Project Kona Updated valuation materials December 15, 2025 DRAFT All numbers

and references herein are highly preliminary and subject to material refinement Exhibit (c)(viii)

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

CHANGE Disclaimer 1. Section name This presentation was prepared by Rothschild & Co US Inc. (“Rothschild & Co”) on a confidential basis for the benefit and internal use of the Special Committee (the “Special Committee”) of the Board

of Directors of KORE Group Holdings, Inc. (the “Company” or “Kona”) in the context of the Special Committee’s consideration of the matters described herein. In creating this presentation, Rothschild & Co has relied upon information that is

publicly available or which was provided to Rothschild & Co by or on behalf of the Company’s management, including, without limitation, management operating and financial forecasts or projections. Such information involves numerous

significant assumptions and subjective determinations that may or may not be correct. Rothschild & Co has not assumed any responsibility for independent verification of any of such information contained herein, including, but not limited

to, any forecasts or projections set forth herein, and Rothschild & Co has relied on such information being complete and accurate in all material respects. Accordingly, no representation or warranty, express or implied, can be made or is

made by Rothschild & Co as to the accuracy or completeness of any such information or the achievability of any such forecasts or projections. Except where otherwise indicated, this presentation speaks as of the date hereof and is

necessarily based upon the information available to Rothschild & Co and financial, stock market and other conditions and circumstances existing and disclosed to Rothschild & Co as of the date hereof, all of which are subject to change.

Rothschild & Co does not have any obligation to update, bring-down, review or reaffirm this presentation. Under no circumstances should the delivery of this presentation imply that any information or analyses included in this presentation

would be the same if made as of any other date. Nothing contained in this presentation is, or shall be relied upon as, a promise or representation as to the past, present or future. Nothing contained herein shall be deemed to be a

recommendation from Rothschild & Co to any party, including without limitation, any security holder of the Company, to enter into any transaction or to take any course of action. By accepting these materials, the Special Committee

acknowledges that Rothschild & Co is not in the business of providing (and the Special Committee is not relying on Rothschild & Co for) legal, tax or accounting advice, and the Special Committee should receive (and rely on) separate and

qualified legal, tax and accounting advice. These materials do not constitute an offer or solicitation to sell or purchase any securities. Rothschild & Co is not acting in any capacity as a fiduciary or agent of the Special Committee, the

Board of Directors of the Company, the Company or the Company’s security holders. In the ordinary course of their asset management, merchant banking and other business activities, affiliates of Rothschild & Co may at any time hold long or

short positions, and may trade or otherwise effect transactions, for their own accounts or the accounts of their clients in equity, debt or other securities (or related derivative securities) or financial instruments of the Company or any of

its affiliates or any other company that may be involved in any transaction. This presentation is confidential and was not prepared with a view to public disclosure or filing thereof under state or federal securities laws or otherwise. This

presentation may not be copied by, or disclosed or made available to, any person without the prior written consent of Rothschild & Co. This presentation was not prepared for use by readers not as familiar with the business and affairs of

the Company as the Special Committee, and accordingly, Rothschild & Co does not take any responsibility for the accuracy or completeness of any material if used by persons other than the Special Committee. Rothschild & Co shall not

have any liability, whether direct or indirect, in contract or tort or otherwise, to any person in connection with this presentation. 2

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

CHANGE Contents Situation overview Preliminary valuation perspectives Supplemental analyses Appendix 4 8 15 21

1 Situation overview

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

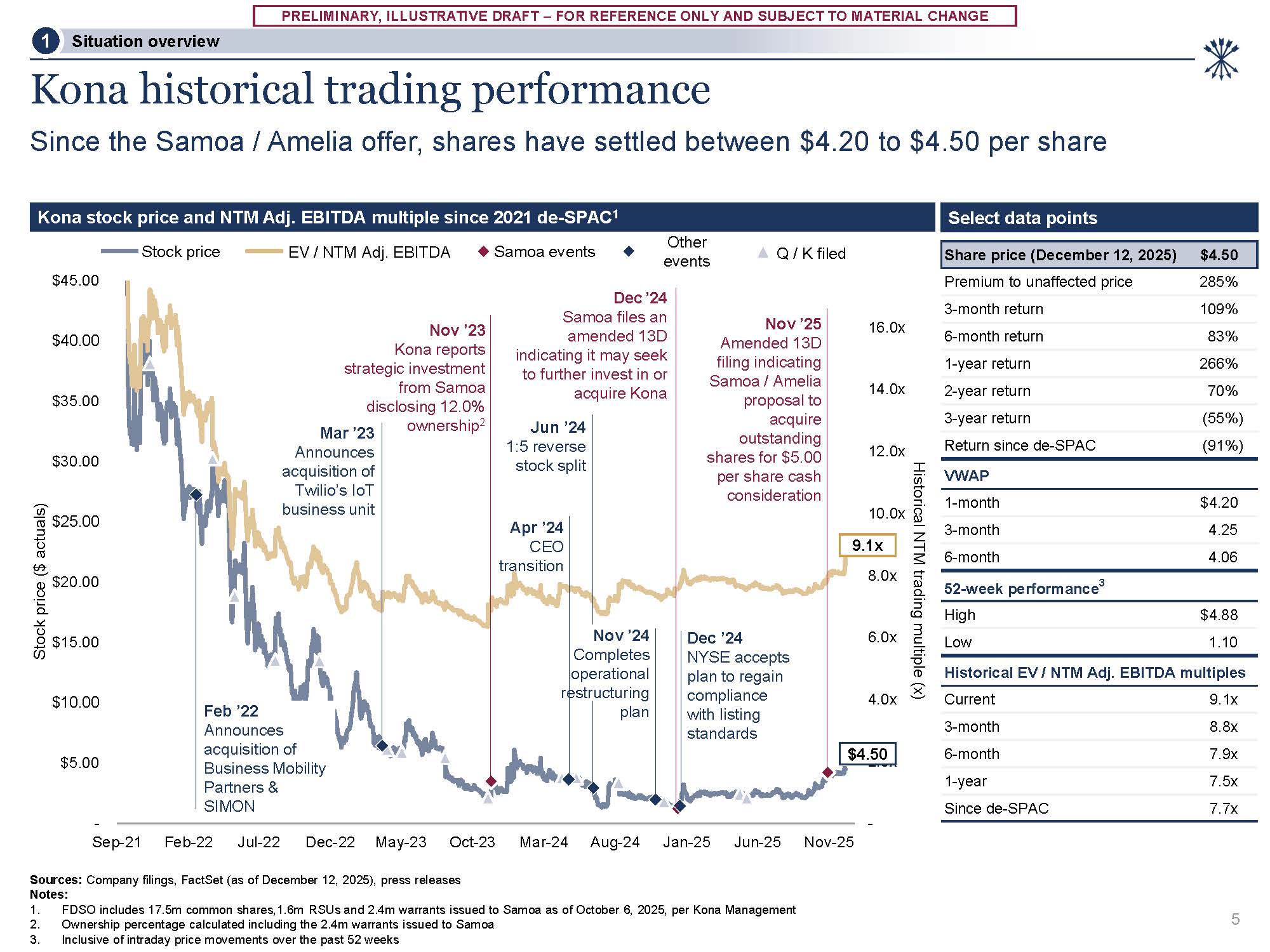

CHANGE Share price (December 12, 2025) $4.50 Premium to unaffected price 285% 3-month return 109% 6-month return 83% 1-year return 266% 2-year return 70% 3-year return (55%) Return since

de-SPAC (91%) VWAP 1-month $4.20 3-month 4.25 6-month 4.06 52-week performance3 High $4.88 Low 1.10 Historical EV / NTM Adj. EBITDA multiples Current 9.1x 3-month 8.8x 6-month 7.9x 1-year 7.5x Since de-SPAC

7.7x - 2.0x 4.0x 6.0x 8.0x 10.0x 12.0x 14.0x 16.0x - $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 Sep-21 Feb-22 Jul-22 Dec-22 May-23 Oct-23 Mar-24 Aug-24 Jan-25 Jun-25 Nov-25 Dec ’24 Samoa files an

amended 13D indicating it may seek to further invest in or acquire Kona Mar ’23 Announces acquisition of Twilio’s IoT business unit Jun ’24 1:5 reverse stock split Nov ’24 Completes operational restructuring plan Nov ’23 Kona reports

strategic investment from Samoa disclosing 12.0% ownership2 Apr ’24 CEO transition Feb ’22 Announces acquisition of Business Mobility Partners & SIMON Kona historical trading performance Since the Samoa / Amelia offer, shares have

settled between $4.20 to $4.50 per share Sources: Company filings, FactSet (as of December 12, 2025), press releases Notes: FDSO includes 17.5m common shares,1.6m RSUs and 2.4m warrants issued to Samoa as of October 6, 2025, per Kona

Management Ownership percentage calculated including the 2.4m warrants issued to Samoa Inclusive of intraday price movements over the past 52 weeks Stock price ($ actuals) Historical NTM trading multiple (x) Select data points Q / K

filed Kona stock price and NTM Adj. EBITDA multiple since 2021 de-SPAC1 Stock price EV / NTM Adj. EBITDA Samoa events Other events Situation overview 1 $4.50 9.1x Dec ’24 NYSE accepts plan to regain compliance with

listing standards Nov ’25 Amended 13D filing indicating Samoa / Amelia proposal to acquire outstanding shares for $5.00 per share cash consideration 5

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

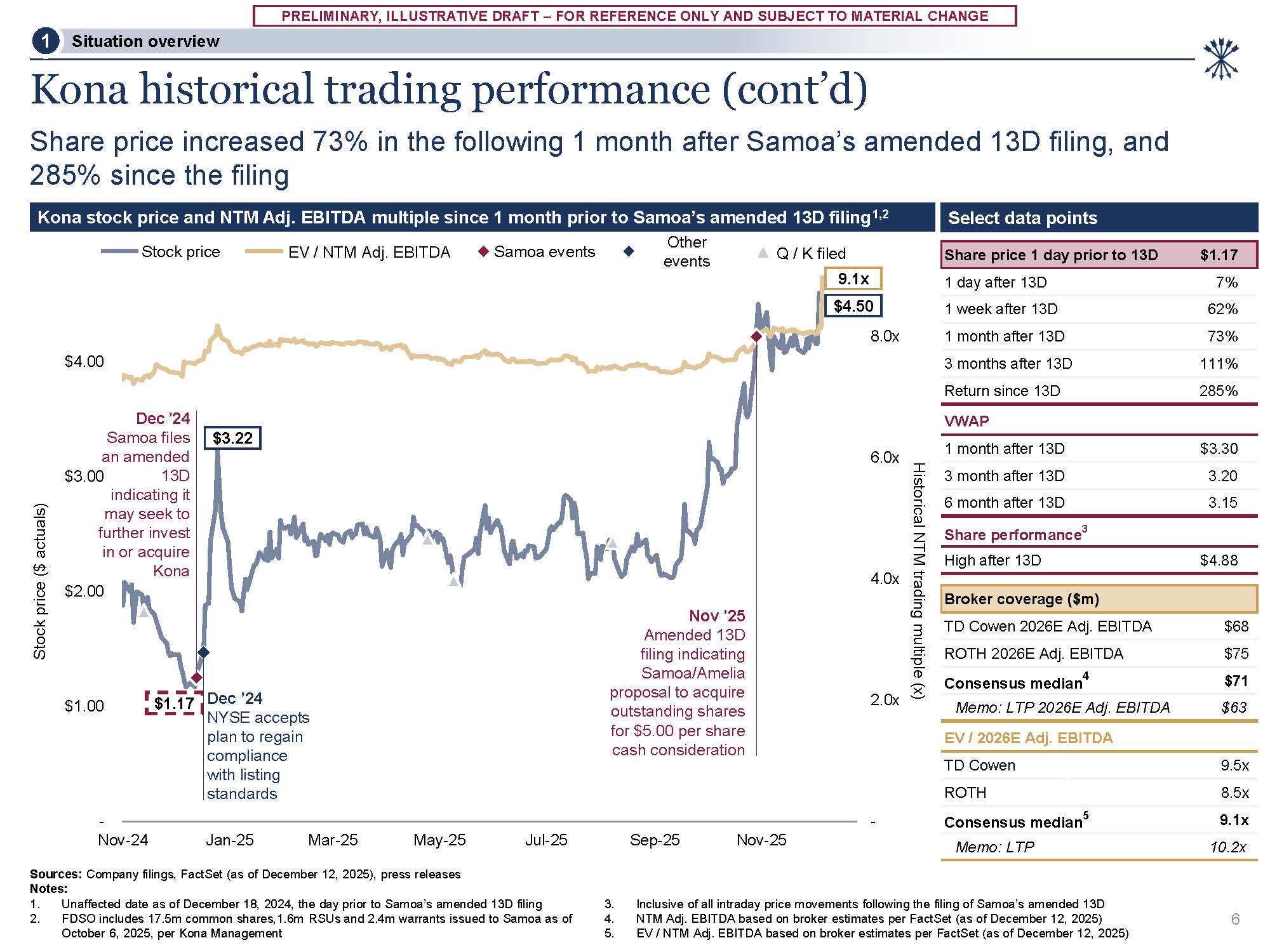

CHANGE Consensus median4 $71 Memo: LTP 2026E Adj. EBITDA $63 EV / 2026E Adj. EBITDA TD Cowen 9.5x ROTH 8.5x Consensus median5 9.1x Memo: LTP 10.2x Share price 1 day prior to 13D $1.17 1 day after 13D 7% 1 week after 13D 62% 1

month after 13D 73% 3 months after 13D 111% Return since 13D 285% VWAP 1 month after 13D $3.30 3 month after 13D 3.20 6 month after 13D 3.15 Share performance3 High after 13D $4.88 Broker coverage ($m) TD Cowen 2026E Adj. EBITDA

$68 ROTH 2026E Adj. EBITDA $75 - 2.0x 4.0x 6.0x 8.0x - Nov-24 Jan-25 Mar-25 May-25 Sources: Company filings, FactSet (as of December 12, 2025), press releases Notes: $1.00 $2.00 $3.00 $4.00 Jul-25 Sep-25 Nov-25 Kona historical

trading performance (cont’d) Share price increased 73% in the following 1 month after Samoa’s amended 13D filing, and 285% since the filing 9.1x $1.17 Kona stock price and NTM Adj. EBITDA multiple since 1 month prior to Samoa’s amended 13D

filing1,2 Select data points Situation overview 1 $4.50 $3.22 Dec ’24 Samoa files an amended 13D indicating it may seek to further invest in or acquire Kona Historical NTM trading multiple (x) Dec ’24 NYSE accepts plan to regain

compliance with listing standards Unaffected date as of December 18, 2024, the day prior to Samoa’s amended 13D filing FDSO includes 17.5m common shares,1.6m RSUs and 2.4m warrants issued to Samoa as of October 6, 2025, per Kona

Management Inclusive of all intraday price movements following the filing of Samoa’s amended 13D NTM Adj. EBITDA based on broker estimates per FactSet (as of December 12, 2025) EV / NTM Adj. EBITDA based on broker estimates per FactSet (as

of December 12, 2025) Nov ’25 Amended 13D filing indicating Samoa/Amelia proposal to acquire outstanding shares for $5.00 per share cash consideration 6 Q / K filed Stock price EV / NTM Adj. EBITDA Samoa events Other events Stock price ($

actuals)

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

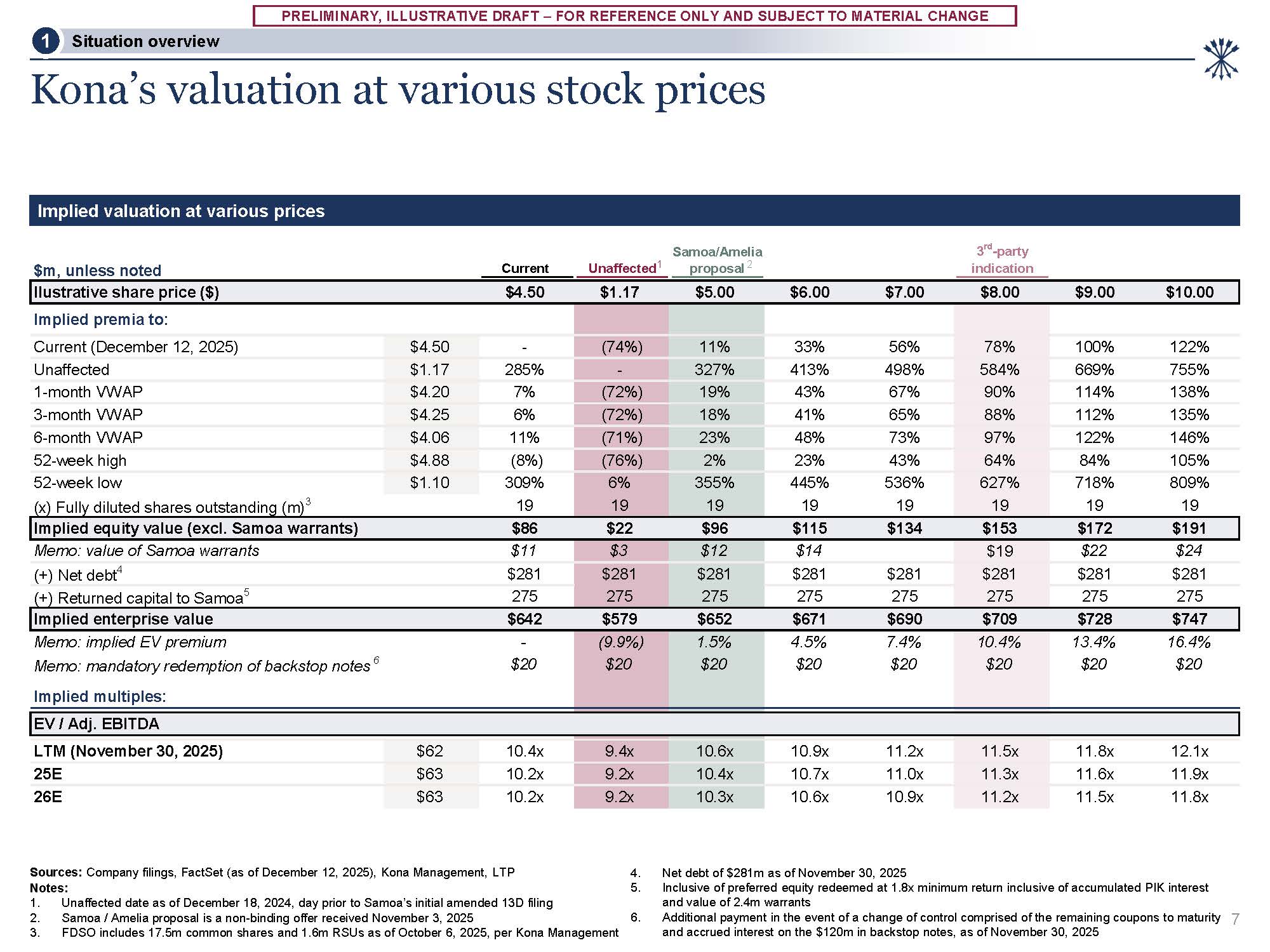

CHANGE Kona’s valuation at various stock prices Sources: Company filings, FactSet (as of December 12, 2025), Kona Management, LTP Notes: Unaffected date as of December 18, 2024, day prior to Samoa’s initial amended 13D filing Samoa /

Amelia proposal is a non-binding offer received November 3, 2025 FDSO includes 17.5m common shares and 1.6m RSUs as of October 6, 2025, per Kona Management Net debt of $281m as of November 30, 2025 Inclusive of preferred equity redeemed at

1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants Additional payment in the event of a change of control comprised of the remaining coupons to maturity 7 and accrued interest on the $120m in backstop notes,

as of November 30, 2025 Implied valuation at various prices Situation overview 1 3rd-party indication $m, unless noted Ilustrative share price ($) $4.50 $1.17 $5.00 $6.00 $7.00 $8.00 $9.00 $10.00 Implied premia to: Current

(December 12, 2025) $4.50 - (74%) 11% 33% 56% 78% 100% 122% Unaffected $1.17 285% - 327% 413% 498% 584% 669% 755% 1-month VWAP $4.20 7% (72%) 19% 43% 67% 90% 114% 138% 3-month

VWAP $4.25 6% (72%) 18% 41% 65% 88% 112% 135% 6-month VWAP $4.06 11% (71%) 23% 48% 73% 97% 122% 146% 52-week high $4.88 (8%) (76%) 2% 23% 43% 64% 84% 105% 52-week

low $1.10 309% 6% 355% 445% 536% 627% 718% 809% (x) Fully diluted shares outstanding (m)3 19 19 19 19 19 19 19 19 Implied equity value (excl. Samoa warrants) $86 $22 $96 $115 $134 $153 $172 $191 Memo: value of Samoa

warrants $11 $3 $12 $14 $19 $22 $24 (+) Net debt4 $281 $281 $281 $281 $281 $281 $281 $281 (+) Returned capital to Samoa5 275 275 275 275 275 275 275 275 Implied enterprise

value $642 $579 $652 $671 $690 $709 $728 $747 Memo: implied EV premium Memo: mandatory redemption of backstop notes 6 - $20 (9.9%) $20 1.5% $20 4.5% $20 7.4% $20 10.4% $20 13.4% $20 16.4% $20 Implied multiples: EV /

Adj. EBITDA LTM (November 30,

2025) $62 10.4x 9.4x 10.6x 10.9x 11.2x 11.5x 11.8x 12.1x 25E $63 10.2x 9.2x 10.4x 10.7x 11.0x 11.3x 11.6x 11.9x 26E $63 10.2x 9.2x 10.3x 10.6x 10.9x 11.2x 11.5x 11.8x Current Samoa/Amelia Unaffected1 proposal 2

2 Preliminary valuation perspectives

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

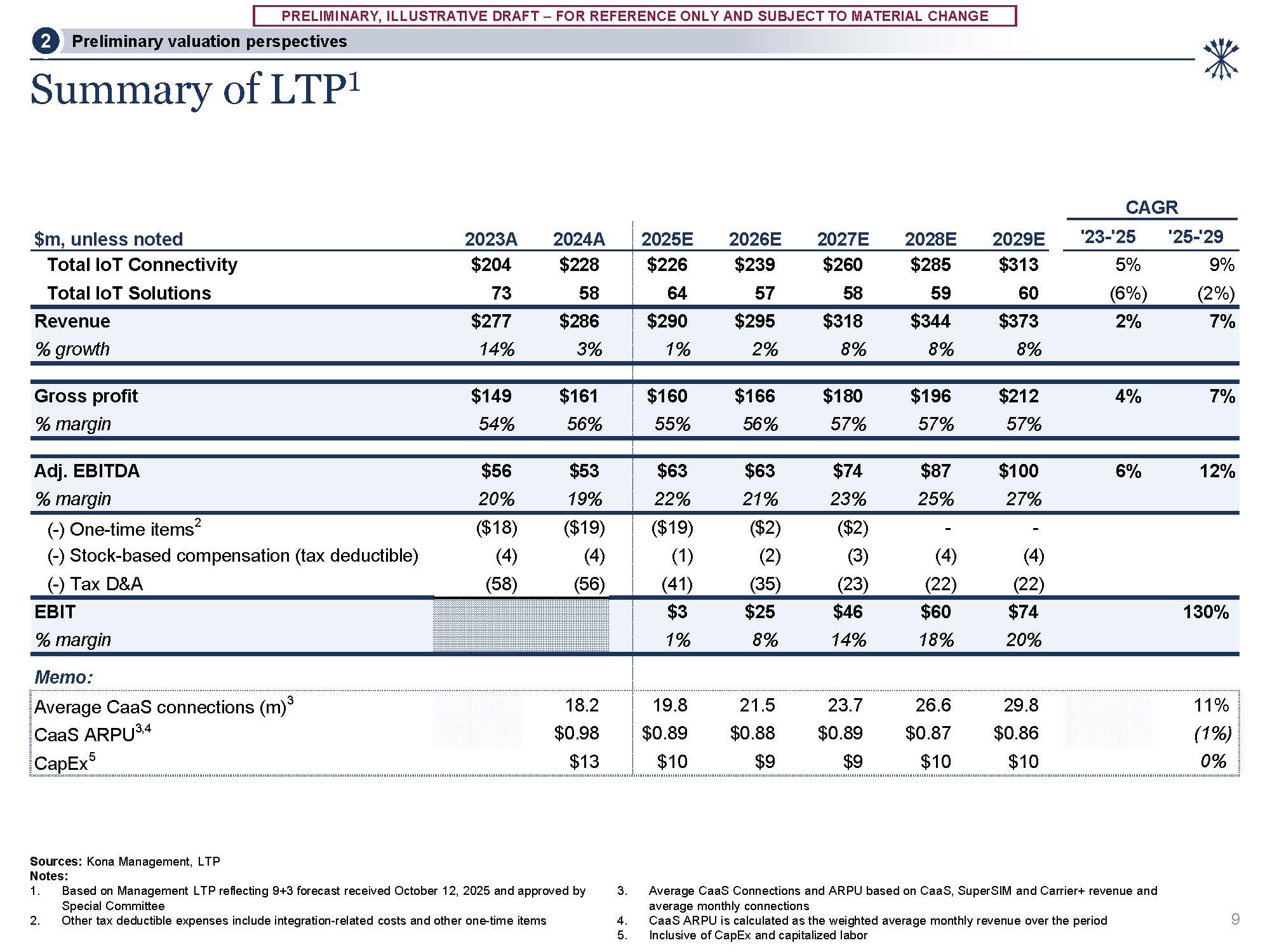

CHANGE Summary of LTP1 Sources: Kona Management, LTP Notes: Based on Management LTP reflecting 9+3 forecast received October 12, 2025 and approved by Special Committee Other tax deductible expenses include integration-related costs and

other one-time items Average CaaS Connections and ARPU based on CaaS, SuperSIM and Carrier+ revenue and average monthly connections CaaS ARPU is calculated as the weighted average monthly revenue over the period Inclusive of CapEx and

capitalized labor 9 Preliminary valuation perspectives 2 $m, unless noted 2023A 2024A 2025E 2026E 2027E 2028E 2029E '23-'25 '25-'29 Total IoT Connectivity $204 $228 Total IoT Solutions 73 58 $226 $239 $260 $285 $313 64 57 58 59 60 5%

9% (6%) (2%) Revenue $277 $286 % growth 14% 3% $290 $295 $318 $344 $373 2% 7% 1% 2% 8% 8% 8% Gross profit $149 $161 % margin 54% 56% $160 $166 $180 $196 $212 4% 7% 55% 56% 57% 57% 57% Adj. EBITDA $56 $53 % margin 20% 19% $63 $63 $74

$87 $100 6% 12% 22% 21% 23% 25% 27% (-) One-time items2 ($18) ($19) (-) Stock-based compensation (tax deductible) (4) (4) (-) Tax D&A (58) (56) ($19) ($2) ($2) - - (1) (2) (3) (4) (4) (41) (35) (23) (22) (22) EBIT % margin $3 $25

$46 $60 $74 130% 1% 8% 14% 18% 20% Memo: Average CaaS connections (m)3 18.2 CaaS ARPU3,4 $0.98 CapEx5 $13 19.8 21.5 23.7 26.6 29.8 11% $0.89 $0.88 $0.89 $0.87 $0.86 (1%) $10 $9 $9 $10 $10 0% CAGR

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

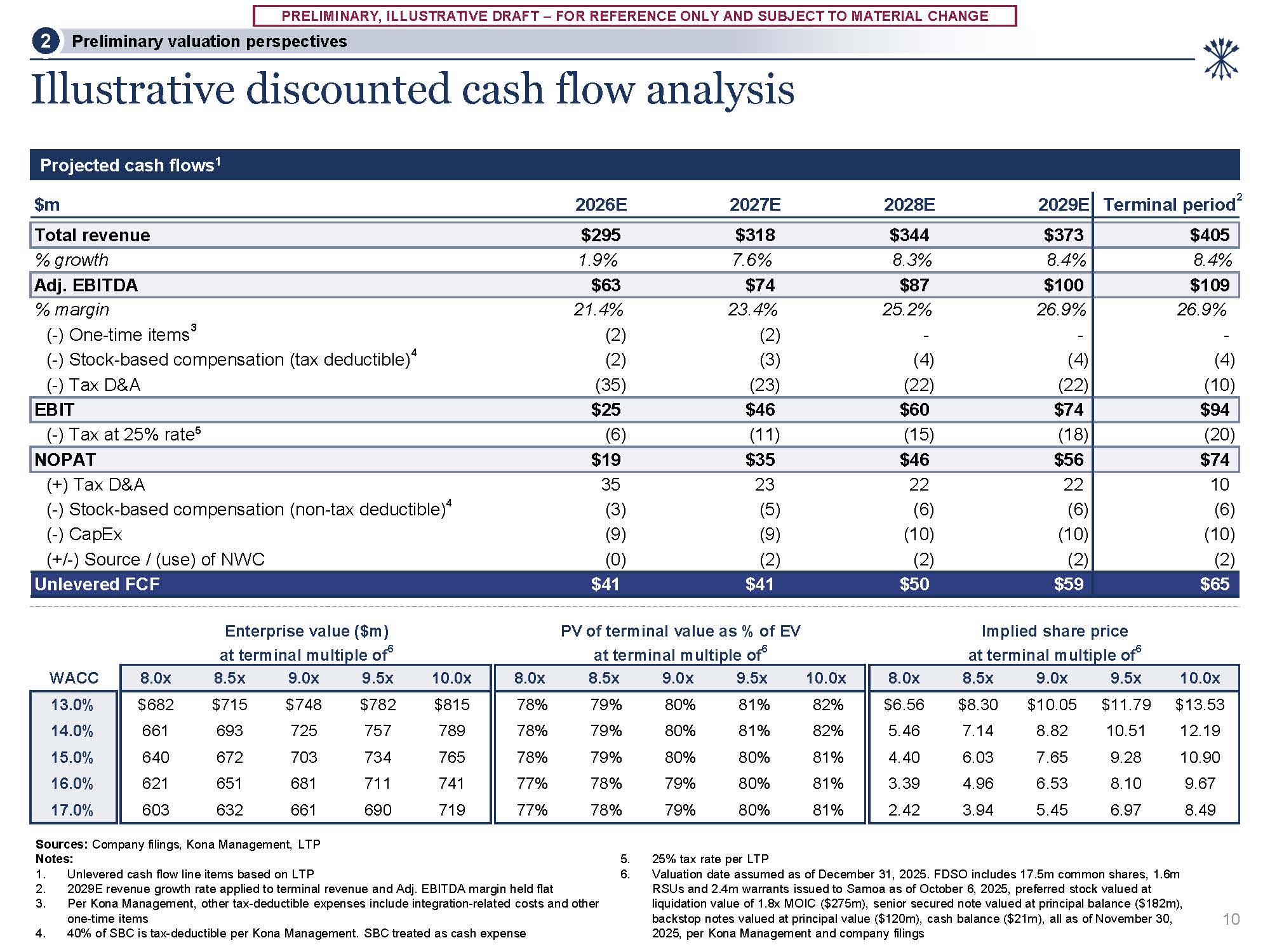

CHANGE Illustrative discounted cash flow analysis Projected cash flows1 Sources: Company filings, Kona Management, LTP Notes: Unlevered cash flow line items based on LTP 2029E revenue growth rate applied to terminal revenue and Adj.

EBITDA margin held flat Per Kona Management, other tax-deductible expenses include integration-related costs and other one-time items 40% of SBC is tax-deductible per Kona Management. SBC treated as cash expense 25% tax rate per

LTP Valuation date assumed as of December 31, 2025. FDSO includes 17.5m common shares, 1.6m RSUs and 2.4m warrants issued to Samoa as of October 6, 2025, preferred stock valued at liquidation value of 1.8x MOIC ($275m), senior secured note

valued at principal balance ($182m), backstop notes valued at principal value ($120m), cash balance ($21m), all as of November 30, 2025, per Kona Management and company filings Enterprise value ($m) PV of terminal value as % of EV Implied

share price at terminal multiple of6 at terminal multiple of6 at terminal multiple of6 2 $m 2026E 2027E 2028E 2029E Terminal period Total revenue $295 $318 $344 $373 $405 % growth 1.9% 7.6% 8.3% 8.4% 8.4% Adj.

EBITDA $63 $74 $87 $100 $109 % margin 21.4% 23.4% 25.2% 26.9% 26.9% (-) One-time items3 (2) (2) - - - (-) Stock-based compensation (tax deductible)4 (2) (3) (4) (4) (4) (-) Tax

D&A (35) (23) (22) (22) (10) EBIT $25 $46 $60 $74 $94 (-) Tax at 25% rate5 (6) (11) (15) (18) (20) NOPAT $19 $35 $46 $56 $74 (+) Tax D&A 35 23 22 22 10 (-) Stock-based compensation (non-tax

deductible)4 (3) (5) (6) (6) (6) (-) CapEx (9) (9) (10) (10) (10) (+/-) Source / (use) of NWC (0) (2) (2) (2) (2) Unlevered FCF $41 $41 $50 $59 $65 Preliminary valuation

perspectives 2 10 WACC 8.0x 8.5x 9.0x 9.5x 10.0x 8.0x 8.5x 9.0x 9.5x 10.0x 8.0x 8.5x 9.0x 9.5x 10.0x 13.0% $682 $715 $748 $782 $815 78% 79% 80% 81% 82% $6.56 $8.30 $10.05 $11.79 $13.53 14.0% 661 693 725 757 789 78% 79% 80% 81% 82% 5.46 7.14 8.82 10.51 12.19 15.0% 640 672 703 734 765 78% 79% 80% 80% 81% 4.40 6.03 7.65 9.28 10.90 16.0% 621 651 681 711 741 77% 78% 79% 80% 81% 3.39 4.96 6.53 8.10 9.67 17.0% 603 632 661 690 719 77% 78% 79% 80% 81% 2.42 3.94 5.45 6.97 8.49

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

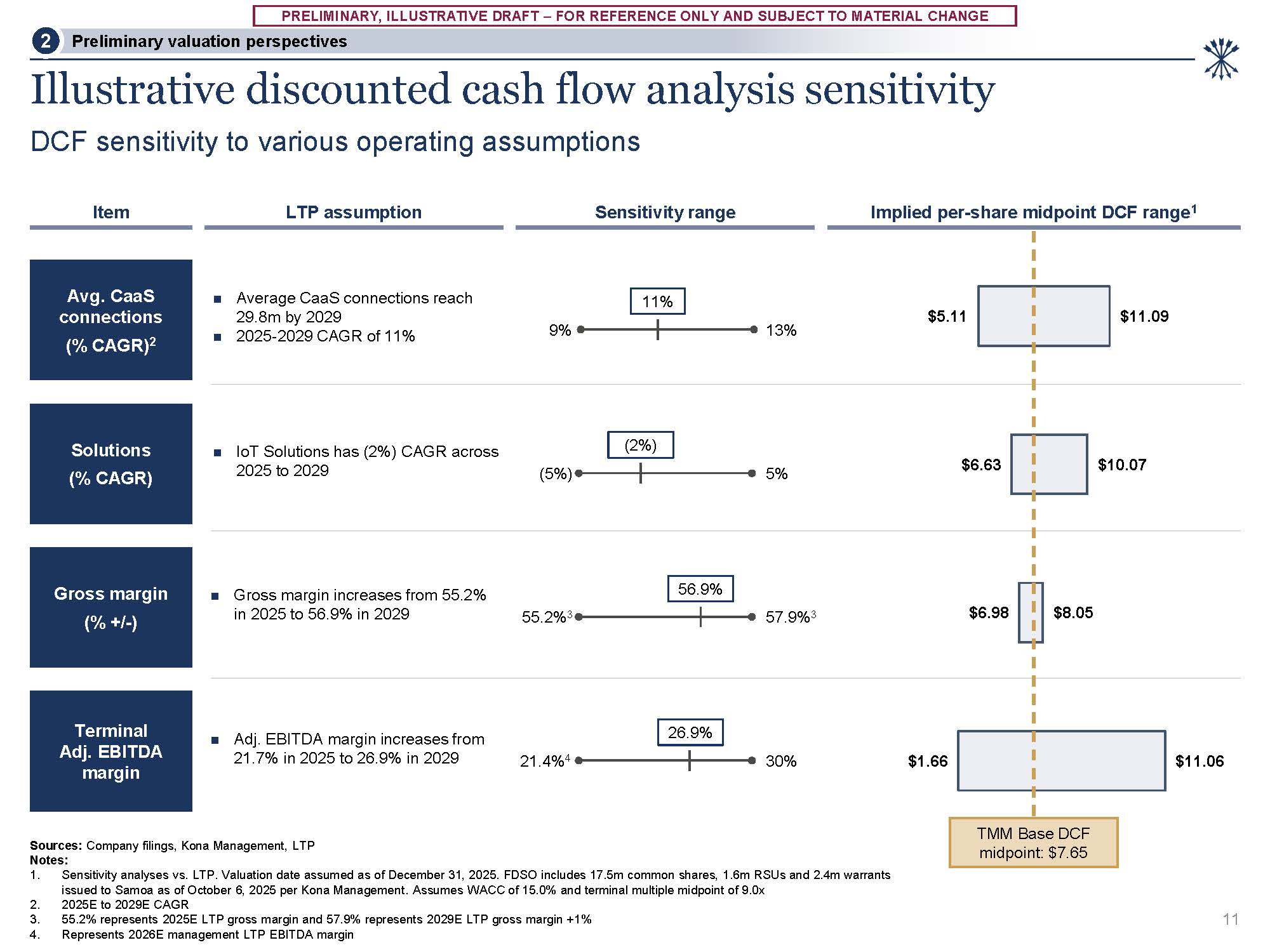

CHANGE $5.11 $6.63 $6.98 $1.66 $11.09 $10.07 $8.05 $11.06 Illustrative discounted cash flow analysis sensitivity DCF sensitivity to various operating assumptions Implied per-share midpoint DCF range1 LTP assumption Item Sources:

Company filings, Kona Management, LTP Notes: Sensitivity analyses vs. LTP. Valuation date assumed as of December 31, 2025. FDSO includes 17.5m common shares, 1.6m RSUs and 2.4m warrants issued to Samoa as of October 6, 2025 per Kona

Management. Assumes WACC of 15.0% and terminal multiple midpoint of 9.0x 2025E to 2029E CAGR 55.2% represents 2025E LTP gross margin and 57.9% represents 2029E LTP gross margin +1% Represents 2026E management LTP EBITDA margin Sensitivity

range Avg. CaaS connections (% CAGR)2 Average CaaS connections reach 29.8m by 2029 2025-2029 CAGR of 11% 9% 13% 11% Solutions (% CAGR) IoT Solutions has (2%) CAGR across 2025 to 2029 (5%) 5% (2%) Gross margin (% +/-) Gross margin

increases from 55.2% in 2025 to 56.9% in 2029 55.2%3 57.9%3 56.9% Adj. EBITDA margin increases from 21.7% in 2025 to 26.9% in 2029 Terminal Adj. EBITDA margin 21.4%4 30% 26.9% TMM Base DCF midpoint: $7.65 Preliminary valuation

perspectives 2 11

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

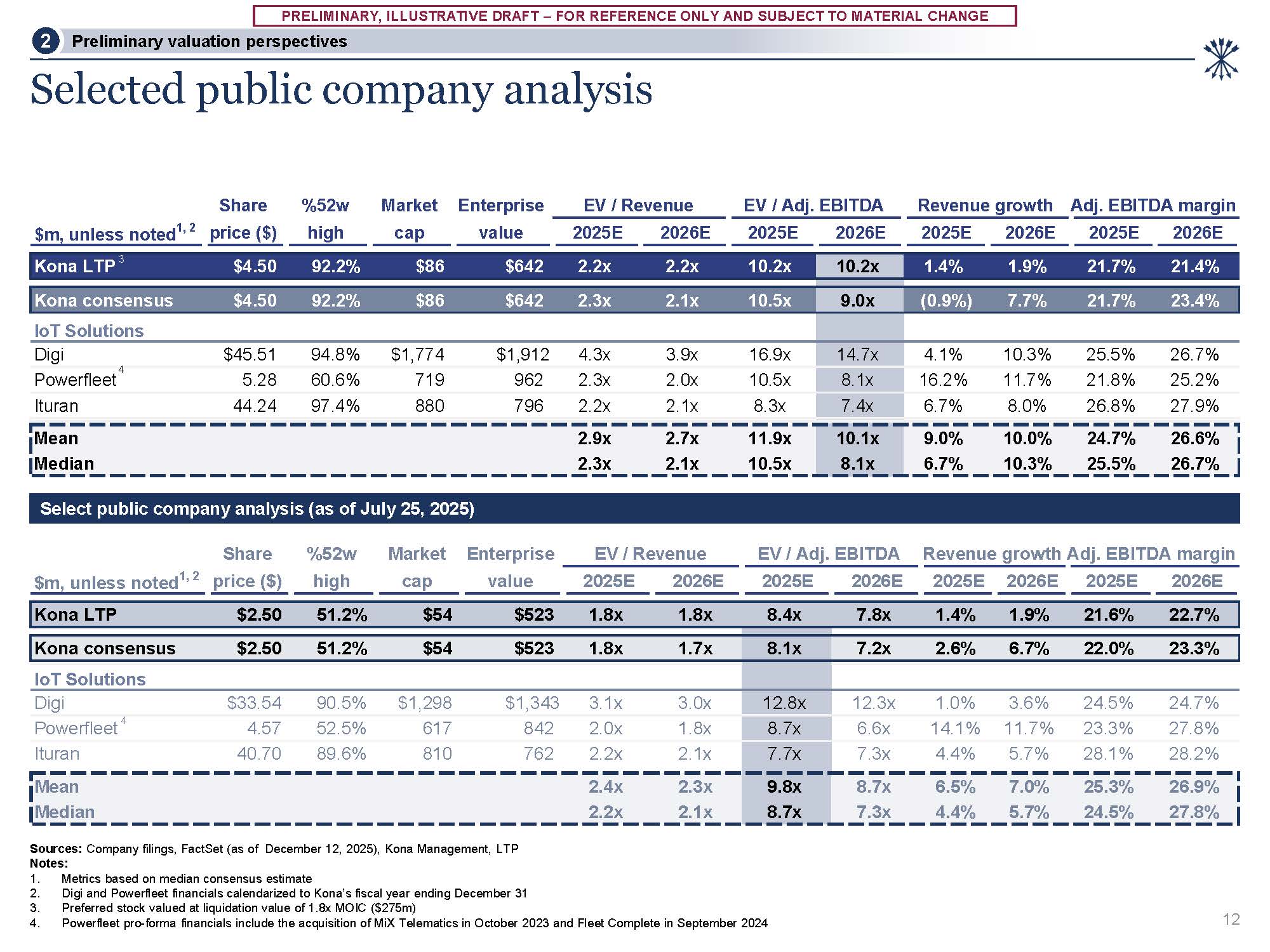

CHANGE Kona LTP $2.50 51.2% $54 $523 1.8x 1.8x 8.4x 7.8x 1.4% 1.9% 21.6% 22.7% Kona consensus $2.50 51.2% $54 $523 1.8x 1.7x 8.1x 7.2x 2.6% 6.7% 22.0% 23.3% IoT

Solutions Digi $33.54 90.5% $1,298 $1,343 3.1x 3.0x 12.8x 12.3x 1.0% 3.6% 24.5% 24.7% Powerfleet

4 4.57 52.5% 617 842 2.0x 1.8x 8.7x 6.6x 14.1% 11.7% 23.3% 27.8% Ituran 40.70 89.6% 810 762 2.2x 2.1x 7.7x 7.3x 4.4% 5.7% 28.1% 28.2% Mean 2.4x 2.3x 9.8x 8.7x 6.5% 7.0% 25.3% 26.9% Median 2.2x 2.1x 8.7x 7.3x 4.4% 5.7% 24.5% 27.8% $m,

unless noted1, 2 Share price ($) %52w high Market cap Enterprise EV / Revenue EV / Adj. EBITDA Revenue growth Adj. EBITDA margin value 2025E 2026E 2025E 2026E 2025E 2026E 2025E 2026E Kona LTP

3 $4.50 92.2% $86 $642 2.2x 2.2x 10.2x 10.2x 1.4% 1.9% 21.7% 21.4% Kona consensus $4.50 92.2% $86 $642 2.3x 2.1x 10.5x 9.0x (0.9%) 7.7% 21.7% 23.4% IoT

Solutions Digi $45.51 94.8% $1,774 $1,912 4.3x 3.9x 16.9x 14.7x 4.1% 10.3% 25.5% 26.7% Powerfleet 4 5.28 60.6% 719 962 2.3x 2.0x 10.5x 8.1x 16.2% 11.7% 21.8% 25.2% Ituran 44.24 97.4% 880 796 2.2x 2.1x 8.3x 7.4x 6.7% 8.0% 26.8% 27.9% Mean 2.9x 2.7x 11.9x 10.1x 9.0% 10.0% 24.7% 26.6% Median 2.3x 2.1x 10.5x 8.1x 6.7% 10.3% 25.5% 26.7% $m,

unless noted1, 2 Share price ($) %52w high Market cap Enterprise value EV / Revenue 2025E 2026E EV / Adj. EBITDA 2025E 2026E Revenue growth 2025E 2026E Adj. EBITDA margin 2025E 2026E Select public company analysis (as of July 25,

2025) Selected public company analysis Sources: Company filings, FactSet (as of December 12, 2025), Kona Management, LTP Notes: Metrics based on median consensus estimate Digi and Powerfleet financials calendarized to Kona’s fiscal year

ending December 31 Preferred stock valued at liquidation value of 1.8x MOIC ($275m) Powerfleet pro-forma financials include the acquisition of MiX Telematics in October 2023 and Fleet Complete in September 2024 Preliminary valuation

perspectives 2 12

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

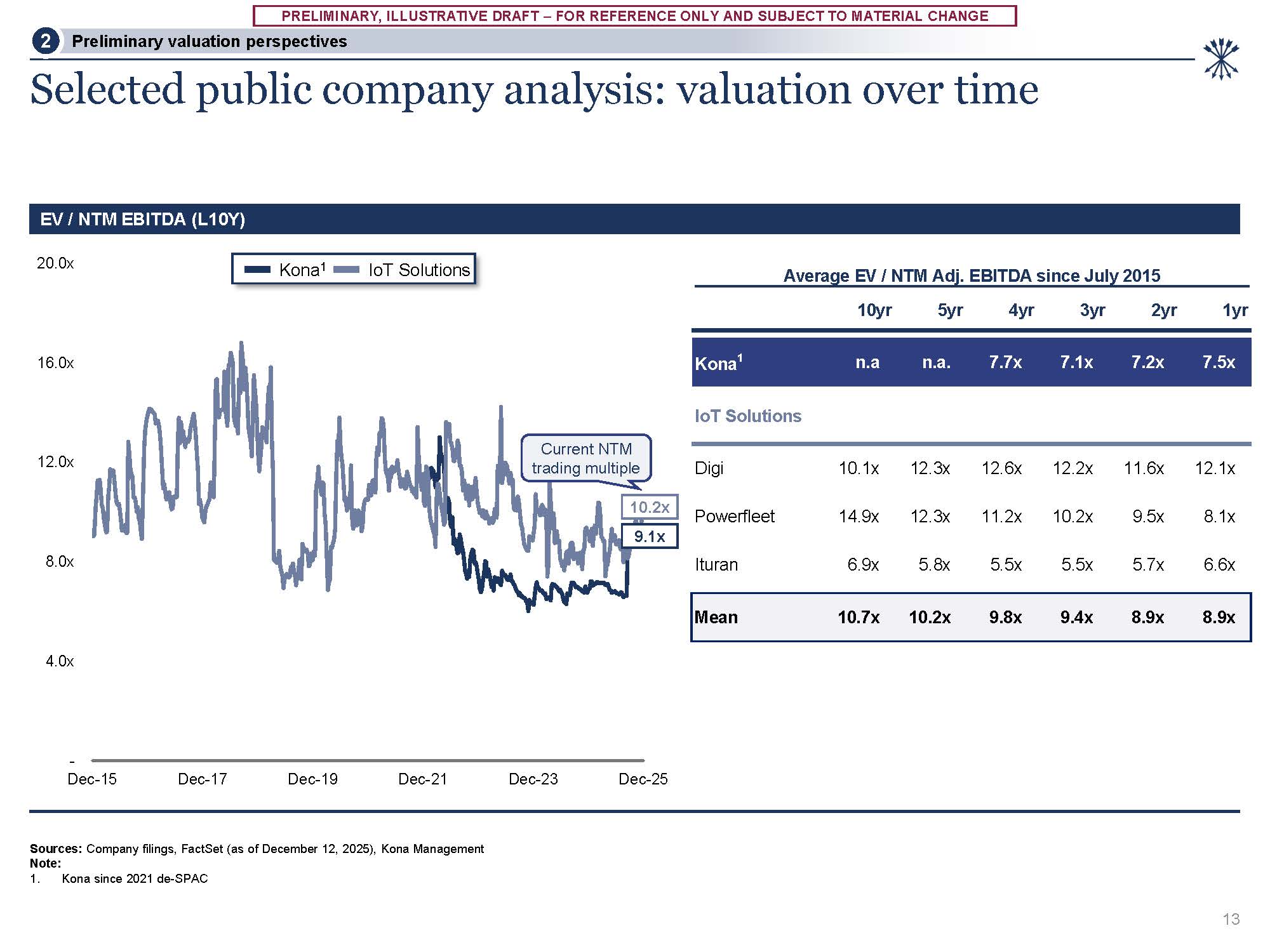

CHANGE - 4.0x 8.0x 12.0x 16.0x 20.0x Dec-15 Dec-17 Dec-19 Dec-21 Dec-23 Dec-25 10yr 5yr 4yr 3yr 2yr 1yr Kona1 n.a n.a. 7.7x 7.1x 7.2x 7.5x IoT

Solutions Digi 10.1x 12.3x 12.6x 12.2x 11.6x 12.1x Powerfleet 14.9x 12.3x 11.2x 10.2x 9.5x 8.1x Ituran 6.9x 5.8x 5.5x 5.5x 5.7x 6.6x Mean 10.7x 10.2x 9.8x 9.4x 8.9x 8.9x Average EV / NTM Adj. EBITDA since July 2015

Selected public company analysis: valuation over time EV / NTM EBITDA (L10Y) Sources: Company filings, FactSet (as of December 12, 2025), Kona Management Note: 1. Kona since 2021 de-SPAC Kona1 IoT Solutions 10.2x 9.1x Preliminary

valuation perspectives 2 13 Current NTM trading multiple

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

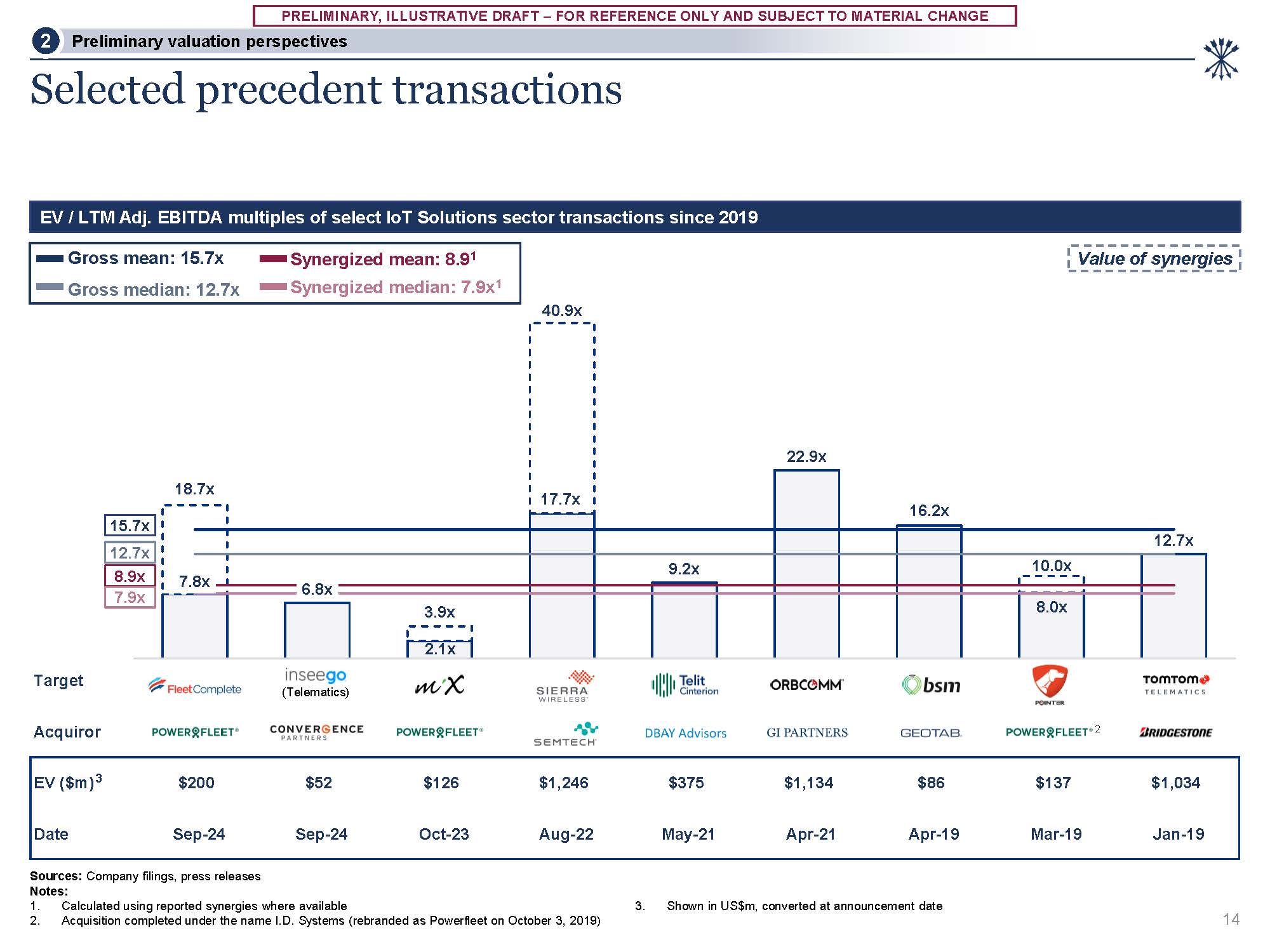

CHANGE Target Acquiror EV

($m)3 $200 $52 $126 $1,246 $375 $1,134 $86 $137 $1,034 Date Sep-24 Sep-24 Oct-23 Aug-22 May-21 Apr-21 Apr-19 Mar-19 Jan-19 7.8x 2.1x 17.7x 8.0x 18.7x 6.8x 3.9x 40.9x 9.2x 22.9x 16.2x 10.0x 12.7x Selected

precedent transactions Sources: Company filings, press releases Notes: Calculated using reported synergies where available Acquisition completed under the name I.D. Systems (rebranded as Powerfleet on October 3, 2019) 3. Shown in US$m,

converted at announcement date EV / LTM Adj. EBITDA multiples of select IoT Solutions sector transactions since 2019 (Telematics) 2 Value of synergies 15.7x 12.7x 8.9x 7.9x Gross mean: 15.7x Gross median: 12.7x Synergized mean: 8.91

Synergized median: 7.9x1 Preliminary valuation perspectives 2 14

3 Supplemental analyses

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

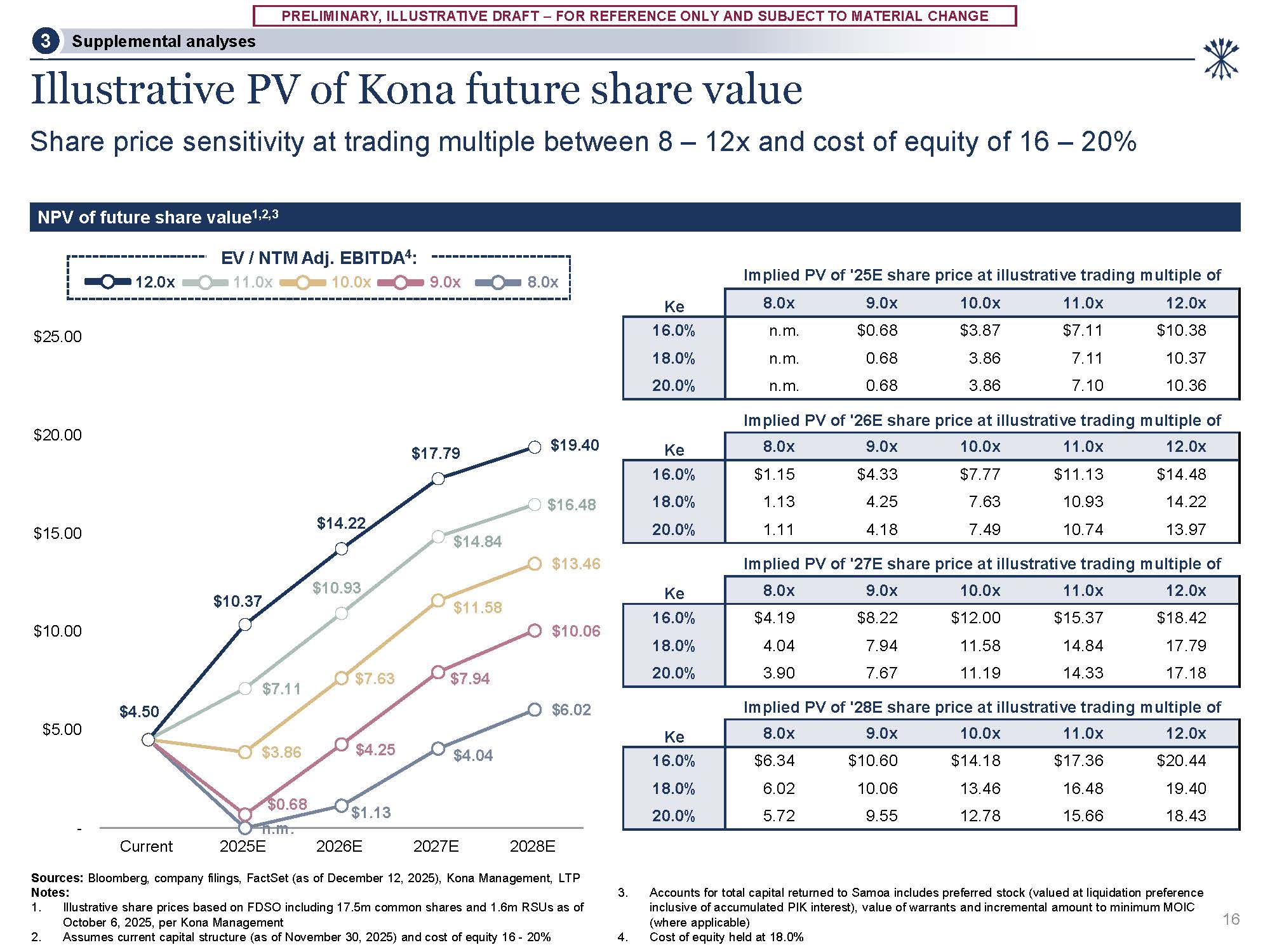

CHANGE Illustrative PV of Kona future share value Share price sensitivity at trading multiple between 8 – 12x and cost of equity of 16 – 20% Sources: Bloomberg, company filings, FactSet (as of December 12, 2025), Kona Management,

LTP Notes: Illustrative share prices based on FDSO including 17.5m common shares and 1.6m RSUs as of October 6, 2025, per Kona Management Assumes current capital structure (as of November 30, 2025) and cost of equity 16 - 20% Accounts for

total capital returned to Samoa includes preferred stock (valued at liquidation preference inclusive of accumulated PIK interest), value of warrants and incremental amount to minimum MOIC (where applicable) Cost of equity held at 18.0% NPV of

future share value1,2,3 9.0x 8.0x EV / NTM Adj. EBITDA4: 11.0x 10.0x 12.0x Supplemental

analyses 3 16 Ke 8.0x 9.0x 10.0x 11.0x 12.0x 16.0% n.m. $0.68 $3.87 $7.11 $10.38 18.0% n.m. 0.68 3.86 7.11 10.37 20.0% n.m. 0.68 3.86 7.10 10.36 Ke 8.0x 9.0x 10.0x 11.0x 12.0x 16.0% $1.15 $4.33 $7.77 $11.13 $14.48 18.0% 1.13 4.25 7.63 10.93 14.22 20.0% 1.11 4.18 7.49 10.74 13.97 Ke 8.0x 9.0x 10.0x 11.0x 12.0x 16.0% $4.19 $8.22 $12.00 $15.37 $18.42 18.0% 4.04 7.94 11.58 14.84 17.79 20.0% 3.90 7.67 11.19 14.33 17.18 Ke 8.0x 9.0x 10.0x 11.0x 12.0x 16.0% $6.34 $10.60 $14.18 $17.36 $20.44 18.0% 6.02 10.06 13.46 16.48 19.40 20.0% 5.72 9.55 12.78 15.66 18.43 Implied

PV of '25E share price at illustrative trading multiple of Implied PV of '26E share price at illustrative trading multiple of Implied PV of '27E share price at illustrative trading multiple of Implied PV of '28E share price at illustrative

trading multiple of $1.13 $4.04 $6.02 $0.68 n.m. $4.25 $7.94 $10.06 $3.86 $7.63 $11.58 $13.46 $7.11 $10.93 $14.84 $16.48 $4.50 $10.37 $14.22 $17.79 $19.40 - $5.00 $10.00 $15.00 $20.00 $25.00 Current 2025E 2026E 2027E

2028E

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

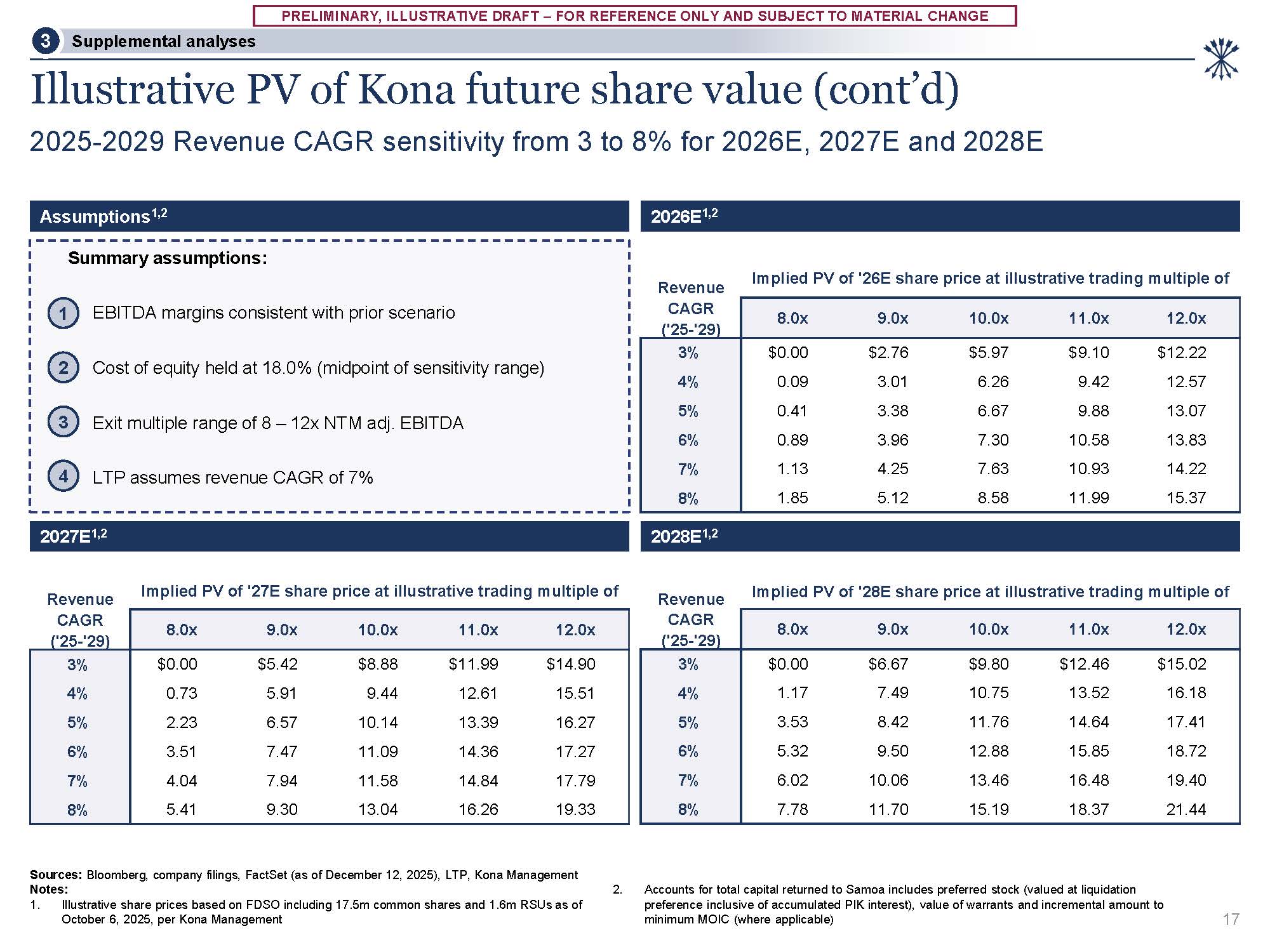

CHANGE Illustrative PV of Kona future share value (cont’d) 2025-2029 Revenue CAGR sensitivity from 3 to 8% for 2026E, 2027E and 2028E Assumptions1,2 2026E1,2 Summary assumptions: 1 EBITDA margins consistent with prior scenario 2 Cost

of equity held at 18.0% (midpoint of sensitivity range) 3 Exit multiple range of 8 – 12x NTM adj. EBITDA 4 LTP assumes revenue CAGR of 7% Sources: Bloomberg, company filings, FactSet (as of December 12, 2025), LTP, Kona

Management Notes: 1. Illustrative share prices based on FDSO including 17.5m common shares and 1.6m RSUs as of October 6, 2025, per Kona Management 2. Accounts for total capital returned to Samoa includes preferred stock (valued at

liquidation preference inclusive of accumulated PIK interest), value of warrants and incremental amount to minimum MOIC (where applicable) 2027E1,2 2028E1,2 17 Supplemental analyses 3 Revenue Implied PV of '26E share price at

illustrative trading multiple of CAGR

('25-'29) 8.0x 9.0x 10.0x 11.0x 12.0x 3% $0.00 $2.76 $5.97 $9.10 $12.22 4% 0.09 3.01 6.26 9.42 12.57 5% 0.41 3.38 6.67 9.88 13.07 6% 0.89 3.96 7.30 10.58 13.83 7% 1.13 4.25 7.63 10.93 14.22 8% 1.85 5.12 8.58 11.99 15.37 Revenue Implied

PV of '27E share price at illustrative trading multiple of CAGR

('25-'29) 8.0x 9.0x 10.0x 11.0x 12.0x 3% $0.00 $5.42 $8.88 $11.99 $14.90 4% 0.73 5.91 9.44 12.61 15.51 5% 2.23 6.57 10.14 13.39 16.27 6% 3.51 7.47 11.09 14.36 17.27 7% 4.04 7.94 11.58 14.84 17.79 8% 5.41 9.30 13.04 16.26 19.33 Revenue Implied

PV of '28E share price at illustrative trading multiple of CAGR

('25-'29) 8.0x 9.0x 10.0x 11.0x 12.0x 3% $0.00 $6.67 $9.80 $12.46 $15.02 4% 1.17 7.49 10.75 13.52 16.18 5% 3.53 8.42 11.76 14.64 17.41 6% 5.32 9.50 12.88 15.85 18.72 7% 6.02 10.06 13.46 16.48 19.40 8% 7.78 11.70 15.19 18.37 21.44

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

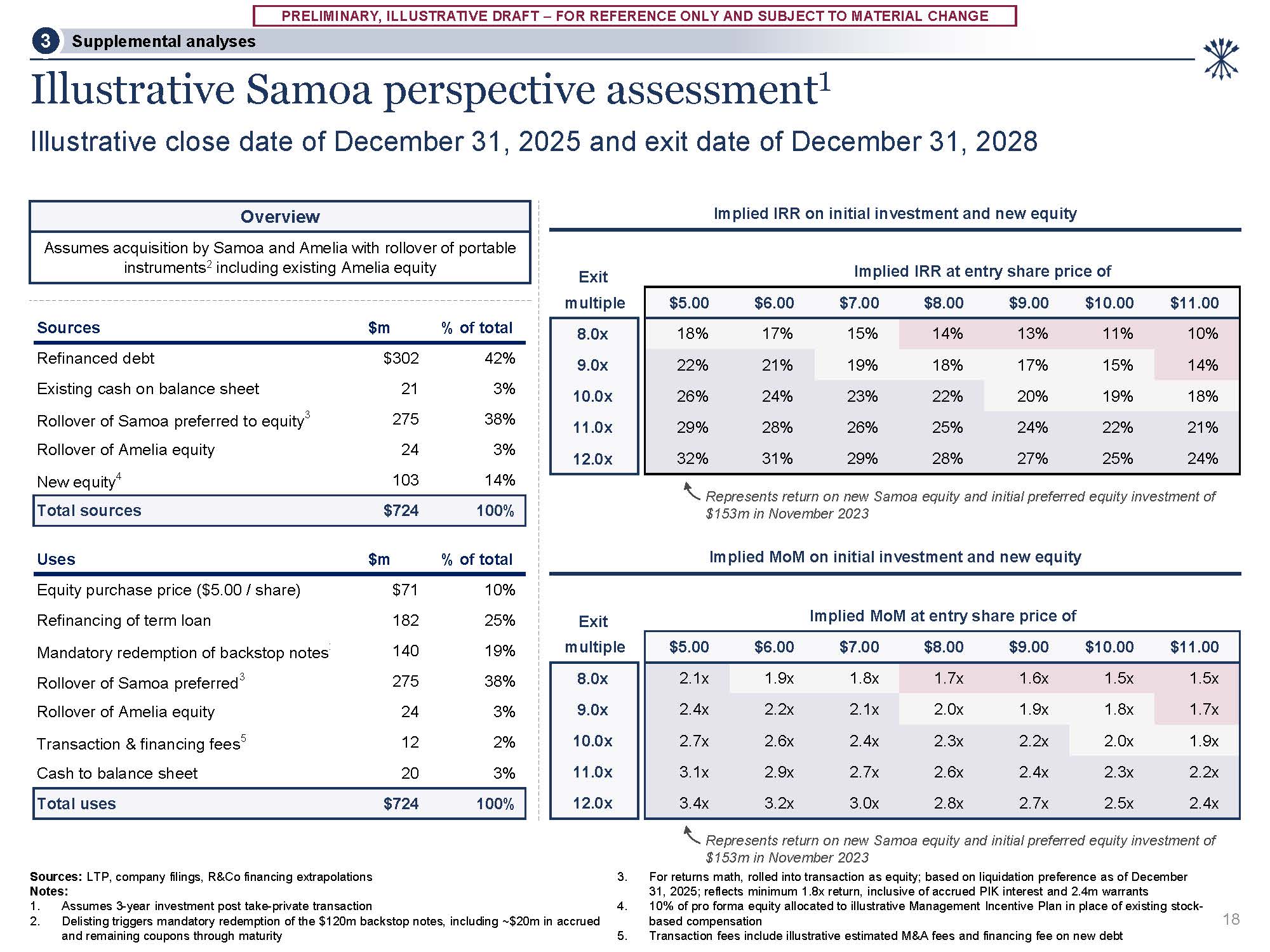

CHANGE Illustrative Samoa perspective assessment1 Illustrative close date of December 31, 2025 and exit date of December 31, 2028 N Assumes 3-year investment post take-private transaction Delisting triggers mandatory redemption of the

$120m backstop notes, including ~$20m in accrued and remaining coupons through maturity Sources $m % of total Refinanced debt $302 42% Existing cash on balance sheet 21 3% Rollover of Samoa preferred to equity3 275 38% Rollover of

Amelia equity 24 3% New equity4 103 14% Total sources $724 100% Uses $m % of total Equity purchase price ($5.00 / share) $71 10% Refinancing of term loan 182 25% Mandatory redemption of backstop notes 140 19% Rollover of Samoa

preferred3 275 38% Rollover of Amelia equity 24 3% Transaction & financing fees5 12 2% Cash to balance sheet 20 3% Total uses $724 100% Sources: LTP, company filings, R&Co financing extrapolations otes: Assumes acquisition

by Samoa and Amelia with rollover of portable instruments2 including existing Amelia equity Overview Implied IRR on initial investment and new equity Represents return on new Samoa equity and initial preferred equity investment of $153m in

November 2023 Implied MoM on initial investment and new equity Represents return on new Samoa equity and initial preferred equity investment of $153m in November 2023 For returns math, rolled into transaction as equity; based on liquidation

preference as of December 31, 2025; reflects minimum 1.8x return, inclusive of accrued PIK interest and 2.4m warrants 10% of pro forma equity allocated to illustrative Management Incentive Plan in place of existing stock-based

compensation Transaction fees include illustrative estimated M&A fees and financing fee on new debt 18 Supplemental analyses 3 Exit Implied IRR at entry share price

of multiple $5.00 $6.00 $7.00 $8.00 $9.00 $10.00 $11.00 8.0x 18% 17% 15% 14% 13% 11% 10% 9.0x 22% 21% 19% 18% 17% 15% 14% 10.0x 26% 24% 23% 22% 20% 19% 18% 11.0x 29% 28% 26% 25% 24% 22% 21% 12.0x 32% 31% 29% 28% 27% 25% 24% Exit multiple $5.00 $6.00 $10.00 $11.00 2.1x 1.9x 1.5x 1.5x 2.4x 2.2x 1.8x 1.7x 2.7x 2.6x Implied

MoM at entry share price of $7.00 $8.00 $9.00 1.8x 1.7x 1.6x 2.1x 2.0x 1.9x 2.4x 2.3x 2.2x 2.0x 1.9x 8.0x 9.0x 10.0x 11.0x 12.0x 3.1x 3.4x 2.9x 3.2x 2.7x 3.0x 2.6x 2.8x 2.4x 2.7x 2.3x 2.5x 2.2x 2.4x

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

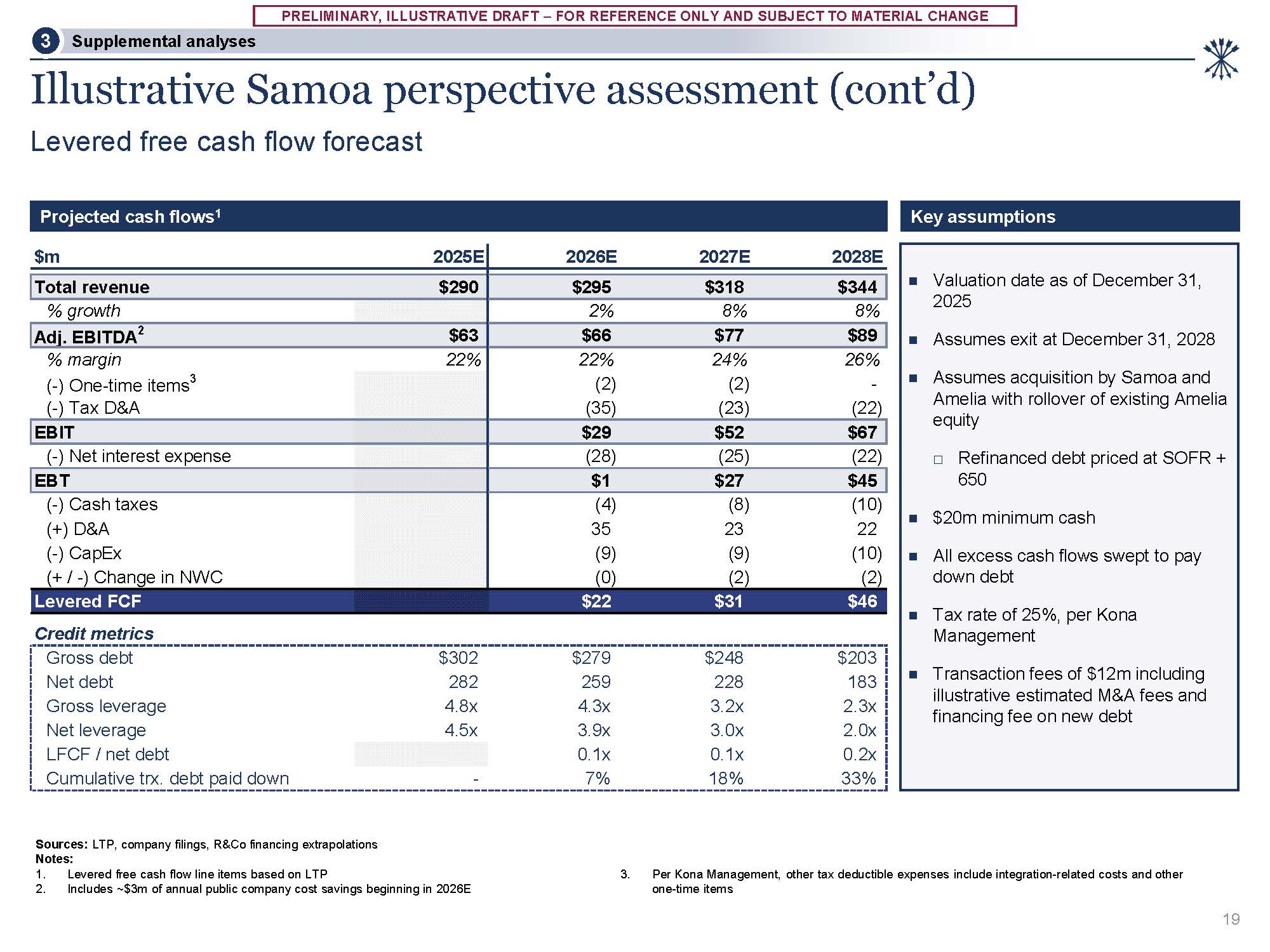

CHANGE Illustrative Samoa perspective assessment (cont’d) Levered free cash flow forecast Projected cash flows1 Sources: LTP, company filings, R&Co financing extrapolations Notes: Levered free cash flow line items based on

LTP Includes ~$3m of annual public company cost savings beginning in 2026E 3. Per Kona Management, other tax deductible expenses include integration-related costs and other one-time items Valuation date as of December 31, 2025 Assumes exit

at December 31, 2028 Assumes acquisition by Samoa and Amelia with rollover of existing Amelia equity □ Refinanced debt priced at SOFR + 650 $20m minimum cash All excess cash flows swept to pay down debt Tax rate of 25%, per Kona

Management Transaction fees of $12m including illustrative estimated M&A fees and financing fee on new debt Key assumptions 19 Supplemental analyses 3 $m 2025E 2026E 2027E 2028E Total revenue $290 $295 $318 $344 %

growth 2% 8% 8% Adj. EBITDA2 $63 $66 $77 $89 % margin 22% 22% 24% 26% (-) One-time items3 (2) (2) - (-) Tax D&A (35) (23) (22) EBIT $29 $52 $67 (-) Net interest expense (28) (25) (22) EBT $1 $27 $45 (-)

Cash taxes (4) (8) (10) (+) D&A 35 23 22 (-) CapEx (9) (9) (10) (+ / -) Change in NWC (0) (2) (2) Levered FCF $22 $31 $46 Credit metrics Gross debt $302 $279 $248 $203 Net debt 282 259 228 183 Gross

leverage 4.8x 4.3x 3.2x 2.3x Net leverage 4.5x 3.9x 3.0x 2.0x LFCF / net debt 0.1x 0.1x 0.2x Cumulative trx. debt paid down - 7% 18% 33%

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

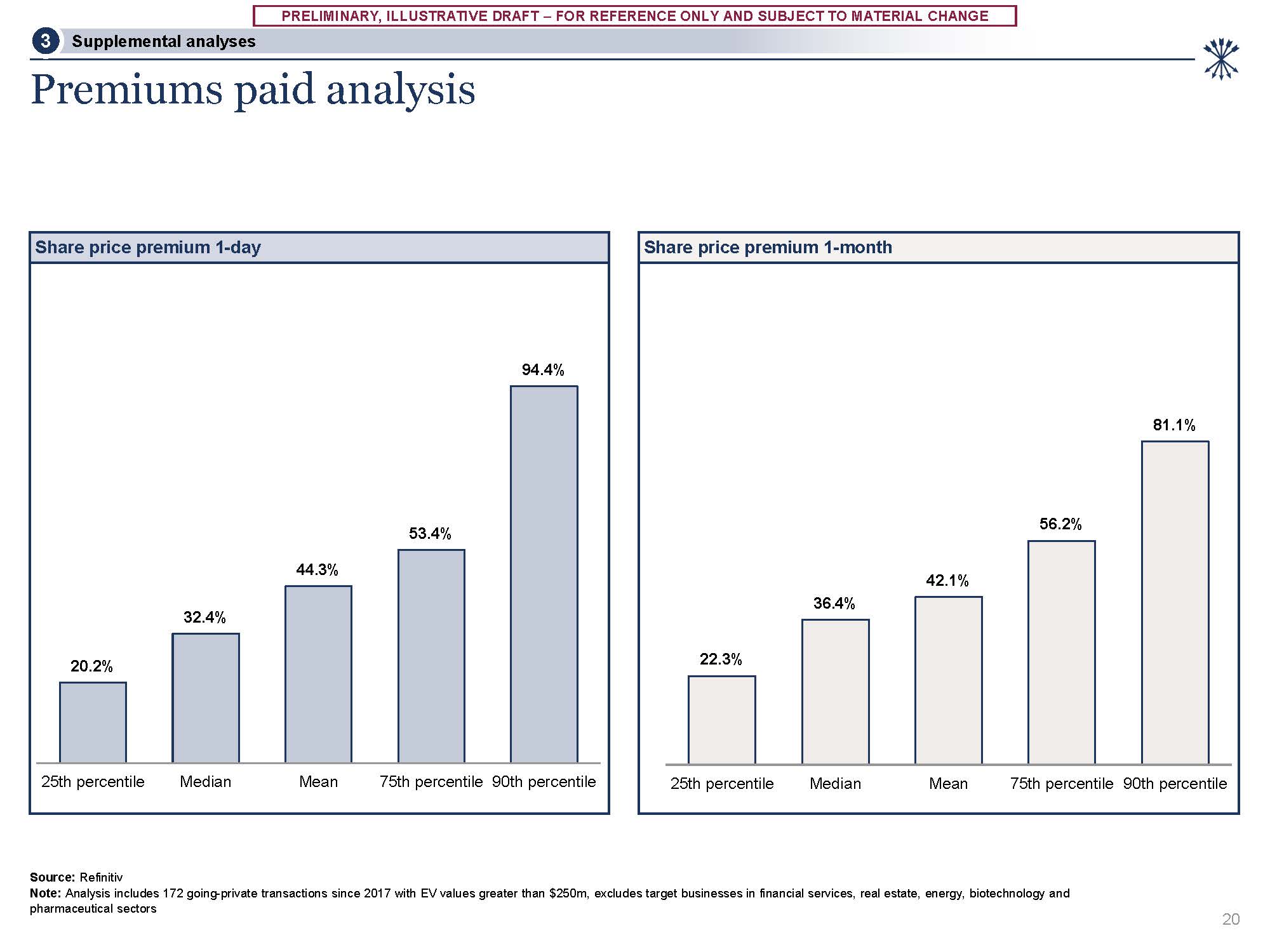

CHANGE 22.3% 36.4% 42.1% 56.2% 81.1% 25th percentile Median Mean 75th percentile 90th percentile 20.2% 32.4% 44.3% 53.4% 94.4% 25th percentile Median Mean 75th percentile 90th percentile Share price premium 1-day Premiums

paid analysis Share price premium 1-month Source: Refinitiv Note: Analysis includes 172 going-private transactions since 2017 with EV values greater than $250m, excludes target businesses in financial services, real estate, energy,

biotechnology and pharmaceutical sectors 20 Supplemental analyses 3

Appendix

Appendix A Other supporting materials

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

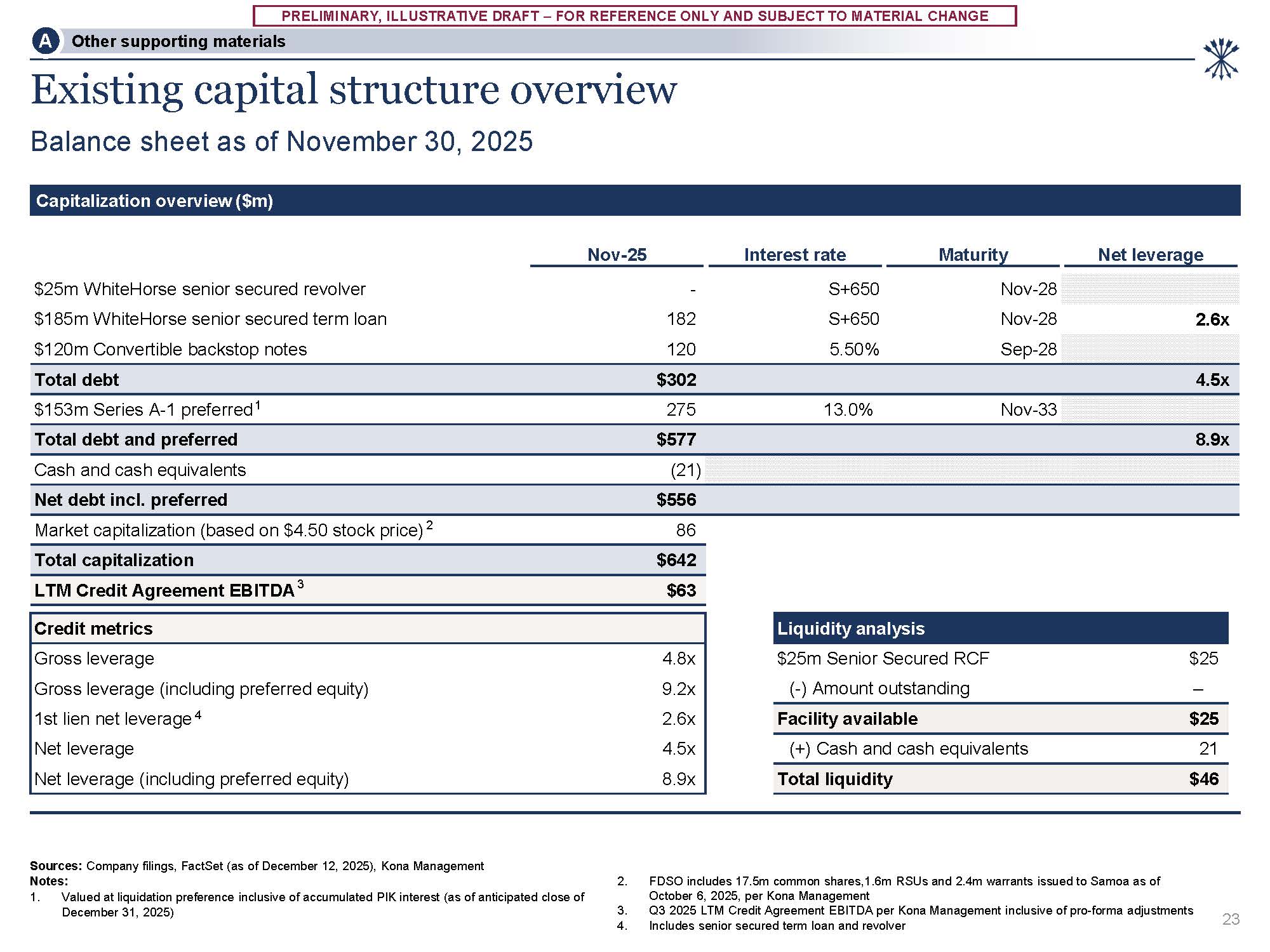

CHANGE Nov-25 Interest rate Maturity Net leverage - $25m WhiteHorse senior secured revolver $185m WhiteHorse senior secured term loan $120m Convertible backstop notes 182 120 S+650 S+650 5.50% Nov-28 Nov-28 Sep-28 Credit

metrics Gross leverage 4.8x Gross leverage (including preferred equity) 9.2x 1st lien net leverage 4 2.6x Net leverage 4.5x Net leverage (including preferred equity) 8.9x 2.6x Existing capital structure overview Balance sheet as of

November 30, 2025 Capitalization overview ($m) Sources: Company filings, FactSet (as of December 12, 2025), Kona Management Notes: 1. Valued at liquidation preference inclusive of accumulated PIK interest (as of anticipated close of

December 31, 2025) FDSO includes 17.5m common shares,1.6m RSUs and 2.4m warrants issued to Samoa as of October 6, 2025, per Kona Management Q3 2025 LTM Credit Agreement EBITDA per Kona Management inclusive of pro-forma adjustments Includes

senior secured term loan and revolver Other supporting materials A 23 Total debt $302 4.5x $153m Series A-1 preferred1 275 13.0% Nov-33 Total debt and preferred $577 8.9x Cash and cash equivalents (21) Net debt incl. preferred

$556 Market capitalization (based on $4.50 stock price) 2 86 Total capitalization $642 LTM Credit Agreement EBITDA 3 $63 Liquidity analysis $25m Senior Secured RCF (-) Amount outstanding $25 – Facility available $25 (+) Cash and cash

equivalents 21 Total liquidity $46

PRELIMINARY, ILLUSTRATIVE DRAFT – FOR REFERENCE ONLY AND SUBJECT TO MATERIAL

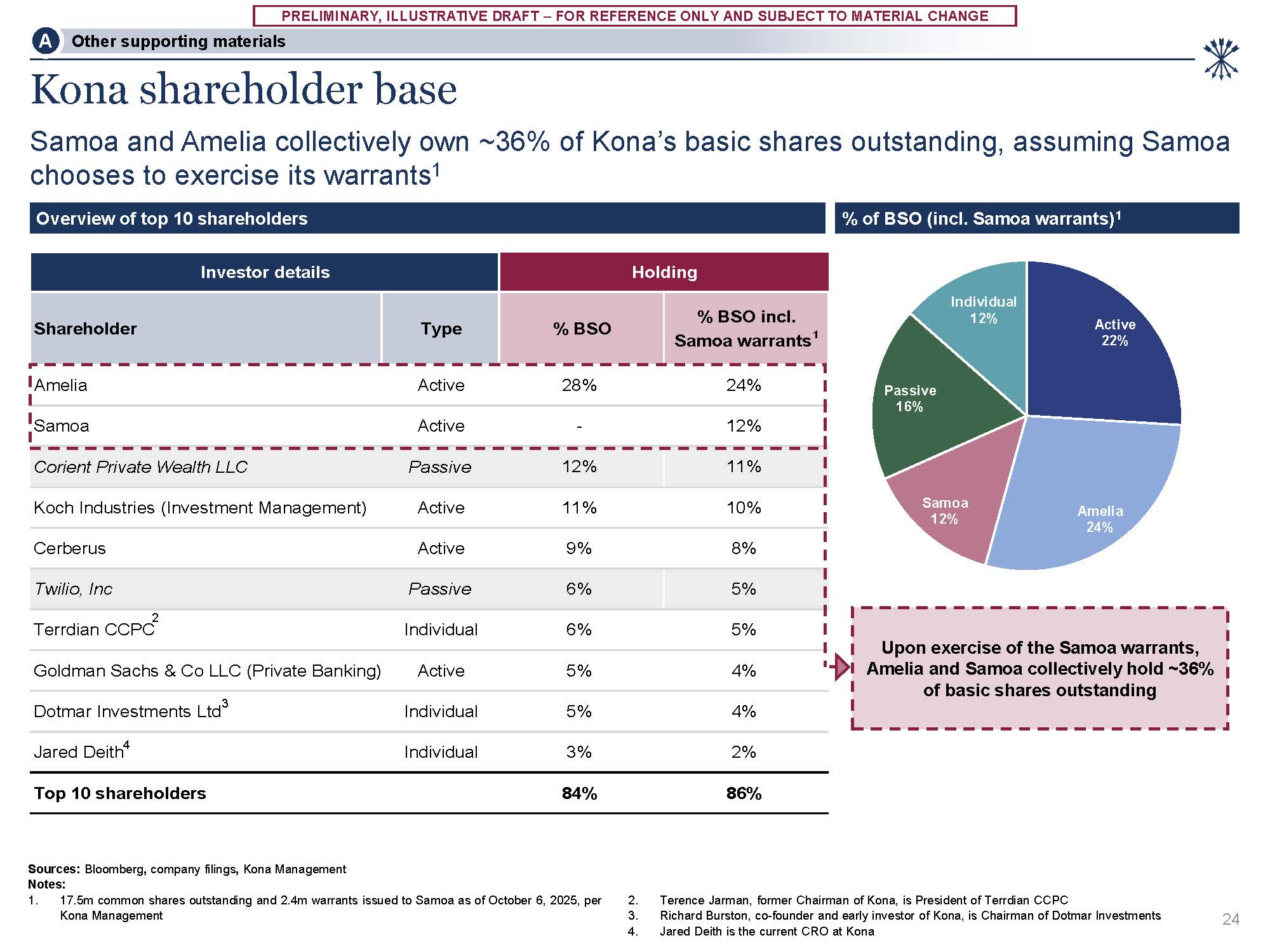

CHANGE Investor details Holding Shareholder Type % BSO % BSO incl. Samoa warrants1 Amelia Active 28% 24% Samoa Active - 12% Corient Private Wealth LLC Passive 12% 11% Koch Industries (Investment

Management) Active 11% 10% Cerberus Active 9% 8% Twilio, Inc Passive 6% 5% Individual 6% 5% Goldman Sachs & Co LLC (Private Banking) Active 5% 4% Dotmar Investments Ltd3 Individual 5% 4% Jared

Deith4 Individual 3% 2% Top 10 shareholders 84% 86% 2 Terrdian CCPC % of BSO (incl. Samoa warrants)1 Kona shareholder base Samoa and Amelia collectively own ~36% of Kona’s basic shares outstanding, assuming Samoa chooses to exercise

its warrants1 Sources: Bloomberg, company filings, Kona Management Notes: 1. 17.5m common shares outstanding and 2.4m warrants issued to Samoa as of October 6, 2025, per Kona Management Terence Jarman, former Chairman of Kona, is President

of Terrdian CCPC Richard Burston, co-founder and early investor of Kona, is Chairman of Dotmar Investments Jared Deith is the current CRO at Kona Overview of top 10 shareholders Other supporting materials A Upon exercise of the Samoa

warrants, Amelia and Samoa collectively hold ~36% of basic shares outstanding 24 Active 22% Amelia 24% Samoa 12% Passive 16% Individual 12%