ANNUAL INFORMATION FORM

of

ERO COPPER CORP.

Suite 1050 – 625 Howe Street

Vancouver, British Columbia

V6C 2T6

Telephone: (604) 449-9244

Facsimile: (604) 398-3767

Website: www.ero.com

E-mail: info@ero.com

For the Year Ended December 31, 2025

Dated: March 30, 2026

TABLE OF CONTENTS

PRELIMINARY NOTES

Date of Information

In this Annual Information Form (“AIF”), Ero Copper Corp., together with its subsidiaries, as the context requires, is referred to as “Ero”, “Ero Copper” or the “Company”. All information contained herein is presented as at December 31, 2025, unless otherwise stated.

Currency

All dollar amounts in this AIF are expressed in Canadian dollars, except as otherwise indicated. References to “$” or “dollars” are to Canadian dollars, references to “US$” and “USD” are to US dollars and references to “R$” and “BRL” are to Brazilian Reais.

Cautionary Note Regarding Forward Looking Statements

This AIF and the documents incorporated by reference herein contain “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation (collectively, “forward-looking statements”). Forward-looking statements include statements that use forward-looking terminology such as “may”, “could”, “would”, “will”, “should”, “intend”, “target”, “plan”, “guidance”, “strategy”, “model”, “expect”, “budget”, “estimate”, “forecast”, “schedule”, “anticipate”, “believe”, “continue”, “potential”, “view”, “assume” or the negative or grammatical variation thereof or other variations thereof or comparable terminology. Forward-looking statements may include, but are not limited to, statements with respect to Mineral Reserve and Mineral Resource (as defined below) estimates; targeting additional Mineral Resources and expansion of deposits; capital and operating cost estimates and economic analyses (including cash flow projections), including those from the Caraíba Operations Technical Report (as defined below), the Xavantina Operations Technical Report (as defined below), the Tucumã Technical Report (as defined below) and the Furnas Project Technical Report (as defined below); the Company’s expectations, strategies and plans for the Caraíba Operations (as defined below), the Xavantina Operations (as defined below), the Tucumã Operation (as defined below) and the Furnas Project (as defined below), including the Company’s planned exploration, development, construction and production activities; the results of future exploration and drilling; estimated completion dates for certain milestones; successfully adding or upgrading Mineral Resources and successfully developing new deposits; the costs and timing of current and future exploration, development and construction including but not limited to the Deepening Extension Project (as defined below) at the Caraíba Operations; the estimated timing for certain milestones and the potential impacts of previously completed initiatives, including the ramp-up of throughput volumes at the Tucumã Operation; the timing and amount of future production at the Caraíba Operations, the Tucumã Operation and the Xavantina Operations; the timing, receipt and maintenance of necessary approvals, licenses and permits from applicable governments, regulators or third parties; expectations regarding consumption, demand and future price of copper, gold and other metals; the marketability of and the Company's ability to monetize the gold concentrate production from the Xavantina Operations, future financial or operating performance and condition of the Company and its business, operations and properties, including expectations regarding liquidity, capital structure, competitive position and payment of dividends; the possibility of entering judgments outside of Canada; expectations regarding future currency exchange rates; and any other statement that may predict, forecast, indicate or imply future plans, intentions, levels of activity, results, performance or achievements.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual results, actions, events, conditions, performance or achievements to materially differ from those expressed or implied by the forward-looking statements, including, without limitation, risks related to:

•copper and gold prices are volatile and may be lower than expected;

•mining operations are risky;

•mining operations require geologic, metallurgic, engineering, title, environmental, economic and financial assessments that may be materially incorrect and thus the Company may not produce as expected;

•geotechnical, hydrological and climatic events could suspend mining operations or increase costs;

•actual production, capital and operating costs may be different than those anticipated;

•the Company’s financial performance and results of operations are currently dependent on the Caraíba Operations, the Tucumã Operation, and the Xavantina Operations;

•infectious diseases may affect the Company’s business and operations;

•changes in climate conditions may affect the Company’s operations;

•currency fluctuations can result in unanticipated losses;

•the successful operation of the Caraíba Operations, the Xavantina Operations and the Tucumã Operation depends on the skills of the Company’s management and teams;

•operations during mining cycle peaks are higher cost;

•title to the Caraíba Operations, the Xavantina Operations, and/or the Tucumã Operation may be disputed;

•the Company may fail to comply with the law or may fail to obtain or renew necessary permits and licenses;

•the failure of a tailings dam could negatively impact the Company’s business, reputation and results of operations;

•compliance with environmental regulations can be costly;

•social and environmental activism can negatively impact exploration, development, construction and mining activities;

•the construction and start-up of new mines and projects at existing mines is subject to a number of factors and the Company may not be able to successfully complete new construction projects;

•land reclamation and mine closure requirements may be burdensome and costly;

•the mining industry is intensely competitive;

•inadequate infrastructure may constrain mining operations;

•operating cash flow may be insufficient for future needs;

•fluctuations in the market prices and availability of commodities and equipment affect the Company’s business;

•the Company is subject to restrictive covenants that limit its ability to operate its business;

•the Company’s indebtedness could adversely affect its financial condition and prevent the Company from fulfilling its obligations under debt instruments;

•the Company may not be able to generate sufficient cash to service all of its indebtedness and may be forced to take other actions to satisfy its obligations under such indebtedness, which may not be successful;

•counterparties may default on their contractual obligations to the Company;

•a failure to maintain satisfactory labour relations can adversely impact the Company;

•the Company’s insurance coverage may be inadequate to cover potential losses;

•it may be difficult to enforce judgments and effect service of process on directors, officers and experts named herein;

•the directors and officers may have conflicts of interest with the Company;

•future acquisitions may require significant expenditures and may result in inadequate returns;

•disclosure and internal control deficiencies may adversely affect the Company;

•failures of information systems or information security threats can be costly;

•the Company may be subject to costly legal proceedings;

•the Company may be subject to shareholder activism;

•product alternatives may reduce demand for the Company’s products;

•a lowering or withdrawal of the ratings assigned to the Company’s debt securities by rating agencies may increase the Company’s future borrowing costs and reduce its access to capital;

•the Company’s Brazilian operations are subject to political and other risks associated with operating in a foreign jurisdiction;

•the Company may be negatively impacted by changes to mining laws and regulations;

•a failure to maintain relationships with the communities in which the Company operates and other stakeholders may adversely affect the Company’s business;

•inaccuracies, corruption and fraud in Brazil relating to ownership of real property may adversely affect the Company’s business;

•the Company is exposed to the possibility that applicable taxing authorities could take actions that result in increased tax or other costs that might reduce the Company’s cash flow;

•inflation in Brazil, along with Brazilian governmental measures to combat inflation, may have a significant negative effect on the Brazilian economy and also on the Company's financial condition and results of operations;

•foreign exchange rate instability may have a material adverse effect on the Brazilian economy;

•the Company’s operations may be impaired as a result of restrictions to the acquisition or use of rural properties by foreign investors or Brazilian companies under foreign control;

•recent disruptions in international and domestic capital markets may lead to reduced liquidity and credit availability for the Company;

•the Company may be responsible for corruption and anti-bribery law violations;

•investors may lose their entire investment;

•dilution from equity financing could negatively impact holders of the common shares of the Company

(the “Common Shares”);

•equity securities are subject to trading and volatility risks;

•sales by existing shareholders can reduce share prices;

•the Company does not currently intend to pay dividends;

•public companies are subject to securities class action litigation risk;

•if securities or industry analysts do not publish research or publish inaccurate or unfavourable research about the Company’s business, the price and trading volume of the Common Shares could decline; and

•global financial conditions can reduce the price of the Common Shares.

This list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements. Although the Company has attempted to identify important factors that could cause actual results, actions, events, conditions, performance or achievements to differ materially from those contained in forward-looking statements, there may be other factors that cause results, actions, events, conditions, performance or achievements to differ from those anticipated, estimated or intended.

Forward-looking statements are not a guarantee of future performance. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements involve statements about the future and are inherently uncertain, and the Company’s actual results, achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in this AIF under the heading “Risk Factors”.

The Company’s forward-looking statements are based on the assumptions, beliefs, expectations and opinions of management on the date the statements are made, many of which may be difficult to predict and beyond the Company’s control. In connection with the forward-looking statements contained in this AIF, the Company has made certain assumptions about, among other things: favourable equity and debt capital markets; the ability to raise any necessary additional capital on reasonable terms to advance the production, development, construction and exploration of the Company’s properties and assets; future prices of copper, gold and other metal prices; the timing and results of exploration and drilling programs; the accuracy of any Mineral Reserve and Mineral Resource estimates; the geology of the Caraíba Operations, the Xavantina Operations and the Tucumã Operation being as described in the Caraíba Operations Technical Report, the Xavantina Operations Technical Report and the Tucumã Technical Report, respectively; production costs; the accuracy of budgeted exploration, development and construction costs and expenditures; the price of other commodities such as fuel; future currency exchange rates, interest rates, royalty rates and tariff rates; operating conditions being favourable such that the Company is able to operate in a safe, efficient and effective manner; work force continuing to remain healthy in the face of prevailing epidemics, pandemics or other health risks, political and regulatory stability; the receipt of governmental, regulatory and third party approvals, licenses and permits on favourable terms; obtaining required renewals for existing approvals, licenses and permits on favourable terms; requirements under applicable laws; sustained labour stability; stability in financial and capital goods markets; availability of equipment; positive relations with local groups and the Company’s ability to meet its obligations under its agreements with such groups; and satisfying the terms and conditions of the Company’s current loan arrangements. Although the Company believes that the assumptions inherent in forward-looking statements are reasonable as of the date of this AIF, these assumptions are subject to significant business, social, economic, political, regulatory, competitive and other risks and uncertainties, contingencies and other factors that could cause actual actions, events, conditions, results, performance or achievements to be materially different from those projected in the forward-looking statements. The Company cautions that the foregoing list of assumptions is not exhaustive. Other events or circumstances could cause actual results to differ materially from those estimated or projected and expressed in, or implied by, the forward-looking statements contained in this AIF.

Forward-looking statements contained herein are made as of the date of this AIF and the Company disclaims any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or results or otherwise, except as and to the extent required by applicable securities laws.

Scientific and Technical Information

Except as set out below, scientific and technical information contained in this AIF relating to the Company’s mining operations located within the Curaçá Valley, northeastern Bahia State, Brazil (the “Caraíba Operations” and formerly known as the MCSA Mining Complex), is derived from, and in some instances is a direct extract from, and based on the assumptions, qualifications and procedures set out in, the report prepared in accordance with National Instrument 43-101, Standards of Disclosure for Mineral Projects (“NI 43-101”) and entitled “2022 Mineral Resources and Mineral Reserves of the Caraíba Operations, Curaçá Valley, Bahia, Brazil”, dated December 22, 2022 with an effective date of September 30, 2022, prepared by Porfirio Cabaleiro Rodriguez, FAIG, Bernardo Horta de Cerqueira Viana, FAIG, Fábio Valério Câmara Xavier, MAIG and Ednie Rafael Moreira de Carvalho Fernandes, MAIG all of GE21 Consultoria Mineral Ltda. (“GE21”), Dr. Beck Nader, FAIG of BNA Mining Solutions (“BNA”) and Alejandro Sepulveda, Registered Member (#0293) (Chilean Mining Commission) of NCL Ingeniería y Construcción SpA (“NCL”) (the “Caraíba Operations Technical Report”). Each of Porfirio Cabaleiro Rodriguez, FAIG, Bernardo Horta de Cerqueira Viana, FAIG, Fábio Valério Câmara Xavier, MAIG, Ednie Rafael Moreira de Carvalho Fernandes, MAIG, Dr. Beck Nader, FAIG and Alejandro Sepulveda, Registered Member (#0293) (Chilean Mining Commission), reviewed and approved the scientific and technical information relating to the Caraíba Operations contained in this AIF, other than under the heading “Caraíba Operations – Updated Information with respect to the Caraíba Operations”, and is a “qualified person” (“QP” or “Qualified Person”) and “independent” of the Company within the meanings of NI 43-101. Information of a scientific and technical nature in respect of the Caraíba Operations set out in the AIF under the heading “Caraíba Operations – Updated Information with respect to the Caraíba Operations”, has been reviewed and approved by Cid Gonçalves Monteiro Filho, SME RM (04317974), MAIG (No. 8444), FAusIMM (No. 329148) and Resource Manager of the Company. Mr. Gonçalves is a “qualified person” within the meanings of NI 43-101.

Scientific and technical information contained in this AIF relating to the Company’s mining operations located approximately 18 km west of the town of Nova Xavantina, southeastern Mato Grosso State, Brazil (the “Xavantina Operations”), is derived from, and in some instances is a direct extract from, and based on the assumptions, qualifications and procedures set out in, the report prepared in accordance with NI 43-101 and entitled “Technical Report on the Xavantina Operations, Mato Grosso, Brazil”, dated December 19, 2025 with an effective date of June 30, 2025, prepared by Branca Horta de Almeida Abrantes, MAIG, Hugo Ribeiro de Andrade Filho, FAusIMM (CP), Leonardo de Moraes Soares, MAIG, Paulo Roberto Bergmann Moreira, FAusIMM and Porfirio Cabaleiro Rodriguez, FAIG, all of GE21 (the “Xavantina Operations Technical Report”). Each of Branca Horta de Almeida Abrantes, MAIG, Hugo Ribeiro de Andrade Filho, FAusIMM (CP), Leonardo de Moraes Soares, MAIG, Paulo Roberto Bergmann Moreira, FAusIMM and Porfirio Cabaleiro Rodriguez, FAIG, reviewed and approved the scientific and technical information relating to the Xavantina Operations contained in this AIF and is a "qualified person" and “independent” of the Company within the meanings of NI 43-101.

Except as set out below, scientific and technical information contained in this AIF relating to the Company’s mining operation, located within southeastern Pará State, Brazil (referred to herein as the “Tucumã Operation” or by its former name, the “Tucumã Project” or the “Boa Esperança Project”), is derived from, and in some instances is a direct extract from, and based on the assumptions, qualifications and procedures set out in, the report prepared in accordance with NI 43-101 and entitled “Boa Esperança Project NI 43-101 Technical Report on Feasibility Study Update”, dated November 12, 2021 with an effective date of August 31, 2021, prepared by Kevin Murray, P. Eng., Scott C. Elfen, P.E. (each of Ausenco Engineering Canada Inc.), Erin L. Patterson, P.E. (formerly employed by its affiliate Ausenco Engineering USA South Inc., and together with Ausenco Engineering Canada Inc., referred to as “Ausenco”), Carlos Guzmán, FAusIMM RM CMC of NCL and Emerson Ricardo Re, MSc, MBA, MAusIMM (CP) (No. 305892), Registered Member (No. 0138) (Chilean Mining Commission) and Resource Manager of the Company on the date of the report (now of HCM Consultoria Geologica Eireli (“HCM”)) (the “Tucumã Project Technical Report” or the “Tucumã Technical Report”). Each of Kevin Murray, P. Eng., Erin L. Patterson, P.E., Scott C. Elfen, P.E., Carlos Guzmán, FAusIMM RM CMC and Emerson Ricardo Re, MAusIMM (CP), reviewed and approved the scientific and technical information relating to the Tucumã Project contained in this AIF, and is a “qualified person” within the meaning of NI 43-101 or, in the case of Erin L. Patterson, P.E., who is no longer employed by Ausenco, was a "qualified person" within the

meaning of NI 43-101 on the date of the report. Each of Kevin Murray, P. Eng., Erin L. Patterson, P.E., Scott C. Elfen, P.E., and Carlos Guzmán, FAusIMM RM CMC is “independent” of the Company within the meaning of NI 43-101 or, in the case of Erin L. Patterson, P.E., was "independent" of the Company on the date of the report. Emerson Ricardo Re, MAusIMM (CP), being the Resource Manager of the Company on the date of the report (now of HCM), was not “independent” of the Company on the date of the report, within the meaning of NI 43-101. Information of a scientific and technical nature in respect of the Tucumã Operation set out in the AIF under the heading “Tucumã Operation – Updated Information with respect to the Tucumã Operation”, has been reviewed and approved by Cid Gonçalves Monteiro Filho, SME RM (04317974), MAIG (No. 8444), FAusIMM (No. 329148) and Resource Manager of the Company, Mr. Gonçalves is a “qualified person” within the meanings of NI 43-101.

Ero has the option to earn a 60% interest in the Furnas copper-gold project, located in the Carajás Mineral Province in Pará State, Brazil (the “Furnas Project”) approximately 50 kilometers southeast of Vale Base Metal's Salobo operations and approximately 190 kilometers northeast of the Tucumã Operation (see below under the headings “Three Year History” for additional information regarding the option). Scientific and technical information contained in this AIF relating to the Furnas Project, is derived from, and in some instances is a direct extract from, and based on the assumptions, qualifications and procedures set out in, the report prepared in accordance with NI 43-101 and entitled “Preliminary Economic Assessment for the Furnas Project, Pará State, Brazil”, dated March 30, 2026 with an effective date of February 23, 2026, prepared by João Estevão Jr., MAIG of SDPM Mining Consulting ("SDPM"), Enrique Alfonso Rubio Esquivel, Registered Member (No. 255) (Chilean Mining Commission), Luis Bernal Venegas, Registered Member (No. 415) (Chilean Mining Commission), and Ricardo Martín Miranda Díaz, Registered Member (No. 145) (Chilean Mining Commission), all of Redco Mining Consultants ("Redco"), and Cid Gonçalves Monteiro Filho, SME RM (04317974), MAIG (No. 8444), FAusIMM (No. 329148) Reserve and Resource Manager of the Company (the “Furnas Project Technical Report”). Each of João Estevão Jr., MAIG, Enrique Alfonso Rubio Esquivel, Registered Member (No. 255) (Chilean Mining Commission), Luis Bernal Venegas, Registered Member (No. 415) Chilean Mining Commission), Ricardo Martín Miranda Díaz, Registered Member (No. 145) (Chilean Mining Commission) and Cid Gonçalves Monteiro Filho, RM SME, FAusIMM, MAIG, reviewed and approved the scientific and technical information relating to the Furnas Project contained in this AIF, and is a “qualified person” within the meaning of NI 43-101. Each of Joao Estevao Jr., MAIG, Enrique Alfonso Rubio Esquivel, Registered Member (No. 255) (Chilean Mining Commission), Luis Bernal Venegas, Registered Member (No. 415) Chilean Mining Commission), Ricardo Martín Miranda Díaz, Registered Member (No. 145) (Chilean Mining Commission) is “independent” of the Company within the meaning of NI 43-101. Cid Gonçalves Monteiro Filho, RM SME, FAusIMM, MAIG, being the Resource and Reserve Manager of the Company, is not “independent” of the Company within the meaning of NI 43-101.

Reference should be made to the full text of the Caraíba Operations Technical Report, the Xavantina Operations Technical Report, the Tucumã Technical Report, and the Furnas Project Technical Report, each of which is available for review on the Company’s website at www.ero.com and under the Company’s profile on SEDAR+ at www.sedarplus.ca/home/ and on EDGAR at www.sec.gov.

CIM Definition Standards

The Mineral Reserves and Mineral Resources for the Caraíba Operations (including as used in the Caraíba Operations Technical Report), the Xavantina Operations (including as used in the Xavantina Operations Technical Report), the Tucumã Operation (including as used in the Tucumã Technical Report) and the Furnas Project (including as used in the Furnas Project Technical Report) have been estimated in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) Definition Standards for Mineral Resources and Mineral Reserves adopted by the CIM Council on May 19, 2014 (the “CIM Standards” or “CIM Definition Standards”) and the CIM Estimation of Mineral Resources and Mineral Reserves Best Practice Guidelines, adopted by CIM Council on November 29, 2019 (the “CIM Guidelines”), which are incorporated by reference in NI 43-101. The following definitions are reproduced from the CIM Definition Standards:

“Feasibility Study” means a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable Modifying Factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate, at the time of reporting, that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or

finance, the development of the project. The confidence level of the study will be higher than that of a Pre-Feasibility Study.

“Indicated Mineral Resource” means that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors as described below in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource and may only be converted to a Probable Mineral Reserve.

“Inferred Mineral Resource” means that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

“Measured Mineral Resource” means that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated Mineral Resource or an Inferred Mineral Resource. It may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve.

“Mineral Reserve” means the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at pre-feasibility or feasibility level as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The reference point at which Mineral Reserves are defined, usually the point where the ore is delivered to the processing plant, must be stated. It is important that, in all situations where the reference point is different, such as for a saleable product, a clarifying statement is included to ensure that the reader is fully informed as to what is being reported. The public disclosure of a Mineral Reserve must be demonstrated by a Pre-Feasibility Study or Feasibility Study.

“Mineral Resource” means a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

“Pre-Feasibility Study” means a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the Modifying Factors and the evaluation of any other relevant factors which are sufficient for a qualified person, acting reasonably, to determine if all or part of the Mineral Resource may be converted to a Mineral Reserve at the time of reporting. A Pre-Feasibility Study is at a lower confidence level than a Feasibility Study.

“Probable Mineral Reserve” means the economically mineable part of an Indicated, and in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve.

“Proven Mineral Reserve” means the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the Modifying Factors.

For the purposes of the CIM Definition Standards, “Modifying Factors” are considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

Cautionary Notes Regarding Mineral Resource and Mineral Reserve Estimates

Unless otherwise indicated, all reserve and resource estimates included in this AIF and the documents incorporated by reference herein have been prepared in accordance with NI 43-101 and the CIM Standards. NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Canadian standards, including NI 43-101, differ significantly from the requirements of the United States Securities and Exchange Commission (the “SEC”), and reserve and resource information included herein may not be comparable to similar information disclosed by U.S. companies. In particular, and without limiting the generality of the foregoing, this AIF and the documents incorporated by reference herein use the terms “measured resources,” “indicated resources” and “inferred resources” as defined in accordance with NI 43-101 and the CIM Standards.

Alternative Performance (Non-IFRS) Measures

The Company utilizes certain alternative performance (non-IFRS) measures to monitor its performance, including copper C1 cash cost, realized copper price, gold C1 cash cost, gold AISC, realized gold price, EBITDA, adjusted EBITDA, adjusted net income attributable to owners of the Company, adjusted net income per share, net (cash) debt, working capital and available liquidity. These performance measures have no standardized meaning prescribed within generally accepted accounting principles under IFRS and, therefore, amounts presented may not be comparable to similar measures presented by other mining companies. These non-IFRS measures are intended to provide supplemental information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The reader is directed to the Management’s Discussion and Analysis of the Company for the year ended December 31, 2025 (see “Alternative Performance (Non-IFRS) Measures” section) for a reconciliation of these non-IFRS measures to the most directly comparable IFRS measures as contained in the Company’s audited consolidated financial statements for the years ended December 31, 2025 and 2024. Unless otherwise noted, the non-IFRS measures presented herein have been calculated on a consistent basis for the periods presented.

Copper C1 Cash Cost and Copper C1 Cash Cost including Foreign Exchange Hedges

Copper C1 cash cost is a non-IFRS performance measure used by the Company to manage and evaluate the performance of its copper mining operations.

Copper C1 cash cost is calculated as C1 cash costs divided by total pounds of copper produced during the period. C1 cash costs comprise the total cost of production, including expenses related to transportation, and treatment and refining charges. These costs are net of by-product credits and incentive payments.

Copper C1 cash cost including foreign exchange hedges is calculated as C1 cash costs, adjusted for realized gains or losses from its operational foreign exchange hedges, divided by total pounds of copper produced during the period. Although the Company does not apply hedge accounting in its consolidated financial statements and recognizes these contracts at fair value through profit or loss, the Company believes it appropriate to present cash costs including the impact of realized gains and losses as these contracts were entered into to mitigate the impact of changes in exchange rates.

While copper C1 cash cost is widely reported in the mining industry as a performance benchmark, it does not have a standardized meaning and is disclosed as a supplement to IFRS measures.

Realized Copper Price

Realized copper price is a non-IFRS ratio which is calculated as gross copper revenue divided by pounds of copper sold during the period. Management believes measuring realized copper price enables investors to better understand performance based on realized copper sales in each reporting period.

Gold C1 Cash Cost

Gold C1 cash cost is a non-IFRS performance measure used by the Company to manage and evaluate the operating performance of its gold mining segment and is calculated as C1 cash costs divided by total ounces of gold produced during the period. C1 cash cost includes total cost of production, net of by-product credits and incentive payments. Gold C1 cash cost is widely reported in the mining industry as benchmarks for performance but does not have a standardized meaning and is disclosed in supplemental to IFRS measures.

Gold AISC

Gold AISC is an extension of gold C1 cash cost discussed above and is also a key performance measure used by management to evaluate operating performance of its gold mining segment. Gold AISC is calculated as AISC divided by total ounces of gold produced during the period. AISC includes C1 cash costs, site general and administrative costs, accretion of mine closure and rehabilitation provision, sustaining capital expenditures, sustaining leases, and royalties and production taxes. Gold AISC is widely reported in the mining industry as benchmarks for performance but does not have a standardized meaning and is disclosed in supplement to IFRS measures.

Realized Gold Price

Realized gold price is a non-IFRS ratio that is calculated as gross gold revenue divided by ounces of gold sold during the period. Management believes measuring realized gold price enables investors to better understand performance based on the realized gold sales in each reporting period.

EBITDA and Adjusted EBITDA

EBITDA and adjusted EBITDA are non-IFRS performance measures used by management to evaluate its debt service capacity and performance of its operations. EBITDA represents earnings before finance expense, finance income, income taxes, depreciation and amortization. Adjusted EBITDA is EBITDA before the pre-tax effect of adjustments for non-cash and/or non-recurring items.

Adjusted net income attributable to owners of the Company and Adjusted net income per share attributable to owners of the Company

“Adjusted net income attributable to owners of the Company” is net income attributed to shareholders as reported, adjusted for certain types of transactions that, in management's judgment, are not indicative of our normal operating activities or do not necessarily occur on a recurring basis. “Adjusted net income per share attributable to owners of the Company” (“Adjusted EPS”) is calculated as "adjusted net income attributable to owners of the Company" divided by weighted average number of outstanding common shares in the period.

The Company believes that, in addition to conventional measures prepared in accordance with IFRS, the Company and certain investor and analysts use these supplemental non-IFRS performance measures to evaluate the normalized performance of the Company. The presentation of Adjusted EPS is not meant to substitute the net income (loss) per share attributable to owners of the Company (“EPS”) presented in accordance with IFRS, but rather it should be evaluated in conjunction with such IFRS measures.

Net (Cash) Debt

Net debt is a performance measure used by the Company to assess its financial position and ability to pay down its debt. Net debt is determined based on cash and cash equivalents, short-term investments, net of loans and borrowings as reported in the Company’s consolidated financial statements.

Working Capital (Deficit) and Available Liquidity

Working capital is calculated as current assets less current liabilities as reported in the Company’s consolidated financial statements. The Company uses working capital as a measure of the Company’s short-term financial health and ability to meet its current obligations using its current assets. Available liquidity is calculated as the sum of cash and cash equivalents, short-term investments and the undrawn amount available on its revolving credit facilities. The Company uses this information to evaluate the liquid assets available.

For further details on Non-IFRS measures, please refer to the Company’s annual audited consolidated financial statements for the year ended December 31, 2025 and Management’s Discussion and Analysis relating thereto, a copy of which is available for review on the Company’s website at www.ero.com and under the Company’s profile on SEDAR+ at www.sedarplus.ca/home/ and EDGAR at www.sec.gov.

LIST OF ABBREVIATIONS

In this AIF, the following abbreviations have the meanings set forth below:

| | | | | | | | | | | |

| Cu | copper | Mt | megatonne |

| Ni | nickel | kt | kilotonne |

| Co | cobalt | t | metric tonne |

| Ag | silver | kg | kilogram |

| Au | gold | g | gram |

| Fe | iron | lb | pound |

| Mn | manganese | ml | millilitre |

| Zn | zinc | MW | megawatt |

| Cr | chromium | kW | kilowatt |

| Al | aluminium | MVA | megavolt amperes |

| Ca | calcium | kV | kilovolt |

| Mo | molybdenum | kWh | kilowatt hour |

| W | tungsten | Hz | hertz |

| Bi | bismuth | d | day |

| S | sulfur | h | hour |

| F | fluorine | s | second |

| Cl | chlorine | Ga | billion years |

| U | uranium | Ma | million years |

| As | arsenic | masl | metres above mean sea level |

| P | phosphorus | m3 | cubic metre |

| Pb | lead | Mm3 | cubic megametre |

| km | kilometre | mmWC | millimeter of water column |

| m | metre | Pa | pascal |

| cm | centimetre | mbar | atmospheric air pressure (bar) |

| mm | millimetre | ° | degree |

| ft | foot | C | Celsius |

| ha | hectare | µm | micrometre |

| oz | troy ounce | tph | Tonnes per hour

per hour |

| gpt or g/t | grams per tonne | | |

CORPORATE STRUCTURE

Ero Copper was incorporated under the Business Corporations Act (British Columbia) (“BCABC”) on May 16, 2016. Ero Copper’s head office is located at Suite 1050, 625 Howe Street, Vancouver, British Columbia, Canada, V6C 2T6 and its registered office is located at Suite 3500, 1133 Melville Street, Vancouver, British Columbia, Canada, V6E 4E5.

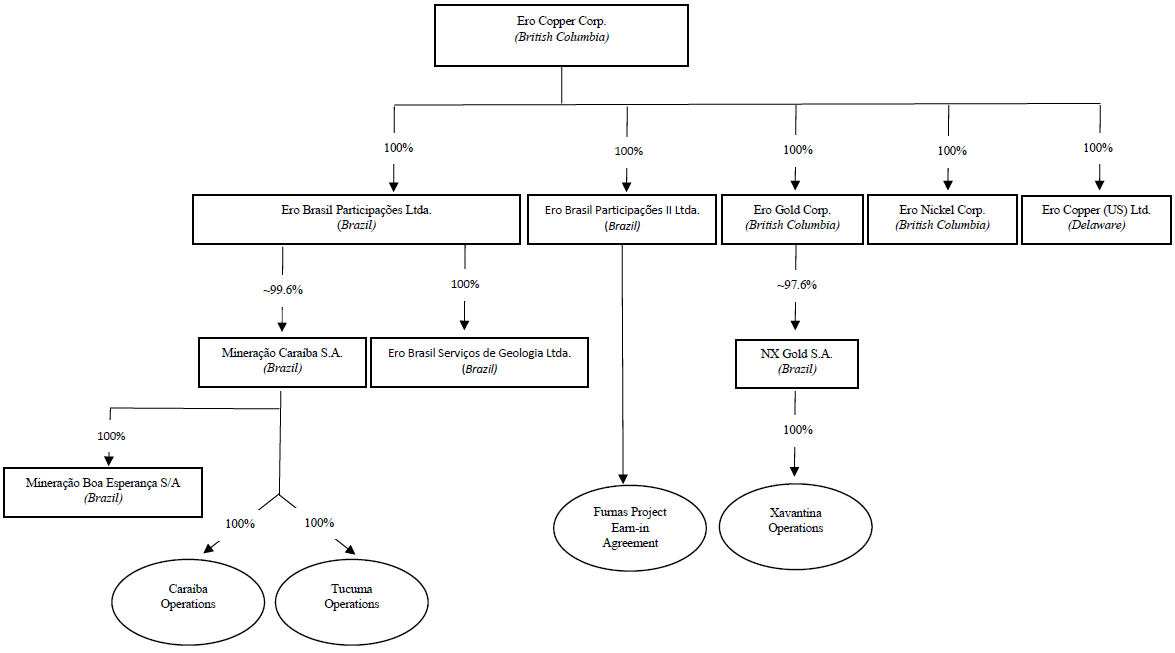

The following chart illustrates the Company’s principal subsidiaries, together with the governing law of each subsidiary and the percentage of voting securities beneficially owned or controlled or directed, directly or indirectly, by the Company, as well as the Company’s operating mines and exploration projects.

The remaining voting shares of Mineração Caraíba S.A. (“MCSA”) are held by a minority group of shareholders, including former employees of MCSA. The remaining voting shares of NX Gold S.A. (“NX Gold”) are held by a minority group of shareholders, including former employees of NX Gold.

GENERAL DEVELOPMENT AND BUSINESS OF THE COMPANY

General

Ero is a Brazil-focused, growth-oriented, copper and gold producer with operations in Brazil and corporate headquarters in Vancouver, British Columbia, Canada. Ero is listed on the Toronto Stock Exchange (the “TSX”) and the New York Stock Exchange (“NYSE”), in each case under the symbol “ERO”.

Ero’s principal asset is its approximately 99.6% ownership interest in MCSA, held indirectly through its wholly-owned subsidiary, Ero Brasil Participações Ltda. (“EBP”). MCSA’s predominant activity is the production and sale of copper concentrate from its 100% ownership interest in the Caraíba Operations and the Tucumã Operation. The Caraíba Operations have been in operation for over 40 years and consist of a fully integrated hub-and-spoke operating model, with current mining activities conducted at the Pilar underground mine, the Vermelhos underground mine, and the Surubim open pit mine feeding the central Caraíba Mill, a conventional crushing, grinding and flotation mill located adjacent to the Pilar underground mine. For further details concerning the Caraíba Operations, see below under the headings “Three Year History” and “Caraíba Operations”. The Tucumã Operation achieved commercial production on July 1, 2025. For further details concerning the Tucumã Operation, see below under the headings “Three Year History” and “Tucumã Operation”.

Ero also owns an approximately 97.6% ownership interest in NX Gold, held indirectly through its wholly-owned subsidiary, Ero Gold Corp. (“Ero Gold”). NX Gold’s predominant activity is the production and sale of

gold from the Xavantina Operations. For further details concerning the Xavantina Operations, see below under the headings “Three Year History” and “Xavantina Operations”.

In addition to its operating assets, Ero has the option to earn a 60% interest in the Furnas Project. For further details concerning the Furnas Project, see below under the headings “Three Year History” and the "Furnas Project".

The Caraíba Operations, Xavantina Operations, the Tucumã Operation and the Furnas Project are the mineral projects material to Ero for the purposes of NI 43-101.

Three Year History

Senior Unsecured Notes

•In February 2022, the Company completed an offering of US$400 million aggregate principal amount of 6.50% senior notes due 2030 (the “Notes”). The Notes will mature on February 15, 2030. EBP and MCSA are currently the only guarantors of the Notes on a senior unsecured basis. The Notes are direct, senior obligations of the Company, EBP and MCSA, and are not secured by any mortgage, pledge or charge. The Company used a portion of the net proceeds of the offering to repay outstanding borrowings under the predecessor credit facility to the 2023 Senior Credit Facility of approximately US$50 million and used the remaining balance for capital expenditures at the Tucumã Operation and general corporate purposes. Additional information on the Notes is set out below under the heading “Description of Capital Structure - Senior Unsecured Notes”.

Senior Credit Facility

•On January 12, 2023, the Company replaced a US$75 million senior secured revolving credit facility agreement with a second amended and restated credit agreement (the “2023 Senior Credit Facility Agreement”) among the Company, as borrower, Bank of Montreal, as administrative agent, joint lead arranger and sole bookrunner, The Bank of Nova Scotia (“Scotiabank”) as joint lead arranger, Canadian Imperial Bank of Commerce as documentation agent, and the lenders party thereto from time to time, as lenders, pursuant to which, amongst other things, (i) the revolving credit facility was increased to US$150 million (the “2023 Senior Credit Facility”) payable in a lump sum at maturity in December 2026. The 2023 Senior Credit Facility Agreement was subsequently amended on November 2, 2023 to, among other things, permit the Company and its subsidiaries to enter into a copper prepayment facility; (ii) December 13, 2024 to, among other things, increase the limit from US$150 million to US$200 million and to extend the maturity from December 2026 to December 2028, with all conditions to drawing of funds being satisfied in January 2025, change the interest rate and commitment fee on the 2023 Senior Credit Facility to sliding scales of SOFR plus an applicable margin ranging from 2.00% to 4.25%, and 0.45% to 0.96%, respectively, and replace the total leverage ratio with a net leverage ratio for the purposes of determining financial covenants and interest rates, with lower leverage ratios resulting in lower pricing; and (iii) March 28, 2025 to amend the defined term of "NX Gold Mine" to incorporate additional tenements acquired by the Company and the associated expansion of the area of influence under the NX Gold Stream Agreements.

Non-Priced Copper Prepayment Facility

•In May 2024, the Company’s subsidiary, MCSA, entered into a US$50 million non-priced copper prepayment facility (the “Non-Priced Copper Prepayment Facility”), structured by the Bank of Montreal and with participation by CIBC Capital Markets, pursuant to the Copper Export Prepayment Facility Agreement dated May 6, 2024 between MCSA and the Bank of Montreal (the “Non-Priced Copper Prepayment Facility Agreement”) to support the commencement of production and associated working capital needs at the Tucumã Operation. This facility is repayable over 27 equal monthly installments, beginning in October 2024, through the delivery of 272 tonnes of copper per month in the form of LME copper warrants. Each monthly delivery's value is determined based on prevailing market copper prices at the time of delivery. Should the value of any delivery exceed the amount of the monthly installment payment of US$2.1 million, the excess value is repaid to the Company. The Non-Priced Copper Prepayment Facility Agreement provided an option to increase the size of the Non-priced Copper Prepayment Facility from US$50 million to US$75 million until March 31, 2025, which the Company exercised on March 11, 2025, resulting in an additional US$25 million repayable over 21 equal monthly installments, beginning in April 2025, through the delivery of a minimum of 161 tonnes of copper each month, with deliveries similarly valued at prevailing market prices and any excess value over the fixed monthly installment payment of US$1.3 million repaid to the Company.

Equity Financing

•On November 14, 2023, the Company completed an offering, on a bought deal basis, of 9,010,000 common shares, including, 500,000 common shares issued pursuant to the partial exercise of the underwriter’s over-allotment option, at a price of US$12.35 per common share for gross proceeds of approximately US$111 million or net proceeds of US$104 million after share issuance costs (the “Offering”). The Offering was conducted by a syndicate of underwriters led by BMO Capital Markets, as sole bookrunner and lead underwriter, and including Canaccord Genuity Corp., CIBC World Markets Inc., Scotia Capital Inc., TD Securities Inc., Cormark Securities Inc., National Bank Financial Inc., Paradigm Capital Inc., PI Financial Corp., Raymond James Ltd. and Stifel Canada. The net proceeds of the Offering have been used to construct the Tucumã Operation and advance growth initiatives at the Caraíba Operations, advance regional exploration in Brazil, and for working capital and other general corporate purposes.

Caraíba Operations

•In December 2023, the Company completed the Caraíba mill expansion, which increased mill throughput capacity from 3.2 to 4.2 million tonnes per annum, with design capacity achieved by year-end.

•Through 2024 and 2025, the Company has made important progress on its growth strategy at the Caraíba Operations by advancing construction of the Pilar Mine’s new external shaft, with completion expected in 2027, and by completing a multi-quarter mill debottlenecking program in 2025 enabling increased processing rates.

Xavantina Operations

•On December 3, 2024, the Company announced an updated mineral resource and mineral reserve estimate for the Xavantina Operations, which includes a 19% increase in proven and probable mineral reserves as compared to the 2023 estimate, including a 24% increase at the Santo Antônio vein and a 26% increase in measured and indicated mineral resources, inclusive of mineral reserves, as compared to the 2023 estimate, including a 31% increase at the Santo Antônio vein.

•On March 28, 2025, the Company entered into an agreement with RGLD Gold AG ("RG AG"), a wholly owned subsidiary of Royal Gold, Inc., that effectively extended the gold delivery threshold under the existing precious metals purchase agreement dated June 29, 2021 (the "Original Xavantina Stream") from 93,000 to 160,000 ounces before the stream percentage decreases from 25% to 10% of gold produced over the remaining life of mine (the "Stream Supplement"). In exchange, the Company received $50 million in upfront cash, bringing total proceeds under the Original Xavantina Stream and the Stream Supplement to $160 million (collectively, the “NX Gold Stream Agreements”). The delivery of additional ounces under the Stream Supplement is expected to commence in 2028.

•On November 4, 2025, the Company announced the results of a year-long value-creation initiative at its Xavantina Operations, which included comprehensive sampling, metallurgical testing, material characterization and commercial negotiations to capture value from stockpiled gold concentrates produced since processing operations began in 2012, and commenced initial gold concentrate shipments in October 2025. The Company also announced an updated mineral resource and mineral reserve estimate for the Xavantina Operations incorporating drilling activities and mining depletion through June 30, 2025, reflecting proven and probable mineral reserves totaling 466,000 ounces (comprised of approximately 46,000 oz of proven reserves and approximately 420,000 ounces of probable reserves), measured and indicated mineral resources totaling 664,000 ounces (comprised of approximately 81,000 ounces of measured resources and 583,000 ounces of indicated resources), inclusive of mineral reserves, and an inferred mineral resource of 365,000 ounces.

Tucumã Operation

•On June 12, 2024, the Company announced that the Tucumã Operation was issued an Operational License by the Pará State environmental agency, Secretaria de Estado de Meio Ambiente e

Sustentabilidade ("SEMAS"), being the last remaining permitting milestone for commercial production, and that physical construction of the project had reached approximately 99% completion.

•On July 23, 2024, the Company announced the production of its first saleable copper concentrate from the Tucumã Operation.

•On July 3, 2025, the Company announced that the Tucumã Operation achieved commercial production, effective July 1, 2025.

Furnas Project

•In July 2024, Ero’s wholly-owned subsidiary, Ero Brasil Participações II Ltda. (“EBP II”), entered into a definitive earn-in agreement with Salobo Metais S.A, a subsidiary of Vale Base Metals (the “Furnas Project Earn-in Agreement”), wherein the Company has the right to earn a 60% interest in the Furnas Project upon completion of several exploration, engineering and development milestones over a five-year period. In exchange for its 60% interest, Ero will solely fund a phased work program during the earn-in period and grant Vale Base Metals up to an 11.0% "free carry" on future Furnas Project construction capital expenditures.

•On October 2, 2024, the Company announced an initial mineral resource estimate for the Furnas Project, supported by over 90,000 meters of historical drilling completed by Vale S.A. and Anglo American plc. and highlighting the project’s significant potential.

•On July 10, 2025, the Company announced the completion of its 28,000-meter Phase 1 drill program at the Furnas Project, which was primarily focused on confirming continuity of high-grade mineralization through infill drilling, as well as increasing confidence at the down-dip limits of the mineral resource. The remaining portion of the program, approximately 25% of total meters, was dedicated to step-out drilling, which has extended the known limits of mineralization to approximately 950 meters down-dip from surface.

•On November 4, 2025, the Company announced the completion of the 17,000-meter Phase 2 drill program approximately three months ahead of schedule and the commencement of the 45,000-meter Phase 3 drill program.

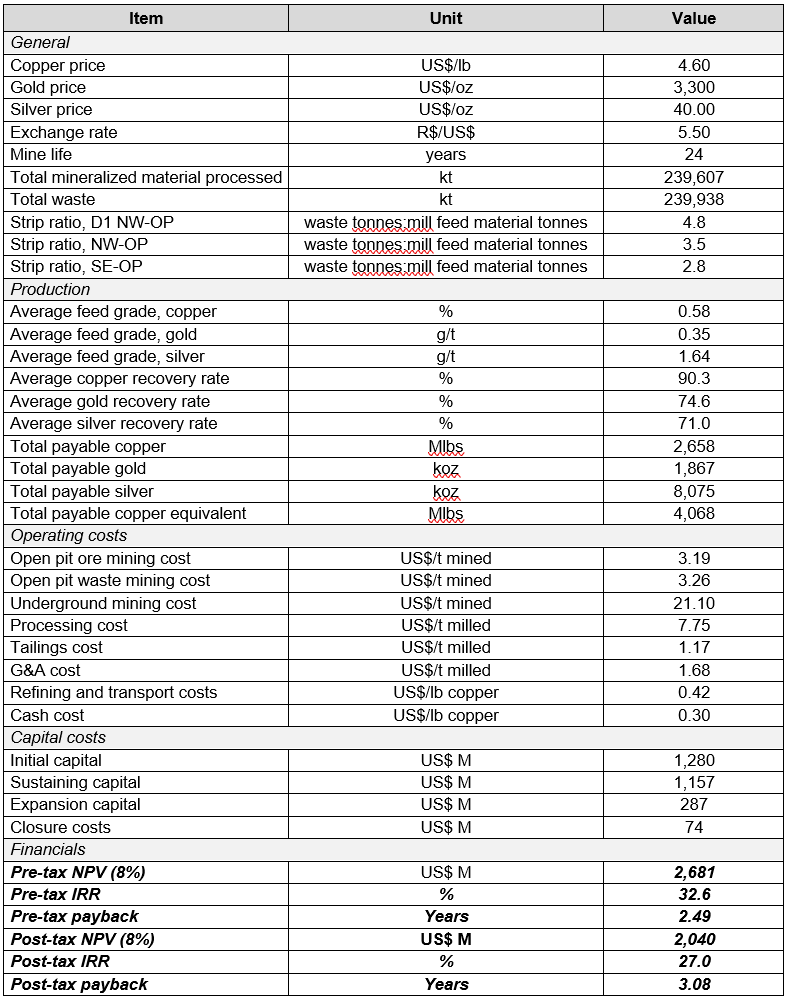

•On February 23, 2026, the Company announced the results of the preliminary economic assessment on the Furnas Project (the "PEA"), outlining a 24-year initial mine life based on an updated mineral resource estimate that remains open to depth and laterally along strike. The updated mineral resource estimate incorporates approximately 90,000 meters of historical drilling completed by Vale S.A. and Anglo American plc., together with 28,000 meters of Phase 1 drilling completed by Ero through July 2025. Additional information on the PEA is set out below under the heading “Furnas Project” The PEA is preliminary in nature and includes inferred mineral resources, which are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Corporate

•On November 1, 2023, the Company announced the appointment of Faheem Tejani to the Board effective November 1, 2023 and Matthew Wubs' intention not to stand for re-election at the 2024 annual meeting of shareholders. Mr. Wubs retired from the Board immediately prior to the commencement of the annual meeting of shareholders on April 24, 2024.

•On December 31, 2024, Christopher Noel Dunn, who co-founded the Company, retired from the Board.

•As part of the next phase of the Company’s leadership succession plan, effective January 1, 2025:

oDavid Strang, who co-founded the Company and served as the Chief Executive Officer of the Company since 2016, assumed the role of Executive Chairman of the Board;

oMakko DeFilippo assumed the role of President and Chief Executive Officer of the Company and joined the Board. Prior thereto, Makko DeFilippo served as President and Chief Operating Officer of the Company since May 2023; and

oGelson Batista, who joined the Company in September 2024, assumed the role of Chief Operating Officer of the Company.

2026 Production Guidance and Three-Year Production Outlook

The Company's 2026 production guidance and three-year production outlook demonstrates the continued execution of its longer-term growth strategy, including the ongoing construction of the new external shaft at the Caraíba Operations’ Pilar Mine (being the Deepening Extension Project) and the delivery of what will be the first preliminary economic assessment ever published on the Furnas Project.

At the Caraíba Operations and Tucumã Operation, consolidated copper production in 2026 is expected to range between 67,500 to 77,500 tonnes, representing an increase of up to 20% compared to 2025. Consolidated copper production is then expected to grow over the next two years, reaching between 80,000 and 90,000 tonnes by 2028.

At the Xavantina Operations, gold production from mine operations is expected to total 40,000 to 50,000 ounces representing an increase of up to 34% compared to 2025. In addition, gold sales from the Xavantina Operations are expected to be bolstered with the continued sale of gold concentrates that commenced in the fourth quarter of 2025, and which are expected to continue through mid-2027. Mining and processing operations are projected to deliver higher sustained production of between 50,000 and 60,000 ounces in 2027 and 2028, driven by the transition to mechanized mining and further utilization of excess plant capacity.

| | | | | | | | | | | | | | | | | | | | |

Three-year Outlook(1) | | 2026 | | 2027 | | 2028 |

| Copper (tonnes) | | | | | | |

Caraíba Operations | | 35,000 – 40,000 | | 40,000 – 45,000 | | 45,000 – 50,000 |

Tucumã Operation | | 32,500 – 37,500 | | 35,000 – 40,000 | | 35,000 – 40,000 |

| Total Copper | | 67,500 – 77,500 | | 75,000 – 85,000 | | 80,000 – 90,000 |

| | | | | | |

| Gold (ounces) | | | | | | |

| Xavantina Operations | | 40,000 – 50,000 | | 50,000 – 60,000 | | 50,000 – 60,000 |

| Gold in Concentrates | | Concentrate sales expected to continue through mid-2027(2) |

Note:

(1) Guidance is based on estimates and assumptions including, but not limited to, Mineral Resource and Mineral Reserve estimates, grade and continuity of interpreted geological formations and metallurgical recovery performance. Please refer to the Risk Factors section of this AIF for a discussion of the various risk factors that could adversely impact the Company’s business, production levels, financial condition, results of operations, cash flows and prospects.

(2) Gold concentrate sales over the projection period related to the Xavantina Operations' stockpiled gold concentrate remain subject to ongoing sampling.

Total capital expenditures in 2026 are expected to range between US$275 to US$320 million. Capital expenditures at the existing operations are expected in the range of US$245 to US$280 million and include growth capital of approximately US$80 million related to the continued construction of the Pilar Mine's new shaft and ancillary infrastructure at the Caraíba Operations, as well as investments in additional mine ventilation, development, and equipment to support future growth at the Xavantina Operations. The Company expects to spend an additional $30 to $40 million to continue advancing exploration, engineering, and permitting workstreams at the Furnas Project, as well as advancing several exploration opportunities within the Company's portfolio.

Figures presented below are in USD millions.

| | | | | | | | |

| | 2026 Guidance |

Caraíba Operations | | $170 - $185 |

Tucumã Operation | | $35 - $45 |

| Xavantina Operations | | $40 - $50 |

| Furnas Copper-Gold Project and Other Exploration | | $30 - $40 |

Total | | $275 - $320 |

Principal Products and Operations

The Company’s principal product is copper produced and sold from the Caraíba Operations and the Tucumã Operation, with gold and silver produced and sold as by-products. Gold and, as a by-product, silver is also produced and sold from the Xavantina Operations. During the year ended December 31, 2025, the Caraíba Operations processed 3,656,240 tonnes of material, producing 36,035 tonnes of copper; the Tucumã Operation, where production continues to ramp-up, processed 1,805,300 tonnes of material, producing 28,272 tonnes of copper; and, the Xavantina Operations processed 172,178 tonnes of material, producing 37,291 ounces of gold. An additional 14,999 ounces of gold in concentrates were sold from the Xavantina Operations during the fourth quarter of 2025, net of 2,245 ounces deliverable to RG AG under the NX Gold Stream Agreements.

The Caraíba Operations

| | | | | | | | | | | | | | |

| | 2025 | | 2024 |

Ore mined (tonnes) | | 3,732,992 | | 3,274,410 |

Ore processed (tonnes) | | 3,656,240 | | 3,431,294 |

Grade (% Cu) | | 1.09 | | | 1.14 |

Recovery (%) | | 90.0 | | | 90.6 |

Cu Production (tonnes) | | 36,035 | | 35,444 |

Cu Production (lbs) | | 79,443,361 | | 78,139,888 |

Concentrate grade (% Cu) | | 32.6 | | | 33.0 |

Concentrate sales (tonnes) | | 109,748 | | 110,650 |

Cu Sold in concentrate (tonnes) | | 35,820 | | 36,557 |

Cu Sold in concentrate (lbs) | | 78,969,414 | | 80,593,665 |

The Tucumã Operation

| | | | | | | | | | | | | | |

| | 2025 | | 2024 |

Ore mined (tonnes) | | 3,659,917 | | 1,932,423 |

Ore processed (tonnes) | | 1,805,300 | | 333,791 |

Grade (% Cu) | | 1.79 | | | 1.78 |

Recovery (%) | | 88.7 | | | 86.6 | |

Cu Production (tonnes) | | 28,272 | | 5,156 |

Cu Production (lbs) | | 62,329,079 | | 11,365,980 |

Concentrate grade (% Cu) | | 29.9 | | | 28.0 |

Concentrate sales (tonnes) | | 93,935 | | 15,036 |

Cu Sold in concentrate (tonnes) | | 27,487 | | 4,107 |

Cu Sold in concentrate (lbs) | | 60,598,403 | | 9,055,352 | |

The Xavantina Operations

| | | | | | | | | | | | | | |

| | 2025 | | 2024 |

Ore mined (tonnes) | | 176,980 | | 146,160 |

Ore processed (tonnes) | | 172,178 | | 146,161 |

Head grade (grams per tonne Au) | | 8.24 | | 13.37 |

Recovery (%) | | 82.8 | | | 92.0 | |

Gold ounces produced (oz) | | 37,291 | | 57,210 |

Silver ounces produced (oz) | | 23,090 | | 33,927 |

Gold sold in dore (oz) | | 35,950 | | 60,195 |

Silver sold in dore (oz) | | 22,753 | | 34,503 |

Gold sold in concentrate (oz)(1) | | 12,754 | | — |

(1) Gold sold in concentrate includes 14,999 ounces of gold shipped to customer, net of 2,245 ounces deliverable to RG AG under the NX Gold Stream Agreements.

During the year ended December 31, 2025, the Company generated revenue of US$785.8 million. The following table summarizes the net revenue of the Company for the financial years ended December 31, 2025 and 2024. Tabular amounts are in thousands of US dollars:

| | | | | | | | |

| Year Ended December 31, 2025 (US$000s) | Year Ended December 31, 2024 (US$000s) |

Copper concentrate | 619,736 | 342,956 |

Gold | 166,108 | 127,303 |

Net Operating Revenues: | 785,844 | 470,259 |

There are global copper and gold markets into which the Company can sell its copper and gold concentrates and gold doré and, as a result, the Company is not dependent on a particular purchaser with regard to the sale of the copper and gold concentrate and gold doré that it produces.

MCSA sells its final copper concentrate, containing gold and silver as by-product metals, to various international trading companies that ship the copper concentrate to smelters globally via ports located in Brazil. All copper concentrate is transported from site to the port by road using standard highway trucks, which are weighed and sampled for final assay prior to shipment.

NX Gold produces and sells doré bars containing gold and silver to COIMPA Industrial Ltda. (“COIMPA”). The doré bars are transported to COIMPA’s facility in Manaus, State of Amazonas, Brazil by airplane using a secure gravel airstrip located on the Xavantina Operations. NX Gold sells its gold concentrate to at least one international trading company that ships the gold concentrate to smelters globally via ports located in Brazil. All gold concentrate is transported from site to the port by road using standard highway trucks, which are weighed and sampled for provisional invoicing prior to shipment, with final assays conducted at the port of destination.

Competitive Conditions

The Company’s primary business is to produce and sell copper. The Company also produces and sells gold. Prices are determined by world markets over which the Company has no influence or control. Ero’s competitive position is primarily determined by its costs compared to other producers throughout the world and its ability to maintain its financial integrity through metal price cycles. Costs are governed to a large extent by the grade, nature and location of the Company’s Mineral Reserves and Mineral Resources as well as by input costs and the level of operating and management skill employed in the production process.

The mining industry is competitive, particularly in the acquisition of additional Mineral Reserves and Mineral Resources in all phases of operation, and the Company competes with many companies possessing similar or greater financial and technical resources. The Company also competes with other mining companies and other third parties over sourcing raw materials, equipment and supplies in connection with its production, development and exploration operations, as well as for skilled and experienced personnel and transportation capacity.

Specialized Skills and Knowledge

The nature of the Company’s business requires specialized skills, knowledge and technical expertise in the areas of geology, engineering, mine planning, mine operations, metallurgical processing, and environmental compliance. In addition to the specialized skills listed above, the Company also relies on staff members, contractors and consultants with specialized knowledge of logistics and operations in Brazil and local community relations. In order to attract and retain personnel with the specialized skills and knowledge required for the Company’s operations, the Company maintains competitive remuneration and compensation packages. To date, the Company has been able to meet its staffing requirements.

Business Cycles

The mining business is subject to global economic cycles which affect the marketability of products derived from mining.

Employees

As at December 31, 2025, Ero and its subsidiaries employed a total of 3,547 employees (consisting of 20 employees of Ero, two employees of Ero Copper (US) Ltd., 94 employees of EBP, 28 employees of EBP II, 17 employees of Ero Brasil Services Geologic Ltda., 2,415 employees of MCSA, 392 employees of Mineração Boa Esperança S/A and 579 employees of NX Gold) and 4,379 contractors (consisting of 10 contractors of Ero, 126 contractors of EBP II, 2,613 contractors of MCSA, 1,158 contractors of Mineração Boa Esperança S/A, and 472 contractors of NX Gold.

Foreign Operations

Ero’s material operating properties are the Caraíba Operations, the Xavantina Operations and the Tucumã Operation, each located in Brazil. Foreign operations accounted for 100% of the Company’s revenue and represented approximately 97% of its assets as at December 31, 2025. Accordingly, the Company is entirely

dependent on its foreign operations for the exploration and development of its properties and for the production of copper and gold. Any changes in regulations or shifts in political attitudes in any of these jurisdictions, or other jurisdictions in which Ero has projects from time to time, are beyond the control of the Company and may adversely affect its business. Future development and operations may be affected in varying degrees by such factors as government regulations (or changes thereto) with respect to the restrictions on production, export controls, taxes, royalties, tariffs, fees and penalties, expropriation of property, repatriation of profits, environmental legislation, land use, water use, land claims of local people, mine safety, work force health and safety in the face of prevailing epidemics, pandemics or other health risks, and receipt of necessary permits. The effect of these factors cannot be accurately predicted. See below under the heading “Risks Factors”.

The risks of the corporate structure of the Company and its subsidiaries are risks that are typical and inherent for companies that have material assets and property interests held indirectly through foreign subsidiaries and located in foreign jurisdictions. The Company’s business and operations in Brazil are exposed to various levels of political, economic and other risks and uncertainties associated with operating in a foreign jurisdiction such as a difference in laws, business cultures and practices, banking systems and internal control over financial reporting. See below under the heading “Risk Factors”.

The Company has implemented a system of corporate governance, internal controls over financial reporting and disclosure controls and procedures that apply at all levels of the Company and its subsidiaries. These systems are overseen by the Board and implemented by the Company’s senior management. The relevant features of these systems are set out below.

Control over and Communication with Foreign Subsidiaries

The Company controls its foreign subsidiaries by virtue of corporate oversight and by its ownership interest in such entities (see above under the heading “Corporate Structure”). The Company’s management has the (i) power to appoint and dismiss, at any time, any and all of the foreign subsidiaries’ officers and directors, (ii) power to instruct the foreign subsidiaries’ officers to pursue business activities in accordance with the Company’s wishes, and (iii) legal right, as a shareholder, to require the officers of each such foreign subsidiary to comply with their fiduciary obligations. As a result, management of the Company can effectively align its business objectives with those of the foreign subsidiaries and implement such objectives at the subsidiary level.

The Company maintains open communication with each of its operations in Brazil through several senior officers who are proficient (or fluent) in Brazilian Portuguese. In addition, all management team members in Brazil are fluent in Brazilian Portuguese and fluent (or proficient) in English. The primary language used in management and Board meetings is English and material documents relating to the Company and its operations that are provided to the Board and its committees are in English. If necessary, management of the Company and the Board and its committees have access to independent translators to overcome any language differences. The Company does not currently have a formal communication plan or policy in place and has not, to date, experienced any communication-related issues.

Board and Management Expertise

Each of the Company’s non-executive directors and senior officers have experience in Brazil, being the jurisdiction in which the Company operates. In addition, the Board, through its corporate governance practices, receives quarterly management and technical updates and progress reports in connection with the foreign subsidiaries, and at each quarterly Board meeting, the directors meet with management on topics including short, medium and long-term corporate objectives, strategic risk and mitigation strategies and strategic planning, and in so doing, maintains effective oversight of the Company’s business and operations. Moreover, Board members and senior officers have access to corporate director education programs which offer courses on topics such as strategic direction and risks, financial essentials, audit committee effectiveness, risks and disclosure, human resource and compensation committee performance and enterprise risk oversight.

In 2025, most senior officers visited the Company’s operations in Brazil quarterly, or more frequently if circumstances required, on a rotating basis, to ensure effective control and management of the Company’s foreign operations. All but one non-executive director of the Company visited the Caraíba Operations and the

Tucumã Operation in 2025, and a total of five non-executive directors visited the Xavantina Operations in 2025. During these visits and/or past visits, they have met with local employees and community members, with such interactions enhancing the visiting directors’ and officers’ knowledge of local culture and key stakeholders.

Further, to ensure effective control and management of the Company’s foreign operations, all non-executive directors are provided with quarterly reports regarding the Company’s business and operations, and virtual or in-person meetings are held amongst the Board and management quarterly, or more frequently if circumstances required, and virtual meetings are held amongst management and the operations team in Brazil weekly, or more frequently if circumstances required.

Internal Control Over Financial Reporting and Funds

The Company maintains internal control over financial reporting with respect to its operations in Brazil by taking various measures. Several of the Company’s senior officers have the relevant language proficiency (Brazilian Portuguese) and each senior officer has local cultural understanding and relevant work experience in Brazil which facilitates better understanding and oversight of the Company’s operations in the context of internal controls over financial reporting.

Pursuant to the requirements of National Instrument 52-109, Certification of Disclosure in Issuers’ Annual and Interim Filings, the Company assesses the design and effectiveness of its internal controls over financial reporting on an annual basis. Furthermore, key controls for the accounts in scope are tested across the Company on an annual basis and the working papers of these tests performed at all the locations are reviewed at the head office level.

Differences in banking systems and controls between Canada and Brazil are addressed by having internal controls over cash; especially over access to cash, cash disbursements, appropriate authorization levels, performing and reviewing bank reconciliations and the segregation of duties.

The Company ensures the flow of funds between Canada and Brazil functions as intended by:

•appointing common officers of the Company and Ero Brasil/MCSA/NX Gold;

•involving the Executive Vice President and Chief Financial Officer and the Senior Vice President, Finance, located in Vancouver, in hiring key finance personnel in Brazil; and

•monitoring the finance departments in Brazil by regular personal visits by the Executive Vice President and Chief Financial Officer, the Executive Vice President, Brazil, the Senior Vice President, Finance and other key executives to Brazil.

Records

All of the minute books and corporate records and documents of the foreign subsidiaries are filed at the relevant entity’s headquarters, and with the relevant governmental or regulatory body in Brazil. The custodians of such documents report directly to the Company’s head office and senior management team to ensure continued oversight.

Environmental Protection

The Company’s exploration, development and mining activities are subject to various levels of federal, state and local laws and regulations relating to the protection of the environment, including requirements for closure and reclamation of mining properties. Specific statutory and regulatory requirements and standards must be met throughout the exploration, development and mining stage of a property regarding air quality, water quality, fisheries, wildlife and forestry management and protection, tailing facility management, solid and hazardous waste management and disposal, noise, land use and reclamation. Details and qualification of the Company’s mine closure and restoration obligations are set out in Note 13 of the Company’s audited consolidated financial statements for the year ended December 31, 2025, a copy of which is available for

review on the Company's website at www.ero.com and under the Company’s profile on SEDAR+ at www.sedarplus.ca/home/ and EDGAR at www.sec.gov.

The financial and operating effect of environmental protection requirements on the capital expenditures and earnings of each mineral property are not significantly different than those of similar sized mines and therefore do not and will not impact the Company’s competitive position in the current or future financial years.

Social and Environmental Policies

The Company places great emphasis on providing a safe and secure working environment for all its employees, suppliers, contractors and consultants, and recognizes the importance of operating in a sustainable manner. The Board has adopted a Code of Business Conduct and Ethics of the Company, which sets out the standards which guide the conduct of the Company’s business and the behavior of its directors, officers, employees and consultants. All new employees must read, and acknowledge that they will abide by, the code when hired. The code, among other things, sets out standards in areas relating to the Company’s commitment to health and safety in its business operations and the identification, elimination or control of workplace hazards; promotion and provision of a work environment in which individuals are treated with respect, provided with equal opportunity and is free of all forms of discrimination and abusive and harassing conduct; and ethical business conduct and legal compliance. The Board has also adopted a Supplier Code of Conduct, which sets out the core values that each supplier of the Company is expected to respect and abide by at all times, including among other things: (i) adhering to all applicable laws and regulations of the countries and regions where they conduct business, including laws protective of human rights, worker health and safety, and the environment; (ii) conducting their business ethically and not engaging, directly or indirectly, in unethical or illegal practices; (iii) adhering to the Company’s Anti-Corruption Policy (discussed below), and with all applicable anti-corruption laws, including the Corruption of Foreign Public Officials Act (Canada); (iv) adhering to the Company’s Global Human Rights Policy and Corporate Social Responsibility Policy (discussed below) in all of their dealings with workers, community members and others affected by their activities while providing services to the Company, including not engaging in any form of modern slavery such as the use of forced, compulsory or child labour; and, (v) adhering to the Company’s Environmental Policy (discussed below), Health and Safety Policy (discussed below) and all other site-specific environmental, health and safety practices and procedures that apply to their activities.