Project Kona: Special Committee discussion materials April 9, 2025 Exhibit

(c)(ii)

Contents Rothschild & Co qualifications Executive

summary Appendix 3 14 26

1 Rothschild & Co qualifications

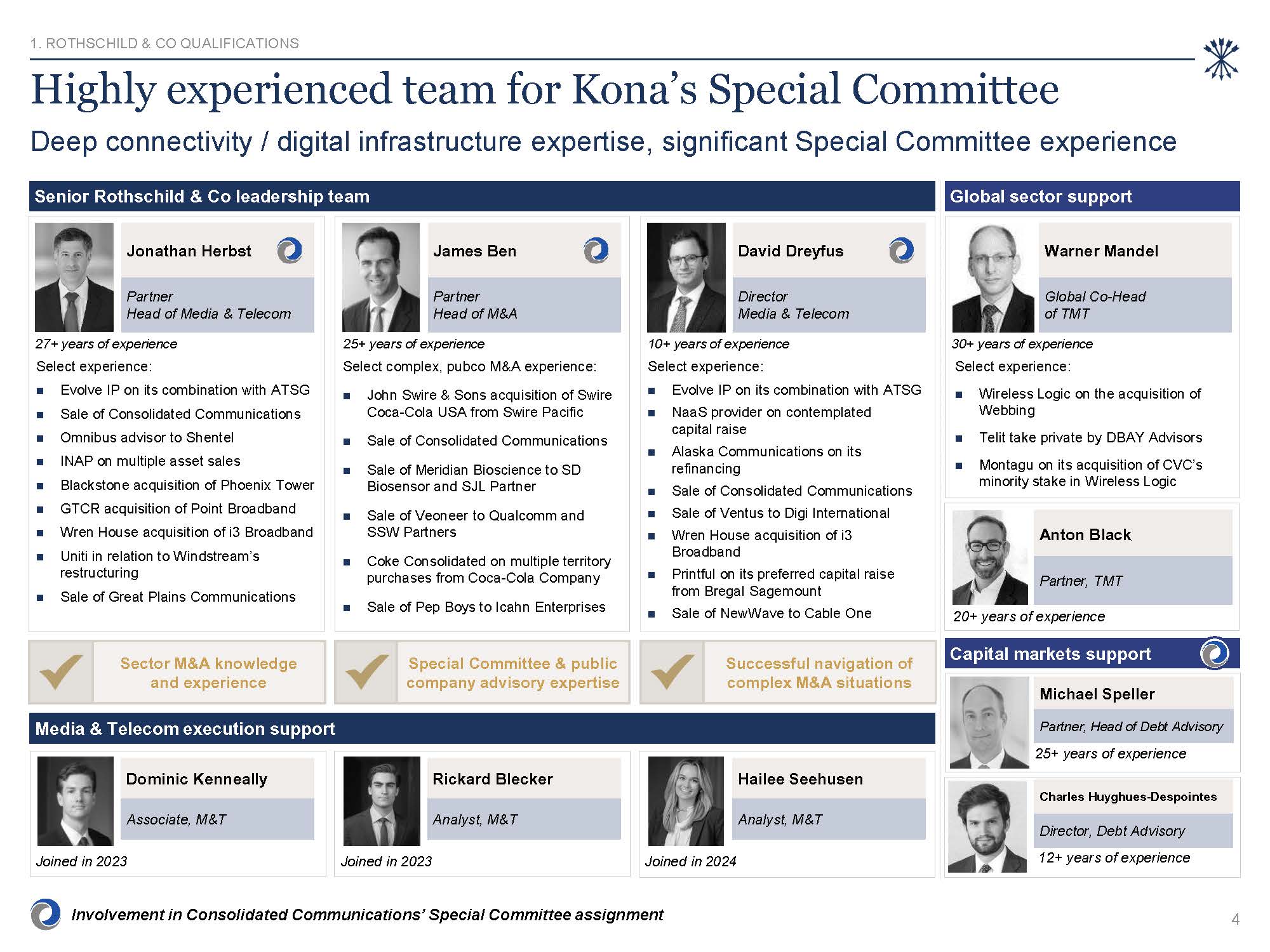

Highly experienced team for Kona’s Special Committee Deep connectivity / digital

infrastructure expertise, significant Special Committee experience Involvement in Consolidated Communications’ Special Committee assignment Media & Telecom execution support Sector M&A knowledge and experience Special Committee

& public company advisory expertise Successful navigation of complex M&A situations Dominic Kenneally Associate, M&T Joined in 2023 Rickard Blecker Analyst, M&T Joined in 2023 Hailee Seehusen Analyst, M&T Joined in

2024 Senior Rothschild & Co leadership team Jonathan Herbst Partner Head of Media & Telecom 27+ years of experience Select experience: Evolve IP on its combination with ATSG Sale of Consolidated Communications Omnibus advisor

to Shentel INAP on multiple asset sales Blackstone acquisition of Phoenix Tower GTCR acquisition of Point Broadband Wren House acquisition of i3 Broadband Uniti in relation to Windstream’s restructuring Sale of Great Plains

Communications James Ben Partner Head of M&A 25+ years of experience Select complex, pubco M&A experience: John Swire & Sons acquisition of Swire Coca-Cola USA from Swire Pacific Sale of Consolidated Communications Sale of

Meridian Bioscience to SD Biosensor and SJL Partner Sale of Veoneer to Qualcomm and SSW Partners Coke Consolidated on multiple territory purchases from Coca-Cola Company Sale of Pep Boys to Icahn Enterprises David Dreyfus Director Media

& Telecom 10+ years of experience Select experience: Evolve IP on its combination with ATSG NaaS provider on contemplated capital raise Alaska Communications on its refinancing Sale of Consolidated Communications Sale of Ventus to

Digi International Wren House acquisition of i3 Broadband Printful on its preferred capital raise from Bregal Sagemount Sale of NewWave to Cable One Global sector support Warner Mandel Global Co-Head of TMT 30+ years of

experience Select experience: Wireless Logic on the acquisition of Webbing Telit take private by DBAY Advisors Montagu on its acquisition of CVC’s minority stake in Wireless Logic Anton Black Partner, TMT 20+ years of experience Capital

markets support Michael Speller Partner, Head of Debt Advisory 25+ years of experience Charles Huyghues-Despointes Director, Debt Advisory 12+ years of experience 1. ROTHSCHILD & CO QUALIFICATIONS 4

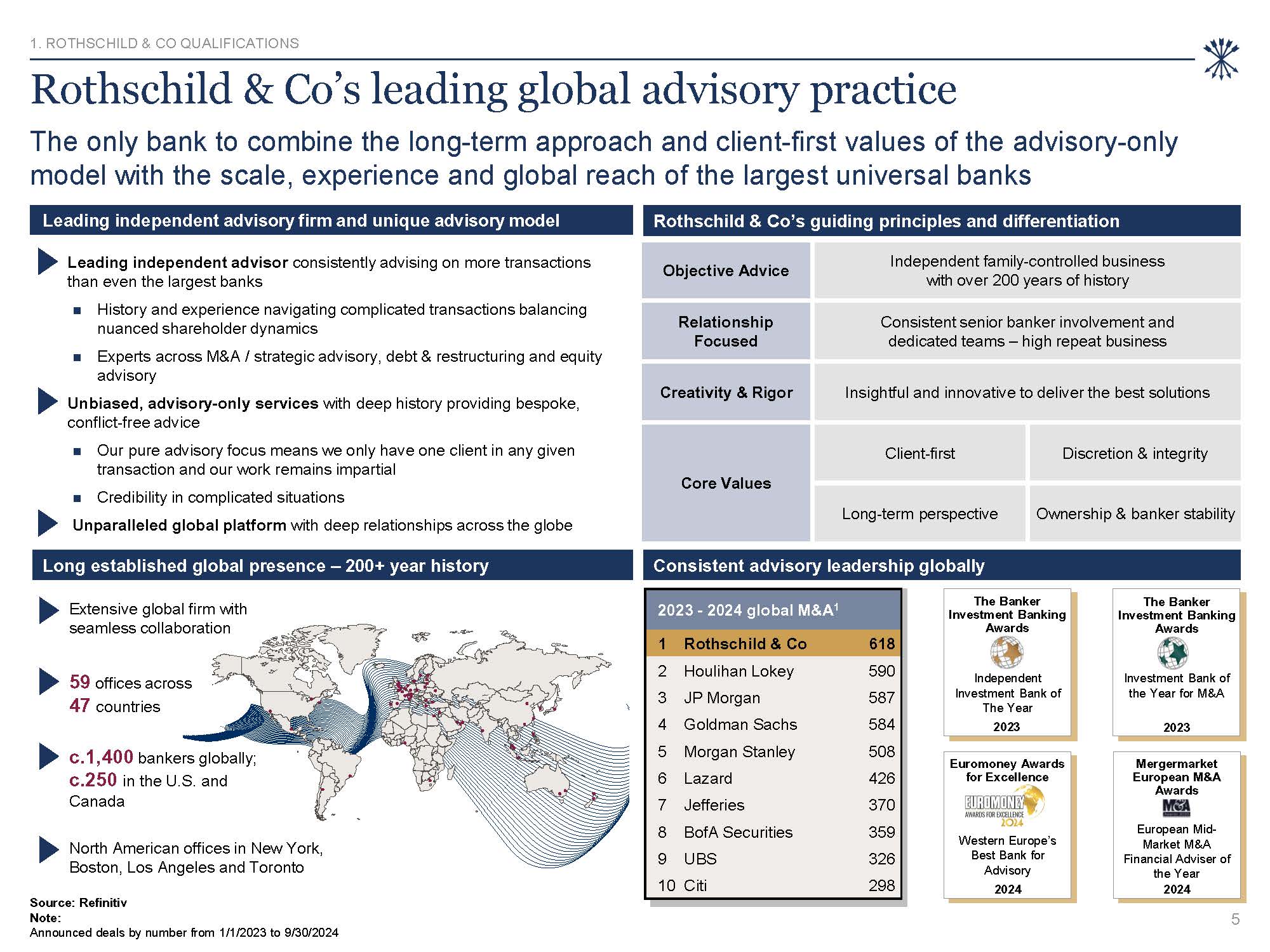

2023 - 2024 global M&A1 1 Rothschild & Co 618 2 Houlihan

Lokey 590 3 JP Morgan 587 4 Goldman Sachs 584 5 Morgan Stanley 508 6 Lazard 426 7 Jefferies 370 8 BofA Securities 359 9 UBS 326 10 Citi 298 Rothschild & Co’s leading global advisory practice The only bank to

combine the long-term approach and client-first values of the advisory-only model with the scale, experience and global reach of the largest universal banks Rothschild & Co’s guiding principles and differentiation Objective

Advice Independent family-controlled business with over 200 years of history Relationship Focused Consistent senior banker involvement and dedicated teams – high repeat business Creativity & Rigor Insightful and innovative to deliver

the best solutions Core Values Client-first Discretion & integrity Long-term perspective Ownership & banker stability Consistent advisory leadership globally Extensive global firm with seamless collaboration c.1,400 bankers

globally; c.250 in the U.S. and Canada 59 offices across 47 countries North American offices in New York, Boston, Los Angeles and Toronto Leading independent advisory firm and unique advisory model Leading independent advisor consistently

advising on more transactions than even the largest banks History and experience navigating complicated transactions balancing nuanced shareholder dynamics Experts across M&A / strategic advisory, debt & restructuring and equity

advisory Unbiased, advisory-only services with deep history providing bespoke, conflict-free advice Our pure advisory focus means we only have one client in any given transaction and our work remains impartial Credibility in complicated

situations Unparalleled global platform with deep relationships across the globe Long established global presence – 200+ year history The Banker Investment Banking Awards Independent Investment Bank of The Year 2023 The Banker Investment

Banking Awards Investment Bank of the Year for M&A 2023 Euromoney Awards for Excellence Western Europe’s Best Bank for Advisory 2024 Mergermarket European M&A Awards European Mid-Market M&A Financial Adviser of the

Year 2024 Source: Refinitiv Note: Announced deals by number from 1/1/2023 to 9/30/2024 1. ROTHSCHILD & CO QUALIFICATIONS 5

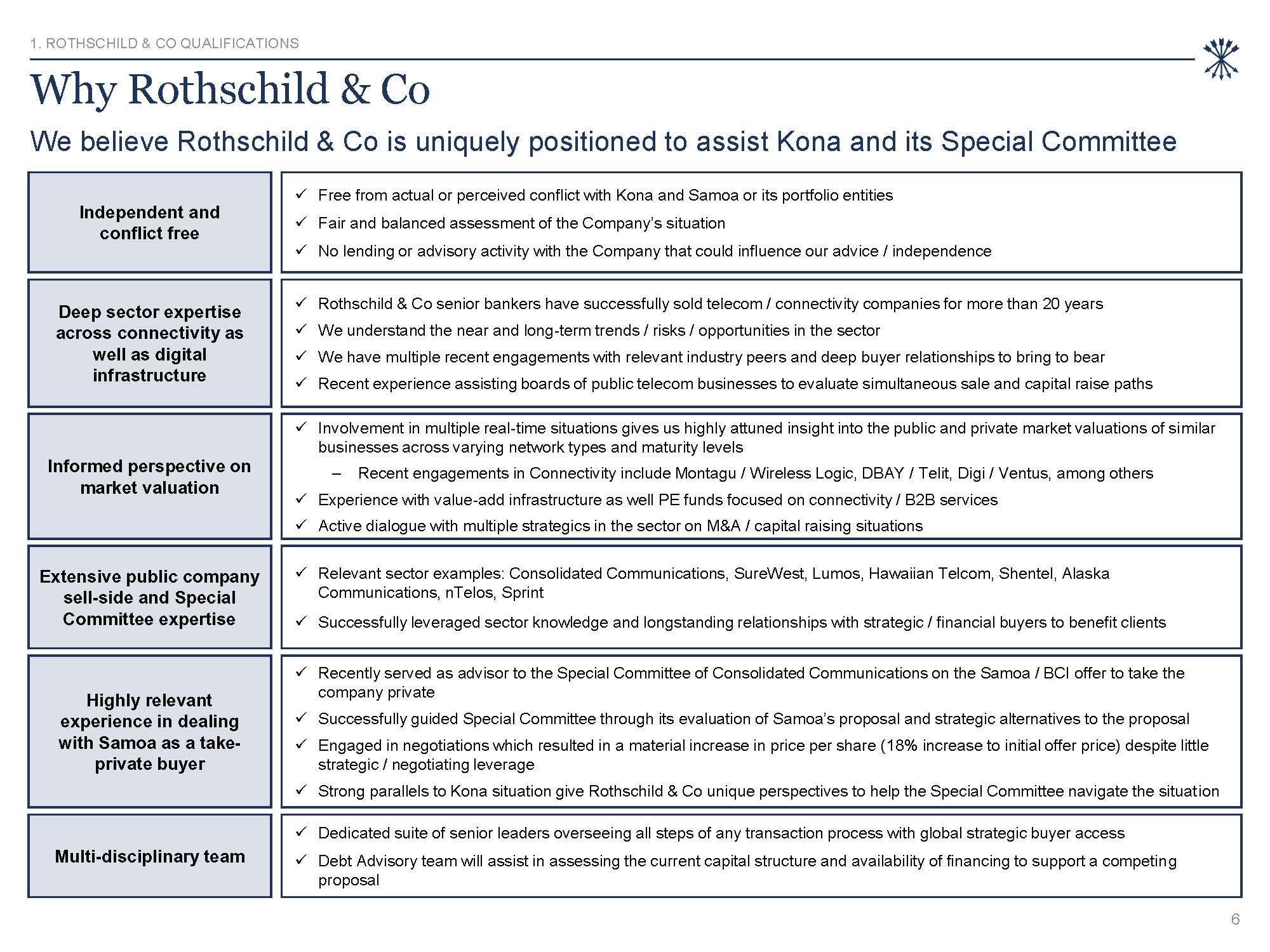

Why Rothschild & Co We believe Rothschild & Co is uniquely positioned to

assist Kona and its Special Committee Deep sector expertise across connectivity as well as digital infrastructure Rothschild & Co senior bankers have successfully sold telecom / connectivity companies for more than 20 years We understand

the near and long-term trends / risks / opportunities in the sector We have multiple recent engagements with relevant industry peers and deep buyer relationships to bring to bear Recent experience assisting boards of public telecom businesses

to evaluate simultaneous sale and capital raise paths Informed perspective on market valuation Involvement in multiple real-time situations gives us highly attuned insight into the public and private market valuations of similar businesses

across varying network types and maturity levels – Recent engagements in Connectivity include Montagu / Wireless Logic, DBAY / Telit, Digi / Ventus, among others Experience with value-add infrastructure as well PE funds focused on

connectivity / B2B services Active dialogue with multiple strategics in the sector on M&A / capital raising situations Extensive public company sell-side and Special Committee expertise Relevant sector examples: Consolidated

Communications, SureWest, Lumos, Hawaiian Telcom, Shentel, Alaska Communications, nTelos, Sprint Successfully leveraged sector knowledge and longstanding relationships with strategic / financial buyers to benefit clients Independent and

conflict free Free from actual or perceived conflict with Kona and Samoa or its portfolio entities Fair and balanced assessment of the Company’s situation No lending or advisory activity with the Company that could influence our advice /

independence Multi-disciplinary team Dedicated suite of senior leaders overseeing all steps of any transaction process with global strategic buyer access Debt Advisory team will assist in assessing the current capital structure and

availability of financing to support a competing proposal Highly relevant experience in dealing with Samoa as a take-private buyer Recently served as advisor to the Special Committee of Consolidated Communications on the Samoa / BCI offer to

take the company private Successfully guided Special Committee through its evaluation of Samoa’s proposal and strategic alternatives to the proposal Engaged in negotiations which resulted in a material increase in price per share (18%

increase to initial offer price) despite little strategic / negotiating leverage Strong parallels to Kona situation give Rothschild & Co unique perspectives to help the Special Committee navigate the situation 1. ROTHSCHILD & CO

QUALIFICATIONS 6

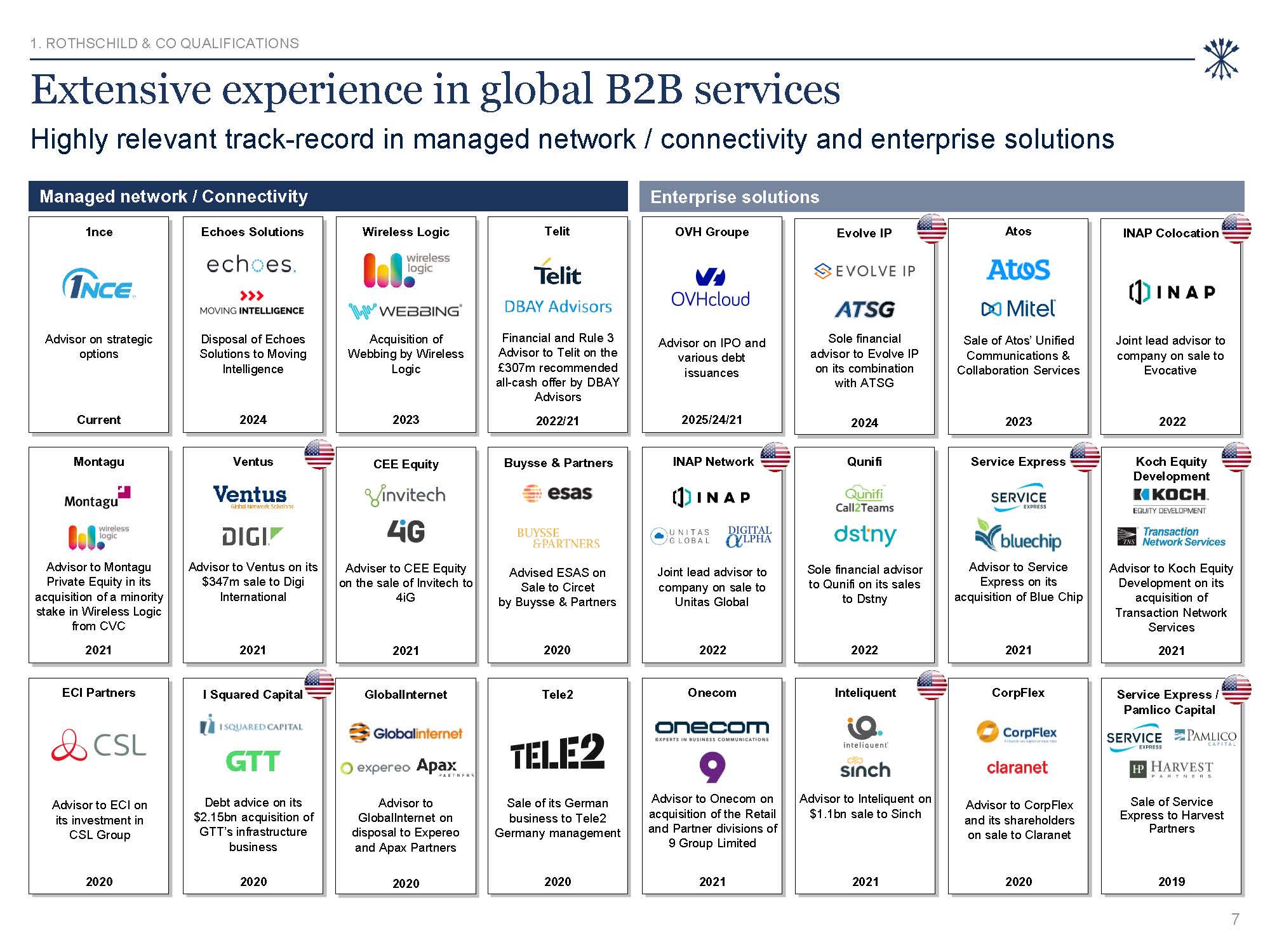

Extensive experience in global B2B services Highly relevant track-record in

managed network / connectivity and enterprise solutions Managed network / Connectivity Wireless Logic Acquisition of Webbing by Wireless Logic 2023 Echoes Solutions Disposal of Echoes Solutions to Moving Intelligence 2024 Qunifi Sole

financial advisor to Qunifi on its sales to Dstny 2022 INAP Network Joint lead advisor to company on sale to Unitas Global 2022 2021 Ventus Advisor to Ventus on its $347m sale to Digi International 2021 Service Express Advisor to

Service Express on its acquisition of Blue Chip Montagu Advisor to Montagu Private Equity in its acquisition of a minority stake in Wireless Logic from CVC 2021 Koch Equity Development Advisor to Koch Equity Development on its acquisition

of Transaction Network Services 2021 1nce Advisor on strategic options Current Telit Financial and Rule 3 Advisor to Telit on the £307m recommended all-cash offer by DBAY Advisors 2022/21 Onecom Advisor to Onecom on acquisition of the

Retail and Partner divisions of 9 Group Limited 2021 CEE Equity Adviser to CEE Equity on the sale of Invitech to 4iG 2021 CorpFlex Advisor to CorpFlex and its shareholders on sale to Claranet 2020 ECI Partners Advisor to ECI on its

investment in CSL Group 2020 Tele2 Sale of its German business to Tele2 Germany management 2020 2020 I Squared Capital Debt advice on its $2.15bn acquisition of GTT’s infrastructure business Buysse & Partners Advised ESAS on Sale

to Circet by Buysse & Partners 2020 2021 Inteliquent Advisor to Inteliquent on $1.1bn sale to Sinch Service Express / Pamlico Capital Sale of Service Express to Harvest Partners 2019 Enterprise solutions OVH Groupe Advisor on

IPO and various debt issuances 2025/24/21 Evolve IP Atos INAP Colocation Sole financial Sale of Atos’ Unified Joint lead advisor to advisor to Evolve IP Communications & company on sale to on its combination Collaboration Services

Evocative with ATSG 2024 2023 2022 GlobalInternet Advisor to GlobalInternet on disposal to Expereo and Apax Partners 2020 1. ROTHSCHILD & CO QUALIFICATIONS 7

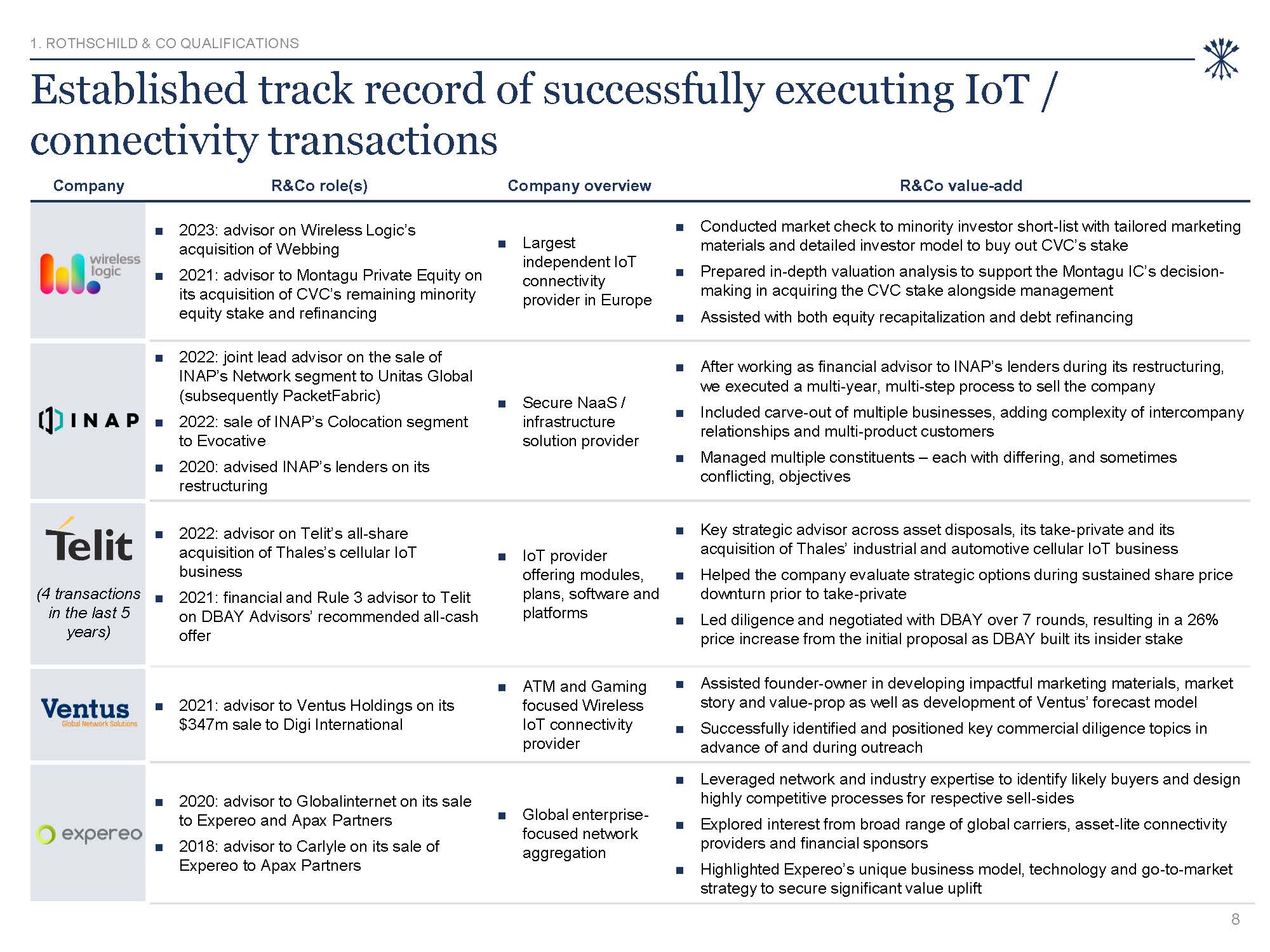

Company R&Co role(s) Company overview R&Co value-add 2023: advisor on

Wireless Logic’s acquisition of Webbing 2021: advisor to Montagu Private Equity on its acquisition of CVC’s remaining minority equity stake and refinancing Largest independent IoT connectivity provider in Europe Conducted market check to

minority investor short-list with tailored marketing materials and detailed investor model to buy out CVC’s stake Prepared in-depth valuation analysis to support the Montagu IC’s decision- making in acquiring the CVC stake alongside

management Assisted with both equity recapitalization and debt refinancing 2022: joint lead advisor on the sale of INAP’s Network segment to Unitas Global (subsequently PacketFabric) 2022: sale of INAP’s Colocation segment to

Evocative 2020: advised INAP’s lenders on its restructuring Secure NaaS / infrastructure solution provider After working as financial advisor to INAP’s lenders during its restructuring, we executed a multi-year, multi-step process to sell

the company Included carve-out of multiple businesses, adding complexity of intercompany relationships and multi-product customers Managed multiple constituents – each with differing, and sometimes conflicting, objectives (4 transactions in

the last 5 years) 2022: advisor on Telit’s all-share acquisition of Thales’s cellular IoT business 2021: financial and Rule 3 advisor to Telit on DBAY Advisors’ recommended all-cash offer IoT provider offering modules, plans, software and

platforms Key strategic advisor across asset disposals, its take-private and its acquisition of Thales’ industrial and automotive cellular IoT business Helped the company evaluate strategic options during sustained share price downturn prior

to take-private Led diligence and negotiated with DBAY over 7 rounds, resulting in a 26% price increase from the initial proposal as DBAY built its insider stake 2021: advisor to Ventus Holdings on its $347m sale to Digi International ATM

and Gaming focused Wireless IoT connectivity provider Assisted founder-owner in developing impactful marketing materials, market story and value-prop as well as development of Ventus’ forecast model Successfully identified and positioned key

commercial diligence topics in advance of and during outreach 2020: advisor to Globalinternet on its sale to Expereo and Apax Partners 2018: advisor to Carlyle on its sale of Expereo to Apax Partners Global enterprise-focused network

aggregation Leveraged network and industry expertise to identify likely buyers and design highly competitive processes for respective sell-sides Explored interest from broad range of global carriers, asset-lite connectivity providers and

financial sponsors Highlighted Expereo’s unique business model, technology and go-to-market strategy to secure significant value uplift Established track record of successfully executing IoT / connectivity transactions 1. ROTHSCHILD & CO

QUALIFICATIONS 8

Comverse Technology $1.9bn merger with Verint Systems (Advisor to

parent) Advisor to the Board of Directors Leading advisor to Special Committees & public companies Reinsurance Group of America* Advisor to the Special Committee of Reinsurance Group of America Incorporated in the context of its

separation from MetLife Advisor to Special Committee Justice Holdings Ltd.* $7.5bn merger with Burger King Worldwide Holdings Advisor to Special Committee Cargill (Trustee of the Charitable Trust) $24.3bn split-off and distribution of

Cargill’s stake in Mosaic Advisor to trustee of Charitable Trust Sitronics (Special Committee) Advised Special Committee on tender offer by majority shareholder to minority shareholders for remaining 37% stake in $950mm transaction Advisor

to Special Committee Federal-Mogul Advisor to Special Committee of Federal-Mogul on $500mm rights issue Advisor to Special Committee Dana Advisor to the Special Committee on repurchase of Series A Preferred Stock from Centerbridge

Partners, LP for $472mm Advisor to Special Committee Olam Independent adviser to Independent Directors of Olam on $4.2bn cash offer of Olam by Breedens Investments Advisor to Independent Directors Verso Corporation Sale of Verso

Corporation to BillerudKorsnäs AB for c. $825mm equity value Advisor to Special Committee Edison Fairness opinion in to independent directors in connection with the public tender offer on Edison's share capital launched by EdF Advisor to

Independent Directors Adelphia Communications Corp.* Advisor to the Special Committee of Adelphia Communications Corp. in the context of its $17.6bn acquisition by Time Warner Inc. and Comcast Corp. Advisor to Special Committee Coca-Cola

Bottling Consolidated Co. Fairness Opinion in connection with distribution rights and assets in DL, MD, NC, PA, VA, & WV Advisor to Board / Related Party transaction *Transaction led by Rothschild banker while at predecessor

firm BAT $3.5bn delisting offer of Souza Cruz Advisor to minority shareholders of Target NCO Group* $1.2bn Special Committee role for the NCO Group going private proposal received from management and backed by One Equity Partners Advisor

to Special Committee Revlon, Inc.* Special Committee Advisor (withdrawn) on attempted take private by MacAndrews & Forbes Advisor to Special Committee Consolidated Communications Sale to Searchlight Capital and BCI

for $3.1bn Advisor to Special Committee Chesapeake Corp Advisor to the Special Committee of Chesapeake Corp. in the context of its $485m acquisition by Irving Place Capital and Oaktree Advisor to Special Committee* BWAY Spectrum Brands,

Inc.* Advisor to the Special Committee of BWAY in the context of its $915m acquisition by Madison Dearborn Capital Special Committee Advisor on $675mm combination with Russell Hobbs, Inc. Advisor to Special Committee* Advisor to Special

Committee Select Special Committee & BoD advisory mandates Panavision * Advisor to the Special Committee of Panavision on the acquisition of the remaining stock by MacAndrews & Forbes Holding Advisor to Special Committee GCR

International Shipping Corp. Possible going-private proposed by direct competitor Advisor to Special Committee* AMC Entertainment Going-private transaction initiated by controlling stockholder Advisor to Special

Committee* OSG Going-private transaction initiated by majority equity holder Advisor to Special Committee* Panavision * Advisor to the Special Committee of the Board of Directors of Panavision in two transactions involving the controlling

shareholder (MacAndres & Forbes) Advisor to Special Committee Tele-Communications, Inc.* Advisor to TCI on $69bn sale to AT&T Advisor to Special Committee Clearlake STG $7.7bn take-private acquisition of Dun &

Bradstreet ~$1.4bn acquisition of Avid Technology by STG 2025 2023 Note: 1. Pending transaction Cision Solera ~$2.7bn sale of Cision ~$6.5bn sale of Solera to Platinum Equity to Vista Equity Partners 2020 2019 Trusted advisor for

public company M&A Paramount Global Advisor to Paramount Global on its $28bn+ merger with Skydance Media1 Current Rio Tinto $2.7bn proposal for 49% of Turquoise Hill Resources Financial Advisor to Ro Tinto Apollo Global $7.1bn

acquisition of Tenneco 2023 Meridian Bioscience $1.5 billion all-cash sale to SDB Biosensor and SJL Partners 2022 Veoneer $4.5bn sale to Qualcomm 2022 Cornerstone / Clearlake Builders FirstSource $7.0bn merger with ~$5.2bn

acquisition of BMC Stock Holdings Cornerstone OnDemand 2021 2021 1. ROTHSCHILD & CO QUALIFICATIONS 9

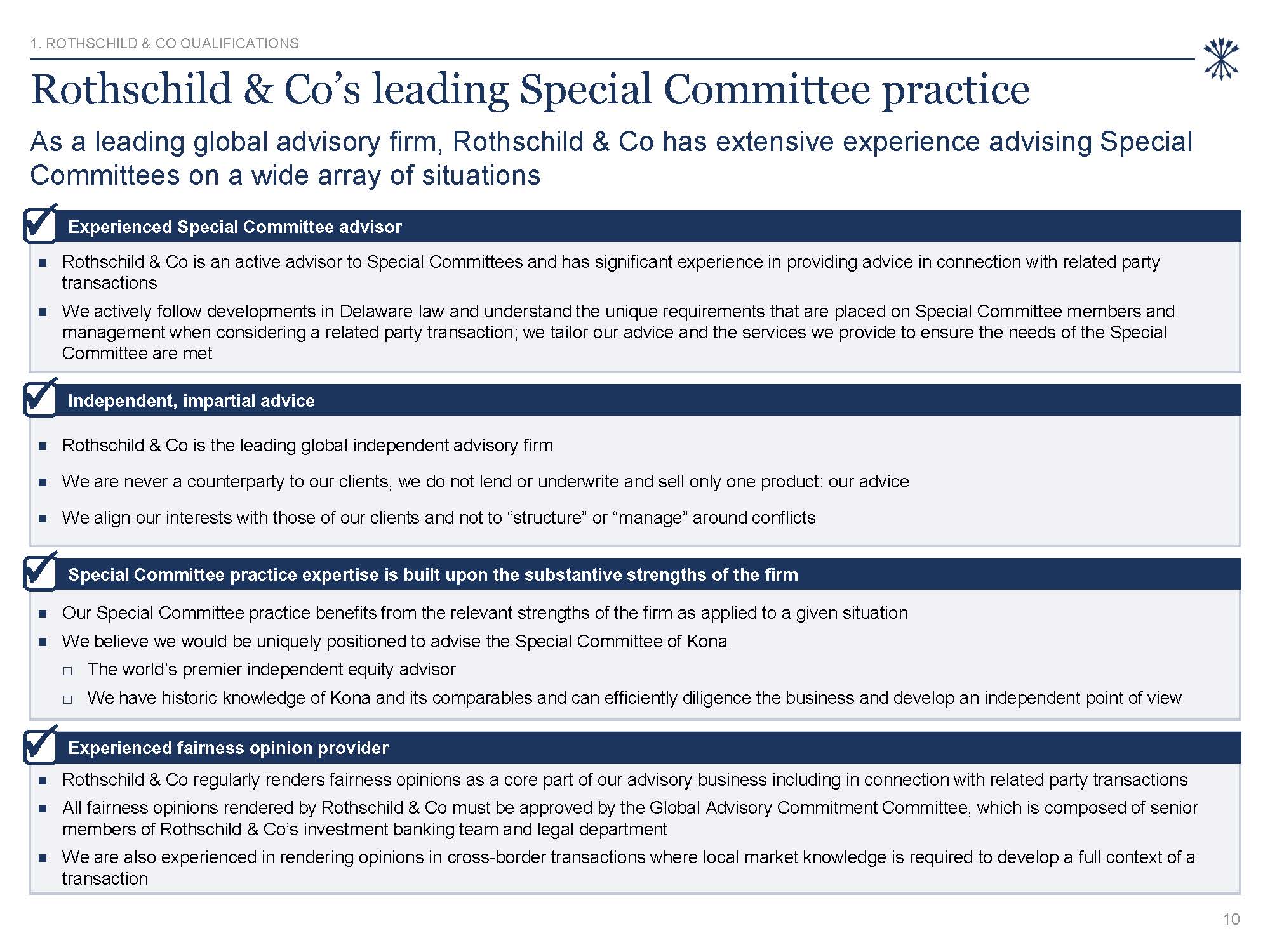

Rothschild & Co’s leading Special Committee practice Rothschild & Co is

an active advisor to Special Committees and has significant experience in providing advice in connection with related party transactions We actively follow developments in Delaware law and understand the unique requirements that are placed on

Special Committee members and management when considering a related party transaction; we tailor our advice and the services we provide to ensure the needs of the Special Committee are met Rothschild & Co is the leading global independent

advisory firm We are never a counterparty to our clients, we do not lend or underwrite and sell only one product: our advice We align our interests with those of our clients and not to “structure” or “manage” around conflicts Our Special

Committee practice benefits from the relevant strengths of the firm as applied to a given situation We believe we would be uniquely positioned to advise the Special Committee of Kona The world’s premier independent equity advisor We have

historic knowledge of Kona and its comparables and can efficiently diligence the business and develop an independent point of view Rothschild & Co regularly renders fairness opinions as a core part of our advisory business including in

connection with related party transactions All fairness opinions rendered by Rothschild & Co must be approved by the Global Advisory Commitment Committee, which is composed of senior members of Rothschild & Co’s investment banking team

and legal department We are also experienced in rendering opinions in cross-border transactions where local market knowledge is required to develop a full context of a transaction Long established global presence – 200+ year history As a

leading global advisory firm, Rothschild & Co has extensive experience advising Special Committees on a wide array of situations Experienced Special Committee advisor Experienced fairness opinion provider Special Committee practice

expertise is built upon the substantive strengths of the firm Independent, impartial advice 1. ROTHSCHILD & CO QUALIFICATIONS 10

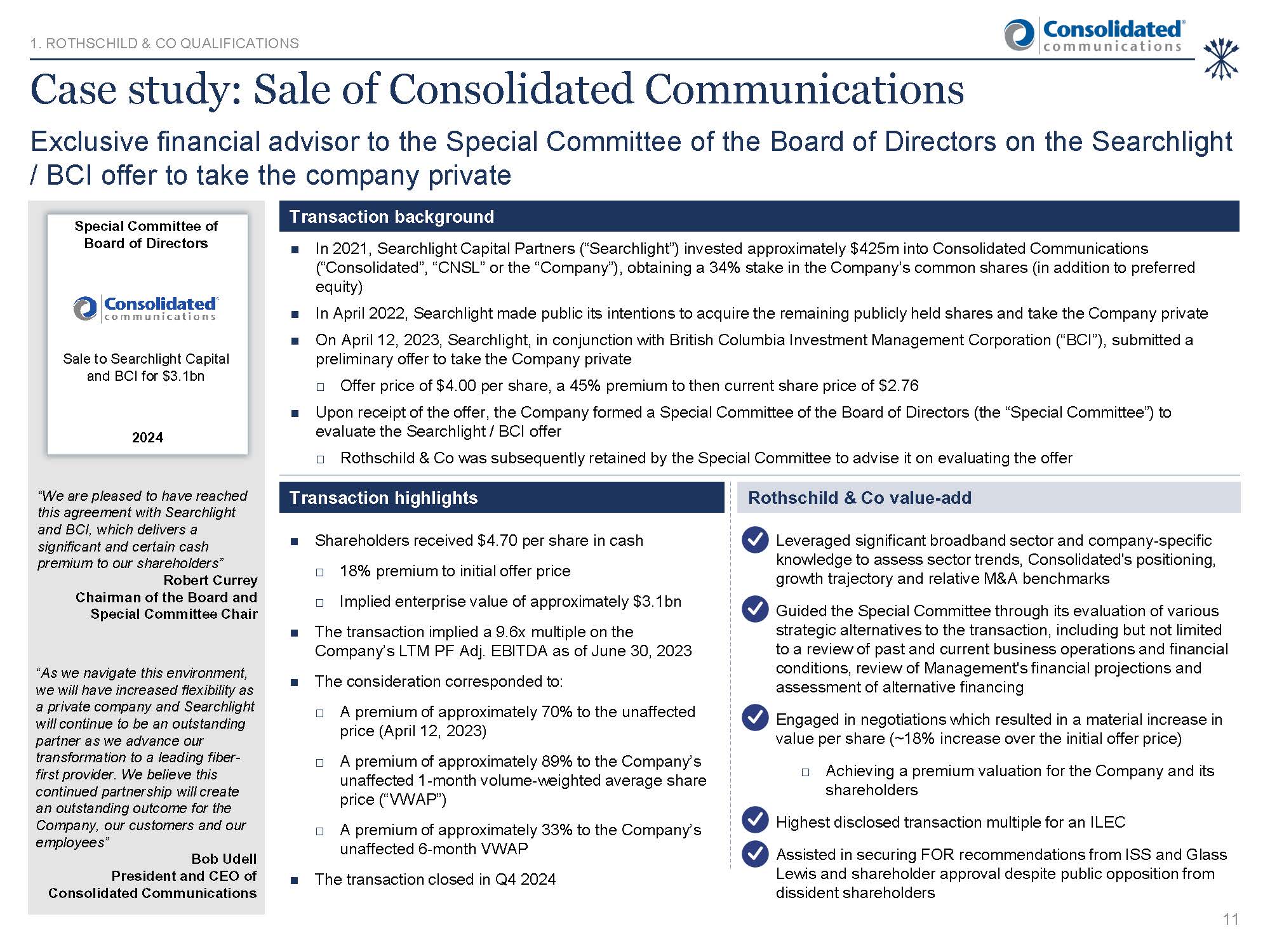

Case study: Sale of Consolidated Communications Exclusive financial advisor to

the Special Committee of the Board of Directors on the Searchlight / BCI offer to take the company private Transaction background Transaction highlights Shareholders received $4.70 per share in cash 18% premium to initial offer

price Implied enterprise value of approximately $3.1bn The transaction implied a 9.6x multiple on the Company’s LTM PF Adj. EBITDA as of June 30, 2023 The consideration corresponded to: A premium of approximately 70% to the unaffected

price (April 12, 2023) A premium of approximately 89% to the Company’s unaffected 1-month volume-weighted average share price (“VWAP”) A premium of approximately 33% to the Company’s unaffected 6-month VWAP The transaction closed in Q4

2024 In 2021, Searchlight Capital Partners (“Searchlight”) invested approximately $425m into Consolidated Communications (“Consolidated”, “CNSL” or the “Company”), obtaining a 34% stake in the Company’s common shares (in addition to preferred

equity) In April 2022, Searchlight made public its intentions to acquire the remaining publicly held shares and take the Company private On April 12, 2023, Searchlight, in conjunction with British Columbia Investment Management Corporation

(“BCI”), submitted a preliminary offer to take the Company private Offer price of $4.00 per share, a 45% premium to then current share price of $2.76 Upon receipt of the offer, the Company formed a Special Committee of the Board of Directors

(the “Special Committee”) to evaluate the Searchlight / BCI offer Rothschild & Co was subsequently retained by the Special Committee to advise it on evaluating the offer Rothschild & Co value-add Special Committee of Board of

Directors Sale to Searchlight Capital and BCI for $3.1bn 2024 “We are pleased to have reached this agreement with Searchlight and BCI, which delivers a significant and certain cash premium to our shareholders” Robert Currey Chairman of the

Board and Special Committee Chair “As we navigate this environment, we will have increased flexibility as a private company and Searchlight will continue to be an outstanding partner as we advance our transformation to a leading fiber-first

provider. We believe this continued partnership will create an outstanding outcome for the Company, our customers and our employees” Bob Udell President and CEO of Consolidated Communications Leveraged significant broadband sector and

company-specific knowledge to assess sector trends, Consolidated's positioning, growth trajectory and relative M&A benchmarks Guided the Special Committee through its evaluation of various strategic alternatives to the transaction,

including but not limited to a review of past and current business operations and financial conditions, review of Management's financial projections and assessment of alternative financing Engaged in negotiations which resulted in a material

increase in value per share (~18% increase over the initial offer price) Achieving a premium valuation for the Company and its shareholders Highest disclosed transaction multiple for an ILEC Assisted in securing FOR recommendations from ISS

and Glass Lewis and shareholder approval despite public opposition from dissident shareholders 11 1. ROTHSCHILD & CO QUALIFICATIONS

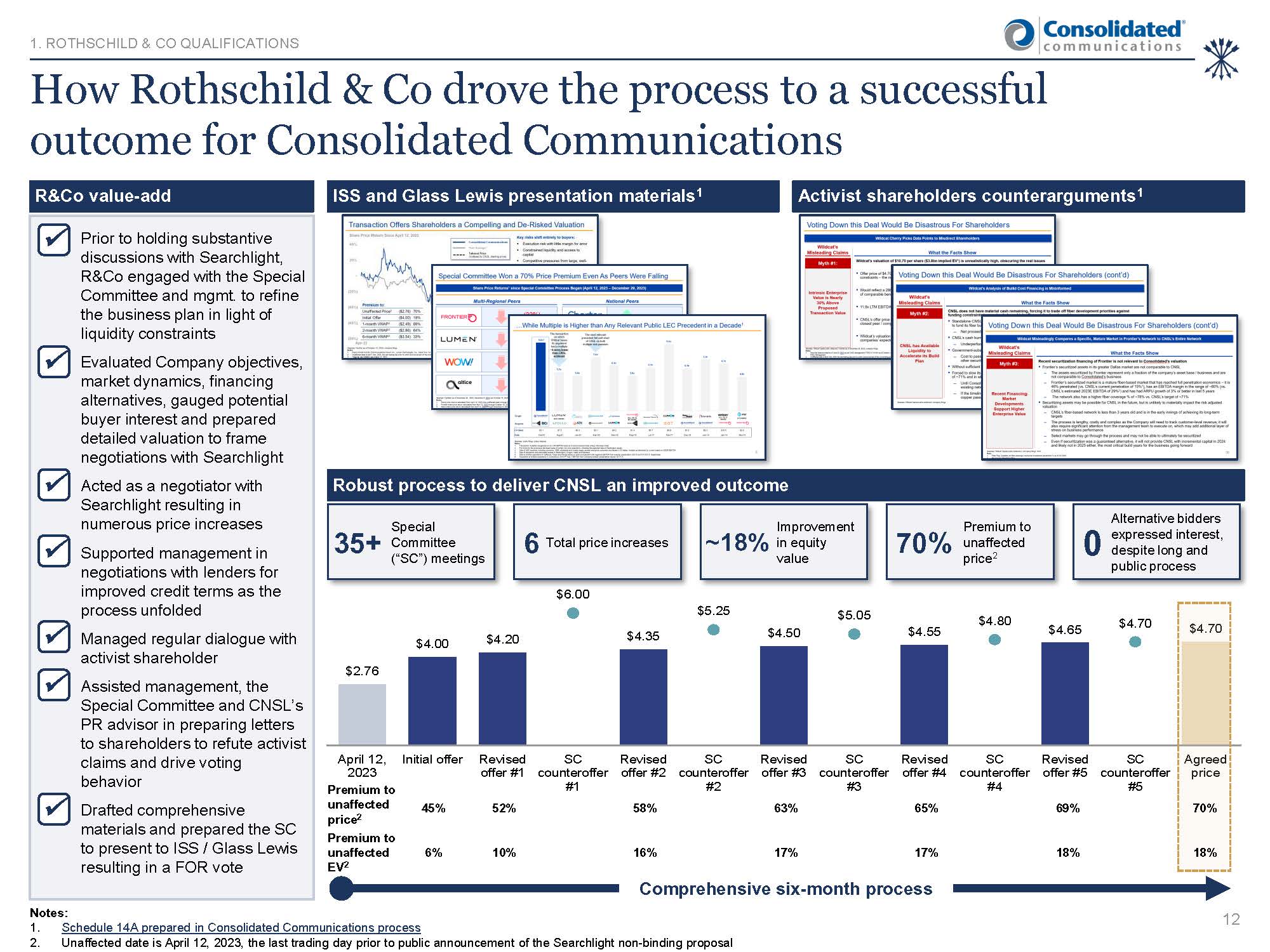

$2.76 $4.00 $4.20 $4.35 $4.50 $4.55 $4.65 $6.00 $5.25 $5.05 $4.80 $4.70 How

Rothschild & Co drove the process to a successful outcome for Consolidated Communications Prior to holding substantive discussions with Searchlight, R&Co engaged with the Special Committee and mgmt. to refine the business plan in light

of liquidity constraints Evaluated Company objectives, market dynamics, financing alternatives, gauged potential buyer interest and prepared detailed valuation to frame negotiations with Searchlight Acted as a negotiator with Searchlight

resulting in numerous price increases Supported management in negotiations with lenders for improved credit terms as the process unfolded Managed regular dialogue with activist shareholder Assisted management, the Special Committee and

CNSL’s PR advisor in preparing letters to shareholders to refute activist claims and drive voting behavior Drafted comprehensive materials and prepared the SC to present to ISS / Glass Lewis resulting in a FOR vote ISS and Glass Lewis

presentation materials1 Activist shareholders counterarguments1 Comprehensive six-month process Robust process to deliver CNSL an improved outcome Special 35+ Committee (“SC”) meetings 6 Total price increases Improvement ~18% in

equity value Premium to 70% unaffected price2 Alternative bidders 0 despite long and expressed interest, public process $4.70 April 12, Initial

offer Revised SC Revised SC Revised SC Revised SC Revised SC Agreed 2023 offer #1 counteroffer offer #2 counteroffer offer #3 counteroffer offer #4 counteroffer offer #5 counteroffer price Premium to unaffected

price2 45% 52% #1 58% #2 63% #3 65% #4 69% #5 70% Premium to unaffected EV2 6% 10% 16% 17% 17% 18% 18% R&Co value-add Notes: Schedule 14A prepared in Consolidated Communications process Unaffected date is April 12,

2023, the last trading day prior to public announcement of the Searchlight non-binding proposal 1. ROTHSCHILD & CO QUALIFICATIONS 12

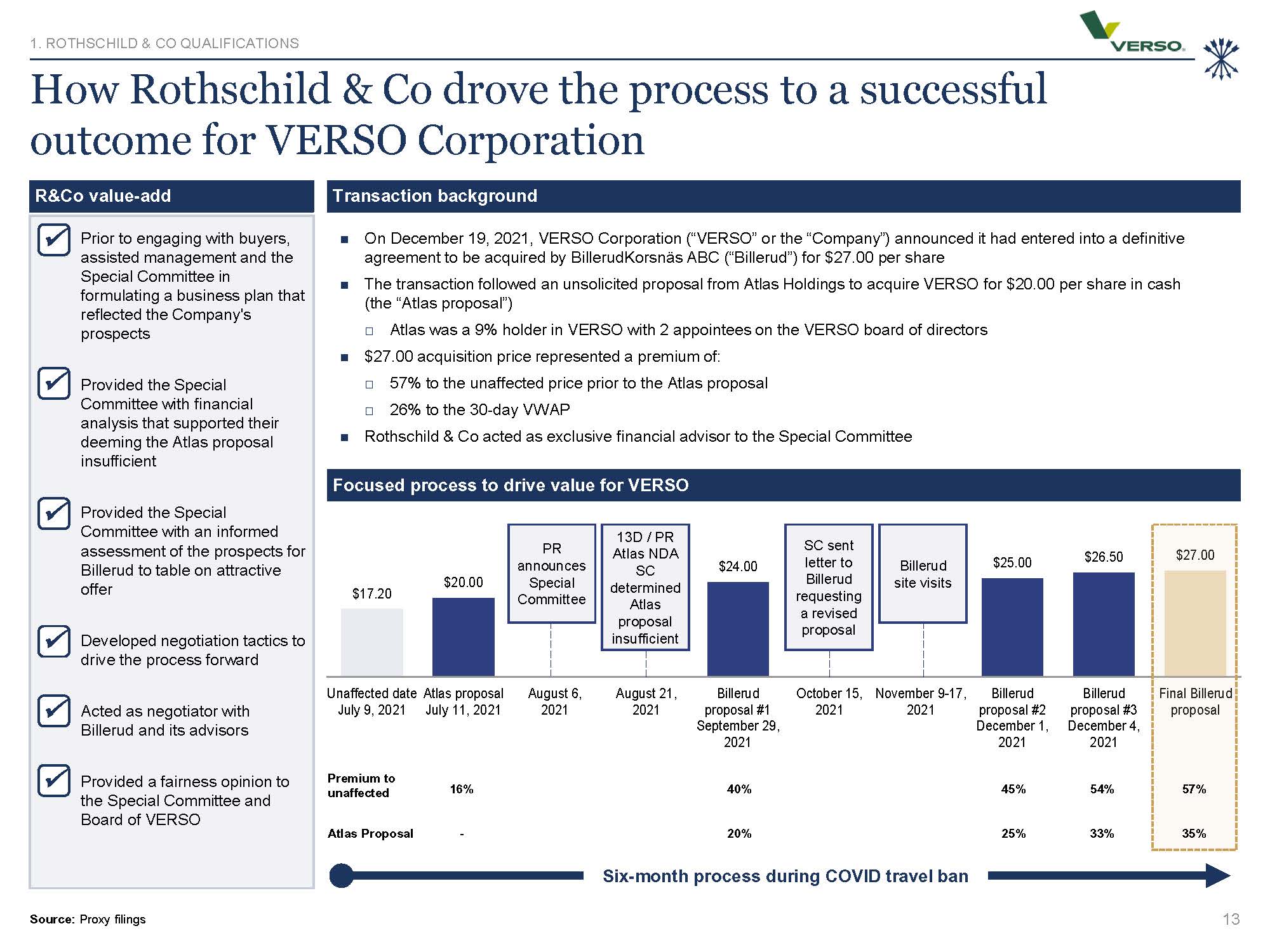

$17.20 $20.00 $24.00 $25.00 $26.50 $27.00 Unaffected date Atlas proposal

July 9, 2021 July 11, 2021 August 6, August 21, 2021 2021 September 29, 2021 Billerud October 15, November 9-17, proposal #1 2021 2021 Billerud proposal #2 December 1, 2021 Billerud proposal #3 December 4, 2021 Final Billerud

proposal PR announces Special Committee On December 19, 2021, VERSO Corporation (“VERSO” or the “Company”) announced it had entered into a definitive agreement to be acquired by BillerudKorsnäs ABC (“Billerud”) for $27.00 per share The

transaction followed an unsolicited proposal from Atlas Holdings to acquire VERSO for $20.00 per share in cash (the “Atlas proposal”) Atlas was a 9% holder in VERSO with 2 appointees on the VERSO board of directors $27.00 acquisition price

represented a premium of: 57% to the unaffected price prior to the Atlas proposal 26% to the 30-day VWAP Rothschild & Co acted as exclusive financial advisor to the Special Committee 13D / PR Atlas NDA SC determined Atlas proposal

insufficient How Rothschild & Co drove the process to a successful outcome for VERSO Corporation Source: Proxy filings R&Co value-add Prior to engaging with buyers, assisted management and the Special Committee in formulating a

business plan that reflected the Company's prospects Provided the Special Committee with financial analysis that supported their deeming the Atlas proposal insufficient Provided the Special Committee with an informed assessment of the

prospects for Billerud to table on attractive offer Developed negotiation tactics to drive the process forward Acted as negotiator with Billerud and its advisors Provided a fairness opinion to the Special Committee and Board of

VERSO Transaction background Focused process to drive value for VERSO Six-month process during COVID travel ban Premium to unaffected 16% 40% 45% 54% 57% Atlas Proposal - 20% 25% 33% 35% SC sent letter to Billerud requesting a

revised proposal Billerud site visits 1. ROTHSCHILD & CO QUALIFICATIONS 13

2 Executive summary

Preliminary thoughts on Kona’s situation Samoa looks to have followed a playbook

with Kona similar to that used with CNSL (and other distressed public company situations) Rescue preferred investment with material common ownership Portable capital structure and blocking rights on new capital position for a high probability

take-private Deep integration with management to drive strategy in direction they desire post take-private Simply getting repaid on its preferred is a suboptimal outcome for Samoa Initial capital deployment below target size for a Samoa

investment ($153m on a $4bn fund) Significant time / attention invested in Kona business from Samoa team to date 13% per annum preferred coupon plus value of warrants only hits typical Samoa return targets at significant premium to current

stock price Long dated maturity (2033) with no ability to accelerate liquidity limits Samoa options outside of a take-private In December 2024, Samoa filed an amended Schedule 13D indicating it may seek to acquire all of Kona’s outstanding

shares; Samoa has a strong incentive to succeed in its effort to take Kona private Allows topping up investment to typical Samoa levels Ability to reposition Kona outside the eye of public markets Provides full control of outcome /

timing Unlocks ability to generate Samoa level returns However, Kona’s recent operational / financial improvements give it options Attractive business to short list of high-probability, motivated buyers Synergy potential unlocks value that

Samoa cannot capture Samoa does have certain structural advantages Samoa can roll the existing capital structure and require a third-party to refinance its preferred Preferred make-whole starting in November 2025 materially increases

obligation for third-party buyer In partnership with Amelia, they control ~37% of diluted common shares which creates a challenge to an alternate buyer obtaining >50% of the shareholder vote Key to driving to best outcome for Kona

shareholders is creating viability of alternatives Support that standalone business plan will generate greater risk adjusted value Near-term process to surface real alternative interest in the business inside of minimum return threshold

beginning in November 2025 Willingness to push Samoa to maximum “ability to pay” 3 2 1 4 5 6 2. EXECUTIVE SUMMARY 15

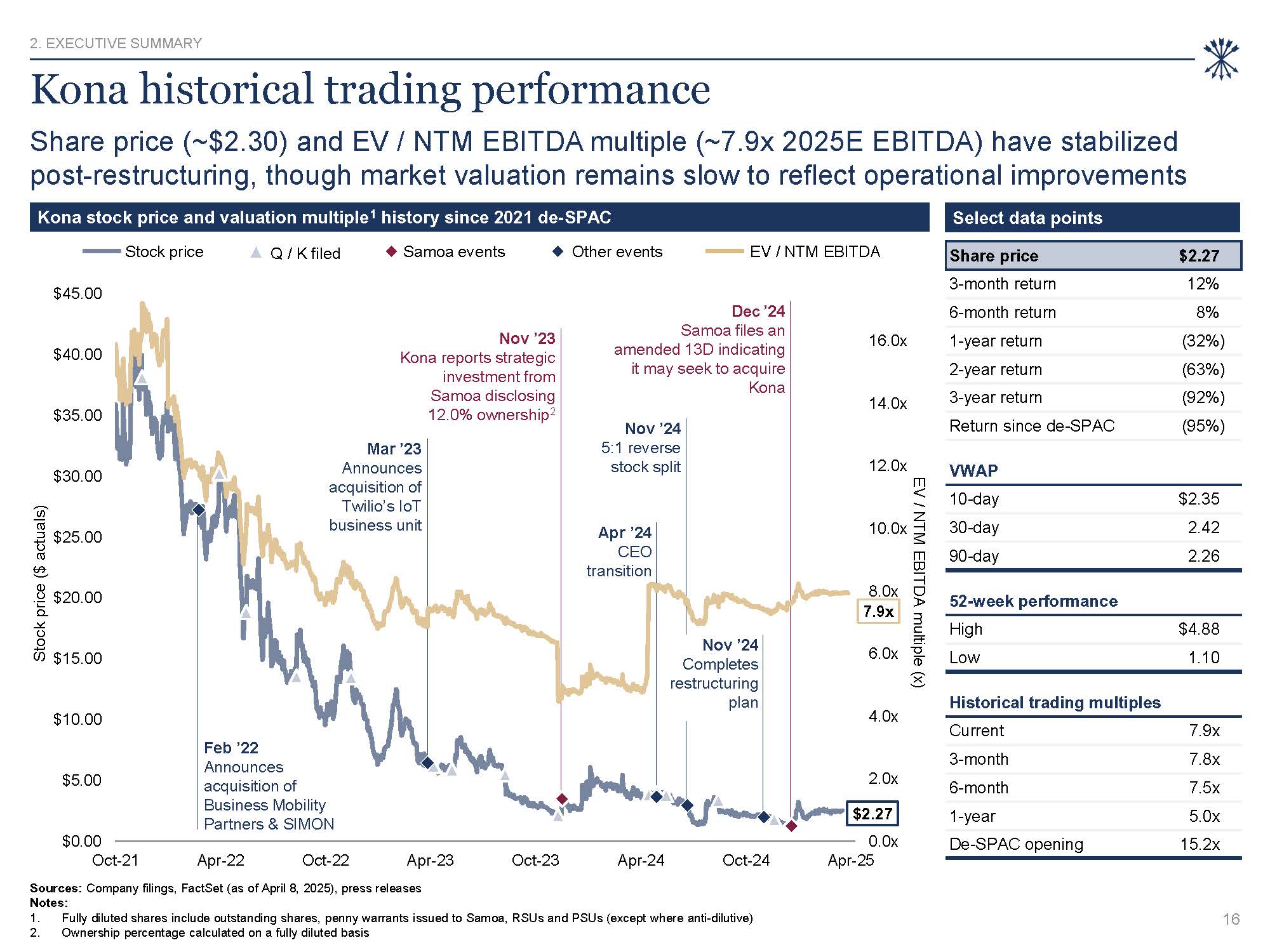

Nov ’24 5:1 reverse stock split Nov ’24 Completes restructuring plan Kona

historical trading performance Share price (~$2.30) and EV / NTM EBITDA multiple (~7.9x 2025E EBITDA) have stabilized post-restructuring, though market valuation remains slow to reflect operational improvements Sources: Company filings,

FactSet (as of April 8, 2025), press releases Notes: Fully diluted shares include outstanding shares, penny warrants issued to Samoa, RSUs and PSUs (except where anti-dilutive) Ownership percentage calculated on a fully diluted basis Kona

stock price and valuation multiple1 history since 2021 de-SPAC Stock price ($ actuals) EV / NTM EBITDA multiple (x) Select data points Nov ’23 Kona reports strategic investment from Samoa disclosing 12.0% ownership2 Dec ’24 Samoa files an

amended 13D indicating it may seek to acquire Kona Apr ’24 CEO transition Feb ’22 Announces acquisition of Business Mobility Partners & SIMON Mar ’23 Announces acquisition of Twilio’s IoT business unit Stock price Q / K filed Samoa

events Other events EV / NTM EBITDA Share price $2.27 3-month return 12% 3-year return (92%) Return since de-SPAC (95%) VWAP 10-day $2.35 30-day 2.42 90-day 2.26 52-week performance High $4.88 Low 1.10 Historical trading

multiples Current 7.9x 3-month 7.8x 6-month 7.5x 1-year 5.0x De-SPAC opening 15.2x $2.27 0.0x 2.0x 4.0x 6.0x 8.0x 7.9x 10.0x 12.0x 14.0x 6-month return 8% 16.0x 1-year return (32%) 2-year

return (63%) $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 Oct-21 Apr-22 Oct-22 Apr-23 Oct-23 Apr-24 Oct-24 Apr-25 2. EXECUTIVE SUMMARY 16

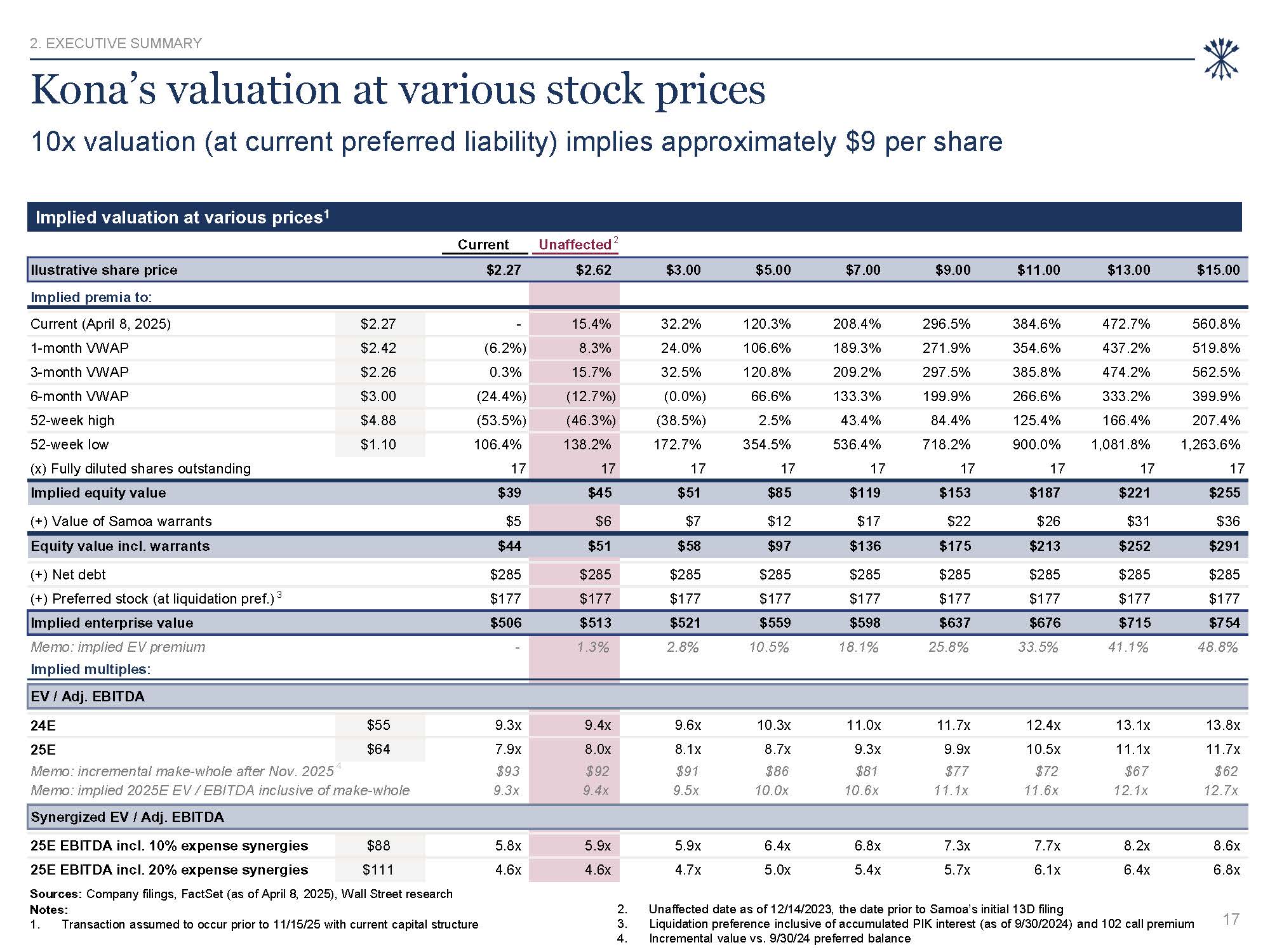

Ilustrative share

price $2.27 $2.62 $3.00 $5.00 $7.00 $9.00 $11.00 $13.00 $15.00 Implied premia to: Current (April 8, 2025) $2.27 - 15.4% 32.2% 120.3% 208.4% 296.5% 384.6% 472.7% 560.8% 1-month

VWAP $2.42 (6.2%) 8.3% 24.0% 106.6% 189.3% 271.9% 354.6% 437.2% 519.8% 3-month VWAP $2.26 0.3% 15.7% 32.5% 120.8% 209.2% 297.5% 385.8% 474.2% 562.5% 6-month

VWAP $3.00 (24.4%) (12.7%) (0.0%) 66.6% 133.3% 199.9% 266.6% 333.2% 399.9% 52-week high $4.88 (53.5%) (46.3%) (38.5%) 2.5% 43.4% 84.4% 125.4% 166.4% 207.4% 52-week

low $1.10 106.4% 138.2% 172.7% 354.5% 536.4% 718.2% 900.0% 1,081.8% 1,263.6% (x) Fully diluted shares outstanding 17 17 17 17 17 17 17 17 17 Implied equity value $39 $45 $51 $85 $119 $153 $187 $221 $255 (+) Value

of Samoa warrants $5 $6 $7 $12 $17 $22 $26 $31 $36 Equity value incl. warrants $44 $51 $58 $97 $136 $175 $213 $252 $291 25E EBITDA incl. 10% expense synergies $88 5.8x 5.9x 5.9x 6.4x 6.8x 7.3x 7.7x 8.2x 8.6x 25E

EBITDA incl. 20% expense synergies $111 4.6x 4.6x 4.7x 5.0x 5.4x 5.7x 6.1x 6.4x 6.8x (+) Net debt $285 $285 $285 $285 $285 $285 $285 $285 $285 (+) Preferred stock (at liquidation pref.)

3 $177 $177 $177 $177 $177 $177 $177 $177 $177 Implied enterprise value $506 $513 $521 $559 $598 $637 $676 $715 $754 Memo: implied EV premium Implied multiples: - 1.3% 2.8% 10.5% 18.1% 25.8% 33.5% 41.1% 48.8% EV /

Adj. EBITDA 24E $55 9.3x 9.4x 9.6x 10.3x 11.0x 11.7x 12.4x 13.1x 13.8x 25E $64 7.9x 8.0x 8.1x 8.7x 9.3x 9.9x 10.5x 11.1x 11.7x Memo: incremental make-whole after Nov. 2025 4 Memo: implied 2025E EV / EBITDA inclusive of

make-whole $93 9.3x $92 9.4x $91 9.5x $86 10.0x $81 10.6x $77 11.1x $72 11.6x $67 12.1x $62 12.7x Synergized EV / Adj. EBITDA Current Unaffected 2 Kona’s valuation at various stock prices 10x valuation (at current preferred

liability) implies approximately $9 per share Sources: Company filings, FactSet (as of April 8, 2025), Wall Street research Notes: 1. Transaction assumed to occur prior to 11/15/25 with current capital structure Unaffected date as of

12/14/2023, the date prior to Samoa’s initial 13D filing Liquidation preference inclusive of accumulated PIK interest (as of 9/30/2024) and 102 call premium Incremental value vs. 9/30/24 preferred balance Implied valuation at various

prices1 2. EXECUTIVE SUMMARY 17

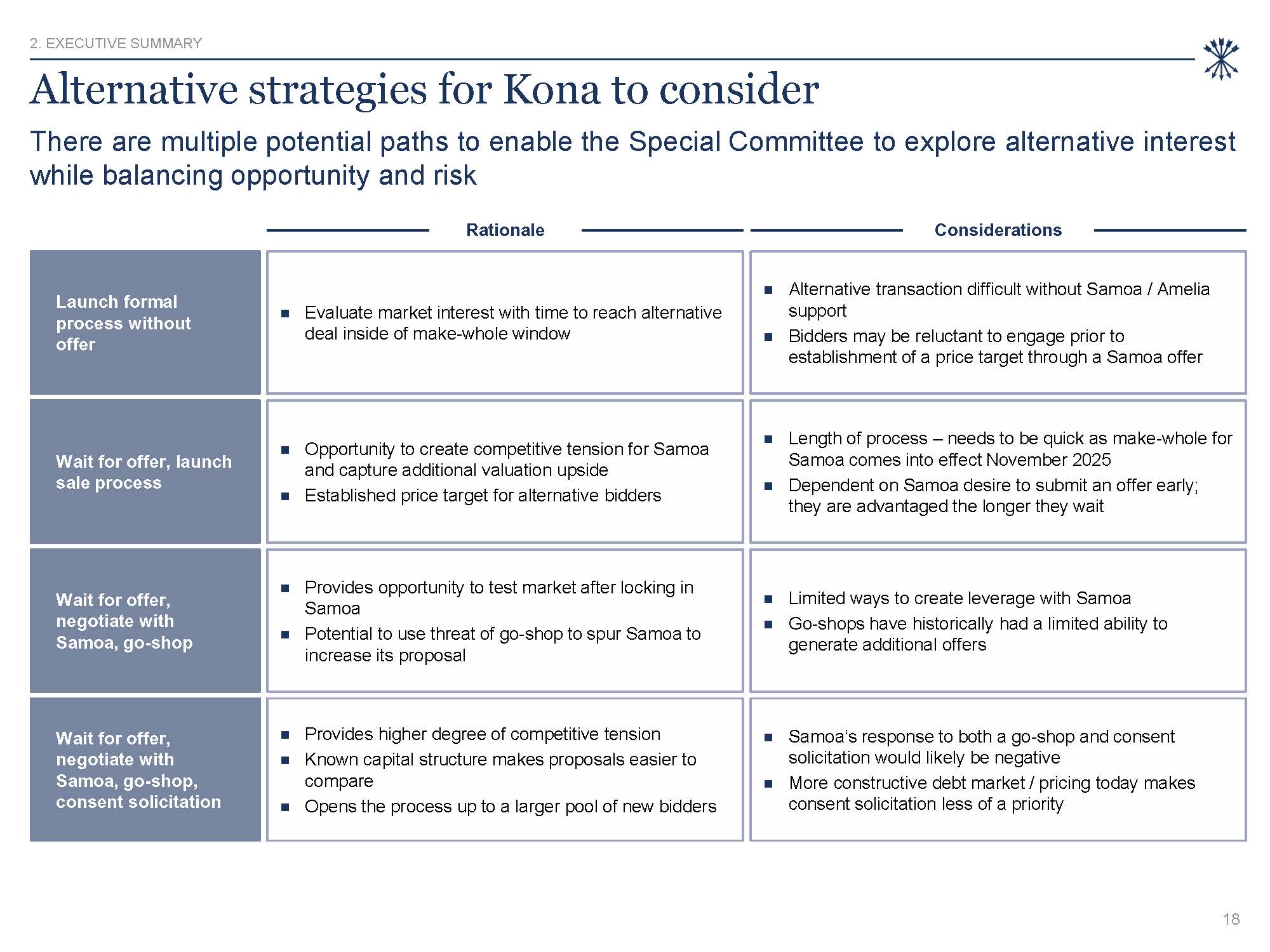

Alternative strategies for Kona to consider There are multiple potential paths to

enable the Special Committee to explore alternative interest while balancing opportunity and risk Rationale Considerations Launch formal process without offer Wait for offer, launch sale process Wait for offer, negotiate with Samoa,

go-shop Wait for offer, negotiate with Samoa, go-shop, consent solicitation Evaluate market interest with time to reach alternative deal inside of make-whole window Alternative transaction difficult without Samoa / Amelia support Bidders

may be reluctant to engage prior to establishment of a price target through a Samoa offer Provides opportunity to test market after locking in Samoa Potential to use threat of go-shop to spur Samoa to increase its proposal Limited ways to

create leverage with Samoa Go-shops have historically had a limited ability to generate additional offers Provides higher degree of competitive tension Known capital structure makes proposals easier to compare Opens the process up to a

larger pool of new bidders Samoa’s response to both a go-shop and consent solicitation would likely be negative More constructive debt market / pricing today makes consent solicitation less of a priority Opportunity to create competitive

tension for Samoa and capture additional valuation upside Established price target for alternative bidders Length of process – needs to be quick as make-whole for Samoa comes into effect November 2025 Dependent on Samoa desire to submit an

offer early; they are advantaged the longer they wait 2. EXECUTIVE SUMMARY 18

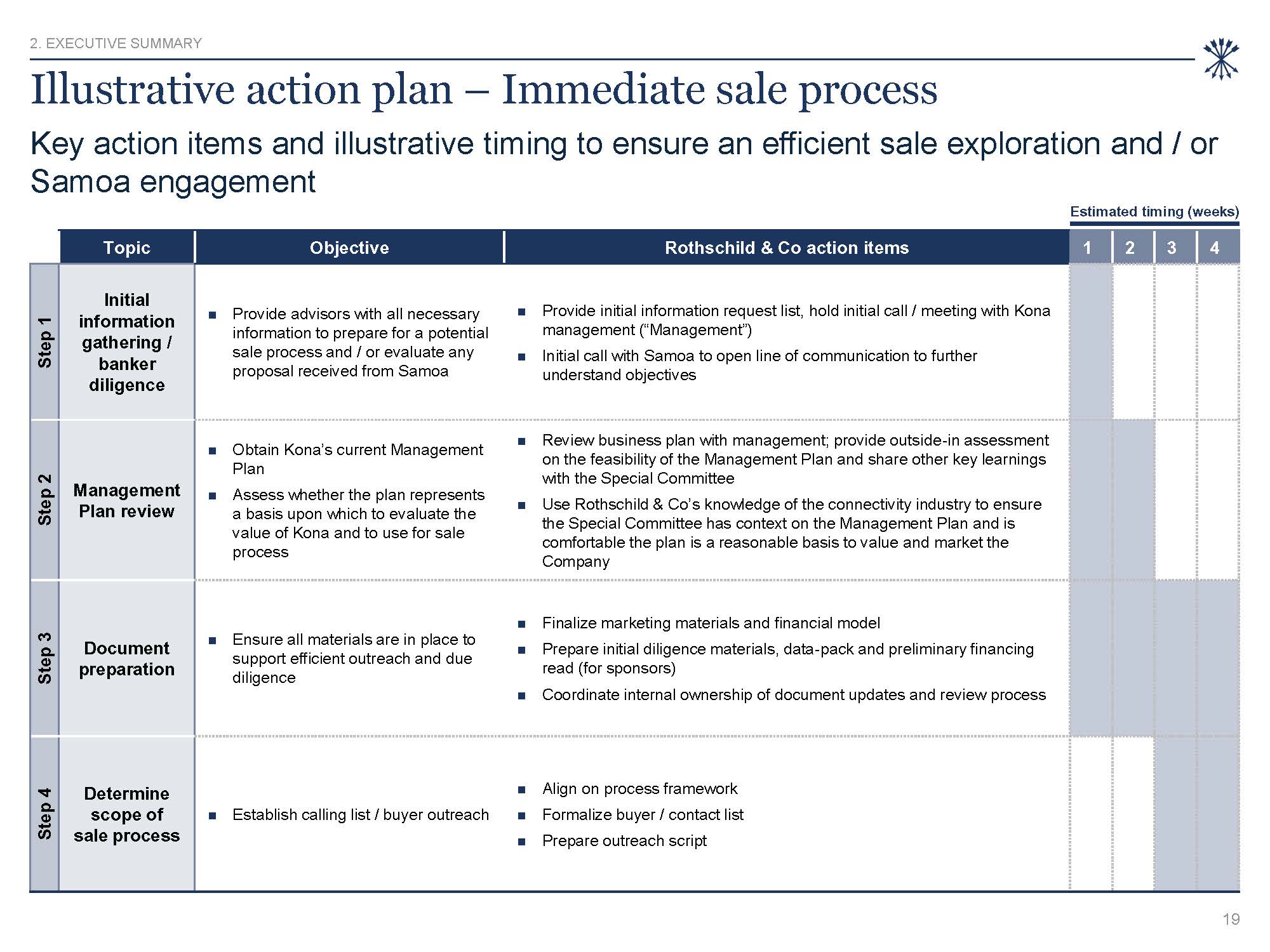

Illustrative action plan – Immediate sale process Key action items and

illustrative timing to ensure an efficient sale exploration and / or Samoa engagement Estimated timing (weeks) Topic Objective Rothschild & Co action items 1 2 3 4 Step 1 Initial information gathering / banker diligence Provide

advisors with all necessary information to prepare for a potential sale process and / or evaluate any proposal received from Samoa Provide initial information request list, hold initial call / meeting with Kona management

(“Management”) Initial call with Samoa to open line of communication to further understand objectives Step 2 Management Plan review Obtain Kona’s current Management Plan Assess whether the plan represents a basis upon which to evaluate the

value of Kona and to use for sale process Review business plan with management; provide outside-in assessment on the feasibility of the Management Plan and share other key learnings with the Special Committee Use Rothschild & Co’s

knowledge of the connectivity industry to ensure the Special Committee has context on the Management Plan and is comfortable the plan is a reasonable basis to value and market the Company Step 3 Document preparation Ensure all materials are

in place to support efficient outreach and due diligence Finalize marketing materials and financial model Prepare initial diligence materials, data-pack and preliminary financing read (for sponsors) Coordinate internal ownership of document

updates and review process Step 4 Determine scope of sale process Establish calling list / buyer outreach Align on process framework Formalize buyer / contact list Prepare outreach script 2. EXECUTIVE SUMMARY 19

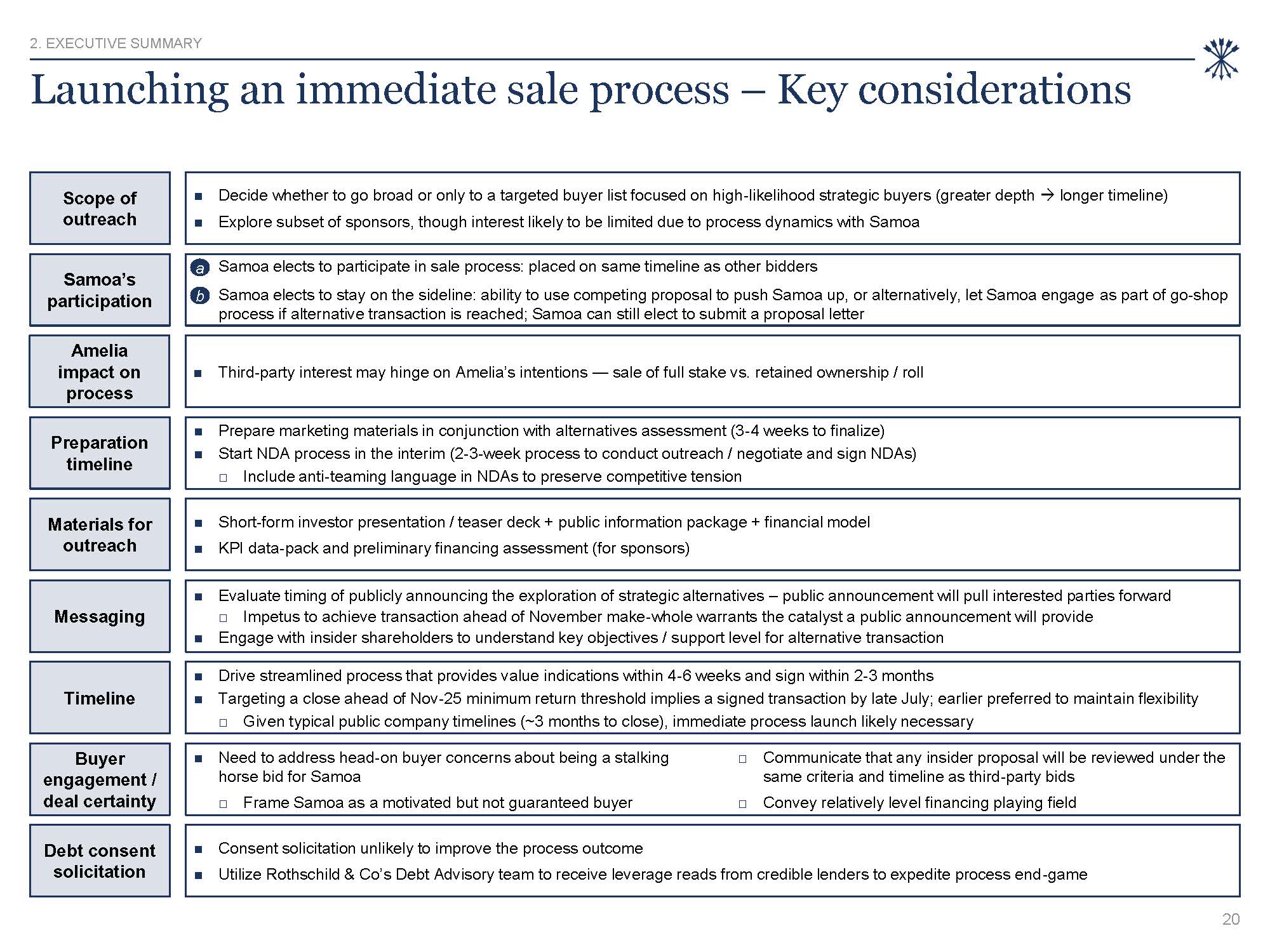

Launching an immediate sale process – Key considerations Decide whether to go

broad or only to a targeted buyer list focused on high-likelihood strategic buyers (greater depth → longer timeline) Explore subset of sponsors, though interest likely to be limited due to process dynamics with Samoa Scope

of outreach Short-form investor presentation / teaser deck + public information package + financial model KPI data-pack and preliminary financing assessment (for sponsors) Preparation timeline Drive streamlined process that provides value

indications within 4-6 weeks and sign within 2-3 months Targeting a close ahead of Nov-25 minimum return threshold implies a signed transaction by late July; earlier preferred to maintain flexibility □ Given typical public company timelines

(~3 months to close), immediate process launch likely necessary Buyer engagement / deal certainty Consent solicitation unlikely to improve the process outcome Utilize Rothschild & Co’s Debt Advisory team to receive leverage reads from

credible lenders to expedite process end-game Debt consent solicitation Samoa’s participation a Samoa elects to participate in sale process: placed on same timeline as other bidders b Samoa elects to stay on the sideline: ability to use

competing proposal to push Samoa up, or alternatively, let Samoa engage as part of go-shop process if alternative transaction is reached; Samoa can still elect to submit a proposal letter Evaluate timing of publicly announcing the exploration

of strategic alternatives – public announcement will pull interested parties forward □ Impetus to achieve transaction ahead of November make-whole warrants the catalyst a public announcement will provide Engage with insider shareholders to

understand key objectives / support level for alternative transaction Messaging Materials for outreach Timeline Prepare marketing materials in conjunction with alternatives assessment (3-4 weeks to finalize) Start NDA process in the

interim (2-3-week process to conduct outreach / negotiate and sign NDAs) □ Include anti-teaming language in NDAs to preserve competitive tension Need to address head-on buyer concerns about being a stalking horse bid for Samoa □ Frame Samoa

as a motivated but not guaranteed buyer Communicate that any insider proposal will be reviewed under the same criteria and timeline as third-party bids Convey relatively level financing playing field Amelia impact on process Third-party

interest may hinge on Amelia’s intentions — sale of full stake vs. retained ownership / roll 2. EXECUTIVE SUMMARY 20

Potential strategic buyers Rationale Potential counterparties Expands footprint

to North America Cross-sell opportunity into existing customer base Enhances enterprise offerings Global carriers IoT connectivity Expands geographic presence Cross-sell opportunity into existing customer base Expands vertical

expertise Significant synergy opportunity bringing customers on network Protection against losses for legacy revenue streams Enhances enterprise offerings North American wireless carriers Expands and / or converges wireless / fixed line

offering Protection against losses for legacy revenue streams Managed network Multiple strategic buyer categories that could be worth considering in a sale process Category Key buyer criteria 1 Capacity to complete a $600m+

acquisition 2 Familiarity and historic participation in the IoT / connectivity / networking space 3 Potential synergies 2. EXECUTIVE SUMMARY 21

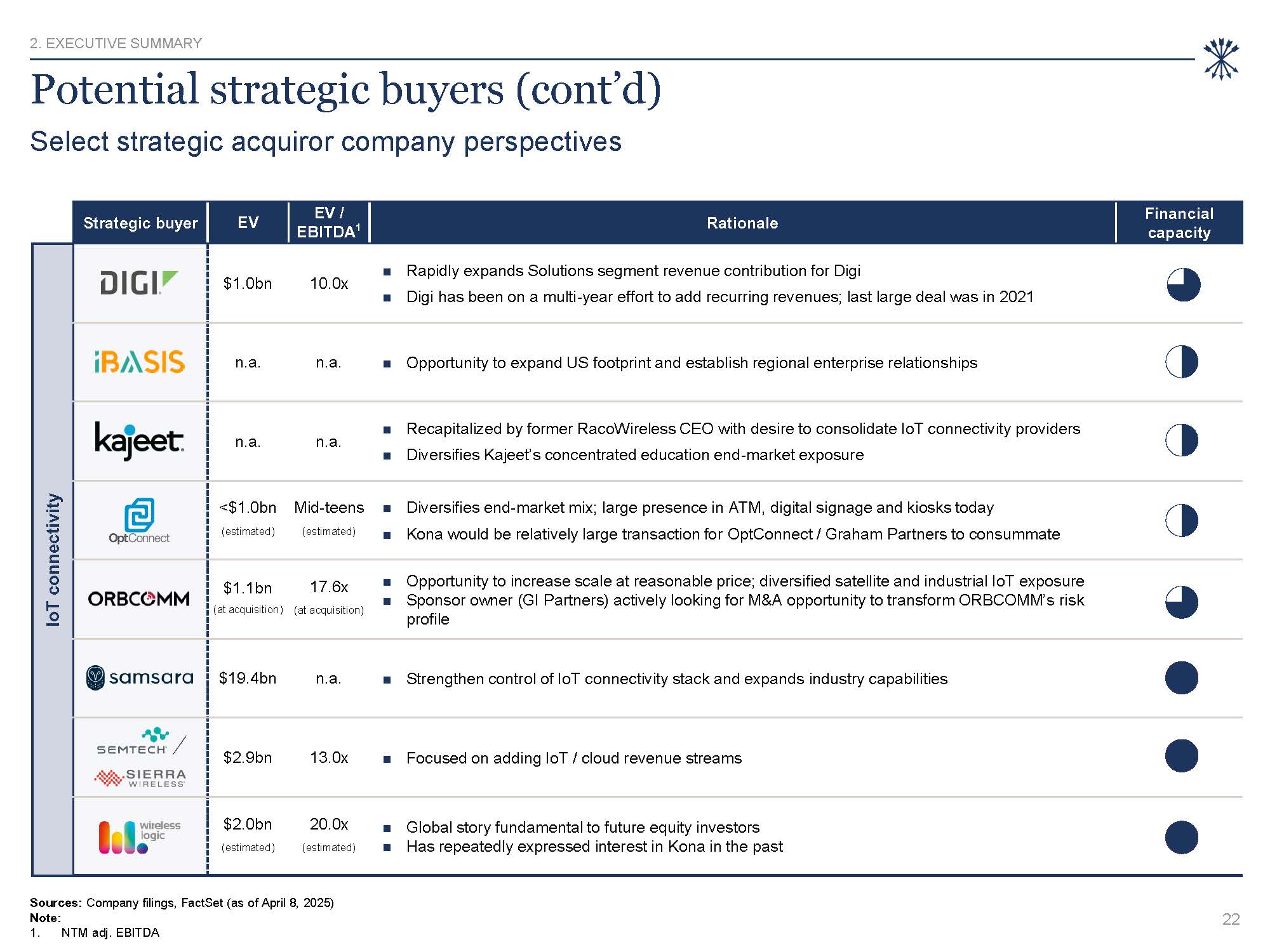

Potential strategic buyers (cont’d) Select strategic acquiror company

perspectives Strategic buyer EV EV / EBITDA1 Rationale Financial capacity IoT connectivity $1.0bn 10.0x Rapidly expands Solutions segment revenue contribution for Digi Digi has been on a multi-year effort to add recurring revenues;

last large deal was in 2021 n.a. n.a. Opportunity to expand US footprint and establish regional enterprise relationships n.a. n.a. Recapitalized by former RacoWireless CEO with desire to consolidate IoT connectivity providers Diversifies

Kajeet’s concentrated education end-market exposure <$1.0bn Mid-teens (estimated) (estimated) Diversifies end-market mix; large presence in ATM, digital signage and kiosks today Kona would be relatively large transaction for OptConnect /

Graham Partners to consummate $1.1bn 17.6x (at acquisition) (at acquisition) Opportunity to increase scale at reasonable price; diversified satellite and industrial IoT exposure Sponsor owner (GI Partners) actively looking for M&A

opportunity to transform ORBCOMM’s risk profile $19.4bn n.a. Strengthen control of IoT connectivity stack and expands industry capabilities $2.9bn 13.0x Focused on adding IoT / cloud revenue streams $2.0bn 20.0x (estimated)

(estimated) Global story fundamental to future equity investors Has repeatedly expressed interest in Kona in the past Sources: Company filings, FactSet (as of April 8, 2025) Note: 1. NTM adj. EBITDA 2. EXECUTIVE SUMMARY 22

Financial sponsors Potential financial buyers Sizable group of mid-to-large-cap

sponsors 1 Capacity to complete a $600m+ acquisition 2 Familiarity and historic participation in the IoT / connectivity / networking / IT services space Key buyer criteria 2. EXECUTIVE SUMMARY 23

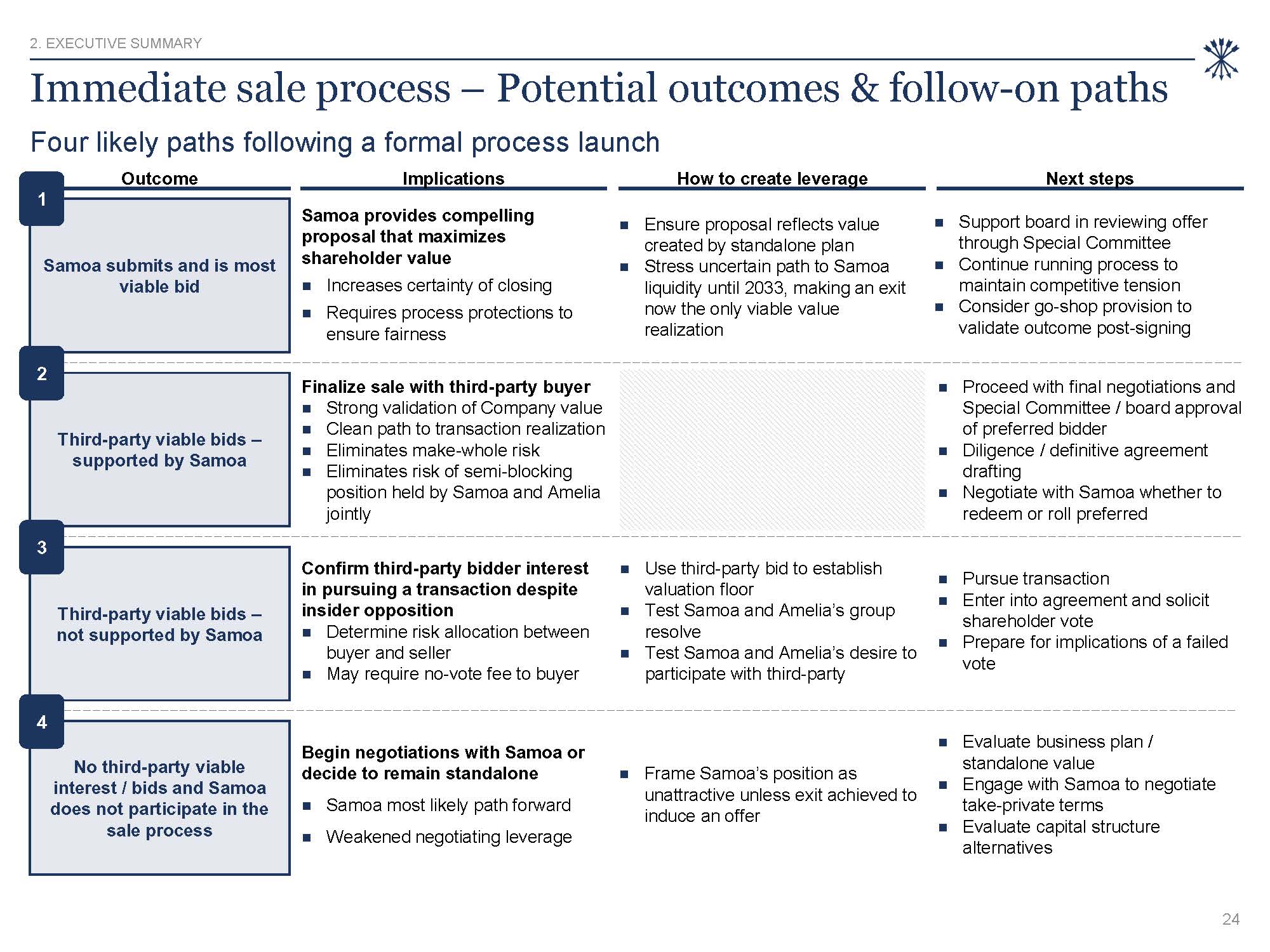

Third-party viable bids – not supported by Samoa Immediate sale process –

Potential outcomes & follow-on paths Four likely paths following a formal process launch No third-party viable interest / bids and Samoa does not participate in the sale process Third-party viable bids – supported by Samoa Begin

negotiations with Samoa or decide to remain standalone Samoa most likely path forward Weakened negotiating leverage Confirm third-party bidder interest in pursuing a transaction despite insider opposition Determine risk allocation between

buyer and seller May require no-vote fee to buyer Finalize sale with third-party buyer Strong validation of Company value Clean path to transaction realization Eliminates make-whole risk Eliminates risk of semi-blocking position held by

Samoa and Amelia jointly Evaluate business plan / standalone value Engage with Samoa to negotiate take-private terms Evaluate capital structure alternatives Pursue transaction Enter into agreement and solicit shareholder vote Prepare for

implications of a failed vote Proceed with final negotiations and Special Committee / board approval of preferred bidder Diligence / definitive agreement drafting Negotiate with Samoa whether to redeem or roll preferred Frame Samoa’s

position as unattractive unless exit achieved to induce an offer Use third-party bid to establish valuation floor Test Samoa and Amelia’s group resolve Test Samoa and Amelia’s desire to participate with third-party Samoa submits and is

most viable bid Samoa provides compelling proposal that maximizes shareholder value Increases certainty of closing Requires process protections to ensure fairness Support board in reviewing offer through Special Committee Continue running

process to maintain competitive tension Consider go-shop provision to validate outcome post-signing 2 3 Outcome Implications How to create leverage Next steps 1 4 Ensure proposal reflects value created by standalone plan Stress

uncertain path to Samoa liquidity until 2033, making an exit now the only viable value realization 2. EXECUTIVE SUMMARY 24

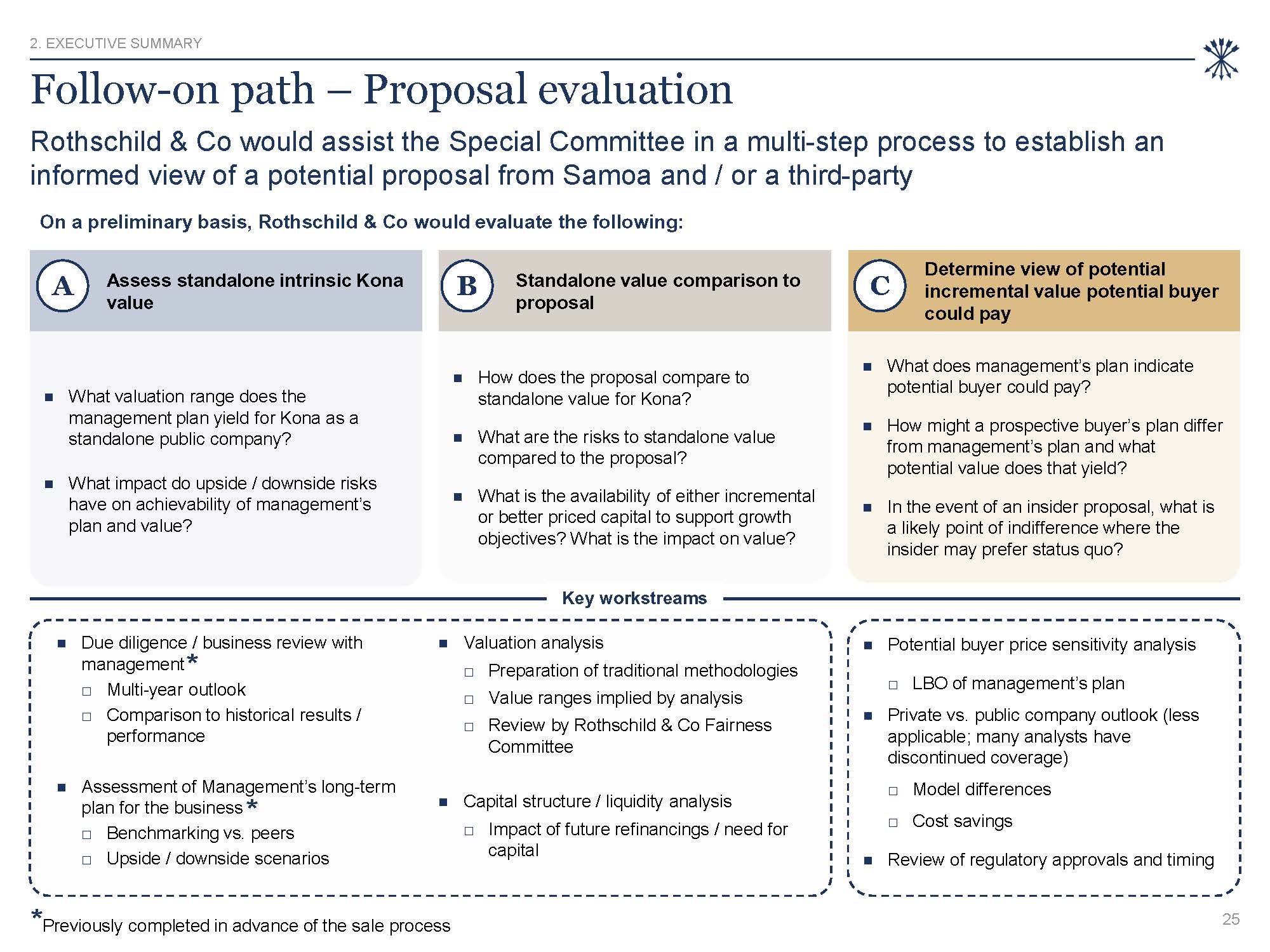

Follow-on path – Proposal evaluation Rothschild & Co would assist the Special

Committee in a multi-step process to establish an informed view of a potential proposal from Samoa and / or a third-party On a preliminary basis, Rothschild & Co would evaluate the following: What valuation range does the management plan

yield for Kona as a standalone public company? What impact do upside / downside risks have on achievability of management’s plan and value? How does the proposal compare to standalone value for Kona? What are the risks to standalone value

compared to the proposal? What is the availability of either incremental or better priced capital to support growth objectives? What is the impact on value? What does management’s plan indicate potential buyer could pay? How might a

prospective buyer’s plan differ from management’s plan and what potential value does that yield? In the event of an insider proposal, what is a likely point of indifference where the insider may prefer status quo? Assess standalone intrinsic

Kona value Standalone value comparison to proposal Determine view of potential C incremental value potential buyer could pay A B Potential buyer price sensitivity analysis LBO of management’s plan Private vs. public company outlook

(less applicable; many analysts have discontinued coverage) Model differences Cost savings Review of regulatory approvals and timing Valuation analysis Preparation of traditional methodologies Value ranges implied by analysis Review by

Rothschild & Co Fairness Committee Capital structure / liquidity analysis □ Impact of future refinancings / need for capital Due diligence / business review with management* Multi-year outlook Comparison to historical results

/ performance Assessment of Management’s long-term plan for the business * Benchmarking vs. peers Upside / downside scenarios Key workstreams *Previously completed in advance of the sale process 2. EXECUTIVE SUMMARY 25

Appendix

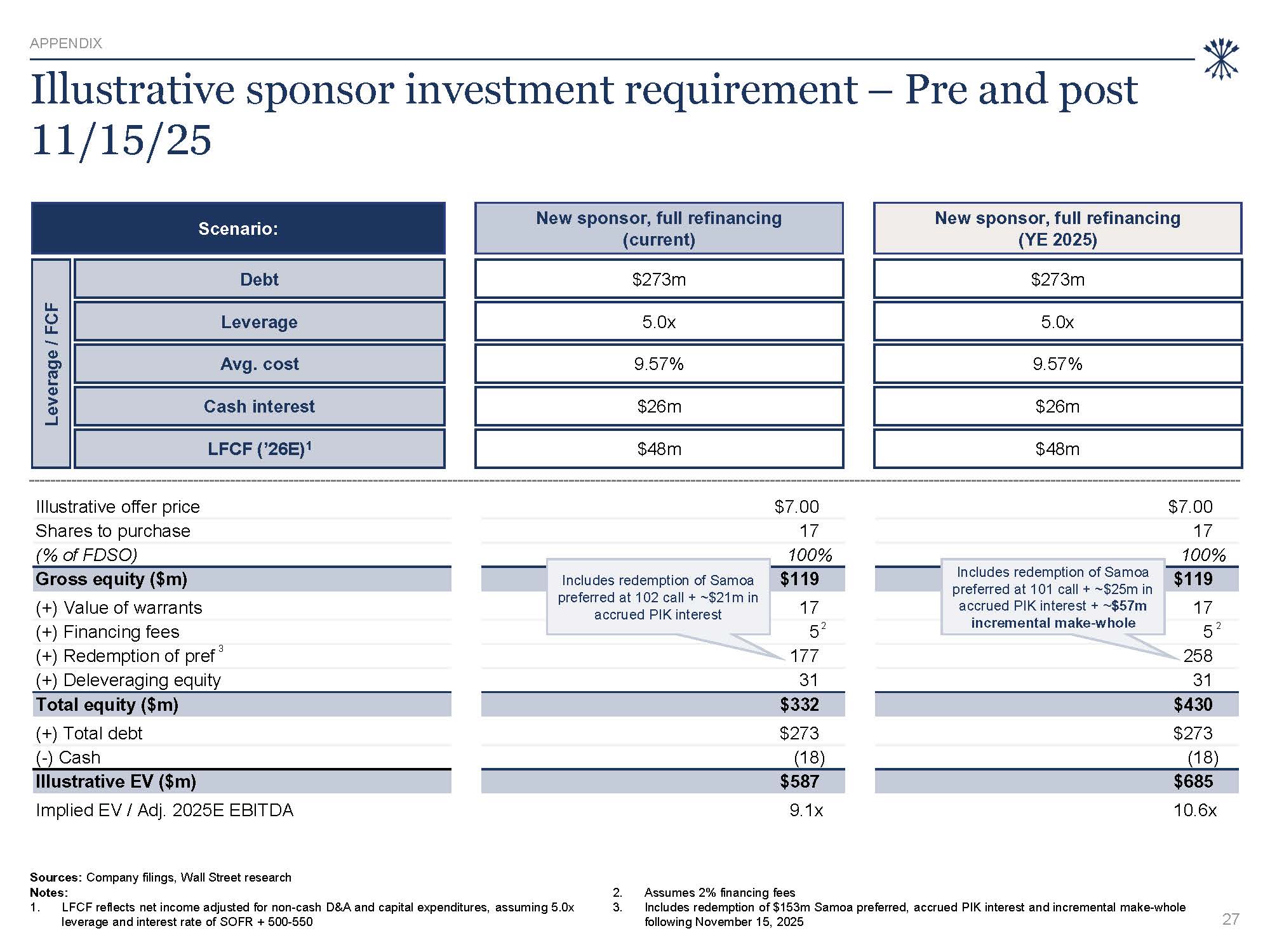

Illustrative offer price $7.00 $7.00 Shares to purchase 17 17 (% of

FDSO) 100% 100% Gross equity ($m) $119 17 $119 17 (+) Value of warrants 177 258 (+) Financing fees (+) Redemption of pref 3 52 5 2 Illustrative sponsor investment requirement – Pre and post 11/15/25 Scenario: Leverage /

FCF Debt Leverage Avg. cost Cash interest LFCF (’26E)1 1. LFCF reflects net income adjusted for non-cash D&A and capital expenditures, assuming 5.0x leverage and interest rate of SOFR + 500-550 (+) Deleveraging equity 31 31 Total

equity ($m) $332 $430 (+) Total debt $273 $273 (-) Cash (18) (18) Illustrative EV ($m) $587 $685 Implied EV / Adj. 2025E EBITDA 9.1x 10.6x Sources: Company filings, Wall Street research Notes: 2. Assumes 2% financing fees 3.

Includes redemption of $153m Samoa preferred, accrued PIK interest and incremental make-whole following November 15, 2025 New sponsor, full refinancing (current) $273m 5.0x 9.57% $26m $48m New sponsor, full refinancing (YE

2025) $273m 5.0x 9.57% $26m $48m Includes redemption of Samoa preferred at 102 call + ~$21m in accrued PIK interest Includes redemption of Samoa preferred at 101 call + ~$25m in accrued PIK interest + ~$57m incremental

make-whole APPENDIX 27

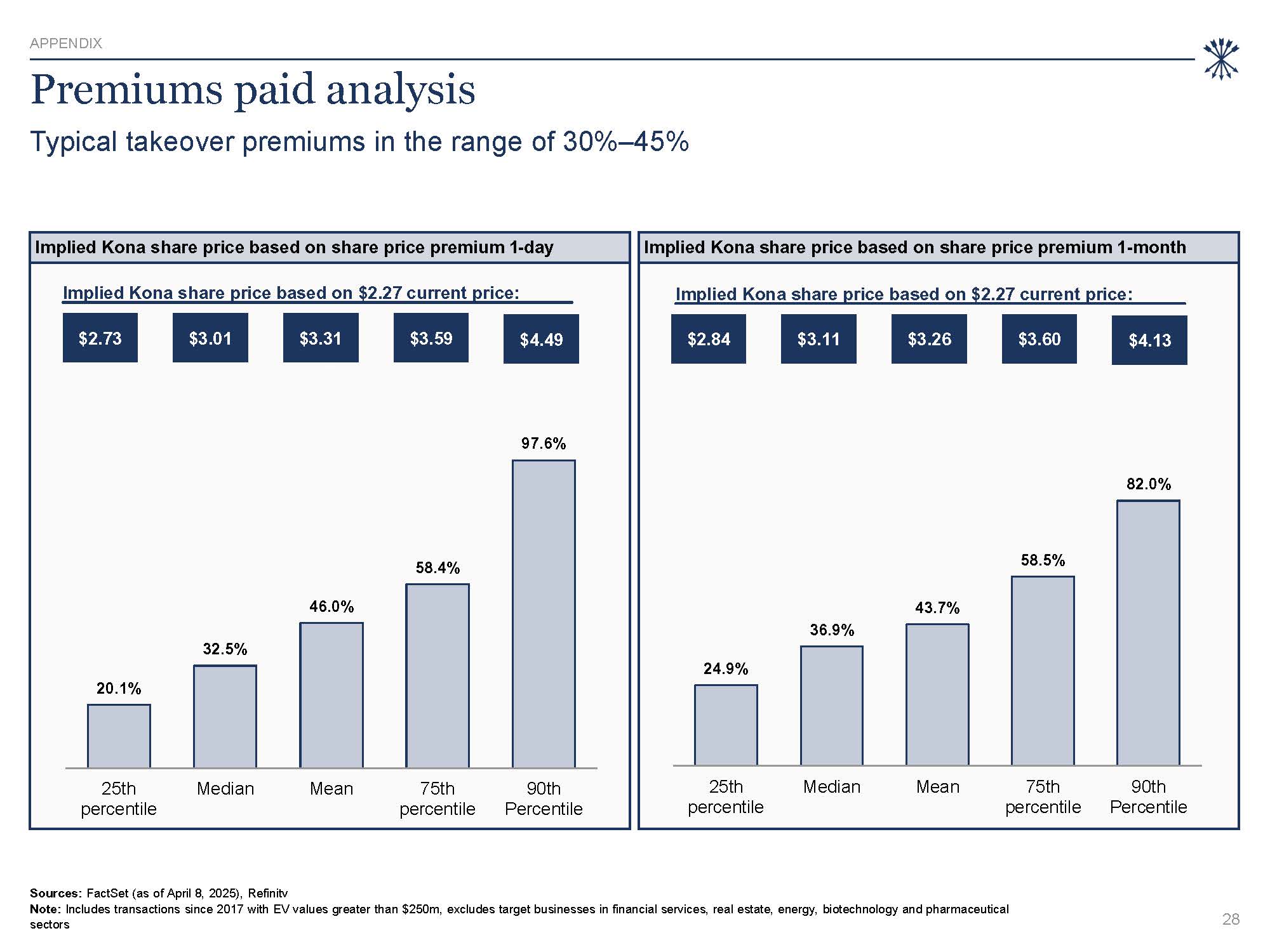

Premiums paid analysis Typical takeover premiums in the range of 30%–45% Implied

Kona share price based on share price premium 1-day $2.73 $3.31 $3.01 $3.59 Implied Kona share price based on $2.27 current price: $4.49 Sources: FactSet (as of April 8, 2025), Refinitv Note: Includes transactions since 2017 with EV

values greater than $250m, excludes target businesses in financial services, real estate, energy, biotechnology and pharmaceutical sectors 20.1% 32.5% 46.0% 58.4% 97.6% 25th percentile Median Mean 75th percentile 90th

Percentile Chart Title Implied Kona share price based on share price premium 1-month Implied Kona share price based on $2.27 current price:

$2.84 $3.11 $3.60 $4.13 24.9% 36.9% 43.7% 58.5% 82.0% 25th percentile Median Mean 75th percentile 90th Percentile Chart Title $3.26 APPENDIX 28

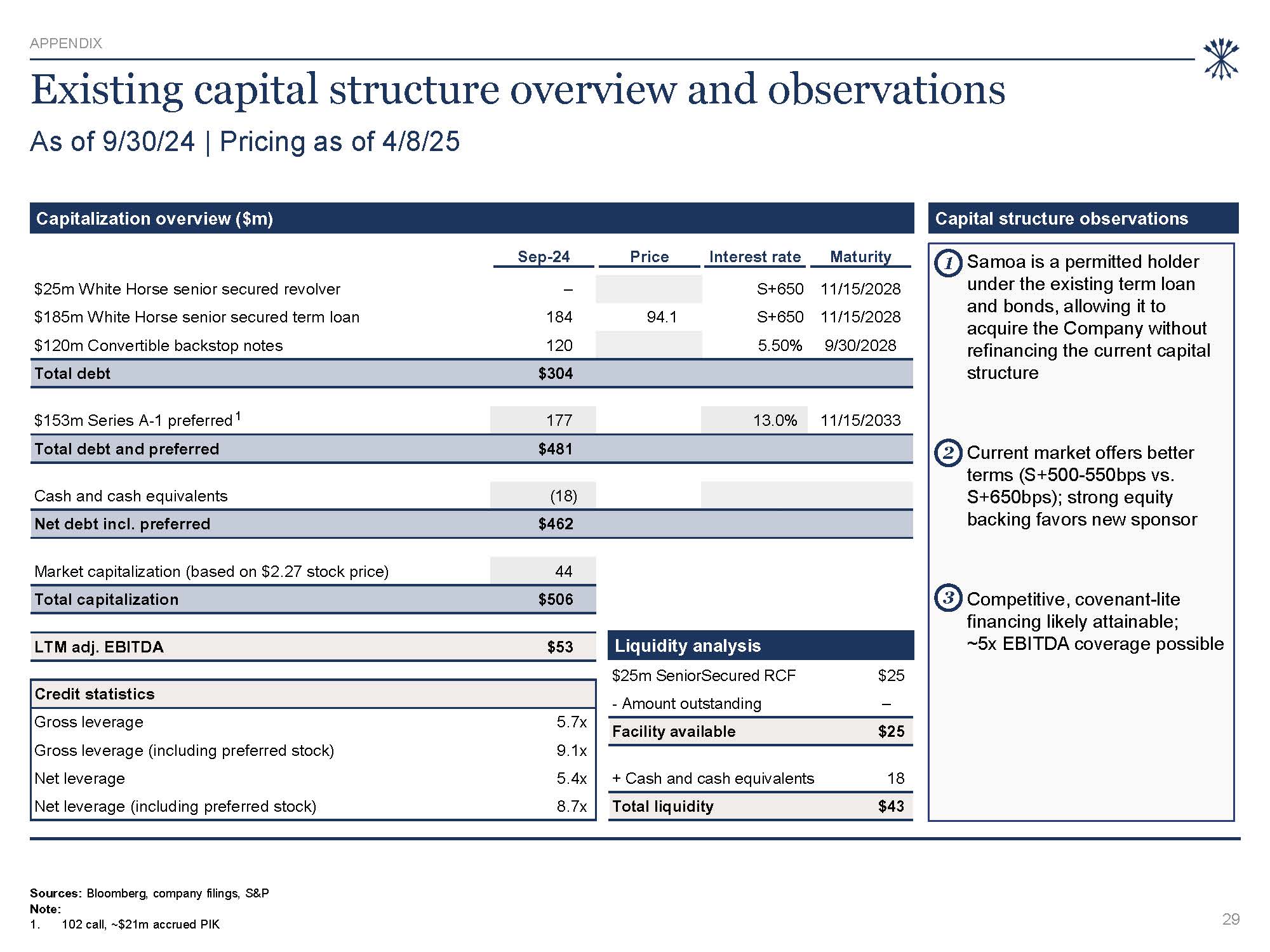

$25m White Horse senior secured revolver – S+650 11/15/2028 $185m White Horse

senior secured term loan 184 94.1 S+650 11/15/2028 $120m Convertible backstop notes 120 5.50% 9/30/2028 Total debt $304 $153m Series A-1 preferred 1 177 13.0% 11/15/2033 Total debt and preferred $481 Cash and cash

equivalents (18) Net debt incl. preferred $462 Market capitalization (based on $2.27 stock price) 44 Total capitalization $506 Credit statistics Gross leverage 5.7x Gross leverage (including preferred stock) 9.1x Net

leverage 5.4x Net leverage (including preferred stock) 8.7x Sep-24 Price Interest rate Maturity LTM adj. EBITDA $53 Existing capital structure overview and observations As of 9/30/24 | Pricing as of 4/8/25 Capitalization overview

($m) Capital structure observations Sources: Bloomberg, company filings, S&P Note: 1. 102 call, ~$21m accrued PIK Liquidity analysis $25m SeniorSecured RCF $25 - Amount outstanding – Facility available $25 + Cash and cash

equivalents 18 Total liquidity $43 1 Samoa is a permitted holder under the existing term loan and bonds, allowing it to acquire the Company without refinancing the current capital structure 2 Current market offers better terms

(S+500-550bps vs. S+650bps); strong equity backing favors new sponsor 3 Competitive, covenant-lite financing likely attainable; ~5x EBITDA coverage possible APPENDIX 29

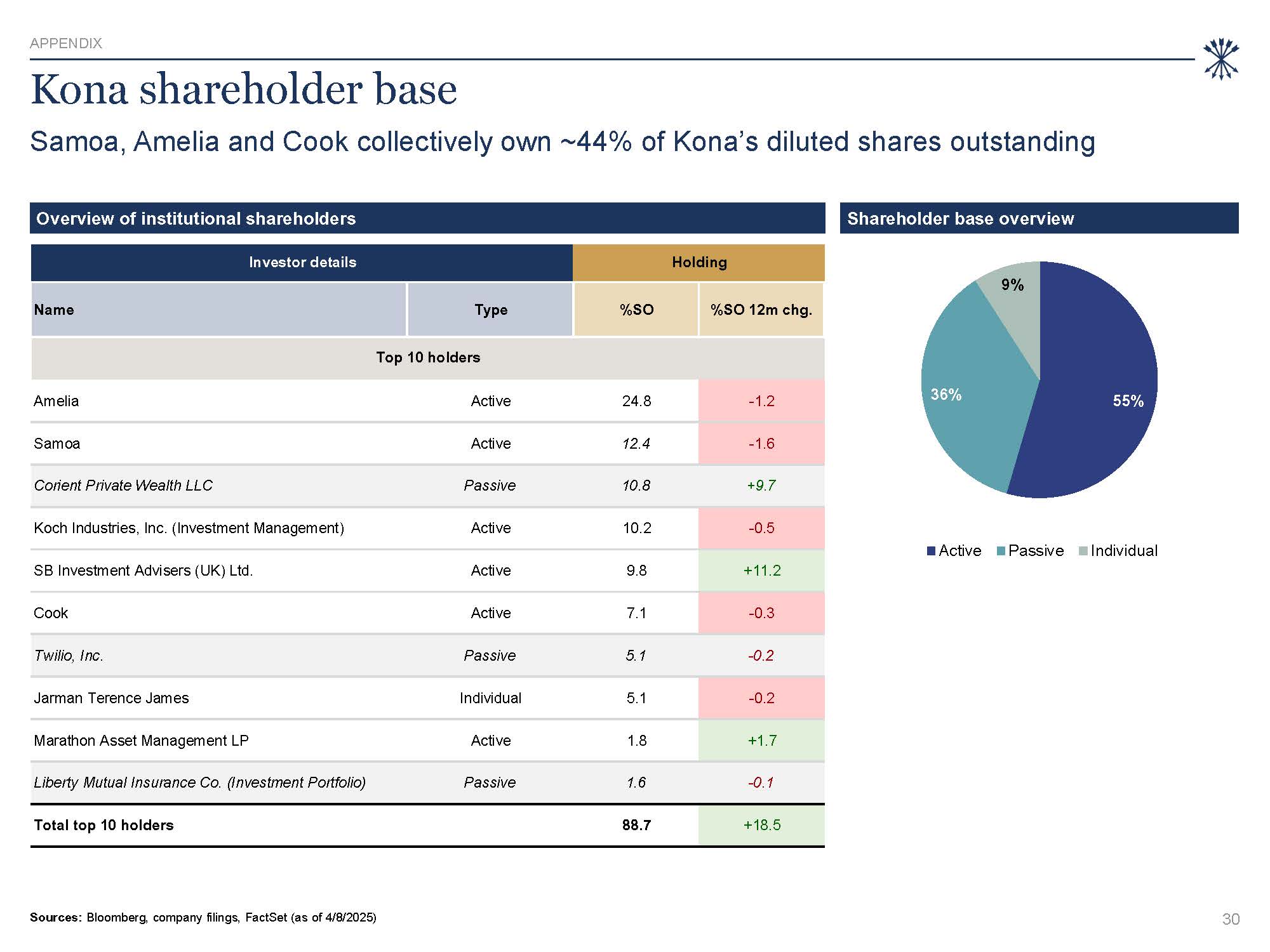

55% 36% 9% Active Passive Individual Kona shareholder base Sources:

Bloomberg, company filings, FactSet (as of 4/8/2025) Shareholder base overview Samoa, Amelia and Cook collectively own ~44% of Kona’s diluted shares outstanding HS to re flash Overview of institutional shareholders Investor

details Holding Name Type %SO %SO 12m chg. Top 10 holders Amelia Active 24.8 -1.2 Samoa Active 12.4 -1.6 Corient Private Wealth LLC Passive 10.8 +9.7 Koch Industries, Inc. (Investment Management) Active 10.2 -0.5 SB

Investment Advisers (UK) Ltd. Active 9.8 +11.2 Cook Active 7.1 -0.3 Twilio, Inc. Passive 5.1 -0.2 Jarman Terence James Individual 5.1 -0.2 Marathon Asset Management LP Active 1.8 +1.7 Liberty Mutual Insurance Co. (Investment

Portfolio) Passive 1.6 -0.1 Total top 10 holders 88.7 +18.5 APPENDIX 30

Disclaimer This presentation was prepared exclusively by Rothschild & Co US

Inc. (“Rothschild & Co”) on a confidential basis. Rothschild & Co has not assumed any responsibility for independent verification of any of the information contained herein and Rothschild & Co has relied on such information being

complete and accurate in all material respects. Accordingly, no representation or warranty, express or implied, can be made or is made by Rothschild & Co as to the accuracy or completeness of any such information. Except where otherwise

indicated, this presentation speaks as of the date hereof and is necessarily based upon the information available to Rothschild & Co and financial, stock market and other conditions and circumstances existing and disclosed to Rothschild

& Co as of the date hereof, all of which are subject to change. Rothschild & Co does not have any obligation to update, bring-down, review or reaffirm this presentation. Under no circumstances should the delivery of this presentation

imply that any information or analyses included in this presentation would be the same if made as of any other date. Nothing contained in this presentation is, or shall be relied upon as, a promise or representation as to the past, present or

future. This presentation provides summary information only and is being delivered solely for informational purposes. Rothschild & Co does not provide legal, tax or accounting advice of any kind. By receipt of this presentation, the

recipient acknowledges that it is not relying on Rothschild & Co for legal, tax or accounting advice, and that the recipient should receive separate and qualified legal, tax and accounting advice in connection with any transaction or course

of conduct. Nothing contained herein shall be deemed to be a recommendation from Rothschild & Co to any party to enter into any transaction or to take any course of action. This presentation is not intended to provide a basis for

evaluating any transaction or other matter. This presentation is confidential and may not be copied by, or disclosed or made available to, any person without the prior written consent of Rothschild & Co. Rothschild & Co shall not have

any liability, whether direct or indirect, in contract or tort or otherwise, to any person in connection with this presentation.