Exhibit 99.1

UNITED STATES BANKRUPTCY COURT

SOUTHERN DISTRICT OF TEXAS

HOUSTON DIVISION

| ) | ||

| In re: | ) | Chapter 11 |

| ) | ||

| QVC Group, INC., et al.,1 | ) | Case No. 26-[____] ([·]) |

| ) | ||

| Debtors. | ) | (Joint Administration Requested) |

| ) |

DISCLOSURE STATEMENT FOR THE JOINT PREPACKAGED

PLAN OF REORGANIZATION OF QVC GROUP, INC. AND ITS DEBTOR

AFFILIATES PURSUANT TO CHAPTER 11 OF THE BANKRUPTCY CODE

| GRAY REED | KIRKLAND & ELLIS LLP | |||

| Jason S. Brookner (TX Bar No. 24033684) | KIRKLAND & ELLIS INTERNATIONAL LLP | |||

| Lydia R. Webb (TX Bar No. 24083758) | Joshua A. Sussberg, P.C. (pro hac vice pending) | |||

| Emily F. Shanks (TX Bar No. 24110350) | Aparna Yenamandra, P.C. (pro hac vice pending) | |||

| 1300 Post Oak Blvd. | 601 Lexington Avenue | |||

| Suite 2000 | New York, New York 10022 | |||

| Houston, Texas 77056 | Telephone: | (212) 446-4800 | ||

| Telephone: | (713) 986-7000 | Facsimile: | (212) 446-4900 | |

| Facsimile: | (713) 986-7100 | Email: | joshua.sussberg@kirkland.com | |

| Email: | jbrookner@grayreed.com | aparna.yenamandra@kirkland.com | ||

| lwebb@grayreed.com | ||||

| -and- | ||||

| Chad J. Husnick, P.C. (pro hac vice pending) | ||||

| Gabriela Z. Hensley (pro hac vice pending) | ||||

| 333 West Wolf Point Plaza | ||||

| Chicago, Illinois 60654 | ||||

| Telephone: | (312) 862-2000 | |||

| Facsimile: | (312) 862-2200 | |||

| Email: | chad.husnick@kirkland.com | |||

| gabriela.hensley@kirkland.com | ||||

| Proposed Co-Counsel for the Debtors and Debtors in Possession | Proposed Co-Counsel for the Debtors and Debtors in Possession | |||

| 1 | A complete list of each of the Debtors in these chapter 11 cases may be obtained on the website of the Debtors’ proposed solicitation agent at https://restructuring.ra.kroll.com/QVC. The location of Debtor QVC Group, Inc.’s corporate headquarters and the Debtors’ service address in these chapter 11 cases is 1200 Wilson Drive, West Chester, Pennsylvania 19380. |

THIS IS A SOLICITATION OF VOTES TO ACCEPT OR REJECT THE PLAN IN ACCORDANCE WITH BANKRUPTCY CODE SECTION 1125 AND WITHIN THE MEANING OF BANKRUPTCY CODE SECTION 1126, 11 U.S.C. §§ 1125, 1126. THIS DISCLOSURE STATEMENT HAS NOT YET BEEN APPROVED BY THE BANKRUPTCY COURT. THE DEBTORS INTEND TO SUBMIT THIS DISCLOSURE STATEMENT TO THE BANKRUPTCY COURT FOR APPROVAL FOLLOWING COMMENCEMENT OF SOLICITATION AND THE DEBTORS’ FILING FOR RELIEF UNDER CHAPTER 11 OF THE BANKRUPTCY CODE. THE INFORMATION IN THIS DISCLOSURE STATEMENT IS SUBJECT TO CHANGE. THIS DISCLOSURE STATEMENT IS NOT AN OFFER TO SELL ANY SECURITIES AND IS NOT SOLICITING AN OFFER TO BUY ANY SECURITIES.

Important information about this Disclosure Statement

SOLICITATION OF VOTES ON THE JOINT PREPACKAGED PLAN OF REORGANIZATION OF QVC GROUP, INC. AND ITS DEBTOR AFFILIATES PURSUANT TO CHAPTER 11 OF THE BANKRUPTCY CODE FROM THE HOLDERS OF OUTSTANDING:

| VOTING CLASS | NAME OF CLASS UNDER THE PLAN |

| B3 | RCF Claims |

| B4 | QVC Notes Claims |

| C3 | LINTA Notes Claims |

IF YOU ARE IN CLASS B3, Class B4, or CLASS c3 YOU ARE RECEIVING THIS DOCUMENT AND THE ACCOMPANYING MATERIALS BECAUSE YOU ARE ENTITLED TO VOTE ON THE PLAN.

ii

DELIVERY

OF BALLOTS (as Defined herein) BY HOLDERS OF RCF Claims,

BALLOTS

of the aforementioned PARTIES MAY BE Returned in |

If you have any questions regarding the procedures for voting on the PlaN:

You

can contact the Solicitation Agent by email at: qvcBALLOTS@RA.KROLL.com

you

can also contact the Solicitation Agent by phone toll-free at |

iii

Important information about this disclosure statement

THE DEBTORS ARE PROVIDING THIS DISCLOSURE STATEMENT TO HOLDERS OF CLAIMS FOR PURPOSES OF SOLICITING VOTES TO ACCEPT OR REJECT THE JOINT pREPACKAGED PLAN OF REORGANIZATION OF QVC GROUP, INC. AND ITS DEBTOR AFFILIATES PURSUANT TO CHAPTER 11 OF THE BANKRUPTCY CODE (AS MAY BE AMENDED, MODIFIED, OR SUPPLEMENTED FROM TIME TO TIME, AND INCLUDING ALL EXHIBITS AND SUPPLEMENTS THERETO, THE “PLAN”).2 THIS DISCLOSURE STATEMENT HAS NOT YET BEEN APPROVED BY THE BANKRUPTCY COURT. FUTURE APPROVAL OF THIS DISCLOSURE STATEMENT DOES NOT CONSTITUTE A GUARANTEE BY THE BANKRUPTCY COURT OF THE ACCURACY OR COMPLETENESS OF THE INFORMATION CONTAINED HEREIN OR AN ENDORSEMENT BY THE BANKRUPTCY COURT OF THE MERITS OF THE PLAN. THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT IS INCLUDED FOR PURPOSES OF SOLICITING VOTES FOR AND CONFIRMATION OF THE PLAN AND MAY NOT BE RELIED UPON OR USED BY ANY ENTITY FOR ANY OTHER PURPOSE.

BEFORE DECIDING WHETHER TO VOTE TO ACCEPT OR REJECT THE PLAN, EACH HOLDER OF A CLAIM ENTITLED TO VOTE ON THE PLAN SHOULD CAREFULLY CONSIDER ALL OF THE INFORMATION IN THIS DISCLOSURE STATEMENT, INCLUDING THE RISK FACTORS DESCRIBED IN ARTICLE IX HEREIN.

the debtors and certain holders of claims support the plan, including over 75% of the RCF Claims, over 55% of the QVC Notes Claims, and over 45% of the LINTA Notes Claims. The debtors believe that the compromises contemplated under the plan are fair and equitable, maximize the value of the debtors’ estates, and provide the best possible recovery to stakeholders. at this time, the debtors believe the plan represents the best available option for ACCOMPLISHING THE DEBTORS’ OVERALL RESTRUCTURING OBJECTIVES. the debtors strongly recommend that you vote to accept the plan.

HOLDERS OF CLAIMS SHOULD NOT CONSTRUE THE CONTENTS OF THIS DISCLOSURE STATEMENT AS PROVIDING ANY LEGAL, BUSINESS, FINANCIAL, OR TAX ADVICE. THE DEBTORS URGE EACH HOLDER OF A CLAIM entitled to vote on the plan TO CONSULT WITH ITS OWN ADVISORS WITH RESPECT TO ANY LEGAL, FINANCIAL, SECURITIES, TAX, OR BUSINESS ADVICE IN REVIEWING THIS DISCLOSURE STATEMENT, THE PLAN, AND THE RESTRUCTURING TRANSACTIONS CONTEMPLATED THEREBY. FURTHERMORE, THE BANKRUPTCY COURT’S APPROVAL OF THE ADEQUACY OF THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT (when and if approved) DOES NOT CONSTITUTE THE BANKRUPTCY COURT’S APPROVAL OF THE PLAN.

| 2 | Capitalized terms used but not otherwise defined in this Disclosure Statement have the meanings ascribed to such terms in the Plan or the RSA, as applicable. The summary of the Plan provided herein is qualified in its entirety by reference to the Plan. In the case of any inconsistency between this Disclosure Statement and the Plan, the Plan shall govern. |

iv

THIS DISCLOSURE STATEMENT CONTAINS, AMONG OTHER THINGS, SUMMARIES OF THE PLAN, CERTAIN STATUTORY PROVISIONS, AND CERTAIN ANTICIPATED EVENTS IN THE debtors’ forthcoming CHAPTER 11 CASES. ALTHOUGH THE DEBTORS BELIEVE THAT THESE SUMMARIES ARE FAIR AND ACCURATE, THESE SUMMARIES ARE QUALIFIED IN THEIR ENTIRETY TO THE EXTENT THAT THEY DO NOT SET FORTH THE ENTIRE TEXT OF SUCH DOCUMENTS OR STATUTORY PROVISIONS OR EVERY DETAIL OF SUCH ANTICIPATED EVENTS. IN THE EVENT OF ANY INCONSISTENCY OR DISCREPANCY BETWEEN A DESCRIPTION IN THIS DISCLOSURE STATEMENT AND THE TERMS AND PROVISIONS OF THE PLAN, the rsa, OR ANY OTHER DOCUMENTS INCORPORATED HEREIN BY REFERENCE, THE PLAN, the rsa, OR SUCH OTHER DOCUMENTS WILL GOVERN FOR ALL PURPOSES. FACTUAL INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT HAS BEEN PROVIDED BY THE DEBTORS’ MANAGEMENT EXCEPT WHERE OTHERWISE SPECIFICALLY NOTED. THE DEBTORS DO NOT REPRESENT OR WARRANT THAT THE INFORMATION CONTAINED HEREIN OR ATTACHED HERETO IS WITHOUT ANY MATERIAL INACCURACY OR OMISSION. EXCEPT AS OTHERWISE PROVIDED IN THE PLAN OR IN ACCORDANCE WITH APPLICABLE LAW, THE DEBTORS ARE UNDER NO DUTY TO UPDATE OR SUPpLeMENT THIS DISCLOSURE STATEMENT.

IN PREPARING THIS DISCLOSURE STATEMENT, THE DEBTORS RELIED ON FINANCIAL DATA DERIVED FROM THE DEBTORS’ BOOKS AND RECORDS AND ON VARIOUS ASSUMPTIONS REGARDING THE DEBTORS’ BUSINESS. WHILE THE DEBTORS BELIEVE THAT SUCH FINANCIAL INFORMATION FAIRLY REFLECTS THE FINANCIAL CONDITION OF THE DEBTORS AS OF THE DATE HEREOF AND THAT THE ASSUMPTIONS REGARDING FUTURE EVENTS REFLECT REASONABLE BUSINESS JUDGMENTS, NO REPRESENTATIONS OR WARRANTIES ARE MADE AS TO THE ACCURACY OF THE FINANCIAL INFORMATION CONTAINED HEREIN OR ASSUMPTIONS REGARDING THE DEBTORS’ BUSINESS AND THEIR FUTURE RESULTS AND OPERATIONS. THE DEBTORS EXPRESSLY CAUTION READERS NOT TO PLACE UNDUE RELIANCE ON ANY FORWARD-LOOKING STATEMENTS CONTAINED HEREIN.

THIS DISCLOSURE STATEMENT DOES NOT CONSTITUTE, AND MAY NOT BE CONSTRUED AS, AN ADMISSION OF FACT, LIABILITY, STIPULATION, OR WAIVER, NOR SHALL IT BE ADMISSIBLE IN ANY NONBANKRUPTCY PROCEEDING INVOLVING THE DEBTORS OR ANY OTHER PARTY, NOR SHALL IT BE CONSTRUED TO BE CONCLUSIVE ADVICE ON THE TAX, SECURITIES, OR OTHER LEGAL EFFECTS OF THE PLAN ON HOLDERS OF CLAIMS AGAINST, OR INTERESTS IN, THE DEBTORS. THE DEBTORS or any other Authorized Party MAY SEEK TO INVESTIGATE, FILE, AND PROSECUTE CLAIMS AND MAY OBJECT TO CLAIMS AFTER THE CONFIRMATION OR EFFECTIVE DATE OF THE PLAN IRRESPECTIVE OF WHETHER THIS DISCLOSURE STATEMENT IDENTIFIES ANY SUCH CLAIMS OR OBJECTIONS TO CLAIMS.

THE DEBTORS ARE MAKING THE STATEMENTS AND PROVIDING THE FINANCIAL INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT AS OF THE DATE HEREOF, UNLESS OTHERWISE SPECIFICALLY NOTED. there is no assurance that the statements contained herein will be correct at any time after such date. ALTHOUGH THE DEBTORS MAY SUBSEQUENTLY UPDATE THE INFORMATION IN THIS DISCLOSURE STATEMENT, THE DEBTORS HAVE NO AFFIRMATIVE DUTY TO DO SO, AND EXPRESSLY DISCLAIM ANY DUTY TO PUBLICLY UPDATE ANY FORWARD-LOOKING STATEMENTS, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS, OR OTHERWISE. HOLDERS OF CLAIMS OR INTERESTS REVIEWING THIS DISCLOSURE STATEMENT SHOULD NOT INFER THAT, AT THE TIME OF THEIR REVIEW, THE FACTS SET FORTH HEREIN HAVE NOT CHANGED SINCE THIS DISCLOSURE STATEMENT WAS FILED. INFORMATION CONTAINED HEREIN IS SUBJECT TO COMPLETION, MODIFICATION, OR AMENDMENT. THE DEBTORS RESERVE THE RIGHT TO FILE or distribute AN AMENDED OR MODIFIED PLAN AND RELATED DISCLOSURE STATEMENT, FROM TIME TO TIME, SUBJECT TO THE TERMS OF THE PLAN and the RSA.

v

THE DEBTORS HAVE NOT AUTHORIZED ANY ENTITY TO GIVE ANY INFORMATION ABOUT OR CONCERNING THE PLAN or the rsa OTHER THAN THAT WHICH IS CONTAINED IN THIS DISCLOSURE STATEMENT. THE DEBTORS HAVE NOT AUTHORIZED ANY DISCLOSURE or representations CONCERNING THE DEBTORS OR THE VALUE OF THEIR PROPERTY OTHER THAN AS SET FORTH IN THIS DISCLOSURE STATEMENT.

IF THE PLAN IS CONFIRMED BY THE BANKRUPTCY COURT AND THE EFFECTIVE DATE OCCURS, ALL HOLDERS OF CLAIMS OR INTERESTS (INCLUDING THOSE HOLDERS OF CLAIMS OR INTERESTS WHO DO NOT SUBMIT BALLOTS TO ACCEPT OR REJECT THE PLAN, who vote to reject the Plan, or WHO ARE NOT ENTITLED TO VOTE ON THE PLAN) WILL BE BOUND BY THE TERMS OF THE PLAN AND THE RESTRUCTURING TRANSACTIONS CONTEMPLATED THEREBY.

The confirmation and effectiveness of the Plan are subject to certain material conditions precedent described herein and set forth in Article IX of the Plan. There is no assurance that the Plan will be confirmed, or if confirmed, that the conditions required to be satisfied for the Plan to go effective will be satisfied (or waived).

You are encouraged to read the Plan, the RSA, and this Disclosure Statement in their entirety, including Article IX herein, entitled “RISK FACTORS” before submitting your ballot TO vote on the Plan.

THIS DISCLOSURE STATEMENT HAS BEEN PREPARED IN ACCORDANCE WITH SECTION 1125 OF THE BANKRUPTCY CODE AND BANKRUPTCY RULE 3016(b) AND IS NOT NECESSARILY PREPARED IN ACCORDANCE WITH FEDERAL OR STATE SECURITIES LAWS OR OTHER SIMILAR LAWS. This Disclosure Statement has not been approved or disapproved by the United States Securities and Exchange Commission (THE “sec”) or any similar federal, state, local, or foreign regulatory agency, nor has the SEC or any other agency passed upon the accuracy or adequacy of the statements contained in this Disclosure Statement. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The Debtors have sought to ensure the accuracy of the financial information provided in this Disclosure Statement; however, the financial information contained in this Disclosure Statement or incorporated herein by reference has not been, and will not be, audited or reviewed by the Debtors’ independent auditors unless explicitly provided otherwise HEREIN.

vi

Upon Confirmation of the Plan, certain of the securities described or otherwise contemplated in this Disclosure Statement will be issued without registration under the Securities Act of 1933, AS AMENDED (together with the rules and regulations promulgated thereunder, the “Securities Act”), or similar federal, state, local, or foreign laws in reliance on the exemption set forth in section 1145 of the Bankruptcy Code to the extent permitted under applicable law, section 4(a)(2) of the securities act, regulation d promulgated thereunder, regulation s under the securities act, and/or other available exemptions from registration. Other Securities may be issued pursuant to other applicable exemptions under the federal securities laws. If exemptions from registration under section 1145 of the Bankruptcy Code, section 4(a)(2) of the securities act, regulation d promulgated thereunder, regulation s under the securities act, or applicable federal securities law do not apply, the Securities described or otherwise contemplated in this disclosure statement may not be offered or sold except UNDER a valid exemption or upon registration under the Securities Act. The Debtors recommend that potential recipients of Securities issued under the Plan consult their own COUNSEL concerning their ability to freely trade such Securities in compliance with the federal securities laws and any applicable “Blue Sky” laws. The Debtors make no representation concerning the ability of a person to dispose of such Securities.

THIS DISCLOSURE STATEMENT CONTAINS FORWARD-LOOKING STATEMENTS WITHIN THE MEANING OF THE “SAFE HARBOR” PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995, AS AMENDED. The Debtors make statements in this Disclosure Statement that are considered forward-looking statements under federal securities laws. When used in this Disclosure Statement, the words “believe,” “expect,” “anticipate,” “estimate,” “intend,” “project,” “plan,” “likely,” “may,” “will,” “should,” “shall,” or other words or phrases of similar import generally identify forward-looking statements. The Debtors consider all statements regarding anticipated or future matters, including the following, to be forward-looking statements. Although the debtors believe the expectations reflected in such FORWARD-LOOKING statements are based on reasonable assumptions, the debtors can give no assurance that their expectations will be attained, and it is possible that actual results may differ materially from those indicated by these FORWARD-LOOKING statements due to a variety of risks and uncertainties. All forward-looking statements attributable to the Debtors or Entities acting on their behalf are expressly qualified in their entirety by the cautionary statements set forth in this Disclosure Statement. Forward-looking statements speak only as of the date on which they are made. Except as required by law, the Debtors expressly disclaim any obligation to update or revise any forward-looking statement, whether as a result of new information, subsequent events, anticipated or unanticipated circumstances, or otherwise. See Articles VIII–XII of this Disclosure Statement for a discussion of certain considerations and risk factors that Holders entitled to vote on the Plan should consider. forward-looking statements may include, but are not limited to, statements about:

| · | THE DEBTORS’ PLANS, OBJECTIVES, INTENTIONS, AND EXPECTATIONS; |

vii

| · | THE DEBTORS’ BUSINESS STRATEGY; |

| · | THE DEBTORS’ FINANCIAL STRATEGY, BUDGET, AND PROJECTIONS; |

| · | THE DEBTORS’ FINANCIAL CONDITION, REVENUES, CASH FLOWS, AND EXPENSES; |

| · | THE DEBTORS’ LEVELS OF INDEBTEDNESS, LIQUIDITY, AND COMPLIANCE WITH DEBT COVENANTS; |

| · | THE SUCCESS AND COSTS OF THE DEBTORS’ OPERATIONS; |

| · | UNCERTAINTY REGARDING THE DEBTORS’ FUTURE OPERATING RESULTS; |

| · | CUSTOMER AND VENDOR RESPONSES TO THE CHAPTER 11 CASES; |

| · | THE AMOUNT, NATURE, AND TIMING OF THE DEBTORS’ CAPITAL EXPENDITURES; |

| · | THE AVAILABILITY AND TERMS OF CAPITAL; |

| · | GENERAL ECONOMIC AND BUSINESS CONDITIONS (INCLUDING WITH RESPECT TO NON-U.S. CURRENCY FLUCTUATIONS, TARIFFS, AND/OR TRADE NEGOTIATIONS, PARTICULARLY WITH RESPECT TO ANY NON-U.S. MARKETS WHERE THE DEBTORS CONDUCT BUSINESS); |

| · | THE EFFECTIVENESS OF THE DEBTORS’ RISK MANAGEMENT ACTIVITIES; |

| · | THE DEBTORS’ COUNTERPARTIES CREDIT RISK; |

| · | THE OUTCOME OF PENDING AND FUTURE LITIGATION CLAIMS OR ANY REGULATORY PROCEEDINGS; |

| · | THE GOVERNMENTAL REGULATIONS AND TAXATION APPLICABLE TO THE DEBTORS, INCLUDING ANY CHANGES THERETO; |

| · | THE POTENTIAL ADOPTION OF NEW GOVERNMENTAL REGULATIONS; |

| · | OTHER GENERAL ECONOMIC AND POLITICAL CONDITIONS IN THE UNITED STATES AND INTERNATIONALLY, INCLUDING THOSE RESULTING FROM RECESSIONS, POLITICAL EVENTS, ACTS OR THREATS OF TERRORISM, AND MILITARY CONFLICTS; |

| · | PLANS, OBJECTIVES, AND EXPECTATIONS; |

| · | THE DEBTORS’ ABILITY TO SATISFY FUTURE CASH OBLIGATIONS. |

viii

| · | THE DEBTORS’ ABILITY TO LIST THE QVC NEW EQUITY INTERESTS ON A NATIONAL SECURITIES EXCHANGE AND TO COMPLY WITH THE INITIAL LISTING STANDARDS AND ONGOING REQUIREMENTS OF SUCH EXCHANGE; |

| · | THE DEBTORS’ ABILITY TO REGISTER THE QVC NEW EQUITY INTERESTS UNDER SECTION 12(b) OF THE SECURITIES EXCHANGE ACT OF 1934, AS AMENDED (together with the rules and regulations promulgated thereunder), THE “EXCHANGE ACT”), AND TO SATISFY THE PERIODIC REPORTING AND OTHER OBLIGATIONS OF A PUBLIC REPORTING COMPANY UNDER THE EXCHANGE ACT; AND |

| · | THE AVAILABILITY OF EXEMPTIONS FROM REGISTRATION UNDER THE SECURITIES ACT AND APPLICABLE BLUE SKY LAWS FOR THE ISSUANCE AND RESALE OF SECURITIES UNDER THE PLAN. |

Statements concerning these and other matters are not guarantees of the Reorganized Debtors’ future performance. There are risks, uncertainties, and other important factors that could cause the Reorganized Debtors’ or company’s actual performance or achievements to be different from those they may project, and the Debtors undertake no obligation to update the projections made herein. These risks, uncertainties, and factors may include the following: the Debtors’ ability to confirm and consummate the Plan; the potential that THE DEBTORS MAY NEED TO PURSUE AN ALTERNATIVE TRANSACTION IF THE PLAN IS NOT CONFIRMED; the Debtors’ ability to reduce their overall financial leverage; the potential adverse impact of the Chapter 11 Cases on the Debtors’ operations, management, and employees; the risks associated with operating the Debtors’ business during the Chapter 11 Cases; THE DEBTORS’ INABILITY TO MAINTAIN RELATIONSHIPS WITH SUPPLIERS, EMPLOYEES, AND other third parties as a result of this chapter 11 filing or those parties’ failure to comply with their contractual obligations; customer AND VENDOR responses to the Chapter 11 Cases; the Debtors’ inability to discharge or settle Claims during the Chapter 11 Cases; general economic, business, and market conditions; currency fluctuations; interest rate fluctuations; price increases; exposure to litigation; a decline in the Debtors’ market share due to competition; the Debtors’ ability to implement cost reduction initiatives in a timely manner; financial conditions of the Debtors’ customers; adverse tax changes; limited access to capital resources; changes in domestic and foreign laws and regulations; the possibility that foreign courts will not enforce the confirmation order; trade balance; natural disasters; PANDEMICS; geopolitical instability; government shutdowns; the effects of governmental regulation on the Debtors’ business; the Debtors’ ability to list the QVC New Equity Interests on a national securities exchange and to satisfy the initial listing standards thereof; the Debtors’ ability to comply with the periodic reporting and other requirements of the Exchange Act and the rules and regulations of the SEC; the availability of exemptions from registration under the Securities Act for the issuance and resale of securities under the Plan; and the Debtors’ ability to maintain effective internal controls over financial reporting and disclosure controls and procedures as a public reporting company following emergence.

ix

You are cautioned that all forward-looking statements are necessarily speculative, and there are certain risks and uncertainties that could cause actual events or results to differ materially from those referred to in such forward-looking statements. The projections and forward-looking information contained or incorporated by reference herein and attached hereto are only estimates, and the timing and amount of actual distributions to Holders of Allowed Claims and Allowed Interests, among other things, may be affected by many factors that cannot be predicted. Any analyses, estimates, or recovery projections may or may not turn out to be accurate.

Recommendation by the Debtors

each debtor’s board of managers, board of directors, sole shareholder, sole member, majority member, sole general partner, director, managing director, or manager, as applicable, has approved the restructuring transactions contemplated by the plan and described in this disclosure statement. each Debtor believes that the compromises contemplated by the restructuring transactions are fair and equitable, maximize the value of each Debtor’s ASSETS, and provide the best recovery to the DEBTORS’ STAKEholders. At this time, each Debtor believes that the restructuring transactions represent the best alternative for accomplishing the Debtors’ overall restructuring objectives.

EACH OF THE DEBTORS THEREFORE STRONGLY RECOMMENDS THAT ALL HOLDERS OF CLAIMS WHOSE VOTES ON THE PLAN ARE BEING SOLICITED ACCEPT THE PLAN by returning their ballot so as to be actually received by the Solicitation Agent no later than THE VOTING DEADLINE (MAY 19, 2026, at 11:59 P.m. (prevailing central Time) pursuant to the instructions set forth herein and In the SOLICITATION MATERIALS, INCLUDING IN YOUR BALLOT. |

x

Special Notice Regarding Federal and State Securities Laws

The Bankruptcy Court has not reviewed this Disclosure Statement or the Plan, and the securities to be issued pursuant to the Plan on or after the Effective Date will not have been the subject of a registration statement filed with the SEC under the Securities Act, any securities regulatory authority of any state under any state securities law (“Blue Sky Laws”), or the securities laws of any other jurisdiction. The Plan has not been approved or disapproved by the SEC, any state regulatory authority, or the regulatory authority of any jurisdiction and neither the SEC, any state regulatory authority, nor any other regulatory authority in any jurisdiction has passed upon the accuracy or adequacy of the information contained in this Disclosure Statement or the Plan. Any representation to the contrary is a criminal offense. The Reorganized Debtors intend to register the QVC New Equity Interests under section 12(b) of the Exchange Act and to list the QVC New Equity Interests for public trading on a national securities exchange on or as soon as reasonably practicable after the Effective Date; however, neither the Exchange Act registration nor the exchange listing has been approved, and there can be no assurance that such registration or listing will be obtained or maintained. The securities may not be offered or sold within the United States or to, or for the account or benefit of, United States persons (as defined in Regulation S under the Securities Act), except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and applicable laws of other jurisdictions.

After the Petition Date, the Debtors will rely on section 1145(a) of the Bankruptcy Code to exempt from registration under the Securities Act and Blue Sky Laws the offer, issuance, and distribution, if applicable, of securities under the Plan, and to the extent such exemption is not available, then such securities will be offered, issued, and distributed under the Plan pursuant to section 4(a)(2) of the Securities Act, Regulation D promulgated thereunder, Regulation S under the Securities Act, and/or other applicable exemptions from registration under the Securities Act and any other applicable securities laws. Neither the Solicitation nor this Disclosure Statement constitutes an offer to sell or the solicitation of an offer to buy securities in any state or jurisdiction in which such offer or solicitation is not authorized.

Securities issued pursuant to the exemption from registration set forth in section 4(a)(2) of the Securities Act, Regulation D promulgated thereunder, Regulation S under the Securities Act, and/or other available exemptions from registration will be considered “restricted securities,” will bear customary legends and transfer restrictions, and may not be transferred except pursuant to an effective registration statement or under an available exemption from the registration requirements of the Securities Act (including, to the extent applicable, Rule 144 under the Securities Act) and may be subject to any additional restrictions on the transferability of such securities pursuant to the applicable underlying documentation.

Certain securities issued under the plan may constitute “restricted securities” or “control securities” as defined under Rule 144 of the Securities Act and may be subject to legends and transfer restrictions. In addition, QVC New Equity Interests issued pursuant to section 1145(a) of the Bankruptcy Code to persons who are deemed to be “underwriters” under section 1145(b) of the Bankruptcy Code (including, in certain circumstances, “affiliates” as defined in Rule 144(a)(1) under the Securities Act) will also be subject to resale restrictions. Reference is made to Article XII (“Certain Securities Law Matters”) of this Disclosure Statement for important information regarding resales, including limitations applicable to “affiliates” under Rule 144 and “underwriters” under section 1145(b) of the Bankruptcy Code.

xi

EXCEPT TO THE EXTENT PUBLICLY AVAILABLE, THIS DISCLOSURE STATEMENT, THE DOCUMENTS ATTACHED TO THIS DISCLOSURE STATEMENT, THE PLAN, AND THE INFORMATION SET FORTH HEREIN AND THEREIN ARE CONFIDENTIAL. THIS DISCLOSURE STATEMENT, THE DOCUMENTS ATTACHED TO THIS DISCLOSURE STATEMENT, AND THE PLAN MAY CONTAIN MATERIAL NON-PUBLIC INFORMATION CONCERNING THE DEBTORS, THEIR SUBSIDIARIES, AND THEIR RESPECTIVE DEBT AND SECURITIES. FOLLOWING EMERGENCE, THE REORGANIZED DEBTORS INTEND TO BE A PUBLIC REPORTING COMPANY WITH SECURITIES REGISTERED UNDER THE EXCHANGE ACT AND LISTED ON A NATIONAL SECURITIES EXCHANGE, AND APPLICABLE SECURITIES LAWS, INCLUDING THE PROHIBITIONS ON INSIDER TRADING UNDER THE EXCHANGE ACT, WILL APPLY TO TRADING IN THE QVC NEW EQUITY INTERESTS AND ANY OTHER SECURITIES. EACH RECIPIENT HEREBY ACKNOWLEDGES THAT IT (A) IS AWARE THAT THE FEDERAL SECURITIES LAWS OF THE UNITED STATES PROHIBIT ANY PERSON (AS DEFINED IN SECTION 101(41) OF THE BANKRUPTCY CODE, A “PERSON”) WHO HAS MATERIAL NON-PUBLIC INFORMATION ABOUT A COMPANY, WHICH IS OBTAINED FROM THE COMPANY OR ITS REPRESENTATIVES, FROM PURCHASING OR SELLING SECURITIES OF SUCH COMPANY OR FROM COMMUNICATING THE INFORMATION TO ANY OTHER PERSON UNDER CIRCUMSTANCES IN WHICH IT IS REASONABLY FORESEEABLE THAT SUCH PERSON IS LIKELY TO PURCHASE OR SELL SUCH SECURITIES AND (B) IS FAMILIAR WITH THE SECURITIES EXCHANGE ACT OF 1934, AS AMENDED (THE “EXCHANGE ACT”), AND THE RULES AND REGULATIONS PROMULGATED THEREUNDER, AND AGREES THAT IT WILL NOT USE OR COMMUNICATE TO ANY PERSON OR ENTITY, UNDER CIRCUMSTANCES WHERE IT IS REASONABLY LIKELY THAT SUCH PERSON OR ENTITY IS LIKELY TO USE OR CAUSE ANY PERSON OR ENTITY TO USE, ANY CONFIDENTIAL INFORMATION IN CONTRAVENTION OF THE EXCHANGE ACT OR ANY OF ITS RULES AND REGULATIONS, INCLUDING RULE 10B-5 PROMULGATED THEREUNDER.

[Remainder of page intentionally left blank.]

xii

TABLE OF CONTENTS

| Page | |||

| I. | INTRODUCTION | 1 | |

| II. | PRELIMINARY STATEMENT | 1 | |

| III. | QUESTIONS AND ANSWERS REGARDING THIS DISCLOSURE STATEMENT AND THE PLAN | 4 | |

| A. | What is Chapter 11? | 4 | |

| B. | Why Are the Debtors Sending Me this Disclosure Statement? | 4 | |

| C. | Why Are Votes Being Solicited Prior to Bankruptcy Court Approval of this Disclosure Statement? | 4 | |

| D. | What Are the Restructuring Transactions Under the Plan? | 4 | |

| E. | Am I Entitled to Vote on the Plan? | 5 | |

| F. | What If There Is a Controversy Concerning Impairment? | 6 | |

| G. | Are There Any Special Provisions Governing Unimpaired Claims? | 6 | |

| H. | What Is the Deadline to Vote on the Plan? | 6 | |

| I. | How Do I Vote for or Against the Plan? | 7 | |

| J. | Why Is the Bankruptcy Court Holding a Combined Hearing? | 7 | |

| K. | What Is the Purpose of the Combined Hearing? | 7 | |

| L. | Who Do I Contact If I Have Additional Questions with Respect to this Disclosure Statement or the Plan? | 7 | |

| M. | What Will I Receive from the Debtors If the Plan Is Consummated? | 8 | |

| N. | What Will I Receive from the Debtors If I Hold an Allowed Administrative Claim, Priority Tax Claim, Professional Fee Claim, or a DIP LC Claim? | 15 | |

| O. | Are Any Regulatory Approvals Required to Consummate the Plan? | 19 | |

| P. | What Happens to My Recovery If the Plan Is Not Confirmed or Does Not Go Effective? | 19 | |

| Q. | If the Plan Provides That I Get a Distribution, Do I Get it upon Confirmation or When the Plan Goes Effective, and What Is Meant by “Confirmation,” “Effective Date,” and “Consummation?” | 20 | |

| R. | What Are the Sources of Cash and Other Consideration Required to Fund the Plan? | 20 | |

| S. | Are There Risks to Owning the QVC New Equity Interests upon the Debtors’ Emergence from Chapter 11? | 20 | |

| T. | Is There Potential Litigation Related to the Plan? | 20 | |

| U. | What Is the Management Incentive Plan and How Will it Affect the Distribution I Receive Under the Plan? | 21 | |

| V. | Does the Plan Preserve Causes of Action? | 21 | |

| W. | Will the Debtors Release Preference Actions Against Holders of General Unsecured Claims? | 22 | |

| X. | Will There Be Releases, Exculpation, and Injunction Granted to Parties in Interest as Part of the Plan? | 22 | |

| Y. | What Are the Consequences of Opting out of the Releases Provided by the Plan? | 29 | |

| Z. | What Are the Consequences of Not Opting in to the Releases Provided by the Plan? | 30 | |

| AA. | What Are the Consequences of Opting in to the Releases Provided by the Plan? | 30 | |

| BB. | Does the Bankruptcy Code Protect Against Discriminatory Treatment? | 30 | |

| CC. | Will the Company Retain Documents After Any Effective Date? | 30 | |

| DD. | What Is the Effect of Reimbursement or Contribution? | 31 | |

| EE. | What Is the Effect of the Plan on the Debtors’ Capital Structure? | 31 | |

| FF. | What Is the Effect of the Plan on the Debtors’ Ongoing Business? | 31 | |

| GG. | Will Any Party Have Significant Influence over the Corporate Governance and Operations of the Reorganized Debtors? | 31 | |

| HH. | Do the Debtors Recommend Voting in Favor of the Plan? | 32 | |

| II. | Who Supports the Plan? | 32 | |

i

| IV. | CORPORATE HISTORY AND BUSINESS OPERATIONS. | 32 | |

| A. | QVC: “Quality, Value, and Convenience.” | 32 | |

| B. | Origins and Early Success | 33 | |

| C. | The Company’s Business and Operations Today | 34 | |

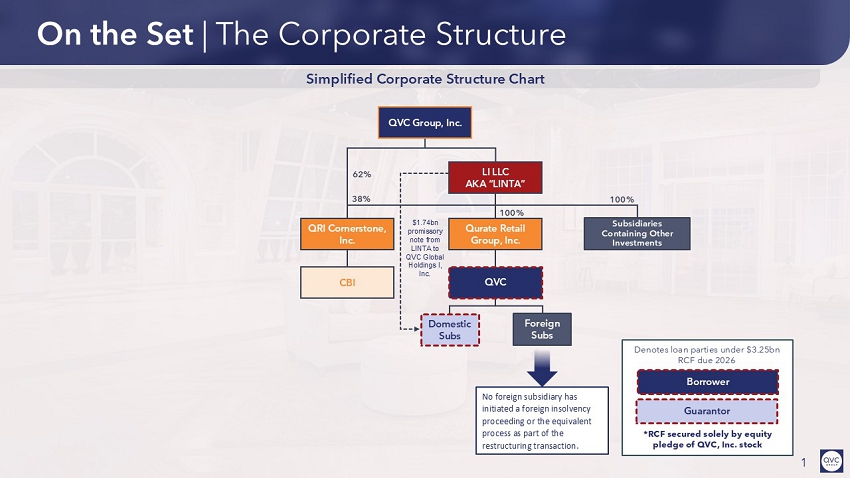

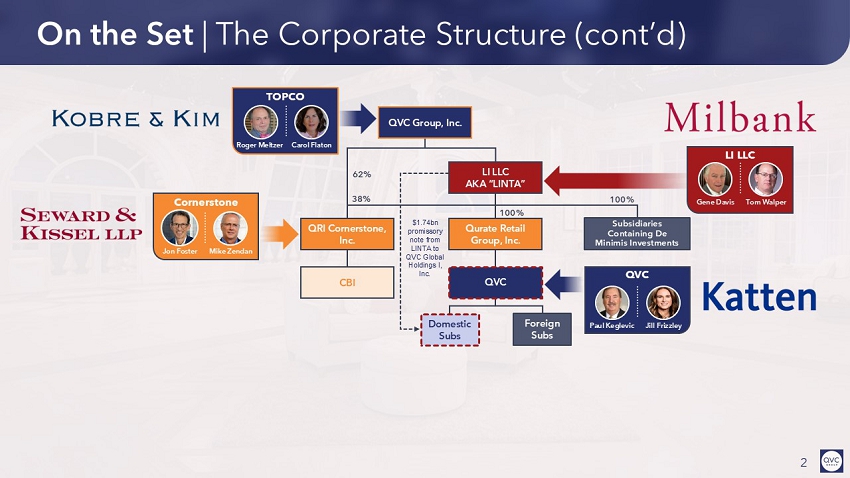

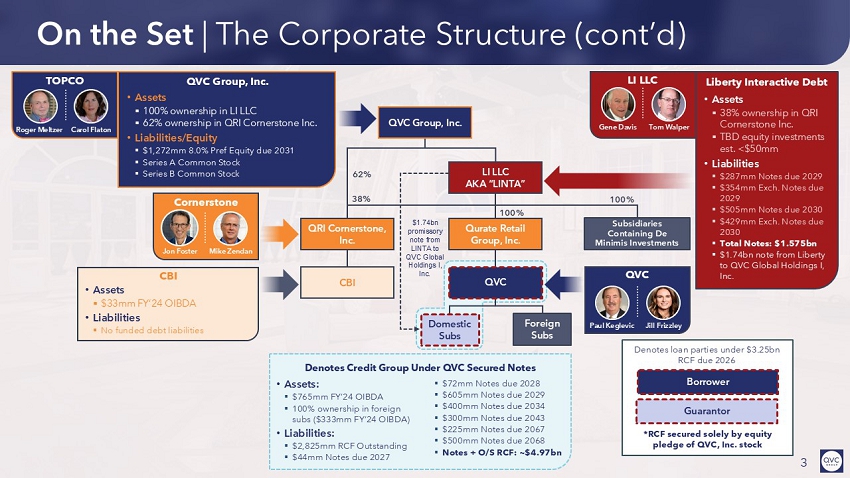

| D. | Prepetition Corporate Structure, Capital Structure, and Liquidity Profile | 36 | |

| V. | EVENTS LEADING TO THESE CHAPTER 11 CASES | 41 | |

| A. | Prepetition Challenges | 41 | |

| B. | Historical Liquidity-Enhancing Initiatives | 42 | |

| C. | Key Operational Initiatives | 44 | |

| D. | Prepetition Initiatives | 46 | |

| VI. | MATERIAL DEVELOPMENTS AND ANTICIPATED EVENTS OF THE CHAPTER 11 CASES | 49 | |

| A. | First Day Relief | 49 | |

| B. | Proposed Confirmation Schedule | 49 | |

| VII. | THE DEBTORS’ PLAN | 50 | |

| A. | General Settlement of Claims and Interests | 50 | |

| B. | Intercompany Settlement. | 50 | |

| C. | Restructuring Transactions | 58 | |

| D. | The Reorganized Debtors | 59 | |

| E. | Sources of Consideration for Plan Distributions | 59 | |

| F. | Corporate Existence | 63 | |

| G. | Vesting of Assets in the Reorganized Debtors | 63 | |

| H. | Cancellation of Existing Securities, Agreements, and Interests | 64 | |

| I. | Corporate Action | 65 | |

| J. | New Organizational Documents | 65 | |

| K. | Directors and Officers of the Reorganized Debtors | 65 | |

| L. | Effectuating Documents; Further Transactions | 66 | |

| M. | Certain Securities Law Matters. | 66 | |

| N. | Section 1146 Exemption | 67 | |

| O. | Employee Compensation and Benefits. | 68 | |

| P. | Director and Officer Liability Insurance | 69 | |

| Q. | Management Incentive Plan. | 69 | |

| R. | Preservation of Causes of Action. | 70 | |

| S. | Release of Avoidance Actions. | 71 | |

| T. | Cashless Transactions. | 71 | |

ii

| VIII. | OTHER KEY ASPECTS OF THE PLAN | 71 | |

| A. | Treatment of Executory Contracts and Unexpired Leases | 71 | |

| B. | Provisions Governing Distributions. | 75 | |

| C. | Procedures for Resolving Contingent, Unliquidated, and Disputed Claims | 82 | |

| D. | Conditions Precedent to Confirmation and Consummation of the Plan | 85 | |

| E. | Modification, Revocation, or Withdrawal of the Plan | 87 | |

| F. | Other Claims and Interest Classification and Treatment Features. | 87 | |

| IX. | RISK FACTORS | 89 | |

| A. | Bankruptcy Law Considerations | 89 | |

| B. | Risks Related to Recoveries Under the Plan | 96 | |

| C. | Risks Related to the Debtors’ and the Reorganized Debtors’ Business | 99 | |

| D. | Risks Related to the Offer and Issuance of Securities Under the Plan | 106 | |

| X. | SOLICITATION AND VOTING PROCEDURES | 109 | |

| A. | Holders of Claims Entitled to Vote on the Plan | 109 | |

| B. | Voting Record Date | 109 | |

| C. | Voting on the Plan. | 110 | |

| D. | Ballots Not Counted. | 110 | |

| E. | Votes Required for Acceptance by a Class. | 110 | |

| F. | Solicitation Procedures. | 111 | |

| G. | How to Opt Out of the Releases. | 111 | |

| XI. | CONFIRMATION OF THE PLAN | 112 | |

| A. | The Combined Hearing | 112 | |

| B. | Requirements for Confirmation of the Plan | 112 | |

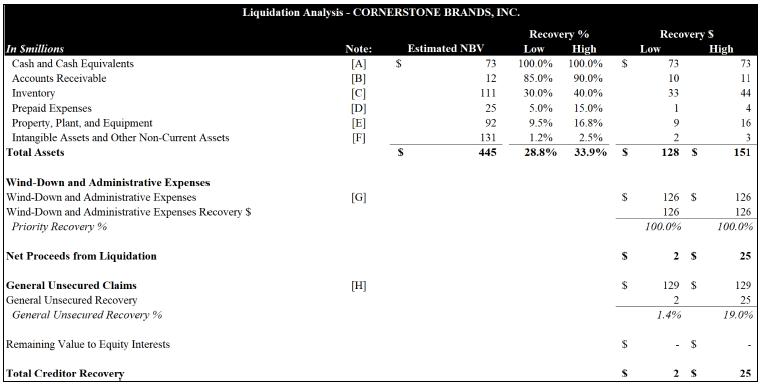

| C. | Best Interests of Creditors/Liquidation Analysis | 112 | |

| D. | Valuation Analysis. | 113 | |

| E. | Feasibility | 113 | |

| F. | Acceptance by Impaired Classes | 113 | |

| G. | Confirmation Without Acceptance by All Impaired Classes | 114 | |

| XII. | CERTAIN SECURITIES LAW MATTERS | 115 | |

| A. | QVC New Equity Interests | 115 | |

| B. | Exemption from Registration Requirements; Issuance of QVC New Equity Interests and Other Securities Under the Plan | 115 | |

| C. | Resales of QVC New Equity Interests and Other Securities; Definition of “Underwriter” Under Section 1145(b) of the Bankruptcy Code | 116 | |

| XIII. | Certain united states Federal Income Tax Consequences of the Plan | 120 | |

| A. | Introduction | 120 | |

| B. | Certain U.S. Federal Income Tax Consequences of the Plan to the Debtors and Reorganized Debtors. | 121 | |

| C. | Certain U.S. Federal Income Tax Consequences to U.S. Holders of Allowed Class B3 Claims, Class B4 Claims, and Class C3 Claims. | 125 | |

| D. | Certain U.S. Federal Income Tax Consequences of the Plan to Non-U.S. Holders. | 131 | |

| E. | FATCA. | 136 | |

| F. | U.S. Information Reporting and Back-Up Withholding. | 136 | |

iii

| XIV. | RECOMMENDATION | 137 | |

EXHIBITS3

| EXHIBIT A | Plan of Reorganization |

| EXHIBIT B | RSA |

| EXHIBIT C | Financial Projections |

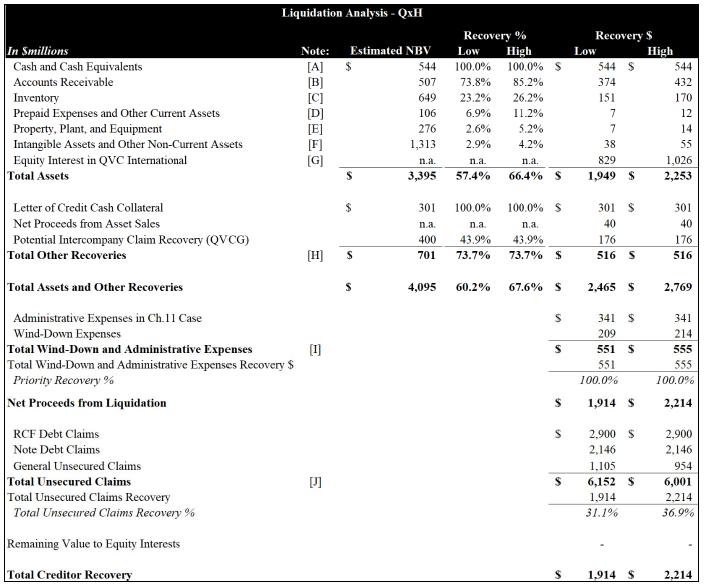

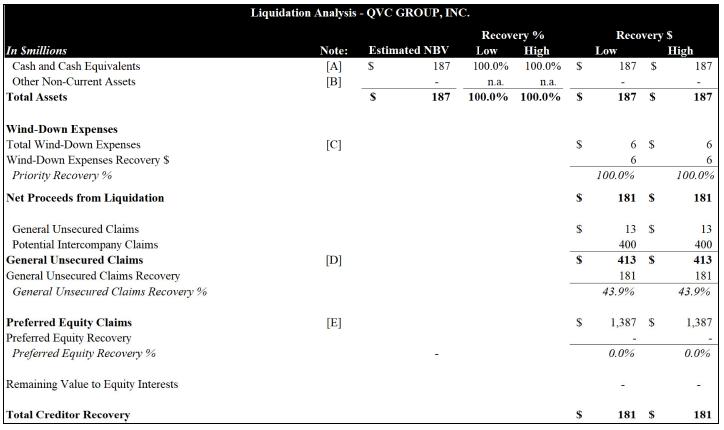

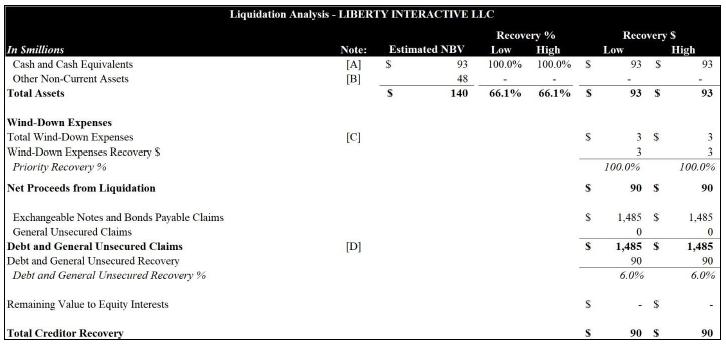

| EXHIBIT D | Liquidation Analysis |

| EXHIBIT E | Valuation Analysis |

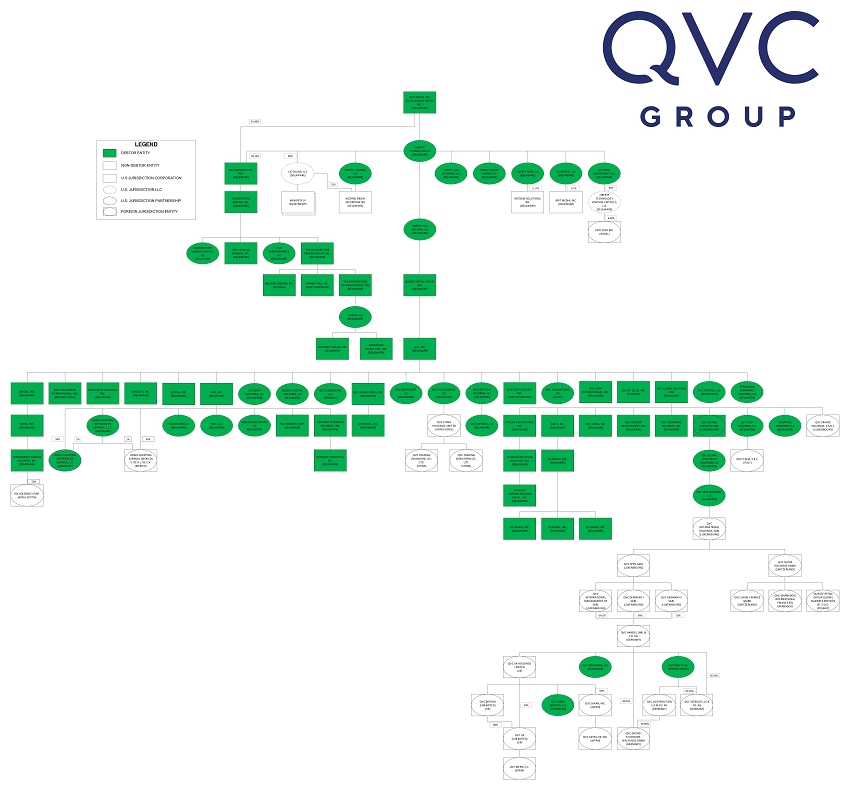

| EXHIBIT F | Simplified Organizational Chart |

| EXHIBIT G | Corporate Structure Chart |

| 3 | Each Exhibit is incorporated herein by reference. |

iv

| I. | INTRODUCTION. |

QVC Group, Inc. (“QVCG”) and its affiliated debtors and debtors in possession in the above-captioned cases (collectively, the “Debtors” and, together with their non-Debtor affiliates, the “Company”), are pursuing proposed restructuring and recapitalization transactions (the “Restructuring Transactions”) pursuant to the terms and conditions set forth in that certain Restructuring Support Agreement by and among the Company and the Consenting Stakeholders (as may be amended, supplemented, or otherwise modified from time to time, and including all schedules, exhibits, and annexes thereto, the “RSA”), attached hereto as Exhibit B. The Plan constitutes a separate chapter 11 plan for each of the Debtors. The rules of interpretation set forth in Article I.B of the Plan govern the interpretation of this Disclosure Statement.

Pursuant to the RSA, the Debtors have launched a solicitation of votes to accept or reject the Plan (the “Solicitation”)1 to Holders of RCF Claims, QVC Notes Claims, and LINTA Notes Claims. The Debtors intend to submit this disclosure statement (this “Disclosure Statement”) pursuant to section 1125 of the Bankruptcy Code, to Holders of RCF Claims, QVC Notes Claims, and LINTA Notes Claims in connection with the Solicitation. A copy of the Plan is attached hereto as Exhibit A and incorporated herein by reference.

In connection with the RSA, and to seek Confirmation and Consummation of the Plan, the Debtors intend to promptly commence voluntary cases (the “Chapter 11 Cases”) under chapter 11 of the Bankruptcy Code in the United States Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court”).

THE DEBTORS BELIEVE THAT THE COMPROMISES CONTEMPLATED UNDER THE PLAN ARE FAIR AND EQUITABLE, MAXIMIZE THE VALUE OF THE DEBTORS’ ESTATES, AND PROVIDE THE BEST AVAILABLE RECOVERY TO STAKEHOLDERS. AT THIS TIME, THE DEBTORS BELIEVE THE PLAN REPRESENTS THE BEST AVAILABLE OPTION FOR COMPLETING THE CHAPTER 11 CASES. THE DEBTORS STRONGLY RECOMMEND THAT YOU VOTE TO ACCEPT THE PLAN.

| II. | PRELIMINARY STATEMENT. |

QVCG revolutionized the way we shop and interact with products. QVCG brought commerce into our living rooms and then to our front doors. For more than 40 years, QVCG has been a steady, credible provider for American consumers. As QVCG transforms itself to better fit the mobile e-commerce world, this chapter 11 process will ensure that it remains an American icon for the next 40 years.

The world has changed, and the Company is changing with it. Linear TV subscriptions continue to decline, customer attention has fragmented, and consumers increasingly shop using digital channels. Embracing those changes, the Company has invested billions to evolve with consumers’ changing preferences.

That transformation is ongoing, and the Company has shown tremendous progress. For example, the Company launched the first ever 24/7 livestream programming on TikTok last April, quickly becoming a top seller on TikTok Shop in the United States, adding 1 million in 2025 alone. The Company’s streaming services have approximately 1.3 million monthly average users, and television broadcast continues to have an engaged customer base, with approximately 91% of worldwide shipped sales coming from repeat customers.

| 1 | Capitalized terms used but not otherwise defined in this Disclosure Statement shall have the meaning ascribed to such terms in the Plan. The summary of the Plan provided herein is qualified in its entirety by reference to the Plan. In the case of any inconsistency between this Disclosure Statement and the Plan, the Plan will govern. |

While the business is making great progress, more time and money is needed to complete the transformation. This restructuring process is a necessary step in that process. In recent years, the Company’s balance sheet has impaired its ability to invest at the level necessary to fully transition to the digital age. Through this Chapter 11, the Company will right-size its balance sheet and free up the capital necessary for the Company to complete its transformation. And it will ensure the Company is a go-to for the next generation of shoppers.

The opportunities for the Company to fully grow into digital shopping are immense. Social shopping is experiencing exponential growth. To succeed in the new landscape, firms need product that is ready to sell, capacity to get products to customers, and an excellent end-to-end user experience. Investment is required across the full value chain—from sourcing to fulfillment to customer service. The Company has all the tools to provide that full end-to-end value: decades of experience with content creation and production expertise; deep vendor relationships; a mature distribution network; and the goodwill earned from a loyal, millions-strong customer base. So, although the means of delivery are changing, the core value proposition of the Company remains strong. The Company will continue to deliver that value during this chapter 11 process and beyond as it completes its transformation into the digital shopping age.

As part of its ongoing story, the Company intends to file prepackaged chapter 11 cases to implement a comprehensive restructuring transaction outlined in the RSA that has been agreed to by the Debtors and the Consenting Stakeholders. The key terms of the RSA include:

| · | QVC, Inc. (“QVC”) or any successor or assign thereto, by merger, consolidation, or otherwise (such entity, “Reorganized QVC”) shall issue takeback debt (the “Takeback Debt”) on the terms and conditions set forth in the Takeback Debt Documents; |

| · | Reorganized QVC shall issue new common stock (the “QVC New Equity Interests”); |

| · | (1) each Holder of an Allowed RCF Claim shall receive, in full and final satisfaction, settlement, release, and discharge of (a) such portion of its RCF Claim comprising RCF Loan Claims, its Pro Rata share (taking into account Claims in Class B4) of the QVC Funded Debt Plan Consideration and (b) such portion of its RCF Claim comprising RCF Letter of Credit Claims, Cash equal to the full amount of its RCF Letter of Credit Claim; provided that any RCF Letter of Credit that remains undrawn and outstanding as of the Effective Date shall be either (x) rolled into the Exit ABL Facility and granted liens pursuant to the Exit ABL Facility on terms acceptable to the Required Consenting RCF Lenders and the applicable issuing bank, (y) cancelled or returned undrawn to the applicable issuing bank, or (z) cash collateralized or otherwise backstopped in a manner reasonably satisfactory to the applicable issuing bank, in each case, on or prior to the Effective Date and (2) the QVC Debtors or the Reorganized QVC Debtors, as applicable, shall pay in full in Cash all RCF Agent Fees; |

| · | (1) each Holder of an Allowed QVC Notes Claim shall receive, in full and final satisfaction, settlement, release, and discharge of such QVC Notes Claim, its Pro Rata share (taking into account Claims in Class B3) of the QVC Funded Debt Plan Consideration and (2) the QVC Debtors or the Reorganized QVC Debtors, as applicable, shall pay in full in Cash all QVC Notes Trustee Fees; |

2

| · | each Holder of an Allowed LINTA Notes Claim shall receive, in full and final satisfaction, settlement, release, and discharge of such LINTA Notes Claim, its Pro Rata share of the LINTA Distributable Cash. |

| · | Third-party General Unsecured Claims will be unimpaired; and |

| · | QVCG Preferred Equity Interests and QVCG Common Equity Interests will be cancelled. |

The RSA and Plan are structured to support the Company’s ongoing commitment to its customers, business partners, and stakeholders while strengthening the business as a going-concern. With the support of their lenders and other key stakeholders, the Debtors seek authority to move through the chapter 11 process efficiently. The Debtors seek to proceed through these Chapter 11 Cases on an approximately 40-day timeline, subject to Court approval, to minimize disruption to the business and accrual of administrative expenses.

Each of the Governing Bodies of Disinterested Directors (as defined herein), with the assistance of their individual counsel, conducted an independent investigation to assess the merits and potential value of any potential claims and Causes of Action held by the Company against any Related Party or otherwise related to any conflicts matter, as further explained in Article VII.B of this Disclosure Statement. Subject to the completion of that investigation by each of the Governing Bodies of Disinterested Directors, and as contemplated by the Intercompany Settlement, the Plan includes customary debtor releases (and, separately, customary third-party releases). The releases, exculpation, and injunction are an integral component of the Plan, which provides significant distributions of value to administrative, priority, secured, and unsecured creditors. Unless otherwise explicitly released under the Plan or separate order of the Bankruptcy Court, all other unencumbered assets, including the Estates’ claims and Causes of Action, are being preserved by the Plan.

The Debtors strongly believe that the deleveraging and liquidity-enhancing Restructuring Transactions contemplated by the RSA and the Plan are in the best interest of the Debtors’ Estates and represent the best available alternative to the Company at this time. Given the Debtors’ core strengths and strong customer relationships, the Debtors are confident that they can implement the Restructuring Transactions contemplated by the Plan and the RSA to ensure the Debtors’ long-term viability. Ultimately, confirmation of the Plan will enable the Company to eliminate approximately $6 billion in funded debt and equity obligations and emerge from chapter 11 in a better position than ever to remain a global retail leader.

| FOR THESE REASONS, THE DEBTORS STRONGLY RECOMMEND THAT HOLDERS OF CLAIMS ENTITLED TO VOTE ON THE PLAN VOTE TO ACCEPT THE PLAN. |

3

| III. | QUESTIONS AND ANSWERS REGARDING THIS DISCLOSURE STATEMENT AND THE PLAN. |

| A. | What is Chapter 11? |

Chapter 11 is the principal business reorganization chapter of the Bankruptcy Code. In addition to permitting debtor rehabilitation, chapter 11 promotes equal treatment for similarly situated creditors and equity holders, subject to the priority of distributions prescribed by the Bankruptcy Code.

The commencement of a chapter 11 case creates an estate that comprises all of the legal and equitable interests of the debtor as of the date the chapter 11 case is commenced. The Bankruptcy Code provides that a debtor may continue to operate its business and remain in possession of its property as a “debtor in possession.”

Consummating a chapter 11 plan is the principal objective of a chapter 11 case. A bankruptcy court’s confirmation of a plan binds the debtor, any person acquiring property under the plan, any creditor or equity holder of the debtor (whether or not such creditor or equity holder voted to accept the plan), and any other entity as may be ordered by the bankruptcy court. Subject to certain limited exceptions, the order issued by a bankruptcy court confirming a plan provides for the treatment of the debtor’s liabilities in accordance with the terms of the confirmed plan.

| B. | Why Are the Debtors Sending Me this Disclosure Statement? |

The Debtors are seeking to obtain Bankruptcy Court approval of the Plan. Before soliciting acceptances of the Plan, section 1125 of the Bankruptcy Code requires that the Debtors prepare a disclosure statement containing adequate information sufficient to enable a hypothetical reasonable investor to make an informed decision regarding acceptance of the Plan and to share such Disclosure Statement with all Holders of Claims whose votes on the Plan are being solicited. This Disclosure Statement is being submitted in accordance with these requirements.

| C. | Why Are Votes Being Solicited Prior to Bankruptcy Court Approval of this Disclosure Statement? |

By sending this Disclosure Statement and soliciting votes for the Plan prior to approval by the Bankruptcy Court, the Debtors are preparing to seek Confirmation of the Plan shortly after commencing the Chapter 11 Cases. The Debtors will ask the Bankruptcy Court to approve this Disclosure Statement on a final basis together with Confirmation of the Plan at the same hearing, which may be scheduled as shortly as forty (40) days after commencing the Chapter 11 Cases, all subject to the Bankruptcy Court’s approval and availability.

| D. | What Are the Restructuring Transactions Under the Plan? |

The RSA and the Plan contemplate a recapitalization of the Debtors, through which certain of the Debtors will issue and distribute the QVC New Equity Interests, enter into the Exit ABL Facility, and issue the Takeback Debt. In addition, the Plan contemplates that CBI will continue to operate as a going-concern on and following the Effective Date.

4

| E. | Am I Entitled to Vote on the Plan? |

Your ability to vote on, and your distribution under, the Plan, if any, depends on what type of Claim or Interest you hold and whether you held that Claim or Interest as of the Voting Record Date (i.e., as of April 13, 2026). Each category of Holders of Claims or Interests, as set forth in Article III of the Plan pursuant to sections 1122(a) and 1123(a)(1) of the Bankruptcy Code is referred to as a “Class.” Each Class’s respective voting status is set forth below:

| Class | Claims and Interests | Status | Voting Rights |

| Class A1 | Other

Secured Claims against QVCG |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class A2 | Other

Priority Claims against QVCG |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class A3 | General

Unsecured Claims against QVCG |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class A4 | QVC-QVCG Settlement Claim | Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class A5 | Other

Intercompany Claims against QVCG |

Unimpaired / Impaired | Not

Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class A6 | QVCG Preferred Equity Interests | Impaired | Not Entitled to Vote (Deemed to Reject) |

| Class A7 | QVCG Common Equity Interests | Impaired | Not Entitled to Vote (Deemed to Reject) |

| Class A8 | Section 510(b) Claims

against QVCG |

Impaired | Not Entitled to Vote (Deemed to Reject) |

| Class B1 | Other

Secured Claims against the QVC Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class B2 | Other

Priority Claims against the QVC Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class B3 | RCF

Claims against the QVC Debtors |

Impaired | Entitled to Vote |

| Class B4 | QVC

Notes Claims against the QVC Debtors |

Impaired | Entitled to Vote |

| Class B5 | General

Unsecured Claims against the QVC Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class B6 | Intercompany

Claims against the QVC Debtors |

Unimpaired / Impaired | Not Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class B7 | Intercompany

Interests in the QVC Debtors |

Unimpaired / Impaired | Not Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class B8 | Section 510(b) Claims

against the QVC Debtors |

Impaired | Not Entitled to Vote (Deemed to Reject) |

| Class C1 | Other

Secured Claims against the LINTA Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class C2 | Other

Priority Claims against the LINTA Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class C3 | LINTA

Notes Claims against the LINTA Debtors |

Impaired | Entitled to Vote |

| Class C4 | General

Unsecured Claims against the LINTA Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class C5 | Other

Intercompany Claims against the LINTA Debtors |

Unimpaired / Impaired | Not

Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class C6 | Intercompany

Interests in the LINTA Debtors |

Unimpaired / Impaired | Not

Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class C7 | Section 510(b) Claims

against the LINTA Debtors |

Impaired | Not Entitled to Vote (Deemed to Reject) |

| Class D1 | Other

Secured Claims against the CBI Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

5

| Class | Claims and Interests | Status | Voting Rights |

| Class D2 | Other

Priority Claims against the CBI Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class D3 | General

Unsecured Claims against the CBI Debtors |

Unimpaired | Not Entitled to Vote (Presumed to Accept) |

| Class D4 | Intercompany Claims against the CBI Debtors | Unimpaired / Impaired | Not

Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class D5 | Intercompany Interests in the CBI Debtors | Unimpaired / Impaired | Not

Entitled to Vote (Presumed to Accept / Deemed to Reject) |

| Class D6 | Section 510(b) Claims

against the CBI Debtors |

Impaired | Not Entitled to Vote (Deemed to Reject) |

Except for the Claims addressed in Article II of the Plan, all Claims and Interests are classified in the Classes set forth above in accordance with sections 1122 and 1123(a)(1) of the Bankruptcy Code. A Claim or an Interest, or any portion thereof, is classified in a particular Class only to the extent that any portion of such Claim or Interest qualifies within the description of that Class and is classified in other Classes to the extent that any portion of such Claim or Interest qualifies within the description of such other Classes. A Claim or an Interest also is classified in a particular Class for the purpose of receiving distributions under the Plan only to the extent that such Claim or Interest is an Allowed Claim or Allowed Interest in that Class and has not been paid, released, or otherwise satisfied prior to the Effective Date.

The Plan constitutes a separate Plan for each of the Debtors, and the classification of Claims and Interests set forth therein shall apply separately to each of the Debtors. All of the potential Classes for the Debtors are set forth in the Plan. Such groupings shall not affect any Debtor’s status as a separate legal Entity, change the organizational structure of the Debtors’ business enterprise, constitute a change of control of any Debtor for any purpose, cause a merger or consolidation of any legal Entities, or cause the transfer of any assets, and, except as otherwise provided by or permitted under the Plan, all Debtors shall continue to exist as separate legal Entities after the Effective Date.

Except as otherwise provided in the Plan, nothing under the Plan shall affect the Debtors’ or the Reorganized Debtors’ rights regarding any Unimpaired Claims, including all rights regarding legal and equitable defenses to, or setoffs or recoupments against, any such Unimpaired Claims.

| F. | What If There Is a Controversy Concerning Impairment? |

If a controversy arises as to whether any Claims or Interests, or any Class of Claims or Interests, are Impaired, the Bankruptcy Court shall, after notice and a hearing, determine such controversy on or before the Confirmation Date or such other date as fixed by the Bankruptcy Court.

| G. | Are There Any Special Provisions Governing Unimpaired Claims? |

Except as otherwise provided in the Plan, nothing under the Plan or the Plan Supplement shall affect the rights of the Debtors or the Reorganized Debtors, as applicable, regarding any Unimpaired Claims, including all rights regarding legal and equitable defenses to, or setoffs or recoupments against, any such Unimpaired Claims.

| H. | What Is the Deadline to Vote on the Plan? |

The voting deadline with respect to the Plan (the “Voting Deadline”) is May 19, 2026, at 11:59 p.m. (prevailing Central Time).

6

| I. | How Do I Vote for or Against the Plan? |

Detailed instructions regarding how to vote on the Plan are contained on the ballots distributed to Holder of Claims that are entitled to vote on the Plan (the “Ballots”). For your vote to be counted, your Ballot (or your Nominee’s Master Ballot containing your vote if you are a beneficial holder of the QVC Notes or LINTA Notes) must be properly completed, executed, and delivered as directed, so that the Ballot containing your vote is actually received by the Solicitation Agent on or before the Voting Deadline, i.e., May 19, 2026 at 11:59 p.m., prevailing Central Time.

| J. | Why Is the Bankruptcy Court Holding a Combined Hearing? |

Section 1128(a) of the Bankruptcy Code requires the Bankruptcy Court to hold a hearing on Confirmation of the Plan and recognizes that any party in interest may object to Confirmation of the Plan. Shortly after the commencement of the Chapter 11 Cases, the Debtors will request that the Bankruptcy Court schedule the Combined Hearing, at which time the Debtors will seek, among other things, Confirmation of the Plan. At the Combined Hearing, the Debtors will also seek Bankruptcy Court approval of this Disclosure Statement pursuant to section 1125 of the Bankruptcy Code as containing adequate information of a kind, and in sufficient detail, to enable a hypothetical reasonable investor to make an informed judgment regarding acceptance of the Plan and that the Debtors shared this Disclosure Statement with all Holders of Claims whose votes on the Plan are being solicited. All parties in interest will be served notice of the time, date, and location of the Combined Hearing once scheduled. The Combined Hearing may be adjourned from time to time without further notice.

| K. | What Is the Purpose of the Combined Hearing? |

The purpose of the Combined Hearing is to seek approval of this Disclosure Statement and confirmation of the Plan. If so approved, the Bankruptcy Court will have held that this Disclosure Statement has provided the Voting Classes with adequate information to make an informed decision as to whether to vote to accept or reject the Plan in accordance with section 1125(a)(1) of the Bankruptcy Code.

The confirmation of a plan of reorganization by a bankruptcy court binds the debtor, any issuer of securities under a plan of reorganization, any person acquiring property under a plan of reorganization, any creditor or interest holder of a debtor, and any other person or entity as may be ordered by the bankruptcy court in accordance with the applicable provisions of the Bankruptcy Code. Subject to certain limited exceptions, the order issued by the bankruptcy court confirming a plan of reorganization discharges a debtor from any debt that arose before the confirmation of such plan of reorganization and provides for the treatment of such debt in accordance with the terms of the confirmed plan of reorganization.

| L. | Who Do I Contact If I Have Additional Questions with Respect to this Disclosure Statement or the Plan? |

If you have any questions regarding this Disclosure Statement or the Plan, please contact the Solicitation Agent, Kroll, by calling (888) 575-5337 (Toll free from US / Canada) OR +1 (347) 292-4386 (International, toll), or emailing QVCBallots@ra.kroll.com with “In re: QVC – Solicitation Inquiry” in the subject line. Copies of the Plan, this Disclosure Statement, and any other publicly filed documents in the Chapter 11 Cases are available free of charge, as applicable, by: (a) visiting the Debtors’ restructuring website at https://restructuring.ra.kroll.com/QVC after the Petition Date; (b) emailing using QVCBallots@ra.kroll.com (with “In re: QVC – Solicitation Inquiry” in the subject line); or (c) calling the Solicitation Agent at the number(s) listed above. You may also obtain copies of any pleadings filed in the Chapter 11 Cases via PACER at https://www.pacer.gov (for a fee).

7

| M. | What Will I Receive from the Debtors If the Plan Is Consummated? |

The following chart provides a summary of the anticipated distributions to Holders of Claims or Interests under the Plan. Your ability to receive distributions under the Plan depends upon the ability of the Debtors to obtain Confirmation and meet the conditions necessary to consummate the Plan.

Pursuant to the Plan, each Holder of an Allowed Claim or Allowed Interest, as applicable, shall receive the treatment described below in full and final satisfaction, settlement, release, and discharge of and in exchange for such Holder’s Allowed Claim or Allowed Interest, except to the extent different treatment is agreed to by the Debtors or the Reorganized Debtors, as applicable, with the consent of the Required Consenting QVC Noteholders and the Required Consenting RCF Lenders, and the Holder of such Allowed Claim or Allowed Interest, as applicable, or unless such Allowed Claim or Allowed Interest has been paid, released, or otherwise satisfied prior to the Effective Date. Unless otherwise indicated, the Holder of an Allowed Claim or Allowed Interest, as applicable, shall receive such treatment on the Effective Date (or, if payment is not then due, in accordance with such Claim’s terms in the ordinary course of business) or as soon as reasonably practicable thereafter.

The allowance, classification, and treatment of all Allowed Claims and Allowed Interests and the respective distributions and treatments under the Plan take into account and conform to the relative priority and rights of the Claims and Interests in each Class in connection with any contractual, legal, and equitable subordination rights relating thereto, whether arising under general principles of equitable subordination, section 510(b) of the Bankruptcy Code, or otherwise. Pursuant to section 510 of the Bankruptcy Code, and subject to any applicable consent or approval rights under the RSA, the Debtors, or the Reorganized Debtors, as applicable, reserve the right to re-classify any Allowed Claim or Allowed Interest in accordance with any contractual, legal, or equitable subordination rights relating thereto.

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class A1 | Other Secured Claims against QVCG | Each Holder of an Allowed Other Secured Claim against QVCG shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Secured Claim, as determined by the applicable Debtors: (i) payment in full in Cash; or (ii) such other treatment rendering such Allowed Other Secured Claim Unimpaired. |

N/A | 100% |

| Class A2 | Other Priority Claims against QVCG | Each Holder of an Allowed Other Priority Claim against QVCG shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Priority Claim, treatment in a manner consistent with section 1129(a) of the Bankruptcy Code. | N/A | 100% |

8

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class A3 | General Unsecured Claims against QVCG | Each Holder of an Allowed General Unsecured Claim against QVCG shall receive, in full and final satisfaction, settlement, release, and discharge of such General Unsecured Claim, as determined by the applicable Debtors: (i) payment in full in Cash on the later of (A) the Effective Date or (B) the date due in the ordinary course of business in accordance with the terms and conditions of the particular transaction giving rise to, or the agreement governing, such Allowed General Unsecured Claim against QVCG; or (ii) such other treatment rendering such Allowed General Unsecured Claims Unimpaired. |

N/A | 100% |

| Class A4 | QVC-QVCG Settlement Claim | QVC shall receive, in full and final satisfaction, settlement, release, and discharge of the QVC-QVCG Settlement Claim: (i) all QVCG Distributable Cash; or (ii) such other treatment otherwise addressed at the option of the Debtors, and acceptable to such Holders of QVC-QVCG Settlement Claims, the Required Consenting QVC Noteholders, and the Required Consenting RCF Lenders rendering such QVC-QVCG Settlement Claims Unimpaired, and in each case as set forth in the Restructuring Steps Plan. |

$400,000,000 | N/A |

| Class A5 | Other Intercompany Claims against QVCG | Each Other Intercompany Claim against QVCG shall be, in full and final satisfaction, settlement, release, and discharge of such Other Intercompany Claim, as determined by the applicable Debtors, with the consent of the Required Consenting QVC Noteholders and the Required Consenting RCF Lenders: (i) Reinstated; (ii) set off, settled, discharged, contributed, cancelled, converted to equity; (iii) released without any distribution on account of such Allowed Other Intercompany Claim; or (iv) otherwise addressed at the option of the Debtors, in each case as set forth in the Restructuring Steps Plan. |

N/A | N/A |

| Class A6 | QVCG Preferred Equity Interests | The QVCG Preferred Equity Interests shall be cancelled, released, discharged, extinguished, and of no further force or effect, and such Holders shall not receive any distribution, property, or other value under the Plan on account of such QVCG Preferred Equity Interests. | N/A | 0% |

| Class A7 | QVCG Common Equity Interests | The QVCG Common Equity Interests shall be cancelled, released, discharged, extinguished, and of no further force or effect, and such Holders shall not receive any distribution, property, or other value under the Plan on account of such QVCG Common Equity Interests. | N/A | 0% |

9

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class A8 | Section 510(b) Claims against QVCG | On the Effective Date, each Section 510(b) Claim against QVCG shall be cancelled, released, discharged, and extinguished and will be of no further force or effect, and such Holders will not receive any distribution on account of such Section 510(b) Claim. | N/A2 | N/A |

| Class B1 | Other Secured Claims against the QVC Debtors | Each Holder of an Allowed Other Secured Claim against a QVC Debtor shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Secured Claim, as determined by the applicable Debtors: (i) payment in full in Cash; (ii) the collateral securing its Allowed Other Secured Claim; (iii) Reinstatement of its Allowed Other Secured Claim; or (iv) such other treatment acceptable to the Required Consenting QVC Noteholders and the Required Consenting RCF Lenders rendering such Allowed Other Secured Claim Unimpaired. |

N/A | 100% |

| Class B2 | Other Priority Claims against the QVC Debtors | Each Holder of an Allowed Other Priority Claim against a QVC Debtor shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Priority Claim, treatment in a manner consistent with section 1129(a) of the Bankruptcy Code. | N/A | 100% |

| Class B3 | RCF Claims against the QVC Debtors | (1) Each Holder of an Allowed RCF Claim shall receive, in full and final satisfaction, settlement, release, and discharge of (a) such portion of its RCF Claim comprising RCF Loan Claims, its Pro Rata share (taking into account Claims in Class B4) of the QVC Funded Debt Plan Consideration, and (b) such portion of its RCF Claim comprising RCF Letter of Credit Claims, Cash equal to the full amount of its RCF Letter of Credit Claim provided that, any RCF Letter of Credit that remains undrawn and outstanding as of the Effective Date shall be either (x) rolled into the Exit ABL Facility and granted liens pursuant to the Exit ABL Facility on terms acceptable to the Required Consenting RCF Lenders and the applicable issuing bank, (y) cancelled or returned undrawn to the applicable issuing bank, or (z) cash collateralized or otherwise backstopped in a manner reasonably satisfactory to the applicable issuing bank, in each case, on or prior to the Effective Date and (2) the QVC Debtors or the Reorganized QVC Debtors, as applicable, shall pay in full in Cash all RCF Agent Fees. | Approximately $2,900,000,000.00 | N/A |

| 2 | Notwithstanding anything to the contrary in the Plan, a Section 510(b) Claim, if any such Claim exists, may only become Allowed by Final Order of the Bankruptcy Court. |

10

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class B4 | QVC Notes Claims against the QVC Debtors | (1) Each Holder of an Allowed QVC Notes Claim shall receive, in full and final satisfaction, settlement, release, and discharge of such QVC Notes Claim, its Pro Rata share (taking into account Claims in Class B3) of the QVC Funded Debt Plan Consideration3 and (2) the QVC Debtors or the Reorganized QVC Debtors, as applicable, shall pay in full in Cash all QVC Notes Trustee Fees. | Approximately $2,146,000,000.00 | N/A |

| Class B5 | General Unsecured Claims against the QVC Debtors | Each Holder of an Allowed General Unsecured Claim against a QVC Debtor shall, in full and final satisfaction, settlement, release, and discharge of such General Unsecured Claim, as determined by the applicable Debtors: (i) payment in full in Cash on the later of (A) the Effective Date or (B) the date due in the ordinary course of business in accordance with the terms and conditions of the particular transaction giving rise to, or the agreement governing, such Allowed General Unsecured Claim against the QVC Debtors; (ii) Reinstated; or (iii) receive such other treatment acceptable to the Required Consenting QVC Noteholders and the Required Consenting RCF Lenders rendering such Allowed General Unsecured Claims Unimpaired. |

N/A | 100% |

| Class B6 | Intercompany Claims against the QVC Debtors | After giving effect to the Intercompany Settlement set forth in the Plan, each other Intercompany Claim against a QVC Debtor shall be, in full and final satisfaction, settlement, release, and discharge of such Intercompany Claim, as determined by the applicable Debtors with the consent of the Required Consenting QVC Noteholders and the Required Consenting RCF Lenders: (i) Reinstated; (ii) set off, settled, discharged, contributed, cancelled, converted to equity; (iii) released without any distribution on account of such Allowed Intercompany Claim; or (iv) otherwise addressed at the option of the Debtors, in each case as set forth in the Restructuring Steps Plan. |

N/A | N/A |

| 3 | QVC Funded Debt Plan Consideration is defined in the Plan and includes QVC Distributable Cash. Assuming an Effective Date of August 2026, the QVC Debtors estimate that QVC Distributable Cash will be approximately $882 million. The actual amount of QVC Distributable Cash may be higher or lower based on a variety of factors. None of the Debtors provide any assurances or warranty the amount of the QVC Distributable Cash as of the Effective Date. |

11

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class B7 | Intercompany Interests in the QVC Debtors | Each Allowed Intercompany Interest in a QVC Debtor shall be, in full and final satisfaction, settlement, release, and discharge of such Intercompany Interest, as determined by the applicable Debtors: (i) Reinstated; (ii) set off, settled, discharged, contributed, cancelled; (iii) released without any distribution on account of such Allowed Intercompany Interest; or (iv) otherwise addressed at the option of the Debtors, in each case as set forth in the Restructuring Steps Plan; provided, that, for the avoidance of doubt, any direct or indirect Interests held by any LINTA Debtor in any QVC Debtor shall be cancelled, released, discharged, and extinguished and will be of no further force or effect. |

N/A | N/A |

| Class B8 | Section 510(b) Claims against the QVC Debtors | On the Effective Date, each Section 510(b) Claim against a QVC Debtor shall be cancelled, released, discharged, and extinguished and will be of no further force or effect, and such Holders will not receive any distribution on account of such Section 510(b) Claim. | N/A4 | N/A |

| Class C1 | Other Secured Claims against the LINTA Debtors | Each Holder of an Allowed Other Secured Claim against a LINTA Debtor shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Secured Claim, as determined by the applicable Debtors, with the consent of the LINTA Noteholder Group: (i) payment in full in Cash; or (ii) such other treatment acceptable to the Required Consenting Stakeholders rendering its Allowed Other Secured Claim Unimpaired. |

N/A | 100% |

| Class C2 | Other Priority Claims against the LINTA Debtors | Each Holder of an Allowed Other Priority Claim against a LINTA Debtor shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Priority Claim, treatment in a manner consistent with section 1129(a) of the Bankruptcy Code, with the consent of the LINTA Noteholder Group. | N/A | 100% |

| Class C3 | LINTA Notes Claims against the LINTA Debtors | Each Holder of an Allowed LINTA Notes Claim shall receive, in full and final satisfaction, settlement, release, and discharge of such LINTA Notes Claim, its Pro Rata share (taking into account Claims in Class C5) of the LINTA Debtors’ Distributable Cash. | Approx. $1,485,000,000 |

Up to Approx. 7.5% |

| 4 | Notwithstanding anything to the contrary in the Plan, a Section 510(b) Claim, if any such Claim exists, may only become Allowed by Final Order of the Bankruptcy Court. |

12

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class C4 | General Unsecured Claims against the LINTA Debtors | Each Holder of an Allowed General Unsecured Claim against a LINTA Debtor shall receive, in full and final satisfaction, settlement, release, and discharge of such General Unsecured Claim, as determined by the applicable Debtors: (i) payment in full in Cash on the later of (A) the Effective Date or (B) the date due in the ordinary course of business in accordance with the terms and conditions of the particular transaction giving rise to, or the agreement governing, such Allowed General Unsecured Claim against the LINTA Debtors; or (ii) such other treatment acceptable to the Required Consenting Stakeholders rendering such Allowed General Unsecured Claims Unimpaired. |

N/A | 100% |

| Class C5 | Other Intercompany Claims against the LINTA Debtors | After giving effect to the Intercompany Settlement set forth in the Plan, each Other Intercompany Claim against a LINTA Debtor shall be, in full and final satisfaction, settlement, release, and discharge of such Other Intercompany Claim, as determined by the applicable Debtors, with the consent of the Required Consenting Stakeholders: (i) Reinstated; (ii) set off, settled, discharged, contributed, cancelled, converted to equity; (iii) released without any distribution on account of such Allowed Other Intercompany Claim; or (iv) otherwise addressed at the option of the Debtors, in each case as set forth in the Restructuring Steps Plan; provided that in no event shall Class C5 receive any Cash from the LINTA Debtors. |

N/A | N/A |

| Class C6 | Intercompany Interests in the LINTA Debtors | Each Allowed Intercompany Interest in a LINTA Debtor shall be, in full and final satisfaction, settlement, release, and discharge of such Intercompany Interests, as determined by the applicable Debtors: (i) Reinstated; (ii) set off, settled, discharged, contributed, cancelled; (iii) released without any distribution on account of such Allowed Intercompany Interest; or (iv) otherwise addressed at the option of the Debtors, in each case as set forth in the Restructuring Steps Plan. |

N/A | N/A |

| Class C7 | Section 510(b) Claims against the LINTA Debtors | On the Effective Date, each Section 510(b) Claim against a LINTA Debtor shall be cancelled, released, discharged, and extinguished and will be of no further force or effect, and such Holders will not receive any distribution on account of such Section 510(b) Claim. | N/A5 | N/A |

| 5 | Notwithstanding anything to the contrary in the Plan, a Section 510(b) Claim, if any such Claim exists, may only become Allowed by Final Order of the Bankruptcy Court. |

13

| Summary of Projected Distributions | ||||

| Class | Claim/Interest | Treatment of Claim / Interest | Projected Allowed Amount of Claims |

Estimated Recovery (%) |

| Class D1 | Other Secured Claims against the CBI Debtors | Each Holder of an Allowed Other Secured Claim against the CBI Debtors shall receive, in full and final satisfaction, settlement, release, and discharge of such Other Secured Claim, as determined by the applicable Debtors: (i) payment in full in Cash; (ii) the collateral securing its Allowed Other Secured Claim; (iii) Reinstatement of its Allowed Other Secured Claim; or (iv) such other treatment acceptable to the Required Consenting QVC Noteholders and the Required Consenting RCF Lenders rendering its Allowed Other Secured Claim Unimpaired. |

N/A | 100% |