Exhibit 99.7

V A LU A T ION REP O R T CON S I DERING THE M A RKET V A L U ES O F 1 00 ƒ / o E Q UITY INTERE S T OF KIKA TE C HN O LO G Y INC. Cli e nt : KIKA TECHNOLOGY INC. Co n tact N o . : KKG202 5 J 0 1 0006 Report d ate : 1 2 Nov e mber 2025

K I NC KEE 2 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . 1 2 Nove m ber 2025 T he Di r ectors KIKA TE C HNOLOGY IN C . Dear Si r s , In accordance with y our i n s truct i o n s, we have und e rtake n an i n v e s ti g ation and anal y s i s to e x pr es s an independent opinion of 1 OOo / o equ i ty value of KIKA T e ch n o l ogy INC . ( " KIK A " or t h e " Compan y " ) a s at 3 0 June 2025 ( t he " V aluation D a t e " ) . T h e report which follo w s i s d a ted 12 N ov e mber 2025 ( t h e " R eport Dat e " ) . T h e purp o se of th i s valuation i s to e xpr e s s an i n depend e nt opinion of t h e fair v a lue of 10 0 % equ i ty value of KIKA for i n t e rnal re f e rence . Our v a luation was carried out on a f air v a l u e b a sis . Fa i r v a l u e is def i ned a s " t h e price that wo u l d be received to s e ll an a s s e t , or paid to transfer a liabili t y , in an ord e rly t ra n s a c tion b e twee n m arket participa n t s at t h e m easur e ment dat e " .

K I NC KEE 3 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . We ha v e conduct e d our valuation in accordance with I n ternational Val u . ation Standar d s i s s ued by the International Valuation Standards Council and US Generally A ccepted Acco u nting Pri n ciple s . W e planned and per f or m e d our valuation so as to obta i n all t he infor m ation and explanations which we co n sid e r e d n ec e s sary i n order to provide u s with sufficient evidence to e xpr e s s our opinion on the subje c t a s s e t . We believe that t he valuation pr o cedur e s we employe d provide a re a s onab l e basis for our opinion . Our valuation of the 1 00 % equity i n ter e st in KIKA w a s de v e l op e d thro u gh the applic a tion of an i nco m e approach kno w n a s discou n t c a sh flow m e thodology . Under di s cou n t cash flow m ethod, t he equity r e s ult depends on t he pr e s ent w o 1 th of future economic benefits to be derived from the pr o jecte d sal e s income . Indication of t h e r e sult is developed by di s cou n ting pr o j e c ted f u ture n e t c a sh flows avai l able for pa y m ent of shareholde r s' inter e st to t h eir pr e sent worth . As part of our anal y si s , we have revie w e d informat i on prepar e d by the Company and relevant op e rational infor m ation reg a rding the subject b u sin e ss f rom public s ourc e s . We h a ve rel i ed to a co n s i d e rable e x tent on such i n for mation in arriving at our opinion of value . T h e conclusion of value i s ba s ed on accepted valuation procedur e s and practic e s that rely su b s ta n tially on our use of numero u s a s sumpt i o n s and our co n sid e r ation of various factors t h a t are rel e va n t to t h e oper a t i on of Company . We ha v e a l s o consid e red var i ous r i s k s and uncertainti e s t hat ha v e pot e ntial impact on t h e b u s ine s s e s . Fur t her, while t h e a s sumptio n s and co n s i d e ration of such m a t ters are considered by us to be re a sona b l e , they are inh e rently subj e ct to s ignificant busi n e ss, economic and compet i tive unce rtai n ti e s and conting e nci e s , many of which a re be y ond the con t rol of t h e Co m pany and King Kee A ppra i sal and Adv i sory Limited (" KK G " ) . We do not int e nd to e x pr e ss any opinion on m atters w hich require legal or oth e r specialized e x p e rt i se or know ledge, be y ond what is custom a rily emplo y ed by valu e r s . Our conclusio n s a ssume continuation of prude n t m anage m e n t of the Comp a ny ov e r wh a te v e r per i od of ti m e that is re a s o nable and n ece ssary to m ai n tain t he charact e r and integrity of t h e a ss e t s valued .

K I NC KEE 4 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . T h e pr o spe c ti ve financial i nf or m ation ( " PF I " ) is b a sed on judgm e ntal e stim ate s and a s s umptions m ade by t he Company 's m anage m e n t abo u t circu m s tanc e s and e ven t s t hat ha v e not y et ta k e n place. In p e r f orming i t s valuation, KKG h a s c hal l e ng e d m ana g e m ent ' s a ssumptio n s, e stim ate s, or c a sh flow projectio n s with r e s p ect to t h e future perfor m ance of the Compan y , whic h invol v e m a t t e r s of opinion, projection, or forec a st ( w h e th e r or not expr e ss l y stat e d). T h e f orecast of future de v e l opm en t s i s m ade so le l y for the purp o s e s of t h e v a luatio n . We ha v e not provided any opinion or any type of a s s ur a nce about s pecific a s sumptio n s or compo ne n ts of t h e PFI or on t h e PFI a s a w hole. T h e re w ill u su a lly be dif f e renc e s b e t w een e stim a ted and a c tual r e su l t s , b eca u s e e v ents and c i r cu m stanc e s freque n tly do not occur a s expe c t e d , and tho s e dif f erenc e s may b e m at e r i a l. We take no r e spo n s ibility for t h e a c h i eve m e n t of projected r e sul t s , if any. Ba s ed on t h e i n v e s t i g a t ion and analy s e s outlined in t h e repo rt w h i c h follow s , w e are of t h e op i nion that t h e f air v a l u e of 10 0 % eq u i t y v a l u e of KIKA a s at t h e V alu a t i on D a te is reasonably s tated a s be l o w : I n U SD ' OOO 8 0 , 000

K I NC KEE 5 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Richard Z ang Managing Dir e ctor A S A, MRIC S , CPV • Any conclusions. and op i nio n s our in formulating emplo y ed T h e follo w i ng pag e s outl i ne t h e fa c tors co n sidered, methodo l ogy and a s s umptio n s op i nions are subj e c t to t he a s s umptio n s and limiting conditio n s contai n ed t h e rein. Yo u rs faithf u ll y , F or and on behalf of K i ng Kee Appra i sal and Ad v i s ory L imited

K I NC KEE 1 Valuat i on R e p o rt - 1 00% E q uity I nter e s t of K I KA T e c h n o lo g y I NC . REMARK: T A BLE OF CONTENTS Th i s report has b e e n prepared solely for the internal us e pu r pose . The r eport should not be other - i - v ise r e ferred to, in - i - vhole or in part, or quoted in any do c ument, c ir c ular or statement in any manner, or d i stributed in whole or i n pa r t or c o pied to any their pa rty - i - v ithout ou r prior - i - vr i tten conse n t. W e shall not under a ny cir c umstances whatsoever be liable to any third party except where we sp e cifi c ally agr e ed in writing to accept such liability. • Intro d uct i on 2 • P u rpose of Va l uat i o n 2 • Basi s o f Va l ue 2 • Basi s o f O p i n i on 2 Th i s report and the c onclusion of values arrived at her e in ar e for the exc l usive use of our c lien t for the sole a nd specific purpos e s as noted herein. Furthermo r e , the r e port and con c lusion o f valu e s a r e not i n tended by the autho r , and should not be c onstrued by the reader, to be inv e stment a d vi c e in any manner whatsoever. The con c lusion o f valu e s r epresents the consideration b a sed on informat i o n furnished by the Company/engagement parti e s and other sources. • C o mpany Bac k g ro u nd 3 • So u rces o f I nf o rmati on 4 • Method o l o gy 5 • M a j o r As s umpt i o ns 7 • Disc o unt Ra t e 9 • Va l uat i o n C o m m ents 12 • Risk Fact o rs 1 3 • Op i n i o n of Va l ue 1 4 • Ex h ib i t A - L i m i ti n g Co n d i t i o ns 1 5 • Ex h ib i t B - Va l uers' P rofessi o nal Dec l arat i o n 1 8 • Ex h ib i t C - Va l uat ion Res u l t o f C o mpany 1 0 0 % Eq u i ty 1 9 • Ex h i b i t E - C o mparab l e Company M ark e t I nf o rmat i o n 22

K I NC KEE 2 Valuat i on R e p o rt - 1 00% E q uity I nter e s t of K I KA T e c h n o lo g y I NC . Introd u ction Th i s r e port h a s been pr e par e d in accordance with ins t ructio n s from y ou to e x pr e s s an i n d e pend e nt opinion of t h e f air value of 1 OOo / o equity v alue of KIKA T e chnology INC. ( " KIK A " or t h e " Comp a n y " ) a s at 30 Ju n e 2025 (t h e " Valu a t i on Dat e " ). T h e report w h i ch follo w s i s dated 12 N ov e mbe r 20 2 5 (t h e " Report Dat e " ). Pu r pose of V a lu a tion The purp o s e of this valuation is to e xpr e ss an i n depende n t opinion of t h e 1 00 % equity value of KIKA a s a t Valu a tion Date f or internal re f e rence only . B a sis of Val u e Our valuation w a s c a rried out on a fair v alue b a s is . F air value is defin ed a s " t h e pr i ce that wou l d be received to s ell an as s e t, or pa i d to tr a nsfer a liabil i ty, in an ord e rly tra n s a c t i on be t w een m a rk e t part i cip a n t s at the m e a s ure m e n t dat e " . Basis of Opinion We ha v e condu c ted our valuation in accordance w i th I n t e rnational Valuation Stand a r d s i ssued by the International Valu a tion Standards Council and US G e nerally Accepted A ccounting Pri n ciple s . W e p lanned and p e rfor m ed our valu a t i on s o a s to obtain all t he in f or m ation and e x planations which w e consid e red n ecessary in ord e r to provide us w i th su f ficient e v i d e nce to e x pr e ss our opin i on on t h e subject as s e t . T h e valu a t i on pr o cedur e s e mployed include t h e review of ph y s i cal and econom i c cond i tion of the s ubject a ss e t, an a ss e ss m e nt of key a s sumpt i o n s, est i m at e s, and repr e sentatio n s made by t h e propr i e tor or t h e op e rator of t h e subject a ss e t . All m a tt e r s w e consider e ss ential to t h e prop e r understanding of t h e valuation will be d i sclo s ed in t h e valuation r e port .

K I NC KEE 3 Valuat i on R e p o rt - 1 00% E q uity I nter e s t of K I KA T e c h n o lo g y I NC . T he foll o wi n g facto r s form an i n tegr a l part o f o u r basis o f o p 1 • n 1 • on: • A s sumpti o ns on t h e m ark e t and t h e as s e t t hat are co n sid e red to be f air and re a s onab l e; • Financial performance that shows a co n si s te n t t r end of t h e op e r a tion; • Co n s ideration and analy s is on t h e micro and m a c ro economy af f ecting t h e subject a ss e t ; • Analysis on ta c t i cal planning, m anage m e nt s tandard and sy n e rgy of t h e subject a ss et; • Anal y tical revi e w of th e s ubject a ss e t ; and • A s s e ss m ent of t h e l e v e rage and liquidity of t h e subje c t a ss et. Company Backgr o und T h e company tak e s i ndependentl y de v elop e d t e chnology a s its core driving forc e , continuo u s l y d e epen s i t s pr e s ence in t h e compr e h ensi v e s ervice field, and rel i e s on so lid techno l ogical accumu l ation and in n ovative barriers to create all - round, h i gh - pro f e ss ional cu s tomized so lut i o n s f or custo m e rs . T he c ore busin e ss f o cus e s o n two high - va l ue c ore segm e nts : one i s the i n d u s t ry - leading AdTech dyna m ic m atching tech n o logy servi c e, a nd th e o th e r i s e n t e rpr i se - level hig h - valu e - added customized s o ftware develop m e n t . All bu s in e ss e s a chieve full chain indep e nd en t a n d irreprodu c ible industry te c hnology . c o n trollable te c hn o logy, a n d build c o m p e titive b a rri e r s with o riginal

K I NC KEE 4 Valuat i on R e p o rt - 1 00% E q uity I nter e s t of K I KA T e c h n o lo g y I NC . Sources of In f ormation We also conduct e d r e s e arch government s t a t i s ti c s and ot h er publicatio n s . us ing vanous sourc es i n cluding Our v aluation is ba s ed on data and in f or m ation furnis h ed by the Company 's mana g e m ent limited t o , t h e follo w in g ; ( " M anage m en t " ), which includ e s , but not to v e rify the and w e believe re a s onable n e ss and f airn e s s of informat i on provided t h a t the in f ormation i s re a s onable and reliable. Background in f or m a tion and future b u si n e s s plan of Company ; Manage m ent accoun t s of Company end e d 3 0 Jun e 2 02 4 , and 3 0 June 2 025 ; C o m p any 's future busi n e s s plan including sal e s forecast from 2026 to 2 0 3 5 ; O t her operational and m arket in f or m ation in relation to t he Com p an y ' s b u si n e ss . W e ha v e a l s o di s c u s sed and e xami n e d ot h er operational and b u si n e s s inform a tion through i n ter v iew s w ith releva nt s enior m anagement . We have reli e d to a co n sid e rable e xt e nt on such in f or m ation in arriving at our opin i on of value . We assumed that t h e data w e obt a ined in t he cour s e of t h e valuati o n, a l ong with t h e opinio n s and repr e se n t a t i o n s provided to us by t h e Compan y , are t rue and accurate .

K I NC KEE 5 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Methodology In arriving at our a s s e s s ed valu e , we h a v e co n sidered thr e e ge n e r ally accepted approac h e s , na m e l y , m ark e t approac h , cost approac h and inco m e approach . C o s t Approa c h co n s i d e r s t h e cost to reproduce or r e place in new condit i on t he a s se t s apprai s e d in accordance with curre n t m ar k e t pric e s f or s i milar a s s e t s , with allowance f or accrued depr e ciation or o b s ol e scence pr e sen t , w h e t h er arising from physical, fun c tional or economic caus e s . T h e cost approa c h g e n erally furnis h e s t h e m ost reliable i ndication of v alue f or a s sets without a known secondary mark e t . M ark e t Approach co n sid e r s pric e s recently paid for s i milar a ss e t s , w i th adju st m e n ts m ade to m ark e t pric e s to r e flect condition and utility of t h e apprai s ed a ss e t s relative to t h e m ark e t comparative . A ss e t s f or which t h ere is an e stablis hed s econdary m ark e t m ay be v alued by t his approach . D e spite t h e simplicity and tra n sparency of t his appr o ac h , it do e s not dire c tly incorporate in f or m ation about t h e contributed by t h e subj e ct as s e t. . economic be n e fi t s Benefits of using this approach include i t s s i mplicity, clarit y , speed and t he n eed for f ew or no a s sumptio n s . I t al s o in t roduc e s objectivity in application as public l y a v ailable inpu t s are u sed . Howeve r , o n e has to be wary of t h e hidden a s sumptio n s in th o s e inp u ts a s t h e re are inh e r ent a s sumptio ns on t h e value of th o s e comparable a s s e t s . I t is al s o diffi c ult to find comparab l e a s se t s . Furt h e r m or e , this approach reli e s e xclusivel y on t h e efficient m ark e t h ypot h e s i s .

K I NC KEE 5 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Methodology (c o ntin u ed) In c ome App r oach is t h e con v ersion of expected p e riodic benefits of ow n ership into an indic a tion of v a l u e . It is ba s ed on t h e pr i nciple that an informed b u yer wo u ld pay no m ore f or t h e pr o je c t than an a mount equ a l to t h e pr e s ent w o 1 th of anticipat e d future b e n efi t s (incom e ) from t h e s a m e or a s u b sta n ti a l l y s im i lar pr o je c t with a sim i lar risk profile . Selecti o n of Val u ation Approach and Met h odology In our opinion, m anag e m e nt provided t he d e tail e d cash f l ow for e c a s t s of Compan y , and t h e s e compani e s operat e s s u stainabl y , thus we believe that t h e i n co m e m ethod is s uita b l e f or t h e v a luation of t h e Company 's equity value . W e have t h e re f o re rel i ed s olely on t h e income appr o ach in d e t e 1 m i ning our opinion of v a l u e . Income approach Th i s approac h allo w s f or t h e pr o sp e c ti ve v a luation of future profits and t h ere are numero u s empiric a l and t heor e tical ju s tificatio n s for t h e pr e s ent v a l u e of e xpect e d future cash flow s . Ho w e v e r, this approach reli e s on nu m erou s a ssum p tio n s o v e r a long time hori z on and t h e r e sult m ay be very s e n sit i ve to certain inpu t s . I t also pr e sen t s a s i n g l e scenario only . In this s tud y , t he v a luation r e sult w a s developed through the application of an inco m e approach technique known a s discou n ted c a sh f l ow method to de v ol v e t h e future v a l u e of t h e b u s i n ess into a pr e s ent mar k e t v a l u e . Th i s m e thod e lim i na t e s t he di s c repancy i n t i m e v a l u e of m o n ey by u sing a di s count rate to refle c t all b u si ne s s risks inclu d ing i n tri n sic and extri n sic unce rtainti e s in relation to t h e b u sin e s s . Und e r this m e tho d , t h e r e sult depends on t h e pr e s ent wo r t h of f u ture economic b e n efi t s to be d e ri v e d from t h e proje c t e d s er v i c e i n co m e . Indicatio n s of t h e r e sult ha v e be e n develop e d by d i s cou n ting pr o jected future n e t c a sh flows available f or pay m e n t of shareh o l d e r s' i n ter e s t to t h eir pr e se n t w orth at discount rat e s which in our opin i on are appropriate for t h e r i s k s of t h e b u sin e s s . In co n sid e ring t he appropr i ate di s count rate to be applie d , w e ha v e taken into account a number of fact o r s including t h e curr e nt c o st of finance and t he co n s id e red risk inh e r ent in t h e busi n e s s .

K I NC KEE 6 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Ma j or Assumptio n s As sumptions co n s idered to ha v e s ignificant s e n sit i vity e f f ec t s i n this valua t i on have been e valuated in ord e r to provide a m ore accur a te a nd re a sonab l e basis f or arriving at our a s s e s s e d value . T h e re are no h i dden or u n e x pect e d condit i o n s a ss ociat e d wi t h t h e a ss e t s valu e d that mig h t adve r sely af f ect t h e r e ported value . Furt h e r, w e a s sume no r e s po n sibility f or c hang e s i n m arket conditio n s after t h e V aluation D ate . In d e term i ning t he fair value of e quity i nt e r e st in t he Compan y , t h e f ol l o w ing key a s s u m ptio n s have b e e n m ad e : T h e facil i ti e s and sy s te m s propo s ed are a s su m ed to be sufficie n t f or future expa ns ion in order to r e alize t he growth pote n tial of t h e b u sin e s s and m aintain a comp e titi v e e dge . T h e re will be no material c han g e in t h e existing politica l , legal, tech n ologica l , f i s cal or economic conditio n s, which mig h t ad ve r sely af f ect t h e b u sin e s s of th e Company T h e projected b u s i n e s s p e r f or m an c e c an be a c hieved with t h e ef f ort of t he m anag e m ent of t h e Compan y . T h e financial and op e rational inform a t i on provided to us by t h e Company is true and accurate .

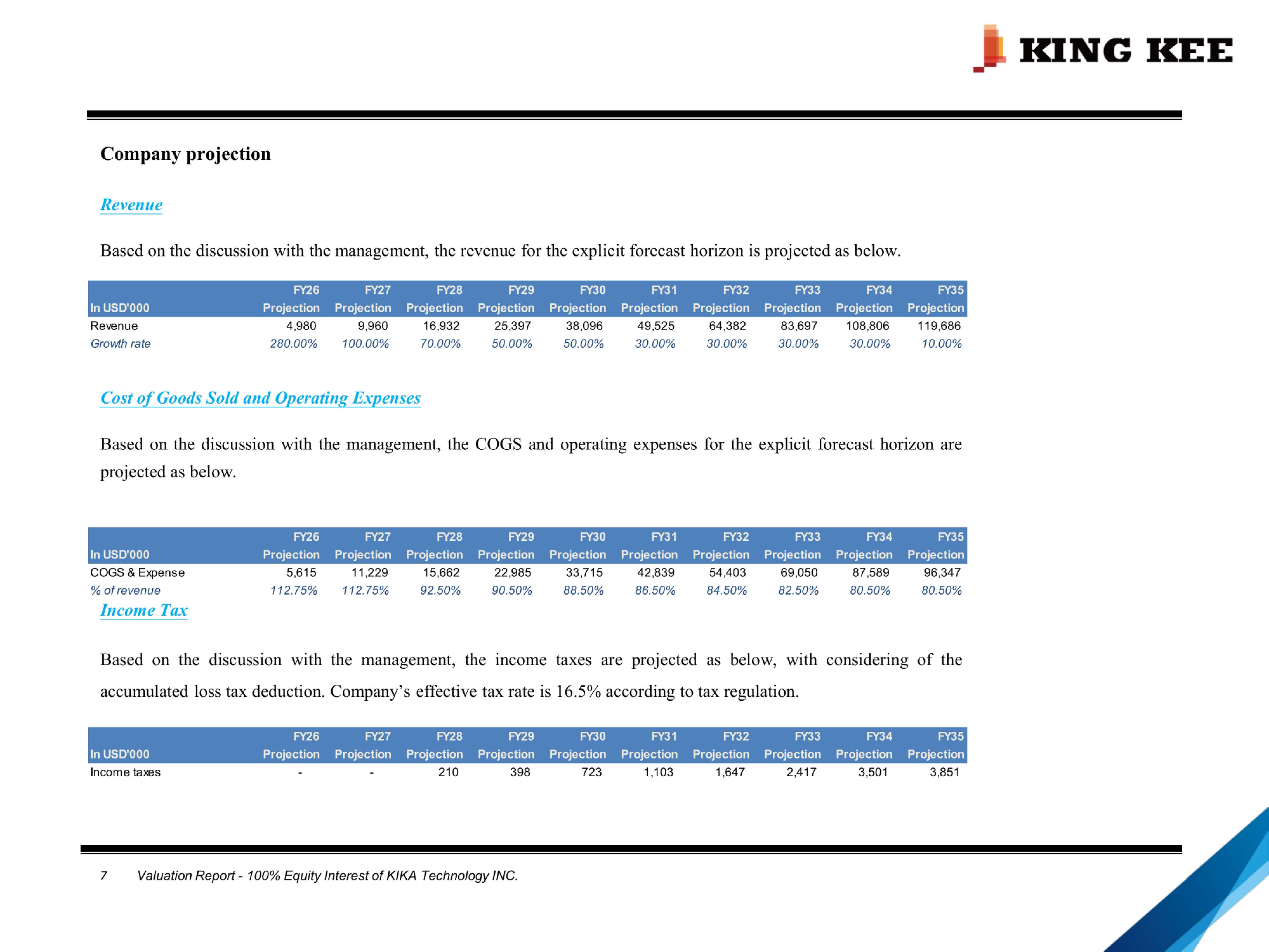

K I NC KEE Company pr o ject i on R evenue B a sed on t h e d i s c u s s i on w i th t h e m ana g e m e n t, t h e r e v e nue f or t h e e x p l i c i t f orec a st hor izon i s projected a s bel o w . C ost o_[ G oo ds S o ld and Opera t i ng Expen s es Ba sed on t h e di s cu s sion with t h e manage m e n t, t h e CO G S and op e rating e xpe n s e s f or t h e e x p l icit forecast horizon are pr o je c ted a s below. In c ome Tax B a sed on t h e disc u s s ion with t h e manageme n t, t h e income tax e s are proje c t e d a s b e l o w , with co n s idering of the accu m u l at e d l o s s tax d e du c tion. Company ' s ef f ec ti ve tax rate is 1 6.5% according to tax regulation. 7 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . I n U S D ' OOO I ncome taxes 2 1 0 398 723 1 , 1 03 1 ,647 2,4 1 7 3 , 501 3 , 851 F Y 3 5 F Y3 4 F Y3 3 F Y3 2 F Y 3 1 F Y 3 0 F Y 2 9 F Y 2 8 F Y 2 7 F Y 2 6 I n U S D ' OOO P r o ject i o n P r o ject i o n P roject i on P roject i on Projec t i on Project i on P r o ject i on P r o ject i o n P r o ject i o n P r o jecti on 11 9 , 686 1 0 8 , 806 83 , 697 64 , 382 49 , 525 38 , 096 25,397 1 6,932 9 , 960 4 , 980 Revenue 1 0. 0 0% 30 . 0 0% 30 . 00% 30 . 00% 30 . 00% 50.00% 50.00% 70.00% 1 00. 0 0% 280 . 0 0% Growth ra t e F Y 3 5 F Y 3 4 F Y 3 3 F Y3 2 F Y 3 1 F Y 3 0 F Y 2 9 F Y 2 8 F Y 2 7 F Y 2 6 I n U S D ' OOO P r o ject i o n P r o ject i o n P r o jecti on P roject i on Proje c t i on Project i on P r o ject i on P r o ject i o n P r o ject i o n P r o jecti on 9 6 , 347 8 7 , 589 69 , 050 54 , 403 4 2 , 839 33 , 7 1 5 22 , 985 1 5 ,662 1 1 , 229 5 , 6 1 5 COGS & Expense 80.50% 80 . 50% 82 . 50% 84 . 50% 86 . 50% 88.50% 90.50% 9 2 . 50% 1 1 2 . 75% 112 . 75% % of revenue m s m 4 m 3 m 2 m1 mo m g m a m 1 m s P r o ject i o n P roject i o n P roject i on P roject i on Projec t i on Project i on P r o ject i o n P r o ject i o n P roject i o n P roject i on

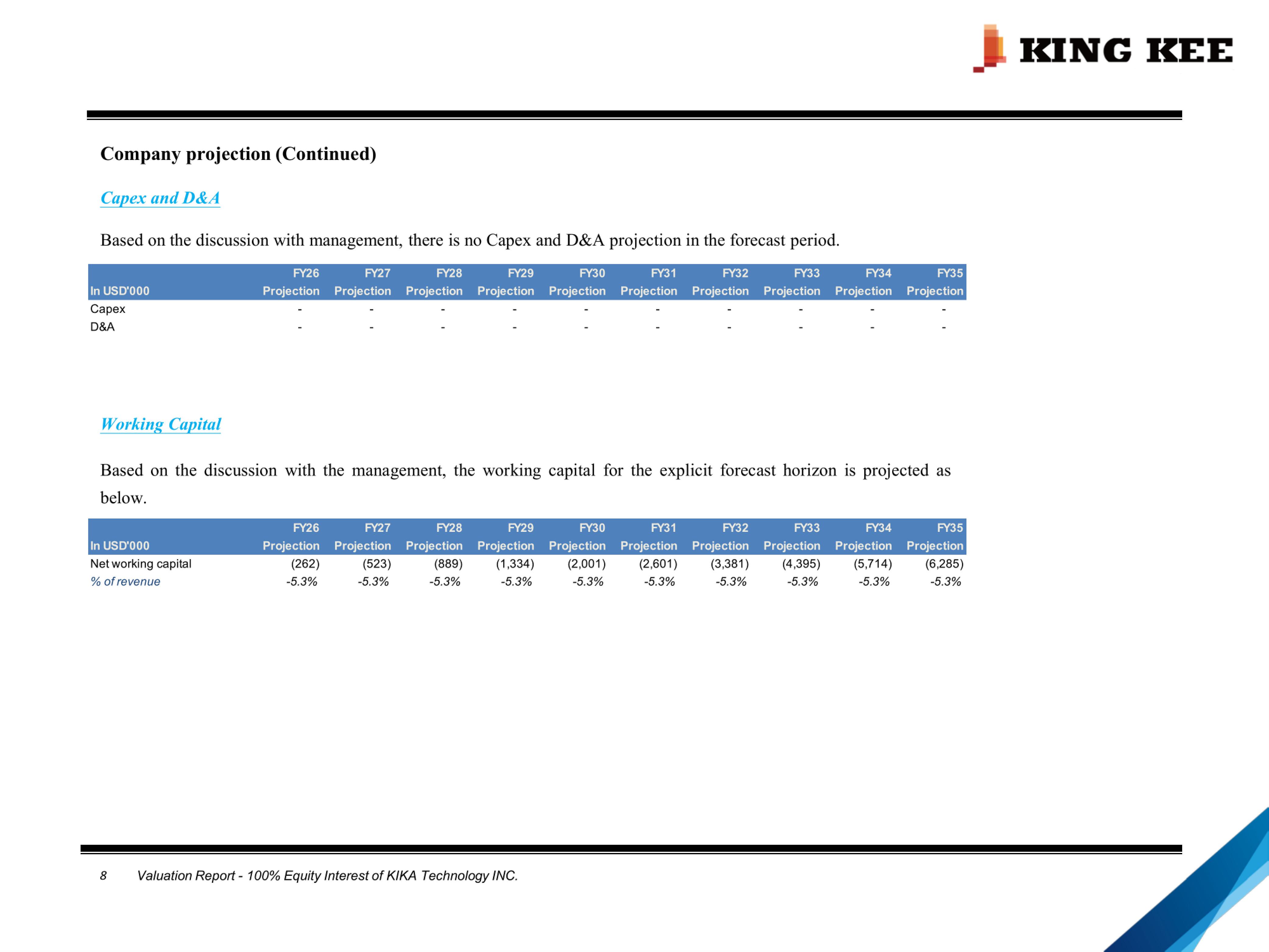

K I NC KEE Company pr o jecti on (Conti n ued) C a pex and D&A B a sed on t h e di s c us sion with m anage m e n t , t h e re is no Cap e x and D&A pr o j e c tion i n t he f orec a st period. m G m 1 m s m g m o m 1 m 2 m 3 m 4 m s I n U S D ' OOO P r o ject i o n Project i on Project i on P r o jecti on P r o ject i o n Pr o ject i on Project i on P roject i on P roject i o n Pr o ject i on C a pex D&A W o rk i n g C a p i t a l B a sed on t h e d i sc u ss i on w i th t h e m anagemen t , t h e w orking capital for t h e e x pl i c i t for e c a st hor i z on i s projected a s below. mG m 1 m s m g m o m 1 m 2 m 3 m 4 m s I n U S D ' OOO P r o ject i o n Project i on Project i on P r o jecti on P r o ject i o n Pr o j ect i on Project i on P roject i on P r o ject i o n Pr o j ect i on 8 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Net worki n g cap i tal % of revenue (262) - 5.3% (523) - 5 . 3% (88 9 ) - 5 . 3% ( 1 , 334) - 5 . 3% (2 , 001 ) - 5.3% ( 2 , 601) - 5 . 3% ( 3 , 38 1 ) - 5 . 3% ( 4,395) - 5 . 3% (5 , 714) - 5 . 3% (6 , 285) - 5 . 3%

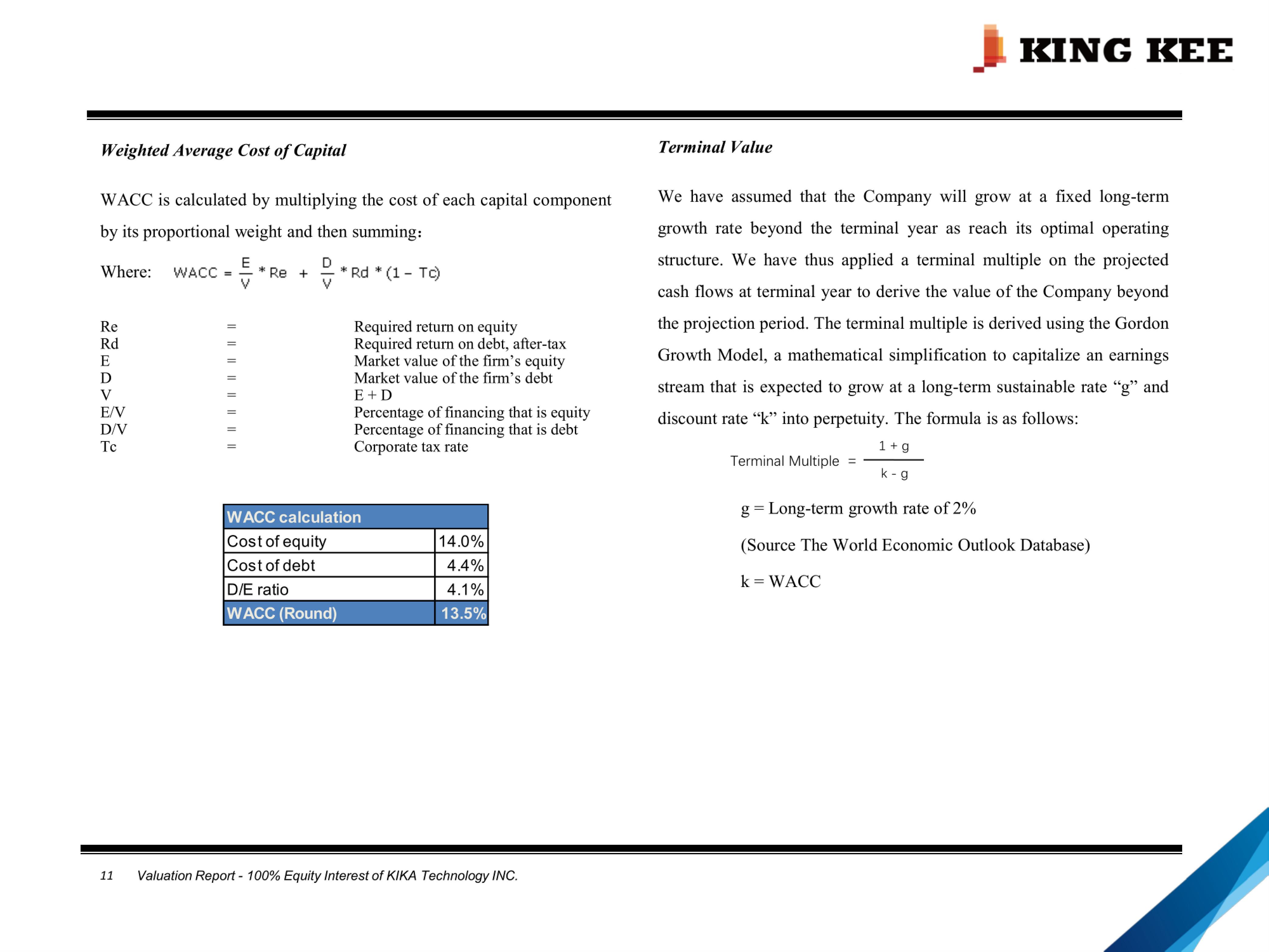

K I NC KEE 9 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Disco u nt R ate In applying t he discounted c a s h flow m e t hod, it is n e c e s s a ry to d e termine an appropriate di s count r a te f or t h e a s s e t s und e r r e vi e w . T h e discount rate repr e s e n ts an e sti m ate of t h e rate of r e turn required by a t hird party i n v e stor for an i n v e stm e nt of this type. T h e r a te of return e x p e cted from an i n v e stm e nt by an i n v e stor relat e s to perceived r i sk. Ri s k fact o r s relevan t in our s e l ect i on of an appropriate discou n t rate includ e : Inter e st r a te ris k , which m e a sur e s variability of r e tur n s , ca u sed by chang e s in t h e g e n e ral l e vel of int e r e s t rat e s. Pur c h a sing po w e r ri s k, w hich m easur e s loss of purch a sing po w er over ti m e due to inflation. Liquidity ris k , whi c h m easur e s t he e ase with which an i n s t ru m e nt can be s old at t h e prevailing m arket price. Marke t r i s k , which measur e s t h e ef f ec t s of t h e g e n e ral mark e t on t h e price b ehavior of s ecuriti e s. Bu sin e s s ris k , which m e a sur e s t h e un c erta i nty in h e r ent in pr o je c tions of oper a ting inco me. E x change rat e , w hich m e a sur e s t h e possible influence that c hang e s in e x c han g e rat e s , might ha v e on t h e value of t he inv e st m e n t . Consideration of risk also i n v o l v e s elem ents such as quality of m anageme n t, degree of liqui d it y , and ot h er factors af f ecting the rate of return acceptable to a g iv e n in v e st o r in a specif i c inv e st m e n t . An adjust m ent for risk is an increme n t added to a b a se r a te to compe n s a te for t he e xte n t of r i s k beli e ved to be in v olved in t h e inv e s t m ent .

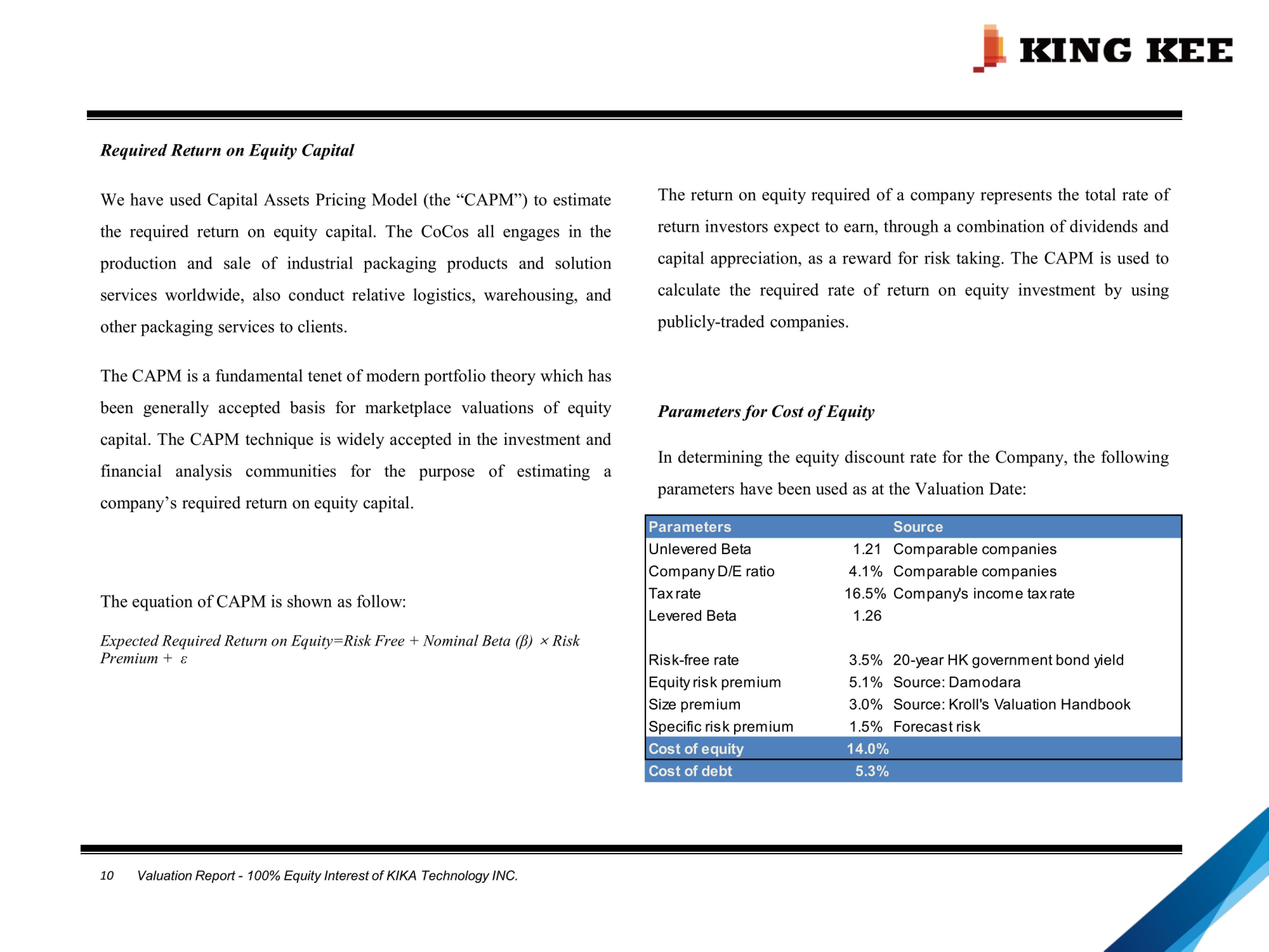

K I NC KEE R equ i r ed R e turn on Equ i ty Cap i t a l W e have u sed Capital As s e t s Pricing M odel (t h e " CA P M " ) to e stim a te t h e r e quired r e turn on e q u ity capital . T h e Co C o s all engag e s in t h e production and s ale of indu s t rial pac k a g i ng produc t s and solution s ervic e s w orldw i d e , al s o conduct rel a tive l og i s ti c s, w ar e ho u sing, and o t h e r pa c ka g ing s e rv i c e s to clie n t s . T h e CAPM i s a funda m ental t e n e t of m o d e rn po r tfolio t h eory w hi c h h a s b e en g e n eral l y ac c ept e d basis f or m arketplace v a l u . ations of eq u ity capital . T h e CAPM te c hnique i s w i d e l y ac c ept e d in t h e i n v e s t m e nt and financial analy s is communiti e s f or t h e purpo s e of e s t i m at i ng a company's r eq u ired r eturn on equity capital . The r e turn on equ i ty r e quired of a company repr e se n ts t he total rate of return inv e sto r s e xpect to ear n , through a combi n ation of dividends and capital appreciation, a s a r eward for risk taking . T h e C APM is u s ed to calculate t h e r e quired rate of return on equity investme n t by u sing publicl y - trad e d compani e s . Pa r am e ter s for Co s t of Eq u i ty In d e t e rmin i ng the eq u i t y discount r a te for the Compan y , the follow i ng param e te r s h a v e b een used a s a t t h e Valu a tion D a t e : Parame t ers S o u rce 10 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . T h e equation of C APM i s s ho w n a s follo w : Exp e c ted R eq u i r ed R e t urn on Equity = Risk Free + Nominal B eta ( /J ) x Risk P remium + E: Un l evered B e t a Company D/E ra t i o T ax rate Le v ered Be t a 1 . 21 4 . 1 ƒ / o Comparab l e com panies Co m parab l e com panies 1 6 . 5o / o Company's inco m e tax rate 1 . 26 Ri s k - free rate Equity r i s k prem i um S i z e prem i um S p ec i fic ri s k prem ium 3 . 5 ƒ / o 5 . 1 ƒ / o 3 . 0 ƒ / o 1 . 5 ƒ / o 20 - year HK government bond yield Sour c e: Da m odara Sour c e: Kro l l ' s V a l uation H andbook Fore c a s t r i s k

W A - C C = "' Re + l + g Re Rd E - - - - - - - - - - - - - - - - Required r e turn on equity Required return o n debt , after - tax M arket value of the fir n 1 ' s equity M arket value of the fir n 1 ' s debt E + D Percentage of fin a ncing that is equity Percentage of fin a ncing that is debt Corporate tax rate D v E N DN T c Ter m inal M u l ti p l e = k - g K I NC KEE W e i ghted Average Co s t of C ap i t a l W ACC is calc u l a ted by multiplying t h e cost of each capital compo n ent by i t s proportional w e i g h t and t h e n s umming: Term i n a l Va l ue Whe r e : E v v "' Rd "' ( 1 - T c ) We have a ssum ed that t h e Company will grow at a fixed long - term growth rate beyond t h e termi n al year a s rea c h its optimal operat i ng s t ructure . We have t hus applied a terminal multiple on the projected c a sh flow s a t term i nal year to deri v e the value of t h e Company beyond t h e projection period . T h e term i nal multiple is der i v ed using t he Gordon Gro w th M ode l , a mat h ematical s i mplification to capitalize an earn i ngs s t ream t h at is e xpe c t e d to grow at a long - term sustainable rate " g " and di s count rate " k " into pe r petuity . The f o 1 m ula is a s f ollo w s : W A C C ca l c u l at i on g = Long - term growth rate of 2% (Source T h e World Economic Outlook D a tab a s e) k = W A CC W A C C ( R o u nd) 1 3.5 ƒ / o 11 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . 1 4 . 0 ƒ / o Co s t of e qu i ty 4 . 4 ƒ / o Co s t of debt 4 . 1 ƒ / o D / E ratio

K I NC KEE 12 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . V a luat i on C ommen t s The valuat i on of an i n ter e s t in a busi n ess e nt erprise requir e s co n sideration of all rele v ant f acto r s aff e c ting t he operation of t he bu s i n e ss and ass e ts and its abil i ty to ge n erate future inv e stme n t retur n s . The f acto r s co n s i dered in t he valuation includes, but not limit ed t o , t he f ollow i ng : obtained such further information which is co n s idered n ec e ssary f or t he purp o s e s of th i s valuat i on. In a rriving at our as s e s s ed valu e , w e have m ainly co n sid e red t h e core busi n e ss of t he bu s i n e ss . We have not m ade provi s i on for ot h e r non operat i ng cash flow item s such as int e r e s t incom e , exchange rate gain / l o s s , e tc . in t h e v a luation m odel . t h e nature ent e rpri s e; of t h e busi n e s s and t h e historical per f or m ance of t he t h e f i nancial condition of t h e b u si n e s s and t h e economic outl ook in g e n e ral; t h e operational co n tra c t s and agree m ents in rel a tion to t h e b u s i n e s s ; past and proje c t e d operat i ng r e s ul t s; t h e f i nancial and b u s i n ess risk of t he e n terpri s e i ncluding t he continuity of inco m e and t he projected f u ture r e s ults; and t h e nature of t h e related agre e m en t s . T h e conclusion of value is ba s ed on acc e pt e d valuation pr o cedur e s and pra c tic e s th a t re l y substa n ti a l l y on t h e us e of numero u s a s sumptio n s and t he co n s ideration of m any unce r tai n ti e s , not all of w hich can be e a s ily quantified or a s c e rtained . Furt h e r, whil e t he a s sumptio n s and co n sideration of s uch m a t t e rs are co n s idered b y us to be re a sonabl e , t h ey are inherently subject to significant b u sin e s s , economic and comp e t iti v e unce rtainti e s and contingenc i e s, m any of whi c h are beyond t h e co n trol of t h e Company and KKG . We confirm t hat w e have carri e d out an i n spection on the a ss e ts of t h e Company and we ha v e m ade relevant search e s, enquiri e s and have

K I NC KEE 13 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Risk Factors We caut i on reade r s to be a w are of t he follo w ing r i s k s w hich w e beli e ve could influence t he as s e ssment . Such ris k s can range from very subj e ct s p e cific f actors to m ore s y st e m a t i c f actors . Soc i a l , P o l i t i c al and M acroe c onom i c Con s i derat i ons facto r s of production and demand facto r s w i thin an economy f or t h e count e rparty . The occurrence of natural d i sast e r s, r e source d e pl e tion and v ariatio n s in cl i m ate cond i tions m ay influence r e s ource avai l ability and pric e s for inpu t s on the supply side or m ay influence m arket acc e s s and pre f e r e nc e s for produ c t s and s e rvices a ssoci a ted to t h e count e rparty from end - us er dem and . Rea l iza t i on o f fore c a s t and proje c t i on This valu a tion is premised i n pa r t on the hi s torical f i nancial in f or m ation and pr o j e c tio n s provided by the mana g e m ent of the Company . We ha v e a ssu m ed accuracy of the i nform a tion provided and relied to a considerable e xtent on such i nform a tion i n a 1 1 · iv i ng at our opinion of value . Although appropriate t e sts and ana l y s e s have b e en carried out to v erify t h e re a s onable n e s s and fairn e s s of t h e i nform a tion provide d , eve n ts and cir c u m s tanc e s frequ e nt l y do not occur as e xpected . Sin c e pro j ectio n s relate to t h e f u ture, t here will usual l y be differenc e s b e t w een pro j ectio n s and a c tual r e sults and in so m e c a s e s , th o s e varianc e s m ay be m aterial . A ccordingly, to t he extent any of the above m entio n ed in f or m ation requir e s adjustment ; t h e r e sult i ng in v estment v alue m ay dif f er . Various economi c , political and s o cial p h enomena surrounding t h e subje c t items m ay c hange so a s to af f ect our opinion of v alue . Int e rn a tional or nationwide policy and I or legis l a ti v e change s t hat alter e xi s ting righ t s and obligations m ay d i re c tly or indire c tly i nfluen c e t h e Subject item s . M acr o economic c i r c umstanc e s i ncluding inflatio n , i n ter e st rate flu c tuatio n s and e xi s ting and forec a st le v els of growth in t he broad e r e conomy m ay also have an effe c t . S o ci e tal fa c to r s encompassing t h e per c eption and preferenc e s of people i n ge n eral m ay swing rendering t h e Subje c t ite m s m ore or l e s s d e s i rable and t h us more or l e s s valuable . T h e Company is subj e c t to various laws and regulatio n s go v erning i t s operatio n s i n Hong Kong . Future political and legal c hang e s in Hong Kong might ha v e eit he r f a v orable or u nfavorable impa c t s on t h e Company . E n v i ronme n t al Cond i ti ons Ph enom e na within t h e ph y sical e n viron m e nt can sev e rely i mpact t h e

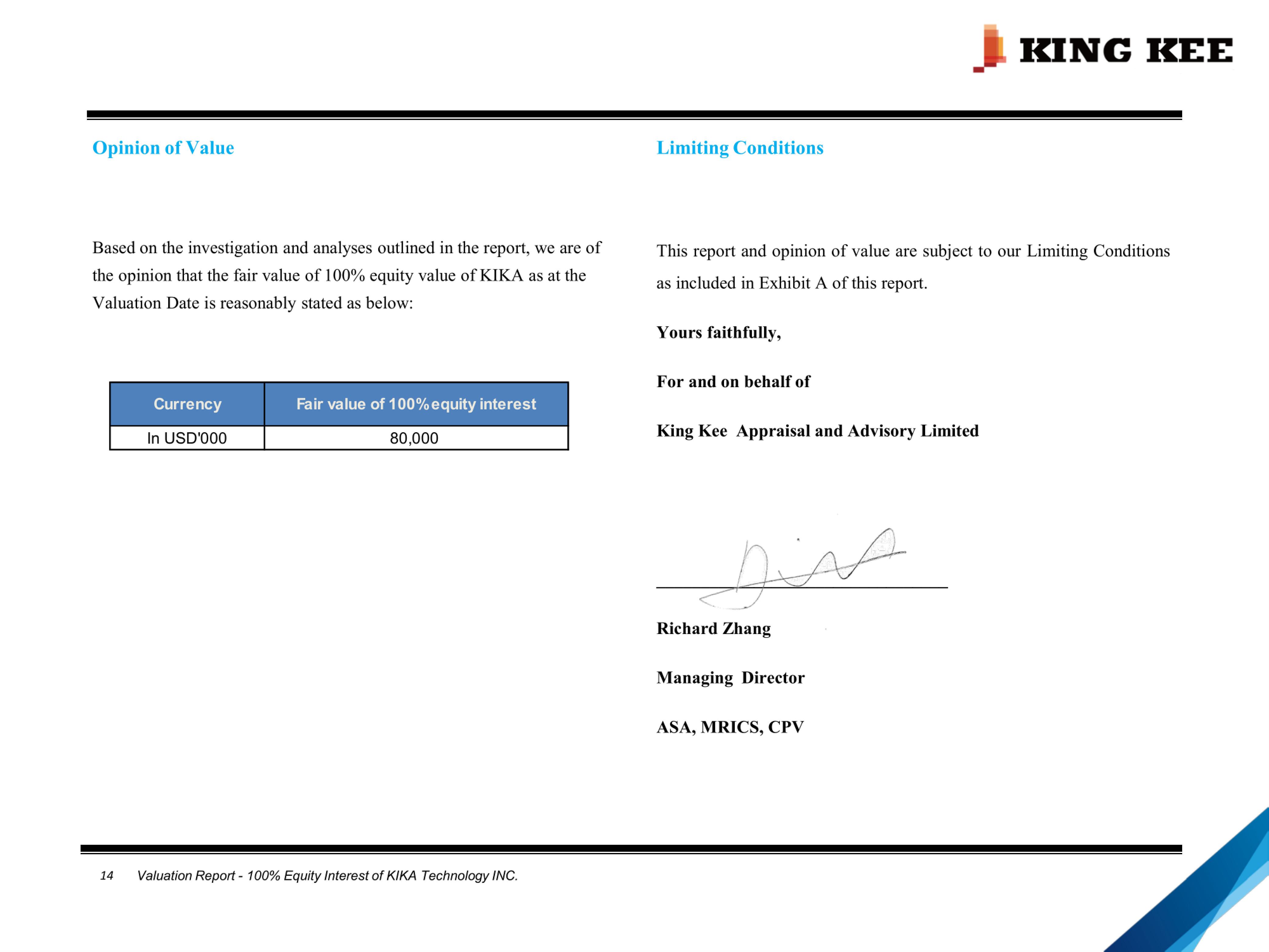

K I NC KEE 14 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Opinion of Value Limiting Cond i tions Ba s ed on the in v e stigation and analy s e s outlined i n the repo r t , w e are of t h e opinion t hat t h e fair value of 10 0 % equ i ty value of KIKA as at t he Valuation Date is re a s onably s tated a s b e l o w: This report and opinion of v a lue are subje c t to our L i miting Conditio n s a s includ e d in Exhibit A of t his report. Yo u rs f a i th f u l ly, F or and on beha l f of I n U S D ' OOO 80 , 000 K i ng Kee A p pra i s al and Adv i sory L i mit e d ' Rich a rd Z hang Man a ging Dire c tor AS A , MR I C S , C P V

K I NC KEE 15 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . E xhibit A - Limit i ng C o n diti o n s 1 . In the preparation of our repo rts, we relied o n t he a c c ur a cy, c o mplet e n e ss a n d reasonablen e ss of the Company inf o r m ation, a ssumptio n s a nd other d a ta pro v ided to us by t h e Compan y / e ngage m ent parti e s a nd/o r its re p r e s e ntati v es . We did not c arry out any work in t he n at u re o f a n a udit a n d nei t h e r are we required to e x press a n audit o r viability o pini o n . We t a ke n o r e sponsibility for the a c curacy of su c h i n f o rmation . The r e sponsibility for det e rmining ex p ected values rests solely with t h e Comp a n y /engage m ent parti e s and our reports were Company' s / e ngage m ent c o ncl u sion of v alue. only used a s p art of parties' a n al y sis in rea c hing t h e t heir 5. KKG sha l l not be required to give testimo n y or attendance in co u rt o r to a ny go v ernm e nt ag e n c y by reas o n o f th i s e x e rc i se, wi t h ref e rence to the project des c ribed h erein . S h o uld there be any k i n d o f su b sequent s e rvic e s re q uired, t h e c orre sponding exp e n ses a n d time c o s t s will b e reimbu r sed fr o m yo u . Su c h ki n d o f additi o nal w o rk m a y i n c u r wi t h out prior notifi c ation to yo u . 6. No opinion i s intended to be e xpr e ssed f o r ma t ters which re q uire legal or o t h er s p ecialized e xpert i se or kno w ledge, be y ond w h at is c ustomarily e mplo y ed by val u e r s . 7. T he use o f and/or the vali d ity of the report i s subject to t he t e rms o f e ngage m e n t l e tt e r/prop o sal and the full s e ttle m ent o f t h e fe e s a nd all t h e ex p e n ses . 8. O ur c o n c l u si o n s assu m e c o n ti n u a ti o n o f p r ude n t ma n ag e m e nt poli c i e s ov e r wh a tever p e riod o f ti m e th a t i s c onsidered to be nec e ss a ry in o rd e r to mai n tain t h e c h ar a cter a n d i n tegr i ty of t h e a s s e ts valued . 9. We a s sume th a t th e re a re no hidden or unex p ected c on d itio n s a s soci a t e d with the s ubje c t matter under review th a t might adversely a ffe c t the reported review r e sult. Furth e r, we a s sume n o r e spo n sibility for c h a ng e s in market c onditi o n s, gov e rn m ent policy or other c o n d itions a f ter the Valuat i on/Ref e r e nce D a te. We c an n ot provide a s sur a n c e on the a c hievability of the r e sul t s fore c asted by the C omp a n y / engage m ent p a rti e s be c ause ev e nts and circu m st a n c e s frequently do not o c cur a s expe c ted; diff e re n c e b e twee n a ctual a nd expected r e sul t s may be materia l ; and a chieve m ent of the foreca sted resul t s i s dep e ndent on a c t io n s , plans and a s su m ptio n s of manag e m e nt. prop e r boo k s of a c c oun t s a re mai n tained, a n d the financial i n f o r m ation and f o r e c a st g ive a t r ue a n d fair view a nd h ave been prep a red in a c c ord a n c e with t h e relev a nt stand a rds a n d c o mpani e s or d in a n c e . 3. Publ i c inf o rm a tion a n d i n dustry a nd stat i sti c al inform a t i on h ave been o b tained from sourc e s we de e m to be reputable ; h owev e r we m a ke n o repr e sent a tion a s to the a c cur a cy o r c o mpl et e n e s s of su c h i n for m ation, and have ac c epted the infor m a ti o n without any verificati o n . 4. The m a nage m ent a nd the Board of the Company h a s reviewed a n d agreed a ssumptio n s, reas o nable. on t h e report a nd c on f rrmed th a t t h e b a s i s, c a l c ul a t i o n s a nd r e sul t s a re appr o p ri a te a n d our s e rvi c e engage m ent part of a s explained We h ave 2. r e spo n sibility to e n sure d ire c tor ' s the t h at it i s pr o cedure

K I NC KEE 16 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . 10. This report has b e en prepared s o lely for the inter n al use purpos e . The report s hould n ot be otherw i se r e f e rred to, in wh ole or in p a rt, o r q uoted in any d o cu m ent, cir c ul a r o r st a t e m e n t in any m a nner, o r d i stributed in wh o le or in part or c opi e d to any th eir party wit h o ut our p rior writt e n c o n s ent . We s h all n ot und e r any circu m s ta nc e s wh a tsoever be liable to a ny third party ex c ept where we s p ecifical l y agreed in writing to a cc ept such liability . 11. This report is c onfid e ntial to t he client a n d t he cal c ulati o n of valu e s e xpre s sed h e rein i s v alid only f o r the p u rpose c h arges paid to u s f o r t he p o rtion of i t s s e rvic e s or work pr o ducts gi v ing r i se to liabilit y . In no event sh a ll we be liable f o r c o n se q ue n tial, s p ecial, i n cide n tal or punitive l o ss, d a m a ge o r expe n se (i n c luding wit h out limitation, l o st pr o fi t s , opportunity c o s ts, e t c . ), even if it h a s be e n adv i sed of th eir p o s s i ble ex i sten c e . 14 . We are n ot e n v ir o n m ent a l c onsult a nts o r audit o r s, a n d we take n o r e sponsibility f o r a n y actual or pot e ntial e n v ir o n m ent a l l iabi l iti e s ex i st, and the e ffect on t he value st a t e d in the e ngage m ent l e t ter/ o r p rop o sal as o f the o u r and Valuati o n I R e fere n c e Dat e . In ac c o rd a n c e wi t h st a nd a rd practice, we must state t h at th i s repo rt exercise is for t h e u se o n ly by the p a rty to wh o m it i s ad d r e ssed a n d no r e s pon s ibility i s a c c ept e d with res p ect to any third party for t h e w h ole or any part o f i t s content s . 12. Wh e re a d i sti n c t and definite repr e s e n t a tion h a s b e en made to us by p a rt y / parti e s int e r e sted in t he ass e t s valued, we are entitled to rely on th a t re p r e s e n t a tion w i th o ut furth e r inv estig a tion into the ver a city of th e re p r e s e n t a ti o n if su c h inv estig a tion i s beyond t he s c ope of n o r m al s c enario anal y s is work . 13. You agree to indem n ify and h old us and o ur p ersonn el h a rml e s s agai n st and from any a n d all l o ss e s, c lai m s, a c tio n s , da m ag e s, exp e n s e s o r liabiliti e s , i n clu d ing re a sonable attorne y 's fe e s, to which we m ay subje c ts in c onnecti o n with th i s engage m ent. m a ximum liability relating to s e r v i c es rend e red u n der t his engage m ent (regardl e ss o f f o rm o f acti o n, w h e t h e r in contr a c t, neglig e n c e or o t h erwis e ) sh a ll b e limited to the of t h e a sset is enco u raged to obtain a prof e ssional e n v ir o n m ent a l as s ess m ent. We do not c o nduct or pr o v ide e n v ir o n m ental as s ess m en t s and h a v e n ot p erf o r m ed one for t h e subject p ro p erty. 15. T h i s exerc i se i s pre m i sed in part o n the inf o r m a ti o n and future e s tim a t e s p rovided by th e m anag e m e nt of t h e C o m p a n y / engage m ent parti e s . We have a s s u m ed the a c c ur a cy a n d re a sonablen e ss o f t he i n for m ati o n provided a n d relied to a c o n s iderable extent on su c h infor m ation in arriving a t our c alculation o f value . Si n c e e sti m at e s relate to th e future, t h ere will usually be differ e n c e s b e tween esti m a t e s and a ctual r e sul t s and in s o me c a s e s , and t h ose varia n c e s m ay be m aterial . A c c ordingly, to the ext e nt any of the above m e n ti o ned i n f o r m ation re q uir e s adjust m e nts, th e resulting value m ay differ signific a n tly . 16. Actual tra n s a c tio n s in v olving th e subject a ss ets I busin e ss might be c o n c lud e d at a higher o r low e r value, depe n ding up o n the cir c u m stanc e s of the t rans a ction a n d the b u s in e ss, a n d the knowledge and m otivati o n o f the bu y ers a n d sell e rs at that tim e . bec o me Our

K I NC KEE 17 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . 17 . This repo rt and the concl u sion o f v alue s a rrived at h erein a re for the excl u sive u se of our client f o r the sole a n d s p ecific purpos e s a s n oted h e rein . Furt h er m ore, the repo rt a n d conclu s ion of v alue s are not int e n ded by t h e au t h o r, a n d s h ould not be cons t rued by the read e r, to be in v est ment ad v ice in any m an n er whatsoev e r . T he co n cl u sion of v alue s re p res e nts t he con s iderati o n ba s ed on information f u rn i s h ed by t he Co m p a n y /engage m ent p arti e s a nd other so u r c es .

K I NC KEE 18 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . E xhibit B - Val u ers' Professi o n a l Declaration bi a s with r e spect to the p a rti e s involved. The v al u ers c e rtify, to t he best of t heir knowledge a n d belief, t h a t : The v al u ers' comp e n sation is not c ontingent up o n t h e a mo u nt of the v alue estimate, the att a in m ent of a stipulated r e sult, t h e occurr e n c e of a su b seq u ent event, o r t he repo rting o f a pre deter m ined v alue or direction in value t h at f a v ors t h e cause of the cli e nt . I n for m a ti o n h a s be e n obtained from sourc e s th a t are believed to be reliable . All f a c t s which h ave a be a ring on the value c o n c luded have been c o n s idered by the valu e r s a n d n o important f a c t s have been int e n tio n a lly d i sregarded . The a nal y s e s , opinio n s, a n d c o n c lusi o n s were develo p ed, a n d th i s report h a s been prepared, in a c c orda n c e with t h e Int e rn a tional Valuation S t a n d a rds publ i s h ed by t h e Inter n a tional Valu a tion S ta n d a r d s C o uncil . T he reported anal y s es, opinions, and c onclusio n s are subject to t h e a s sumptio n s a s s t a ted in the report a nd b a sed on the value r s' p e r sonal, unbi a sed pr o f e ss io n al analys e s, opinio n s , and c o n c l u s i o n s . T he valu a tion ex e r c i se i s also bounded by the limiting c on d itions . T he reported anal y s e s , i n depe n dent and objective. • • a n d c o n c l u sio n s are o p 1 n 1 o n s , T he valu e r s have no pr e sent o r pr o s p e c tive inter e s t in the a s s e t t h a t i s t h e subje c t of th i s report, a n d h ave n o p e r so n al inter e s t or

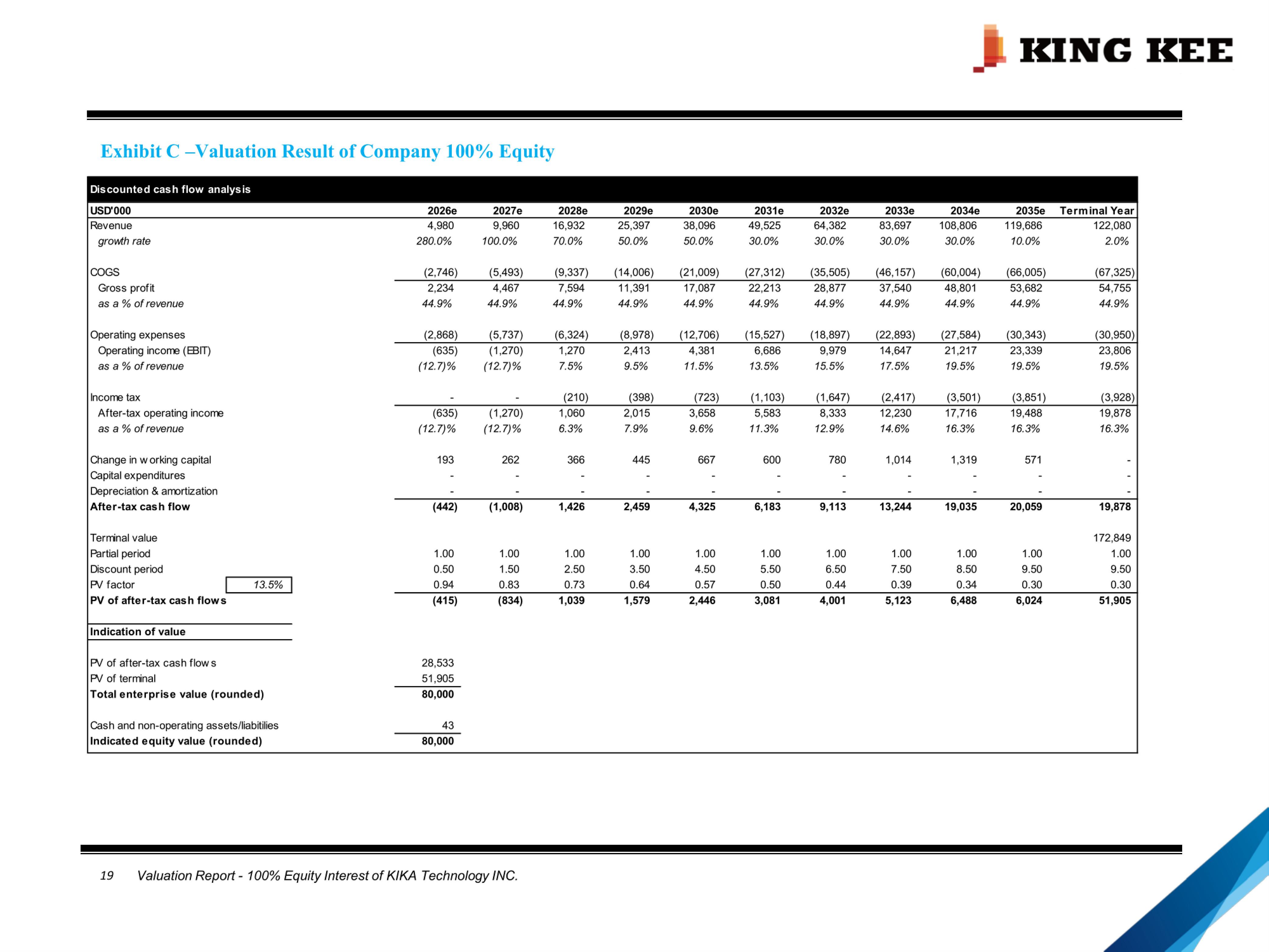

19 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . K I NC KEE E xhibit C - Valuati o n Result of Compa n y l O O o / o Equity s D i s counte d cas h f l ow analys i T e r m i n a l Ye a r 2 0 3 5 e 2 0 3 4 e 2 0 3 3e 2 0 3 2e 2 0 3 1 e 2 0 3 0e 2 029e 2 028e 2 027e 2 02 6 e U SD ' O OO 1 2 2 , 0 8 0 1 1 9 , 68 6 1 0 8 , 8 0 6 8 3 , 6 97 6 4 , 3 8 2 4 9 , 52 5 3 8 , 0 9 6 2 5 , 3 97 1 6 , 9 3 2 9 , 9 6 0 4 , 9 8 0 R eve n u e 2 . 0% 1 0 . 0 % 3 0 . 0% 3 0 . 0 % 3 0 . 0 % 3 0 . 0 % 5 0 . 0 % 5 0 . 0 % 7 0 . 0% 10 0 . 0% 2 8 0 . 0% growth ra t e ( 6 7 , 325) (6 6 , 005) (6 0 , 004) ( 4 6 , 1 5 7) (3 5 , 5 05) ( 2 7 , 3 1 2 ) ( 2 1 , 0 0 9) (1 4 , 0 0 6) ( 9 , 3 3 7) ( 5 , 493) ( 2 , 7 4 6) C OGS 5 4 , 755 5 3 , 68 2 4 8 , 8 0 1 3 7 , 5 4 0 2 8 , 8 77 2 2 , 2 1 3 1 7 , 0 8 7 11 , 3 9 1 7 , 5 9 4 4 , 4 67 2 , 2 34 G r o ss p rof i t 44.9% 44.9% 44.9% 44.9% 44.9% 44.9% 44.9% 44.9% 44.9% 44.9% 44.9% as a % of rev e n ue (3 0 , 9 5 0) (3 0 , 3 4 3) (2 7 , 584) (2 2 , 8 93) ( 1 8 , 8 97) ( 1 5 , 5 27) ( 1 2 , 7 0 6) ( 8 , 9 7 8) ( 6 , 3 2 4 ) ( 5 , 737) ( 2 , 8 6 8) O p era t i ng e x penses 2 3 , 8 0 6 2 3 , 33 9 2 1 , 2 1 7 1 4 , 647 9 , 9 7 9 6 , 6 8 6 4 , 3 8 1 2 , 4 1 3 1 , 2 7 0 ( 1 , 2 7 0) (635) O p e r a t i n g i n c o rre ( E B I T ) 1 9 . 5% 1 9 . 5 % 1 9 . 5% 1 7 . 5 % 1 5 . 5 % 1 3 . 5 % 1 1 . 5 % 9 . 5% 7 . 5% ( 1 2 . 7)% ( 1 2 . 7)% as a % of r e v e n ue ( 3 , 9 2 8) ( 3 , 8 5 1 ) ( 3 , 5 0 1 ) ( 2 , 4 1 7) ( 1 , 6 4 7) ( 1 , 1 03) (723) (3 9 8) ( 2 1 0) - - l n corre t ax 1 9 , 8 7 8 1 9 , 4 8 8 1 7 , 7 1 6 1 2 , 2 3 0 8 , 3 33 5 , 583 3 , 65 8 2 , 0 1 5 1 , 0 6 0 ( 1 , 2 7 0) (635) A f t e r - tax o p er a t i n g i n c o rre 16.3% 16.3% 16.3% 1 4. 6 % 12.9% 11.3% 9 . 6 % 7 .9% 6.3% (12 . 7 )% (12 . 7 )% as a % of rev e n ue - 5 7 1 1 , 3 1 9 1 , 0 1 4 7 8 0 6 0 0 6 67 445 3 6 6 26 2 1 9 3 C h ange i n w o r k i ng ca p i tal - - - - - - - - - - - Ca p i t al expe n d i t u res - - - - - - - - - - - De p re c i a t i o n & am o r t i z a t i o n 1 9 , 8 7 8 2 0 , 0 5 9 1 9 , 035 1 3 , 2 44 9 , 11 3 6 , 1 83 4 , 3 25 2 , 4 5 9 1 , 4 2 6 ( 1 , 0 0 8 ) ( 4 4 2 ) A f te r - tax cas h f l o w 1 7 2 , 8 4 9 T e r n i n al v a l u e 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 1 . 0 0 P a r t i al p e r i o d 9 . 5 0 9 . 5 0 8 . 5 0 7 . 5 0 6 . 5 0 5 . 5 0 4 . 5 0 3 . 5 0 2 . 5 0 1 . 5 0 0 . 5 0 D i sco u nt p e r i o d 0 . 3 0 0 . 3 0 0 . 34 0 . 3 9 0 . 44 0 . 5 0 0 . 57 0 . 64 0 . 7 3 0 . 8 3 0 . 94 1 3. 5 % I Pv' f act o r I 5 1 , 9 0 5 6 , 0 2 4 6 , 4 88 5 , 1 23 4 , 0 0 1 3 , 0 8 1 2 , 4 4 6 1 , 5 7 9 1 , 0 3 9 ( 8 3 4 ) ( 4 1 5) P V of afte r - tax cas h f l o w s 2 8 , 5 33 I nd i c a t i on of v a l u e Pv' of a f ter - tax c ash f l ow s Pv' of t ern i n al T o t a l e n te r p r i se v a l u e ( r o u n d ed) Cash a n d no n - o p e r a t i n g a ssets/ l i a b i t ili es I nd i c a t e d e q u i ty v a l u e ( r o u n d e d ) 5 1 , 9 05 8 0 , 0 00 43 8 0 , 0 0 0

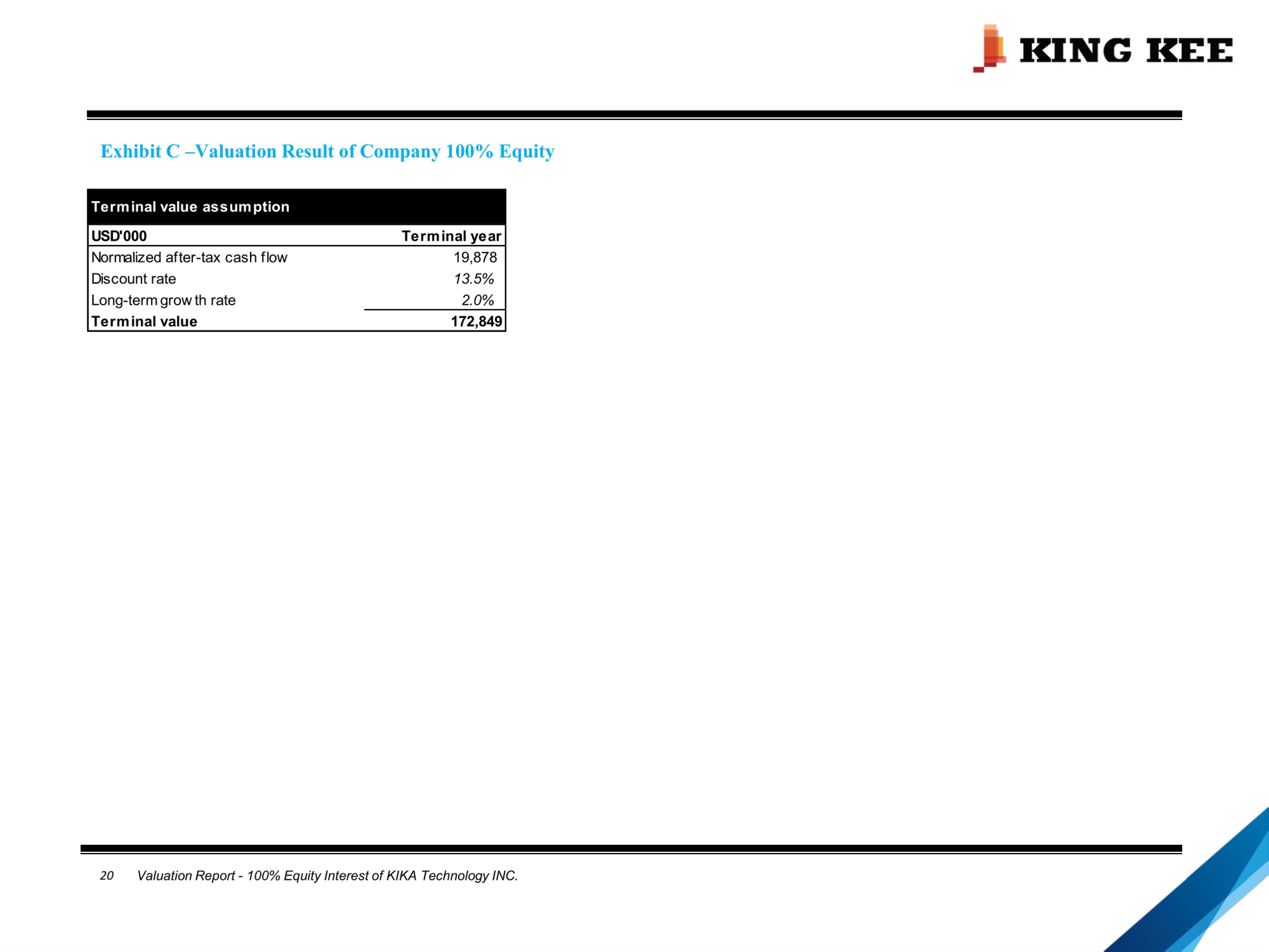

K I NC KEE 20 Valuati o n Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . Exhibit C - Valuat i on Result of Company lO O o / o Equ i ty Te rm i nal v a l ue ass u m pt i on N o r m a l i zed a f te r - tax cash f l ow D i s c ou nt r ate L on g - term g r ow th r ate Te rm i nal v a l ue 1 9 , 8 7 8 1 3 . 5% 2 .0% U S D ' OOO Te rm i nal y e a r 1 7 2, 8 4 9

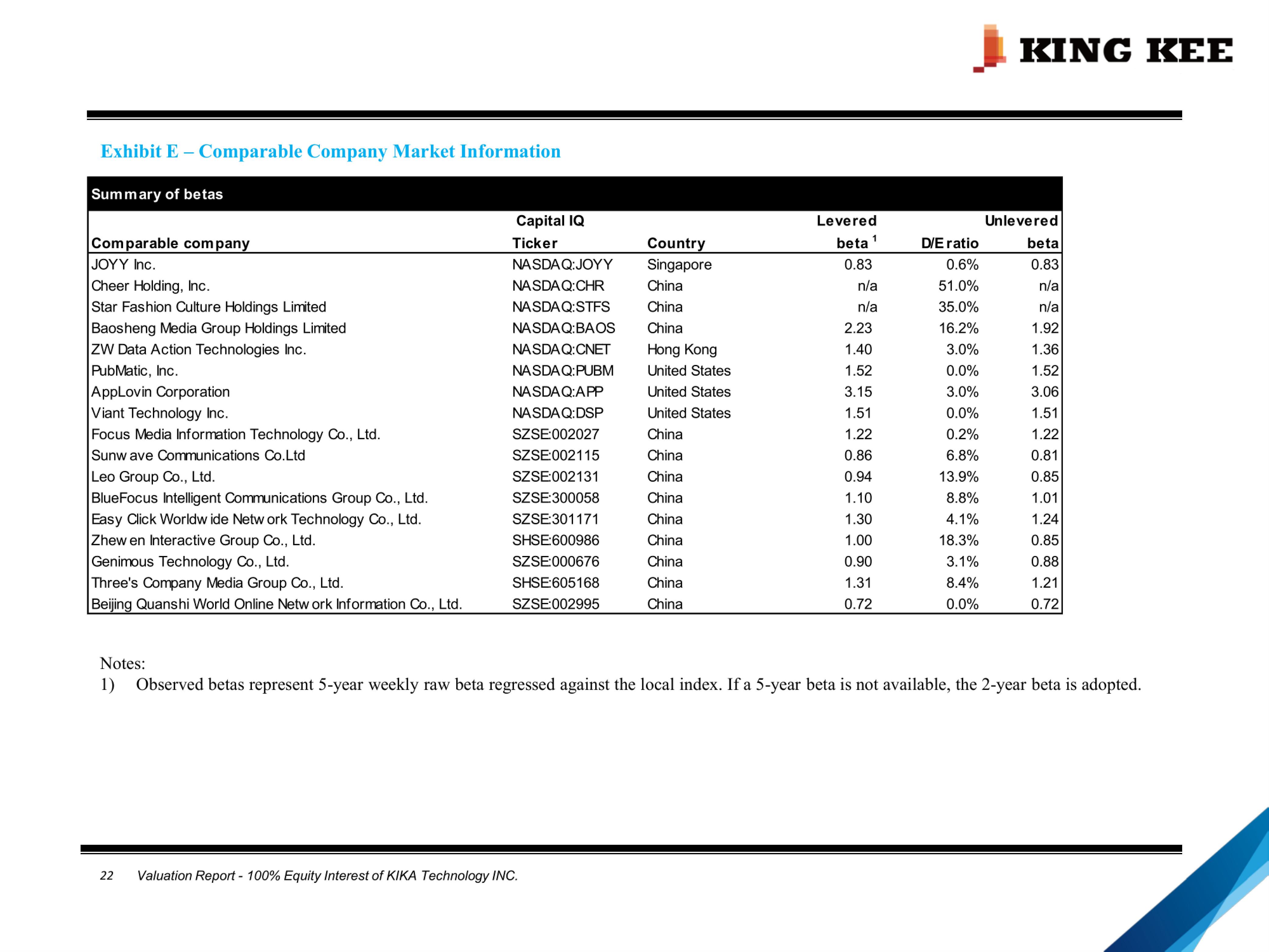

22 Valuation Rep o rt - 100% Equity Interest of K IKA Tec h nology I N C . K I NC KEE E xhibit E - Comparable C o mpa n y Market Infor m ation Not e s: 1 ) O b s er v ed b e tas repr e sent 5 - year w e e k l y raw beta regr e s sed against t h e l o c a l i n d e x. If a 5 - y ear b e ta is not ava i l a b l e , t he 2 - year b e ta is adopted. S u m m a r y of betas U n l e ve red b e ta D I E r a tio L e ve r e d b e ta 1 Countr y C a p i tal I Q T i c ker Com pa r a b l e c om p a ny 0 . 8 3 0. 6 ƒ / o 0 . 83 S i n g ap o re NAS D A Q : J O Y Y J O YY I n c. n/a 5 1 . 0 ƒ / o n/a C h i na NA S D A Q : C H R C h eer H o l d i n g, I n c . n/a 3 5 . 0 ƒ / o n/a C h i na NAS D A Q : S T F S S t a r F as h i o n Cu l t u r e H o l d i n g s L i n i ted 1 . 9 2 1 6. 2 ƒ / o 2 . 23 C h i n a NAS D A Q : B A O S B aoshe n g f \ Aed i a G r o up H o l d i ngs L i m i t ed 1 . 36 3 . 0 ƒ / o 1 . 4 0 H o n g K o ng NAS D A Q : C N ET ZW D a t a Act i o n T ec h n o l o g i es I n c . 1 . 5 2 0. 0 ƒ / o 1 . 52 U n i ted S tates NAS D A Q : P U B M P u b l \ Aat i c , I nc. 3 . 06 3 . 0 ƒ / o 3 . 1 5 U n i ted S tates NA S D A Q : A App L ov i n C o r p o rat i on 1 . 5 1 0. 0 ƒ / o 1 . 5 1 U n i ted S tates NAS D A Q : D S P V i a n t T ec h no l ogy I nc. 1 . 22 0 . 2 ƒ / o 1 . 22 C h i na SZSE: 0 02027 F ocus f \ Ae d i a I n f o r mat i o n T ec h n o l ogy C o . , L t d . 0 . 81 6 . 8 ƒ / o 0 . 86 C h i na SZSE: 0 02 1 15 S unw ave Com m u n i c a t i o ns C o . L td 0 . 8 5 1 3. 9 ƒ / o 0 . 94 C h i n a SZSE: 0 02 1 31 L eo G ro u p C o . , L t d . 1 . 01 8 . 8 ƒ / o 1 . 1 0 C h i na SZSE:3 0 0 0 5 8 B l u e F ocus I n tell i g e nt C o mmu n i cat i o n s G r o u p C o . , L t d . 1 . 24 4. 1 ƒ / o 1 . 30 C h i na SZSE:3 0 1 1 7 1 Easy C l i ck W o r l dw i de N etw o rk T ec h n o l ogy C o . , L t d . 0 . 8 5 1 8 . 3 ƒ / o 1 . 0 0 C h i na SH S E : 6 0 0986 Z h e w e n I n ter a ct i ve G r o up C o . , L t d . 0 . 8 8 3. 1 ƒ / o 0 . 90 C h i na SZSE: 0 0 06 7 6 G e n i rrous T ec h no l ogy Co . , L td. 1 . 21 8 . 4 ƒ / o 1 . 3 1 C h i na SH S E : 6 0 5 1 68 Three's Corrpa n y f \ Aed i a G ro u p C o . , L t d . 0 . 72 0. 0 ƒ / o 0 . 72 C h i na SZSE: 0 029 9 5 B e i j i ng Q ua n s h i W o r l d O n l i n e N e t w ork I n f o rmat i on Co . , L td.