CANAGOLD RESOURCES LTD.

Fourth Quarter Report

Management Discussion and Analysis

(expressed in United States dollars)

Years ended December 31, 2025 and 2024

CANAGOLD RESOURCES LTD.

(the "Company")

Fourth Quarter Report

Management's Discussion and Analysis

For the Years ended December 31, 2025 and 2024

(expressed in United States dollars)

CAUTION - FORWARD LOOKING STATEMENTS

Certain statements contained herein regarding the Company and its operations constitute "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995. All statements that are not historical facts, including without limitation statements regarding future estimates, plans, objectives, assumptions or expectations of future performance, are "forward-looking statements". We caution you that such "forward looking statements" involve known and unknown risks and uncertainties that could cause actual results and future events to differ materially from those anticipated in such statements. Such risks and uncertainties include fluctuations in precious metal prices, unpredictable results of exploration activities, uncertainties inherent in the estimation of mineral reserves and resources, if any, fluctuations in the costs of goods and services, problems associated with exploration and mining operations, changes in legal, social or political conditions in the jurisdictions where the Company operates, lack of appropriate funding and other risk factors, as discussed in the Company's filings with Canadian and American Securities regulatory agencies. The Company expressly disclaims any obligation to update any forward-looking statements, other than as may be specifically required by applicable securities laws and regulations.

1.0 Preliminary Information

The following Management's Discussion and Analysis ("MD&A") of Canagold Resources Ltd. (the "Company", "Canagold") should be read in conjunction with the accompanying the audited consolidated financial statements as at December 31, 2025, 2024 and 2023, and a summary of significant accounting policies and other explanatory information, prepared in accordance with IFRS Accounting Standards as issued by the International Accounting Standards Board ("IASB"), all of which are available on the SEDAR+ website at www.sedarplus.ca.

All dollar amounts in the MD&A are expressed in United States dollars unless otherwise indicated.

All information contained in the MD&A is effective as of March 31, 2026 unless otherwise indicated.

1.1 Background

The Company was incorporated under the laws of British Columbia, and was engaged in the acquisition, exploration, development and exploitation of precious metal properties.

As the Company is focused on its mineral exploration activities, there is no mineral production, sales or inventory in the conventional sense. The recoverability of amounts capitalized for mineral property interests is dependent upon the existence of reserves in its mineral property interests, the ability of the Company to arrange appropriate financing and receive necessary permitting for the exploration and development of its property interests, confirmation of the Company's interest in certain properties, and upon future profitable production or proceeds from the disposition thereof. Such exploration and development activities normally take years to complete and the amount of resulting income, if any, is difficult to determine with any certainty at this time. Many of the key factors are outside of the Company's control. As the carrying value and amortization of mineral property interests and capital assets are, in part, related to the Company's mineral reserves and resources, if any, the estimation of such reserves and resources is significant to the Company's financial position and results of operations.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.2 Overall Performance

The Company currently owns a direct interest in the precious metal properties, known as the New Polaris property (British Columbia), the Windfall Hills property (British Columbia), and the Corral Canyon property (Nevada) as well as a portfolio of smaller exploration properties in Nevada and Idaho.

1.2.1 New Polaris property (British Columbia, Canada)

The Company owns a 100% interest in the New Polaris property, located in the Atlin Mining Division, British Columbia, The Company acquired the 100% interest in the New Polaris property from Rembrandt Gold Mines Ltd in 1994. The project is stated in certain public disclosure to be subject to a 15% net profit interest, which Canagold can reduce to 10% net profit interest by issuing 150,000 shares to Rembrandt Gold Mines Ltd. Canagold has disputed the validity of the net profit interest and no net profit interest, royalty or other duly executed agreement has been proffered or presented which supports the existence of the net profit interest. As such, Canagold has excluded the net profit interest from the economic model calculation.

Feasibility study

On July 21, 2025, the Company announced the feasibility study results. The feasibility study report was filed on SEDAR PLUS on September 3, 2025.

Feasibility study highlights include (all dollar figures in the highlights are in Canadian dollars, unless otherwise indicated):

Project Economics

High Grade, Low CAPEX and Low AISC

After-Tax NPV (5%), IRR and Cash Flow Sensitivities to Gold Prices

| Low Case | Base Case | High Case | Spot Case | |

| Gold Price (US$/oz) | $2,200 | $2,500 | $2,800 | $3,300 |

| After-Tax NPV (5%) (C$M) | $287 | $425 | $564 | $793 |

| After-Tax IRR (%) | 23.5 | 30.9 | 37.5 | 47.3 |

| After-Tax Payback (years) | 2.9 | 2.4 | 2.1 | 1.7 |

| After-Tax NPV/Initial Capex | 1.1 | 1.7 | 2.3 | 3.2 |

| After-Tax Free Cash Flow ($M) | $465 | $649 | $835 | $1,145 |

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Table 2: New Polaris FS Project Parameters

| Base Case Economic Assumptions | |

| Gold Price (US$/oz) | $2,500 |

| Exchange Rate (C$/US$) | 0.725 |

| Discount Rate | 5% |

| Contained Metals Mined | |

| Contained Gold (koz) | 904 |

| Contained Antimony (tonnes) | 5173 |

| Mining | |

| Mine Life (years) | 8.3 |

| Waste (Mt) | 1.8 |

| Total Material Mined (Mt) | 4.6 |

| Total Mineralized Material Mined (Mt) | 2.8 |

| Processing | |

| Processing Throughput (ktpa) | 340 |

| Average Diluted Gold Grade (g/t) | 9.9 |

| Gold Production | |

| Gold Recovery (%) | 89.1 |

| LOM Recovered Gold in Concentrate (xoz) | 806 |

| LOM Payable Gold Production (koz) | 709 |

| LOM Avg. Annual Gold Production (koz) | 85.7 |

| Operating Costs Per Tonne | |

| Mining Cost ($/t Milled) | $135 |

| Processing Cost ($/t Milled) | $64 |

| G&A Cost (C$/t Milled) | $68 |

| Total Operating Costs ($/t Milled) | $267 |

| Other Costs | |

| Concentrate Transportation to Smelter ($/wmt) | $1,089 |

| Cash Costs and All-in Sustaining Costs | |

| LOM Cash Cost (US$/oz Au) | $997 |

| LOM All-in Sustaining Cost (US$/oz Au) | $1,247 |

| Capital Expenditures | |

| Pre-production Capital Expenditures ($M) | $250 |

| Sustaining Capital Expenditures ($M) | $225 |

| Closure Expenditures ($M) | $21 |

| Economics | |

| After-Tax NPV (5%) ($M) | $425 |

| After-Tax IRR % | 30.9 |

| After-Tax Payback Period (years) | 2.4 |

| After-Tax NPV / Initial Capex | 1.7 |

| Pre-Tax NPV (5%) ($M) | $667 |

| Pre-Tax IRR % | 38.4 |

| Pre-Tax Payback Period (years) | 2.3 |

| Pre-Tax NPV / Initial Capex | 2.7 |

| LOM After-tax Free Cash Flow ($M) | 649 |

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Mineral Resource Estimate

The Company's current Mineral Resource Estimate ("MRE"), completed by Moose Mountain Technical Services, has an effective date of January 22, 2025 with the mineralization model as the basis for the FS. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability at this time.

The New Polaris Mineral Resources for gold and antimony are shown in the tables below:

New Polaris April 2, 2025 Gold Resource Estimate at 4 g/t cut-off

| Resource Class | Tonnes (000's) | Au (g/t) | Au Metal Ozs (000's) |

| Indicated | 2,965 | 11.6 | 1,107 |

| Inferred | 926 | 8.5 | 266 |

Antimony Resource Estimate within the Base Case Au Resource

| Resource Class | Tonnes (000's) | Sb (%) | Sb Metal (Tonnes) |

| Indicated | 860 | 0.65 | 5,630 |

| Inferred | 100 | 1.2 | 1,195 |

Notes on the Resource Tables:

1. The Mineral Resource Estimate was completed by Sue Bird, P.Eng. who is a Qualified Person as defined under NI 43-101.

2. Resources are reported using the 2014 CIM Definition Standards and were estimated using the 2019 CIM Best Practices Guidelines.

3. The base case Mineral Resource has been confined by "reasonable prospects of eventual economic extraction" shape using the following assumptions:

4. The resulting Net Smelter Return per tonne of ore equation is: NSR (CDN$/t) = Au (g/t) x 90.5% x C$74.72 /g Au.

5. The specific gravity is 2.81 for the entire deposit.

6. The Antimony Resource is reported as a subset of the total Mineral resource at the 4 g/t Au cutoff.

7. The Sb is a by-product of the Au processing and therefore is reported using the same Classification as the Au resource at the 4 gpt Au cutoff.

8. Numbers may not add due to rounding.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

About the Mineral Resource Estimate

Mineral Reserve Estimate

The mineral reserves are summarized in table below.

Mineral Reserves

| Reserve Class | Tonnes (000's) | Au (g/t) | Au Metal Ounces ('000s) |

| Probable | 2,830.2 | 9.94 | 904.4 |

| Total | 2,830.2 | 9.94 | 904.4 |

Notes on the Reserve Table:

1. This Mineral Reserve Estimate has an effective date of July 10, 2025 and is based on the updated Mineral Resource estimate issued on February 21, 2025 by Moose Mountain Technical Services.

2. The Mineral Reserve estimate was completed under the supervision of Dino Pilotto, P.Eng. of JDS Energy and Mining Inc., who is a Qualified Person as defined under NI 43-101.

3. A cut-off grade of 6.0 g/t Au was used to define reserves for production and a 4.2 g/t Au marginal cut-off value for development ore, based on a gold metal price of U$2,245/oz., exchange rate of CAD$1.39 = US$1.00.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

4. Processing costs of C$88/t ore, C$105/t mining costs, G&A costs of C$67/t ore, gold processing recovery of 89.75%, and payable gold of 90%.

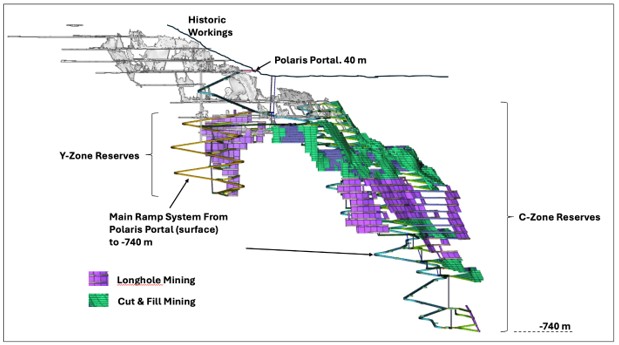

Mining Overview

The New Polaris mine is designed as a modern, fully-mechanized underground operation, targeting the safe and cost-effective extraction of mineral reserves over an estimated 8.3 year mine life. The plan anticipates delivering approximately 2.8 million tonnes (Mt) of mill feed at an average grade of 9.9 g/t gold.

A total of 1.8 Mt of waste rock will be generated during LOM underground development. Of this, the majority will be used as backfill material within the mine to support mined-out areas, with the remaining volume placed on surface in the integrated tailings and waste rock storage facility.

The mineral reserves are located beneath the historic workings of the Polaris-Taku mine, which operated from 1938 to 1951 and produced 740,000 tonnes at an average grade of 10.3 g/t gold. The new underground access will be established via a ramp extending from the existing New Polaris portal, reaching an ultimate depth of approximately 780 meters. The primary ore body, known as the 'C' zone, accounts for nearly 90% of total reserves, extends up to 500 meters along strike, and dips at an average angle of 50 to 60 degrees.

Geotechnical assessments indicate favorable rock conditions, with typical ground control measures and associated costs anticipated.

To optimize recovery and minimize costs, two main mining methods will be employed:

Mine development and early construction activities will be carried out by an experienced underground mining contractor, with operations transitioning to an owner-operated model upon commencement of production. The underground mine is expected to employ approximately 190 personnel, sustaining an average production rate of 950 tpd throughout the mine's operating life.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Processing Overview

Processing will occur in a 1000 tpd crushing, grinding and flotation plant to produce a bulk sulphide flotation concentrate which will be shipped off site for final processing at an independent processing facility.

Crushed ore is ground to 80% minus 74um and fed into a flotation circuit consisting of one stage of rougher flotation with two cleaning stages to produce concentrate grading > 100 g/t Au.

Flotation concentrate is thickened, filtered and dried, to a moisture of approximately 5% and flown to Juneau, Alaska, which is located approximately 60 km from site, then barged to Seattle for loading onto ocean going ships for transportation to third-party smelters worldwide.

A portion of the process tailings will be fed to a backfill plant and used for filling underground mining voids, the balance will be filtered and trucked to a dry-stack storage facility located about 1 km from the plant site. Waste rock not used for underground backfilling will also be trucked to this facility for storage with the tailings.

Concentrate Marketing Study

An independent concentrate marketing study for the New Polaris Project, evaluating marketability and treatment terms for its gold concentrate has been completed as part of the FS. The study confirms that the New Polaris gold concentrate, targeted at a grade exceeding 100 g/t Au, and an average 12% As, is marketable under current global conditions.

The report identifies potential outlets for the sale of New Polaris gold concentrate, including:

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Based on indicative commercial terms provided by several prospective buyers, the marketing study validated the project's financial modeling assumptions related to treatment charges and gold payability. The analysis concluded that an average net smelter return (NSR) of 87.9% for gold is reasonable over the LOM and reflects treatment charges associated with the presence of As in the concentrate.

Capital Costs

The initial capital cost is estimated at $250M (US$181M) and shown in the table below:

| Initial | Sustaining | LOM Total | |

| Mining ($M) | $63.3 | $196.1 | $259.4 |

| Processing ($M) | $43.0 | - | $43.0 |

| Tailings ($M) | $7.4 | $4.7 | $12.1 |

| Onsite Infrastructure ($M) | $38.5 | - | $38.5 |

| Offsite Infrastructure ($M) | $9.4 | - | $9.4 |

| Indirects ($M) | $42.3 | - | $42.3 |

| Project Delivery ($M) | $9.8 | - | $9.8 |

| Owner's Costs ($M) | $7.8 | - | $7.8 |

| Total excluding Contingency ($M) | $221.5 | $200.8 | $422.3 |

| Project Contingency ($M) | $28.8 | $24.2 | $53.0 |

| Closure ($M) | - | - | $20.5 |

| Total ($M) | $250.4 | $225.0 | $495.8 |

Note: Totals may differ slightly due to rounding

Operating Costs

The LOM Total Cash Cost is US$997/oz Au payable while the LOM AISC is US$1,247/oz Au payable. Unit Operating costs are shown in the table below.

Operating Costs Per Tonne Milled

| Operating Costs Per Tonne | $/t |

| Mining Cost ($/t Milled) | 135.45 |

| Processing Cost ($/t Milled) | 64.28 |

| G&A Cost ($/t Milled) | 67.58 |

| Total Operating Costs ($/t Milled) | 267.31 |

Financial Analysis

At a US$2,500 base case gold price and a C$:US$ exchange of 0.725:1, the Project generates an after-tax NPV (5%) of $425 million and IRR of 30.9%. Payback on initial capital is 2.4 years.

The Project Financials are shown in table below:

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

New Polaris Project Financials

| After-Tax NPV (5%) ($M) | $425 |

| After-Tax IRR (%) | 30.9 |

| After-Tax Payback Period (years) | 2.4 |

| After-Tax NPV / Initial Capex | 1.7 |

| Pre-Tax NPV (5%) ($M) | $667 |

| Pre-Tax IRR (%) | 38.4 |

| Pre-Tax Payback Period (years) | 2.3 |

| Pre-Tax NPV / Initial Capex | 2.7 |

| LOM After-tax Free Cash Flow ($M) | $649 |

Regulatory and Environmental Assessment Process

The Project is subject to a range of regulatory approvals, including a consent decision from the Taku River Tlingit First Nation (TRTFN) and an Environmental Assessment Certificate (EAC) under British Columbia's Environmental Assessment Act. Once the environmental assessment process is completed, the necessary construction and operating permits may be applied for and issued in accordance with applicable provincial and federal legislation.

The project formally entered the BC Environmental Assessment (EA) process in 2023. In September 2024, the British Columbia Environmental Assessment Office (BCEAO) issued a Readiness Decision, concluding there is sufficient information to proceed with the Environmental Assessment Application. Canagold's consulting team is currently preparing the required technical studies and supporting documentation, with the EA application targeted for submission at the end March 2026.

The ongoing involvement, input, and support of the TRTFN have been instrumental in ensuring that their interests are recognized and addressed throughout the process. Their collaboration continues to play a critical role in helping advance and streamline the regulatory review.

For more details, see the news release of the Company issued on July 21, 2025 and named Canagold Announces Positive Feasibility Study Results for the New Polaris Project.

Qualified Persons who approved the issuance of the feasibility results are:

In accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects, Garry Biles, P. Eng., President & COO is the Qualified Person for the Company and has prepared, validated, and approved the technical and scientific content of this news release. The Company strictly adheres to CIM Best Practices Guidelines in conducting, documenting, and reporting activities on its projects.

Sue Bird, M Sc., P.Eng., V.P. of Resources and Engineering at Moose Mountain Technical Services, an independent Qualified Person as defined by NI 43-101. Sue has also reviewed and approved the technical information about the 2025 MRE resource contained in this news release.

Tommaso Roberto Raponi, P. Eng., Principal Metallurgist with Ausenco Engineering Canada ULC., is an independent Qualified Person as defined by NI 43-101 and has reviewed and verified the contents of this news release. Mr. Raponi is responsible for mineral processing and metallurgical testing in the technical report.

Kevin Murray, P. Eng., Principal Process Engineer for Ausenco Engineering Canada ULC., is an independent Qualified Person as defined by NI 43-101 and has reviewed and verified the contents of this news release. Mr. Murray is responsible for processing, process and infrastructure capital and operating cost estimation, financial analysis and marketing in the technical report.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

James Millard, P. Geo., Director, Strategic Projects with Ausenco Sustainability ULC., a wholly owned subsidiary of Ausenco Engineering Canada ("Ausenco") is an independent Qualified Person as defined by NI 43-101 and has reviewed and verified the contents of this news release. Mr. Millard is responsible for the sections and subsections related to environmental, permitting, and social and community aspects in the technical report.

Jonathan Cooper, MSc., P.Eng., Water Resources Engineer with Ausenco Sustainability ULC., a wholly owned subsidiary of Ausenco Engineering Canada ("Ausenco") is an independent Qualified Person as defined by NI 43-101 and has reviewed and verified the contents of this news release. Mr. Cooper is responsible for the sections and subsections related to site-wide water management in the technical report.

Dino Pilotto, P. Eng., General Manager, Technical Services with JDS Energy & Mining Inc., is an independent Qualified Person as defined by NI 43-101 and has reviewed and verified the contents of this news release. Mr. Pilotto is responsible for mining methods in the technical report.

Mike Levy, P. Eng., Geotechnical Manager with JDS Energy & Mining Inc., is an independent Qualified Person as defined by NI 43-101 and has reviewed and verified the contents of this news release. Mr. Levy is responsible for the underground geotechnical assessment in the technical report.

History of other exploration advancements:

On April 17, 2019, the Company filed on SEDAR its updated NI 43-101 report (the "Preliminary Economic Assessment") by Moose Mountain Technical Services ("Moose Mountain"). The details of the Preliminary Economic Assessment" report can be found in the latest annual information form of the Company filed on SEDAR +.

In September 2020, the Company was granted a Multi Year Area Based Notice of Work Mineral and Coal Exploration Activities and Reclamation Permit by the BC Ministry of Energy, Mines and Low Carbon Innovation to conduct exploration work on the property. Site preparation and refurbishment was completed to facilitate environmental baseline study and infill drilling to advance to a feasibility study. In late 2020, the Company had initiated environmental baseline studies which are required for an Environmental Assessment Certificate application and which is a critical first step in advancing the project through the BC major mine permitting process.

In 2021, the Company completed its 47-hole, 24,000 meter (m) infill drilling program designed to upgrade the Inferred Resources of the CWM vein system to an Indicated Resource category for inclusion in a future feasibility study. The infill drill holes range in depth from 300 to 650 m and are designed to provide greater density of drill intercepts (20 - 25 m spacing) in areas of Inferred Resources between 150 and 600 m below surface. The drill program was extended with an additional 6,000 m and 7 drill holes completed by the end of February 2022. The infill drill holes intercepted gold grades over widths throughout the CWM vein system that support the current resource at depth as predicted by the geological model and defined in the Preliminary Economic Assessment. Additionally, the infill drill program has defined new areas of significant gold mineralization such as the C-9 and C-10 veins that have potential to add resource to the deposit. By mid July 2022, assay results were received for all 54 holes of the drill program.

In August 2022, the Company mobilized an 8,000 m drilling program targeting the shallower high-grade Y-vein system which consists of two parallel, steeply dipping veins striking north-south and located just north of the C-West Main vein. This target provides an opportunity to define high grade resources at a shallow depth that could be accessed early in the mine life. High grade intercepts from previous drill holes in this area included 30.6 grams per tonne ("gpt") gold ("Au") over 3.2 m, 13.0 gpt Au over 6.8 m and 22.7 gpt Au over 8.0 m. The drilling program was designed to upgrade the Y-vein resources from Inferred to Indicated category for inclusion in the feasibility study and to explore this vein system for extensions at depth. By late January 2023 assay results were received for all 25 drill holes of the Y vein drill program.

In October 2022, the Company retained Ausenco Engineering Canada Inc. to complete a feasibility study for the New Polaris gold project. Key objectives for the feasibility study include:

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

The feasibility study concluded in the summer of 2025.

In October 2022, the Company signed the Hà Khustìyxh / "Our Way" agreement that establishes the framework for a cooperative and mutually respectful working relationship with the Taku River Tlingit First Nation ("TRTFN") to support Canagold's exploration and advancement activities at New Polaris while ensuring to minimize any adverse impacts of mining activity on the rights and interests of the TRTFN. The agreement also lays the foundation for negotiation of future long-term agreements as the project progresses through its permitting, construction and production phases.

In March 2023, the Company submitted its Initial Project Description (IPD) and Engagement Plan submission to the B.C. Environmental Assessment Office. The Company's IPD submission formally initiates the early engagement phase of the provincial assessment process. In the IPD, the Company provides an overview and detailed description of the Company's plans to develop, operate, and eventually decommission the New Polaris Gold Project.

In May 2023, the resource model was updated to:

• 89% increase in the Indicated category contained ounces of gold compared to the 2019 preliminary economic assessment resource due to a very successful 2021-22 infill drill program.

• 23% increase to the overall resource tonnage due to the additional veins defined by the 2021-22 infill drilling that were integrated into the new geological model

• Gold grade improvement by 8% in the indicated category to 11.61 gpt Au, up from 10.8 gpt Au in the 2019 preliminary economic assessment due to the refined geological model constrained by the additional drilling.

• The updated 2023 MRE provides the Indicated category resource required to underpin the feasibility study announced on October 11, 2022.

• Underground mineral resource estimate 2.97 million tonnes (Mt)@ 11.6 grams per tonne gold (gpt Au) for 1.11 million ounces (Moz) contained gold indicated and 0.93 Mt @ 8.93 gpt Au for 0.27 Moz contained gold inferred.

Deepak Malhotra, Ph.D., SME-RM and Sue Bird, P.Eng, are the QPs for the mineral resource update report.

On March 28, 2024, the Company raised $CAD 4.1 million from issuance of flow through shares. The Company used the proceeds for exploration activities at the Company's New Polaris project. The exploration activities consisted mainly of a drilling program targeting an increase in the mineral resource. The program concluded in August 2024 with the following highlights:

• 10.8 grams per tonne ("gpt") gold ("Au") over 4.3 m from 176.4 m down hole in Hole NP24-34

o Including 15.5 gpt Au over 2.0 m from 177.5 m

• 10.4 gpt Au over 3.6 m from 166.8 m down hole in Hole NP24-34

o Including 12.3 gpt Au over 1.3 m from 166.8 m

• 14.1 gpt Au over 1.1 m from 202.7 m down hole in Hole NP24-33A

• 10.4 gpt Au over 1.2 m from 252.3 m down hole in Hole NP24-33A

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

In September 2024, the British Columbia Environmental Assessment Office (BCEAO) has recommended that the New Polaris Project proceed to the Process Planning Phase of the environmental assessment. This recommendation follows a thorough review that evaluated the potential environmental and socio-economic impacts of the project.

In January 2025, BCEAO issued a process order, enabling the Project to proceed to the Application Development and Review phase of the Environmental Assessment. This marks a crucial step forward in the permitting process for the New Polaris Project.

During this phase, Canagold will prepare and submit its application for an Environmental Assessment Certificate while continuing its robust engagement efforts with Indigenous Nations, regulatory bodies, and other stakeholders. Prior to issuing the process order, BCEAO conducted a thorough review process that included feedback from participating Indigenous Nations, the Technical Advisory Committee (TAC), Alaskan Tribes, and the public, facilitated through a public comment period.

In February 2025, Canagold updated the mineral resource to quantify the antimony metal contained within the gold resource:

In 2025, further analysis of the antimony resource and expansion potential will take place, accompanied by additional metallurgical testing, aimed at establishing the best processing methods for producing a commercially viable antimony product.

Sue Bird, M Sc., P.Eng. V.P. of Resources and Engineering at Moose Mountain Technical Services, an independent Qualified Person as defined by NI 43-101, has reviewed and approved the technical information about the 2023 mineral resource update and 2025 antimony resource published by the Company (see News Release dated February 21, 2025 and titled "Canagold Announces Antimony Mineral Resource Estimate for New Polaris Gold Project")

In March 2025, Canagold closed a charity flow-through financing for the New Polaris project. The Company issued 9,200,000 common shares of the Company for total gross proceeds of CAD $3,220,000.

In August 2025, the Company closed a private placement for 4,651,163 flow through common shares at a price of CAD$0.43 per share for gross proceeds of CAD$2 million.

On February 13, 2026, Canagold closed an offering for total proceeds of CAD5,000,000 consisting of 10,000,000 common shares that qualify as flow-through shares for the purposes at a price of CAD$0.50 per share.

On February 25, 2026, announced plans for a comprehensive 2026 work program at New Polaris, focused on expanding gold-antimony resources and advancing technical studies to evaluate the financial benefits of incorporating antimony production into the project development plans and economics. The fully funded program, will include approximately 7,000 metres of diamond drilling, scheduled to commence in June and continue through July 2026. The drilling will target expansion of the high-grade gold-antimony mineralization within and adjacent to the current mine plan outlined in the feasibility study completed in July 2025. The objective is to further define and potentially increase the gold-antimony resource base in areas expected to have a direct and positive impact on early production and overall project economics.

On March 16, 2026, Canagold announced that its 100%-owned New Polaris has been added to the Canadian government advanced gold-antimony projects map.

Further details of the 2021, 2022 and 2024 drilling programs are provided in the Company's news releases:

• News release dated July 6, 2021 and titled, "Canagold Announces Initial 2021 Drill Results From New Polaris Project Including 24.2 gpt Gold over 6.6 m and 15.8 gpt Gold Over 13.0 m";

• News release dated July 19, 2021 and titled, "Canagold Announces Additional Results From New Polaris Drill Program Including 14.3 gpt Au Over 2.7 m and 15.3 gpt Au Over 1.7 m";

• News release dated July 27, 2021 and titled, "Canagold Drills 30.8 gpt Gold Over 3.9 Meters at New Polaris Project";

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

• News release dated September 22, 2021 and titled, "Canagold Intersects 17.1 gpt Au Over 8.4 m in Hanging-Wall C10 Vein and 25.7 gpt Au Over 2.1 m in C West Main Vein at New Polaris, BC";

• News release dated November 10, 2021 and titled, "Canagold Intersects 11.1 gpt Au over 17.8 m and 11 gpt over 8.9 m in 2 Separate Hanging-Wall Veins Adjacent to C West Main Vein at New Polaris Gold Project, BC";

• News release dated November 10, 2021 and titled, "Canagold Intersects 11.1 gpt Au over 17.8 m and 11 gpt over 8.9 m in 2 Separate Hanging-Wall Veins Adjacent to C West Main Vein at New Polaris Gold Project, BC";

• News release dated November 30, 2021 and titled, "Summary of High-Grade Drill Intercepts in the C-9 and C- 10 Veins at the New Polaris Project in BC";

• News release dated January 26, 2022 and titled, "Canagold Announces High-Grade Drill Intercepts Containing Visible Gold from the C-West Main Zone at New Polaris Project, B";

• News release dated February 24, 2022 and titled, "Canagold Continues to Intersect High-Grade Gold Mineralization in C-West Main Vein at New Polaris Project, BC";

• News release dated March 2, 2022 and titled, "Canagold Drilling Intersects Deep Extension of C-West Main Vein, and Discovers New High-Grade Parallel C-Vein at New Polaris Project, BC";

• News release dated March 21, 2022 and titled, "Canagold Announces Additional High-Grade Gold Drill Intercepts from the C-10 and the C-West Main Veins at New Polaris Project, BC";

• News release dated April 21, 2022 and titled, "Canagold Continues to Intersect High-Grade Gold Mineralization in C-West Main Vein Including 42.5 gpt Au over 2 m at New Polaris Project, BC".

• News release dated June 14, 2022 and titled, "Canagold Drilling Intersects New Vein Grading 7.54 gpt Gold over 18.6 m Length at New Polaris Project, BC, Additional High-Grade Mineralization Outlined in C-West Main Vein";

• News release dated June 28, 2022 and titled, "Canagold Drilling Reports Two Highest Grade Drill Results of 54 Hole Program Including 13.6 gpt Gold over 25.1 m Length and 34.4 gpt over 6.6 m Length at New Polaris Project, BC";

• News release dated July 12, 2022 and titled, "Canagold Summarizes Results of 30,000 m Infill Drill Program at New Polaris Project, BC, Highlights Include 13.6 gpt Over 25.1 m";

• News release dated August 18, 2022 and titled, "Canagold Mobilizes Drill Crews and Restarts Resource Expansion Drilling at the New Polaris Project";

• News release dated October 11, 2022 and titled, "Canagold Retains Ausenco Engineering to Complete Feasibility Study on New Polaris Project";

• News release dated October 27, 2022 and titled, "Canagold Drills 22.1 Grams per Tonne Gold over 4.3 Metres in Y-Vein System at New Polaris";

• News release dated January 25, 2023 and titled, "Canagold Announces Agreement with Taku River Tlingit First Nation for Flagship New Polaris Project";

• News release dated February 6, 2023 and titled, "Canagold Confirms Near Surface High-Grade Gold, Including 53.8 gpt Au over 2.78 m and 18.0 gpt Au over 5.64 m in Y-Vein System at New Polaris"; and

• News release dated May 16, 2023 and titled, "Canagold Increases Indicated Gold Resource by 89% in Updated Mineral Resource Estimate for New Polaris Gold Project, BC".

• News release dated June 5, 2024 and titled, "Canagold Initiates Resource Expansion Drilling at New Polaris Project"

• News release dated July 18, 2024 and titled, "Canagold Intercepts Strong Mineralization in First Five Resource Expansion Drill Holes at New Polaris"

• News release dated August 29, 2024 and titled, "Canagold Continues to Intercept Strong Mineralization in Resource Expansion Drilling Program at New Polaris"

• News release dated September 18, 2024 and titled, "Canagold Completes Resource Expansion Drilling Program at New Polaris with Additional Strong Mineralization Intercepts"

Details of the expenditures amounts incurred by the Company to advance New Polaris are included in section 1.4 of this MD&A.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.2.2 American Innovative Minerals, LLC

1.2.2. Purchase Agreement with American Innovative Minerals, LLC

In 2017, the Company closed a Membership Interest Purchase Agreement (the "Membership Agreement") with American Innovative Minerals, LLC ("AIM") and securityholders of AIM ("the AIM Securityholders") to acquire either a direct or indirect 100% legal and beneficial interests in mineral resource properties located in Nevada, Idaho and Utah (USA) for a purchase price of $2 million in cash and honouring pre-existing NSRs.

AIM owns 8 gold properties in Nevada and one gold property in Idaho. Until December 29, 2023, the Company owned two additional gold properties in Nevada (Fondaway Canyon and Dixie Comstock). Pursuant to an agreement from January 2020, on December 29, 2023, Getchell Gold Corp ("Getchell") exercised its option to acquire the Fondaway Canyon and Dixie Comstock properties by making the final payment of $1.6 million in cash stipulated under the January 2020 agreement and issuing 10,167,000 Getchell Shares to the Company.

AIM's properties include:

1.2.2.a Silver King (Nevada, USA)

Silver King property is located in Humboldt County, Nevada on 4 patented claims in the Iron Point mining district near Golconda Summit. Previous exploration focused on low grade gold values but the property has never been explored for silver.

On October 25, 2018, the Company entered into an option agreement with Brownstone Ventures (US) Inc., a subsidiary of Casino Gold Corp., ("Brownstone Ventures") on the Company's wholly owned Silver King patented claim group located in Humboldt County, Nevada. Under the terms of the ten-year agreement, the Company will receive annual payments of $12,000 plus an option exercise payment of $120,000. Upon exercise of the option, the Company will retain a 2% NSR royalty on the property of which Brownstone Ventures will have the right to buy back one-half (1%) of the royalty for $1 million.

1.2.2.b Lightning Tree (Idaho, USA)

Lightning Tree property is located in Lemhi County, Idaho, on 4 unpatented claims near the Musgrove gold deposit.

On September 10, 2020, the Company entered into an option agreement in the form of a definitive mineral property purchase agreement for its Lightning Tree property located in Lemhi County, Idaho, with Ophir Gold Corp. ("Ophir"), whereby Ophir shall acquire a 100% undivided interest in the property. In order to acquire the property, over a three year period, Ophir shall pay to the Company a total of CAD$137,500 in cash over a three year period and issue 2.5 million common shares and 2.5 million warrants over a two year period, and shall incur aggregate exploration expenditures of at least $4 million over a three year period. In Q3 2023, the Company and Ophir mutually terminated the option agreement, and the Lightning Tree property has been returned to the Company.

1.2.2.c Corral Canyon property (Nevada, USA)

Corral Canyon property lies 35 km west of the town of McDermitt in Humboldt County along the western flank of the McDermitt caldera complex, an area of volcanic rocks that hosts significant lithium and uranium mineralization in addition to gold. It contains volcanic-hosted, epithermal, disseminated and vein gold mineralization evidenced by previous drilling.

In 2018, the Company staked 92 mining claims covering 742 hectares in Nevada, USA.

In November 2019, a five hole, 1600 meter drilling program was completed. Further details of the drilling program for the Corral Canyon project are provided in the Company's news release dated November 28, 2019 and titled, "Canarc Completes Phase 1 Drill Program at Corral Canyon, Nevada".

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.2.3 Windfall Hills property (British Columbia, Canada)

The Windfall Hills gold project is located 65 km south of Burns Lake, readily accessible by gravel logging roads and a lake ferry crossing in the summer-time, or by charter aircraft year-round. The project consists of the Atna properties, comprised of 2 mineral claims totalling 959 hectares and the Dunn properties, comprised of 8 mineral claims totalling 2820 hectares.

In April 2013, the Company acquired 100% undivided interests in the two adjacent gold properties (Uduk Lake and Dunn properties) located in British Columbia. The Uduk Lake properties are subject to a 1.5% NSR production royalty that can be purchased for CAD$1 million and another 3% NSR production royalty. The Dunn properties are subject to a 2% NSR royalty which can be reduced to 1% NSR royalty for $500,000.

In the third quarter of 2020, the Company completed a Phase 2 diamond drill program. Six drill holes were completed for a total of 1,500 meters of core over an area of 30 hectares designed to follow up from gold-silver mineralization intersected in the 2014 Phase 1 drill holes. Further analysis of the structural and lithological controls on mineralization are needed to determine the next steps for the Windfall Hills property. The Company may seek a partner to advance the project.

Further details of the drilling program for the Windfall Hills project are provided in the Company's news release dated October 21, 2020 and titled, "Canarc Announces Results of its Special General Meeting of Shareholders Approving Upsized Financing Totaling CAD$8.4 Million".

1.2.4 Eskay Creek property (British Columbia, Canada)

In December 2017, the Company signed an agreement with Barrick Gold Inc ("Barrick") and Skeena Resources Ltd. ("Skeena") involving the Company's 33.3% carried interest in certain mining claims adjacent to the past-producing Eskay Creek Gold mine located in northwest British Columbia, whereby the Company will retain its 33.33% carried interest. The Company and Barrick have respectively 33.33% and 66.67% interests in 6 claims and mining leases totaling 2323 hectares at Eskay Creek. Pursuant to an option agreement between Skeena and Barrick, Skeena had the right to earn Barrick's 66.67% interest in the property which right had been exercised in October 2020.

Garry Biles, PEng, President and Chief Operating Officer of the Company, was the qualified person, as defined by National Instrument 43-101, and had approved the technical information from the drilling programs for the New Polaris and Windfall Hills projects.

Other Matters

As of March 30, 2026, Sun Valley Investments AG ("Sun Valley") owns 48.25% of the outstanding shares of the Company.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.3 Selected Annual Information

| (in $000s except | Years ended December 31, | ||||||||

| per share amounts) | 2025 | 2024 | 2023 | ||||||

| Total revenues | $ | - | $ | - | $ | - | |||

| Net (loss) income: | |||||||||

| (i) Total | $ | (2,593 | ) | $ | (1,122 | ) | $ | (3,050 | ) |

| (ii) Basic and diluted per share | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.02 | ) |

| Total assets | $ | 38,423 | $ | 32,745 | $ | 33,226 | |||

| Total long-term liabilities | $ | 3,207 | $ | 1,775 | $ | 1,774 | |||

1.4 Results of Operations

Year ended December 31, 2025 compared with December 31, 2024

The Company has no sources of operating revenues. Operating losses were incurred for ongoing activities of the Company in acquiring and exploring its mineral property interests, advancing the New Polaris property, and pursuing mineral projects of merit. The Company incurred a net loss of $2.56 million for fiscal 2025, which is higher than the net loss of $1.12 million for fiscal 2024. Net losses were impacted by different functional expense items. The table below (in thousands of US dollars) provides a comparison of the results of operations for 2025 vs 2024:

| Years ended December 31, | ||||||

| 2025 | 2024 | |||||

| Expenses: | ||||||

| Amortization | $ | 76 | $ | 81 | ||

| Corporate development | 127 | 126 | ||||

| Employee and director remuneration | 451 | 475 | ||||

| General and administrative | 478 | 458 | ||||

| Share-based payments | 551 | 316 | ||||

| Operating loss | (1,683 | ) | (1,456 | ) | ||

| Interest and other income | 38 | 148 | ||||

| Foreign exchange (loss) gain | (19 | ) | 71 | |||

| Change in fair value of marketable securities | (97 | ) | (143 | ) | ||

| Mineral property option income | 12 | 12 | ||||

| Interest and finance charges | (9 | ) | (12 | ) | ||

| Net loss before income tax | (1,758 | ) | (1,380 | ) | ||

| Income tax recovery | 148 | 258 | ||||

| Deferred income tax expense | (983 | ) | - | |||

| Net loss for the year | (2,593 | ) | (1,122 | ) | ||

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Overall operating losses are consistent for 2025 and 2024, with the focus of the company, advancing the New Polaris project, being unchanged. Other than the share-based compensation, which is higher in 2025, mainly because of the revaluation of the outstanding deferred shared units to a higher share price of the company, the individual expenses listed as operating expenses are consistent year over year.

The non-operating expenses are mainly non-cash items.

Interest is income is higher in 2024 mainly because of interest received from the taxation government on a refund for a mineral tax credit claim.

Foreign exchange (loss) gains are a result of assets and liabilities held in foreign currency being revalued to end of accounting period exchange rates or higher/lower exchange rates on settlement or conversion dates.

The change in the fair value of marketable securities is attributable to changes in the quoted market prices of the investments up to their date of disposal or to period end if continued to be held.

The income tax recovery is the allocation of the premium in the flow through private placement on a pro rata basis of qualified exploration expenditures incurred during the period. In 2024, the Company incurred more flow through eligible exploration expenditures, and as such, the income tax recovery premium is higher in 2024.

The deferred tax expense of $983,000 is primarily due to the temporary difference in tax basis vs. accounting basis of the mineral property interest.

As at December 31, 2025, the Company has mineral property interests which are comprised of the following:

| Canada | |||

| British Columbia | |||

| New Polaris | |||

| (Note 7(a)(i)) | |||

| Acquisition Costs: | |||

| Balance, December 31, 2024 | |||

| Acquisition | $ | 3,921 | |

| Foreign currency translation adjustment | 12 | ||

| Balance, December 31, 2025 | 10 | ||

| 3,943 | |||

| Deferred Exploration Expenditures: | |||

| Balance, December 31, 2024 | 27,379 | ||

| Additions: | |||

| Exploration: | |||

| Assays and sampling | 5 | ||

| Community engagement and social | 716 | ||

| Drilling | 48 | ||

| Environmental | 2,639 | ||

| Feasibility | 531 | ||

| General, administrative, sundry | 6 | ||

| Metallurgy | 28 | ||

| Rental and storage | 31 | ||

| Royalties | 7 | ||

| Salaries | 350 | ||

| Transportation | 25 | ||

| Foreign currency translation adjustment | 1,574 | ||

| Balance December 31, 2025 | 33,339 | ||

| Mineral property interest: | |||

| Balance, December 31, 2025 | $ | 37,282 |

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Details of the exploration programs are provided in section 1.2.1 of this MD&A. In 2025, the Company incurred $4.4 million in costs on advancing New Polaris, with most of the spending being attributable to environmental studies ($2.56 million), needed to obtain the environmental permit, and $716,000 of first nations community engagement. The note references in the table above pertain to the 2025 Audited Consolidated Financial Statements of the Company.

Cash flow for the year ended December 31, 2025

During 2025, the Company had an overall increase in cash of $144,000 (2024 - decrease of $2.1 million). Operating activities consumed cash of $815,000 (2024 - $364,000). Financing activities generated $4.9 million in 2025 (2024 - $2.9 million), while investing activities consumed a net of $4.2 million in 2025 (2024 - $4.6 million)

The Company generates cash from financing activities from issuance of shares and consumes the cash mainly for investing activities (advancing the New Polaris project), the secondary use of cash being administrative activities.

1.5 Summary of Quarterly Results and fourth quarter of 2025

The following table provides selected financial information of the Company for each of the last eight quarters ended at the most recently completed quarter, December 31, 2025. All dollar amounts are expressed in thousands of U.S. dollars..

| (in $000s except | 2025 | 2025 | 2025 | 2025 | 2024 | 2024 | 2024 | 2024 | ||||||||||||||||

| per share amounts) | 31-Dec | 30-Sep | 30-Jun | 31-Mar | Dec 31 | 30-Sep | June 30 | Mar 31 | ||||||||||||||||

| Total revenues | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

| Net (loss) income: | ||||||||||||||||||||||||

| (i) Total | $ | (1,164 | ) | $ | (575 | ) | $ | (436 | ) | $ | (418 | ) | $ | (86 | ) | $ | (328 | ) | $ | (644 | ) | $ | (64 | ) |

| (ii) Basic and diluted per share | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

| Total assets | $ | 38,423 | $ | 38,002 | $ | 36,499 | $ | 34,689 | $ | 32,745 | $ | 34,758 | $ | 35,034 | $ | 35,308 | ||||||||

| Total long-term liabilities | $ | 3,207 | $ | 2,240 | $ | 2,008 | $ | 1,855 | $ | 1,775 | $ | 1,838 | $ | 1,743 | $ | 1,751 | ||||||||

| Dividends per share | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

The Company's main focus for the past years, including the last eight quarters, was advancing the New Polaris project. The Company's accounting policy is to capitalize project related expenses. As such, the net loss of the Company does not include expenditures directly attributable to advancing New Polaris. In general, the overhead expenses of the Company are consistent, with variances across quarters being generally attributable to non-cash items, such as changes in fair market values of the Company's investments, write-off of book values of mineral properties for which there is no planned activities, deferred income tax expense, and share based compensation expense recognized in connection with the stock options and share units issued under the compensation plan. The fourth quarter of 2025 is consistent with other quarters in terms of operating expenses, with the higher accounting loss being attributable to the recognition of a deferred tax expense due to temporary differences between the tax basis and book value of the mineral property interests.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.6 Liquidity

The Company has no operating revenues, has incurred a significant net loss of $2.56 million for the year ended December 31, 2025, and has a deficit of $59.2 million as at December 31, 2025. In addition, the Company has negative cash flows from operations. The Company's ability to continue as a going concern is dependent on the ability of the Company to raise debt or equity financings, and the attainment of profitable operations. Management continues to find opportunities to raise the necessary capital to meet its planned business objectives and continues to seek financing opportunities. There can be no assurance that management's plans will be successful. These matters indicate the existence of material uncertainties that cast substantial doubt about the Company's ability to continue as a going concern. The Company's financial statements do not include any adjustments to the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern, and such adjustments could be material.

The recoverability of amounts capitalized for mineral property interests is entirely dependent upon the existence of reserves, the ability of the Company to obtain the necessary financing to complete the development and upon future profitable production. The Company knows of no trends, demands, commitments, events or uncertainties that may result in the Company's liquidity either materially increasing or decreasing at the present time or in the foreseeable future except as disclosed in this MD&A and in its regulatory filings. Material increases or decreases in the Company's liquidity are substantially determined by the success or failure of the Company's exploration and development programs and overall market conditions for smaller mineral exploration companies. In the past, the Company has endeavored to secure mineral property interests that in due course could be brought into production to provide the Company with cash flow which would be used to undertake work programs on other projects. To that end, the Company has expended its funds on mineral property interests that it believes have the potential to achieve cash flow within a reasonable time frame. As a result, the Company has incurred losses during each of its fiscal years since incorporation. This result is typical of smaller exploration companies and will continue unless positive cash flow is achieved.

The following table contains selected financial information of the Company's liquidity:

| December 31, | December 31, | |||||

| ($000s) | 2025 | 2024 | ||||

| Cash | $ | 820 | $ | 676 | ||

| Working capital | (232 | ) | 151 | |||

Ongoing operating expenses continue to reduce the Company's cash resources and working capital, as the Company has no sources of operating revenues.

During 2025, the Company generated $111,000 from disposition of marketable securities (2024 - $1.1 million).

On March 28, 2024, the Company closed a financing for 15,700,000 flow through common shares at a price of CAD$0.2625 per share for gross proceeds of CAD$4.1 million.

On March 4, 2025, the Company closed a private placement issuing 9,200,000 flow through common shares at a price of CAD$0.35 per share for gross proceeds of CAD$3.2 million

On August 18, 2025, the Company closed a private placement for 4,651,163 flow through common shares at a price of CAD$0.43 per share for gross proceeds of CAD$2 million. The fair value of the shares on August 18, 2025 was CAD$0.39 per share, resulting in the recognition of a flow through premium liability of CAD$0.04 per share for a total of CAD$186,047.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

On August 18, 2025, the Company closed a financing consisting of 5,128,205 shares at CAD $0.39 per share for aggregate gross proceeds of CAD $2 million.

On February 13, 2026 Canagold closed an offering for total proceeds of CAD$9,228,456.50 consisting of:

(i) 9,396,570 common shares iat a price of CAD$0.45 per Common Share, and

(ii) 10,000,000 common shares that qualify as flow-through shares for the purposes at a price of CAD$0.50 per share.

The Company will continue to rely upon equity financing as its principal source of financing its projects.

1.7 Capital Resources

See 1.2 above for commitments on mineral property interests.

Certain amounts may be reduced in the future as the Company determines which properties to continue to explore and which to abandon.

In January 2022, the Company entered into an office lease arrangement for a term of five years with a commencement date of September 1, 2022. The basic rent per year is CAD$84,700 for years 1 to 2, CAD$87,300 for years 3 to 4, and CAD$89,900 for year 5.

As at December 31, 2025, the Company is committed to the following payments for base rent at its corporate head office in Vancouver, BC, as follows:

| Amount | |||

| (CAD$000) | |||

| Year: | |||

| 2026 | $ | 88 | |

| 2027 | $ | 60 | |

| $ | 148 |

1.8 Off-Balance Sheet Arrangements

There are no off-balance sheet arrangements.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.9 Transactions with Related Parties

Key management includes directors (executive and non-executive) and senior management. The compensation paid or payable to key management is disclosed in the table below.

Except as disclosed elsewhere in the consolidated financial statements, the Company had the following general and administrative costs with related parties during the years ended December 31, 2025, 2024, and 2023:

| Net balance receivable (payable) | |||||||||||||||

| Years ended December 31, | as at December 31, | ||||||||||||||

| 2025 | 2024 | 2023 | 2025 | 2024 | |||||||||||

| Key management compensation: | |||||||||||||||

| Executive salaries and remuneration (1) | $ | 785 | $ | 833 | $ | 803 | $ | (11 | ) | $ | (13 | ) | |||

| Severance | - | - | 73 | - | - | ||||||||||

| Directors fees | 83 | 85 | 86 | (42 | ) | (27 | ) | ||||||||

| Share-based payments | 598 | 316 | 391 | - | - | ||||||||||

| $ | 1,466 | $ | 1,234 | $ | 1,353 | $ | (53 | ) | $ | (40 | ) | ||||

(1) Includes key management compensation which is included in employee and director remuneration, mineral property interests, and corporate development.

As of December 31, 2025, Sun Valley owned 48% common shares of the Company. During the year ended December 31, 2025, the Company received from and provided to Sun Valley corporate and technical related services. The Company incurred CAD$35,000 (2024 - CAD$155,000) in expenses and charged CAD$75,000 (2024 - CAD$56,000) to Sun Valley for services and reimbursements. The 2024 and 2025 amounts are outstanding at year end December 31, 2025, for a net amount of CAD$59,000 due to Sun Valley.

In March 2024, Sun Valley participated in the financing offering of the Company and acquired 15,700,000 shares of the Company. In 2025, Sun Valley participated in the March 2025 financing, acquiring 4,600,000 shares of the Company and in the August 2025 financings acquiring 4,889,684 shares of the Company. In 2026, Sun Valley participated in the February 2026 private placements and acquired a total of 9,698,285 shares.

1.10 Proposed Transactions

There are no proposed material asset or business acquisitions or dispositions, other than those in the ordinary course of business and other than those already disclosed in this MD&A, before the board of directors for consideration, and other than those already disclosed in its regulatory and public filings.

1.11 Critical Accounting Estimates and Judgements

The preparation of financial statements in accordance with IFRS Accounting Standards requires management to make estimates, assumptions and judgements that affect the application of accounting policies and the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements along with the reported amounts of revenues and expenses during the period. Actual results may differ from these estimates and, as such, estimates and judgements and underlying assumptions are reviewed on an ongoing basis. Revisions are recognized in the period in which the estimates are revised and in any future periods affected.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

Significant areas requiring the use of management estimates relate to determining the recoverability of mineral property interests and receivables; valuation of certain marketable securities; accrued site remediation; amount of flow-through obligations; recognition of deferred income tax liability; the variables used in the determination of the fair value of stock options granted and finder's fees warrants issued or modified; and the recoverability of deferred tax assets. While management believes the estimates are reasonable, actual results could differ from those estimates and could impact future results of operations and cash flows.

The Company applies judgment in assessing the functional currency of each entity consolidated in the financial statements.

For right of use assets and lease liability, the Company applies judgement in determining whether the contract contains an identified asset, whether they have the right to control the asset, and the lease term. The lease term is based on considering facts and circumstances, both qualitative and quantitative, that can create an economic incentive to exercise renewal options. Management considers all facts and circumstances that create an economic incentive to exercise an extension option, or not to exercise a termination option.

The Company applies judgment in assessing whether material uncertainties exist that would cast substantial doubt as to whether the Company could continue as a going concern.

Acquisition costs of mineral properties and exploration and development expenditures incurred thereto are capitalized and deferred. The costs related to a property from which there is production will be amortized using the unit-of-production method. Capitalized costs are written down to their estimated recoverable amount if the property is subsequently determined to be uneconomic. The amounts shown for mineral property interests represent costs incurred to date, less recoveries and write-downs, and do not reflect present or future values.

At the end of each reporting period, the Company assesses each of its mineral properties to determine whether any indication of impairment exists. Judgment is required in determining whether indicators of impairment exist, including factors such as: the period for which the Company has the right to explore; expected renewals of exploration rights; whether substantive expenditures on further exploration and evaluation of resource properties are budgeted or planned; and results of exploration and evaluation activities on the exploration and evaluation assets. If such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment, if any. The recoverable amount is the higher of fair value less costs to sell and value in use. Fair value is determined as the amount that would be obtained from the sale of the asset in an arm's length transaction between knowledgeable and willing parties. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. If the recoverable amount of an asset is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount and the impairment loss is recognized in profit or loss for the period.

Where an impairment loss subsequently reverses, the carrying amount of the asset (or cash-generating unit) is increased to the revised estimate of its recoverable amount, but to an amount that does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the asset (or cash-generating unit) in prior periods. A reversal of an impairment loss is recognized immediately in profit or loss.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.12 Changes in Accounting Policies including Initial Adoption

New Accounting Pronouncements

The Company did not early adopt any recent pronouncements disclosed in Note 3, of the audited consolidated financial statements for the year ended December 31, 2025.

1.13 Financial Instruments and Other Instruments

IFRS 9 Financial Instruments:

The Company has classified its financial instruments under IFRS 9 Financial Instruments ("IFRS 9") as follows:

| IFRS 9 | |

| Financial Assets | |

| Cash | Amortized Cost |

| Marketable securities | FVTPL |

| Receivables | Amortized cost |

| Financial Liability | |

| Accounts payable and accrued liabilities | Amortized cost |

| Lease liability | Amortized cost |

Management of Financial Risk

The Company is exposed in varying degrees to a variety of financial instrument related risks, including credit risk, liquidity risk, and market risk which includes foreign currency risk, interest rate risk and other price risk. The types of risk exposure and the way in which such exposure is managed are provided as follows.

The fair value hierarchy categorizes financial instruments measured at fair value at one of three levels according to the reliability of the inputs used to estimate fair values. The fair values of assets and liabilities included in Level 1 are determined by reference to quoted prices in active markets for identical assets and liabilities. Assets and liabilities in Level 2 are valued using inputs other than quoted prices for which all significant inputs are based on observable market data. Level 3 valuations are based on inputs that are not based on observable market data.

The fair values of the Company's receivables, accounts payable and accrued liabilities, approximate their carrying values due to the short terms to maturity. Cash and certain marketable securities are measured at fair values using Level 1 inputs. Certain other marketable securities are measured using Level 3 of the fair value hierarchy. The fair value of deferred royalty and lease liabilities approximate their carrying values as they are at estimated market interest rates using Level 2 inputs.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

(a) Credit risk:

Credit risk is the risk of potential loss to the Company if the counterparty to a financial instrument fails to meet its contractual obligations.

The Company's credit risk is primarily attributable to its liquid financial assets including cash. The Company limits exposure to credit risk on liquid financial assets through maintaining its cash with high-credit quality Canadian financial institutions.

To reduce credit risk, the Company regularly reviews the collectability of its amounts receivable, which may include amounts receivable from certain related parties, and records an expected credit loss based on its best estimate of potentially uncollectible amounts. Management believes that the credit risk with respect to these financial instruments is remote.

The financial instruments that potentially subject the Company to credit risk comprise investments, cash and cash equivalents and certain amounts receivable, the carrying value of which represents the Company's maximum exposure to credit risk.

(b) Liquidity risk:

Liquidity risk is the risk that the Company will not be able to meet its financial obligations as they become due.

The Company ensures that there is sufficient capital in order to meet short-term business requirements, after taking into account the Company's holdings of cash and its ability to raise equity financings. As at December 31, 2025, the Company had a working capital deficit (current assets less current liabilities) of $232,000 (December 31, 2024 - working capital surplus of $151,000. In February 2026, the Company raised CAD$9.2 million and has sufficient funding to meet its short-term liabilities, flow-through obligations and administrative overhead costs, and to maintain its mineral property interests in 2026.

(c) Market risk:

The significant market risk exposures to which the Company is exposed are foreign currency risk, interest rate risk and other price risk.

(i) Foreign currency risk:

Certain of the Company's mineral property interests and operations are in Canada. Most of its operating expenses are incurred in Canadian dollars. Fluctuations in the Canadian dollar would affect the Company's consolidated statements comprehensive income (loss) as its functional currency is the Canadian dollar, and fluctuations in the U.S. dollar would impact its cumulative translation adjustment as consolidated financial statements are presented in U.S. dollars.

The Company is exposed to currency risk for its U.S. dollar equivalent of assets and liabilities denominated in currencies other than U.S. dollars as follows:

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

| December 31, | ||||||

| 2025 | 2024 | |||||

| Cash | $ | 797 | $ | 589 | ||

| Marketable securities | 16 | 218 | ||||

| Receivables and prepaids | 173 | 247 | ||||

| Accounts payable and accrued liabilities | (1,129 | ) | (828 | ) | ||

| Lease liability | (102 | ) | (150 | ) | ||

| Deferred compensation liability | (856 | ) | (422 | ) | ||

| Net financial assets (liabilities) | $ | (1,101 | ) | $ | (346 | ) |

Based upon the above net exposure as at December 31, 2025 and assuming all other variables remain constant, a 10% (2024 - 10%) depreciation or appreciation of the U.S. dollar relative to the Canadian dollar could result in a decrease (increase) of approximately $110,000 (2024 - $35,000) in the cumulative translation adjustment in the Company's shareholders' equity.

The Company has not entered into any agreements or purchased any instruments to hedge possible currency risks at this time.

(ii) Interest rate risk:

In respect of financial assets, the Company's policy is to invest cash at floating rates of interest in cash equivalents, in order to maintain liquidity, while achieving a satisfactory return. Fluctuations in interest rates impact on the value of cash equivalents. Interest rate risk is not significant to the Company as it has no interest bearing debt.

(iii) Other price risk:

Other price risk is the risk that the value of a financial instrument will fluctuate as a result of changes in market prices.

The Company's other price risk includes equity price risk, whereby investments in marketable securities are held for trading financial assets with fluctuations in quoted market prices recorded at FVTPL. There is no separately quoted market value for the Company's investments in the shares of certain investments.

As certain of the Company's marketable securities are carried at market value and are directly affected by fluctuations in value of the underlying securities, the Company considers its financial performance and cash flows could be materially affected by such changes in the future value of the Company's marketable securities. Based upon the net exposure as at December 31, 2025 and assuming all other variables remain constant, a net increase or decrease of 10% in the market prices of the underlying securities would increase or decrease respectively net (loss) income by $1,600 (2024 - $22,000).

1.14. Other MD&A Requirements

1.14.1 Additional information

Additional information relating to the Company are as follows:

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

(a) may be found on SEDAR+ at www.sedarplus.ca;

(b) may be found in the Company's annual information form; and

(c) is also provided in the Company's audited consolidated financial statements for the year ended December 31, 2025, 2024 and 2023.

1.14.2 Outstanding Share Data

The following table presents an updated share data as of March 31, 2026.

| Common Shares: | ||||

| Common shares outstanding at December 31, 2025 | 193,965,699 | |||

| Conversion of RSU to shares in January 2026 | 587,497 | |||

| Private placements in February 2026 | 19,396,570 | |||

| Common shares outstanding at March 31, 2026 | 213,949,766 | |||

| Stock Options | ||||

| Stock options outstanding at December 31, 2025 and March 31, 2026 | 800,000 | |||

| Warrants: | ||||

| Warrants outstanding at December 31, 2025 and March 31, 2026 | - | |||

| Deferred share units (DSUs): | ||||

| DSUs outstanding at December 31, 2025 and March 31, 2026 | 2,607,937 | |||

| Restricted share units (RSUs): | ||||

| RSUs outstanding at December 31, 2025 | 587,497 | |||

| Conversion of RSU to shares in January 2026 | (587,497 | ) | ||

| RSUs issued in March 2026 | 462,128 | |||

| RSUs outstanding at March 31, 2026 | 462,128 | |||

1.15 Outlook

The Company expects to continue to depend upon equity financings to continue exploration work on and to advance its mineral property interests, and to meet its administrative overhead costs for the 2026 fiscal year and beyond. There are no assurances that capital requirements will be met by this means of financing as inherent risks are attached therein including commodity prices, financial market conditions, and general economic factors. The Company does not expect to realize any operating revenues from its properties in the foreseeable future.

| CANAGOLD RESOURCES LTD. Management’s Discussion and Analysis For the year ended December 31, 2025 (expressed in United States dollars) |

1.16 Risk Factors

Mineral exploration, development and operation involves a number of risks and uncertainties, many of which are beyond the Company's control. These risks and uncertainties include, without limitation, the risks discussed elsewhere in this MD&A and those identified in the Company's Annual Information Form dated March 31, 2026 for the year ended December 31, 2025 and which was filed on SEDAR + on March 31, 2026, and the Company's other disclosure documents as filed in Canada on SEDAR + at www.sedarplus.ca.

1.17 Internal Controls over Financial Reporting

The Company's management, under the supervision of the Chief Executive Officer and the Chief Financial Officer, is responsible for establishing and maintaining adequate internal control over financial reporting ("ICOFR"). Except as noted below, our ICOFR is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS Accounting Standards. Management of the Company recognizes that any controls and procedures, no matter how well conceived and operated, have inherent limitations. As a result, even those systems designed to be effective can only provide reasonable assurance, and not absolute assurance, of achieving the desired control objectives, and management necessarily was required to apply its judgement in evaluating the cost-benefit relationship of possible controls and procedures.

In common with many other smaller companies, the Company has insufficient resources to appropriately review increasingly complex areas of accounting such as those in relation to deferred income tax and share based compensation expenses. To remedy this deficiency in its ICOFR, the Company shall engage the services of an external accounting firm to assist in applying complex areas of accounting as and when needed.

Management performed an assessment of the Company's ICOFR as at December 31, 2025. Based upon the results of that assessment as at December 31, 2025, management concluded that its internal control over financial reporting is effective.

Changes in Internal Controls over Financial Reporting

Except as disclosed above, there have been no changes in our internal control over financial reporting during the year ended December 31, 2025 that have materially affected, or are reasonably likely to materially affect, our ICOFR.