2025 Annual Information Form

EXHIBIT 99.1

|

| 2025 Annual Information Form |

ORION DIGITAL CORP.

2025 ANNUAL INFORMATION FORM

DATED: March 31, 2026

| 1 | Page |

|

| 2025 Annual Information Form |

TABLE OF CONTENTS

| CERTAIN INTERPRETATION MATTERS |

| 4 |

|

|

|

|

|

|

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS |

| 4 |

|

|

|

|

|

|

| CORPORATE STRUCTURE |

| 8 |

|

|

|

|

|

|

| NAME, ADDRESS, AND INCORPORATION |

| 8 |

|

| INTERCORPORATE RELATIONSHIPS |

| 9 |

|

|

|

|

|

|

| BUSINESS DESCRIPTION |

| 10 |

|

|

|

|

|

|

| GENERAL |

| 10 |

|

| PRODUCTS AND SERVICES |

| 10 |

|

| PRODUCT DEVELOPMENT |

| 13 |

|

| OUR PLATFORMS |

| 13 |

|

| SPECIALIZED SKILL AND KNOWLEDGE |

| 15 |

|

| SALES AND MARKETING |

| 15 |

|

| COMPETITIVE CONDITIONS |

| 16 |

|

| INTANGIBLE PROPERTIES |

| 17 |

|

| CREDIT FACILITY |

| 17 |

|

| EMPLOYEES |

| 18 |

|

| FOREIGN OPERATIONS |

| 18 |

|

|

|

|

|

|

| GENERAL DEVELOPMENT OF THE BUSINESS |

| 18 |

|

|

|

|

|

|

| CURRENT FINANCIAL YEAR – RECENT DEVELOPMENTS |

| 19 |

|

| THREE YEAR HISTORY |

| 19 |

|

|

|

|

|

|

| RISK FACTORS |

| 23 |

|

|

|

|

|

|

| DIVIDENDS AND DISTRIBUTIONS |

| 46 |

|

|

|

|

|

|

| DESCRIPTION OF CAPITAL STRUCTURE |

| 46 |

|

|

|

|

|

|

| MARKET FOR SECURITIES |

| 47 |

|

|

|

|

|

|

| TRADING PRICE AND VOLUME |

| 47 |

|

| ESCROWED SECURITIES AND SECURITIES SUBJECT TO A CONTRACTUAL RESTRICTION ON TRANSFER |

| 47 |

|

| PRIOR SALES |

| 47 |

|

|

|

|

|

|

| DIRECTORS AND OFFICERS |

| 47 |

|

|

|

|

|

|

| NAME, OCCUPATION AND SECURITY HOLDING |

| 47 |

|

| BIOGRAPHIES |

| 48 |

|

| CEASE TRADE ORDERS, BANKRUPTCIES, PENALTIES OR SANCTIONS |

| 50 |

|

|

|

|

|

|

| INTERESTS OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS |

| 50 |

|

|

|

|

|

|

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS |

| 51 |

|

|

|

|

|

|

| LEGAL PROCEEDINGS |

| 51 |

|

| REGULATORY ACTIONS |

| 51 |

|

|

|

|

|

|

| TRANSFER AGENT AND REGISTRAR |

| 51 |

|

|

|

|

|

|

| MATERIAL CONTRACTS |

| 51 |

|

|

|

|

|

|

| 2 | Page |

|

| 2025 Annual Information Form |

| EXPERTS |

| 52 |

|

|

|

|

|

|

| NAMES OF EXPERTS |

| 52 |

|

| INTERESTS OF EXPERTS |

| 52 |

|

|

|

|

|

|

| INFORMATION ON THE AUDIT COMMITTEE |

| 52 |

|

|

|

|

|

|

| THE AUDIT COMMITTEE'S CHARTER |

| 52 |

|

| COMPOSITION OF THE AUDIT COMMITTEE |

| 52 |

|

| RELEVANT EDUCATION AND EXPERIENCE |

| 52 |

|

| AUDIT COMMITTEE OVERSIGHT |

| 52 |

|

| PRE-APPROVAL POLICIES AND PROCEDURES |

| 52 |

|

| EXTERNAL AUDITOR SERVICE FEES (BY CATEGORY) |

| 53 |

|

|

|

|

|

|

| ADDITIONAL INFORMATION |

| 53 |

|

|

|

|

|

|

| APPENDIX A – AUDIT COMMITTEE CHARTER |

| A-1 |

|

| 3 | Page |

|

| 2025 Annual Information Form |

Certain Interpretation Matters

Unless otherwise noted or the context indicates otherwise "we", "us", "our", the "Company" or "Orion Digital" refer to Orion Digital Corp. and its direct and indirect subsidiaries. Amounts in this annual information form ("AIF") are stated in Canadian dollars unless otherwise indicated.

This AIF may refer to trademarks, trade names and material which is subject to copyright and which are protected under applicable intellectual property laws and are the property of Orion Digital. Solely for convenience, our trademarks, trade names and copyrighted material referred to in this AIF may appear without the ® or © symbol, but such references are not intended to indicate in any way, that we will not assert, to the fullest extent under applicable law, our rights to these trademarks, trade names and copyrights. All other trademarks used in this AIF are the property of their respective owners.

This AIF is for the financial year ended December 31, 2025 and is dated March 31, 2026. Except where otherwise indicated, the information contained in this AIF is stated as of December 31, 2025.

Cautionary Note Regarding Forward-Looking Statements

This AIF may contain "forward-looking information" within the meaning of applicable securities laws in Canada and "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995, as amended. Forward-looking information may relate to our future financial outlook and anticipated events or results and may include information regarding our financial position, business strategy, growth strategies, budgets, operations, financial results, taxes, dividend policy, plans and objectives. Particularly, information regarding our expectations of future results, performance, achievements, prospects or opportunities or the markets in which we operate is forward-looking information. In some cases, forward-looking information can be identified by the use of forward-looking terminology such as "plans", "targets", "expects", "does not expect", "is expected", "scheduled", "estimates", "outlook", "intends", "anticipates", "does not anticipate", "believes", or variations (including negative and grammatical variations) of such words and phrases or state that certain actions, events or results "may", "could", "would", "might", "will", "will be taken", "occur" or "be achieved". In addition, any statements that refer to expectations, intentions, projections or other characterizations of future events or circumstances contain forward-looking information. Statements containing forward-looking information are not historical facts but instead represent management's expectations, estimates and projections regarding future events or circumstances. This forward-looking information includes, among other things, statements relating to:

|

| · | the Company's expectations regarding its revenue (including loan interest), expenses and operations, key performance indicators, provision for loan losses (net of recoveries) and delinquencies ratios; |

|

|

|

|

|

| · | the Company's anticipated cash needs and its needs for additional financing, funding costs, and ability to extend or refinance any outstanding amounts under the Credit Facility (as defined below) and debentures; |

|

|

|

|

|

| · | the Company's ability to protect, maintain and enforce its intellectual property; |

|

|

|

|

|

| · | third-party claims of infringement or violation of, or other conflicts with, intellectual property rights; |

|

|

|

|

|

| · | the resolution of any legal matters or disputes; |

|

|

|

|

|

| · | the Company's plans for and timing of expansion of its products and services; |

|

|

|

|

|

| · | the Company's future growth plans; |

|

|

|

|

|

| · | the acceptance by consumers and the marketplace of new technologies and solutions; |

| 4 | Page |

|

| 2025 Annual Information Form |

|

| · | the Company's ability to attract new members and develop and maintain existing members; |

|

|

|

|

|

| · | the Company's ability to attract and retain personnel; |

|

|

|

|

|

| · | the Company's expectations with respect to advancement of its product offering; |

|

|

|

|

|

| · | the Company's competitive position and the regulatory environment in which the Company operates; |

|

|

|

|

|

| · | anticipated trends and challenges in the Company's business and the markets in which it operates; |

|

|

|

|

|

| · | the Company's historical investment approach, objectives and strategy, including its focus on specific sectors; |

|

|

|

|

|

| · | the structuring of its investments and its plans to manage its investments; and |

|

|

|

|

|

| · | the Company's expectations regarding the performance of certain sectors in which it has invested. |

Forward looking statements are based on our opinions, estimates and assumptions in light of our experience and perception of historical trends, current conditions and expected future developments, as well as other factors that we currently believe are appropriate and reasonable in the circumstances. Despite a careful process to prepare and review the forward-looking information, there can be no assurance that the underlying opinions, estimates and assumptions will prove to be correct. Given these assumptions, investors or users of this document should not place undue reliance on this forward-looking information. Whether actual results, performance or achievements will conform to the Company's expectations and predictions is subject to a number of known and unknown risks, uncertainties, assumptions and other factors that are discussed elsewhere in this AIF, including risks related to:

|

| · | disruptions in the credit markets; |

|

|

|

|

|

| · | an increase in member default rates; |

|

|

|

|

|

| · | our risk management efforts; |

|

|

|

|

|

| · | our limited operating history in an evolving industry; |

|

|

|

|

|

| · | our history of losses; |

|

|

|

|

|

| · | our efforts to expand our market reach and product portfolio; |

|

|

|

|

|

| · | changes in the regulatory environment or in the way regulations are interpreted; |

|

|

|

|

|

| · | the impact of trade relations and ongoing trade tensions, including the threat of tariffs and other governmental actions, as well as retaliatory actions; |

|

|

|

|

|

| · | privacy considerations; |

|

|

|

|

|

| · | material changes to the interest rate charged to our members and paid to our lenders; |

|

|

|

|

|

| · | our negative operating cash flow; |

|

|

|

|

|

| · | our ability to access additional capital through issuances of equity and debt securities; |

| 5 | Page |

|

| 2025 Annual Information Form |

|

| · | the concentration of our debt funding sources and our ability to access additional capital from those sources; |

|

|

|

|

|

| · | the financial covenants under the Credit Facility; |

|

|

|

|

|

| · | security breaches of members' confidential information; |

|

|

|

|

|

| · | a decline in demand for our products; |

|

|

|

|

|

| · | our products achieving sufficient market acceptance; |

|

|

|

|

|

| · | protecting our intellectual property rights; |

|

|

|

|

|

| · | claims by third parties for alleged infringement of their intellectual property rights; |

|

|

|

|

|

| · | the use of open source software and any failure to comply with the terms of open source licenses; |

|

|

|

|

|

| · | serious errors or defects in our software and attacks or security breaches; |

|

|

|

|

|

| · | the reliability of our credit scoring model; |

|

|

|

|

|

| · | access to reliable third-party data; |

|

|

|

|

|

| · | our levels of indebtedness; |

|

|

|

|

|

| · | the adequacy of our allowance for loan losses; |

|

|

|

|

|

| · | exchange rate fluctuations; |

|

|

|

|

|

| · | our marketing efforts and ability to increase brand awareness; |

|

|

|

|

|

| · | member complaints and negative publicity; |

|

|

|

|

|

| · | misconduct or errors by our employees and third-party service providers; |

|

|

|

|

|

| · | our ability to collect payment on and service the loans we make to our members; |

|

|

|

|

|

| · | our reliance on data centers to deliver our services and any disruption thereof; |

|

|

|

|

|

| · | competition in our industry; |

|

|

|

|

|

| · | the reliability of information provided by our members; |

|

|

|

|

|

| · | our reliance on key personnel, and in particular, our management; |

|

|

|

|

|

| · | competition for employees; |

|

|

|

|

|

| · | preserving our corporate culture; |

|

|

|

|

|

| · | risks related to litigation; |

|

|

|

|

|

| · | risks related to actively managing our investment portfolio; |

| 6 | Page |

|

| 2025 Annual Information Form |

|

| · | earthquakes, fire, power outages, flood, and other catastrophic events, and interruption by man-made problems such as terrorism; |

|

|

|

|

|

| · | volatility in the market price for our publicly traded securities; |

|

|

|

|

|

| · | future sales of our securities by existing shareholders causing the market price for our publicly traded securities to fall; |

|

|

|

|

|

| · | no cash dividends for the foreseeable future; |

|

|

|

|

|

| · | our trading price and volume declining if analysts publish inaccurate or unfavourable research about us or our business; |

|

|

|

|

|

| · | a failure to maintain effective internal controls; |

|

|

|

|

|

| · | our reliance on third parties to perform key functions; |

|

|

|

|

|

| · | risks related to cost-cutting; |

|

|

|

|

|

| · | insurance coverage and related expense; |

|

|

|

|

|

| · | risks related to flexible remote working model; |

|

|

|

|

|

| · | risks related to our platform for independent portfolio managers; |

|

|

|

|

|

| · | risks related to our use of artificial intelligence and machine learning technologies; |

|

|

|

|

|

| · | maintaining the net capital levels required by regulators; |

|

|

|

|

|

| · | risks related to the Company's investment portfolio including: |

|

| o | investment risk; |

|

|

|

|

|

| o | our ability to monetize the portfolio given investments in private issuers and illiquid securities; |

|

|

|

|

|

| o | foreign currency exposure if investments in the Company's portfolio consist of securities denominated in foreign currencies; |

|

|

|

|

|

| o | concentration of investments; |

|

|

|

|

|

| o | there is no guaranteed return on the Company's investments; |

|

|

|

|

|

| o | intellectual property claims against issuers that the Company invests in; |

|

|

|

|

|

| o | the Company's portfolio may include securities of issuers established in jurisdictions outside of Canada and the U.S.; |

|

|

|

|

|

| o | some investments of the Company may be in markets that are new and emerging; |

|

|

|

|

|

| o | fluctuation in net asset value and valuation of the Company's portfolio; |

|

|

|

|

|

| o | non-controlling interests; |

|

|

|

|

|

| o | trading costs; and |

|

|

|

|

|

| o | the Company may be limited in its ability to make follow-on investments and the dilution in the Company's holdings resulting from a failure to make such follow-on investments. |

| 7 | Page |

|

| 2025 Annual Information Form |

If any of these risks or uncertainties materialize, or if the opinions, estimates or assumptions underlying the forward-looking information prove incorrect, actual results or future events might vary materially from those anticipated in the forward-looking information. Although we have attempted to identify important risk factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other risk factors not presently known to us or that we presently believe are not material that could also cause actual results or future events to differ materially from those expressed in such forward-looking information. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information, which speaks only as of the date made. The forward-looking information contained in this AIF represents our expectations as of the date of this AIF (or as the date they are otherwise stated to be made), and are subject to change after such date. However, we disclaim any intention or obligation or undertaking to update or revise any forward-looking information whether as a result of new information, future events or otherwise, except as required under applicable securities laws. All of the forward-looking information contained in this AIF is expressly qualified by the foregoing cautionary statements.

Corporate Structure

Name, Address, and Incorporation

Mogo Finance Technology Inc. ("Mogo Finance") was incorporated under the Company Act on August 26, 2003 under the name "675909 B.C. Ltd." and transitioned under the Business Corporations Act (British Columbia) ("BCBCA") on May 4, 2005. Mogo Finance's name was changed several times, the last of which occurred on June 1, 2012 when its name was changed from "Hornby Management Inc." to the current name, "Mogo Finance Technology Inc.". Mogo Finance completed an initial public offering of its common shares on the Toronto Stock Exchange ("TSX") under the trading symbol "GO" in June 2015.

The Company was incorporated by letters patent under the laws of Canada on January 14, 1972 under the name "Eskimo International Resources Limited." On August 17, 1972, the Company changed its name to "Natalma Mines Limited" by supplementary letters patent. The Company was continued under the Canada Business Corporations Act ("CBCA") by articles of continuance dated November 19, 1979. On May 4, 1983, the Company's name was changed to "Tonka Resources Inc.". The Company underwent several name changes between 1988 and 2013. On June 13, 2013, the Company changed its name to "Difference Capital Financial Inc" ("Difference").

On June 21, 2019, the Company completed a statutory plan of arrangement (the "Arrangement"), being a business combination with Mogo Finance. In connection with the Arrangement, the Company was continued into British Columbia under the BCBCA and changed its name to "Mogo Inc." (referred to in this section as the "Combined Entity").

Under the Arrangement, Mogo Finance was amalgamated with a wholly owned subsidiary of Difference and each Mogo Finance common share (each a "Mogo Finance Share") outstanding immediately prior to the Arrangement, other than Mogo Finance Shares held by Difference, was exchanged for one common share of the Combined Entity (each, a "Common Share"). On completion of the Arrangement, former Mogo Finance shareholders owned approximately 80% of the Combined Entity, on a fully diluted basis and the former directors of Mogo Finance made up a majority of the directors of the Combined Entity and the former officers of Mogo Finance became officers of the Combined Entity. In connection with the Arrangement, all of Mogo Finance's outstanding convertible securities became exercisable or convertible, as applicable, for Common Shares in accordance with the provisions thereof.

The Common Shares began trading on the TSX under the trading symbol "MOGO" in place of the Difference common shares at the open of trading on June 25, 2019. In addition, the Combined Entity was treated as a successor in interest to Mogo Finance and, as such, the Combined Entity was listed on the Nasdaq Capital Market (the "Nasdaq") under the symbol "MOGO". Mogo Finance Shares were delisted from the TSX on the close of trading on June 24, 2019. On August 10, 2023, the issued and outstanding Common Shares of the Combined Entity were consolidated on a three for one basis.

| 8 | Page |

|

| 2025 Annual Information Form |

Following the completion of the Arrangement, Mogo Finance became a wholly owned subsidiary of the Company. The Arrangement was accounted for as a reverse acquisition of the Company by Mogo Finance under IFRS 3 - Business Combinations, and accordingly, beginning with the second quarter of 2019, the Company's financial statements, management's discussion and analysis and all other documents filed with securities commissions or similar authorities in each of the provinces and territories of Canada reflect the continuing operations of Mogo Finance.

On December 29, 2025, the Company’s name was changed to Orion Digital Corp. and on January 2, 2026 the Company’s common shares began trading under the new ticker symbol ORIO on the Nasdaq and TSX.

Orion Digital's head office is located at 516-409 Granville St, Vancouver, BC, V6C 1T2 and its registered office is located at Suite 2700, 666 Burrard Street, Vancouver, British Columbia, V6C 2X8.

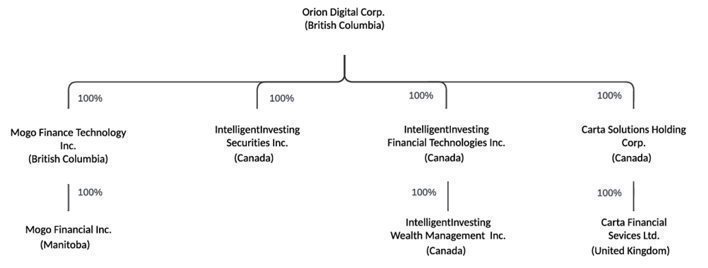

Intercorporate Relationships

Orion Digital has a number of direct and indirect subsidiaries including Mogo Finance wholly owned by Orion Digital, and Mogo Financial Inc., wholly owned by Mogo Finance, which together operate Orion Digital's online lending platform, IntelligentInvesting Financial Technologies Inc. (formerly, Moka Financial Technologies Inc.) (“IIFTI”) wholly owned by Orion Digital, and it’s wholly owned subsidiary IntelligentInvesting Wealth Management Inc. (formerly, Mogo Asset Management Inc.)(“IIWMI”), which together operate our passive investing app and portfolio management business, IntelligentInvesting Securities Inc. (formerly, MogoTrade Inc.) (“IISI”), wholly owned by Orion Digital, which operates our commission free stock trading platform, and Carta Solutions Holding Corp. (“Carta Solutions”), wholly owned by Orion Digital, which holds the Carta group of companies (together with its subsidiaries, “Carta”). Carta Financial Services Ltd. is a material indirect subsidiary wholly owned by Carta Solutions, incorporated under the laws of the United Kingdom on November 28, 2007, and operates Carta's European payments business.

| 9 | Page |

|

| 2025 Annual Information Form |

Business Description

General

Orion Digital Corp. is a financial technology company focused on its digital wealth platform. The Company’s Intelligent Investing platform provides structured investment solutions designed to support long-term portfolio construction through automated and technology-enabled processes.

Orion Digital also operates a European payments infrastructure business that provides transaction authorization and processing services, and a Canadian consumer lending portfolio that generates cash flow and is managed with a focus on risk and capital efficiency.

Orion Digital’s capital allocation framework prioritizes reinvestment in its wealth platform, followed by investment in payments infrastructure and share repurchases where appropriate, with excess liquidity retained on the balance sheet to support operating stability and capital flexibility.

Products and Services

The Company’s primary products focus on wealth, payments and lending.

Revenue Model and Economics

The Company generates revenue across three primary business lines:

|

| · | Wealth (subscription and services): Recurring revenue derived from platform membership fees and investment-related services, with revenue scaling alongside assets under management and member growth. |

|

|

|

|

|

| · | Payments (transaction and platform fees): Revenue generated from issuer processing, transaction-based fees, and program management services provided to enterprise and fintech clients. Revenue is correlated with transaction volume and client program activity. |

|

|

|

|

|

| · | Lending (interest income): Revenue generated from consumer lending products, with profitability driven by pricing and credit performance. |

The Company’s strategy is to increase the contribution of recurring and scalable revenue streams from wealth and payments over time, while managing lending as a capital-efficient source of cash flow.

Wealth: Primary growth and strategic focus of the Company

IntelligentInvesting.ai

Intelligent Investing is a digital wealth platform designed to help Canadians build long-term wealth through disciplined, technology-enabled investing solutions. As of December 31, 2025, Intelligent Investing was delivered through two mobile applications, the Intelligent Investing app (managed investing) and the MogoTrade app (self-directed investing), which together formed an integrated investing ecosystem. Intelligent Investing consists of two core offerings:

Managed Investing

The Company’s managed investing solution is delivered through the Intelligent Investing mobile application.

The Intelligent Investing app provides a fully managed digital investing experience designed to simplify long-term wealth building through automation and structured portfolio management. Members make recurring or one-time contributions into professionally managed portfolios constructed with a strategic focus on broad-market ETFs, such as those tracking the S&P 500. Dividends are automatically reinvested.

| 10 | Page |

|

| 2025 Annual Information Form |

There are no account minimums, and members may deposit or withdraw funds without transaction fees. Portfolios are constructed and managed based on each member’s investment objectives and risk profile.

Investments held through the Intelligent Investing app are managed by IIWMI, a registered portfolio manager, investment fund manager, and exempt market dealer in Canada.

The Intelligent Investing application is available on the Apple App Store and Google Play Store.

Self-Directed Investing

The Company’s self-directed investing solution is a commission-free self-directed stock trading platform delivered through a mobile app that allows members to trade equities listed on major exchanges, including the TSX, TSX Venture Exchange, Nasdaq, and NYSE. The platform is designed to support informed investment decision-making through integrated research tools and educational resources.

The Company’s self-directed investing platform is offered by IISI, a dealer member regulated by the Canadian Investment Regulatory Organization (CIRO).

The Intelligent Investing self-directed trading application is available on the Apple App Store and Google Play Store.

Platform Integration and Technology

While managed and self-directed investing were offered through separate applications as of December 31, 2025, they operate within a common Intelligent Investing framework and subscription model. Together, they provide members with access to both professionally managed portfolios and self-directed trading capabilities within a single investing ecosystem.

The Intelligent Investing platform is built on cloud-based infrastructure leveraging internally developed microservices and standardized APIs. The architecture is designed to support scalability, regulatory compliance, and integration with third-party data providers, custodians, and market infrastructure.

The Company continues to invest in technology enhancements across the Intelligent Investing platform. This includes ongoing development and evaluation of advanced analytics and artificial intelligence–enabled capabilities intended to enhance personalization, portfolio insights, research functionality, and operational efficiency. While such capabilities were at various stages of development as of December 31, 2025, the Company expects data-driven and AI-enabled tools to play an increasing role in supporting member experience and platform differentiation over time.

Wealth revenue is primarily recurring in nature and benefits from operating leverage as assets under management and member engagement increase.

Tactex Asset Management

Tactex, a division of IIWMI, offers an independent platform designed to empower portfolio managers to grow their business on their own terms. Tactex provides the regulatory, technological, and operational infrastructure needed for advisors to thrive - professionally and financially. IIWMI is registered as a portfolio manager in all Canadian provinces and territories, as an Investment fund manager in the provinces of Ontario and Quebec, and as an exempt market dealer in the provinces of Alberta, British Columbia, Saskatchewan, Manitoba, Ontario, Quebec, New Brunswick, Nova Scotia, Newfoundland and Labrador and Prince Edward Island.

| 11 | Page |

|

| 2025 Annual Information Form |

Payments: Infrastructure layer supporting transaction authorization and client programs

Carta is a digital payments software company, founded in 2008, which provides technology and services that enable financial technology companies, banks, and corporations to issue payment products to consumers via multiple channels, including physical, virtual and tokenized cards, as well as payment switching and routing services. The Carta platform provides the infrastructure needed to help fintech and payments businesses build and manage their payment systems, and supports prepaid, debit, and credit card issuer processing. Carta is certified as a Visa and MasterCard processor with active card programs in over 11 countries, and annual transaction volume of approximately $12 billion.

Payments revenue is driven by transaction volume and client program activity, with revenue scaling as customer programs grow and expand.

Lending: Cash-generative business managed for risk and capital efficiency

The Company’s lending business provides unsecured consumer credit and is operated with a focus on disciplined underwriting, portfolio monitoring, and cash flow generation. The business is not a primary growth driver and is managed within defined risk and capital constraints.

Operating under the Mogo brand, the Company primarily offers an unsecured open line of credit product (the “Mogo Line of Credit”), which is designed to provide members with access to short-term liquidity. The Mogo Line of Credit provides approved members with access to credit up to $5,000 at a rate of 34.37%, subject to applicable provincial regulations and individual credit assessment. The Company's loan portfolio also includes loans originated prior to 2025 at rates higher than 34.37%, which remain in effect at their original terms for existing borrowers. Members may obtain a no-obligation pre-approval through a fully digital application process and funding is completed electronically.

The lending experience is designed to be digital-first and highly automated, with the objective of reducing paperwork and minimizing manual intervention. The Company utilizes proprietary credit decisioning models that incorporate multiple data sources and analytical methodologies to assess risk and determine eligibility and credit limits.

Credit Decisioning and Technology

A core component of the Company’s lending platform is its data-driven underwriting and risk management framework. The Company leverages internally developed risk models, behavioral data, third-party bureau data, and other permitted data sources to inform credit decisions and ongoing account management. The Company continues to enhance its credit decisioning and operational capabilities through advanced analytics and artificial intelligence–enabled tools. These technologies are used to support: risk assessment and credit limit determination; fraud detection and identity verification; automated income and account verification processes; portfolio monitoring and collections prioritization.

Automation is embedded throughout the lending lifecycle, from application and underwriting through servicing and collections. While automated systems are central to the workflow, human oversight remains in place where required by policy, regulation, or internal risk controls.

The Company expects continued investment in AI-driven and automation technologies to improve operational efficiency, reduce manual processing requirements, strengthen risk management, and streamline the member experience over time. These initiatives remain subject to regulatory requirements, internal governance standards, and technological development timelines.

| 12 | Page |

|

| 2025 Annual Information Form |

Integrated Financial Ecosystem

The Company’s lending business operates within a broader financial ecosystem that includes Intelligent Investing.

While the lending product is designed to address short-term liquidity needs, the broader platform provides members with access to tools and services intended to support longer-term financial management and wealth-building objectives.

Investment Portfolio (“Orion Digital Ventures”)

Orion Digital owns a portfolio consisting of approximately 15 investments in private and public companies and bitcoin ETFs. The Company’s investment portfolio is managed opportunistically and is not a core component of its operating strategy.

As of December 31, 2025, Orion Digital's investment portfolio was valued at approximately $21 million and included:

|

| · | A stake in TSX-listed WonderFi Technologies Inc. ("WonderFi"), a fully regulated crypto exchange in Canada; |

|

|

|

|

|

| · | Investments in leading and emerging Crypto, Web 3.0 platforms and gaming companies, including Gemini, NFT Trader, and Enthusiast Gaming (NASDAQ:EGLX); and |

|

|

|

|

|

| · | Legacy investments including Hootsuite, Blue Ant Media and Alida, with a focus on monetizing these investments. |

In the financial year ended December 31, 2025 and subsequently in 2026, Orion Digital monetized approximately $19.5 million and $8.4 million respectively, of its investment portfolio through a sale of its remaining stake in WonderFi.

Product Development

Orion Digital is a product-driven company focused on building digital wealth solutions that support disciplined capital allocation in financial systems that are increasingly automated and AI-assisted. Our CEO leads our product team, ensuring that development priorities are aligned with the Company's capital allocation framework, which prioritizes reinvestment in our wealth platform, followed by investment in payments infrastructure. Our product development is informed by member behavior data, platform performance metrics, and market trends, and we continuously refine our platforms to improve usability, reliability, and the overall member experience. Our primary product development focus is the Intelligent Investing platform, a unified wealth platform that integrates managed and self-directed investing capabilities within a single interface. We expect to continue to invest in products and platform enhancements that we believe meet our return-on-investment criteria and that advance the Company's position as a digital wealth infrastructure business.

Our Platforms

Intelligent Investing Platform

Intelligent Investing is a cloud-based system built on internally developed microservices that communicate through RESTful Application Program Interfaces ("APIs"). Application data resides in both Canada as well as the United States. The Company utilizes third-party service providers to support the delivery of market data and analytics used in customer investment decision-making.

The platform is designed to support a largely self-directed user experience, reducing reliance on operational support. Its core technology foundation was acquired in 2021 and has since been further developed and enhanced by the Company. The platform also leverages shared infrastructure developed across Orion Digital’s other business lines, including services related to ledgering, funds transfer, account creation and account management.

| 13 | Page |

|

| 2025 Annual Information Form |

Mogo Platform

The Company operates an integrated, cloud-based platform designed to deliver financial products to consumers, with a focus on providing access to credit for individuals with non-prime or evolving credit profiles. The platform is built using a modular architecture of internally developed services, supporting reliability and flexibility.

The platform is designed to provide a largely self-service user experience through digital interfaces. For loan customers, this includes the MogoAccount portal, which enables members to manage their accounts, access product information and receive communications.

Automation and data analytics are embedded within the platform’s processes, supporting application processing, transaction execution, credit decisioning and marketing activities. The platform also utilizes standardized interfaces to integrate with third-party service providers, allowing for flexibility and ongoing enhancement of functionality. Data generated through platform operations is used to monitor performance and support continuous improvement in credit and operational processes.

Carta Platform

Carta's business-to-business ("B2B") platform is a cloud-based system with direct connectivity to global card payment networks – Visa and MasterCard ("Payment Networks"). The platform is designed to comply with applicable data security and privacy standards, including Payment Card Industry Data Security Standards (PCI DSS Level 1), General Data Protection Regulation (GDPR), and regional and bank partner regulatory requirements.

Carta serves customers seeking to issue payment cards by providing connectivity to the Payment Networks and client facing interfaces that enable management of the card programs. Customers access the platform through APIs and administration portals built on these APIs, enabling real-time creation and modification of user accounts and issuing of 16 Digit Personal Account Numbers ("PANs").

A core component of the platform is the authorization functionality which enables real-time authorizations of transactions based on configurable rules within the Carta system. Customers may also interact with the authorization process through Carta's delegated authorization service, Issuer Link, which allows for the application of additional customer-defined controls beyond standard processing rules. This functionality enables enhanced transaction-level controls and supports the development of differentiated card products and features.

The integrity, security and reliability of the Company’s technology and payments infrastructure are critical to its operations. The Company intends to continue investing in its platform to meet client needs and maintain confidence in its services, including through ongoing optimization of its cloud-based infrastructure to support global payment processing with localized performance and connectivity to the Payment Networks. The platform is designed to maintain low authorization latency and high availability, while delivering scalable, consistent performance and resilience as transaction volumes grow.

In 2025, Carta exited its Canadian payments business to focus on its core European market.

Platform Maintenance

We maintain our platforms with 37 full‑time technology and credit risk analysis employees (credit risk, product, design, development, business intelligence and information technology) as of December 31, 2025 (excluding Carta). For Carta, we have 52 full time technology employees (Payment Systems, Information Technology and Compliance, Software Engineering, Site Reliability Engineering)

| 14 | Page |

|

| 2025 Annual Information Form |

Specialized Skill and Knowledge

As of December 31, 2025, Orion Digital had 198 team members including employees and contractors. With over twenty years of operating experience, we have developed strong competencies across multiple disciplines. In addition to 50 software developers, designers, data scientists, product managers, and marketers, we have all of the traditional roles of a financial services provider including credit risk, finance, customer experience, operations, governance, legal and compliance. Our team supports the delivery and development of Orion Digital's wealth, payments infrastructure, and consumer lending operations through a combination of technology, financial services, and operational expertise. Our future success partly depends on our continuing ability to attract, develop, motivate, and retain highly qualified and skilled employees who share Orion Digital's passion for innovation through our products, platform and brand.

Sales and Marketing

Mogo and Intelligent Investing

The Company’s marketing strategy is focused on acquiring and retaining long-term investing customers through clear value propositions, transparent pricing, and consistent product experience. Marketing efforts emphasize disciplined investing, simplicity, and alignment with long-term market performance.

We deploy a fully integrated, multi-channel strategy that blends performance marketing with long-term brand building. This includes:

|

| · | Web & Funnel Optimization - Our websites - including intelligentinvesting.ai and mogo.ca - serve as core entry points for onboarding new members. Each site is optimized to reflect the sophistication and simplicity of the Intelligent Investing experience, with an emphasis on education, clarity, and frictionless activation. |

|

|

|

|

|

| · | Content-Driven Education & Inspiration - Intelligent Investing is not built for everyone. It’s designed for those who want to break free from the noise, think independently, and build wealth with conviction. Our content - delivered through email series, in-app lessons, social media, and educational articles - reinforces core investing principles and helps members rewire their behavior for long-term success. |

|

|

|

|

|

| · | Performance Marketing - We run data-driven campaigns across digital platforms to acquire high-intent users efficiently. Messaging focuses on our key differentiators: no-fee self-directed investing, automated S&P 500 portfolios and access to Fiscal.ai research tools, all under a simple, subscription-based membership. |

|

|

|

|

|

| · | Strategic Partnerships - We've partnered with Fundstrat and Tom Lee, one of Wall Street’s most respected strategists, to infuse institutional-grade market insights into our platform. |

|

|

|

|

|

| · | Referral & Viral Growth - Intelligent Investing is designed to be shareable. In-app referrals, social content, and member-driven moments are key levers for low-cost growth and organic momentum. |

|

|

|

|

|

| · | Social Media & PR - We engage audiences across TikTok, Instagram, LinkedIn, and X with high-integrity insights, anti-noise messaging, and high-impact creative. PR efforts focus on thought leadership, investor trust, and brand storytelling that challenges the status quo in Canadian finance. |

|

|

|

|

|

| · | Email & Lifecycle Marketing - Our email engine drives onboarding, activation, education, and long-term retention. We tailor campaigns to different stages of the member journey, always reinforcing the behaviors and mindset that lead to better outcomes. |

We continue to market our consumer lending products through the Mogo brand, which generates stable demand through established digital channels and customer base. Lending acquisition efforts are managed efficiently alongside our wealth marketing, with a focus on disciplined underwriting and high-quality borrower acquisition.

| 15 | Page |

|

| 2025 Annual Information Form |

Carta

Carta is a B2B platform with sales and marketing activities focused on fintechs, banks, and other corporations seeking to issue payment cards. Carta's primary market is Europe, with business development driven primarily through existing client relationships, channel partnerships and inbound interest, including industry referrals and digital channels.

Competitive Conditions

Mogo and Intelligent Investing

The financial services industry continues to undergo rapid transformation, driven by shifting consumer expectations, digital innovation, and growing dissatisfaction with traditional financial institutions. Our competitors include other financial technology companies, other consumer finance companies, brokerages, online lenders, mortgage brokerages, traditional financial institutions such as banks, credit unions, and new market entrants. We compete with various financial services companies in each of our main products including financial technology companies such as Wealthsimple, Koho, Questrade, Qtrade and Webull; large Schedule I banks such as TD Canada Trust, Scotiabank, Royal Bank of Canada, Tangerine, Canadian Imperial Bank of Commerce, EQ Bank and Bank of Montreal; credit unions such as Meridian Credit Union and Coast Capital Savings Federal Credit Union; and consumer credit companies such as Capital One, Fairstone Financial Inc., and goeasy.

What sets Orion Digital apart is our strategic focus on long-term financial outcomes rather than short-term engagement or product volume. Our Intelligent Investing platform is designed to disrupt the traditional wealth industry by offering a simple, powerful solution that helps users actually build wealth over time, where banks and brokers often profit from complexity, fees and frequent trading. The platform is designed to emphasize long-term investing principles, including diversification, cost efficiency, and minimizing behavioral decision errors.

We are also the only non-prime lender in Canada offering an integrated pathway from borrowing to investing -allowing us to serve a broader financial journey than most competitors. We believe our multi-pronged differentiation, including a clear value-driven strategy, 22 years of proprietary data, a strong brand, a talented team, and growing scale, positions us as a category-defining alternative to both legacy institutions and newer fintech entrants. As new players continue to enter the market, few are aligned with long-term outcomes in the way we are. Our focus is not just on acquiring users, but on helping them win financially for life.

Carta

As an issuer processor, Carta operates in a competitive market landscape that includes established legacy processing platforms as well other modern platforms. Legacy processing platforms, including TSYS, FISERV, FIS, and others historically emerged as an outsourcing of traditional bank credit and debit card processing functions and grew to become incumbent players in the payment card market. Often these platforms are based on legacy technology and were not designed to support the complex and dynamic requirements of modern fintech card issuing ecosystem.

As Carta competes against other modern issuer processors, the business leverages product differentiation, service level, pricing models, and partnership engagement to effectively compete in the market. Modern issuer processing platform competitors include Marqeta and Galileo (a subsidiary of SoFi). In some markets, Carta may also face competition from large fintech platforms such as Stripe, Adyen and Checkout.com, whose core business is not issuer processing but may be expanding to more directly compete with Carta. Competitive dynamics vary across countries and regions where Carta operates as well as within industry verticals, and Carta's B2B sales and marketing approach follows a model that is tailored to optimize growth within target market segmentation.

| 16 | Page |

|

| 2025 Annual Information Form |

Intangible Properties

In accordance with industry practice, we protect our proprietary rights through a combination of copyright, trademark, design patent, trade secret laws and contractual provisions. The source code for our software is protected under Canadian and applicable international copyright laws. We currently have a pending and registered Canadian industrial design and a pending United States design application for "Display Screen Having Graphical User Interface for Investment Management". We have no issued or pending utility patent applications.

We also seek to avoid disclosure of our intellectual property and proprietary information by requiring employees and consultants to execute non‑disclosure and assignment of intellectual property agreements. Such agreements require our employees and consultants to assign to us all intellectual property developed in the course of their employment or engagement. We also utilize non‑disclosure agreements to govern interaction with business partners and prospective business partners and other relationships where disclosure of proprietary information may be necessary.

Our software includes software components licensed from third parties, including open source software. We believe that we follow industry best practices for using open source software and that replacements for third‑party licensed software are available either as open source software or on commercially reasonable terms.

We are the registered owners of trademarks in Canada, the United Kingdom and the European Union. We are the authorized user of various social media handles, pages and profiles that reflect the Mogo and Intelligent Investing brands and we have registered and maintain the registration of a variety of domain names that include "Mogo" or variations of "Mogo", and "intelligentinvesting" as well as cartaworldwide.com.

The enforcement of our intellectual property rights depends on any legal actions against any infringers being successful, but these actions may not be successful or may be prohibitively expensive, even when our rights have been infringed.

Credit Facility

As of December 31, 2025, the Company had one credit facility outstanding: the second amended and restated revolving credit and guarantee agreement dated as of February 26, 2025, as amended (the "Credit Facility"), which is used to finance the Company's non-installment loan products. As of the date hereof, the Credit Facility remains outstanding. The 2025 amendment extended the maturity date by three years, reduced the interest rate by 100 basis points and increased the available capital from $60 million to $100 million in certain circumstances.

The Credit Facility consists of a $60 million senior secured credit facility maturing on January 2, 2029. The Credit Facility is subject to variable interest rates that reference the Secured Overnight Financing Rate ("SOFR"), or under certain conditions, the Federal Funds Rate in effect. On December 16, 2021, the Company amended the Credit Facility to lower the effective interest rate from a maximum of LIBOR plus 9%, to LIBOR plus 8%. In June 2023, this was transitioned to SOFR plus 8% upon the cessation of USD LIBOR. In February 2025, the effective interest rate was reduced to SOFR plus 7%. There is a 0.33% fee on the available but undrawn portion of the $60 million facility. The principal and interest balance outstanding for the Credit Facility as at December 31, 2025 was $51.7 million.

The Credit Facility is subject to certain covenants and events of default, including the following:

|

| · | Financial covenants that may include, among others, requirements with respect to minimum tangible net worth, maximum leverage ratio, minimum consolidated liquidity, and minimum unrestricted cash. |

|

|

|

|

|

| · | Portfolio performance covenants that may include, among others, requirements that the portfolio not exceed certain stated static pool default ratios and delinquency rates and that the loan yield not be less than stated minimum levels. |

| 17 | Page |

|

| 2025 Annual Information Form |

|

| · | Other events that may include, among others, change of control events, certain insolvency-related events, events constituting a servicer default, an inability to engage a replacement backup servicer following termination of the current backup servicer, senior management changes, the occurrence of an event of default or acceleration under other facilities, failure to make required payments or deposits, events related to the entry of an order decreeing dissolution that remains undischarged, events related to the entry or filing of judgments, attachments or certain tax liens that remain undischarged, and events related to breaches of terms, representations, warranties or affirmative and restrictive covenants. Restrictive covenants may, among other things, impose limitations or restrictions on our ability to pay dividends, redeem our stock, make payments in order to retire or obtain the surrender of warrants or options, or our ability and of the guarantors thereunder to incur additional indebtedness, pay dividends, make investments, engage in transactions with affiliates, sell assets, consolidate or merge, make changes in the nature of the business, and create liens. |

|

|

|

|

|

| · | Early termination fees that may be payable under the Credit Facility in the event of a termination or other permanent reductions of the credit commitments at the Company's option prior to the expiration of the Credit Facility. |

The Company is in compliance with these covenants. Interest expense on the Credit Facility is included in Credit Facility interest expense in the consolidated statements of operations and comprehensive loss. Management routinely reviews and renegotiates terms, including interest rates and maturity dates, and expects to continue to refinance the Credit Facility as it becomes due and payable.

Employees

As of December 31, 2025 we had 182 full-time employees and 6 part-time employees across the following functional areas, including Carta:

| Functional Area |

| Number of Full-time Employees |

| Number of Part-time Employees |

| Technology & Development |

| 56 |

| 2 |

| Customer Service & Operations |

| 97 |

| 4 |

| General and Administrative |

| 27 |

| 0 |

| Marketing |

| 2 |

| 0 |

Foreign Operations

The Company’s foreign operations consist primarily of Carta, which provides issuer processing and payments infrastructure services across Europe. Carta currently operates card programs in over 11 countries with approximately 97% of Carta's 2025 revenues being derived from its operations in Europe. During 2025, the Company ceased Carta’s Canadian payments operations in order to focus the platform on its core European business.

General Development of the Business

Orion Digital has continued its evolution with a series of strategic and financial initiatives throughout 2025 and early 2026 as described in more detail below.

| 18 | Page |

|

| 2025 Annual Information Form |

Current Financial Year – Recent Developments

In 2026 year-to-date, Orion Digital:

|

| · | Completed a Corporate Rebrand and Ticker Change. On December 29, 2025, the Company changed its corporate name from Mogo Inc. to Orion Digital Corp., reflecting its evolution toward a multi-platform digital financial infrastructure business operating across wealth and payments. The Company’s common shares began trading under the new ticker symbol “ORIO” on Nasdaq and TSX on January 2, 2026. |

|

|

|

|

|

| · | Exited Remaining WonderFi Position. In January 2026, the Company exited its remaining equity position in WonderFi. The transaction increased the Company’s cash and cash equivalents by more than 50% compared to Q3 2025 to approximately $27 million, further strengthening the Company’s balance sheet and liquidity position. |

Three Year History

In 2025, Orion Digital:

|

| · | Completed Phase 1 of the Redesign and Rebuild of Intelligent Investing Platform. In Q4 2025, the Company completed Phase 1 of the comprehensive redesign and rebuild of the Intelligent Investing platform, including enhancements to performance and reliability, expanded portfolio information and suitability processes, new goal-setting and planning tools, improved transfer management capabilities, and other product and user experience improvements. Assets under management on the Company’s wealth platform totaled $498.3 million as at Q4 2025, representing a 17% increase year-over-year. |

|

|

|

|

|

| · | Extended Credit Facility with Fortress Investment Group. In February 2025, the Company amended the Credit Facility, being its senior secured credit facility with funds managed by affiliates of Fortress Investment Group LLC. The amendments extended the maturity date by three years, until January 2, 2029, and reduced the interest rate by 100 basis points from SOFR plus 8%, to SOFR plus 7%. |

|

|

|

|

|

| · | Exited Legacy Institutional Brokerage Business. In Q1 2025, the Company exited its legacy institutional brokerage business, as part of management’s strategic focus on eliminating sub-scale revenue streams and prioritizing higher margin offerings. The institutional brokerage business contributed $5.3 million of revenue for the financial year ended December 31, 2024, with a negligible operating margin. These revenues were reported within other subscription and services revenue. |

|

|

|

|

|

| · | Monetized WonderFi Investment. In May 2025, WonderFi announced that it had entered into a definitive agreement to be acquired by Robinhood Markets, Inc. In 2025, the Company monetized approximately $19.5 million of its investment in WonderFi. |

|

|

|

|

|

| · | Refocused Carta on European Payments Operations. During 2025, the Company ceased payments operations in Canada in order to focus the Carta platform primarily on European payments programs. Excluding the previously exited Canadian operations, European payments volume increased from $2.8 billion in Q4 2024 to $3.1 billion in Q4 2025, representing growth of 14% year-over-year. |

|

|

|

|

|

| · | Completed Carta Migration to Oracle Cloud Infrastructure. In Q1 2025, Carta completed its transition to Oracle Cloud Infrastructure (“OCI”), supporting the scalability and operational efficiency of the Company’s payments platform in Europe. |

|

|

|

|

|

| · | Continued Share Repurchase Program. In 2025, the Company repurchased 548,091 common shares under its share repurchase program. As of December 31, 2025, Orion Digital had repurchased a total of 1,667,185 common shares since June 2022, representing approximately 7.0% of its outstanding shares. |

| 19 | Page |

|

| 2025 Annual Information Form |

|

| · | Continued Execution on its Bitcoin treasury strategy. The Company believes its Bitcoin exposure appropriately reflects its long-term capital allocation objectives. Management’s near-term capital allocation priorities remain focused on reinvesting in the Company’s Wealth and Payments platforms and opportunistically repurchasing common shares where appropriate. |

|

|

|

|

|

| · | Adapted Lending Products to New Interest Rate Legislation. Effective January 1, 2025, the Company became subject to new legislation in Canada that reduces the maximum allowable interest rate to 35% APR. The Company has implemented changes to its lending products to comply with these requirements. All loans originated in 2025 were issued at rates within the new legislative limit. |

In 2024, Orion Digital:

|

| · | Launched Moka.ai. In March 2024, the Company announced the launch of Moka.ai, the next generation of its wealth-building app with significant updates and enhancements designed to help the next generation of Canadians get on a real path to becoming millionaires and achieving financial freedom. |

|

|

|

|

|

| · | Added Bitcoin to its Treasury Management Strategy. In March 2024, the Company announced that its Board of Directors has approved a change to its treasury management strategy to include Bitcoin and Bitcoin ETFs and authorized an initial investment of up to $5.0 million. As of the date hereof, the Company holds less than US$1 million in Bitcoin ETFs. |

|

|

|

|

|

| · | Resumed share repurchases under Nasdaq buyback program. The Company announced the resumption of repurchases of Common Shares under its Nasdaq buyback program as part of its ongoing efforts to enhance shareholder value. In 2024, the Company repurchased 44,741 Common Shares at an average price of $2.30 per Common Share. This follows the repurchase of 474,353 Common Shares in 2023 at an average price of $2.36 per Common Share. By continuing the buyback program, the Company aims to address the perceived valuation of the Common Shares and support long-term growth to better reflect the Company’s financial performance and strategic investments, such as its 13% stake in WonderFi. |

|

|

|

|

|

| · | Extended Maturity of $60 Million Credit Facility to 2026. The Company announced an extension of the maturity date for its $60 million senior credit facility with Fortress Investment Group from July 2, 2025, to January 2, 2026. This amendment provided the Company with continued access to the resources and flexibility necessary to support its digital lending product. |

|

|

|

|

|

| · | Launched “Buffett Mode” Self-Directed Investing App. The Company announced the launch of its “Buffett Mode” self-directed investing app, designed to help Canadians move away from speculative trading and adopt long-term, value-based investing principles inspired by Warren Buffett. The app encourages disciplined, patient investing by adding thoughtful prompts and reducing the temptation for frequent trading, a common issue in many trading platforms. With a flat subscription fee model, the app offers zero commission and FX fees, aligning success with user outcomes. Additionally, the platform promotes positive environmental impact, with users contributing to replanting Canadian forests. |

|

|

|

|

|

| · | Partnered with Postmedia to Launch Educational Wealth Content Channel. The Company announced a strategic partnership with Postmedia, Canada’s largest news media company, to create a new digital wealth content channel aimed at educating Canadians on investing, wealth accumulation, and financial management. As the founding sponsor, Mogo will contribute educational resources, including its wealth calculator, to help users improve their financial literacy. Postmedia, with a reach of 17.8 million Canadians monthly, will independently operate the channel on its Financial Post platform. Additionally, Mogo issued 500,000 warrants to purchase Common Shares to Postmedia as part of the agreement. |

| 20 | Page |

|

| 2025 Annual Information Form |

|

| · | Partnered Exclusively with Tom Lee’s Fundstrat to Offer Equity Market Research. The Company announced an exclusive partnership with Thomas Lee’s Fundstrat Global Advisors to provide users of its digital wealth solutions with premium access to top-tier equity market research. This collaboration offers Canadian retail investors exclusive insights from Fundstrat’s FS Insight research, which is typically available to large institutional clients. As a result of the partnership, our users have access to exclusive webinars, interviews, and research from Tom Lee and other experts, aimed at enhancing their investment decision-making and giving them a competitive edge in the market. |

|

|

|

|

|

| · | Carta Reported 23% Increase in Transaction Volume. Carta reported a 23% increase in quarterly transaction volume, reaching a record $3.0 billion in Q3 2024. This growth highlights Carta’s expanding reach, particularly with large European customers, bringing its annual run rate to $12 billion. |

|

|

|

|

|

| · | appointed a New Auditor. On October 1, 2024, the Company appointed MNP LLP, Chartered Professional Accountants, as the Company’s new auditor, replacing KPMG LLP, Chartered Professional Accountants. |

In 2023, Orion Digital:

|

| · | Announced WonderFi Business Combination. In July 2023, the Company announced that Coinsquare Ltd. (“Coinsquare”) completed a business combination with WonderFi and CoinSmart Financial Inc. This transaction positioned the resulting entity, WonderFi (TSX:WNDR), as the only fully regulated crypto exchange in Canada. The Company’s shares in Coinsquare were exchanged for ~87.0 million shares of WonderFi in the business combination, making the Company the largest shareholder of WonderFi. Certain of the WonderFi shares were subject to a lock-up period, with gradual release scheduled until January 2025. |

|

|

|

|

|

| · | Entered Multi-Year Agreements with Oracle. The Company entered multi-year agreements with OCI in October 2023 to transition to its cloud infrastructure to support the long-term growth of the Company’s digital wealth platform. Carta also announced that it selected OCI to accelerate innovation and support future growth. |

|

|

|

|

|

| · | Expanded Partnership with Snowflake. The Company expanded its partnership with Snowflake, the Data Cloud company, to integrate AI applications and scale its digital wealth offerings. By leveraging Snowflake’s Data Cloud, Mogo aims to enhance processing efficiency and introduce innovative AI solutions, empowering users to invest more effectively and achieve financial freedom. |

|

|

|

|

|

| · | Completed a Share Consolidation. In August 2023, the Company completed a share consolidation at a ratio of three pre-consolidation Common Shares to one post-consolidation Common Share (the “Share Consolidation”), regaining compliance with the minimum bid price requirement under the Nasdaq Listing Rule 555(a)(2). The Common Shares commenced trading on the TSX and Nasdaq on a post-consolidation basis at the start of trading on August 14, 2023. |

|

|

|

|

|

| · | Prioritized Profitability. During the year ended December 31, 2023, the Company continued to focus on accelerating the path to profitability by placing an emphasis on cost efficiency and building financial resiliency in light of challenging financial market conditions. The Company narrowed its strategic focus and completed the wind down of its legacy Mogo app including its prepaid card product, MogoCard, and its identity fraud monitoring product, MogoProtect. |

|

|

|

|

|

| · | Amended Postmedia Agreement. The company amended its marketing collaboration agreement with Postmedia, and extended it until December 31, 2024, aiming to leverage Postmedia’s extensive media network to reach a broader audience. |

| 21 | Page |

|

| 2025 Annual Information Form |

|

| · | Launched MogoTrade App in Quebec. In 2023, the Company expanded its market reach by launching the MogoTrade app in Quebec, offering it in both English and French languages. This move increased the company’s total addressable market opportunity by approximately 28%. Additionally, on May 15, 2023, MogoTrade removed invitation-only restrictions, making the application available to the general public. |

|

|

|

|

|

| · | Filed New Base Shelf Prospectus. On November 6, 2023, the Company filed a final short form base shelf prospectus with the securities regulators in each province and territory of Canada, except Quebec. The prospectus replaced the prospectus that was filed in 2021, enabling the Company to make offerings of Common Shares, preferred shares, debt securities, warrants to purchase Common Shares, preferred shares or debt securities, or any combination thereof of up to an aggregate offering price of US$250 million at any time during the 25-month period that the prospectus remains effective. |

|

|

|

|

|

| · | Announced Carta’s Growth. The Company’s digital payment solutions business, Carta, experienced significant growth, processing over $2.2 billion of payments volume in Q1 2023. This marked a notable increase of over 43% compared to Q1 2022, reflecting the continued expansion and adoption of Carta’s services. |

|

|

|

|

|

| · | Launched Normal Course Issuer Bid on TSX. In August 2023, the Company received approval from the TSX to commence repurchasing its Common Shares on the TSX pursuant to a normal course issuer bid (the “NCIB”). The NCIB is in addition to the Company’s existing Common Share buyback program launched on the Nasdaq in March 2022 (the “Nasdaq Bid” and together with the NCIB, the “Bids”). Under the Bids, the Company may purchase up to 2,183,000 Common Shares (on a post-consolidation basis), representing approximately 10% of the public float of Mogo’s outstanding Common Shares as at March 21, 2023. Purchases under the Bids will be made through the facilities of the TSX, Nasdaq or other designated exchanges or any Canadian or US alternative trading system. In accordance with the policies of the TSX, the period of the NCIB was considered to have commenced on March 22, 2023 and ran until March 21, 2024. Under the NCIB, the Company repurchased 104,800 Common Shares through the facilities of the TSX. The Nasdaq Bid remains on-going and the Company is able to repurchase up to US$7.5 million in Common Shares thereunder. |

| 22 | Page |

|

| 2025 Annual Information Form |

Risk Factors

In addition to any other risks contained in this AIF, as well as our management’s discussion and analysis and consolidated financial statements and accompanying notes, the risks described below are the principal risks that could have a material and adverse effect on our business, financial condition, results of operations, cash flows, future prospects or the trading price of our Common Shares. This AIF also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of a number of factors, including the risks described below. See “Cautionary Note Regarding Forward Looking Statements”.

Worsening economic conditions may cause our members’ loan default rates to increase and harm our operating results.

Approximately 35% of our assets as of December 31, 2025 consisted of loans to our members. Uncertainty and negative trends in general economic conditions in Canada and abroad, including significant tightening of credit markets, historically have created a difficult environment for companies operating in our industries. Current global and macroeconomic conditions remain in a state of heightened volatility due to a number of factors, including geopolitical risks and tensions, changes in government administrations, regulations, legislation and policies, and trade relations and ongoing trade tensions, including the threat of tariffs, other governmental actions and retaliatory actions. In particular, tariffs imposed by the United States on Canadian imports, together with retaliatory tariffs imposed by Canada on U.S imports, have created significant economic uncertainty. These tariffs have contributed to inflationary pressures, supply chain disruptions, reduced consumer confidence, and increased volatility in the Canadian dollar and capital markets. There can be no assurance that the current tariff regime will be eased, and any escalation or prolonged continuation of trade tensions between Canada and the United States could further weaken the economic conditions in which we operate. These factors, which are beyond our control, may influence inflation, interest rates, unemployment levels, consumer confidence, economic growth in the geographies in which the Company operates and other general economic conditions. The Company continues to monitor global and macroeconomic developments and may take steps to mitigate potential risks. However, there can be no assurance that such developments will not have a material adverse effect on the Company’s business, financial condition or results of operations.

In addition, there can be no assurance that economic conditions will remain favorable for our business or that default rates on our loans by our members will remain at current levels. Increased default rates by our members on our loans may inhibit our access to capital and negatively impact our profitability. If delinquency or uncollectable rates on our consumer loans exceed certain levels defined in the Credit Facility it could constitute a default under the Credit Facility or other credit facilities, reducing or terminating such facilities. Furthermore, we receive a number of applications from potential members who do not satisfy the requirements for our loans. If an insufficient number of qualified individuals apply for our loans, our growth and revenue could decline.

Our allowance for loan losses is determined based upon both objective and subjective factors and may not be adequate to absorb loan losses.

We face the risk that our members will fail to repay their loans in full. We reserve for such losses by establishing an allowance for loan losses, the increase of which results in a charge to our earnings as a provision for loan losses. We have established an evaluation process designed to determine the adequacy of our allowance for loan losses. While this evaluation process uses historical and other objective information, the classification of loans and the forecasts and establishment of loan losses are also dependent on our subjective assessment based upon our experience and judgment. Actual losses are difficult to forecast, especially if such losses stem from factors beyond our historical experience, and unlike traditional banks, we are not subject to periodic review by bank regulatory agencies of our allowance for loan losses. As a result, there can be no assurance that our allowance for loan losses will be comparable to that of traditional banks subject to regulatory oversight or sufficient to absorb losses. A significant increase in our allowance for loan losses could also adversely affect our available capital and our ability to comply with financial covenants under our Credit Facility, which could restrict our access to funding. Any of the foregoing could have a material adverse effect on our business, financial condition and results of operations.

| 23 | Page |

|

| 2025 Annual Information Form |

We rely on our proprietary credit scoring model in the forecasting of loss rates. If we are unable to effectively forecast loss rates, it may negatively impact our operating results.