S-K 1604, De-SPAC Transaction

Nov. 14, 2025

To the Shareholders of Live Oak Acquisition Corp. V:

You are cordially invited to attend the extraordinary general meeting of shareholders (the “”) of Live Oak Acquisition Corp. V (“”), which will be held at [ ] a.m., Eastern Time, on [ ], 2026. The board of directors of Live Oak (the “” or “ ”) has determined to convene and conduct the Live Oak Extraordinary General Meeting in a virtual meeting format at For the purposes of Live Oak’s Amended and Restated Memorandum and Articles of Association (the “”), the Live Oak Extraordinary General Meeting may also be attended in person at [ ]The accompanying proxy statement/prospectus includes instructions on how to access the virtual Live Oak Extraordinary General Meeting and how to listen, participate and vote from home or any remote location with internet connectivity. You or your proxy holder will be able to attend and vote at the Live Oak Extraordinary General Meeting by visiting and using a control number assigned by Continental Stock Transfer & Trust Company and printed on your proxy card. To register and receive access to the Live Oak Extraordinary General Meeting, registered shareholders and beneficial shareholders (those holding shares through a stock brokerage account or by a bank or other holder of record) of Live Oak will need to follow the instructions applicable to them provided in the accompanying proxy statement/prospectus.

Live Oak Extraordinary General Meeting

Live Oak

Board

Live Oak

Board

www.cstproxy.com/[ ].

Current Charter

.

www.cstproxy.com/[ ]

The Live Oak Board did not obtain a fairness opinion (or any similar report or appraisal) in connection with its determination to approve the Business Combination, including the securities to be issued in connection with, or the consideration to be delivered to, Teamshares Stockholders under the terms of the Merger Agreement.

Except for possibility that, prior to the Closing, Live Oak Securities held by the Sponsor may be distributed out of the Sponsor entity pursuant to the governing documents of the Sponsor, there are currently no specified circumstances or arrangements under which Live Oak Securities held by the Sponsor or its affiliates could be transferred, or that could result in the forfeiture, surrender or cancellation of such securities, subject to certain permitted exceptions for

pre-closing

distributions or transfers of Sponsor securities (subject, as applicable, to contractual lock-up

restrictions), provided, that it is possible that other pre-closing

changes to Sponsor securities could occur in connection with transaction financing arrangements, should any such arrangements or transactions be identified and pursued in connection with the Business Combination. This summary, together with the section entitled “Questions and Answers about the Live Oak Extraordinary General Meeting” highlights certain information contained in this proxy statement/prospectus and may not contain all of the information that is important to you. To better understand the Business Combination and the Proposals to be considered at the Live Oak Extraordinary General Meeting, you should read this entire proxy statement/prospectus carefully, including the annexes. See also the section entitled “Where You Can Find More Information” of this proxy statement/prospectus.

Unless otherwise indicated or the context otherwise requires, references in this summary to “Live Oak” refer to Live Oak Acquisition Corp. V and references to “Teamshares” refer to Teamshares Inc. prior to the Business Combination. References to “Combined Company” refer to Teamshares Inc., and include Teamshares and any other direct or indirect subsidiaries of Teamshares, (to the extent applicable) after giving effect to the Business Combination.

Unless otherwise specified, all share calculations assume no exercise of redemption rights by Live Oak’s public shareholders and do not include any shares issuable upon the exercise of the Warrants.

Proposals to be Voted on by Live Oak Shareholders

The Business Combination Proposal (Proposal 1)

Live Oak, Teamshares, Merger Sub and Merger Sub II have agreed to the Business Combination under the terms of the Merger Agreement, dated as of November 14, 2025, as amended by that certain First Amendment to the Merger Agreement, dated as of April 1, 2026. Pursuant to the terms and subject to the conditions of the Merger Agreement, at the Effective Time, respectively, of the Merger, among other things:

| • | all of the issued and outstanding capital stock of Teamshares as of immediately prior to the First Effective Time shall automatically be cancelled and cease to exist, in exchange for the rights of (A) each Teamshares Stockholder to receive its pro rata share of the Stockholder Merger Consideration (after giving effect to Liquidation Preference Elections by applicable holders of Teamshares preferred |

| stock and, thereafter, giving effect to the Company Preferred Stock Exchange or otherwise treating shares of Company Preferred Stock on an as-converted to Company Common Stock basis, but excluding treasury stock owned by Teamshares or a direct or indirect subsidiary) and (B) each eligible Earnout Participant to receive certain Earnout Shares, if any are issued in accordance with the terms and conditions of the Merger Agreement; |

| • | all outstanding “in-the-money” |

| • | all Teamshares warrants, convertible debt, “out-of the-money” options and other convertible securities outstanding and not exercised or converted prior to the First Effective Time will be terminated. |

Assuming the other Required Proposals are approved, Live Oak is asking its shareholders to vote upon a proposal to approve and adopt the Merger Agreement.

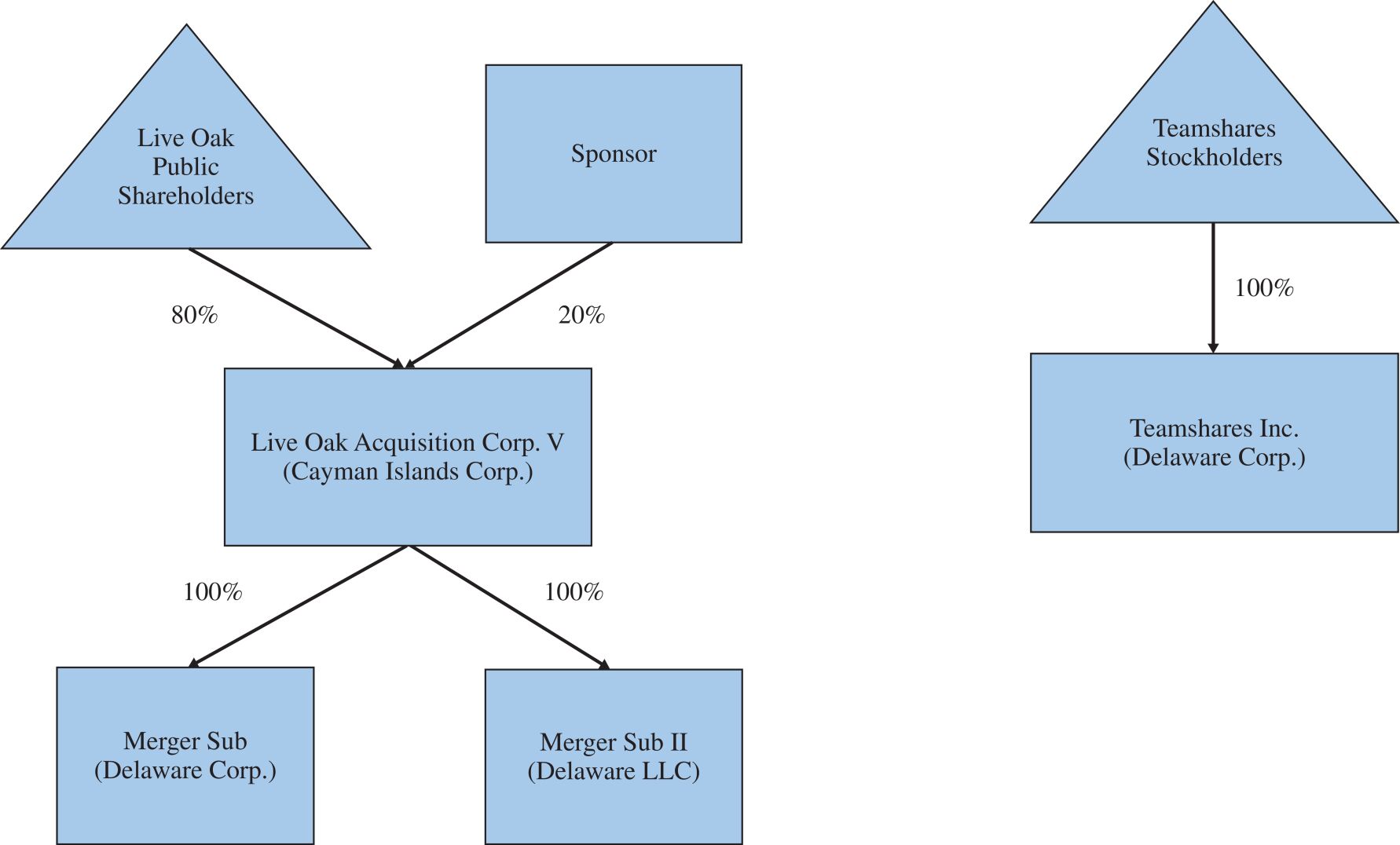

Organizational Structure

The diagram below depicts a simplified version of the current organizational structures of Live Oak and Teamshares prior to, and after, the consummation of the proposed Business Combination, taking into account various assumptions, as further described below and under the section of this proxy statement/prospectus entitled “” and as described under the presentation described as the “Assuming No Redemption” in the section entitled “.”

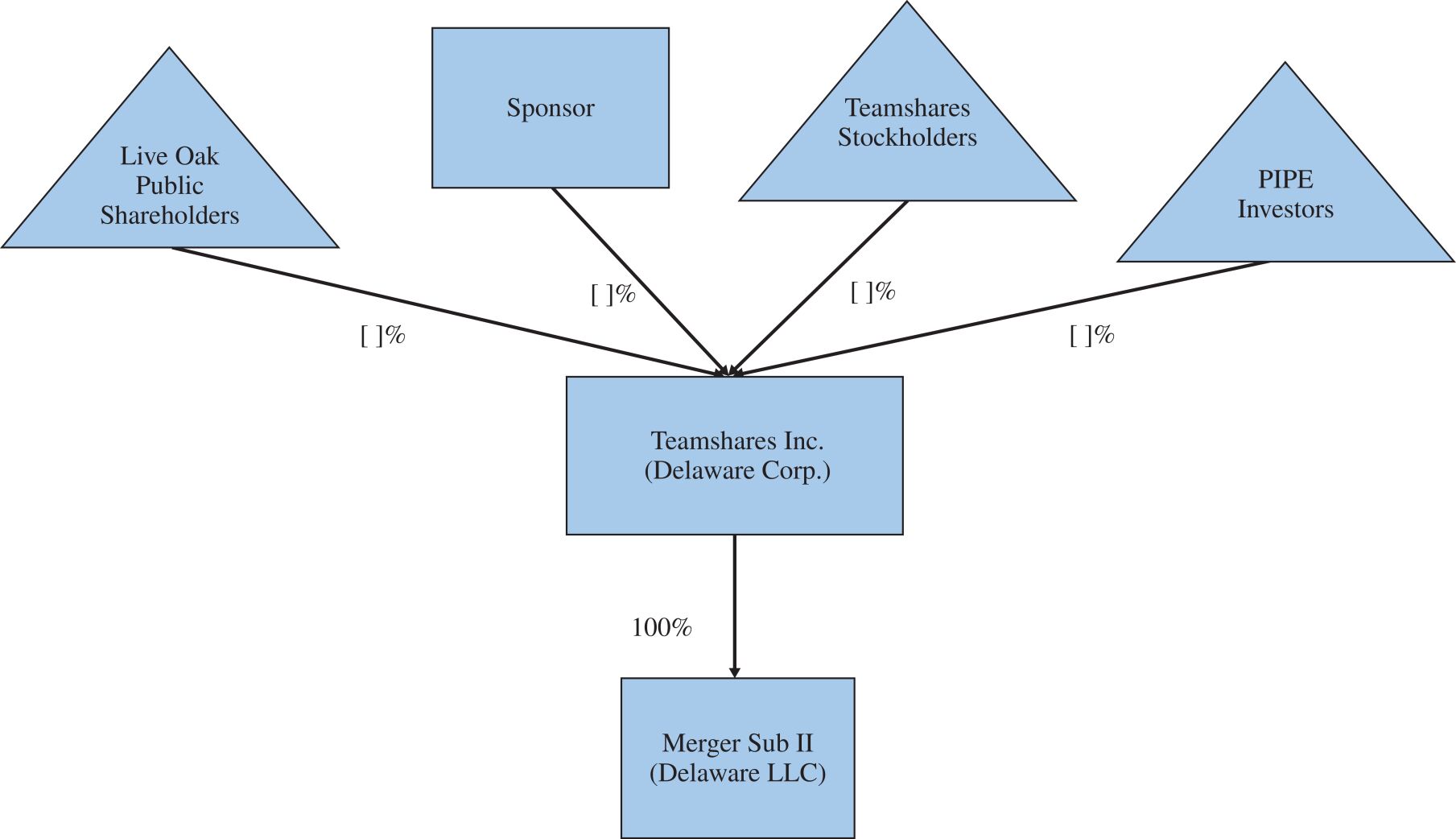

Share Calculations and Ownership Percentages

Unaudited Pro Forma Condensed Combined Financial Information

The diagram below depicts a simplified version of the Combined Company’s organizational structure immediately following the completion of the Business Combination, taking into account the assumptions identified in the caption above.

The Domestication Proposal (Proposal 2)

Live Oak is asking its shareholders to consider and vote on a proposal to approve, by special resolution of the Live Oak Class B Shareholders, (a) to change the domicile of Live Oak pursuant to a transfer by way of continuation of an exempted company out of the Cayman Islands and a domestication into the State of Delaware as a corporation; (b) the adoption upon the Domestication taking effect, the certificate of incorporation in the form appended to the accompanying proxy statement/prospectus as , in place of Live Oak’s Current Charter and which will remove or amend those provisions of Live Oak’s Current Charter that terminate or otherwise cease to be applicable as a result of the Domestication; and (c) the filing of a Certificate of Corporate Domestication and the Interim Charter with the Secretary of State of Delaware, under which Live Oak will be transferred by way of continuation out of the Cayman Islands and domesticated as a corporation in the State of Delaware. Only the Live Oak Class B Shareholders will carry the right to vote to transfer Live Oak by way of continuation in a jurisdiction outside the Cayman Islands (including, but not limited to, the approval of the organizational documents of Live Oak in such other jurisdiction). The Domestication Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “.”

Annex B

The Domestication Proposal (Proposal 2)

The Charter Proposal (Proposal 3)

Live Oak is asking its shareholders to consider and vote on a proposal to approve, by ordinary resolution, the Proposed Charter, as attached to this proxy statement/prospectus as . The Proposed Charter, which will be effective as of the Closing, will, among other things, increase the authorized shares of capital stock of the Combined Company to [ ] shares of capital stock, consisting of [ ] shares of Combined Company Common Stock and [ ] shares of undesignated Combined Company Preferred Stock. Concurrent with the adoption of the Proposed Charter, the Proposed Bylaws in the form attached to this proxy statement/prospectus as will also be adopted.

Annex C

Annex D

A summary of these provisions is set forth in the “” section of this proxy statement/prospectus and a copy of these provisions is attached hereto as . You are encouraged to read them in their entirety.

The Charter Proposal (Proposal 3)

Annex C

The Organizational Documents Proposals (Proposals 4-9)

Live Oak is asking its shareholders to consider and vote upon proposals to approve, by ordinary resolution and on a

non-binding

advisory basis, certain material differences between the Current Charter in effect prior to the Domestication and the terms and provisions to be set forth in the Proposed Charter of the Combined Company upon completion of the Business Combination. In accordance with SEC guidance, each of the Organizational Documents Proposals is being presented separately and will be voted upon on a non-binding

advisory basis. A brief summary of each of the Organizational Documents Proposals is set forth below. These summaries are qualified in their entirety by reference to the complete text of the Proposed Organizational Documents.

| • | Organizational Documents Proposal 4 — Under the Proposed Organizational Documents, the Combined Company would be authorized to issue (A) [ ] shares of Combined Company Common Stock and (B) [ ] shares of Combined Company Preferred Stock. |

| • | Organizational Documents Proposal 5 — The Proposed Organizational Documents would adopt (a) Delaware as the exclusive forum for certain stockholder litigation and (b) the federal district courts of the United States of America as the exclusive forum for the resolution of any complaint asserting a cause of action arising under the Securities Act. |

| • | Organizational Documents Proposal 6 — The Proposed Charter would require the affirmative vote of at least two-thirds of the total voting power of all then-outstanding shares of the Combined Company to amend, alter, repeal or rescind certain provisions of the Proposed Charter. |

| • | Organizational Documents Proposal 7 — The Proposed Charter would require the affirmative vote of at least two-thirds of the outstanding shares entitled to vote at an election of directors, voting together as a single class, to remove a director only for cause. |

| • | Organizational Documents Proposal 8 — The Proposed Charter would prohibit stockholder action by written consent in lieu of a meeting and require stockholders to take action at an annual or special meeting. |

| • | Organizational Documents Proposal 9 — The Proposed Charter would (1) change the corporate name from “Live Oak Acquisition Corp. V” to “Teamshares Inc.”, (2) make the Combined Company’s corporate existence perpetual and (3) remove certain provisions related to Live Oak’s status as a blank check company that will no longer be applicable upon consummation of the Business Combination. |

A summary of these provisions is set forth in the “” section of this proxy statement/prospectus. You are encouraged to read them in their entirety.

The Organizational Documents Proposals (Proposals 4 – 9)

The Incentive Plan Proposal (Proposal 10)

Live Oak is asking its shareholders to consider and vote on a proposal to approve, by ordinary resolution, the Incentive Plan and the material terms thereunder.

If approved by the Live Oak shareholders and adopted by the Combined Company, the Incentive Plan will be available to the Combined Company on a

go-forward

basis from the Closing. The initial aggregate number of shares of Combined Company Common Stock available for issuance under the Incentive Plan generally will be equal to 7% of the number of shares of outstanding Combined Company Common Stock (assuming all shares of Combined Company Common Stock reserved under the Incentive Plan have been issued) as of immediately following the Closing of the Business Combination. A summary of the Incentive Plan is set forth in the “” section of this proxy statement/prospectus and the form of the Incentive Plan is attached to this proxy statement/prospectus as .

The Incentive Plan Proposal (Proposal 10)

Annex E

The Employee Stock Purchase Plan Proposal

(

Proposal 11

)

Live Oak is asking its shareholders to consider and vote on a proposal to approve, by ordinary resolution, the ESPP and the material terms thereunder.

If approved by the Live Oak shareholders and adopted by the Combined Company, the ESPP will be available to the Combined Company on a go-forward basis from the Closing. The initial aggregate number of shares of Combined Company Common Stock available for issuance under the ESPP generally will be equal to 2% of the number of shares of outstanding Combined Company Common Stock (assuming all shares of Combined Company Common Stock reserved under the Incentive Plan have been issued) as of immediately following the Closing of the Business Combination.

A summary of the ESPP is set forth in the “” section of this proxy statement/prospectus and the form of the ESPP is attached to this proxy statement/prospectus as .

The Employee Stock Purchase Plan Proposal (Proposal 11)

Annex F

The Nasdaq Proposal (Proposal 12)

Live Oak is asking its shareholders to consider and vote upon a proposal to approve, by ordinary resolution, for purposes of complying with the applicable provisions of the Nasdaq Listing Rules, the issuance of the shares of Common Stock to be issued in the Business Combination and the additional shares of Combined Company Common Stock that will, upon Closing, be reserved for issuance pursuant to the Incentive Plan, to the extent such issuances would require shareholder approval under Nasdaq Listing Rule.

The Director Election Proposal (Proposal 13)

Live Oak is asking its shareholders to consider and vote upon a proposal to approve, by ordinary resolution, the election of five (5) directors, effective upon the Closing, to serve on the Combined Company Board until their respective successors are duly elected and qualified, or until such directors’ earlier death, resignation or removal.

The Insider Letter Amendments Proposal (Proposal 14)

Live Oak is asking its shareholders to consider and vote upon a proposal to approve, by ordinary resolution, amendments to the Insider Letter, reflected in the First Insider Letter Amendment and Second Insider Letter Amendment, each attached to this proxy statement/prospectus as , respectively, to (a) as described in the First Insider Letter Amendment, revise the Sponsor Lock-Up to end on the six (6) month anniversary of the Closing Date and (b) as described in the Second Insider Letter Amendment, release from the Sponsor Lock-Up such number of Incentive Founder Shares (up to 1,150,000 Incentive Founder Shares) as are actually utilized to secure commitments for Financing Transactions consummated prior to the Closing. The Insider Letter Amendments Proposal is described in more detail in this proxy statement/prospectus under the heading “.”

Annex H and Annex I

The Insider Letter Amendments Proposal (Proposal 14)

The Adjournment Proposal (Proposal 15)

Live Oak is asking its shareholders to consider and vote upon a proposal to approve, by ordinary resolution, the adjournment of the Live Oak Extraordinary General Meeting to a later date or time, if necessary or appropriate as determined by the chairman of the Live Oak Extraordinary General Meeting, at the determination of the chairman of the Live Oak Extraordinary General Meeting.

Conditionality of Proposals

The Required Proposals are conditioned on the approval of the Business Combination Proposal and each of the other Required Proposals. Unless the Business Combination Proposal is approved, the other Required Proposals will not be presented to the shareholders of Live Oak at the Live Oak Extraordinary General Meeting. The Adjournment Proposal is not conditioned on any other proposal. It is important for you to note that in the event the Required Proposals (consisting of the Business Combination Proposal, the Domestication Proposal, the Charter Proposal, the Nasdaq Proposal and the Director Election Proposal) do not receive the requisite vote for approval, then Live Oak will not consummate the Business Combination. If Live Oak does not consummate the Business Combination and fails to complete an initial business combination by February 27, 2027 (or such other date as may be approved by the Live Oak shareholders), it will be required to dissolve and liquidate its Trust Account by returning the then-remaining funds in such account to its public shareholders (net of taxes payable and up to $100,000 of interest to pay dissolution expenses).

The Live Oak Board considered a variety of factors in connection with its evaluation of the Business Combination. In light of the number and complexity of those factors, the Live Oak Board, as a whole, did not consider it practicable to, and did not attempt to, quantify or otherwise assign relative weights to the specific factors that it considered in reaching its determination and supporting its decision. Individual directors may have given different weight to different factors. The Live Oak Board viewed its decision as being a business judgment that was based on all of the information available to, and the factors presented to and considered by it. Certain information presented in this section is forward-looking in nature and, therefore, should be read in light of the factors discussed under “.”

Cautionary Note

Regarding

Forward-Looking Statements

The Live Oak Board did not obtain a fairness opinion (or any similar report or appraisal) in connection with its determination to approve the Business Combination (including the consideration to be delivered to the Teamshares Stockholders under the terms of the Merger Agreement). Live Oak management and the members of the Live Oak Board have extensive experience evaluating the financial merits of companies across a variety of industries, including asset management, financial services, real estate, energy, technology, industrial, and business and consumer services sectors, and the Board concluded that this experience and background enabled them to make the necessary analyses and determinations regarding the Business Combination and its terms. The

factors and information considered by the Live Oak Board, as further

described

below, included certain guideline public company data and other relevant information selected based on the business experience and professional judgment of Live Oak management. The independent directors of the Live Oak Board did not retain an unaffiliated representative to act solely on behalf of the unaffiliated Live Oak shareholders to negotiate the terms of the Business Combination and/or prepare a report concerning the approval of the Business Combination. The existence of

financial

and personal interests of Live Oak’s directors and officers may result in conflicts of interest, including a conflict between what may be in the best interests of Live Oak and what may be best for a director’s personal interests when determining to recommend that Live Oak shareholders vote for the proposals set forth in the accompanying proxy statement/prospectus (the “Proposals”). Teamshares Stockholders, officers and directors also have interests in the Business Combination that are different than those of Live Oak’s shareholders. As a result, there may be actual or potential material conflicts of interest between, on the one hand, Live Oak’s sponsor, its affiliates, Live Oak directors and officers, or Teamshares directors and officers, and on the other hand, unaffiliated security holders of Live Oak. See the sections entitled “The Business Combination Proposal — Interests of Live Oak’s Sponsor, Directors, Officers and Advisors in the Business Combination”, “Beneficial Ownership of Securities” and “Questions and Answers About the Live Oak Extraordinary General Meeting —

What interests do Teamshares directors and officers have in the Business Combination?”

in the accompanying proxy statement/prospectus for a further discussion.

Redemption Rights

Pursuant to the Current Charter, holders of Public Shares may demand that such shares be redeemed in exchange for a pro rata share of the aggregate amount on deposit in the Trust Account, net of taxes payable and up to $100,000 of interest to pay dissolution expenses, calculated as of two (2) business days prior to the

consummation of the Business Combination. If demand is properly made in accordance with the procedures reflected in this proxy statement/prospectus and the Current Charter and the Business Combination is consummated, these shares, immediately prior to the Business Combination, will cease to be outstanding and will represent only the right to receive a pro rata share of the aggregate amount on deposit in the Trust Account (calculated as of two (2) business days prior to the consummation of the Business Combination, including interest earned on the funds held in the Trust Account (net of taxes payable)). For illustrative purposes, based on funds in the Trust Account of approximately $[ ] million on [ ], 2026, the estimated per share Redemption Price at the Closing would have been approximately $[ ]. A Public Shareholder, together with any of such shareholder’s affiliates or any other person with whom it is acting in concert or as a “group” (as defined under Section 13 of Exchange Act) will be restricted from redeeming in the aggregate such shareholder’s shares or, if part of such a group, the group’s shares, with respect to 15% or more of the Live Oak Ordinary Shares included in the Units.

In order to exercise redemption rights, holders of Public Shares must:

| • | prior to 5:00 p.m. Eastern Time on [ ], 2026 (two (2) business days before the Live Oak Extraordinary General Meeting), tender your shares physically or electronically using The Depository Trust Company’s DWAC system and submit a request in writing that your Public Shares be redeemed for cash to CST, Live Oak’s transfer agent, at the following address: |

Continental Stock Transfer & Trust Company One State Street Plaza, 30

th

Floor New York, New York 10004 Attention: SPAC Redemption Team

E-mail:

spacredemptions@continentalstock.com | • | In your request to CST for redemption, you must also affirmatively certify if you “ ARE ARE NOT Section 13d-3 of the Exchange Act) with any other shareholder with respect to Live Oak Ordinary Shares; and |

| • | deliver your Public Shares either physically or electronically through DTC to Live Oak’s transfer agent at least two (2) business days before the Live Oak Extraordinary General Meeting. Public Shareholders seeking to exercise redemption rights and opting to deliver physical certificates should allot sufficient time to obtain physical certificates from the transfer agent and time to effect delivery. It is Live Oak’s understanding that shareholders should generally allot at least two weeks to obtain physical certificates from the transfer agent. However, Live Oak does not have any control over this process, and it may take longer than two weeks. Shareholders who hold their Public Shares in “street name” will have to coordinate with their bank, broker or other nominee to have the shares certificated or delivered electronically. If you do not submit a written request and deliver your Public Shares as described above, your shares will not be redeemed. |

Any demand for redemption, once made, may be withdrawn at any time until the deadline for exercising redemption requests (and submitting shares to the transfer agent) and thereafter, with Live Oak’s consent, until the consummation of to the Business Combination, or such other date and time as may be determined by the Live Oak Board in its sole discretion. If you delivered your shares for redemption to Live Oak’s transfer agent and decide within the required timeframe not to exercise your redemption rights, you may request that Live Oak’s transfer agent return the shares (physically or electronically). You may make such a request by contacting Live Oak’s transfer agent at the phone number or address listed above. See the accompanying proxy statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your Public Shares for cash.

If Live Oak receives valid redemption requests from holders of Public Shares prior to the redemption deadline, Live Oak may, at its sole discretion, following the redemption deadline and until the date of Closing (or such earlier date and time, if any, as Live Oak may determine in its sole discretion), seek and permit withdrawals

by one or more of such holders of their redemption requests. Live Oak may select which holders to seek such withdrawals of redemption requests from based on any factors Live Oak may deem relevant, and the purpose of seeking such withdrawals may be to increase the funds held in the Trust Account. If a holder of Public Shares delivered its Public Shares for redemption to the transfer agent and decides within the required timeframe not to exercise its redemption rights, it may request that the transfer agent return the shares (physically or electronically). The holder can make such request by contacting the transfer agent, at the address or email address listed in this proxy statement/prospectus.

Prior to exercising redemption rights, shareholders should verify the market price of Live Oak Ordinary Shares as they may receive higher proceeds from the sale of their Live Oak Ordinary Shares in the public market than from exercising their redemption rights if the market price per share is higher than the redemption price. We cannot assure you that you will be able to sell your Live Oak Ordinary Shares in the open market, even if the market price per share is higher than the redemption price stated above, as there may not be sufficient liquidity in Live Oak Ordinary Shares when you wish to sell your shares.

If you exercise your redemption rights, your Live Oak Ordinary Shares will cease to be outstanding immediately prior to the Business Combination and will only represent the right to receive a pro rata share of the aggregate amount on deposit in the Trust Account, calculated as of two business days prior to the consummation of the Business Combination. You will no longer own those shares and will have no right to participate in, or have any interest in, the future growth of the Combined Company, if any. You will be entitled to receive cash for these shares only if you properly and timely demand redemption.

If the Business Combination is not consummated and Live Oak otherwise does not consummate an initial business combination by February 27, 2027 (or such other date as may be approved by the Live Oak shareholders), Live Oak will be required to redeem all Public Shares and dissolve and liquidate its Trust Account by returning the then-remaining funds in such account to the public shareholders and the Warrants will expire worthless.

The following table presents the net tangible book value per share at specified redemption levels assuming various sources of material probable dilution (but excluding the effects of the Business Combination transaction itself):

(in thousands, except share and per share amounts) |

No Redemption Scenario (1) |

25% Redemption Scenario (2) |

50% Redemption Scenario (3) |

Maximum Redemption Scenario (4) |

||||||||||||

| IPO offering price per share |

$ |

10.00 |

$ |

10.00 |

$ |

10.00 |

$ |

10.00 |

||||||||

| Net tangible book value as of December 31, 2025, as adjusted (5) |

$ |

332,248 |

$ |

274,212 |

$ |

216,177 |

$ |

100,106 |

||||||||

| As adjusted shares (6) |

40,200,000 |

34,450,000 |

28,700,000 |

17,200,000 |

||||||||||||

| Net tangible book value per share |

$ |

8.26 |

7.96 |

$ |

7.53 |

$ |

5.82 |

|||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Dilution per share to Public Shareholders |

$ |

(1.74 |

) |

$ |

(2.04 |

) |

$ |

(2.47 |

) |

$ |

(4.18 |

) | ||||

| |

|

|

|

|

|

|

|

|||||||||

(1) |

Assumes that no Public Shareholders exercise redemption rights with respect to their Public Shares for a pro rata share of the funds in the Trust Account, which is a redemption scenario that could occur. |

(2) |

Assumes that holders of 25% of the Public Shares, 5,750,000 Public Shares, exercise redemption rights for an aggregate payment of approximately $59.8 million (based on the estimated per-share redemption price of approximately $10.39 per share) from the Trust Account based on funds in the Trust Account as of December 31, 2025, which is a redemption scenario that could occur. |

(3) |

Assumes that holders of 50% of the Public Shares, 11,500,000 Public Shares, exercise redemption rights for an aggregate payment of approximately $119.5 million (based on the estimated per-share redemption price of approximately $10.39 per share) from the Trust Account based on funds in the Trust Account as of December 31, 2025, which is a redemption scenario that could occur. |

(4) |

Assumes that holders of 100% of the Public Shares, 23,000,000 Public Shares, exercise redemption rights for an aggregate payment of approximately $239.0 million (based on the estimated per-share redemption price of approximately $10.39 per share) from the Trust Account based on funds in the Trust Account as of December 31, 2025, which is a redemption scenario that could occur. |

(5) |

See table below for reconciliation of net tangible book value, as adjusted. |

(6) |

See table below for reconciliation of as adjusted shares. |

If any of the Public Shareholders redeem their Public Shares prior to or in connection with the Closing, the percentage of the outstanding Combined Company Common Stock held by Public Shareholders will decrease and the percentages of the outstanding Combined Company Common Stock held by the Sponsor and by the Teamshares stockholders and the PIPE Investors will increase, in each case, relative to the percentage held if none of the shares of Live Oak Class A Ordinary Shares are redeemed.

If any of the Public Shareholders redeem their Public Shares at Closing in accordance with the Current Charter but continue to hold Public Warrants after the Closing, the aggregate value of the Public Warrants that may be retained by them, based on the closing trading price per Public Warrant as of [ ], 2026, would be $[ ], regardless of the amount of redemptions by the Public Shareholders. Upon the issuance of Combined Company Common Stock in connection with the Business Combination, the percentage ownership of the total outstanding shares of Combined Company Common Stock by Public Shareholders who do not redeem their Public Shares will be diluted. Public Shareholders that do not redeem their Public Shares in connection with the Business Combination will experience further dilution upon the exercise of Public Warrants that are retained after the Closing by redeeming Public Shareholders. The percentage of the total number of outstanding shares of Combined Company Common Stock that will be owned by Public Shareholders as a group will vary based on the number of Public Shares for which the holders thereof elect to have redeemed in connection with the Business Combination.

The following table illustrates Live Oak’s net tangible book value per share and the increase in Live Oak’s as adjusted net tangible book value per share following the Closing, excluding the effects of the Business Combination transaction, while giving effect to probable or consummated transactions that are material and other material effects on Live Oak’s net tangible book value per share. These are presented in relation to the initial public offering price per share paid by original investors in Live Oak as set forth as follows under the four redemption scenarios:

(in thousands, except share and per share amounts) |

No Redemption Scenario (1) |

25% Redemption Scenario (2) |

50% Redemption Scenario (3) |

Maximum Redemption Scenario (4) |

||||||||||||

| Numerator |

||||||||||||||||

| Live Oak’s Historical Net tangible book value as of December 31, 2025 |

$ |

225,562 |

$ |

225,562 |

$ |

225,562 |

$ |

225,562 |

||||||||

| Numerator adjustments |

||||||||||||||||

| Deferred Founder Shares Earnout Liability (5) |

(14,659 |

) |

(14,659 |

) |

(14,659 |

) |

(14,659 |

) | ||||||||

| Anticipated transaction expenses (6) |

(5,155 |

) |

(5,155 |

) |

(5,155 |

) |

(5,155 |

) | ||||||||

| Reduction of underwriting fees based on redemptions(7) |

0 |

1,725 |

3,450 |

6,900 |

||||||||||||

| Initial PIPE Investment proceeds (8) |

126,500 |

126,500 |

126,500 |

126,500 |

||||||||||||

| Redemptions from Trust Account (9) |

0 |

(59,761 |

) |

(119,521 |

) |

(239,042 |

) | |||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net tangible book value as of December 31, 2025, as adjusted |

$ |

332,248 |

$ |

274,212 |

$ |

216,17 7 |

$ |

100,106 |

||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Denominator |

||||||||||||||||

| Sponsor Shares |

3,450,000 |

3 ,4 50,000 |

3 ,4 50,000 |

3,450,000 |

||||||||||||

| Public Shareholders |

23,000,000 | 23,000,000 |

23,000,000 |

23,000,000 |

||||||||||||

| Live Oak Ordinary Shares issued and outstanding as of December 31, 2025 |

26,450,000 | 2 6 ,45 0,000 |

2 6 ,4 50,000 |

26,450,000 |

||||||||||||

| Denominator adjustments |

||||||||||||||||

| Live Oak Public Shareholders |

0 |

(5,750,000 |

) |

(11,500,000 |

) |

(23,000,000 |

) | |||||||||

| Initial PIPE Investors |

13,750,000 |

13,750,000 |

13,750,000 |

13,750,000 |

||||||||||||

| |

|

|

|

|

|

|

|

|||||||||

| As adjusted Live Oak shares outstanding |

40,200,000 |

3 4 ,4 50,000 |

28 ,70 0,000 |

17,200,000 |

||||||||||||

| |

|

|

|

|

|

|

|

|||||||||

(1) |

Assumes that no Public Shareholders exercise redemption rights with respect to their Public Shares for a pro rata share of the funds in the Trust Account, which is a redemption scenario that could occur. |

(2) |

Assumes that holders of 25% of the Public Shares, 5,750,000 Public Shares, exercise redemption rights for an aggregate payment of approximately $59.8 million (based on the estimated per-share redemption price of approximately $10.39 per share) from the Trust Account based on funds in the Trust Account as of December 31, 2025, which is a redemption scenario that could occur. |

(3) |

Assumes that holders of 50% of the Public Shares, 11,500,000 Public Shares, exercise redemption rights for an aggregate payment of approximately $119.5 million (based on the estimated per-share redemption price of approximately $10.39 per share) from the Trust Account based on funds in the Trust Account as of December 31, 2025, which is a redemption scenario that could occur. |

(4) |

Assumes that holders of 100% of the Public Shares, 23,000,000 Public Shares, exercise redemption rights for an aggregate payment of approximately $239.0 million (based on the estimated per-share redemption price of approximately $10.39 per share) from the Trust Account based on funds in the Trust Account as of December 31, 2025, which is a redemption scenario that could occur. |

(5) |

Represents a decrease in net tangible book value, resulting from the recognition of Live Oak’s contingent liability relating to the deferred sponsor shares. The deferred sponsor shares There is no adjustment to the denominator as the deferred founder shares are subject to vesting upon the occurrence |

of the Founder Share Tier I Share Price Target and Founder Share Tier II Share Price Target or upon the occurrence of a Qualifying Change of Control during the Founder Share Measurement Period. |

| (6) | Expected and actual transaction and other costs is inclusive of a decrease to net tangible book value for expected and actual Live Oak transaction and other costs to be incurred subsequent to December 31, 2025 and paid on or before the Closing Date of $5.2 million. |

(7) |

Represents the impact of the reduction in underwriting fees on a proportional basis with redemptions. |

(8) |

Assumes completion of a $126.5 million PIPE investment. |

(9) |

Represents reductions in the Trust Account reflecting the four redemption scenarios. |