After careful consideration, the CAEP Board has unanimously approved the Business Combination Agreement and the other Proposals described in the accompanying proxy statement/prospectus and the CAEP Board has determined that it is advisable to consummate the Business Combination. The CAEP Board did not obtain a fairness opinion (or any similar report or appraisal) in connection with its determination to approve the Business Combination. However, CAEP’s management, the members of the CAEP Board and the other representatives of CAEP have reviewed certain financial information of AIR and other relevant financial information selected based on the experience and the professional judgment of CAEP’s management team. Accordingly, investors will be relying solely on the judgment of the CAEP Board in valuing AIR’s business and accordingly, investors assume the risk that the CAEP Board may not have properly valued such business. For more information, see Risk Factors — Risks Related to the Business Combination — Neither the CAEP Board nor any committee thereof obtained a fairness opinion (or any similar report or appraisal) in determining whether or not to pursue the Business Combination. Consequently, CAEP Shareholders have no assurance from an independent source that the number of Pubco Ordinary Shares to be issued to the Sellers and CAEP Shareholders in the Business Combination is fair to CAEP — and, by extension, CAEP Shareholders — from a financial point of view.” The CAEP Board recommends that Public Shareholders vote “FOR” the Proposals described in the accompanying proxy statement/prospectus (including each of the sub-proposals).

Upon the completion of the Business Combination, and assuming, among other things, that no Public Shareholders (as defined below) exercise redemption rights with respect to their Public Shares (as defined below) in connection with the Business Combination, all Sponsor Earnout Shares are released in accordance with their terms, all AIR Earnout Shares are released in accordance with their terms and that no Pubco Ordinary Shares are issued pursuant to the Pubco omnibus equity incentive plan, to be adopted prior to Closing, as amended from time to time (the “Incentive Plan”), (i) Public Shareholders, (ii) the Sponsor, (iii) the Kingsway Holders and (iv) the AIR Shareholders (excluding the Kingsway Holders), in each case, will own approximately 15.1%, 2.3%, 53.3%, and 29.3% of the issued and outstanding Pubco Ordinary Shares, respectively, subject to adjustments based on AIR Ordinary Shares outstanding immediately prior to the Jersey Closing and based on the assumptions set forth elsewhere in this proxy statement/prospectus.

The negotiated price per Pubco Ordinary Share is $10.00 per share for (i) Public Shareholders, (ii) the Sponsor, (iii) the directors and officers of CAEP, and (iv) the AIR Shareholders.

The total consideration that the Sponsor and its affiliates will receive at Closing, comprising Pubco Ordinary Shares at the negotiated price of $10.00 per share (in exchange for the CAEP Ordinary Shares held by the Sponsor after accounting for the surrender by the Sponsor and cancellation of 3,400,000 of the 6,900,000 CAEP Founder Shares (as defined below) it holds today immediately prior to, and subject to the consummation of, the Cayman Merger) and the cash fees to be paid to Cantor Fitzgerald & Co. (“CF&Co.”), an affiliate of the Sponsor, as further described herein, is $77,165,000, assuming, among other things, that the Sponsor Loan is fully drawn (for a maximum amount of $1,750,000), that no Public Shareholders exercise redemption rights with respect to their Public Shares upon completion of the Business Combination, no amount is drawn under the Sponsor Note, and the Sponsor Earnout Shares are released and not forfeited.

The total consideration that AIR Shareholders will receive at Closing, comprising Pubco Ordinary Shares at $10.00 per share (in exchange for the AIR Ordinary Shares held by the AIR Shareholders immediately prior to the Jersey Merger), and holders of certain AIR incentive awards will receive at Closing, is approximately $1,456 million, assuming AIR Earnout Shares are released and not forfeited and excluding any Pubco Ordinary Shares issuable on exercise or settlement of the Assumed Conditional Awards (as defined below) and the Incentive Plan (as defined below).

Entity |

|

Interest in Securities/Other Consideration |

|

Price Paid or to be Paid or |

Sponsor |

|

• The Sponsor will receive 3,500,000 Pubco Ordinary Shares in exchange for its 3,500,000 CAEP Founder Shares (after accounting for the surrender by the Sponsor and cancellation of 3,400,000 of the 6,900,000 CAEP Founder Shares it holds today immediately prior to, and subject to the consummation of, the Cayman Merger); provided that 1,500,000 of such Pubco Ordinary Shares will be subject to release upon the Sponsor Earnout Conditions. • The Sponsor will receive 580,000 Pubco Ordinary Shares in exchange for its 580,000 CAEP Private Placement Shares • Additional Pubco Ordinary Shares in exchange for CAEP Class A Ordinary Shares and/or cash |

|

• $25,000 paid to purchase the 6,900,000 CAEP Founder Shares • $5,800,000 paid to purchase the 580,000 CAEP Private Placement Shares • Amounts outstanding at Closing under (a) the Sponsor Loan will be repaid by the issuance of CAEP Class A Ordinary Shares at $10.00 per share and (b) all other outstanding loans provided by the Sponsor to CAEP (other than the Sponsor Loan) will be repaid in cash |

|

|

|

||

|

|

|

||

CF&Co. |

|

• $10,380,000 in cash • Approximately $24.235 million in cash, being equal to 1.5% of the enterprise value of AIR less $2 million, which fee will be reduced by an amount equal to the lesser of (i) $1.98 million and (ii) the product of: (x) 5.5%, (y) $10.00 and (z) the number of Public Shares redeemed in connection with the Transactions. |

|

• Services pursuant to the Business Combination Marketing Agreement • Services pursuant to the CF&Co. M&A Engagement Letter |

|

|

|

SUMMARY OF THE PROXY STATEMENT/PROSPECTUS

This summary highlights selected information contained in this proxy statement/prospectus and does not contain all of the information that is important to you. You should read carefully this entire proxy statement/prospectus, including the Annexes and accompanying financial statements of Pubco, CAEP and AIR, to fully understand the proposed Business Combination (as described below) before voting on the Proposals to be considered at the Meeting (as described below). Please see the section entitled “Where You Can Find More Information.”

Parties to the Business Combination

CAEP

CAEP is a blank check company incorporated in the Cayman Islands on November 11, 2020 as a Cayman Islands exempted company for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or other similar business combination, involving one or more businesses or assets.

CAEP Class A Ordinary Shares are currently listed on the Nasdaq Global Market under the ticker symbol “CAEP.” Upon the Closing, CAEP Class A Ordinary Shares will be delisted from Nasdaq.

CAEP completed the CAEP IPO of 27,600,000 CAEP Class A Ordinary Shares on June 27, 2025, generating gross proceeds to CAEP of $276,000,000. Simultaneously with the closing of the CAEP IPO, CAEP completed the sale to the Sponsor of 580,000 CAEP Private Placement Shares at a purchase price of $10.00 per CAEP Private Placement Share, generating gross proceeds to CAEP of $5,800,000. Following the closing of the CAEP IPO and the CAEP Private Placement, a total of $276,000,000, comprised of the net proceeds from the CAEP IPO and the CAEP Private Placement, was placed in the Trust Account. As of December 31, 2025, the Trust Account balance was approximately $282,000,000. Since the CAEP IPO, CAEP’s activity has been limited to efforts toward locating and completing a suitable business combination.

The mailing address of CAEP’s principal executive office is 110 East 59th Street, New York, New York 10022, and its telephone number is (212) 938-5000. As part of the Business Combination, Cayman Merger Sub will merge with and into CAEP, with CAEP continuing as the surviving entity and a direct, wholly owned subsidiary of Pubco.

AIR

AIR is a private limited company incorporated under the laws of Jersey on September 20, 2019. AIR is a leading global producer of branded flavored molasses by sales volume and market share. For the year ended December 31, 2024, AIR has an estimated global market share of approximately 36% to 44% based on sales volume in the markets in which it operates (excluding Russia and Turkey) as of December 31, 2024, according to the 2025 Market Assessment Report. AIR considers itself to be the only global player, with its sales volume surpassing the combined share of its next four competitors, who remain regional or local, as of December 31, 2024, according to AIR’s internal estimates. AIR produces and sells branded flavored molasses through direct-to-consumer, distributor and licensed retail channels in more than 90 markets, serving both at-home consumers and HoReCa channels, including lounges and other hospitality venues. AIR’s portfolio includes established flavored molasses brands such as Al Fakher, Shisha Kartel, Zødiac, NameLess and a newer brand called Kloud King. AIR’s portfolio also includes innovation-led inhalation devices, such as OOKA and VANT, and a collaboration between Snoop Dogg and Al Fakher. During the years ended December 31, 2025 and 2024, AIR generated revenue of $399.7 million and $376.6 million, respectively, operating profit of $83.2 million and $91.0 million, respectively, and Adjusted EBITDA of $139.3 million and $129.5 million, respectively.

The mailing address of AIR’s principal executive office is Festival Office Tower, Dubai Festival City, 7th Floor, Dubai, United Arab Emirates.

Pubco

Pubco is a private limited company incorporated under the laws of Jersey on October 28, 2025. Pubco will be converted to a public limited company incorporated under the laws of Jersey prior to consummation of the Business Combination. To date, Pubco has not conducted any material activities other than those incidental to its formation, the incorporation of the Cayman Merger Sub and Jersey Merger Sub and the pending Business Combination and only has nominal assets consisting of cash and cash equivalents.

Pubco intends to apply to list the Pubco Ordinary Shares on Nasdaq under the symbol “AIIR,” upon the Closing.

The mailing address of Pubco’s registered office is 15 Esplanade, St. Helier, JE1 1RB, Jersey. After the consummation of the Business Combination, Pubco’s principal executive office will be that of AIR, located at Festival Office Tower, Dubai Festival City, 7th Floor, Dubai, United Arab Emirates.

Cayman Merger Sub

Cayman Merger Sub is an exempted company incorporated with limited liability in the Cayman Islands and wholly owned subsidiary of Pubco that was incorporated on October 29, 2025 to facilitate the consummation of the Business Combination. Cayman Merger Sub will be directly owned by Pubco prior to and on the Closing Date. As part of the Business Combination, Cayman Merger Sub will merge with and into CAEP, with CAEP continuing as the surviving entity and a direct, wholly owned subsidiary of Pubco.

The mailing address of Cayman Merger Sub’s registered office is Walkers Corporate Limited, 190 Elgin Avenue, George Town, Grand Cayman KY1-9008, Cayman Islands.

Jersey Merger Sub

Jersey Merger Sub is a private limited company incorporated under the laws of Jersey and wholly owned subsidiary of Pubco that was incorporated on October 28, 2025 to facilitate the consummation of the Business Combination. Jersey Merger Sub will be directly owned by Pubco prior to and on the Closing Date. As part of the Business Combination, Jersey Merger Sub will merge with and into AIR, with AIR continuing as the surviving entity and a direct, wholly owned subsidiary of Pubco.

The mailing address of Jersey Merger Sub’s registered office is 15 Esplanade, St. Helier, JE1 1RB, Jersey.

The Business Combination Agreement

Overview

On November 7, 2025, CAEP, AIR, Pubco, Cayman Merger Sub and Jersey Merger Sub entered into the Business Combination Agreement, which contains customary representations and warranties, covenants, closing conditions and other terms relating to the Transactions.

In accordance with the terms and subject to the conditions of the Business Combination Agreement, the parties to the Business Combination Agreement have agreed that, in connection with the Closing, Cayman Merger Sub will merge with and into CAEP, with CAEP continuing as the surviving company and a wholly owned direct subsidiary of Pubco, and, separately and immediately following the Cayman Effective Time, Jersey Merger Sub will merge with and into AIR, with AIR continuing as the surviving company and a wholly owned direct subsidiary of Pubco.

For more information about the Transactions contemplated in the Business Combination Agreement, please see the section entitled “The Business Combination Agreement and Ancillary Documents.” The Business Combination Agreement is incorporated by reference into this proxy statement/prospectus, a copy of which is attached to this proxy statement/prospectus as Annex A.

Effects of the Merger

At the Cayman Effective Time, all the property, rights, privileges, agreements, powers and franchises, debts, liabilities, duties and obligations of CAEP and Cayman Merger Sub shall become the property, rights, privileges, agreements, powers and franchises, debts, liabilities, duties and obligations of the Surviving Cayman Company (including all rights and obligations with respect to the Trust Account), which shall include the assumption by the Surviving Cayman Company of any and all agreements, covenants, duties and obligations of CAEP and Cayman Merger Sub set forth in the Business Combination Agreement to be performed after the Cayman Effective Time.

At the Jersey Effective Time, (i) all property and rights to which each of AIR and Jersey Merger Sub are entitled immediately before the Jersey Merger is completed become the property and rights of the Surviving Jersey Company, (ii) the Surviving Jersey Company becomes subject to all criminal and civil liabilities, and all contracts, debts and other obligations, to which each of AIR and Jersey Merger Sub were subject immediately before the Jersey Merger is completed and (iii) all actions and other legal proceedings, which, immediately before the Jersey Merger is completed, are pending by or against any of AIR and Jersey Merger Sub may be continued by or against the Surviving Jersey Company, which shall include the assumption by the Surviving Jersey Company of any and all agreements, covenants, duties and obligations of AIR and Jersey Merger Sub set forth in the Business Combination Agreement to be performed after the Jersey Effective Time.

Conditions to the Closing

Under the Business Combination Agreement, the Closing is subject to customary and other conditions (subject to the parties’ ability to waive such conditions as permitted by the Business Combination Agreement), including, among other things (for the purposes of this section, defined terms have the meanings given to such terms in the Business Combination Agreement):

The obligations of the parties to the Business Combination Agreement to consummate the Business Combination are subject to additional conditions, as described more fully below in the section entitled “The Business Combination Agreement and Ancillary Documents — The Business Combination Agreement — Conditions to Complete the Business Combination.”

Related Agreements

A&R Registration Rights Agreement

The Business Combination Agreement contemplates that, at Closing, Pubco will enter into the A&R Registration Rights Agreement with the Sponsor and certain AIR Shareholders, substantially in the form attached to this proxy statement/prospectus as Annex D, which supersedes and replaces the registration rights agreement that was entered into by CAEP and the Sponsor in connection with the CAEP IPO, pursuant to which Pubco will agree to register for resale the Pubco Ordinary Shares that are held by the Sponsor and the AIR Shareholders at Closing pursuant to a shelf registration statement to be filed with the SEC no later than ninety (90) days following the date of Closing. Pursuant to the A&R Registration Rights Agreement, the Sponsor and certain AIR Shareholders will also have certain other registration rights, including unlimited demand and piggy-back rights, subject to cooperation and cut back provisions with respect to Pubco Ordinary Shares held by such parties at Closing.

The A&R Registration Rights Agreement amends and restates the registration rights agreement that was entered into by CAEP and the Sponsor in connection with the CAEP IPO.

Sponsor Support Agreement

Concurrently with the execution of the Business Combination Agreement, CAEP, the Sponsor, Pubco and AIR entered into the Sponsor Support Agreement, pursuant to which, among other things, the Sponsor agreed (a) to vote its Pubco Ordinary Shares in favor of the Proposals, (b) vote its Pubco Ordinary Shares against any Acquisition Proposal or Alternative Transaction, (c) to comply with the restrictions imposed by the Insider Letter and (d) to waive the anti-dilution rights of the issued and outstanding CAEP Class B Ordinary Shares set forth in the CAEP Memorandum and Articles. The Sponsor also agreed that, subject to the Closing, it will (x) surrender, for no consideration, 3,400,000 CAEP Class B Ordinary Shares to be cancelled by CAEP and (y) not transfer 1,500,000 of the Pubco Ordinary Shares that it will receive in exchange for its CAEP Founder Shares until the occurrence of certain release events.

Shareholder Support Agreement

In connection with the execution of the Business Combination Agreement, certain Key AIR Shareholders entered into the Shareholder Support Agreement with CAEP, Pubco and AIR, which includes covenants to approve the Business Combination Agreement, the Jersey Merger and related transactions by special written resolution, to refrain from transferring AIR Ordinary Shares prior to Closing (subject to limited exceptions), and not to amend or revoke the approving special written resolution, together with other customary support and cooperation undertakings.

Date, Time and Place of the Extraordinary General Meeting of CAEP

The Meeting will be held on , 2026, at , Eastern Time, at the offices of DLA Piper LLP (US) at 1251 Avenue of the Americas, New York, New York 10020 and virtually via live audio webcast on the Internet at . You will be able to attend, vote your shares and submit questions during the Meeting via a live webcast available at .

You or your proxyholder will be able to attend and vote at the Meeting by visiting and using a control number assigned by CST. To register and receive access to the Meeting, registered shareholders and beneficial owners (those holding shares through a stock brokerage account or by a bank or other holder of record) will need to follow the instructions applicable to them provided in this proxy statement/prospectus. You will need the voter control number included on your proxy card in order to be able to vote your shares or submit questions during the Meeting. If you do not have a voter control number, you will be able to listen to the Meeting only and you will not be able to vote or submit questions during the Meeting.

Voting Power; Record Date

CAEP Shareholders will be entitled to vote or direct votes to be cast at the Meeting if they owned CAEP Ordinary Shares at the close of business on , 2026, which is the Record Date for the Meeting. CAEP Shareholders are entitled to one vote at the Meeting for each CAEP Ordinary Share held as of the Record Date. If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or nominee, you should contact your broker, bank or nominee to ensure that votes related to the shares you beneficially own are properly counted. In this regard, you must provide the broker, bank or nominee with instructions on how to vote your shares or, if you wish to attend the Meeting and vote, obtain a proxy from your broker, bank or nominee.

As of the close of business on the Record Date, there were 35,080,000 CAEP Ordinary Shares issued and outstanding, consisting of 28,180,000 CAEP Class A Ordinary Shares and 6,900,000 CAEP Class B Ordinary Shares. Of these shares, 27,600,000 were Public Shares, with the rest being held by the Sponsor.

Proxy Solicitation

Proxies may be solicited by mail, telephone or in person. CAEP has engaged Sodali & Co as the proxy solicitor to assist in the solicitation of proxies. If a CAEP Shareholder grants a proxy, it may still vote its shares itself if it revokes its proxy before the Meeting. A CAEP Shareholder may also change its vote by entering a new vote by Internet or telephone, submitting a later-dated proxy or attending and voting, virtually via the live webcast or in person, during the Meeting as described in the section of this proxy statement/prospectus entitled “Extraordinary General Meeting of CAEP Shareholders — Revoking Your Proxy.”

Quorum and Required Vote of CAEP Shareholders for Proposals at the Meeting

A quorum of CAEP Shareholders is necessary to hold a valid meeting. A quorum for the Meeting consists of the holders of a majority of the then issued and outstanding CAEP Ordinary Shares (whether in person or by proxy). As of the Record Date, the presence, in person or by proxy, of CAEP Shareholders holding 17,540,001 CAEP Ordinary Shares would be required to achieve a quorum at the Meeting. In addition to the CAEP Ordinary Shares held by the Sponsor, which represent approximately 21.3% of the issued and outstanding CAEP Ordinary Shares and which will count towards this quorum, CAEP will need only CAEP Shareholders holding 10,060,001 CAEP Ordinary Shares, or 36.4%, of the 27,600,000 Public Shares represented in person or by proxy at the Meeting to have a valid quorum.

To pass each of the Business Combination Proposal, the Nasdaq Proposal and the Adjournment Proposal requires an ordinary resolution of CAEP Shareholders, which requires the affirmative vote of a simple majority of the votes cast by, or on behalf of, the CAEP Shareholders as, being entitled to do so, vote in person or, where proxies are allowed, by proxy at the Meeting (assuming the presence of a quorum). To pass, the Merger Proposal requires a special resolution of CAEP Shareholders, which requires the affirmative vote of at least two-thirds of the votes cast by, or on behalf of, the CAEP Shareholders as, being entitled to do so, vote in person or, where proxies are allowed, by proxy at the Meeting (assuming the presence of a quorum). CAEP Shareholders are also being asked to approve, on a non-binding advisory basis, each of the Organizational Documents Proposals. Although the CAEP Board is asking CAEP Shareholders to approve each of the Organizational Documents Proposals on the non-binding advisory basis, regardless of the outcome of the non-binding advisory vote on each of the Organizational Documents Proposals, the A&R Pubco Articles will take effect upon the Closing if the Business Combination Proposal and the Merger Proposal are approved.

Assuming a quorum is established, a CAEP Shareholder’s failure to vote by proxy or to vote at the Meeting will have no effect on the Proposals. Abstentions and Broker non-votes, while considered present for the purposes of establishing a quorum, are not treated as votes cast and will have no effect on the approval or rejection of any of the Proposals.

The Sponsor has agreed to vote its 7,480,000 CAEP Ordinary Shares, representing approximately 21.3% of the issued and outstanding CAEP Ordinary Shares, in favor of each of the Proposals. As a result, with respect to each Proposal that requires approval of CAEP Shareholders by an ordinary resolution, in addition to the Sponsor’s CAEP Ordinary Shares, CAEP would need only 10,060,001, or approximately 36.4%, of the 27,600,000 Public Shares (assuming all issued and outstanding CAEP Ordinary Shares are voted at the Meeting), and only 1,290,001, or approximately 4.7%, of the 27,600,000 Public Shares (assuming only a majority of the issued and outstanding CAEP Ordinary Shares are voted at the Meeting), to be voted in favor of such Proposals in order to have such Proposals approved. With respect to each Proposal that requires approval of CAEP Shareholders by a special resolution, in addition to the Sponsor’s CAEP Ordinary Shares, CAEP would need only 15,906,667, or approximately 57.6%, of the 27,600,000 Public Shares (assuming all issued and outstanding CAEP Ordinary Shares are voted at the Meeting), and only 4,213,334, or approximately 15.3%, of the 27,600,000 Public Shares (assuming only a majority of the issued and outstanding CAEP Ordinary Shares are voted at the Meeting), to be voted in favor of such Proposals in order to have such Proposals approved.

Redemption Rights

Pursuant to the CAEP Memorandum and Articles, Public Shareholders may elect to have their Public Shares redeemed for cash at the applicable redemption price per share equal to the sum of (a) quotient obtained by dividing (i) the aggregate amount on deposit in the Trust Account as of two (2) business days prior to the Closing, including interest (net of taxes payable), by (ii) the total number of the then issued and outstanding Public Shares, plus (b) $0.15 per redeemed Public Share, which CAEP has agreed to pay, from funds provided by the Sponsor pursuant to the Sponsor Note, in respect of each redeemed Public Share. As of the date of this proxy statement/prospectus, based on funds in the Trust Account of approximately $281.9 million as of December 31, 2025, this would have amounted to approximately $10.36 per share (inclusive of $0.15 per redeemed Public Share to be funded pursuant to the Sponsor Note and which amount takes into account CAEP’s estimate of the amount that may be withdrawn to pay applicable taxes). Public Shareholders may exercise redemption rights whether or not they are holders as of the Record Date and whether or not such shares are voted at the Meeting and whether they vote for or against the Business Combination Proposal. Notwithstanding the foregoing, the CAEP Memorandum and Articles provides that a Public Shareholder, together with any Affiliate of such shareholder or any other person with whom such shareholder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will be restricted from redeeming its shares with respect to more than 15% of the Public Shares in the aggregate, without the prior consent of CAEP.

If a Public Shareholder exercises its redemption rights, then such Public Shareholder will be exchanging its Public Shares for cash and will not hold Pubco Ordinary Shares upon consummation of the Business Combination. Such a Public Shareholder will be entitled to receive cash for its Public Shares only if it properly demands redemption and delivers its shares (either physically or electronically) to CST in accordance with the procedures described herein. See the section titled “Extraordinary General Meeting of CAEP Shareholders — Redemption Rights” for the procedures to be followed if you wish to redeem your Public Shares for cash.

In connection with the CAEP IPO, the Sponsor and CAEP’s executive officers and directors agreed to waive any redemption rights with respect to any CAEP Ordinary Shares held by them in connection with the completion of the Business Combination. Such waivers are standard in transactions of this type and the Sponsor and CAEP’s executive officers and directors did not receive separate consideration for the waiver.

Appraisal or Dissenters’ Rights

No appraisal or dissenters’ rights are available to CAEP Shareholders in connection with the ordinary resolution to approve the Business Combination Proposal. However, in respect of the special resolution to approve the Merger Proposal, under Section 238 of the Companies Act, shareholders of a Cayman Islands exempted company ordinarily have a right to dissent to a statutory merger and if they so dissent, they are entitled to be paid the fair value of their shares, which if necessary, may ultimately be determined by the court. Therefore, CAEP Class A Record Holders have a right to dissent to the Cayman Merger. Please see the section titled “The Merger Proposal — Appraisal or Dissenters’ Rights” for additional information.

In addition, Public Shareholders are still entitled to exercise the rights of redemption as detailed in this proxy statement/prospectus and the redemption proceeds payable to Public Shareholders who exercise such redemption rights will represent the fair value of those shares. For a discussion about Public Shareholders’ redemption rights, please see “Extraordinary General Meeting of CAEP Shareholders — Redemption Rights.”

Proxy Solicitation

Proxies may be solicited by mail, telephone or in person. CAEP has engaged Sodali & Co as the proxy solicitor to assist in the solicitation of proxies. If a CAEP Shareholder grants a proxy, it may still vote its shares if it revokes its proxy before the Meeting. A CAEP Shareholder may also change its vote by entering a new vote by Internet or telephone, submitting a later-dated proxy or attending and voting, virtually via the live webcast or in person, during the Meeting as described in the section of this proxy statement/prospectus entitled “Extraordinary General Meeting of CAEP Shareholders — Revoking Your Proxy.”

Ownership of Pubco following the Business Combination

The following table summarizes the pro forma ownership of Pubco immediately following the Business Combination under: (1) the No Redemptions Scenario; (2) the 50% Redemptions Scenario; and (3) the 100% Redemptions Scenario, in each case, including the Sponsor Earnout Shares and the AIR Earnout Shares and excluding any Pubco Ordinary Shares issuable on exercise or settlement of the Assumed Conditional Awards and the Incentive Plan.

|

|

No Redemptions |

|

50% Redemptions |

|

100% Redemptions |

|

||||||

|

|

Shares |

|

% |

|

Shares |

|

% |

|

Shares |

|

% |

|

Public Shareholders |

|

27,600,000 |

|

15.1% |

|

13,800,000 |

|

8.2% |

|

— |

|

— |

|

Sponsor(1) |

|

4,111,178 |

|

2.3% |

|

4,111,178 |

|

2.4% |

|

4,111,178 |

|

2.7% |

|

AIR Shareholders (excluding the |

|

53,583,869 |

|

29.3% |

|

53,583,869 |

|

31.7% |

|

53,583,869 |

|

34.5% |

|

Kingsway Holders(4) |

|

97,385,657 |

|

53.3% |

|

97,385,657 |

|

57.7% |

|

97,385,657 |

|

62.8% |

|

Total |

|

182,680,704 |

|

100.0% |

|

168,880,704 |

|

100.0% |

|

155,080,704 |

|

100.0% |

|

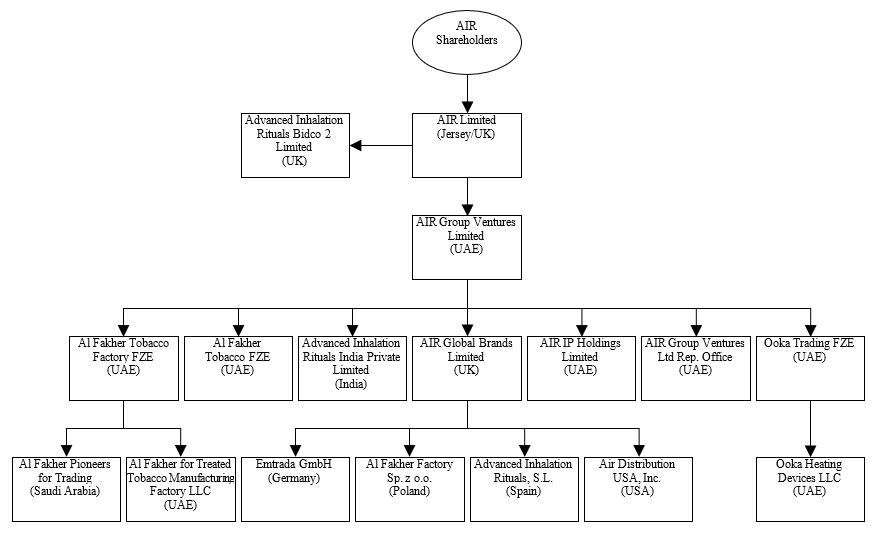

Organizational Structure

Prior to the Business Combination

The following diagram depicts the organizational structure of AIR and its principal and certain other subsidiaries, before the Business Combination.

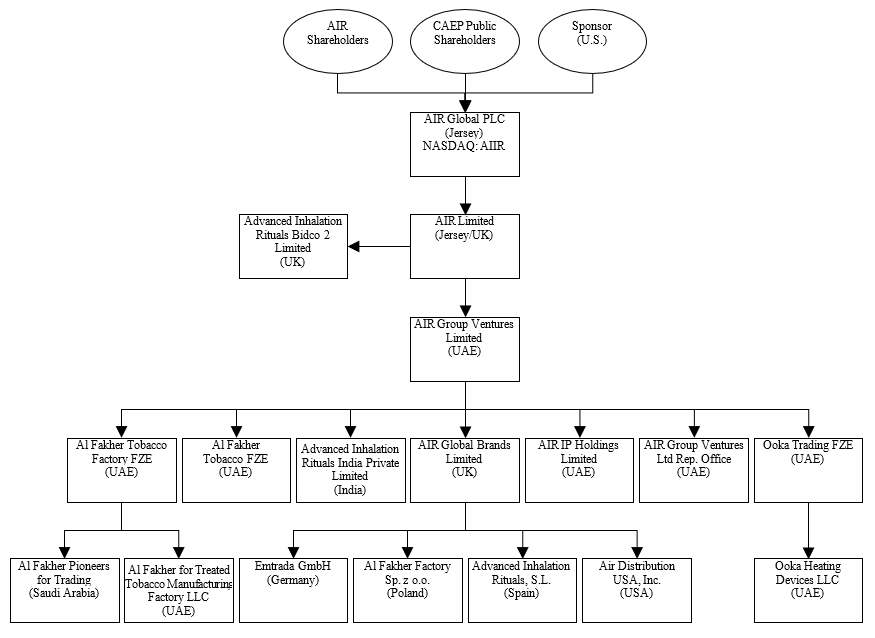

Following the Business Combination

The following diagram depicts the organizational structure of Pubco and its principal and certain other subsidiaries following the Business Combination.

Board of Directors of Pubco following the Business Combination.

At the consummation of the Business Combination, the directors of Pubco will be Faisal Bari, Stuart Brazier, Ian Fearon, Andrew Gundlach, Husam Manna, Reinhard Mieck, Tamir Saeed and Manuel Stotz, with Mr. Saeed serving as the chairman of the Pubco Board. Stuart Brazier is expected to serve as Chief Executive Officer, and Bassem Lotfy is expected to serve as Chief Financial Officer of Pubco. Please see “Management of Pubco After the Business Combination” for more information.

Recommendation to CAEP Shareholders

The CAEP Board has determined that the Business Combination Proposal and each of the other Proposals are in the commercial interests of CAEP and the CAEP Shareholders and unanimously recommends that CAEP Shareholders vote “FOR” the Business Combination Proposal, “FOR” the Merger Proposal, “FOR” each of the Organizational Documents Proposals, “FOR” the Nasdaq Proposal and “FOR” the Adjournment Proposal, if presented.

For more information about the CAEP Board’s recommendation and the Proposals, see the sections titled “Extraordinary General Meeting of CAEP Shareholders — Recommendation of the CAEP Board” and “The Business Combination Proposal — The CAEP Board’s Reasons for Approval of the Business Combination.”

The CAEP Board’s Reasons for the Approval of the Business Combination

The CAEP Board considered a variety of factors in connection with its evaluation of the Business Combination. In light of the complexity of those factors, the CAEP Board, as a whole, did not consider it practicable to, nor did it attempt to, quantify or otherwise assign relative weights to the specific factors it took into account in reaching its decision. Individual members of the CAEP Board may have given different weight to different factors. Certain information presented in this section is forward-looking in nature and, therefore, should be read in light of the factors discussed under “Cautionary Note Regarding Forward-Looking Statements.”

Neither the CAEP Board nor any committee thereof obtained a fairness opinion (or any similar report or appraisal) in determining whether to pursue the terms of the Business Combination (including the consideration to be received by CAEP Shareholders and AIR Shareholders). The independent directors of the CAEP Board did not retain an unaffiliated representative to act solely on behalf of the unaffiliated CAEP Shareholders to negotiate the terms of the Business Combination and/or prepare a report concerning the approval of the Business Combination.

Before reaching its decision, the CAEP Board was provided information regarding the findings from the due diligence conducted by its advisors, reviewed the analyses conducted by its management, representatives of the Sponsor and CAEP’s legal and financial advisors, and discussed the diligence findings at the November 5, 2025 special meeting. The due diligence conducted by CAEP’s management, CAEP’s legal and financial advisors and representatives of the Sponsor included:

The CAEP Board determined that pursuing a potential business combination with AIR would be an attractive opportunity for CAEP and CAEP Shareholders, which determination was based on a number of factors including, but not limited to, the following material factors:

In the course of its deliberations, in addition to the various other risks associated with the business of AIR, as described in the section entitled “Risk Factors” appearing elsewhere in this proxy statement/prospectus, the CAEP Board also considered a variety of uncertainties, risks and other potentially negative factors relevant to the Business Combination, including the following:

In addition to considering the factors described above, the CAEP Board also considered that:

Interests of CAEP Directors and Officers in the Business Combination

When Public Shareholders consider the recommendation of the CAEP Board in favor of approval of the Business Combination and other Proposals, Public Shareholders should keep in mind that the Sponsor and CEPT’s directors and officers have interests in the Proposals that are different from or in addition to (and which may conflict with), the interests of a Public Shareholder as a CAEP Shareholder. These interests include, among other things:

Anticipated Accounting Treatment of the Business Combination

The Business Combination will be accounted for as a capital reorganization in accordance with IFRS. Under this method of accounting, CAEP will be treated as the “acquired” company for financial reporting purposes. Accordingly, the Business Combination will be treated as the equivalent of AIR issuing shares in exchange for the net assets of CAEP as of the Cayman Effective Time, accompanied by a recapitalization of AIR as of the Jersey Effective Time. The net assets of CAEP are stated at historical cost, with no goodwill or other intangible assets recorded.

Please see the section entitled “Unaudited Pro Forma Condensed Combined Financial Information—Accounting for the Business Combination” elsewhere in this proxy statement/prospectus for additional information.

Regulatory Approvals

The Transactions were subject to the expiration or earlier termination of the applicable waiting period under the Hart-Scott-Rodino Antitrust Improvements Act (the “HSR Act”), under which the Transactions could not be completed until notification and report forms were filed with the Federal Trade Commission (“FTC”) and the Antitrust Division of the Department of Justice, and the applicable waiting period expired or was terminated. The required notification and report forms were filed, and the applicable waiting period under the HSR Act expired on January 21, 2026. Accordingly, the condition to Closing relating to the HSR Act has been satisfied.

The Business Combination is not subject to any additional federal or state regulatory requirement or approval, except for filings in Jersey and the Cayman Islands necessary to effectuate the Business Combination.

Description of Pubco Securities

If the Business Combination is successfully completed, AIR Shareholders and CAEP Shareholders will become Pubco shareholders, and their rights as Pubco shareholders will be governed by the A&R Pubco Articles and Jersey law. Please see the section entitled “Description of Pubco Securities” elsewhere in this proxy statement/prospectus for additional information.

Comparison of Shareholder Rights

There are certain differences in the rights of CAEP Shareholders prior to the Business Combination and the rights of Pubco shareholders after the Business Combination. Please see the section entitled “Comparison of Shareholder Rights” elsewhere in this proxy statement/prospectus for additional information.

Certain Information Relating to Pubco

Listing of Pubco Ordinary Shares on Nasdaq

Upon Closing, the Public Shares will be delisted from Nasdaq. Pubco intends to apply to list the Pubco Ordinary Shares on Nasdaq under the symbol “AIIR” upon Closing. Neither Pubco nor CAEP can assure you that the Pubco Ordinary Shares will be approved for listing on Nasdaq.

Emerging Growth Company; Foreign Private Issuer; Controlled Company

Following the Business Combination, Pubco will be an “emerging growth company” as defined in the JOBS Act. Pubco will remain an “emerging growth company” until the earliest to occur of (a) the last day of the fiscal year (i) following the fifth anniversary of the effective date of the registration statement of which this proxy statement/prospectus is a part, (ii) in which Pubco has total annual gross revenue of at least $1.235 billion or (iii) in which Pubco is deemed to be a large accelerated filer, which means the market value of Pubco Ordinary Shares held by non-affiliates exceeds $700 million as of the last business day of Pubco’s prior second fiscal quarter; and (b) the date on which Pubco issued more than $1.0 billion in non-convertible debt during the prior three-year period. Pubco intends to take advantage of exemptions from various reporting requirements that are applicable to most other public companies, whether or not they are classified as “emerging growth companies,” including, but not limited to, an exemption from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that Pubco’s independent registered public accounting firm provide an attestation report on the effectiveness of its internal control over financial reporting.

As a “foreign private issuer,” Pubco will be subject to different U.S. securities law rules than domestic U.S. issuers. The rules governing the information that Pubco must disclose differ from those governing U.S. corporations pursuant to the Exchange Act. For example, Pubco will be exempt from the rules under the Exchange Act prescribing the furnishing and content of proxy statements to shareholders. In addition, as a “foreign private issuer,” Pubco’s officers and directors and holders of more than 10% of the issued and outstanding Pubco Ordinary Shares, will be exempt from the rules under the Exchange Act requiring insiders to report purchases and sales of ordinary shares as well as from Section 16 short swing profit reporting and liability.

After the Closing, the Kingsway Holders will own at least 53.3% of the equity interests of Pubco, subject to adjustments based on AIR Limited shares outstanding immediately prior to the Jersey Closing and based on the assumptions set forth elsewhere in this proxy statement/prospectus. As a result, Pubco will be a “controlled company” within the meaning of the rules of Nasdaq. Under Nasdaq corporate governance standards, a company of which more than 50% of the voting power is held by an individual, group or another company is a “controlled company” and may elect not to comply with certain corporate governance standards, including (i) the requirement that a majority of the board of directors consist of independent directors, (ii) the requirement that Pubco has a compensation committee that is composed entirely of independent directors and (iii) the requirement that Pubco’s director nominations be made, or recommended to the full Pubco Board, by the Pubco independent directors or by a nomination committee that consists entirely of independent directors and that Pubco adopt a written charter or board resolution addressing the nominations process. Pubco does not intend to take advantage of the foregoing exemptions. However, if Pubco decides to take advantage of one or more of the foregoing exemptions, Pubco shareholders may not have the same protections afforded to shareholders of companies that are subject to all of the Nasdaq corporate governance requirements. In the event that Pubco ceases to be a “controlled company,” it will be required to comply with these provisions within the transition periods specified in Nasdaq corporate governance rules. See “Risk Factors— Risks Related to Being a Public Company— As a ‘controlled company’ within the meaning of the rules of Nasdaq, we will qualify for certain exemptions from Nasdaq corporate governance requirements” for additional information.

Sources and Uses of Funds for the Business Combination

The following table summarizes the sources and uses for funding the Business Combination. Where actual amounts are not known or knowable, the figures below represent Pubco’s and CAEP’s good faith estimate of such amounts.

|

|

|

Assuming No Redemptions Scenario |

|

|

Assuming 50% Redemptions Scenario |

|

|

Assuming 100% Redemptions Scenario |

|

|

|

|

(in $ millions) |

|

||||||

Sources |

|

|

|

|

|

|

|

|

|

|

Proceeds from Trust Account(1) |

|

$ |

281.9 |

|

$ |

281.9 |

|

$ |

281.9 |

|

Uses |

|

|

|

|

|

|

|

|

|

|

Estimated fees and expenses |

|

$ |

48.9 |

|

$ |

46.9 |

|

$ |

46.9 |

|

Redemptions |

|

$ |

0.0 |

|

$ |

140.9 |

|

$ |

281.9 |

|

Cash to Balance Sheet |

|

$ |

233.0 |

|

$ |

94.1 |

|

$ |

(46.9 |

) |

(1) As based on Trust account balance as of December 31, 2025.

Parties to the Business Combination

CAEP

CAEP is a blank check company incorporated in the Cayman Islands on November 11, 2020 as a Cayman Islands exempted company for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or other similar business combination, involving one or more businesses or assets.

CAEP Class A Ordinary Shares are currently listed on the Nasdaq Global Market under the ticker symbol “CAEP.” Upon the Closing, CAEP Class A Ordinary Shares will be delisted from Nasdaq.

CAEP completed the CAEP IPO of 27,600,000 CAEP Class A Ordinary Shares on June 27, 2025, generating gross proceeds to CAEP of $276,000,000. Simultaneously with the closing of the CAEP IPO, CAEP completed the sale to the Sponsor of 580,000 CAEP Private Placement Shares at a purchase price of $10.00 per CAEP Private Placement Share, generating gross proceeds to CAEP of $5,800,000. Following the closing of the CAEP IPO and the CAEP Private Placement, a total of $276,000,000, comprised of the net proceeds from the CAEP IPO and the CAEP Private Placement, was placed in the Trust Account. As of December 31, 2025, the Trust Account balance was approximately $282,000,000. Since the CAEP IPO, CAEP’s activity has been limited to efforts toward locating and completing a suitable business combination.

The mailing address of CAEP’s principal executive office is 110 East 59th Street, New York, New York 10022, and its telephone number is (212) 938-5000. As part of the Business Combination, Cayman Merger Sub will merge with and into CAEP, with CAEP continuing as the surviving entity and a direct, wholly owned subsidiary of Pubco.

AIR

AIR is a private limited company incorporated under the laws of Jersey on September 20, 2019. AIR is a leading global producer of branded flavored molasses by sales volume and market share. For the year ended December 31, 2024, AIR has an estimated global market share of approximately 36% to 44% based on sales volume in the markets in which it operates (excluding Russia and Turkey) as of December 31, 2024, according to the 2025 Market Assessment Report. AIR considers itself to be the only global player, with its sales volume surpassing the combined share of its next four competitors, who remain regional or local, as of December 31, 2024, according to AIR’s internal estimates. AIR produces and sells branded flavored molasses through direct-to-consumer, distributor and licensed retail channels in more than 90 markets, serving both at-home consumers and HoReCa channels, including lounges and other hospitality venues. AIR’s portfolio includes established flavored molasses brands such as Al Fakher, Shisha Kartel, Zødiac, NameLess and a newer brand called Kloud King. AIR’s portfolio also includes innovation-led inhalation devices, such as OOKA and VANT, and a collaboration between Snoop Dogg and Al Fakher. During the years ended December 31, 2025 and 2024, AIR generated revenue of $399.7 million and $376.6 million, respectively, operating profit of $83.2 million and $91.0 million, respectively, and Adjusted EBITDA of $139.3 million and $129.5 million, respectively.

The mailing address of AIR’s principal executive office is Festival Office Tower, Dubai Festival City, 7th Floor, Dubai, United Arab Emirates.

Pubco

Pubco is a private limited company incorporated under the laws of Jersey on October 28, 2025. Pubco will be converted to a public limited company incorporated under the laws of Jersey prior to consummation of the Business Combination. To date, Pubco has not conducted any material activities other than those incidental to its formation, the incorporation of the Cayman Merger Sub and Jersey Merger Sub and the pending Business Combination and only has nominal assets consisting of cash and cash equivalents.

Pubco intends to apply to list the Pubco Ordinary Shares on Nasdaq under the symbol “AIIR,” upon the Closing.

The mailing address of Pubco’s registered office is 15 Esplanade, St. Helier, JE1 1RB, Jersey. After the consummation of the Business Combination, Pubco’s principal executive office will be that of AIR, located at Festival Office Tower, Dubai Festival City, 7th Floor, Dubai, United Arab Emirates.

Cayman Merger Sub

Cayman Merger Sub is an exempted company incorporated with limited liability in the Cayman Islands and wholly owned subsidiary of Pubco that was incorporated on October 29, 2025 to facilitate the consummation of the Business Combination. Cayman Merger Sub will be directly owned by Pubco prior to and on the Closing Date. As part of the Business Combination, Cayman Merger Sub will merge with and into CAEP, with CAEP continuing as the surviving entity and a direct, wholly owned subsidiary of Pubco.

The mailing address of Cayman Merger Sub’s registered office is Walkers Corporate Limited, 190 Elgin Avenue, George Town, Grand Cayman KY1-9008, Cayman Islands.

Jersey Merger Sub

Jersey Merger Sub is a private limited company incorporated under the laws of Jersey and wholly owned subsidiary of Pubco that was incorporated on October 28, 2025 to facilitate the consummation of the Business Combination. Jersey Merger Sub will be directly owned by Pubco prior to and on the Closing Date. As part of the Business Combination, Jersey Merger Sub will merge with and into AIR, with AIR continuing as the surviving entity and a direct, wholly owned subsidiary of Pubco.

The mailing address of Jersey Merger Sub’s registered office is 15 Esplanade, St. Helier, JE1 1RB, Jersey.

The Business Combination Agreement

Overview

On November 7, 2025, CAEP, AIR, Pubco, Cayman Merger Sub and Jersey Merger Sub entered into the Business Combination Agreement, which contains customary representations and warranties, covenants, closing conditions and other terms relating to the Transactions.

In accordance with the terms and subject to the conditions of the Business Combination Agreement, the parties to the Business Combination Agreement have agreed that, in connection with the Closing, Cayman Merger Sub will merge with and into CAEP, with CAEP continuing as the surviving company and a wholly owned direct subsidiary of Pubco, and, separately and immediately following the Cayman Effective Time, Jersey Merger Sub will merge with and into AIR, with AIR continuing as the surviving company and a wholly owned direct subsidiary of Pubco.

For more information about the Transactions contemplated in the Business Combination Agreement, please see the section entitled “The Business Combination Agreement and Ancillary Documents.” The Business Combination Agreement is incorporated by reference into this proxy statement/prospectus, a copy of which is attached to this proxy statement/prospectus as Annex A.

Effects of the Merger

At the Cayman Effective Time, all the property, rights, privileges, agreements, powers and franchises, debts, liabilities, duties and obligations of CAEP and Cayman Merger Sub shall become the property, rights, privileges, agreements, powers and franchises, debts, liabilities, duties and obligations of the Surviving Cayman Company (including all rights and obligations with respect to the Trust Account), which shall include the assumption by the Surviving Cayman Company of any and all agreements, covenants, duties and obligations of CAEP and Cayman Merger Sub set forth in the Business Combination Agreement to be performed after the Cayman Effective Time.

At the Jersey Effective Time, (i) all property and rights to which each of AIR and Jersey Merger Sub are entitled immediately before the Jersey Merger is completed become the property and rights of the Surviving Jersey Company, (ii) the Surviving Jersey Company becomes subject to all criminal and civil liabilities, and all contracts, debts and other obligations, to which each of AIR and Jersey Merger Sub were subject immediately before the Jersey Merger is completed and (iii) all actions and other legal proceedings, which, immediately before the Jersey Merger is completed, are pending by or against any of AIR and Jersey Merger Sub may be continued by or against the Surviving Jersey Company, which shall include the assumption by the Surviving Jersey Company of any and all agreements, covenants, duties and obligations of AIR and Jersey Merger Sub set forth in the Business Combination Agreement to be performed after the Jersey Effective Time.

Conditions to the Closing

Under the Business Combination Agreement, the Closing is subject to customary and other conditions (subject to the parties’ ability to waive such conditions as permitted by the Business Combination Agreement), including, among other things (for the purposes of this section, defined terms have the meanings given to such terms in the Business Combination Agreement):

The obligations of the parties to the Business Combination Agreement to consummate the Business Combination are subject to additional conditions, as described more fully below in the section entitled “The Business Combination Agreement and Ancillary Documents — The Business Combination Agreement — Conditions to Complete the Business Combination.”

Related Agreements

A&R Registration Rights Agreement

The Business Combination Agreement contemplates that, at Closing, Pubco will enter into the A&R Registration Rights Agreement with the Sponsor and certain AIR Shareholders, substantially in the form attached to this proxy statement/prospectus as Annex D, which supersedes and replaces the registration rights agreement that was entered into by CAEP and the Sponsor in connection with the CAEP IPO, pursuant to which Pubco will agree to register for resale the Pubco Ordinary Shares that are held by the Sponsor and the AIR Shareholders at Closing pursuant to a shelf registration statement to be filed with the SEC no later than ninety (90) days following the date of Closing. Pursuant to the A&R Registration Rights Agreement, the Sponsor and certain AIR Shareholders will also have certain other registration rights, including unlimited demand and piggy-back rights, subject to cooperation and cut back provisions with respect to Pubco Ordinary Shares held by such parties at Closing.

The A&R Registration Rights Agreement amends and restates the registration rights agreement that was entered into by CAEP and the Sponsor in connection with the CAEP IPO.

Sponsor Support Agreement

Concurrently with the execution of the Business Combination Agreement, CAEP, the Sponsor, Pubco and AIR entered into the Sponsor Support Agreement, pursuant to which, among other things, the Sponsor agreed (a) to vote its Pubco Ordinary Shares in favor of the Proposals, (b) vote its Pubco Ordinary Shares against any Acquisition Proposal or Alternative Transaction, (c) to comply with the restrictions imposed by the Insider Letter and (d) to waive the anti-dilution rights of the issued and outstanding CAEP Class B Ordinary Shares set forth in the CAEP Memorandum and Articles. The Sponsor also agreed that, subject to the Closing, it will (x) surrender, for no consideration, 3,400,000 CAEP Class B Ordinary Shares to be cancelled by CAEP and (y) not transfer 1,500,000 of the Pubco Ordinary Shares that it will receive in exchange for its CAEP Founder Shares until the occurrence of certain release events.

The CAEP Board has determined that the Business Combination Proposal and each of the other Proposals are in the commercial interests of CAEP and the CAEP Shareholders and unanimously recommends that CAEP Shareholders vote “FOR” the Business Combination Proposal, “FOR” the Merger Proposal, “FOR” each of the Organizational Documents Proposals, “FOR” the Nasdaq Proposal and “FOR” the Adjournment Proposal, if presented.

The CAEP Board considered a variety of factors in connection with its evaluation of the Business Combination. In light of the complexity of those factors, the CAEP Board, as a whole, did not consider it practicable to, nor did it attempt to, quantify or otherwise assign relative weights to the specific factors it took into account in reaching its decision. Individual members of the CAEP Board may have given different weight to different factors. Certain information presented in this section is forward-looking in nature and, therefore, should be read in light of the factors discussed under “Cautionary Note Regarding Forward-Looking Statements.”

Neither the CAEP Board nor any committee thereof obtained a fairness opinion (or any similar report or appraisal) in determining whether to pursue the terms of the Business Combination (including the consideration to be received by CAEP Shareholders and AIR Shareholders). The independent directors of the CAEP Board did not retain an unaffiliated representative to act solely on behalf of the unaffiliated CAEP Shareholders to negotiate the terms of the Business Combination and/or prepare a report concerning the approval of the Business Combination.

Before reaching its decision, the CAEP Board was provided information regarding the findings from the due diligence conducted by its advisors, reviewed the analyses conducted by its management, representatives of the Sponsor and CAEP’s legal and financial advisors, and discussed the diligence findings at the November 5, 2025 special meeting. The due diligence conducted by CAEP’s management, CAEP’s legal and financial advisors and representatives of the Sponsor included:

The CAEP Board determined that pursuing a potential business combination with AIR would be an attractive opportunity for CAEP and CAEP Shareholders, which determination was based on a number of factors including, but not limited to, the following material factors:

In the course of its deliberations, in addition to the various other risks associated with the business of AIR, as described in the section entitled “Risk Factors” appearing elsewhere in this proxy statement/prospectus, the CAEP Board also considered a variety of uncertainties, risks and other potentially negative factors relevant to the Business Combination, including the following:

In addition to considering the factors described above, the CAEP Board also considered that:

Set forth below is a summary of the terms and amount of the consideration received or to be received by the Sponsor and its Affiliates in connection with the Business Combination, the amount of securities issued or to be issued by Pubco to the Sponsor and the price paid or to be paid or consideration provided for such securities or any related financing transaction.

Entity |

|

|

Interest in Securities/Other Consideration |

|

|

Price Paid or to be Paid or |

Sponsor |

|

|

The Sponsor will receive 3,500,000 Pubco Ordinary Shares in exchange for its 3,500,000 CAEP Founder Shares (after accounting for the surrender by the Sponsor and cancellation of 3,400,000 of the 6,900,000 CAEP Founder Shares it holds today immediately prior to, and subject to the consummation of, the Cayman Merger); provided that 1,500,000 of such Pubco Ordinary Shares will be subject to the Sponsor Earnout Conditions |

|

|

$25,000 paid to purchase the 6,900,000 CAEP Founder Shares |

|

|

|

The Sponsor will receive 580,000 Pubco Ordinary Shares in exchange for its 580,000 CAEP Private Placement Shares |

|

|

$5,800,000 paid to purchase the 580,000 CAEP Private Placement Shares |

|

|

|

Additional Pubco Ordinary Shares in exchange for CAEP Class A Ordinary Shares and/or cash |

|

|

Amounts outstanding at Closing under (a) the Sponsor Loan will be repaid by the issuance of CAEP Class A Ordinary Shares at $10.00 per share and (b) all other loans (other than the Sponsor Loan) will be repaid in cash |

CF&Co. |

|

|

$10,380,000 in cash

Approximately $24.235 million in cash, being equal to 1.5% of the enterprise value of AIR less $2 million, which fee will be reduced by an amount equal to the lesser of (i) $1.98 million and (ii) the product of: (x) 5.5%, (y) $10.00 and (z) the number of Public Shares redeemed in connection with the Transactions |

|

|

Services pursuant to the Business Combination Marketing Agreement

Services pursuant to the CF&Co. M&A Engagement Letter

|

Redemption Rights

Pursuant to the CAEP Memorandum and Articles, Public Shareholders may elect to have their Public Shares redeemed for cash at the applicable redemption price per share equal to the sum of (a) quotient obtained by dividing (i) the aggregate amount on deposit in the Trust Account as of two (2) business days prior to the Closing, including interest (net of taxes payable), by (ii) the total number of the then issued and outstanding Public Shares, plus (b) $0.15 per redeemed Public Share, which CAEP has agreed to pay, from funds provided by the Sponsor pursuant to the Sponsor Note, in respect of each redeemed Public Share. As of the date of this proxy statement/prospectus, based on funds in the Trust Account of approximately $281.9 million as of December 31, 2025, this would have amounted to approximately $10.36 per share (inclusive of $0.15 per redeemed Public Share to be funded pursuant to the Sponsor Note and which amount takes into account CAEP’s estimate of the amount that may be withdrawn to pay applicable taxes). Public Shareholders may exercise redemption rights whether or not they are holders as of the Record Date and whether or not such shares are voted at the Meeting and whether they vote for or against the Business Combination Proposal. Notwithstanding the foregoing, the CAEP Memorandum and Articles provides that a Public Shareholder, together with any Affiliate of such shareholder or any other person with whom such shareholder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will be restricted from redeeming its shares with respect to more than 15% of the Public Shares in the aggregate, without the prior consent of CAEP.

If a Public Shareholder exercises its redemption rights, then such Public Shareholder will be exchanging its Public Shares for cash and will not hold Pubco Ordinary Shares upon consummation of the Business Combination. Such a Public Shareholder will be entitled to receive cash for its Public Shares only if it properly demands redemption and delivers its shares (either physically or electronically) to CST in accordance with the procedures described herein. See the section titled “Extraordinary General Meeting of CAEP Shareholders — Redemption Rights” for the procedures to be followed if you wish to redeem your Public Shares for cash.

In connection with the CAEP IPO, the Sponsor and CAEP’s executive officers and directors agreed to waive any redemption rights with respect to any CAEP Ordinary Shares held by them in connection with the completion of the Business Combination. Such waivers are standard in transactions of this type and the Sponsor and CAEP’s executive officers and directors did not receive separate consideration for the waiver.

The following table illustrates the changes in NTBV and dilution to non-redeeming Public Shareholders under: (1) the No Redemptions Scenario; (2) the 50% Redemptions Scenario; and (3) the 100% Redemptions Scenario (in thousands, except share and per share data).

|

|

|

No |

|

|

50% |

|

|

100% |

|

Initial public offering price per share |

|

$ |

10.00 |

|

$ |

10.00 |

|

$ |

10.00 |

|

As adjusted NTBV(1) |

|

$ |

243,340 |

|

$ |

102,308 |

|

$ |

(40,704) |

|

As adjusted total shares(2) |

|

$ |

31,711,178 |

|

$ |

17,911,178 |

|

$ |

4,111,178 |

|

Adjusted NTBV per share as of December 31,2025 |

|

$ |

7.67 |

|

$ |

5.71 |

|

$ |

(9.90) |

|

Dilution per share to the non-redeeming Public Shareholders |

|

$ |

2.33 |

|

$ |

4.29 |

|

$ |

19.90 |

|

Change in NTBV per share attributable to non-redeeming Public |

|

$ |

(7.84) |

|

$ |

(5.99) |

|

$ |

9.10 |

|

The following table illustrates the NTBV per share and the change in NTBV per share, as adjusted, following the Closing but excluding the other effects of the Business Combination, while giving effect to probable or consummated transactions that are material and other material effects on NTBV per share. These are presented in relation to the offering price per Public Share in the CAEP IPO as set forth as follows under each of the three redemption scenarios: (1) the No Redemptions Scenario; (2) the 50% Redemptions Scenario; and (3) the 100% Redemptions Scenario (in thousands, except share and per share data) assuming various sources of material probable dilution (but excluding the direct effects of the Business Combination transaction itself).

If you acquired Public Shares in the CAEP IPO, your ownership interest will be immediately diluted to the extent of the difference between the $10.00 price per share sold in the CAEP IPO and the NTBV per share, as adjusted, of the Pubco Ordinary Shares immediately after consummation of the Business Combination.

|

|

Assuming No Redemptions Scenario |

|

Assuming 50% Redemptions Scenario |

|

Assuming 100% Redemptions Scenario |

||||

Public Shareholders |

|

|

27,600,000 |

|

|

13,800,000 |

|

|

— |

|

Sponsor |

|

|

7,480,000 |

|

|

7,480,000 |

|

|

7,480,000 |

|

Total CAEP Ordinary Shares as of December 31, 2025 |

|

|

35,080,000 |

|

|

21,280,000 |

|

|

7,480,000 |

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted for: |

|

|

|

|

|

|

|

|

|

|

CAEP Class B Ordinary Shares forfeited by Sponsor |

|

|

(3,400,000) |

|

|

(3,400,000) |

|

|

(3,400,000) |

|

CAEP Class A Ordinary Shares to be issued in repayment of |

|

|

31,178 |

|

|

31,178 |

|

|

31,178 |

|

Total CAEP Ordinary Shares outstanding as of |

|

|

31,711,178 |

|

|

17,911,178 |

|

|

4,111,178 |

|

NTBV as of December 31, 2025 (1) |

|

$ |

(5,957) |

|

$ |

(5,957) |

|

$ |

(5,957) |

|

Adjusted for(2): |

|

|

|

|

|

|

|

|

|

|

Reclassification of CAEP Class A Ordinary Shares subject to |

|

|

286,024 |

|

|

143,012 |

|

|

— |

|

Transaction expenses to be paid by CAEP |

|

|

(37,039) |

|

|

(35,059) |

|

|

(35,059) |

|

Repayment of the Sponsor Loan in CAEP Class A Ordinary |

|

|

312 |

|

|

312 |

|

|

312 |

|

NTBV as of December 31, 2025, as adjusted |

|

$ |

243,340 |

|

$ |

102,308 |

|

$ |

(40,704) |

|

|

|

|

|

|

|

|

|

|

|

|

NTBV per share as of December 31, 2025, as adjusted |

|

$ |

7.67 |

|

$ |

5.71 |

|

$ |

(9.90) |

|

Dilution(3) |

|

$ |

2.33 |

|

$ |

4.29 |

|

$ |

19.90 |

|