Exhibit 99.1

Calle La Colonia N° 150

Urb. El Vivero - Santiago de Surco

Tel: 317-6000

Lima, April 6, 2026

Sirs

Superintendencia del Mercado de Valores – SMV

Intendencia General de Supervisión de Conductas

| Attention: | Alix Godos |

| General Superintendent | |

| General Superintendency of Conduct Supervision |

| Reference: | Official Letter Nº 1383-2026-SMV/11.1 |

Dear Sirs:

Pursuant to the referenced Official Letter, Cementos Pacasmayo S.A.A. hereby submits its responses to the requests contained therein for communication as a Material Event

In compliance with your request, we hereby submit as a Material Event the written response, which is included as an Annex to this communication.

Sincerely,

CEMENTOS PACASMAYO S.A.A.

Diego Roda Lynch

Stock Market Representative

Calle La Colonia N° 150

Urb. El Vivero - Santiago de Surco

Tel: 317-6000

Lima, April 6, 2026

Sirs

SUPERINTENDENCIA DEL MERCADO DE VALORES – SMV

Intendencia General de Supervisión de Conductas

Present.-

| Attention: | Sr. Alix Godos |

| General Superintendent | |

| General Superintendency of Conduct Supervision |

| Reference: | Official Letter No. 1383-2026-SMV/11.1 |

Dear Sirs,

CEMENTOS PACASMAYO S.A.A. (the “Company”), holding Taxpayer Identification Number (RUC) No. 20419387658, with its registered office at Calle La Colonia N° 150, district of Santiago de Surco, province and department of Lima, duly represented by Mr. Diego Roda Lynch, identified by DNI No. 09753981, in his capacity as Stock Market Representative, respectfully states:

That on March 27, 2026, the Company was notified of Official Letter No. 1383-2026-SMV/11.1 (the “Official Letter 1383”), through which the General Superintendency of Conduct Supervision (the “Superintendency”) of the Superintendency of the Securities Market (“SMV”) issued various information requests regarding expenses registered under the heading “Expenses associated with the Holcim acquisition” in the Company’s Audited Financial Statements as of December 31, 2025 (the “Transaction Expenses”) and the agreements adopted at the Annual General Mandatory Shareholders’ Meeting held on March 24, 2026 (the “2026 AGM”).

Furthermore, we refer to the Material Event dated December 16, 2025, by virtue of which the Company informed the market that the majority shareholders of Inversiones ASPI S.A. (“ASPI”), owners of 50.01% of the Company’s capital stock, entered into a Share Purchase Agreement (the “SPA”) with Holcim Ltd. (“Holcim”) for the sale of 99.99% of ASPI shares in favor of the Swiss corporation Holcim Ltd., under the terms and conditions established in said contract (the “Transaction”).

2

In this regard, within the period granted to address the points expressed in the aforementioned Official Letter, we proceed to respond to each of the aspects mentioned therein, in the order in which they were included.

| I. | REGARDING THE AGM OF 03/24/26. |

| 1. | The directors elected at the 2026 AGM were the same board members from the immediately preceding period and, therefore, were and are aware of the information requests sent by the SMV, including the request sent via Official Letter No. 1197-2026-SMV/11.1 (the “Official Letter 1197”). |

Furthermore, on March 30, 2026, and within the context of the closing of the Transaction, we reported via a Material Event the resignation from the Board of Directors of Mr. Eduardo Hochschild Beeck and Ms. Ana Sofia Hochschild Correa, with Mr. Simon Rolf Kronenberg and Mr. Santiago María Ojea Quintana being elected as their replacements. These replacement directors are also aware of the information requests sent by the SMV.

Additionally, regarding the knowledge of the Company’s shareholders, the content of Official Letter 1197 was disclosed to the market as a Material Event dated March 23, 2026—that is, prior to the holding of the 2026 AGM. During the course of said meeting, none of the shareholders made any inquiries or observations specifically regarding Official Letter 1197.

| 2. | The reduction in net income for the year 2025 did not affect the amount of dividends distributed during said fiscal year. In this regard, since 2023, the Company has been distributing S/ 190.3 million in dividends annually. Along the same lines, in 2025, the Board of Directors meeting held on October 21, 2025, approved the distribution of the sum of S/ 190,300,410.65 as dividends (considering the total shares of the Company, including investment shares of its own issuance held by the Company), which were timely paid to the Company’s shareholders on December 4, 2025. |

Likewise, to date, the Company’s retained earnings (which include the results of the 2025 fiscal year) amount to the sum of S/ 264 million. In that sense, as of today, in the hypothetical case that the Board of Directors decided to approve the distribution of dividends based on the delegation from the 2026 AGM, the Company would be in a position to distribute dividends charged against retained earnings obtained as of December 31, 2025, in the same amount it has been distributing since 2023. The decision to distribute dividends, however, rests solely with the General Shareholders’ Meeting and the Company’s Board of Directors based on the powers delegated to them.

It should be noted that the statements included in the Company’s Annual Report corresponding to the 2025 fiscal year, which are cited in Official Letter 1383, are consistent with the information reported to the market through the Press Release corresponding to the Financial Statements for the fourth quarter of 2025 (communicated via Material Event on February 12, 2026), where the specific impact of the Transaction Expenses on both the consolidated EBITDA and the Company’s net income was described in detail.

| 3. | A copy of the minutes of the 2026 AGM (the “2026 AGM Minutes”) is being submitted separately and on a confidential basis to the SMV. While the text has been approved by the shareholders intended to sign, the document is currently awaiting one remaining signature¹.The content complies with the provisions of the General Corporations Act. Regarding the confidential nature of the 2026 AGM Minutes, we respectfully request that the confidential nature of private documents of legal entities be taken into account; specifically, those documents containing matters of a private nature to the Company and which are of interest only to its shareholders, who must prove their status as such to participate in general shareholders’ meetings or access information therefrom. These non-public documents are protected under the Political Constitution of Peru, as they fall within the scope of personal privacy and the constitutional guarantees of secrecy and inviolability of private communications and documents. |

3

There is no recording or verbatim transcript of the session other than what is incorporated into the corresponding minutes. In this regard, Article 135 of the General Corporations Act does not require an additional transcript or recording of the session. The referred article states that the minutes of each meeting must record the place, date, and time it was held; an indication of whether it was held upon first, second, or third call; the names of the shareholders present or those representing them; the number and class of shares they hold; the names of those acting as chairman and secretary; an indication of the dates and newspapers in which the notices of the call were published; and the method and result of the votes and the agreements adopted—all of which are requirements met by the 2026 AGM Minutes being submitted.

Furthermore, we clarify that it is not the Company’s practice to make recordings or videos of these sessions, as the transcript contained in the minutes is sufficient support for the interventions of the Chairman, the Secretary, and the shareholders. As reflected in the submitted minutes, the document includes transcripts of the statements made by shareholder representatives—including the Pension Fund Administrators (AFPs)—detailing their voting positions and the responses provided by Company management to their inquiries. It should be noted that the four AFPs have confirmed their agreement with the text of the minutes, which accurately reflect their questions, statements, and the responses provided during the session.

Regarding the existence of any fairness opinion or technical support to validate the assumption of the Transaction Expenses, we clarify that no report of this nature was required or requested for the purposes of the 2026 AGM. As we have stated in our previous filings, including the document dated March 17, 2026, through which we responded to Official Letter 1004-2026-SMV/11.1 (the “Official Letter 1004”), the payment of the Transaction Expenses does not reach or exceed the threshold of 5% of the Company’s assets provided for in literal c) of Article 53 of the Unified Ordered Text (T.U.O.) of the Securities Market Law (“LMV”), nor does it qualify as a transaction between related parties, and therefore was not required to comply with the procedures and requirements set forth in that regulation.

| 4. | The interventions and inquiries made by the shareholders, as well as the responses thereto, are recorded in the 2026 AGM Minutes. |

| 5. | The inquiries made by the shareholders regarding the agenda items of the 2026 AGM are recorded in the 2026 AGM Minutes. |

| 6. | The inquiries made by the shareholders regarding the Transaction Expenses during the 2026 AGM are recorded in the 2026 AGM Minutes. |

| 7. | The responses to the shareholders’ inquiries are recorded in the 2026 AGM Minutes. |

| 8. | No additional document, presentation, or report was exhibited during the 2026 AGM in relation to the Transaction Expenses. |

Notwithstanding the above, it was stated during the 2026 AGM that the Company had requested a report or opinion from an independent third-party expert to certify the existence of the Company’s prior contractual agreement with the Chief Executive Officer regarding the payment of his performance bonus, as well as the nature of the payment made.

To date, the referred reports have been issued and also submitted to the SMV via a confidential filing dated March 27, 2026.

4

| 9. | The voting results for each of the agenda items addressed in the 2026 AGM are recorded in the 2026 AGM Minutes. Likewise, said minutes reflect the direction of the votes cast by the pension funds managed by the AFPs, in compliance with the provisions established by Supreme Decree No. 182-2003-EF and as expressly requested by them during the session. |

| 10. | Shareholders who cast votes against or abstentions on the agenda items did not submit supporting documentation. Said shareholders cast their votes directly, or through their representatives, during the 2026 AGM session. All of this is recorded in the 2026 AGM Minutes. |

Regarding the second inquiry under this numeral, we indicate that the General Shareholders’ Meeting approved the 2025 Financial Statements and the Company’s Annual Report in accordance with the powers granted by Article 114 of the General Corporations Act.

Pursuant to Article 111 of the aforementioned law, the General Shareholders’ Meeting is the highest governing body of the company. Shareholders assembled in a duly convened meeting with the requisite quorum shall decide, by the legally established majority, on all matters within the Meeting’s authority.

In that sense, the approval of the corporate management, the 2025 Financial Statements, and the Annual Report was adopted at the 2026 AGM, duly convened, with the required quorum and by the vote of the absolute majority of the subscribed shares with right to vote represented therein, in accordance with the provisions of Article 127 of the General Corporations Act.

| II. | REGARDING THE S/ 5.9 MILLION THAT MR. HOCHSCHILD WILL PAY TO CEMPACASMAYO. |

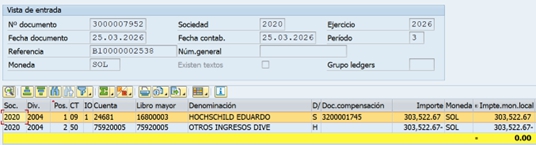

| 11. | The amount of S/ 5,904,535.66 is a sum equivalent to the total amount paid and registered for legal, tax, and financial advisory fees as part of the Transaction Expenses, amounting to S/ 5,601,013.00, plus the VAT (IGV) corresponding to the fees of non-domiciled advisors amounting to S/ 303,522.66, which were assumed, registered, and paid by the Company in accordance with the approval of its Board of Directors. |

| 12. | Mr. Eduardo Hochschild was a Director and held the position of Chairman of the Board until March 30, 2026, and, in that sense, requested to be informed of the amount of legal, tax, and financial advisory fees that were part of the Transaction Expenses. Said information was provided to him verbally. |

Mr. Eduardo Hochschild stated his voluntary decision to pay the Company the referred amount through his intervention at the 2026 AGM, as well as through a letter sent to the Company dated March 24, 2026, as a discretionary act(a título de liberalidad), in response to the dissatisfaction expressed by some of the Company’s shareholders and the repeated official letters from the SMV of which he had become aware.

| 13. | We have no knowledge of any report in this regard, and the Company has not requested the preparation of any. Notwithstanding the above, see our response to question 14. |

| 14. | Mr. Eduardo Hochschild stated his unilateral decision to pay the referred amount to the Company through his verbal intervention at the 2026 AGM session. Additionally, on March 24, 2026, Mr. Hochschild sent a communication to the Company expressing his intention to make a payment of S/ 5,904,535.66 in favor of the Company (without requiring any consideration from the Company). Said discretionary act was accepted by the Company on that same date through a written communication accepting the offer of payment, proceeding to register the respective account receivable. The signatures on the referred letters were notarized on said date. Furthermore, on April 6, 2026, Mr. Eduardo Hochschild and the Company entered into a donation contract in order to formalize said discretionary act. A copy of the referred communications is being sent through confidential channels and directly to the SMV due to their confidential nature. As for the donation contract signed on April 6, 2026, it will be sent tomorrow to the SMV along with a legal opinion regarding the legal nature of the payment made, also through confidential channels and directly to the SMV. |

5

| 15. | The decision to accept the payment offered by Mr. Eduardo Hochschild was stated by the Company through a letter dated March 24, 2026, duly signed by its Chief Executive Officer in the exercise of his corresponding powers. This decision by the Company has also been formalized through the execution of the donation contract dated April 6, 2026, between Mr. Eduardo Hochschild and the Company. |

| 16. | The payment constitutes a donation and will be treated as such for accounting and tax purposes. In this regard, see our response to question 14. |

| 17. | We are not aware of the motivation for said decision beyond what is indicated in point 12 above—that is, what was expressed in the 2026 AGM Minutes and in his letter dated March 24, 2026. The payment does not constitute an admission of any kind, but rather a discretionary act by Mr. Eduardo Hochschild. The expenditure incurred in 2025 for the payment of legal, financial, and tax advisors was and continues to be an expense validly incurred by the Company, in accordance with the approval of its Board of Directors on November 17, 2025, and registered as its own expense in its 2025 Audited Financial Statements. |

| 18. | This is not a reimbursement or refund of expenses that do not belong to the Company. In this sense, it does not qualify as a “Prior Period Error Correction” under IAS 8 and IFRS. |

Furthermore, it is important to clarify that the payment made by Mr. Hochschild does not affect the Company’s financial statements corresponding to the 2025 fiscal year; therefore, the Company does not consider it appropriate, nor does it intend to present new financial statements for said period.

The Company has reached this conclusion considering that: (i) the referred payment was made as a donation and, as such, implies a transfer of resources as discretionary act and in the absence of consideration; (ii) the assumption by the Company of the legal, tax, and financial advisory fees that were part of the Transaction Expenses, and the payment made by Mr. Hochschild, correspond to separate economic events; and (iii) the payment made by Mr. Hochschild corresponds to a subsequent event occurring after the 2025 fiscal year.

In view of the above, the donation made by Mr. Hochschild in the year 2026 does not qualify as a reimbursement or refund but rather corresponds to income for the 2026 fiscal year.

Regarding the application of IAS 8, titled “Accounting Policies, Changes in Accounting Estimates and Errors,” the objective of this standard is to prescribe the criteria for selecting and changing accounting policies, together with the accounting treatment and disclosure of changes in accounting policies, changes in accounting estimates, and corrections of errors.

The payment decision made by Mr. Hochschild as a donation does not qualify, by definition, as a change in any accounting policy nor a change in an accounting estimate; therefore, it would only be appropriate to analyze whether it could qualify as a correction of a prior period error.

In this regard, according to the aforementioned IAS 8, paragraph 5, “prior period errors” are omissions from, and misstatements in, the entity’s financial statements for one or more prior periods arising from a failure to use, or misuse of, reliable information that: (i) was available when the financial statements for those periods were authorized for issue; and (ii) could reasonably be expected to have been obtained and taken into account in the preparation and presentation of those financial statements.

Such errors include the effects of mathematical mistakes, mistakes in applying accounting policies, oversights or misinterpretations of facts, and fraud.

6

The donation made by Mr. Hochschild in the current 2026 fiscal year cannot be considered information that was available for the preparation of the 2025 financial statements and, therefore, could not have caused a misinterpretation of facts, for the following reasons:

| a. | It cannot be considered a misinterpretation of facts: The accounting entry made in 2025 for the Transaction Expenses assumed by the Company, including legal, tax, and financial advisory fees, was performed taking into consideration the approval of the Company’s Board of Directors at the meeting held on November 17, 2025. Therefore, the Company was the entity obligated to pay said expenses in 2025. Consequently, the invoices issued in the name of the Company were registered and paid by the Company as its own obligations in December 2025. |

Notably, the Company’s Audit Committee and Board of Directors approved the 2025 audited financial statements (which received unqualified opinions) during their respective meetings on February 12, 2026. As a matter of public record, the Transaction Expenses were expressly and transparently disclosed within these statements.

On the other hand, Mr. Hochschild’s decision to make the aforementioned donation in favor of the Company (for an amount equivalent to the fees for legal, tax, and financial advisors assumed by the Company) is a new event of a different economic nature, which corresponds to the year 2026 and, as such, is recorded in said year.

As previously indicated, the fact that Mr. Hochschild decided to pay the Company an amount equivalent to the expenses assumed by it does not mean that they should have been originally assumed by the previous controlling shareholder. Being two separate economic events, it is clear that this cannot be treated as a misinterpretation that leads to an error in the preparation of the Company’s financial statements.

| b. | There was no information available that the donation would be made as of December 31, 2025: As of December 31, 2025, the possibility of Mr. Hochschild making a donation in favor of the Company did not exist; therefore, there was no enforceable right, nor information that would allow for the recognition of an account receivable for such concept. Likewise, there was no information related to a potential donation to be made by Mr. Hochschild. The decision to make this donation was communicated to the Company on March 24, 2026. |

Therefore, as of December 31, 2025, there was no information available regarding a donation from Mr. Hochschild that should have been considered for the purposes of preparing the financial statements for the 2025 fiscal year, nor information that could be misinterpreted and, consequently, lead to an error in the preparation of the financial statements for said year.

In view of the foregoing, the premises for the use of IAS 8 (NIC 8) are not applicable to the donation made by Mr. Hochschild in the current 2026 fiscal year. Therefore, it is not appropriate to make any changes to the Company’s financial statements as of December 31, 2025.

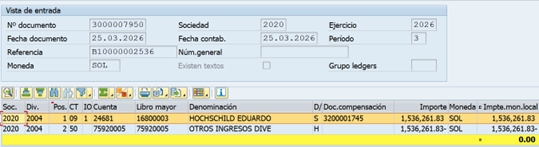

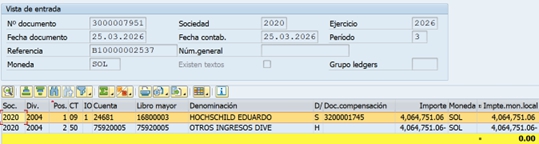

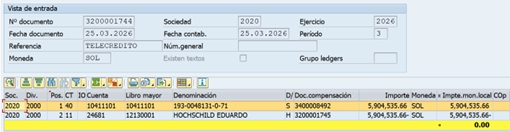

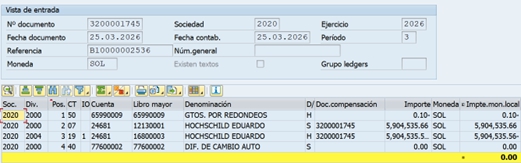

| 19. | Following receipt of the letter dated March 24, 2026, in which Mr. Hochschild committed to a donation to the Company, an accounting entry was recorded that month. This entry recognized an account receivable (debit) and sundry income (credit) in the amount of S/ 5,904,535.66. |

For greater precision, the accounting records and accounts used are: (i) account 16800003 for the registration of the account receivable from Mr. Eduardo Hochschild, and (ii) account 75920005 as the offset for the concept of other sundry income.

A copy of the corresponding accounting entry logs is attached as Annex 1 to this communication.

| 20. | Regarding Mr. Hochschild’s donation, it is important to clarify that this amount does not technically constitute a “reimbursement”. Instead, it is classified as income from third party transactions. As an inflow that increases the Company’s equity without originating from a permanent source the disposal of assets, or qualifying as imputed income, this payment will be recognized as taxable income for the 2026 fiscal year, the period in which it was received. |

Regarding the legal, tax, and financial advisory fees included in the Transaction Expenses, the Company has elected not to deduct them for 2025 Income Tax purposes. This decision was made on a precautionary basis, as these fees may not strictly satisfy the principle of causality under Article 37 of the Income Tax Law, specifically, the requirement that expenses be directly linked to generating taxable income or maintaining its source.

7

This tax treatment does not alter the underlying economic rationale for the Company’s decision to assume these costs. These disbursements served a legitimate corporate purpose (fin social), as detailed in our disclosures to the SMV and as determined the Board of Directors. Consequently, while this reflects an exercise of tax prudence, it does not diminish the validity, timing, or commercial justification for incurring these expenses for the benefit of the Company and its shareholders.

| 21. | The Company has requested a legal report from a third party regarding the nature of the payment in the amount of S/ 5,904,535.66 made by Mr. Eduardo Hochschild in favor of the Company, a copy of which will be presented to the SMV as indicated in response to question 14. The Company considers that said payment constitutes extraordinary income for the Company, which will be reflected for accounting, financial, and tax purposes in accordance with applicable regulations. |

| 22. | The Transaction Expenses are expenses of the Company, as we have explained in our previous filings, and it did not correspond to Mr. Eduardo Hochschild to assume them. |

Mr. Eduardo Hochschild’s decision to pay the Company an amount equivalent to the amount paid for legal, tax, and financial advisory fees as part of the Transaction Expenses is an exclusive and unilateral decision of Mr. Eduardo Hochschild.

| 23. | To date, there is no agreement between Pacasmayo and Holcim, its shareholders, or directors. Furthermore, we have no knowledge of any agreement between Holcim, its shareholders, directors, or affiliates with any director or shareholder affiliated with Pacasmayo. |

Notwithstanding the foregoing, we cannot rule out that, in the future, Holcim and Pacasmayo or their affiliates may enter into contracts in the ordinary course of business and with the formalities required by applicable law. Should that be the case, the Company will disclose what is appropriate in accordance with applicable regulations.

| 24. | We have no information regarding any situation of conflict of interest. |

Notwithstanding the above, we mention: (1) the board meeting minutes dated September 9, 2025, submitted to the SMV as part of the request for confidential material event status, in which, among others, the Company’s participation in the due diligence process and in the agreements that the controlling shareholder maintains with Holcim and any third party for the potential transfer of its shares was approved, recording the abstentions of Mr. Eduardo Hochschild Beeck and Ms. Ana Sofía Hochschild Correa; and (2) the board meeting held on November 17, 2025, in which the Board agreed, among others, (i) that the Company make a donation to UTEC, with the abstention of directors Eduardo Hochschild Beeck and Ana Sofía Hochschild Correa; (b) that the Company assume certain costs and fees related to the Transaction, such as legal, financial, and tax advisory fees, as well as certain bonuses, with the abstention of directors Eduardo Hochschild Beeck and Ana Sofía Hochschild Correa; and (c) that, should the agreements to finalize the potential Transaction be signed, the compensation paid to the Chief Executive Officer by virtue of the agreement previously signed with the Company be considered as part of the costs derived from the potential Transaction, recognizing that the payment corresponded to a contractual obligation assumed by the Company in advance, with the abstentions of directors Humberto Nadal del Carpio, Eduardo Hochschild Beeck, and Ana Sofía Hochschild Correa.

| 25. | The corresponding supporting information is submitted to the SMV in accordance with the indications in the preceding numerals, as well as in previous response letters to information requests formulated by the SMV. |

| 26. | We have indicated the necessary clarifications within this written statement. |

| 27. | We have no knowledge of any additional support information and/or documentation. |

We request that the foregoing be taken into account and that the information requests sent to the Company be considered solved.

Without further ado, we remain sincerely yours.

Sincerely,

Cementos Pacasmayo S.A.A.

Diego Roda Lynch

Stock Market Representative

8

Annex 1

Below are the accounting entries:

1.- Accounting entries for the generation of the account receivable and income:

2. Accounting entry for the credit to the Company’s account:

Recording of the credit entry:

3. Accounting entry for the clearing of the generated account receivable:

|

|

Firmado Digitalmente por: GODOS GARCIA Alix Fernando FAU 20131016396 soft Fecha: 27/03/2026 15:11:28 |

“Decenio de la Igualdad de Oportunidades para Mujeres y Hombres”

“Año de la Esperanza yel Fortalecimiento de la Democracia”

| San Isidro, March 27, 2026 |

OFICCIAL LETTER Nº 1383-2026-SMV/11.1

Mr.

Humberto Nadal del Carpio

Chief Executive Officer

Cementos Pacasmayo S.A.A.

Calle La Colonia Nº 150, Urbanización El Vivero, Surco

Present.-

| Ref.: | (1) Material Events of 24/03/261 2 | |

| (2) Material Event of 23/03/263 | ||

| Case Nº 2025054605 |

We address you regarding the supervision of the material events (1) and (2) of the reference (hereinafter, HI-23/03/26 and HI/24-03-26) disclosed by Cementos Pacasmayo S.A.A. (hereinafter, CEMPACASMAYO), and the information linked to operating expenses for S/ 77.6 Million and S/ 75.9 Million, under the concept of «Expenses associated with the Holcim acquisition» (hereinafter, HOLCIM EXPENSES), which is disclosed in your 2025 Audited Consolidated Annual Financial Statements (2025 Consolidated FS), in your 2025 Audited Separate Annual Financial Statements (2025 Separate FS); and in your 2025 Annual Report; which were approved on March 24, 2026, at the 2026 Annual General Shareholders’ Meeting (AGSM). 4

On page 147 of the 2025 Annual Report of CEMPACASMAYO, it is expressly stated:

«Net income was S/. 154.2 million, a decrease of 22.5% compared to 2024, mainly due to the increase in non-recurring operating expenses associated with the share purchase agreement with Holcim for the acquisition of Inversiones ASPI S.A. of the Hochschild Group, the company that controls 50.01% of Cementos Pacasmayo S.A.A. Without the expenses related to the acquisition, net income would have been S/. 231.8 million, which represents an increase of 16.5%. Likewise, the net profit margin decreased 2.8 percentage points, reaching 7.3% in this period.

Consolidated EBITDA was S/. 506.6 million, a decrease of 7.8% compared to 2024, mainly due to the expenses related to the acquisition mentioned above. Without these extraordinary expenses, consolidated EBITDA would have been S/. 584.2 million, an increase of 6.4%.»

| 1 | Agreements of the 2026 Annual Mandatory Shareholders’ Meeting, see web link: https://www.smv.gob.pe/ConsultasP8/documento.aspx?vidDoc={6016239D-0000-C011-8BE8-1A3F3B0DF024} |

| 2 | Approval of 2025 FS and Sworn Statement of full compliance with IFRS. See web link: web: https://www.smv.gob.pe/ConsultasP8/documento.aspx?vidDoc={5017239D-0000-CE10- B6FC-70E5D24D93D4} |

| 3 | HI-23/03/26. Additional time is requested to respond to Requirements of Official Letter No. 1197-2026-SMV/11.1. See web link: https://www.smv.gob.pe/SIMV/Content/images/descarga.png |

| 4 | In this document, the emphasis and underlining of the transcribed and drafted texts have been added. |

| Av. Paseo de la República | |

| 3617 San Isidro | |

| Central : 610-6300 | |

| www.smv.gob.pe | |

| Página 1 de 6 |

| |

“Decenio de la Igualdad de Oportunidades para Mujeres y Hombres”

“Año de la Esperanza yel Fortalecimiento de la Democracia”

In this regard, it is necessary to indicate that by means of Official Letter No. 1197-2026-SMV/11.1 dated March 20, 2026 (hereinafter OFFICIAL LETTER 1197), information requirements were formulated to CEMPACASMAYO, and others were reiterated. The deadline to address all those requirements expires on March 27, 2026. The documentation related to the information requirements is found in Case File No. 2025054605

Information requirements

Under these premises and the applicable legal framework, as well as the supervisory powers of the SMV, especially those provided for in Article 27 of the HI Regulations, considering that your responses have the character of a sworn statement; your represented company is required to provide the following:

| I. | Regarding the agsm of 24/03/26 |

| 1. | Indicate whether the Directors of CEMPACASMAYO—including, if any, the newly elected ones—were informed; and at the AGSM about the pending requirements of OFFICIAL LETTER 1197. Specify if a full copy of said official letter was delivered to the Directors. | |

| If they were not informed, explain the reasons for it. |

| 2. | Considering that on page 147 of the 2025 Annual Report it is expressly stated: |

«Net income was S/. 154.2 million, a decrease of 22.5% compared to 2024, mainly due to the increase in non-recurring operating expenses associated with the share purchase agreement with Holcim for the acquisition of Inversiones ASPI S.A. of the Hochschild Group, the company that controls 50.01% of Cementos Pacasmayo S.A.A. Without the expenses related to the acquisition, net income would have been S/. 231.8 million, which represents an increase of 16.5%. Likewise, the net profit margin decreased 2.8 percentage points, reaching 7.3% in this period. Consolidated EBITDA was S/. 506.6 million, a decrease of 7.8% compared to 2024, mainly due to the expenses related to the acquisition mentioned above. Without these extraordinary expenses, consolidated EBITDA would have been S/. 584.2 million, an increase of 6.4%.»

It is verified that CEMPACASMAYO explicitly recognizes that the reduction of its net income and its 2025 EBITDA was caused by the recognition of the HOLCIM EXPENSES, which were accountingly recorded at the end of 2025; and with this, the amount of dividends to be distributed was also reduced. In this regard:

Provide all explanations and documentation related to these statements in the 2025 Annual Report, and explain why the dividends to be distributed to your 10 thousand minority shareholders were reduced in this manner, including the dividends of the pension funds of approximately 10 million people.

| Av. Paseo de la República | |

| 3617 San Isidro | |

| Central : 610-6300 | |

| www.smv.gob.pe | |

| Página 2 de 6 |

| |

“Decenio de la Igualdad de Oportunidades para Mujeres y Hombres”

“Año de la Esperanza yel Fortalecimiento de la Democracia”

| 3. | Certified copy of the minutes of the AGSM and the full transcript of the session.

Specifically, a detailed record of the inquiries made by the shareholders and the responses provided by the Board of Directors or others is required, regarding the reasonableness, causality, and direct benefit for CEMPACASMAYO of the expense of S/ 77.6 million before proceeding to the vote on the 2025 Financial Statements and 2025 Annual Report. |

|

| Specify if a «Fairness Opinion» report or technical support exists and was delivered or explained, which served to validate the assumption of expenses of a transaction between the third parties ASPI and Holcim. |

| 4. | If they exist, include the literal transcription and magnetic tape or video recording of the AGSM, of the interventions, questions, and answers provided by the administration to the shareholders, especially regarding the HOLCIM EXPENSES |

| 5 | Copy of all inquiries made by the shareholders regarding the agenda items of the AGSM. |

| 6 | Copy of the inquiries made regarding the S/ 77.6 Million of the HOLCIM EXPENSES, and a copy of the responses from the Board of Directors or Management. |

| 7. | Copy of the responses to all inquiries. |

| 8. | Copy of any additional document, presentation, or report exhibited during the AGSM in relation to the HOLCIM EXPENSES. |

| 9. | Detailed voting table: Report on the results of the voting for each agenda item, identifying the percentage of votes in favor, against, and abstentions. |

| 10. | In the event of abstentions or votes against, the documentation that supported said abstentions or votes against, and if no documents exist, report by what way and/or means said abstentions or votes against were formulated. | |

| Report if the Board of Directors resolved these technical reservations or the lack of conviction prior to the closing of the session; and why, despite the doubt or reservation of the shareholders and what was indicated on page 147 of the 2025 Annual Report, it was considered the best alternative to proceed with the approval of the social management, the 2025 FS, and said annual report. |

| II. | REGARDING THE S/ 5.9 MILLION THAT MR. HOCHSCHILD WILL PAY TO CEMPACASMAYO FOR LEGAL, TAX, AND FINANCIAL ADVISORS |

| 11. | Confirm and report if the amount of S/ 5.9 Million offered by Mr. Eduardo Hochschild is the same total amount that was paid and accountingly recorded between December 18, 2025, and December 31, 2025, by CEMPACASMAYO for «Legal advisor fees, Tax advisor fees, and Financial advisor fees», and as part of the HOLCIM EXPENSES referred to in the HI-03/03/26 of CEMPACASMAYO. |

| 12. | Report when and in what manner Mr. Eduardo Hochschild became aware that the “Legal advisor fees, Tax advisor fees, and Financial advisor fees” of the Transaction totaled S/ 5.9 Million. | |

| On what date and in what manner did CEMPACASMAYO inform him about said payments and total amount, or how is it that Mr. Hochschild offered that amount at the AGSM. |

| Av. Paseo de la República | |

| 3617 San Isidro | |

| Central : 610-6300 | |

| www.smv.gob.pe | |

| Página 3 de 6 |

| |

“Decenio de la Igualdad de Oportunidades para Mujeres y Hombres”

“Año de la Esperanza yel Fortalecimiento de la Democracia”

| 13. | Copy of the technical and legal reports that were considered and/or evaluated for Mr. Eduardo Hochschild to offer to pay those S/ 5.9 Million. In the event that no reports exist, please specify so expressly. |

| 14. | Copy of the document where Mr. Eduardo Hochschild formalizes his offer to pay those S/ 5.9 Million to CEMPACASMAYO, which has been reported as a material event in HI-24/03/26. |

| 15. | Copy of the Board of Directors’ minutes of CEMPACASMAYO where the payment of S/ 5.9 Million from Mr. Eduardo Hochschild is accepted, and where the nature of said payment and all its effects are evaluated. |

| 16. | Inform and support what the real and legal nature of this offer and/or payment by Mr. Eduardo Hochschild — final controlling shareholder of CEMPACASMAYO and Inversiones Aspi S.A.— of S/ 5.9 Million to CEMPACASMAYO is: |

Is it a donation?

Is it a reimbursement of third-party expenses?

Is it the payment or refund for the fees paid by CEMPACASMAYO to the advisors of the Transaction between Aspi and Holcim?

Is it a refund of the Chief Executive Officer bonus?, or

What is it?

| 17. | Report why Mr. Eduardo Hochschild, who is the owner of the controlling shareholder of CEMPACASMAYO (ASPI), has assumed an expense that the company defended as «operational and its own». | |

| Precise if that payment is an admission that the expense for the consultancies of the Transaction between Aspi and Holcim is an expense of either of these or both and Not of CEMPACASMAYO. |

| 18. | Regarding the S/ 5.9 Million from Mr. Eduardo Hochschild: In the event that it is actually a reimbursement or refund for expenses that do not belong to CEMPACASMAYO, report if the company will proceed with the presentation of new 2025 Financial Statements correcting the net income and the dividends to be distributed. Inform if this qualifies as a “Correction of Prior Period Errors” under IAS 8 and IFRS. |

| 19. | Explain the accounting treatment applied by CEMPACASMAYO to recognize those S/ 5.9 Million from Mr. Hochschild. Send a copy of all respective accounting registry entries. |

| 20. | Report on the analysis of all tax impacts of that offer or payment by Mr. Hochschild. Precise if that reimbursement entails the recognition that the original expenses for S/ 5.9 Million do not comply with the causality principle of Article 37 of the Income Tax Law, and if this fact will be recognized in the 2025 annual tax return before SUNAT. |

| Av. Paseo de la República | |

| 3617 San Isidro | |

| Central : 610-6300 | |

| www.smv.gob.pe | |

| Página 4 de 6 |

| |

“Decenio de la Igualdad de Oportunidades para Mujeres y Hombres”

“Año de la Esperanza yel Fortalecimiento de la Democracia”

| 21. | Copy of the technical/legal report in which all legal, accounting, financial, tax, corporate, corporate governance, or other effects have been evaluated, regarding the offer and/or payment of those S/ 5.9 Million from Mr. Hochschild; both for CEMPACASMAYO, for its governing bodies, and for the natural persons who integrate them. |

| 22. | Report on the reasons why Mr. Hochschild covered only S/ 5.9 Million and not the remaining S/ 71.7 Million (of the total S/ 77.6 Million of the HOLCIM EXPENSES). Present the technical support that differentiates the causality and benefit of these two groups of expenses for CEMPACASMAYO, detailing why the remaining balance should indeed be charged to the company and consequently to all shareholders, especially the minority shareholders. |

| 23. | Report whether or not there exists, or will or will not exist after the transfer of control over CEMPACASMAYO—from Aspi to Holcim Ltd.—any: (a) Agreement in which Holcim or its shareholders or its directors participate with CEMPACASMAYO; (b) Agreement in which Holcim or its shareholders or its directors or its affiliates participate with any director or shareholder or affiliate of CEMPACASMAYO or with CEMPACASMAYO. In each case, report on the nature and effects of the agreement, as well as the detail of the agreements or pacts referred to payments, remunerations, benefits, and considerations of any type or for any concept. |

| 24. | All information provided by the members of the Board of Directors, Managers, and main executives of CEMPACASMAYO regarding the existence and respective detail of any conflict of interest, real or potential, that they might have regarding the Transaction between ASPI and HOLCIM communicated in the HI-16/12/26. In the case that no information exists regarding said conflicts of interest, specify it expressly in your response. |

| 25. | Attach all supporting documentation necessary to evidence and back your responses. In the event that you do not have the specifically required documentation, please explain the reasons for it. |

| 26. | In case the texts of the present document—which are based on CEMPACASMAYO’s information—are not precise, please clarify them in a detailed and documented manner. |

| 27. | Report on any other additional information and/or supporting documentation related to the matters of this requirement. |

The present requirement must be addressed within a maximum period of four (04) business days, counted from the business day following the notification of this official letter, via the corresponding “Material Events” route of the MV Net System; except if you submit the magnetic or video recording of the AGSM of March 24, 2026, which must go through MV Net to Case File 2025054605. Furthermore, CEMPACASMAYO must include in its communication responding to the information requirements a copy of this official letter, under notice that the SMV will proceed with its respective dissemination, under the provisions of article 27, numeral 27.1, of the HI Regulations.

| Av. Paseo de la República | |

| 3617 San Isidro | |

| Central : 610-6300 | |

| www.smv.gob.pe | |

| Página 5 de 6 |

| |

“Decenio de la Igualdad de Oportunidades para Mujeres y Hombres”

“Año de la Esperanza yel Fortalecimiento de la Democracia”

Finally, your represented company is reminded that in compliance with the regulations cited in the previous information requirements and what is indicated in the «GUIDE FOR ORIENTATIVE SUPERVISION ON THE REGIME OF MATERIAL EVENTS OF ISSUERS: CRITERIA OF RELEVANCE AND DUTIES OF TRANSPARENCY» which was notified to you on January 20, 2026, through Circular No. 031-2026-SMV/11.1; you must comply with your obligation to keep the market informed in a truthful, sufficient, and timely manner regarding any act, fact, or set of circumstances with significant influence capacity, and must take the necessary measures to ensure full compliance with the obligations emanating from the securities market regulations, as well as to address the requirements made by the Superintendence of the Securities Market; being necessary to point out that failure to address said requirements is a conduct subject to sanction in accordance with the provisions of the Sanctions Regulation, approved by SMV Resolution No. 035-2018-SMV/01.5

| Without further ado, I remain yours truly. | |

| Sincerely, | |

| /s/ Alix Godos | |

| Alix Godos | |

| General Intendant | |

| General Intendancy of Conduct Supervision |

EGLL/MP/RPG

With copy to:

Mr. Sergio Espinosa Chiroque; Superintendente de Banca, Seguros y AFP

Mr. Mariano Álvarez de la Torre Jara, Gerente General AFP HABITAT

Mr. Aldo Ferrini Cassinelli, Gerente General AFP INTEGRA

Mr. Sergio Vélez Montes, Gerente General PRIMA AFP S.A.

Mr. Carlo Castoldi Crosby, Gerente General PROFUTURO AFP

Mr. Humberto Nadal del Carpio, CEO de Inversiones Aspi S.A.

Mr. Norberto Ledea, CEO Holcim Perú

Lima Stock Exchange (Bolsa de Valores de Lima S.A.)

| 5 | Ver enlace web: https://www.gob.pe/institucion/smv/normas-legales/7660778-031-2026-smv-11-1 |

| Av. Paseo de la República | |

| 3617 San Isidro | |

| Central : 610-6300 | |

| www.smv.gob.pe | |

| Página 6 de 6 |