| Class A | Class C | Class I | Class L | ||||||||

| Stockholder Transaction Expenses (as a percentage of offering price)(1) |

|

|

| ||||||||

| Sales load to Dealer Manager(2) | 6.75 | % | 0.75 | % |

| 4.25 | % | ||||

| Distribution reinvestment plan fees(3) |

|

|

|

|

|

|

| ||||

| Total stockholder transaction expenses | 6.75 | % | 0.75 | % |

| 4.25 | % | ||||

____________

(1) Amount assumes that the Fund raises approximately $25.0 million in net equity proceeds during the 12 months following the effectiveness of this Registration Statement, resulting in estimated net assets of approximately $87.7 million as of the period ended 12 months following the effectiveness of this Registration Statement. Actual expenses will depend on the number of Shares the Fund sells in this offering and the amount of leverage it employs. For example, if the Fund were to raise proceeds significantly less than this amount over the next twelve months, the Fund’s expenses as a percentage of its average net assets would be significantly higher. There can be no assurance that the Fund will sell $25.0 million of Shares during the twelve months following the effectiveness of this Registration Statement.

(2) “Sales load” includes selling commissions of 6.0% and dealer manager fees of 0.75% payable upon a purchase of Class A Shares, dealer manager fees of 0.75% payable upon a purchase of Class C Shares and selling commissions of 3.50% and dealer manager fees of 0.75% payable upon a purchase of Class L Shares. The table assumes the maximum sales load for Class A Shares, Class C Shares and Class L Shares is charged.

(3) The expenses of the distribution reinvestment plan are included in Other Expenses. See “Distribution Reinvestment Plan.”

| Annual expenses (as a percentage of net assets attributable to shares)(1) |

|

|

|

| ||||||||

| Base management fee(4) | 2.08 | % | 2.08 | % | 2.08 | % | 2.08 | % | ||||

| Incentive fees payable under our investment advisory agreement (20% of net investment income)(5) | 2.29 | % | 2.29 | % | 2.29 | % | 2.29 | % | ||||

| Interest payments on borrowed funds(6) |

|

|

|

|

|

|

|

| ||||

| Distribution and shareholder servicing fee(7) |

|

|

|

|

|

| 0.50 | % | ||||

| Other expenses(8) | 4.97 | % | 4.97 | % | 4.97 | % | 4.97 | % | ||||

| Total Annual Fund Operating Expenses(9) | 9.34 | % | 9.34 | % | 9.34 | % | 9.84 | % | ||||

| Less expense waiver and/or expense reimbursement(10) | (3.98 | )% | (3.98 | )% | (3.98 | )% | (3.98 | )% | ||||

| Total annual net expenses(9) | 5.36 | % | 5.36 | % | 5.36 | % | 5.86 | % |

(1) Amount assumes that the Fund raises approximately $25.0 million in net equity proceeds during the 12 months following the effectiveness of this Registration Statement, resulting in estimated net assets of approximately $87.7 million as of the period ended 12 months following the effectiveness of this Registration Statement. Actual expenses will depend on the number of Shares the Fund sells in this offering and the amount of leverage it employs. For example, if the Fund were to raise proceeds significantly less than this amount over the next twelve months, the Fund’s expenses as a percentage of its average net assets would be significantly higher. There can be no assurance that the Fund will sell $25.0 million of Shares during the twelve months following the effectiveness of this Registration Statement.

(4) The Fund’s base management fee is calculated monthly and payable quarterly in arrears at an annual rate equal to 2.00% of its gross assets, including assets purchased with borrowed funds or other forms of leverage, at the end of the two most recently completed quarters.

(5) Amount reflects the estimated annual incentive fees payable to the Adviser over the next twelve months. Based on its current business plan, the Fund anticipates that the net proceeds from the offering of securities will be invested within three months after receipt of proceeds, although such period may vary and depends on the size of the offering and the availability of appropriate investment opportunities consistent with the Fund’s investment objectives and market conditions. The Fund cannot assure you it will achieve its targeted investment pace, which may negatively impact its returns.

The Incentive Fee, which is payable quarterly in arrears, equals 20.0% of the excess, if any, of the Funds “Pre-Incentive Fee Net Investment Income” that exceeds a 1.75% quarterly (7.0% annualized) hurdle rate, which the Fund refers to as the “Hurdle,” subject to a “catch-up” provision measured at the end of each calendar quarter. The Incentive Fee is computed and paid on income that may include interest that is accrued but not yet received in cash.

The incentive fee in each calendar quarter is paid to the Adviser as follows:

• no Incentive Fee is payable to the Adviser in any calendar quarter in which the Fund’s Pre-Incentive Fee Net Investment Income does not exceed the Hurdle of 1.75%;

• 100% of the Fund’s Pre-Incentive Fee Net Investment Income with respect to that portion of such Pre-Incentive Fee Net Investment Income, if any, that exceeds the Hurdle but is less than 2.1875% in any calendar quarter (8.75% annualized) is payable to the Adviser. The Fund refers to this portion of its Pre-Incentive Fee Net Investment Income (which exceeds the Hurdle but is less than 2.1875%) as the “catch-up.” The “catch-up” is meant to provide the Adviser with 20.0% of the Fund’s Pre-Incentive Fee Net Investment Income, as if a Hurdle did not apply when the Fund’s Pre-Incentive Fee Net Investment Income exceeds 2.1875% in any calendar quarter; and

• 20.0% of the amount of the Fund’s Pre-Incentive Fee Net Investment Income, if any, that exceeds 2.1875% in any calendar quarter (8.75% annualized) is payable to the Adviser (once the Hurdle is reached and the catch-up is achieved, 20.0% of all Pre-Incentive Fee Net Investment Income thereafter is allocated to the Adviser).

No Incentive Fee is payable to the Adviser on capital gains. For a more detailed discussion of the calculation of this fee, see “Management and Incentive Fees.”

(6) Assumes that the Fund will refrain from borrowing for investment purposes over the next twelve months. The Fund does not currently anticipate incurring indebtedness on its portfolio or paying any interest during the next twelve months following the effectiveness of this Registration Statement. Although the Fund has no current intention to do so, the Fund may borrow additional funds to make investments, to the extent the Fund determines that additional capital would allow the Fund to take advantage of additional investment opportunities, if the market for debt financing presents attractively priced debt financing opportunities, or if the Board of Directors determines that leveraging the Fund’s portfolio would be in the Fund’s best interests and the best interests of the Fund’s shareholders. The Fund does not currently anticipate issuing any preferred stock over the next twelve months. The costs associated with any borrowing will be indirectly borne by the Fund’s investors.

(7) Class L Shares are subject to a distribution and/or shareholder servicing fee at an annual rate of 0.50% of the Fund’s NAV attributable to Class L Shares most recently determined preceding the payment date. With respect to Class L Shares, 0.25% of the fee is characterized as a “shareholder servicing fee” and 0.25% is characterized as a “distribution fee.”

(8) Other expenses include reasonably estimated costs the Fund can expect to incur related to accounting, custody, transfer agency, legal, valuation agent, pricing vendor, market data, marketing and auditing fees of the Fund, organizational and offering costs, as well as the reimbursement of the compensation of administrative personnel and fees payable to the Independent Directors. The amount presented in the table are based upon estimated amounts for the current fiscal year.

(9) Each of “Total annual Fund operating expenses” and “Total annual net expenses” is presented as a percentage of net assets attributable to common stockholders because the holders of shares of our common stock bear all of our fees and expenses, all of which are included in this fee table presentation. The indirect expenses associated with the Fund’s CLO equity investments are not included in the fee table presentation, but if such expenses were included in the fee table presentation then the Fund’s total annual expenses would have been 14.69% for Class A, Class C and Class I Shares and 15.19% for Class L Shares and total annual net expenses would have been 10.71% for Class A, Class C and Class I Shares and 11.21% for Class L Shares.

(10) The Fund and the Adviser entered into an Amended and Restated Expense Support Agreement, effective May 31, 2025. Until the Expense Payment Period, the Adviser will pay and otherwise be legally responsible for the Ordinary Operating Expenses (as defined in the Amended and Restated Expense Support Agreement) incurred by or on behalf of the Fund that exceed the Expense Cap. The Fund will pay and otherwise be legally responsible for Ordinary Operating Expenses up to the Expense Cap incurred by it or by others on its behalf until the end of the Expense Payment Period and for all Ordinary Operating Expenses incurred by it or others on its behalf on and after the Expense Payment Period. The Ordinary Operating Expenses paid by the Adviser pursuant to the Amended and Restated Expense Support Agreement are not subject to reimbursement from the Fund. Pursuant to the Waiver Letter, the Adviser agreed to irrevocably waive any Management Fee and Incentive Fee due from the Fund to the Adviser through the period ended March 31, 2024, pursuant to the Investment Advisory Agreement between the Fund and the Adviser. The Adviser subsequently irrevocably waived any Management Fee and Incentive Fee through the period ended March 31, 2025, and any Incentive Fee through the period ended March 31, 2026, due from the Fund to the Adviser pursuant to the Investment Advisory Agreement between the Fund and the Adviser.

Example

The following example demonstrates the projected dollar amount of total expenses that would be incurred over various periods with respect to a hypothetical investment in each of Class A, Class C, Class I Shares and Class L Shares. In calculating the following expense amounts, the Fund has assumed its annual net expenses would remain at the percentage levels set forth in the table above. The table assumes the maximum sales load for Class A Shares, Class C Shares and Class L Shares is charged.

An investor would pay the following expenses on a $1,000 investment, assuming a 5.0% annual return:(1)(11)

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||

| Class A | $ | 117 | $ | 227 | $ | 334 | $ | 593 | ||||

| Class C | $ | 61 | $ | 177 | $ | 291 | $ | 567 | ||||

| Class I | $ | 54 | $ | 171 | $ | 285 | $ | 563 | ||||

| Class L | $ | 103 | $ | 223 | $ | 339 | $ | 608 | ||||

(1) Amount assumes that the Fund raises approximately $25.0 million in net equity proceeds during the 12 months following the effectiveness of this Registration Statement, resulting in estimated net assets of approximately $87.7 million as of the period ended 12 months following the effectiveness of this Registration Statement. Actual expenses will depend on the number of Shares the Fund sells in this offering and the amount of leverage it employs. For example, if the Fund were to raise proceeds significantly less than this amount over the next twelve months, the Fund’s expenses as a percentage of its average net assets would be significantly higher. There can be no assurance that the Fund will sell $25.0 million of Shares during the twelve months following the effectiveness of this Registration Statement.

(11) Reflects conversion of Class L Shares to Class I Shares (which pay lower ongoing expenses) of the Fund on the first business day of the month following the eighth anniversary of the issuance.

The following table is intended to assist you in understanding the costs and expenses that an investor in Shares sold in this offering will bear directly or indirectly. You will pay (i) selling commissions and dealer manager fees for the purchase of Class A Shares or Class L Shares, (ii) dealer manager fees, but no selling commissions, for the purchase of Class C Shares and (iii) no selling commissions or dealer manager fees for the purchase of Class I Shares. The Fund cautions you that some of the percentages indicated in the table below are estimates and may vary. Except where the context suggests otherwise, whenever this Prospectus contains a reference to fees or expenses paid by “you,” “us” or “Oxford Park Income Fund, Inc.,” or that “Fund,” or “we” will pay fees or expenses, shareholders will indirectly bear such fees or expenses as investors in the Fund.

INVESTMENT OBJECTIVE, OPPORTUNITIES AND STRATEGIES

Investment Objective

The Fund’s investment objective is to maximize its portfolio’s risk-adjusted total return. The Fund implements its investment objective by purchasing portions of equity and junior debt tranches of CLO vehicles. Substantially all of the CLO vehicles in which the Fund may invest would be deemed to be investment companies under the 1940 Act but for the exceptions set forth in section 3(c)(1) or section 3(c)(7). Structurally, CLO vehicles are entities formed to originate and/or acquire a portfolio of loans. The loans within the CLO vehicle are limited to loans which meet established credit criteria and are subject to concentration limitations in order to limit a CLO vehicle’s exposure to a single credit. A CLO vehicle is formed by raising various classes or “tranches” of debt (with the most senior tranches being rated “AAA” to the most junior tranches typically being rated “BB” or “B”) and equity. The CLO vehicles which the Fund focuses on are collateralized primarily by Senior Loans and, to a limited extent, other CLO Assets (such as second lien loans, other subordinated loans, unsecured loans and bonds) and generally have very little or no exposure to real estate, mortgage loans or to pools of consumer-based debt, such as credit card receivables or auto loans. Below investment grade securities, such as the CLO securities in which the Fund primarily invests, are often referred to as “junk.” In addition, the CLO equity and junior debt securities in which the Fund invests are highly leveraged (with CLO equity securities typically being leveraged between nine and thirteen times), which significantly magnifies the Fund’s risk of loss on such investments relative to senior debt tranches of CLOs. A CLO is itself highly leveraged because it borrows significant amounts of money to acquire the underlying commercial loans in which it invests. A CLO borrows money by issuing debt securities to investors (including junior debt securities of the type that the Fund invests), and the CLO equity is the first to bear the risk on the underlying investment. The Fund’s investment strategy also includes investing capital in warehouse facilities, which are financing structures intended to aggregate loans that may be used to form the basis of a CLO vehicle. Warehouse facilities typically incur leverage between four and six times prior to a CLO’s pricing. The Fund may also invest, on an opportunistic basis, in other corporate credits of a variety of types. Oxford Park Management manages the Fund’s investments and its affiliate arranges for the performance of the administrative services necessary for the Fund to operate.

CLO vehicles, due to their high leverage, are more complicated to evaluate than direct investments in Senior Loans and other CLO Assets. Since the Fund invests in the residual interests of CLO securities, the Fund’s investments are riskier than the profile of the Senior Loans by which such CLO vehicles are collateralized. The Fund’s investments in CLO vehicles are riskier and less transparent to the Fund and its shareholders than direct investments in the underlying Senior Loans. The Fund’s portfolio of investments may lack diversification among CLO vehicles which would subject the Fund to a risk of significant loss if one or more of these CLO vehicles experience a high level of defaults on its underlying CLO Assets. The CLO vehicles in which the Fund invests will have debt that ranks senior to its investment. The market price for CLO vehicles may fluctuate dramatically, which would make portfolio valuations unreliable and negatively impact the Fund’s NAV and its ability to make distributions to its shareholders. The Fund’s financial results may be affected adversely if one or more of its significant equity or junior debt investments in such CLO vehicles defaults on its payment obligations or fails to perform as the Fund expects.

The Fund’s investments in CLO vehicles may be subject to special anti-deferral provisions that could result in the Fund incurring tax or recognizing income prior to receiving cash distributions related to such income. Specifically, the CLO vehicles in which the Fund invests may generally constitute PFICs. Because the Fund will acquire investments in PFICs (including equity tranche investments in CLO vehicles that are PFICs), the Fund may be subject to U.S. federal income tax on a portion of any “excess distribution” or gain from the disposition of such investments even if such income is distributed as a taxable dividend by the Fund to its shareholders. See “Risks — Risks Related to the Fund’s Investments” beginning on page 31 to read about factors you should consider before investing in the Fund’s securities.

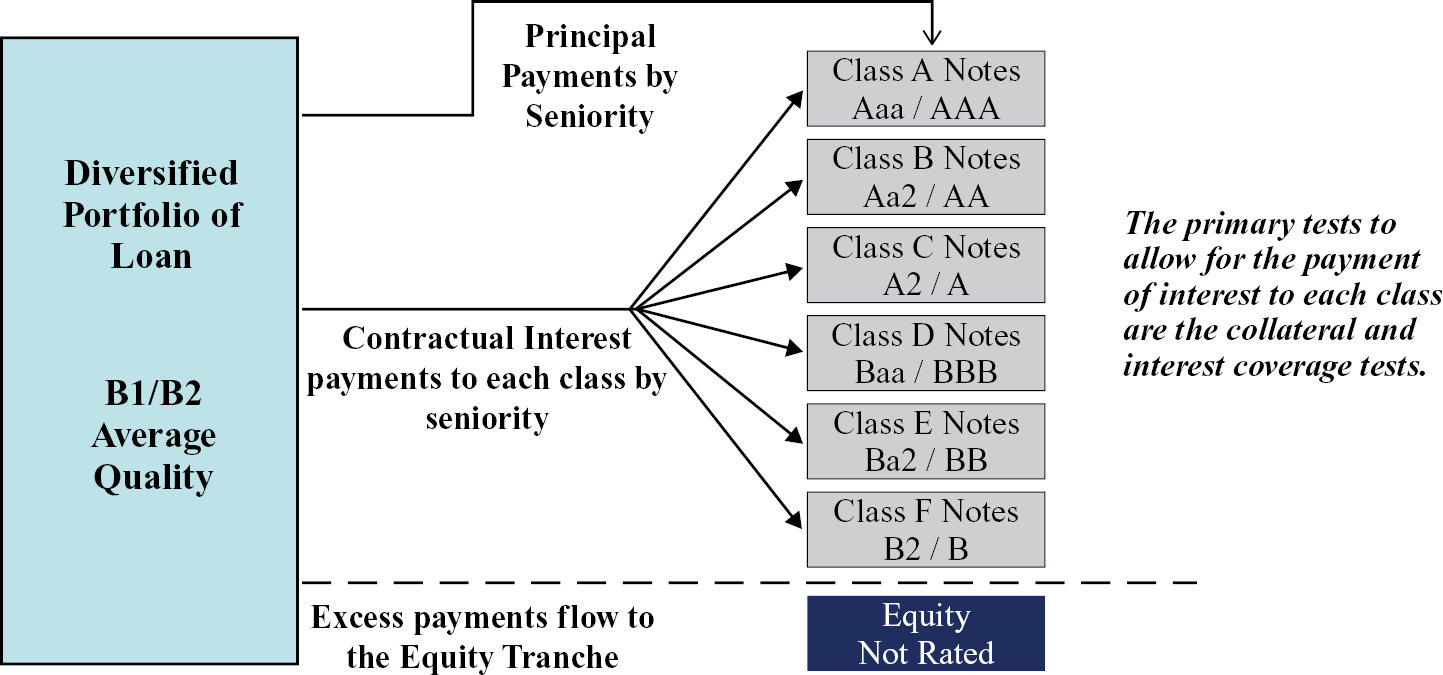

CLO Structural Elements

Structurally, CLO vehicles are entities formed to originate and/or acquire a portfolio of loans. The CLO portfolio is managed by a collateral manager, which is unaffiliated with the Fund or the Adviser. The loans within the CLO vehicle are generally limited to loans which meet established credit criteria and are subject to concentration limitations in order to limit a CLO vehicle’s exposure to a single credit.

A CLO vehicle is formed by raising multiple “tranches” of debt (with the most senior tranches being rated “AAA” to the most junior tranches typically being rated “BB” or “B”) and equity. As interest payments are received, the CLO vehicle makes contractual interest payments to each tranche of debt based on their seniority. If there are funds remaining after each tranche of debt receives its contractual interest rate and the CLO vehicle meets or exceeds required collateral coverage levels (or other similar covenants) the remaining funds may be paid to the equity tranche. The contractual provisions setting out this order of payments are set out in detail in the CLO vehicle’s indenture. These provisions are referred to as the “priority of payments” or the “waterfall” and determine any other obligations that may be required to be paid ahead of payments of interest and principal on the securities issued by a CLO vehicle. In addition, for payments to be made to each tranche, after the most senior tranche of debt, there are various tests which must be complied with, which are different for each CLO vehicle.

CLO indentures typically provide for adjustments to the priority of payments in the event that certain cashflow or collateral requirements are not maintained. The collateral quality tests that may divert cashflows in the priority of payments are predominantly determined by reference to the par values of the underlying loans, rather than their current market values. Accordingly, the Fund believes that CLO equity and junior debt investments allow investors to gain exposure to the Senior Loan market on a levered basis without being structurally subject to mark-to-market price fluctuations of the underlying loans. As such, although the current valuations of CLO equity and junior debt tranches are expected to fluctuate based on price changes within the loan market, interest rate movements and other macroeconomic factors, those tranches will generally be expected to continue to receive distributions from the CLO vehicle periodically so long as the underlying portfolio does not suffer defaults, realized losses or other covenant violations sufficient to trigger changes in the waterfall allocations. The Fund therefore believes that an investment portfolio consisting of CLO equity and junior debt investments of this type has the ability to provide attractive risk-adjusted rates of return.

The diagram below is for illustrative purposes only. The CLO structure highlighted below is illustrative only and depicts structures among CLO vehicles in which the Fund may invest may vary substantially from the illustrative example set forth below.

The Fund will typically invest in the equity tranches, which are not rated, and to a lesser extent the “B” and “BB” tranches of CLO vehicles.

The Syndicated Senior Loan Market

The Fund believes that while the syndicated leveraged corporate loan market is relatively large, with Morningstar LSTA Leveraged Loan Index estimating the total par value outstanding at approximately $1.5 trillion as of March 31, 2026, this market remains largely inaccessible to a significant portion of investors that are not lenders or approved institutions. The CLO market permits wider exposure to syndicated Senior Loans, but this market is almost exclusively private and predominantly institutional.

The Senior Loan market is characterized by various factors, including:

• Floating rate instruments. Senior Loans and other types of CLO Assets typically contain a floating interest rate as opposed to a fixed interest rate, which the Fund believes provides some measure of protection against the risk of interest rate fluctuation. However, all of the Fund’s CLO investments have many CLO Assets which are subject to interest rate floors and since interest rates on CLO Assets may only reset periodically and the amount of the increase following an interest rate reset may be below the interest rate floors of such CLO Assets, the Fund’s ability to benefit from rate resets following an increase in interest rates may be limited.

• Frequency of interest payments. Senior Loans and other CLO Assets typically provide for scheduled interest payments no less frequently than quarterly.

Investment Opportunity

The Fund believes that the market for CLO-related assets provides the Fund with opportunities to generate attractive risk-adjusted returns over the long term.

The long-term and relatively low-cost capital that many CLO vehicles have secured, compared with current asset spreads, have created opportunities to purchase certain CLO equity and junior debt instruments that may produce attractive risk-adjusted returns. Additionally, given that the CLO vehicles the Fund invests in are cash flow-based vehicles, this term financing may be beneficial in periods of market volatility.

The Fund will review a large number of CLO investment opportunities in the current market environment, and it expects that the majority of its portfolio holdings, over the near to intermediate-term, will continue to be comprised of CLO debt and equity securities, with the more significant focus over the near-term likely to be on CLO equity securities.

Investment Selection

Oxford Park Management’s investment team (the “Investment Team”) is responsible for all aspects of the Fund’s investment process. Oxford Park Management’s senior investment team currently consists of Messrs. Cohen and Rosenthal, who serve as members of the investment committee of Oxford Park Management. While the investment strategy involves a team approach, whereby potential transactions are screened by various members of the investment team, Messrs. Cohen or Rosenthal must approve all investments in order for them to close. The stages of the Fund’s investment selection process are as follows:

Deal Sourcing

Deal sourcing is generally conducted through brokers and bankers, and may also be sourced through industry contacts, CLO vehicle sponsors and investors. The Fund believes that it has an active pipeline of deal flow, particularly through multiple CLO trading desks.

Screening

In screening potential investments in CLO vehicles, the Investment Team utilizes a similar income-oriented investment philosophy they employ in their work managing other CLO investments at Oxford Lane Capital Corp. and Oxford Square Capital Corp.

Identification

The Fund identifies opportunities in the CLO market through its network of brokers, dealers, agent banks, collateral mangers and sponsors. The Fund believes that it has developed an infrastructure that provides the Fund with a competitive advantage in locating and acquiring attractive CLO opportunities. The Fund believes that it also has an active pipeline of deal flow, particularly through multiple CLO trading desks. The CLO vehicles which the Fund focuses on are collateralized primarily by senior secured loans made to companies whose debt is unrated or is rated below investment grade, and generally have very little or no direct exposure to real estate, mortgage loans or to pools of consumer-based debt, such as credit card receivables or auto loans. In screening potential investments in CLO vehicles,

the Fund’s due diligence process generally includes a review of current financial information and projections, review of collateral quality, concentration limitation and coverage test ratios, and a review of the prospective investment’s capital structure and the terms and conditions.

Due Diligence

The Investment Team conducts due diligence on prospective investments.

The Adviser’s due diligence process generally includes some or all of the following elements:

• review of indenture structures;

• review of underlying collateral loans;

• analysis of projected future cash flows; and

• analysis of compliance with covenants.

Upon the completion of due diligence, the investment professionals present the opportunity to the Adviser’s investment committee, which then determines whether to proceed with the potential investment. Any fees and expenses incurred by Oxford Park Management in connection with due diligence investigations undertaken by third parties will be subject to reimbursement by the Fund, which reimbursements will be in addition to any management or incentive fees payable under the Investment Advisory Agreement to Oxford Park Management. While the investment strategy involves a team approach, the Fund may not enter into a transaction without the prior approval of either Messrs. Cohen or Rosenthal.

Ongoing Relationships

Monitoring

The Adviser monitors the Fund’s investments on an ongoing basis. The Adviser has several methods of monitoring the performance and value of the Fund’s investments, which include the following:

• review of pricing data and indicative bids for recent transactions in the Fund’s investments;

• comparisons to other Senior Loans and CLO vehicles; and

• review of available financial reports for the Fund’s investments.

RISKS

Investing in the Fund’s Shares involves a number of significant risks. In addition to the other information contained elsewhere in this Prospectus, you should consider carefully the following information before making an investment in the Shares. If any of the following events occur, the Fund’s business, financial condition and results of operations could be materially and adversely affected. In such case, the NAV of the Fund’s Shares could decline, and you may lose all or part of your investment.

Risks Related to the Fund’s Business and Structure

Lack of Diversification. The Fund is classified as “non-diversified” under the 1940 Act. As a result, the Fund can invest a greater portion of its assets in obligations of a single issuer than a “diversified” fund. The Fund may therefore be more susceptible than a diversified fund to being adversely affected by any single corporate, economic, political or regulatory occurrence. The Fund intends to continue to qualify as a RIC under Subchapter M of the Code, and thus the Fund intends to satisfy the diversification requirements of Subchapter M, including its less stringent diversification requirements that apply to the percentage of the Fund’s total assets that are represented by cash and cash items (including receivables), U.S. government securities, the securities of other regulated investment companies and certain other securities.

“Best-Efforts” Offering Risk. This offering is being made on a best efforts basis, whereby the Dealer Manager is only required to use its best efforts to sell the Shares and has no firm commitment or obligation to purchase any of the Shares. To the extent that less than the maximum offering amount is subscribed for, the opportunity for the allocation of the Fund’s investments among various issuers and industries may be decreased, and the returns achieved on those investments may be reduced as a result of allocating all of the Fund’s expenses over a smaller capital base.

Inadequate Network of Broker-Dealer Risk. The success of the Fund’s continuous public offering, and correspondingly the Fund’s ability to implement its investment objective and strategies, depends upon the ability of the Dealer Manager to establish, operate and maintain a network of selected broker-dealers to sell the Shares. If the Dealer Manager fails to perform, the Fund may not be able to raise adequate proceeds through the Fund’s continuous public offering to implement the Fund’s investment objective and strategies. If the Fund is unsuccessful in implementing its investment objective and strategies, an investor could lose all or a part of his or her investment in the Fund.

Senior Management and Personnel of the Adviser. The Fund’s ability to achieve its investment objective depends on the Fund’s ability to effectively manage and deploy capital, which depends, in turn, on the Adviser’s ability to identify, evaluate and monitor, and the Fund’s ability to acquire, investments that meet its investment criteria.

Accomplishing the Fund’s investment objective on a cost-effective basis is largely a function of the Adviser’s handling of the investment process, its ability to provide competent, attentive and efficient services and the Fund’s access to investments offering acceptable terms, either in the primary or secondary markets. Even if the Fund is able to grow and build upon its investment operations, any failure to manage its growth effectively could have a material adverse effect on the Fund’s business, financial condition, results of operations and prospects. The results of the Fund’s operations will depend on many factors, including the availability of opportunities for investment, readily accessible short and long-term funding alternatives in the financial markets and economic conditions. Furthermore, if the Fund cannot successfully operate its business or implement its investment policies and strategies as described herein, it could negatively impact the Fund’s ability to pay distributions.

The Fund’s success also requires that Oxford Park Management retain investment and administrative personnel in a competitive market. Its ability to attract and retain personnel with the requisite credentials, experience and skills depends on several factors including, but not limited to, its ability to offer competitive wages, benefits and professional growth opportunities. Many of the entities, including investment funds (such as private equity funds, mezzanine funds and business development companies) and traditional financial services companies, with which the Fund competes for experienced personnel have greater resources than the Fund has.

The Adviser has the right, under the Investment Advisory Agreement, to resign at any time upon 60 days’ written notice, whether the Fund has found a replacement or not. If the Adviser resigns, the Fund may not be able to find a new Adviser or hire internal management with similar expertise and ability to provide the same or equivalent services on acceptable terms within 60 days, or at all. If the Fund is unable to do so quickly, its operations are likely to experience a disruption, the Fund’s financial condition, business and results of operations as well as its ability to pay distributions

are likely to be adversely affected and the market price of the Fund’s Shares may decline. In addition, the coordination of the Fund’s internal management and investment activities is likely to suffer if the Fund is unable to identify and reach an agreement with a single institution or group of executives having the expertise possessed by the Adviser and its affiliates. Even if the Fund is able to retain comparable management, whether internal or external, the integration of such management and their lack of familiarity with the Fund’s investment objective may result in additional costs and time delays that may adversely affect the Fund’s financial condition, business and results of operations.

Key Personnel. The Fund depends on the diligence, skill and network of business contacts of the senior management of Oxford Park Management. The senior management, together with other investment professionals, will evaluate, negotiate, structure, close, monitor and service the Fund’s investments. The Fund’s future success will depend to a significant extent on the continued service and coordination of the senior management team, particularly Jonathan H. Cohen, the Chief Executive Officer of Oxford Park Management, and Saul B. Rosenthal, the President of Oxford Park Management. Neither Mr. Cohen nor Mr. Rosenthal will devote all of their business time to the Fund’s operations, and both will have other demands on their time as a result of their other activities. Neither Mr. Cohen nor Mr. Rosenthal is subject to an employment contract. The departure of either of these individuals could have a material adverse effect on the Fund’s ability to achieve its investment objective. In addition, due to Oxford Park Management’s relatively small staff size, the departure of any of Oxford Park Management’s personnel, including investment, accounting and compliance professionals, could have a material adverse effect on the Fund.

Although Messrs. Cohen and Rosenthal have experience managing other investment portfolios, including those of Oxford Lane Capital Corp., a closed-end management investment company that currently invests primarily in CLO debt and equity tranches, Oxford Square Capital Corp., a publicly traded business development company that invests principally in the debt of U.S.-based companies, and Oxford Bridge II, LLC and the Oxford Gate Funds (as defined below), private investment funds that invest principally in the equity of CLOs, their track record and prior achievements are not necessarily indicative of future results that will be achieved by the Adviser. The Fund cannot assure you that it will be able to achieve the results realized by other vehicles managed by Messrs. Cohen and Rosenthal.

Incentive Fee Risks. The Incentive Fee payable by the Fund to Oxford Park Management may create an incentive for Oxford Park Management to pursue investments on the Fund’s behalf that are riskier or more speculative than would be the case in the absence of such compensation arrangement. Such a practice could result in the Fund investing in more speculative securities than would otherwise be the case, which could result in higher investment losses, particularly during economic downturns. The Incentive Fee payable to Oxford Park Management is based on the Fund’s Pre-Incentive Fee Net Investment Income, as calculated in accordance with the Fund’s Investment Advisory Agreement. In addition, the Fund’s Management Fee is calculated on the basis of the Fund’s gross assets, including assets acquired through the use of leverage. This may encourage Oxford Park Management to use leverage to increase the aggregate amount of and the return on the Fund’s investments, even when it may not be appropriate to do so, and to refrain from de-levering when it would otherwise be appropriate to do so. Under certain circumstances, the use of leverage may increase the likelihood of default, which would impair the value of the Fund’s securities.

The Fund may invest, to the extent permitted by law, in the securities and other instruments of other investment companies, including private funds, and, to the extent the Fund so invests, will bear its ratable share of any such investment company’s expenses, including management and performance fees. The Fund will also remain obligated to pay management and incentive fees to Oxford Park Management with respect to the assets invested in the securities and other instruments of other investment companies. With respect to each of these investments, each of the Fund’s shareholders will bear his or her share of the Management Fee and Incentive Fee of Oxford Park Management as well as indirectly bearing the management and performance fees and other expenses of any investment companies in which the Fund invests.

In the course of the Fund’s investing activities, the Fund pays management and incentive fees to Oxford Park Management and reimburses Oxford Park Management for certain expenses it incurs. As a result, investors in the Fund’s Shares invest on a “gross” basis and receive distributions on a “net” basis after expenses, resulting in a lower rate of return than an investor might achieve through direct investments.

In addition, given the structure of the Investment Advisory Agreement with Oxford Park Management, any general increase in interest rates will likely have the effect of making it easier for Oxford Park Management to meet the quarterly hurdle rate for payment of Incentive Fees under the Investment Advisory Agreement without any additional increase in relative performance on the part of Oxford Park Management. In addition, in view of the catch-up provision applicable to Incentive Fees under the Investment Advisory Agreement, Oxford Park Management could potentially

receive a significant portion of the increase in the Fund’s investment income attributable to such a general increase in interest rates. If that were to occur, the Fund’s increase in net earnings, if any, would likely be significantly smaller than the relative increase in the Adviser’s Incentive Fee resulting from such a general increase in interest rates.

Valuation Risk. Under the 1940 Act, the Fund is required to carry its portfolio investments at market value or, if there is no readily available market value, at fair value as determined by the Fund in accordance with its written valuation policy with the Board of Directors having final responsibility for overseeing, reviewing and approving, in good faith, its estimate of fair value. Typically, there will not be a public market for the type of investments the Fund targets, which will require the Fund to value these securities at fair value based on relevant information compiled by the Adviser, third-party pricing services (when available) and Valuation Committee and with the oversight, review and approval of the Board of Directors.

The determination of fair value and, consequently, the amount of unrealized gains and losses in the Fund’s portfolio, are to a certain degree subjective and dependent on a valuation process approved by the Board of Directors. Certain factors that may be considered in determining the fair value of the Fund’s investments include available indicative bids or quotations, as well as external events, such as private mergers, sales and acquisitions involving comparable companies. Because such valuations, and particularly valuations of private securities, are inherently uncertain, they may fluctuate over short periods of time and may be based on estimates. The fair value of the Fund’s investments may differ materially from the values that would have been used if an active public market for these securities existed. The fair value of the Fund’s investments have a material impact on its net earnings through the recording of unrealized appreciation or depreciation of investments and may cause the Fund’s NAV on a given date to materially understate or overstate the value that the Fund may ultimately realize on one or more of its investments. Investors purchasing the Fund’s securities based on an overstated NAV may pay a higher price than the value of the Fund’s investments might warrant. Conversely, investors selling Shares during a period in which the NAV understates the value of the Fund’s investments may receive a lower price for their Shares than the value of its investments might warrant.

Competition. The Fund may compete for investments with other investment funds (potentially including private equity funds, mezzanine funds and business development companies), as well as traditional financial services companies, which could include commercial banks, investment banks, finance companies and other sources of funding.

Many of the Fund’s competitors are substantially larger and have considerably greater financial, technical and marketing resources than the Fund. For example, some competitors may have a lower cost of capital and access to funding sources that may not be available to the Fund. In addition, some of the Fund’s competitors may have higher risk tolerances or different risk assessments than the Fund has. These characteristics could allow the Fund’s competitors to consider a

wider variety of investments, establish more relationships and offer higher pricing than the Fund is willing to offer to potential sellers. The Fund may lose investment opportunities if its competitors are willing to pay more for the types of investments that the Fund targets. If the Fund is forced to pay more for its investments, the Fund may not be able to achieve acceptable returns on its investments or may bear substantial risk of capital loss. An increase in the number and/or the size of the Fund’s competitors in its target markets could force the Fund to accept less attractive investments. Furthermore, many of the Fund’s competitors have greater experience operating under, or are not subject to, the regulatory restrictions that the 1940 Act imposes on the Fund as a closed-end management investment company.

Conflicts of Interest Risks. Oxford Park Management’s Investment Team presently manages the portfolios of Oxford Lane Capital Corp., a closed-end management investment company that currently invests primarily in CLO debt and equity tranches, and Oxford Square Capital Corp., a publicly-traded business development company that invests principally in the debt of U.S.-based companies. Additionally, Oxford Park Management’s Investment Team also manages Oxford Gate Master Fund, LLC, Oxford Gate, LLC and Oxford Gate (Bermuda), LLC (collectively, the “Oxford Gate Funds”) and Oxford Bridge II, LLC, managed by Oxford Gate Management, LLC (“Oxford Gate Management”). Oxford Bridge II, LLC and the Oxford Gate Funds are private investment funds. In addition, the Fund’s executive officers and directors, as well as the current and future members of Oxford Park Management may serve as officers, directors or principals of other entities that operate in the same or a related line of business as the Fund. Accordingly, they may have obligations to investors in those entities, the fulfillment of which obligations may not be in the best interests of the Fund or its shareholders. Each of Oxford Lane Capital Corp., Oxford Square Capital Corp., Oxford Bridge II, LLC and the Oxford Gate Funds, as well as any affiliated investment vehicle formed in the future and managed by Oxford Park Management or its affiliates may, notwithstanding different stated investment objectives, have overlapping investment objectives with the Fund and, accordingly, may invest in asset classes similar to those targeted by the Fund. As a result, Oxford Park Management’s Investment Team may face conflicts in allocating investment opportunities between the Fund and such other entities. Although Oxford Park Management’s Investment Team will endeavor to allocate investment opportunities in a fair and equitable manner, it is possible that, in the future, the Fund may not be given the opportunity to participate in investments made by investment funds, including Oxford Lane Capital Corp., Oxford Square Capital Corp., Oxford Bridge II, LLC and the Oxford Gate Funds, managed by Oxford Park Management or an investment manager affiliated with Oxford Park Management. In any such case, when Oxford Park Management’s Investment Team identifies an investment, it will be required to choose which investment fund should make the investment, although the Fund, Oxford Lane Capital Corp., Oxford Square Capital Corp., Oxford Bridge II, LLC and the Oxford Gate Funds are subject to an allocation policy to ensure the equitable distribution of such investment opportunities, consistent with the requirements of the 1940 Act.

As a registered closed-end fund, the Fund is limited in its ability to co-invest in privately negotiated transactions with certain funds or entities managed by Oxford Park Management or its affiliates without an exemptive order from the SEC. On January 6, 2026, the SEC issued an exemptive order (the “Order”) which permits the Fund to co-invest in portfolio companies with certain funds or entities managed by Oxford Park Management or its affiliates in certain negotiated transactions where co-investing would otherwise be prohibited under the 1940 Act, subject to the conditions of the Order, including the approval by a “required majority” (as defined in Section 57(o) of the 1940 Act) of the Independent Directors of certain potential co-investment transactions.

The Fund will reimburse Oxford Funds an allocable portion of overhead and other expenses incurred by Oxford Funds in performing its obligations under the Administration Agreement, including rent, the fees and expenses associated with performing administrative functions, and the Fund’s allocable portion of the compensation of its Chief Financial Officer and any administrative support staff, including accounting personnel. The Fund will also reimburse Oxford Funds for the costs associated with the functions performed by its Chief Compliance Officer that Oxford Funds pays on the Fund’s behalf pursuant to the terms of an agreement between the Fund and ACA. These arrangements may create conflicts of interest that the Board of Directors must monitor. Oxford Park Management is not reimbursed for any performance-related compensation of its employees.

Oxford Park Management or its affiliates pays the Dealer Manager a fee of up to 1.00% with respect to Class I Shares.

Risks Relating to our RIC Status. Although the Fund has elected to be treated as a RIC under Subchapter M of the Code, no assurance can be given that the Fund will be able to qualify for and maintain RIC status. If the Fund qualifies as a RIC under the Code, it generally will not be subject to corporate-level federal income taxes on its income and capital gains that are timely distributed (or deemed distributed) as dividends for U.S. federal income tax purposes to the Fund’s shareholders. To qualify as a RIC under the Code and to be relieved of federal taxes on income and gains

distributed as dividends for U.S. federal income tax purposes to the Fund’s shareholders, the Fund must, among other things, meet certain source-of-income, asset diversification and distribution requirements. The distribution requirement for a RIC is satisfied if the Fund distributes dividends each tax year for U.S. federal income tax purposes of an amount generally at least equal to 90% of the sum of its net ordinary income and net short-term capital gains in excess of net long-term capital losses, if any, to the Fund’s shareholders.

Risks Related to the Fund’s Investments

Risks Related to CLOs. The Fund has initially invested principally in equity and junior debt tranches issued by CLO vehicles. Generally, there may be less information available to the Fund regarding the underlying debt investments held by such CLO vehicles than if the Fund had invested directly in the debt of the underlying companies. As a result, the Fund’s stockholders may not know the details of the underlying debt investments of the CLO vehicles in which the Fund invests. The Fund’s CLO investments will also be subject to the risk of leverage associated with the debt issued by such CLOs and the repayment priority of senior debt holders in such CLO vehicles. Additionally, CLOs in which the Fund invests are often governed by a complex series of legal documents and contracts. As a result, the risk of dispute over interpretation or enforceability of the documentation may be higher relative to other types of investments.

In addition to the general risks associated with investing in debt securities, CLO vehicles carry additional risks, including, but not limited to: (i) the possibility that distributions from collateral securities will not be adequate to make interest or other payments; (ii) the credit quality of the CLO Assets that serve as collateral may decline or the CLO Asset may default; (iii) the CLO may experience losses associated with selling CLO Assets at a loss; (iv) the Fund’s investments in CLO debt and equity will likely be subordinate to other senior classes of CLO debt; (v) the CLO vehicle itself may experience an event of default, leading to acceleration of the CLO’s debt and liquidation of CLO Assets at undesirable prices and (vi) the complex structure of the security may not be fully understood at the time of investment and may produce disputes among participants of the CLO transaction or unexpected investment results. The Fund’s NAV may also decline over time if its principal recovery with respect to CLO equity investments is less than the price the Fund paid for those investments.

The CLO vehicles in which the Fund invests will issue and sell or have already issued and sold debt tranches that will rank senior to the debt and equity tranches in which the Fund invests. By their terms, such tranches entitle the holders to receive payment of interest or principal on or before the dates on which the Fund is entitled to receive payments with respect to the tranches in which the Fund invests. Also, in the event of default, insolvency, liquidation, dissolution, reorganization or bankruptcy of a CLO vehicle, holders of senior debt instruments would be entitled to receive payment in full before the Fund receives any distribution. After repaying such senior creditors, such CLO vehicle may not have any remaining assets to use for repaying its obligation to the Fund. In the case of tranches ranking equally with the tranches in which the Fund invests, the Fund would have to share on an equal basis any distributions with other investors holding such securities in the event of a default, insolvency, liquidation, dissolution, reorganization or bankruptcy of the relevant CLO vehicle. Therefore, the Fund may not receive back the full amount of its investment (or any of its investment) in a CLO vehicle or may not receive its anticipated yield.

The CLO equity market has experienced significant downturns from time to time. Due to the continued uncertainty in the CLO equity market, the Fund cannot assure you that it will achieve expected investment results and/or maintain its current level of cash distributions. The Fund’s future distributions are dependent upon the investment income the Fund receives on its portfolio investments, including its CLO equity investments. To the extent such CLO investments are terminated prior to the specified maturity date, such proceeds derived from a termination may be less than originally contemplated at that time of such investment. This may result in proceeds which may not be of a sufficient amount to invest in future CLO investments in order to generate cash returns that will enable the Fund to maintain the same level of distributions. This may result in a meaningful reduction in, or complete cessation of, the Fund’s distributions going forward. In addition, due to the asset coverage test applicable to the Fund as a registered closed-end management investment company, a reduction in the fair value of the Fund’s investments may limit its ability to make distributions.

Accounting and Tax Implications. The accounting and tax implications of such investments are complicated. In particular, reported earnings from the equity tranche investments of these CLO vehicles are recorded under GAAP based upon an effective yield calculation. Current taxable earnings on these investments, however, will generally not be determinable until after the end of the fiscal year of each individual CLO vehicle that ends within the Fund’s fiscal year, even though the investments are generating cash flow. In general, the tax treatment of these investments may result in higher distributable earnings in the early years and a capital loss at maturity, while for reporting purposes the totality of cash flows is reflected in a constant yield to maturity.

Limited Access to Information. None of the information contained in a CLO’s monthly reports, other trustee reports or any other financial information furnished to the Fund as an investor in a CLO is audited and reported upon, nor is an opinion expressed, by an independent public accountant. The Fund is not required to share any trustee reports or other reports received from any CLO with the Fund’s stockholders. Thus, you will have limited information on the assets held by, and the performance of, the CLOs in which the Fund invests.

Illiquidity of CLO Securities and their Investments. Some instruments issued by CLO vehicles may not be readily marketable and may be subject to restrictions on resale. Securities issued by CLO vehicles are generally not listed on any U.S. national securities exchange and no active trading market may exist for the securities of CLO vehicles in which the Fund may invest. Although a secondary market may exist for the Fund’s investments in CLO vehicles, the market for the Fund’s investments in CLO vehicles may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods. As a result, these types of investments may be more difficult to value.

Failure to Satisfy Financial Tests. CLO vehicles in which the Fund invests may fail to satisfy certain financial covenants, specifically those with respect to adequate collateralization and/or interest coverage tests. Such failure could lead to a reduction in such CLO’s payments to the Fund because senior debt holders generally would be entitled to additional payments that would, in turn, reduce the payments the Fund would otherwise be entitled to receive.

Risks Related to CLO Structure. The Fund’s portfolio includes equity and junior debt investments in CLOs, which involve a number of significant risks. CLOs are typically very highly levered (with CLO equity securities typically being leveraged between nine and 13 times), and therefore the junior equity and debt tranches in which the Fund invests will be subject to a higher degree of risk of total loss. In particular, investors in CLO securities indirectly bear risks of the collateral held by such CLOs. The Fund generally has the right to receive payments only from the CLOs, and generally does not have direct rights against the underlying borrowers or the entity that sponsored the CLO transaction. In addition, the Fund may have the option in certain CLOs to contribute additional amounts to the CLO issuer for purposes of acquiring additional assets or curing coverage tests, thereby increasing the Fund’s overall exposure and capital at risk to such CLO. Although it is difficult to predict whether the prices of assets underlying CLOs will rise or fall, these prices (and, therefore, the prices of the CLOs’ securities) are influenced by the same types of political and economic events that affect issuers of securities and capital markets generally.

CLO Fees and Expenses. While the CLO vehicles the Fund targets generally enable the investor to acquire interests in a pool of CLO Assets without the expenses associated with directly holding the same investments, the CLO vehicle itself will incur Management Fees (including Incentive Fees) and other expenses. CLO collateral manager fees are charged on the total assets of a CLO but are assumed to be paid from the residual cash flows after interest payments to the CLO senior debt tranches. Therefore, these CLO collateral manager fees are effectively much higher when allocated only to the CLO equity tranche. These fees incurred at the CLO level are in addition to the fees charged by the Adviser at the Fund level. Additionally, CLOs could also be liable to the collateral manager, trustee and other parties for indemnity payments. The Fund, as a CLO equity investor, will generally bear a share of the CLO vehicles’ administrative and other expenses that is proportionate with other CLO equity investors; however, CLO equity investors often negotiate fee rebates through side letters and other arrangements, and there can be no assurance that the Fund will be able to negotiate fee rebates for any CLO in which it invests, or that any fee rebates it does negotiate will be as favorable as fee rebates other CLO equity investors may negotiate. Separately, the Fund may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting CLO vehicle or any other investment the Fund may make. If any of these occur, it could materially and adversely affect the Fund’s operating results and cash flows.

Risks Related to Concentration. The Fund’s portfolio may hold investments in a limited number of CLO vehicles. Beyond the asset diversification requirements associated with its qualification as a RIC under the Code, the Fund does not have fixed guidelines for diversification, it does not have any limitations on the ability to invest in any one CLO vehicle, and its investments may be concentrated in relatively few CLO vehicles. As the Fund’s portfolio is less diversified than the portfolios of some larger funds, it is more susceptible to failure if one or more of the CLO vehicles in which the Fund is invested experiences a high level of defaults on its underlying Senior Loans and Other CLO Assets. Similarly, the aggregate returns the Fund realizes may be significantly adversely affected if a small number of investments perform poorly or if the Fund needs to write down the value of any one investment.

Additionally, the CLO vehicles in which the Fund invests may have CLO Asset portfolios that are concentrated in a limited number of industries or borrowers. A downturn in any particular industry or borrower in which a CLO vehicle is heavily invested may subject that vehicle, and in turn the Fund, to a risk of significant loss and could significantly

impact the aggregate returns the Fund realizes. If an industry in which a CLO vehicle is heavily invested suffers from adverse business or economic conditions, a material portion of the Fund’s investment in that CLO vehicle could be affected adversely, which, in turn, could adversely affect its financial position and results of operations.

The Fund may also invest in multiple CLOs managed by the same CLO collateral manager, thereby increasing its risk of loss in the event the CLO collateral manager were to fail, experience the loss of key portfolio management employees or sell its business.

Concentration of Underlying Obligors Across CLOs. Even if the Fund maintains diversification across different CLO issuers, the Fund may still be subject to concentration risk since CLO portfolios tend to have a certain amount of overlap across underlying obligors. This trend is generally exacerbated when demand for bank loans by CLO issuers outpaces supply. Market analysts have noted that the overlap of obligor names among CLO issuers has increased recently, and is particularly evident across CLOs of the same year of origination, as well as with CLOs managed by the same asset manager. To the extent the Fund invests in CLOs which have a high percentage of overlap, this may increase the likelihood of defaults on the Fund’s CLO investments occurring together.

Risks Related to Reinvestment of CLO Assets. As part of the ordinary management of its portfolio, a CLO will typically generate cash from asset repayments and sales and reinvest those proceeds in substitute assets, subject to compliance with its investment tests and certain other conditions. The earnings with respect to such substitute assets will depend on the quality of reinvestment opportunities available at the time. If the CLO collateral manager causes the CLO to purchase substitute assets at a lower yield than those initially acquired (for example, during periods of loan compression or in response to the need to satisfy the CLO’s covenants) or sale proceeds are maintained temporarily in cash, it would reduce the excess interest-related cash flow that the CLO collateral manager is able to achieve. The investment tests may incentivize a CLO collateral manager to cause the CLO to buy riskier assets than it otherwise would, which could result in additional losses. These factors could reduce the Fund’s return on investment and may have a negative effect on the fair value of our assets and the market value of our securities. In addition, the reinvestment period for a CLO may terminate early, which would cause the holders of the CLO’s securities to receive principal payments earlier than anticipated. In addition, in CLO transactions in which the Fund owns a minority of the equity tranche, the holders of a majority of the equity tranche direct a call or refinancing of a CLO, thus causing such CLO’s outstanding CLO debt securities to be repaid at par earlier than expected. There can be no assurance that the Fund will be able to reinvest such amounts in an alternative investment that provides a comparable return relative to the credit risk assumed.

Risks Related to CLO Managers. The Fund relies on CLO collateral managers to administer and review the portfolios of collateral of the CLOs in which they invest. The actions of the CLO collateral managers may significantly affect the return on the Fund’s investments; however, the Fund, as an investor of the CLO, typically does not have any direct contractual relationship with the collateral managers of the CLOs in which the Fund invests. The ability of each CLO collateral manager to identify and report on issues affecting its securitization portfolio on a timely basis could also affect the return on its investments, as the Fund may not be provided with information on a timely basis in order to take appropriate measures to manage its risks. The Fund will also rely on CLO collateral managers to act in the best interests of a CLO it manages; however, such CLO collateral managers are subject to fiduciary duties owed to other classes of debt besides those in which the Fund invests; therefore, there can be no assurance that the collateral managers will always act in the best interest of the CLO securities in which the Fund is invested. If any CLO collateral manager were to act in a manner that was not in the best interest of the CLOs, this could adversely impact the overall performance of the Fund’s investments. Furthermore, since the underlying CLO issuer often provides an indemnity to its CLO collateral manager, the Fund may not be incentivized to pursue actions against the collateral manager since any such action, if successful, may ultimately be borne by the underlying CLO issuer and payable from its assets, which could create losses to the Fund as an investor in the CLO. In addition, liabilities incurred by the CLO manger to third parties may be borne by the Fund as an investor in the CLO to the extent such CLO is required to indemnify its collateral manager for such liabilities.

Additionally, there is no guarantee that, for any CLO the Fund invests in, the collateral manager in place when the Fund invests in such CLO securities will continue to manage such CLO through the life of our investment. Collateral managers are subject to removal or replacement by other holders of CLO securities without our consent, and may also voluntarily resign as collateral manager or assign their role as collateral manager to another entity. There can be no assurance that any removal, replacement, resignation or assignment of any particular CLO manager’s role will not adversely affect the returns on the CLO securities in which the Fund invests.

Risks Related to Leverage of Underlying Obligors. Underlying obligors of the CLO Assets are typically highly leveraged, and there may not be significant restrictions on the amount of debt an obligor can incur. Substantial indebtedness adds additional risk with respect to an obligor and could (i) limit its ability to borrow money for its working capital, capital expenditures, debt service requirements, strategic initiatives or other purposes; (ii) require it to dedicate a substantial portion of its cash flow from operations to the repayment of its indebtedness, thereby reducing funds available to it for other purposes; (iii) make it more highly leveraged than some of its competitors, which may place it at a competitive disadvantage; and/or (iv) subject it to restrictive financial and operating covenants, which may preclude it from favorable business activities or the financing of future operations or other capital needs. In some cases, proceeds of debt incurred by an obligor could be paid as a dividend to stockholders rather than retained by the obligor for its working capital. Leveraged companies are often more sensitive to declines in revenues, increases in expenses, and adverse business, political, or financial developments or economic factors such as a significant rise in interest rates, a severe downturn in the economy or deterioration in the condition of such companies or their industries. A leveraged company’s income and net assets will tend to increase or decrease at a greater rate than if borrowed money were not used.

If an obligor is unable to generate sufficient cash flow to meet principal and/or interest payments on its indebtedness, it may be forced to take other actions to satisfy its obligations under its indebtedness. These alternative measures may include reducing or delaying capital expenditures, selling assets, seeking additional capital, or restructuring or refinancing indebtedness. Any of these actions could significantly reduce the value of the CLO Assets and thus the CLO securities in which the Fund invests. If such strategies are not successful and do not permit the obligor to meet its scheduled debt service obligations, the obligor may also be forced into liquidation, dissolution or insolvency, and the value of the CLO’s investment in such obligor could be significantly reduced or even eliminated.

Bankruptcy or Insolvency of an Obligor of a CLO Asset. In the event of a bankruptcy or insolvency of an issuer or borrower of a CLO Asset, a court or other governmental entity may determine that the claims of the relevant CLO are not valid or not entitled to the treatment the CLO expected when making its initial investment decision.

Various laws enacted for the protection of debtors may apply to the CLO Assets held by the CLOs in which the Fund invests. The information in this and the following paragraph represents a brief summary of certain points only, is not intended to be an extensive summary of the relevant issues and is applicable with respect to U.S. issuers and borrowers only. The following is not intended to be a summary of all relevant risks. Similar avoidance provisions to those described below are sometimes available with respect to non-U.S. issuers or borrowers, and there is no assurance that this will be the case which may result in a much greater risk of partial or total loss of value in that underlying CLO Asset.

If a court in a lawsuit brought by an unpaid creditor or representative of creditors of an issuer or borrower of a CLO Asset, such as a trustee in bankruptcy, were to find that such issuer or borrower did not receive fair consideration or reasonably equivalent value for incurring the indebtedness constituting such CLO Asset and, after giving effect to such indebtedness, the issuer or borrower (1) was insolvent; (2) was engaged in a business for which the remaining assets of such issuer or borrower constituted unreasonably small capital; or (3) intended to incur, or believed that it would incur, debts beyond its ability to pay such debts as they mature, such court could decide to invalidate, in whole or in part, the indebtedness constituting the CLO Assets as a fraudulent conveyance, to subordinate such indebtedness to existing or future creditors of the issuer or borrower or to recover amounts previously paid by the issuer or borrower in satisfaction of such indebtedness. In addition, in the event of the insolvency of an issuer or borrower of a CLO Asset, payments made on such CLO Asset could be subject to avoidance as a “preference” if made within a certain period of time (which may be as long as one year under U.S. Federal bankruptcy law or even longer under state laws) before insolvency.

The CLO Assets of the CLOs in which the Fund invests may be subject to various laws for the protection of debtors in other jurisdictions, including the jurisdiction of incorporation of the issuer or borrower of such CLO Assets and, if different, the jurisdiction from which it conducts business and in which it holds assets, any of which may adversely affect such issuer’s or borrower’s ability to make, or a creditor’s ability to enforce, payment in full, on a timely basis or at all. These insolvency considerations will differ depending on the jurisdiction in which an issuer or borrower or the related CLO Assets are located and may differ depending on the legal status of the issuer or borrower.

U.S. Risk Retention. In October 2014, six federal agencies (the Federal Deposit Insurance Corporation, or the “FDIC,” the Comptroller of the Currency, the Federal Reserve Board, the SEC, the Department of Housing and Urban Development and the Federal Housing Finance Agency) adopted joint final rules implementing certain credit risk

retention requirements contemplated in Section 941 of the Dodd-Frank Act, or the “Final U.S. Risk Retention Rules.” These rules were published in the Federal Register on December 24, 2014. With respect to the regulation of CLOs, the Final U.S. Risk Retention Rules require that the “sponsor” or a “majority owned affiliate” thereof (in each case as defined in the rules), will retain an “eligible vertical interest” or an “eligible horizontal interest” (in each case as defined therein) or any combination thereof in the CLO in the manner required by the Final U.S. Risk Retention Rules.

The Final U.S. Risk Retention Rules became fully effective on December 24, 2016, and to the extent applicable to CLOs in which the Fund invests, the Final U.S. Risk Retention Rules contain provisions that may adversely affect the return of the Fund’s investments. On February 9, 2018, a three-judge panel of the United States Court of Appeals for the District of Columbia Circuit, or the “DC Circuit Court,” rendered a decision in The Loan Syndications and Trading Association v. Securities and Exchange Commission and Board of Governors of the Federal Reserve System, No. 1:16-cv-0065, in which the DC Circuit Court held that open market CLO collateral managers are not “securitizers” subject to the requirements of the Final U.S. Risk Retention Rules (the “DC Circuit Ruling”). Thus, collateral managers of open market CLOs are no longer required to comply with the Final U.S. Risk Retention Rules at this time. As such, it is possible that some collateral managers of open market CLOs will decide to dispose of the securities (or cause their majority owned affiliates to dispose of the securities) constituting the “eligible vertical interest” or “eligible horizontal interest” they were previously required to retain or take other actions with respect to such securities that is not otherwise prohibited by the Final U.S. Risk Retention Rules. To the extent either the underlying collateral manager or its majority-owned affiliate divests itself of such securities, or to the extent none of the underlying collateral manager or its affiliates holds any CLO securities in any event, this will reduce the degree to which the relevant collateral manager’s incentives are aligned with those of the holders of the CLO debt or equity (which may include the Fund as a CLO investor). This could influence the way in which the relevant collateral manager manages the CLO assets and/or makes other decisions under the transaction documents related to the CLO in a manner that is adverse to the Fund.

There can be no assurance or representation that any of the transactions, structures or arrangements currently under consideration by or currently used by CLO market participants will comply with the Final U.S. Risk Retention Rules to the extent such rules are reinstated or otherwise become applicable to open market CLOs. The ultimate impact of the Final U.S. Risk Retention Rules on the loan securitization market and the leveraged loan market generally remains uncertain, and any negative impact on secondary market liquidity for securities comprising a CLO may be experienced due to the effects of the Final U.S. Risk Retention Rules on market expectations or uncertainty, the relative appeal of other investments not impacted by the Final U.S. Risk Retention Rules and other factors.

EU/UK Risk Retention. The securitization industry in both European Union (“EU”) and the United Kingdom (“UK”) has also undergone a number of significant changes in the past few years. Regulation (EU) 2017/2402 relating to a European framework for simple, transparent and standardized securitization (as amended by Regulation (EU) 2021/557 and as further amended from time to time, the “EU Securitization Regulation”) applies to certain specified EU investors, and Regulation (EU) 2017/2402 relating to a European framework for simple, transparent and standardized securitization in the form in effect on 31 December 2020 (which forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (as amended, the “EUWA”)) (as amended by the Securitization (Amendment) (EU Exit) Regulations 2019 and as further amended from time to time, the “UK Securitization Regulation” and, together with the EU Securitization Regulation, the “Securitization Regulations”) applies to certain specified UK investors, in each case, who are investing in a “securitization” (as such term is defined under each Securitization Regulation).

The due diligence requirements of Article 5 of the EU Securitization Regulation (the “EU Due Diligence Requirements”) apply to each investor that is an “institutional investor” (as such term is defined in the EU Securitization Regulation), being an investor which is one of the following: (a) an insurance undertaking as defined in Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009 on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II) (recast) (“Solvency II”); (b) a reinsurance undertaking as defined in Solvency II; (c) subject to certain conditions and exceptions, an institution for occupational retirement provision falling within the scope of Directive (EU) 2016/2341 of the European Parliament and of the Council of 14 December 2016 on the activities and supervision of institutions for occupational retirement provision (IORPs) (the “IORP Directive”), or an investment manager or an authorized entity appointed by an institution for occupational retirement provision pursuant to the IORP Directive; (d) an alternative investment fund manager (“AIFM”) as defined in Directive 2011/61/EU of the European Parliament and of the Council of 8 June 2011 on Alternative Investment Fund Managers that manages and/or markets alternative investment funds in the EU; (e) an undertaking for the collective investment in transferable securities (“UCITS”) management company, as defined in Directive 2009/65/EC of the European

Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS) (the “UCITS Directive”); (f) an internally managed UCITS, which is an investment company authorized in accordance with the UCITS Directive and which has not designated a management company authorized under the UCITS Directive for its management; or (g) a credit institution as defined in Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms (the “CRR”) for the purposes of the CRR, or an investment firm as defined in the CRR, in each case, such investor an “EU Institutional Investor”.

The due diligence requirements of Article 5 of the UK Securitization Regulation (the “UK Due Diligence Requirements” and, together with the EU Due Diligence Requirements, the “Due Diligence Requirements”) apply to each investor that is an “institutional investor” (as such term is defined in the UK Securitization Regulation), being an investor which is one of the following: (a) an insurance undertaking as defined in the Financial Services and Markets Act 2000 (as amended, the “FSMA”); (b) a reinsurance undertaking as defined in the FSMA; (c) an occupational pension scheme as defined in the Pension Schemes Act 1993 that has its main administration in the UK, or a fund manager of such a scheme appointed under the Pensions Act 1995 that, in respect of activity undertaken pursuant to that appointment, is authorized under the FSMA; (d) an AIFM (as defined in the Alternative Investment Fund Managers Regulations 2013 (the “AIFM Regulations”)) which markets or manages AIFs (as defined in the AIFM Regulations) in the UK; (e) a management company as defined in the FSMA; (f) a UCITS as defined by the FSMA, which is an authorized open ended investment company as defined in the FSMA; (g) a FCA investment firm as defined by the CRR as it forms part of UK domestic law by virtue of EUWA (the “UK CRR”); or (h) a CRR investment firm as defined in the UK CRR, in each case, such investor a “UK Institutional Investor” and, such investors together with EU Institutional Investors, “Institutional Investors”.