and efficacy results from several clinical studies and real-world evidence, including the randomised, multicentre ROCKstar phase 2 study (clinical study identifier: NCT03640481). The medicine was designated ‘orphan’ (a medicine used in rare diseases) in 2019. In addition to the EU, Rezurock is approved in 20 countries, including the US, UK, and Canada for the

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 5 |

treatment of patients 12 years and older with cGVHD after failure of at least two prior lines of systemic therapy, and in China after failure of one prior line of systemic therapy.

Tzield (teplizumab)

The FDA approved the sBLA for Tzield, expanding the indication from eight years and older to as young as one year of age to delay the onset of stage 3 type 1 diabetes (T1D) in patients diagnosed with stage 2 T1D. The approval was granted under a priority review process and is supported by one-year data from the PETITE-T1D phase 4 study (clinical study identifier: NCT05757713), evaluating safety and pharmacokinetics in young children.

Tzield is also being reviewed by the FDA for a potential indication to delay the progression of stage 3 T1D in patients eight years of age and older recently diagnosed with stage 3 T1D.

Tzield is approved in the EU (under the name Teizeild) and in other jurisdictions to delay the onset of stage 3 T1D in adults and paediatric patients eight years and older diagnosed with stage 2 T1D. Other regulatory reviews are ongoing. Tzield was previously granted FDA breakthrough therapy designation and orphan drug designation, for medicines that treat rare diseases affecting fewer than 200,000 people in the US.

amlitelimab (OX40L mAb)

At the American Academy of Dermatology Annual Meeting in Denver, Colorado, US, positive results were presented from three phase 3 studies of amlitelimab in AD as a monotherapy and in combination with topical medicines. Primary and key secondary endpoints in COAST 1, COAST 2, and SHORE were assessed at week 24 in patients who received amlitelimab either every four weeks (Q4W) or every 12 weeks (Q12W) with or without topical medicines. For US and US reference countries, the primary endpoint for all studies was the proportion of patients with a validated investigator global assessment scale for AD (vIGA-AD) of 0 (clear) or 1 (almost clear) and a reduction from baseline score of ≥2 points. In the COAST 1 and COAST 2 studies, amlitelimab met the primary endpoint. In COAST 1, key secondary endpoints, including vIGA-AD 0/1 with barely perceptible erythema (BPE), the proportion of patients reaching a 75% or greater improvement in the eczema area, severity index total score (EASI-75), and a ≥4-point reduction in peak pruritus-numerical rating scale (PP-NRS) were statistically significant. In COAST 2, EASI-75 and PP-NRS≥4 reached nominal significance; vIGA-AD 0/1 with BPE did not reach statistical significance. In the SHORE study, amlitelimab in combination with topical corticosteroids with or without topical calcineurin inhibitors, dosed at both Q4W and Q12W, demonstrated significant improvements in AD clinical signs and symptoms versus placebo as measured across primary and key secondary endpoints at week 24.

In the COAST 1, COAST 2, and SHORE studies, the safety profile of amlitelimab was consistent with previously reported data. Overall, malignancy rates were low (<1%) and generally similar between amlitelimab and placebo groups. There were no events of Kaposi’s sarcoma (KS). Cumulatively, a total of two KS cases, both in patients with known risk factors, were reported out of 3,778 patients confirmed to have been exposed to amlitelimab across all indications. One was previously presented at the Winter Clinical Miami conference, Florida, US, from the open-label ATLANTIS phase 2 study (clinical study identifier: NCT05769777). At the AAD meeting, Sanofi presented the second case, identified in the still-blinded ESTUARY phase 3 extension study (clinical study identifier: NCT06407934) evaluating Q12W maintenance dosing and longer-term safety. In each case, the patient stopped treatment with amlitelimab and is in the recovery phase. Sanofi has not identified any further cases of KS across an estimated 4,630 patients in the full amlitelimab development programme, including still-blinded studies. Sanofi believes that amlitelimab continues to have the potential to be a meaningful and convenient option for patients with AD. Results from ESTUARY are anticipated in H2 2026 followed by regulatory submission in the same period.

duvakitug (TL1A mAb)

Positive results from the RELIEVE UCCD long-term extension (LTE) study (clinical study identifier: NCT05668013) of duvakitug showed durable clinical and endoscopic efficacy maintained over 44 weeks in patients with ulcerative colitis (UC) and Crohn’s disease (CD) that initially responded to the induction phase. RELIEVE UCCD LTE is a double-blind randomised study evaluating the long-term efficacy, safety, and tolerability of duvakitug in UC and CD, the two most common forms of inflammatory bowel disease. The longer duration data reinforce the efficacy from the RELIEVE UCCD phase 2b induction study (clinical study identifier: NCT05499130), which demonstrated that patients achieved clinically meaningful response with duvakitug dosed once every two weeks compared to placebo at week 14. The LTE study enrolled 130 patients who responded to duvakitug in the RELIEVE UCCD induction study and entered a 44-week maintenance period. Patients were re-randomized to receive either a 450 mg or 900 mg subcutaneous dose every four weeks for up to a total of 58 weeks of exposure. Both doses of duvakitug were well tolerated. The findings reinforce the potential of duvakitug which is in ongoing phase 3 programmes in UC and CD.

lunsekimig (IL13xTSLP Nanobody® VHH)

Phase 2 studies of lunsekimig in two chronic respiratory diseases met their primary and key secondary endpoints compared to placebo. Lunsekimig is made of five linked antibody fragments designed to simultaneously block TSLP and IL13, two separate drivers of inflammation that contribute to tissue damage in asthma and related diseases.

•The AIRCULES phase 2b study (clinical study identifier: NCT06102005) met its primary and key secondary endpoints demonstrating a statistically significant and clinically meaningful reduction in exacerbations and improvement in lung function, as measured by pre-bronchodilator forced expiratory volume in one second (pre-BD FEV1). The study enrolled adult patients with moderate-to-severe asthma, a form of the disease marked by recurrent symptoms and frequent flareups despite standard-of-care treatment.

•The DUET phase 2a proof-of-concept study (clinical study identifier: NCT06454240) in CRSwNP, met its primary endpoint of change in nasal polyp score from baseline and met its key secondary endpoints of change in patient reported nasal congestion/obstruction score and change in Lund-Mackay Computed Tomography (LMK-CT) score, all compared to placebo at week 24.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 6 |

•The separate exploratory VELVET phase 2b study (clinical study identifier: NCT06790121) in moderate-to-severe AD did not meet its primary endpoint of percent change from baseline in EASI score. However, improvements were seen in the key secondary endpoints measuring skin clearance including EASI-75, and vIGA-AD 0/1.

Across these studies, lunsekimig was generally well tolerated. Detailed results from the AIRCULES, DUET, and VELVET studies will be presented at forthcoming medical meetings. Lunsekimig is currently in clinical development in the AIRLYMPUS phase 2 study (clinical study identifier: NCT06676319) in high-risk asthma and in the PERSEPHONE (clinical study identifier: NCT07190209) and the THESEUS phase 3 studies (clinical study identifier: NCT07190222).

frexalimab (CD40L mAb)

The FREXERA phase 2/3 study (clinical study identifier: NCT07412470) of frexalimab in kidney transplantation commenced dosing the first patient. The study is testing if frexalimab dosed subcutaneously (after an initial intravenous dose) combined with standard-of-care treatment can reduce the risk of rejection of the new kidney, help it last longer, and improve kidney function.

Rare diseases

Wayrilz (rilzabrutinib)

•The FDA granted a designation as breakthrough therapy to Wayrilz for the treatment of patients with warm autoimmune haemolytic anaemia (wAIHA), a rare autoimmune disease marked by the destruction of red blood cells. The Japanese MHLW also provided Wayrilz an orphan designation for the same condition. Both designations were based on clinical data from the ongoing LUMINA 2 phase 2b study (clinical study identifier: NCT05002777) assessing the efficacy and safety of Wayrilz for patients with wAIHA. In addition, the new LUMINA 3 phase 3 study (clinical study identifier: NCT07086976), is assessing Wayrilz compared with placebo in patients with wAIHA. There is currently no approved treatment that specifically targets the underlying cause of wAIHA, which can lead to anaemia, fatigue, and serious organ damage. An FDA breakthrough therapy designation is designed to expedite the development and review of medicines in the US intended to treat serious or life-threatening conditions and where preliminary clinical evidence indicates the therapy may demonstrate substantial improvement over available treatment options. Orphan designation in Japan is granted to medicines intended to address rare diseases with high unmet medical need.

•The MHLW in Japan also granted an orphan drug designation to Wayrilz for IgG4-related disease (IgG4-RD). There is still unmet medical need and limited treatment options in Japan for IgG4-RD, a rare, progressive, immune-mediated chronic condition in which the immune system attacks various tissues and organs leading to serious damage. Wayrilz for the treatment of IgG4-RD was evaluated in a phase 2 study (clinical study identifier: NCT04520451) and led to reduction in disease flares and other disease markers and minimised the need for treatment with glucocorticoids. The safety profile of Wayrilz in the study was consistent with previous studies in other indications, with no new safety signals observed. Currently, Wayrilz in IgG4-RD is being evaluated in the RILIEF phase 3 study (clinical study identifier: NCT07190196).

venglustat (oral glucosylceramide synthase inhibitor)

•Positive results from the LEAP2MONO phase 3 study (clinical study identifier: NCT05222906) demonstrated that venglustat met the primary and three out of four key secondary endpoints in adults and paediatric patients (12 years and older) with neurological manifestations of type 3 Gaucher disease (GD3), a rare lysosomal storage disorder. Venglustat, which works by reducing the abnormal accumulation of sugar-and-fat molecules in cells and organs, is a glucosylceramide synthase inhibitor that crosses the blood-brain barrier with the goal of targeting some of the neurological aspects of GD3 that currently have no approved therapies. Venglustat is also being studied for the treatment of Fabry disease (FD), another rare lysosomal storage disorder. Data from the phase 3 PERIDOT study (clinical study identifier: NCT05206773) showed that reduction in neuropathic and abdominal pain was observed in both study arms but the primary endpoint was not met. Additional analyses of the data are ongoing with more information to be shared at a forthcoming medical meeting. A second phase 3 study, CARAT (clinical study identifier: NCT05280548), evaluating the effect of venglustat on left cardiac ventricular mass index in men and women with FD, is ongoing. As a result of the positive LEAP2MONO study, Sanofi will pursue global regulatory submissions for venglustat in GD3. Sanofi, through Genzyme, has supported the Gaucher disease community for decades as part of an over 40-year commitment to improving care for rare diseases.

•The FDA granted breakthrough therapy designation to venglustat for the treatment of neurological manifestations of GD3, based on data from the LEAP2MONO phase 3 study (please see the bullet above).

Oncology

Sarclisa (isatuximab)

The CHMP adopted a positive opinion recommending the approval of Sarclisa subcutaneous (SC) in combination with approved standard-of-care regimens for the treatment of patients with multiple myeloma (MM) across all currently approved indications for Sarclisa intravenous (IV) formulation in the EU. If approved, Sarclisa would be the first available cancer medicine to be administered through both an on-body injector (OBI) and manual injection, and the only anti-CD38 monoclonal antibody available in MM to offer the flexibility of both an OBI and manual injection. A final decision is expected in the coming months.

The positive CHMP opinion is based on the results from the IRAKLIA phase 3 study (clinical study identifier: NCT05405166) in relapsed and/or refractory (R/R) MM, which demonstrated non‑inferiority of the SC formulation compared to the IV formulation. Four additional studies supported the decision and include the GMMG-HD8 phase 3 study (clinical study identifier: NCT05804032) in transplant-eligible newly diagnosed MM (NDMM, TE), the IZALCO phase 2 study (clinical study identifier: NCT05704049) in R/R MM, and the ISASOCUT phase 2 study (clinical study identifier: NCT05889221) in transplant-ineligible NDMM (NDMM, TI) and one phase 1b study (clinical study identifier: NCT04045795) in R/R MM patients who received at least two prior lines of therapy.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 7 |

Sarclisa IV is currently approved in four indications in the EU for both NDMM, TI and NDMM, TE, and as early as first relapse in R/R MM. In the US, the FDA extended by up to three months the target action date for its review of the sBLA for Sarclisa SC. The revised target action date for the FDA decision is July 23, 2026. In addition to the EU and the US, a regulatory submission is also under review in Japan.

Other

Acoziborole Winthrop (acoziborole)

The CHMP granted a positive opinion to Acoziborole Winthrop as a single-dose oral treatment for both early and advanced-stage gambiense sleeping sickness in adults as well as in adolescents 12 years and older weighing at least 40 kg. The CHMP positive opinion was granted through accelerated assessment under a specific procedure intended for countries outside of the EU and used for high-priority medicines for diseases with unmet needs. This will facilitate approval of the medicine in the Democratic Republic of Congo and pave the way for an update of WHO’s sleeping sickness treatment guidelines, a move that would eventually expand access to other countries in Central and West Africa, where the disease is endemic. Once approved in endemic countries, the medicine, co-developed by the Drugs for Neglected Diseases initiative and Sanofi, could provide a significant advance over current therapies. Existing treatments require either a ten-day course of oral medicine or a combination of injections and oral therapy for advanced cases. Transmitted by the bite of an infected tsetse fly, human African trypanosomiasis, commonly known as sleeping sickness, is almost always fatal without treatment.

Vaccines

Fluzone HD/Efluelda (influenza)

The FDA and EMA accepted for review the regulatory submission of Fluzone high dose (HD)/Efluelda for use in adults aged 50 years and above to prevent influenza. The regulatory submission follows positive results in the QHD00042 phase 3 study (clinical study identifier: NCT06641180) reported in October 2025.

Beyfortus (RSV)

A new study published in The Lancet Infectious Diseases, the NIRSE-GAL study, conducted in Galicia, Spain, is the first prospective real-world population study to evaluate the impact of a universal Beyfortus immunisation programme during two consecutive RSV seasons. The study showed an 85.9% reduction in hospitalisations from RSV-related lower respiratory tract infection during the first season. The study also compared the number of hospitalisations in immunised infants during their second RSV season versus the number of expected hospitalisation cases based on data from recent seasons. The data confirmed a 55.3% reduction in hospitalisations in the second RSV season among infants who received a dose of Beyfortus during infancy. By preventing severe RSV infections during the first months of life, a critical period of lung development, it is thought the infants may be less prone to subsequent admissions from either RSV or other respiratory infections.

Nuvaxovid (COVID-19)

In the COMPARE study, Nuvaxovid demonstrated statistically significant lower systemic reactogenicity (the expected side effects that might occur following vaccination) compared to mNEXSPIKE (mRNA-1283), Moderna's latest mRNA COVID-19 vaccine, across all pre-specified endpoints in the study. The randomized, double-blind study enrolled 1,000 adults in the US and was presented at the European Society of Clinical Microbiology and Infectious Diseases Global Congress in Munich, Germany.

In the COMPARE study, when side effects did occur with Nuvaxovid, they were less severe and shorter in duration compared to mNEXSPIKE. Severe systemic symptoms (body-wide reactions such as fatigue, headache, or fever) that prevent people from carrying out their normal daily activities were more than 50% less frequent with Nuvaxovid, affecting fewer than one in ten Nuvaxovid recipients compared to one in five mNEXSPIKE recipients, an analysis of the data showed. Severe local symptoms (reactions at the injection site such as pain, redness, or swelling) with Nuvaxovid were rare, and more than 75% less frequent compared to mNEXSPIKE. This was reflected in the study participants' own experience: those who received Nuvaxovid were nearly twice as likely as mNEXSPIKE recipients to say they would definitely choose the same vaccine type again the following year.

Despite the end of the pandemic, COVID-19 continues to cause significant hospitalizations and deaths globally, while placing considerable strain on health systems during seasonal peaks. Yet vaccination uptake remains low, with concerns about vaccine side effects ranking among the top reasons cited by adults for not getting vaccinated against COVID-19.

SP0230 (meningitis)

SP0230, a novel pentavalent meningococcal vaccine candidate, did not achieve the predefined immunogenicity threshold in its phase 2 study. Consequently, the vaccine candidate will revert to earlier stages of development for reformulation.

Anticipated major upcoming pipeline milestones

| | | | | | | | | | | |

| Medicine/vaccine | Indication | Description |

| H1 2026 | Dupixent | CSU children | regulatory decision (US) |

| Tzield | T1D, stage 3, delay progression | regulatory decision (US) |

| Nexviazyme | infantile-onset Pompe disease (IOPD) | phase 3 data |

| venglustat | GD3 | regulatory submission (US, EU, JP) |

| Sarclisa | SC | regulatory decision (EU) |

| tolebrutinib | secondary progressive multiple sclerosis (MS) | regulatory decision (EU) |

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 8 |

| | | | | | | | | | | |

| H2 2026 | Dupixent | CSU children | regulatory decision (JP) |

| BP | regulatory decision (EU) |

| lichen simplex chronicus | phase 3 data |

| regulatory submission (US) |

| amlitelimab | AD | phase 3 data (remaining data) |

| regulatory submission |

| Wayrilz | ITP | regulatory decision (JP) |

| Nexviazyme | IOPD | regulatory submission (US) |

| efdoralprin alfa | alpha-1 antitrypsin deficiency emphysema | regulatory submission (US) |

| Sarclisa | SC | regulatory decision (US, JP) |

| SP0087 | rabies | regulatory decision (EU) |

| regulatory submission (US) |

| 2027 | itepekimab | CRSwNP | phase 3 data |

| brivekimig | hidradenitis suppurativa | phase 2 data |

| fitusiran | haemophilia A/B | phase 3 data (12 years+) |

| regulatory submission (EU, JP) |

| frexalimab | relapsing MS | phase 3 data |

| regulatory submission (US, EU) |

| riliprubart | chronic inflammatory demyelinating polyneuropathy | phase 3 data |

| regulatory submission (US, EU) |

| Fluzone HD/Efluelda | influenza 50 years+ | regulatory decision (US, EU) |

| SP0202 | pneumococcal disease | phase 3 data |

| SP0218 | yellow fever | phase 3 data |

| regulatory submission (EU) |

A status on the Sanofi pipeline as of March 31, 2026, is available at: https://www.sanofi.com/en/our-science/our-pipeline.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 9 |

Sustainability update

Acoziborole positive opinion marks major step forward in sleeping sickness elimination

The CHMP granted a positive opinion on acoziborole, a single-dose oral medicine administered as three tablets, positioning it as a significant advancement in supporting the WHO goal of eliminating the disease by 2030.

The commitment of Sanofi, alongside its long-term partner Drugs for Neglected Diseases initiative, WHO, and other global health actors has resulted in a 98% reduction in sleeping sickness cases since 2001. Sanofi will donate acoziborole to the WHO through its philanthropic arm, Sanofi Foundation, ensuring patients receive the treatment at no cost.

Sanofi-supported study quantifies environmental and socio-economic factors exacerbating respiratory diseases

Sanofi’s sustainability strategy is centred around the ambition to tackle the link between environmental challenges, health, and healthcare.

A study, supported by Sanofi, in partnership with Regeneron, analysed health data from over 710,000 asthma and COPD patients1 in France between 2018 and 2022, integrating environmental and socio-economic indicators to identify risk and protective factors associated with respiratory disease exacerbation.

The study results showed that the setting and living conditions directly influence the severity of respiratory diseases. Urban living increases risk of exacerbations by 40% in people with asthma, by 53% in asthmatic children, and by 8% in people with COPD. Conversely, certain natural environments, such as proximity to a forest or other green areas or bodies of water reduce risk by 5% and 20%, respectively. The study also confirmed the central role of air pollution in the worsening of respiratory diseases. Other factors, such as tobacco use and extreme temperatures, increasingly frequent in the context of climate change, also increase the risk of exacerbations. Additionally, socio-economic inequalities compound environmental risks, with patients in high-poverty areas facing up to 36% higher exacerbation risk.

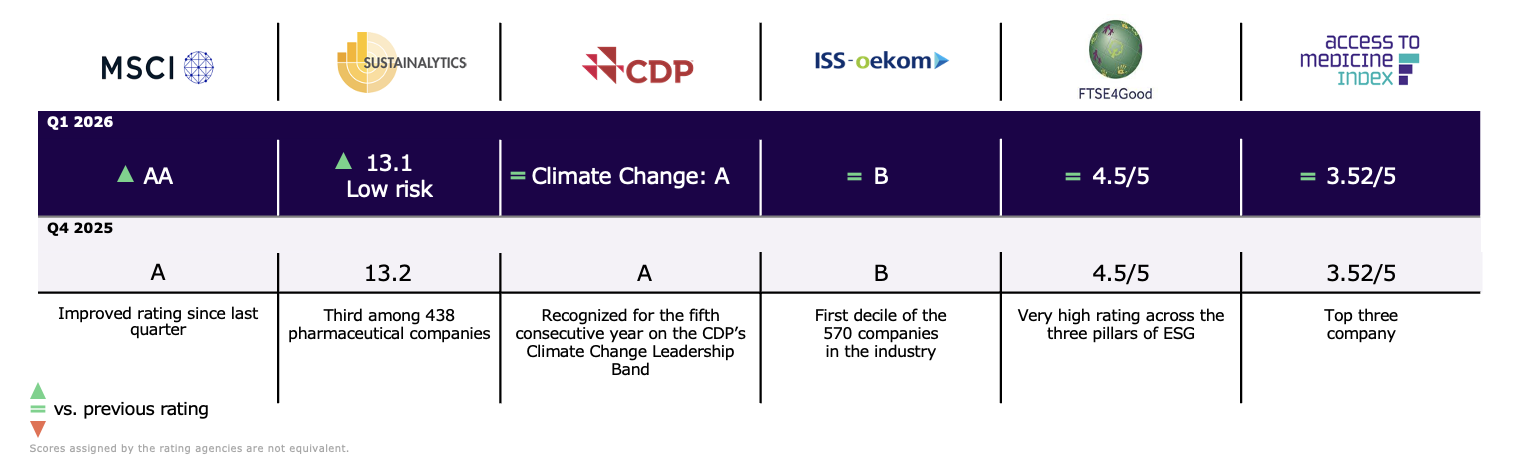

ESG ratings

Sanofi has been recognized as one of the 2026 World’s Most Ethical Companies® by Ethisphere, reflecting the integrity the company brings to leadership, governance, and culture.

Sanofi’s current ESG rankings:

1 Study conducted using data from the National Health Data System, specifically hospital data.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 10 |

Q1 2026 financial results

Business net income1

Net sales were €10,509 million in Q1 2026 and increased by 6.2% (13.6% at CER) from €9,895 million in Q1 2025.

Other revenues were €735 million in Q1 2026 and increased by 3.4% (10.0% at CER) from €711 million in Q1 2025. VaxServe sales of non-Sanofi vaccines were €354 million and decreased by 13.9% (4.4% at CER). In addition, other revenues included manufacturing services and other (€163 million), sales of Opella products in certain markets (€146 million), royalties (€42 million), and supply sales to Opella (€30 million).

Business gross profit was €8,188 million in Q1 2026 and increased by 6.1% (14.4% at CER) from €7,718 million in Q1 2025. The business gross margin was 77.9% and decreased by 0.1pp (78.6% at CER, up by 0.6pp). The margin improvement in Q1 was driven by improved product mix, including the continued portfolio shift towards specialty care medicines and rare diseases.

Research and Development expenses were €1,747 million in Q1 2026 and decreased by 3.4% (up by 1.5% at CER) from €1,808 million in Q1 2025; a quarter which included wind-down costs for the discontinued E. coli sepsis vaccine candidate. The ratio of R&D to net sales was 16.6% and decreased by 1.7pp (16.3% at CER, down by 2.0pp).

Selling and general expenses were €2,327 million in Q1 2026 and increased by 4.7% (11.6% at CER) from €2,222 million in Q1 2025. The SG&A increase was elevated by the consolidation of recent acquisitions: Blueprint (July 2025) and Dynavax (February 2026). The ratio of expenses to net sales was 22.1% and decreased by 0.4pp (22.1% at CER, down by 0.4pp).

Total operating expenses were €4,074 million in Q1 2026 and increased by 1.1% (7.0% at CER) from €4,030 million in Q1 2025.

Other operating income net of expenses was -€1,190 million in Q1 2026 and increased by 43.9% (62.4% at CER) from -€827 million in Q1 2025. Details are available from the table below:

| | | | | | | | | | |

| (€ million) | Q1 2026 | Q1 2025 | | |

| | | | |

| Gains on asset divestments | 38 | | 228 | | | |

| of which medicine divestments/portfolio streamlining | 36 | | 220 | | | |

| Amvuttra® income | 181 | | 63 | | | |

| Other | 63 | | 40 | | | |

| Total other operating income | 282 | | 331 | | | |

| | | | |

| Regeneron alliance: | (1,378) | | (1,062) | | | |

| (i) (Profit)/loss sharing | (1,514) | | (1,115) | | | |

| (ii) Additional profit share for development cost from Regeneron | 303 | | 222 | | | |

| (iii) Selling expense reimbursements to Regeneron | (167) | | (169) | | | |

| Other | (94) | | (96) | | | |

| Total other operating expenses | (1,472) | | (1,158) | | | |

| | | | |

| Other operating income net of expenses | (1,190) | | (827) | | | |

Share of profit from associates and joint ventures was €47 million in Q1 2026 compared to €48 million in Q1 2025 and mainly included the share of profit related to Vaxelis. EUROAPI and Opella are included only in the IFRS accounts (please see net income reconciliation below).

Business operating income was €2,967 million in Q1 2026 and increased by 2.2% (10.9% at CER) from €2,902 million in Q1 2025. The ratio of BOI to net sales was 28.2% and decreased by 1.1pp (28.6% at CER, down by 0.7pp). The decrease was mainly driven by a high increase in other operating expenses, principally from higher Regeneron profit sharing, partly offset by higher business gross profit and lower growth in R&D expenses.

Net financial expenses were €78 million in Q1 2026 compared to €68 million in Q1 2025, reflecting higher net debt in the quarter.

The effective tax rate was 22.0% in Q1 2026 and decreased from 22.3% in Q1 2025. Generally, the effective tax rate will fluctuate from quarter to quarter. Sanofi continues to anticipate a broadly stable tax rate in 2026 of c.20%.

Business net income was €2,264 million in Q1 2026 and increased by 2.4% (+11.1% at CER) from €2,212 million in Q1 2025. The ratio of business net income to net sales was 21.5% and decreased by 0.9pp (21.9% at CER, down by 0.5pp).

Business earnings per share (business EPS) was €1.88 in Q1 2026 and increased by 5.0% (14.0% at CER) from €1.79 in Q1 2025. The average number of shares outstanding was 1,204.2 million compared to 1,233.9 million in Q1 2025.

Opella

On April 30, 2025, Sanofi and CD&R closed the Opella transaction, creating an independent global consumer healthcare leader. Sanofi retained a significant shareholding in Opella through a 48.2% equity interest in OPAL JV Co, which indirectly holds 100% of Opella. Bpifrance owns 1.8% and CD&R the remaining 50.0%. The transaction was completed on the terms previously disclosed, and Sanofi received net cash proceeds of €10.4 billion. To aid the ongoing assessment of the value of Sanofi’s Opella stake, Opella’s summary financials will be disclosed at Q2/H1 and Q4/FY financial results.

1 See Appendix 3 for the consolidated income statement; see Appendix 8 for definitions of non-IFRS financial indicators; and see Appendix 4 for

reconciliation of IFRS net income to business net income.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 11 |

Reconciliation of IFRS net income to business net income (see Appendix 4)

In Q1 2026, the IFRS net income was €1,614 million. The main items excluded from the business net income were:

•Net income from discontinued operations amounted to €26 million.

•An amortisation charge of €535 million, of which €512 million related to intangible assets measured at their acquisition-date fair values (mainly Blueprint €147 million, Bioverativ €142 million, Provention Bio €49 million, Ablynx €41 million, Kadmon €38 million and Beyfortus €29 million), and €23 million related to intangible assets from separate acquisitions, measured initially at acquisition cost (licenses/products). These items had no cash impact.

•A €82 million step-up inventory amortisation mainly from the Blueprint acquisition reported in the cost of sales line.

•Restructuring costs and similar items of €119 million, mainly related to integration and acquisition costs of €59 million (mainly Dynavax and Blueprint) and to redundancy plans of €44 million.

•Other gains and losses, and litigation of €102 million.

•A financial income of €40 million mainly related to the unwinding of the liability related to royalty on Beyfortus US sales.

•A €181 million tax effect arising from the items listed above, mainly comprising €94 million of deferred taxes generated by amortisation and impairment of intangible assets, and €23 million associated with restructuring costs and similar items.

•Other items include Sanofi’s share of losses from associates EUROAPI and OPAL JV Co (Opella).

Cash flow

In Q1 2026, free cash flow before restructuring, acquisitions, and disposals amounted to €1,582 million after a change in net working capital of -€347 million, and capital expenditures of -€520 million. After acquisitions1 of -€322 million, proceeds from disposals1 of €111 million, and payments related to restructuring and similar items of -€317 million, free cash flow2 was €1,054 million.

Net debt

After the acquisition of Dynavax for -€1,660 million, the impact of the share buyback of -€806 million, the forex impact on net debt of -€156 million and the net cash outflow from the Opella transaction of -€185 million, the change in net debt was -€1,892 million. As a result, net debt increased from €11,008 million on December 31, 2025, to €12,900 million on March 31, 2026 (amount net of €5,544 million in cash and cash equivalents).

Shareholder return

In January, the Board of Directors proposed a dividend for 2025 of €4.12, marking 31 years of consecutive increases. The proposal is subject to approval by shareholders at the 2026 annual general meeting on April 29, 2026. Sanofi also announced the intention to execute a share buyback programme in 2026 of €1 billion with the purpose of share cancellation. As of March 31, 2026, €800 million of the programme had been purchased in the open market.

| | | | | | | | | | | | | | |

| | Media Relations |

| | Sandrine Guendoul | +33 6 25 09 14 25 | sandrine.guendoul@sanofi.com |

| | Evan Berland | +1 215 432 0234 | evan.berland@sanofi.com |

| | Léa Ubaldi | +33 6 30 19 66 46 | lea.ubaldi@sanofi.com |

| | Léo Le Bourhis | +33 6 75 06 43 81 | leo.lebourhis@sanofi.com |

| | Victor Rouault | +33 6 70 93 71 40 | victor.rouault@sanofi.com |

| | Timothy Gilbert | +1 516 521 2929 | timothy.gilbert@sanofi.com |

| | | | |

| | | | | | | | | | | | | | |

| | Investor Relations |

| | Thomas Kudsk Larsen | +44 7545 513 693 | thomas.larsen@sanofi.com |

| | Alizé Kaisserian | +33 6 47 04 12 11 | alize.kaisserian@sanofi.com |

| | Keita Browne | +1 781 249 1766 | keita.browne@sanofi.com |

| | Nathalie Pham | +33 7 85 93 30 17 | nathalie.pham@sanofi.com |

| | Nina Goworek | +1 908 569 7086 | nina.goworek@sanofi.com |

| | Thibaud Châtelet | +33 6 80 80 89 90 | thibaud.chatelet@sanofi.com |

| | Yun Li | +33 6 84 00 90 72 | yun.li3@sanofi.com |

| | | | |

1 Not exceeding €500 million per transaction (inclusive of all payments related to the transaction).

2 Non-IFRS financial measure (definition in Appendix 8).

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 12 |

Appendices

| | | | | | | | |

| | |

| | |

| | |

| | |

| Reconciliation of net income attributable to equity holders of Sanofi to business net income | |

| Change in net debt and summarised statements of cash flow | |

| | |

| | |

| Simplified consolidated balance sheet | |

| | |

| | |

| | |

| Sustainability dashboard | |

| | |

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 13 |

Appendix 1: Q1 2026 net sales by medicine/vaccine and geography

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Q1 2026 (€ million) | Total sales | Change

at CER | Change | | United States | Change

at CER | | Europe | Change

at CER | | Rest of World | Change

at CER |

| Immunology | | | | | | | | | | | | |

| Dupixent | 4,170 | | +30.8 | % | +19.8 | % | | 3,023 | | +35.9 | % | | 563 | | +22.4 | % | | 584 | | +14.9 | % |

| Kevzara | 124 | | +20.7 | % | +11.7 | % | | 85 | | +39.7 | % | | 33 | | +10.0 | % | | 6 | | -53.8 | % |

| Rare diseases | | | | | | | | | | | | |

| ALTUVIIIO (*) | 325 | | +42.2 | % | +29.5 | % | | 271 | | +37.6 | % | | — | | — | % | | 54 | | +72.7 | % |

| Fabrazyme | 265 | | +7.6 | % | +1.1 | % | | 124 | | +3.8 | % | | 68 | | +4.6 | % | | 73 | | +18.8 | % |

| Nexviazyme/Nexviadyme (*) | 208 | | +13.3 | % | +6.7 | % | | 99 | | +11.1 | % | | 77 | | +20.3 | % | | 32 | | +6.3 | % |

| Cerezyme | 186 | | +1.1 | % | -2.1 | % | | 41 | | -2.1 | % | | 65 | | +8.5 | % | | 80 | | -2.4 | % |

| Ayvakit (*) | 177 | | — | % | — | % | | 154 | | — | % | | 22 | | — | % | | 1 | | — | % |

| Alprolix | 119 | | -17.5 | % | -25.6 | % | | 102 | | -10.9 | % | | — | | — | % | | 17 | | -43.8 | % |

| Myozyme | 112 | | -13.3 | % | -17.0 | % | | 37 | | -12.5 | % | | 34 | | -32.7 | % | | 41 | | +10.5 | % |

| Cerdelga | 89 | | +9.3 | % | +3.5 | % | | 47 | | +13.0 | % | | 38 | | +8.6 | % | | 4 | | -20.0 | % |

| Cablivi (*) | 68 | | +9.0 | % | +1.5 | % | | 39 | | +19.4 | % | | 26 | | +4.0 | % | | 3 | | -33.3 | % |

| Aldurazyme | 67 | | -25.5 | % | -28.7 | % | | 18 | | +5.3 | % | | 23 | | +9.5 | % | | 26 | | -50.0 | % |

| Xenpozyme (*) | 63 | | +17.9 | % | +12.5 | % | | 23 | | — | % | | 22 | | — | % | | 18 | | +111.1 | % |

| Eloctate | 58 | | -7.1 | % | -17.1 | % | | 37 | | -21.2 | % | | — | | — | % | | 21 | | +33.3 | % |

| Wayrilz (*) | 10 | | — | % | — | % | | 10 | | — | % | | — | | — | % | | — | | — | % |

| Qfitlia (*) | 5 | | — | % | — | % | | 5 | | — | % | | — | | — | % | | — | | — | % |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Oncology | | | | | | | | | | | | |

| Sarclisa (*) | 167 | | +30.1 | % | +22.8 | % | | 59 | | +8.2 | % | | 52 | | +29.3 | % | | 56 | | +70.6 | % |

| Jevtana | 66 | | -1.3 | % | -12.0 | % | | 47 | | -11.9 | % | | 1 | | — | % | | 18 | | +40.0 | % |

| Other main medicines | | | | | | | | | | | | |

| Lantus | 419 | | -0.7 | % | -6.9 | % | | 183 | | +4.1 | % | | 73 | | -2.7 | % | | 163 | | -5.0 | % |

| Toujeo | 375 | | +10.5 | % | +5.9 | % | | 71 | | +19.7 | % | | 134 | | +9.8 | % | | 170 | | +7.2 | % |

| Plavix | 224 | | -3.3 | % | -8.2 | % | | 1 | | 0.0 | % | | 20 | | -9.1 | % | | 203 | | -2.7 | % |

| Lovenox | 184 | | -22.3 | % | -22.7 | % | | 2 | | — | % | | 107 | | -20.9 | % | | 75 | | -24.8 | % |

| Praluent | 153 | | +17.7 | % | +17.7 | % | | — | | — | % | | 131 | | +28.4 | % | | 22 | | -21.4 | % |

| Rezurock (*) | 133 | | +11.5 | % | +1.5 | % | | 106 | | +3.5 | % | | 7 | | -22.2 | % | | 20 | | +144.4 | % |

| Thymoglobulin | 120 | | +6.6 | % | -1.6 | % | | 70 | | +6.8 | % | | 10 | | -9.1 | % | | 40 | | +10.5 | % |

| Aprovel | 104 | | -0.9 | % | -5.5 | % | | 1 | | — | % | | 16 | | -11.1 | % | | 87 | | +1.1 | % |

| Multaq | 80 | | +9.9 | % | -1.2 | % | | 74 | | +10.8 | % | | 2 | | -33.3 | % | | 4 | | +25.0 | % |

| Soliqua/iGlarLixi | 79 | | +18.6 | % | +12.9 | % | | 24 | | +12.5 | % | | 12 | | — | % | | 43 | | +30.3 | % |

| Apidra | 70 | | +1.4 | % | -1.4 | % | | 2 | | 0.0 | % | | 27 | | +3.8 | % | | 41 | | 0.0 | % |

| Synvisc | 35 | | -30.9 | % | -36.4 | % | | 21 | | -28.1 | % | | 4 | | -20.0 | % | | 10 | | -38.9 | % |

| Tzield/Teizeild (*) | 14 | | +36.4 | % | +27.3 | % | | 11 | | +18.2 | % | | 2 | | +100.0 | % | | 1 | | -100.0 | % |

| | | | | | | | | | | | |

| Myqorzo (*) | 1 | | — | % | — | % | | — | | — | % | | — | | — | % | | 1 | | — | % |

| Others | 865 | | -13.7 | % | -16.2 | % | | 75 | | -27.0 | % | | 264 | | -14.3 | % | | 526 | | -10.9 | % |

| Industrial Sales | 81 | | -16.7 | % | -20.6 | % | | 1 | | — | % | | 79 | | -13.7 | % | | 1 | | -71.4 | % |

| Vaccines | | | | | | | | | | | | |

| Polio/pertussis/hib primary vaccines and boosters, incl. Heplisav-B (**) | 664 | | +4.2 | % | -0.6 | % | | 229 | | +47.4 | % | | 98 | | -1.0 | % | | 337 | | -13.1 | % |

| Beyfortus (**) | 284 | | +2.8 | % | — | % | | 46 | | -21.5 | % | | 80 | | +2.6 | % | | 158 | | +14.2 | % |

| Meningitis, travel, and endemic | 278 | | -2.0 | % | -7.9 | % | | 128 | | -17.5 | % | | 60 | | +30.4 | % | | 90 | | +11.8 | % |

| Influenza, COVID-19 (**) | 67 | | -4.1 | % | -8.2 | % | | 23 | | -3.7 | % | | 13 | | +133.3 | % | | 31 | | -25.0 | % |

| Biopharma | 10,509 | | +13.6 | % | +6.2 | % | | 5,289 | | +26.2 | % | | 2,163 | | +5.9 | % | | 3,057 | | +0.2 | % |

| Pharma launches (*) | 1,171 | | +49.6 | % | +38.3 | % | | 777 | | +53.1 | % | | 208 | | +29.0 | % | | 186 | | +60.7 | % |

| Launches (*), (**) | 1,517 | +43.8 | % | +34.1 | % | | 872 | | +53.8 | % | | 301 | | +26.3 | % | | 344 | | +35.7 | % |

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 14 |

Appendix 2: Business net income

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Q1 2026 | Biopharma | Other | Total group |

| (€ million) | Q1 2026 | Q1 2025 | Change | Q1 2026 | Q1 2025 | Change | Q1 2026 | Q1 2025 | Change |

| Net sales | 10,509 | | 9,895 | | +6.2 | % | — | | — | | — | % | 10,509 | | 9,895 | | +6.2 | % |

| Other revenues | 589 | | 617 | | -4.5 | % | 146 | | 94 | | +55.3 | % | 735 | | 711 | | +3.4 | % |

| Cost of sales | (2,987) | | (2,826) | | +5.7 | % | (69) | | (62) | | +11.3 | % | (3,056) | | (2,888) | | +5.8 | % |

| As % of net sales | (28.4 | %) | (28.6 | %) | | — | % | — | % | | (29.1 | %) | (29.2 | %) | |

| Business gross profit | 8,111 | | 7,686 | | +5.5 | % | 77 | | 32 | | +140.6 | % | 8,188 | | 7,718 | | +6.1 | % |

| As % of net sales | 77.2 | % | 77.7 | % | -0.5pp | — | % | — | % | | 77.9 | % | 78.0 | % | -0.1pp |

| Research and development expenses | (1,746) | | (1,808) | | -3.4 | % | (1) | | — | | — | % | (1,747) | | (1,808) | | -3.4 | % |

| As % of net sales | (16.6 | %) | (18.3 | %) | 1.7pp | — | % | — | % | | (16.6 | %) | (18.3 | %) | 1.7pp |

| Selling and general expenses | (2,266) | | (2,200) | | +3.0 | % | (61) | | (22) | | +177.3 | % | (2,327) | | (2,222) | | +4.7 | % |

| As % of net sales | (21.6 | %) | (22.2 | %) | 0.6pp | — | % | — | % | | (22.1 | %) | (22.5 | %) | 0.4pp |

| Other operating income/expenses | (1,187) | | (826) | | +43.7 | % | (3) | | (1) | | +200.0 | % | (1,190) | | (827) | | +43.9 | % |

| Share of profit/loss of associates and joint ventures1 | 47 | | 48 | | | — | | — | | | 47 | | 48 | | |

| Net income attributable to non-controlling interests | (4) | | (7) | | | — | | — | | | (4) | | (7) | | |

| Business operating income | 2,955 | | 2,893 | | +2.1 | % | 12 | | 9 | | +33.3 | % | 2,967 | | 2,902 | | +2.2 | % |

| As % of net sales | 28.1 | % | 29.2 | % | -1.1pp | — | % | — | % | | 28.2 | % | 29.3 | % | -1.1pp |

| | | | | | | | | |

| | | Financial income and expenses | (78) | | (68) | | +14.7 | % |

| | | Income tax expenses | (625) | | (622) | | +0.5 | % |

| | | Tax rate2 | (22.0 | %) | (22.3 | %) | |

| | | Business net income | 2,264 | | 2,212 | | +2.4 | % |

| | | As % of net sales | 21.5 | % | 22.4 | % | -0.9pp |

| | | | | | |

| | | Business EPS (in euros)3 | 1.88 | 1.79 | +5.0 | % |

1 Net of tax.

2 Determined based on business income before tax, associates, and non-controlling interests.

3 Based on an average number of shares outstanding of 1,204.2 million in Q1 2026 and 1,233.9 million in Q1 2025.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 15 |

Appendix 3: Consolidated income statement

| | | | | | | | | | |

| (€ million) | Q1 2026 | Q1 2025 | | |

| Net sales | 10,509 | | 9,895 | | | |

| Other revenues | 735 | | 711 | | | |

| Cost of sales | (3,138) | | (2,889) | | | |

| Gross profit | 8,106 | | 7,717 | | | |

| Research and development expenses | (1,747) | | (1,808) | | | |

| Selling and general expenses | (2,327) | | (2,222) | | | |

| Other operating income | 282 | | 331 | | | |

| Other operating expenses | (1,472) | | (1,158) | | | |

| Amortisation of intangible assets | (535) | | (399) | | | |

| Impairment of intangible assets | — | | (25) | | | |

| Fair value remeasurement of contingent consideration | 35 | | (9) | | | |

| Restructuring costs and similar items | (119) | | (105) | | | |

| Other gains and losses, and litigation | (102) | | (37) | | | |

| | | | |

| Operating income | 2,121 | | 2,285 | | | |

| Financial expenses | (178) | | (213) | | | |

| Financial income | 60 | | 86 | | | |

| Income before tax and associates and joint ventures | 2,003 | | 2,158 | | | |

| Income tax expense | (420) | | (481) | | | |

| Share of profit/(loss) of associates and joint ventures | 11 | | 42 | | | |

| Net income from continuing operations | 1,594 | | 1,719 | | | |

Net income from discontinued operations | 26 | | 174 | | | |

| Net income | 1,620 | | 1,893 | | | |

| Net income attributable to non-controlling interests | 6 | | 21 | | | |

| Net income attributable to equity holders of Sanofi | 1,614 | | 1,872 | | | |

| Average number of shares outstanding (million) | 1,204.2 | | 1,233.9 | | | |

| Basic earnings per share from continuing operations (€) | 1.32 | | 1.39 | | | |

| Basic earnings per share from discontinued operations (€) | 0.02 | | 0.13 | | | |

| Basic earnings per share (€) | 1.34 | | 1.52 | | | |

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 16 |

Appendix 4: Reconciliation of net income attributable to equity holders of Sanofi to business net income

| | | | | | | | | | |

| (€ million) | Q1 2026 | Q1 2025 | | |

| Net income attributable to equity holders of Sanofi | 1,614 | | 1,872 | | | |

| Net income from discontinued operations | (26) | | (174) | | | |

| Amortisation of intangible assets1 | 535 | | 399 | | | |

| Impairment of intangible assets | — | | 25 | | | |

| Fair value remeasurement of contingent consideration | (33) | | 13 | | | |

| Expenses arising from the impact of acquisitions on inventories | 82 | | — | | | |

| | | | |

| Restructuring costs and similar items | 119 | | 105 | | | |

| Other gains and losses, and litigation | 102 | | 37 | | | |

| Financial (income) / expense related to liabilities carried at amortised cost other than net indebtedness | 40 | | 59 | | | |

| | | | |

| Tax effect of the items listed above: | (181) | | (146) | | | |

| Amortisation and impairment of intangible assets | (94) | | (69) | | | |

| Fair value remeasurement of contingent consideration | 8 | | (3) | | | |

| Expenses arising from the impact of acquisitions on inventories | (19) | | — | | | |

| Restructuring costs and similar items | (23) | | (27) | | | |

| | | | |

| Other items | (53) | | (47) | | | |

| Other tax effects | (24) | | 5 | | | |

| Other items | 36 | | 16 | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| Business net income | 2,264 | | 2,212 | | | |

Business earnings per share (€)2 | 1.88 | | 1.79 | | | |

Basic earnings per share (€)2 | 1.34 | | 1.52 | | | |

1 Of which related to amortisation expense generated by the intangible assets measured at their acquisition-date fair values: €512 million in Q1 2026 and

€386 million in Q1 2025.

2 Based on an average number of shares outstanding of 1,204.2 million in Q1 2026 and 1,233.9 million in Q1 2025.

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 17 |

Appendix 5: Change in net debt and summarised statements of cash flow

| | | | | | | | | | |

| (€ million) | Q1 2026 | Q1 2025 | | |

| Business net income | 2,264 | | 2,212 | | | |

| Depreciation, amortisation and impairment of property, plant and equipment and software | 345 | | 349 | | | |

| Other items | (160) | | (380) | | | |

| Operating cash flow | 2,449 | | 2,181 | | | |

| Changes in working capital | (347) | | (96) | | | |

| Acquisitions of property, plant and equipment and software | (520) | | (490) | | | |

| Free cash flow before restructuring, acquisitions, and disposals | 1,582 | | 1,595 | | | |

| Acquisitions of intangibles assets, investments, and other long-term financial assets1 | (322) | | (623) | | | |

| Restructuring costs and similar items paid | (317) | | (287) | | | |

Proceeds from disposals of property, plant, and equipment, intangible assets, and other non-current assets net of taxes1 | 111 | | 344 | | | |

| Free cash flow | 1,054 | | 1,029 | | | |

| Acquisitions2 | (1,703) | | — | | | |

Proceeds net of taxes2 | 56 | | — | | | |

| Issuance of Sanofi shares | 8 | | 22 | | | |

| Acquisition of treasury shares and related tax effect | (806) | | (3,609) | | | |

| Dividends paid to shareholders of Sanofi | — | | — | | | |

| Other items | (316) | | 82 | | | |

| Net cash in/(out)flow from Opella transaction | (185) | | — | | | |

| Net cash provided by/(used in) the discontinued Opella business | — | | 161 | | | |

| Change in net debt before Opella reclassification to “Assets held-for-sale” | (1,892) | | (2,315) | | | |

| Opella net debt reclassified to held for sale as of December 31, 2024 | — | | (158) | | | |

| Change in net debt | (1,892) | | (2,473) | | | |

| Beginning of period | 11,008 | | 8,772 | | | |

| Closing of net debt | 12,900 | | 11,245 | | | |

| | | | | | | | |

(€ million) | Q1 2026 | Q1 2025 |

| Net cash provided by/(used in) continuing operating activities | 1,683 | | 1,908 | |

| Net cash provided by/(used in) operating activities of the discontinued Opella business | — | | 185 | |

| Net cash provided by/(used in) operating activities | 1,683 | | 2,093 | |

| Net cash provided by/(used in) continuing investing activities | (2,093) | | (767) | |

| Net cash provided by/(used in) investing activities of the discontinued Opella business | — | | (9) | |

| Net cash in/(out)flow from the Opella transaction | (185) | | — | |

| Net cash provided by/(used in) investing activities | (2,278) | | (776) | |

| Net cash provided by/(used in) continuing financing activities | (1,527) | | (584) | |

| Net cash provided by/(used in) financing activities of the discontinued Opella business | — | | (8) | |

| Net cash provided by/(used in) financing activities | (1,527) | | (592) | |

| Impact of exchange rates on cash and cash equivalents | 9 | | (20) | |

| Cash and cash equivalents reported as held for sale as of December 31, 2024 | — | | (154) | |

| Net change in cash and cash equivalents | (2,113) | | 550 | |

| Cash and cash equivalents, beginning of period | 7,657 | | 7,441 | |

| Cash and cash equivalents, end of period | 5,544 | | 7,991 | |

| | |

1 Free cash flow includes investments and divestments not exceeding a cap of €500 million per transaction (inclusive of all payments related to the

transaction).

2 Includes transactions that are above a cap of €500 million per transaction (inclusive of all payments related to the transaction).

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 18 |

Appendix 6: Simplified consolidated balance sheet

| | | | | | | | | | | | | | | | | | | | |

Assets (€ million) | March 31, 2026 | December 31, 2025 | | liabilities and equity (€ million) | March 31, 2026 | December 31, 2025 |

| | | | Equity attributable to equity holders of Sanofi | 72,808 | 71,376 |

| | | | Equity attributable to non-controlling interests | 335 | 334 |

| | | | Total equity | 73,143 | 71,710 |

| | | | Long-term debt | 12,298 | 14,248 |

| Property, plant, and equipment – owned assets | 10,157 | 10,052 | | Non-current lease liabilities | 1,542 | 1,467 |

| Right-of-use assets | 1,517 | 1,459 | | Non-current liabilities related to business combinations and to non-controlling interests | 606 | 585 |

| | | | | | |

| | | | | | |

| Intangible assets (including goodwill) | 69,086 | 67,561 | | Non-current provisions and other non-current liabilities | 6,664 | 6,703 |

| Non-current income tax assets | 556 | 550 | | Non-current income tax liabilities | 2,143 | 2,081 |

| | | | | | |

| | | | | | |

| | | | | | |

| Other non-current assets, investments in associates and joint-ventures and deferred tax assets | 16,544 | 16,231 | | Deferred tax liabilities | 1,620 | 1,666 |

| Non-current assets | 97,860 | 95,853 | | Non-current liabilities | 24,873 | 26,750 |

| | | | | | |

| | | | | | |

| | | | Accounts payable and other current liabilities | 22,708 | 22,926 |

| | | | Current liabilities related to business combinations and to non-controlling interests | 0 | 0 |

| | | | | | |

| | | | | | |

| | | | | | |

| Inventories, accounts receivable and other current assets | 23,503 | 22,690 | | Current income tax liabilities | 942 | 751 |

| Current income tax assets | 482 | 397 | | Current lease liabilities | 260 | 272 |

| Cash and cash equivalents | 5,544 | 7,657 | | Short-term debt and current portion of long-term debt | 5,921 | 4,342 |

| Assets held for sale | 635 | 208 | | Liabilities related to assets held for sale | 177 | 54 |

| Current assets | 30,164 | 30,952 | | Current liabilities | 30,008 | 28,345 |

| Total assets | 128,024 | 126,805 | | Total equity and liabilities | 128,024 | 126,805 |

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 19 |

Appendix 7: Currency sensitivity

2026 net sales and business EPS currency sensitivity

| | | | | | | | | | | |

| Currency | Variation | Net sales sensitivity | Business EPS sensitivity |

| US Dollar | +0.05 USD/EUR | -€1,069 | m | -€0.23 |

| Japanese Yen | +5 JPY/EUR | -€46 | m | -€0.02 |

| Chinese Yuan | +0.2 CNY/EUR | -€60 | m | -€0.02 |

| Brazilian Real | +0.4 BRL/EUR | -€44 | m | -€0.01 |

Currency exposure on Q1 2026 sales

| | | | | |

| Currency | Q1 2026 |

| US Dollar | 51.0 | % |

| Euro | 17.8 | % |

| Chinese Yuan | 5.9 | % |

| Japanese Yen | 2.8 | % |

| Brazilian Real | 2.4 | % |

| Canadian Dollar | 1.4 | % |

| Russian Ruble | 1.3 | % |

| British Pound | 1.3 | % |

| Turkish Lira | 1.2 | % |

| Australian Dollar | 1.1 | % |

| Others | 13.8 | % |

Currency average rates

| | | | | | | | | | | | | | |

| Q1 2025 | Q1 2026 | Change | | | |

| Euro/US Dollar | 1.053 | | 1.171 | | +11.2% | | | |

| Euro/Japanese Yen | 160.396 | | 183.590 | | +14.5% | | | |

| Euro/Chinese Yuan | 7.666 | | 8.103 | | +5.7% | | | |

| Euro/Brazilian Real | 6.160 | | 6.154 | | -0.1 | % | | | |

| Euro/Russian Ruble | 98.140 | | 91.873 | | -6.4 | % | | | |

| | | | | |

SANOFI PRESS RELEASE Q1 2026 | 20 |

Appendix 8: Definitions of non-IFRS financial indicators

Company sales at constant exchange rates

References to changes in net sales “at constant exchange rates” (CER) means that it excludes the effect of changes in exchange rates.

The effect of exchange rates is eliminated by recalculating net sales for the relevant period at the exchange rates used for the previous period.

Reconciliation of net sales to company sales at CER

| | | | | | |

| (€ million) | Q1 2026 | |

| Net sales | 10,509 | | |

| Effect of exchange rates | (733) | | |

| Company sales at constant exchange rates | 11,242 | | |

Business gross profit

Business gross profit is a non-IFRS indicator that fully excludes from gross profit under IFRS the effect of the release of the fair value step-up to inventory that is recognised upon acquisition which constitutes a business combination under IFRS 3 ‘Business combinations’ or which is part of a group of assets as per IFRS 3§2b.

Business net income

Sanofi publishes a key non-IFRS indicator. Business net income is defined as net income attributable to equity holders of Sanofi excluding:

•net income from discontinued operations,

•amortisation of intangible assets,

•impairment of intangible assets,

•fair value remeasurement of contingent consideration related to business combinations or to disposals,

•expenses arising from the impact of acquisitions on inventories,

•restructuring costs and similar items (comprising transaction, integration, and separation costs in relation to major acquisitions and disposals)1,

•other gains and losses (including gains and losses on disposals of non-current assets1),

•costs or provisions associated with litigation1,

•financial (income)/expense related to liabilities carried at amortised cost other than net indebtedness,

•tax effects related to the items listed above as well as effects of major tax disputes,

•the share of profits/losses from investments accounted for using the equity method, except for the share of profits/losses from investments accounted for using the equity method, to the extent that this relates (i) to joint ventures or (ii) to associates with which Sanofi has entered into R&D agreements and/or whose operations are managed as an integral part of Sanofi’s business activities; and,

•net income attributable to non-controlling interests related to the items listed above.

Free cash flow

Free cash flow is a non-IFRS financial indicator which is reviewed by management, and which management believes provides useful information to measure the net cash generated from Sanofi’s operations that is available for strategic investments2 (net of divestments2), for debt repayment, and for capital return to shareholders. Free cash flow is determined from the business net income adjusted for depreciation, amortisation, and impairment, share of profit/loss in associates and joint ventures net of dividends received, gains and losses on disposals, net change in provisions including pensions and other post-employment benefits, deferred taxes, share-based expense, and other non-cash items. It comprises net changes in working capital, capital expenditures and other asset acquisitions3 net of disposal proceeds3, and payments related to restructuring and similar items. Free cash flow is not defined by IFRS, and it is not a substitute measure for the IFRS aggregate net cash flow in operating activities.

1 Reported in the line items restructuring costs and similar items and gains and losses on disposals, and litigation.