Exhibit 99.1

ANNUAL INFORMATION FORM

For the Year Ended December 31, 2025

(Dated March 26, 2026)

SOLARIS RESOURCES INC.

Neuhofstrasse 5A Baar

6340 Switzerland

TABLE OF CONTENTS

| Item 1: | PRELIMINARY NOTES | 1 | |

| 1.1 | Effective Date of Information | 1 | |

| 1.2 | Financial Statements and Management Discussion and Analysis | 1 | |

| 1.3 | Currency | 1 | |

| 1.4 | Scientific and Technical Information | 1 | |

| Item 2: | CAUTIONARY NOTES | 1 | |

| 2.1 | Cautionary Note Regarding Forward-Looking Statements and Forward-Looking Information | 1 | |

| 2.2 | Cautionary Note to United States Investors Regarding Classification of Mineral Resource Estimates | 2 | |

| Item 3: | CORPORATE STRUCTURE | 3 | |

| 3.1 | Name, Address and Incorporation | 3 | |

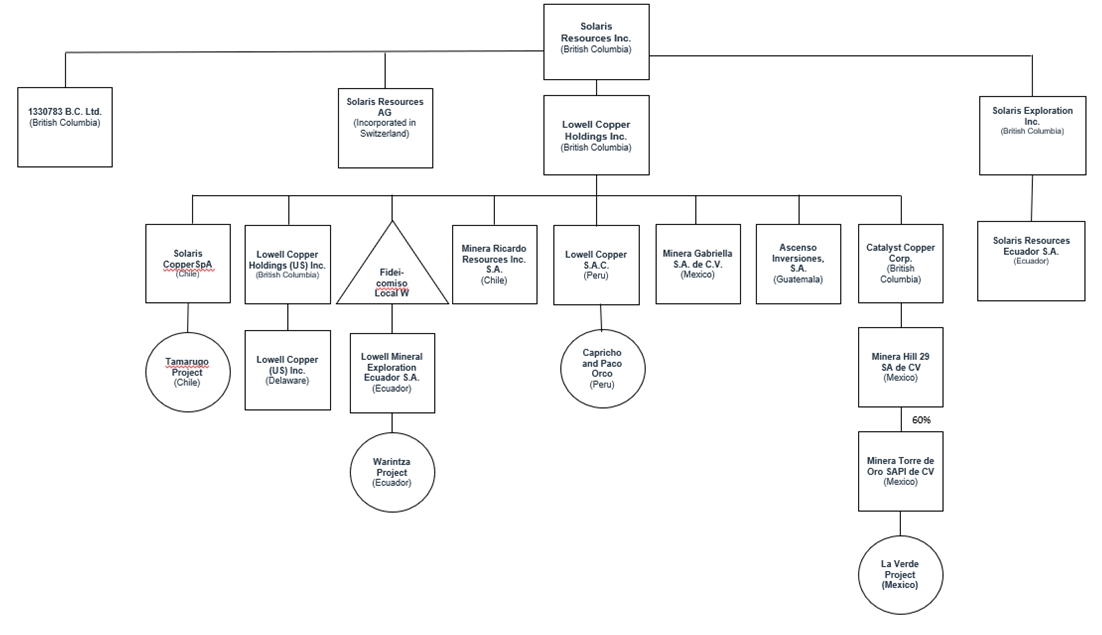

| 3.2 | Inter-corporate Relationships | 3 | |

| Item 4: | GENERAL DEVELOPMENT OF THE BUSINESS | 4 | |

| 4.1 | Three Year History | 4 | |

| Item 5: | DESCRIPTION OF THE BUSINESS | 6 | |

| Item 6: | MATERIAL MINERAL PROJECT | 7 | |

| 6.1 | Current Technical Report | 7 | |

| Item 7: | RISK FACTORS | 28 | |

| Item 8: | DIVIDENDS | 44 | |

| Item 9: | DESCRIPTION OF CAPITAL STRUCTURE | 44 | |

| Item 10: | MARKET FOR SECURITIES | 45 | |

| 10.1 | Trading Price and Volume | 45 | |

| Item 11: | Prior sales | 45 | |

| Item 12: | ESCROWED SECURITIES AND SECURITIES SUBJECT TO CONTRACTUAL RESTRICTION ON TRANSFER | 45 | |

| Item 13: | DIRECTORS AND OFFICERS | 46 | |

| 13.1 | Name, Occupation and Security Holding | 46 | |

| 13.2 | Cease Trade Orders, Bankruptcies, Penalties or Sanctions | 47 | |

i

| 13.3 | Conflicts of Interest | 47 | |

| Item 14: | PROMOTERS | 48 | |

| Item 15: | LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 48 | |

| 15.1 | Legal Proceedings | 48 | |

| 15.2 | Regulatory Actions | 48 | |

| Item 16: | INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 48 | |

| Item 17: | TRANSFER AGENT AND REGISTRAR | 48 | |

| Item 18: | MATERIAL CONTRACTS | 49 | |

| Item 19: | INTERESTS OF EXPERTS | 49 | |

| 19.1 | Names of Experts | 49 | |

| 19.2 | Interests of Experts | 49 | |

| Item 20: | AUDIT COMMITTEE | 50 | |

| 20.1 | The Audit Committee Charter | 50 | |

| 20.2 | Composition of Audit Committee | 50 | |

| 20.3 | Relevant Education and Experience | 50 | |

| 20.4 | Reliance on Certain Exemptions | 51 | |

| 20.5 | Audit Committee Oversight | 51 | |

| 20.6 | Pre-Approval Policies and Procedures | 51 | |

| 20.7 | External Audit Service Fees (By Category) | 51 | |

| Item 21: | ADDITIONAL INFORMATION | 51 | |

| SCHEDULE “A” AUDIT COMMITTEE CHARTER | A-1 | ||

ii

| Item 1: | PRELIMINARY NOTES |

| 1.1 | Effective Date of Information |

References to “Solaris Resources Inc.”, “Solaris”, “Solaris Resources”, “SLS”, the “Company”, “its”, “our” and “we”, or related terms in this Annual Information Form (“AIF”), refer to Solaris Resources Inc. and include, where the context requires, its subsidiaries.

All information contained in this AIF is as at March 26, 2026, unless otherwise stated.

| 1.2 | Financial Statements and Management Discussion and Analysis |

This AIF should be read in conjunction with the Company’s audited consolidated annual financial statements for the years ended December 31, 2025 and December 31, 2024 (the “Financial Statements”), as well as the accompanying Management’s Discussion and Analysis (“MD&A”) for such periods. The Financial Statements and MD&A are available on the System for Electronic Data Analysis and Retrieval + (“SEDAR+”) at www.sedarplus.ca and on Electronic Data Gathering, Analysis, and Retrieval (“EDGAR”) at www.sec.gov.

| 1.3 | Currency |

All references to “$” or “dollars” in this AIF are to United States dollars, unless otherwise expressly stated. References to “C$” are to Canadian dollars.

| 1.4 | Scientific and Technical Information |

Unless otherwise indicated, scientific and technical information in this AIF has been reviewed and approved by Jorge Fierro, M.Sc., DIC, PG, Vice President Exploration of Solaris and a “Qualified Person” (“QP”) as defined in National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”).

| Item 2: | CAUTIONARY NOTES |

| 2.1 | Cautionary Note Regarding Forward-Looking Statements and Forward-Looking Information |

Certain information contained in this AIF constitutes forward-looking statements. All statements, other than statements of historical facts, are forward-looking statements, including but not limited to estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur; exploration and development plans; timing of such exploration plans, and potential results of such exploration plans; financial capacity and availability of capital; statements regarding perceived merit of properties, budgets, work programs, use of available funds, and operational information; the Company’s intention to retain all future earnings and other cash resources for the future development and operation of its business; the Company’s intention not to declare or pay any cash dividends in the foreseeable future; the estimation of Mineral Resources and Mineral Reserves; the success of the synergies and catalysts related to prior transactions, in particular but not limited to, the Funding Package; the ability of the Company to satisfy the conditions precedent to the advancement of the remaining amount under the Funding Package (as defined below); the realization of Mineral Reserve estimates, the timing and amount of potential future production; and the Company’s internal controls over financial reporting (“ICFR”), including its ability to remedy the identified material weakness, as well as any potential future material weaknesses. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “is expected”, “scheduled”, “estimates”, “intends”, “anticipates”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, or “might” occur or be achieved. Any such forward-looking statements are based, in part, on assumptions and factors that may change, thus causing actual results or achievements to differ materially from those expressed or implied by the forward-looking statements. Such factors and assumptions may include, but are not limited to: assumptions concerning copper, gold and other base and precious metal prices; cut-off grades; accuracy of Mineral Resource estimates and resource modeling; timing and reliability of sampling and assay data; representativeness of mineralization; timing and accuracy of metallurgical test work; anticipated political and social conditions; expected government policy, including reforms; ability to successfully raise additional capital; assumptions regarding obtaining required approvals; assumptions regarding Solaris’ ability to satisfy the conditions precedent to the advancement of the remaining amount under the Funding Package; and other assumptions used as a basis for preparation of the Technical Report (as defined below).

1

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Such risks and other factors include, among others, and without limitation: the ability to raise funding to continue exploration, development and mining activities; Funding Package; financing arrangements; global economic conditions; limited supplies, supply chain disruptions and inflation; operating cash flow; uncertainty of future revenues or of a return on investment; estimation risk in Mineral Resources and Mineral Reserves; uncertainty relating to Inferred Mineral Resources; speculative nature of mineral exploration and development; risks from international operations; risks associated with an emerging and developing market; relationships with, and claims by, local communities and Indigenous Groups; geopolitical risk; risks related to obtaining future environmental licenses for exploitation; permitting risk; Ecuadorian constitutional court rulings suspending licenses; anti-mining sentiment; failure to comply strictly with applicable laws, regulations and local practices; pressure from artisanal and illegal miners; risks associated with mining, exploration and development; land title risk; surface rights and access risks; changes in laws and policies regulating international trade; international conflicts; global outbreaks and contagious diseases; fraud and corruption; ethics and business practices; future legal proceedings; tax regime in Ecuador; mineral assets being located outside Canada and held indirectly through foreign affiliates; commodity price risk; exchange rate fluctuations; joint ventures; property commitments; infrastructure; water management; properties located in remote areas; lack of availability of resources; dependence on highly skilled personnel; competition; significant shareholders; reputational risk; conflicts of interest; uninsurable risks; information systems; artificial intelligence (“AI”), public company obligations; reliability of financial reporting and financial statement preparation; foreign subsidiary operations may impact the Company’s ability to fund operations efficiently; price fluctuation of the Company’s common shares (the “Common Shares”); value of the Common Shares; future sales of Common Shares by existing shareholders; costs of land reclamation; measures to protect endangered species; environmental risks and hazards and changes in climate conditions; differences in U.S. and Canadian reporting of Mineral Reserves and Resources; the Company’s “foreign private issuer” status; claims under U.S. securities laws, as well as those factors discussed in ITEM 7: “Risk Factors” below.

Although the Company has attempted to identify important factors and risks that could affect the Company and might cause actual actions, events or results to differ, perhaps materially, from those described in forward-looking statements, there may be other factors and risks not identified herein that cause actions, events or results not to occur as projected, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking statements in this AIF speak only as of the date hereof. The Company does not undertake any obligation to release publicly any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except as required by law.

| 2.2 | Cautionary Note to United States Investors Regarding Classification of Mineral Resource Estimates |

This AIF was prepared in accordance with Canadian standards for reporting of Mineral Resource estimates, which differ from United States standards. In particular, and without limiting the generality of the foregoing, the technical and scientific information contained and incorporated by reference in this AIF was prepared in accordance with NI 43-101 under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum Standards for Mineral Resources and Mineral Reserves, Definitions and Guidelines (“CIM Definition Standards”), which differs from the standards adopted by the U.S. Securities and Exchange Commission (the “SEC”) under the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). Accordingly, estimates of the Company’s Mineral Reserves and Mineral Resources, and other technical and scientific information included or incorporated by reference in this AIF, may differ materially from the information that would be disclosed by a United States company subject to the SEC standards under the Exchange Act.

Investors are cautioned not to assume that any part, or all, mineral deposits categorized as Inferred Mineral Resources or Indicated Mineral Resources will ever be converted into Mineral Reserves. Inferred Mineral Resources are Mineral Resources for which quantity and grade or quality are estimated based on limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. Inferred Mineral Resources are based on limited information and have a great amount of uncertainty as to their existence and as to their economic and legal feasibility, although it is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

2

Under Canadian securities laws, estimates of Inferred Mineral Resources are considered too speculative geologically to have economic considerations applied to them that would enable them to be characterized as Mineral Reserves and, accordingly, may not form the basis of feasibility or pre-feasibility studies, or economic studies except for a preliminary economic assessment as defined under NI 43-101. Indicated and Inferred Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

| Item 3: | CORPORATE STRUCTURE |

| 3.1 | Name, Address and Incorporation |

The Company was incorporated on June 18, 2018 under the Business Corporations Act (British Columbia) (“BCBCA”) under the name “Solaris Copper Inc.” On November 26, 2019, Solaris amended its articles of incorporation to change its name from “Solaris Copper Inc.” to “Solaris Resources Inc.”. The head office of the Company is located at Neuhofstrasse 5A Baar 6340 Switzerland. The registered and records office of the Company is located at 1133 Melville Street Suite 3500, The Stack Vancouver BC V6E 4E5 Canada.

| 3.2 | Inter-corporate Relationships |

The following diagram illustrates the organizational structure of Solaris, including its subsidiaries, as of the date of this AIF. In certain instances, subsidiaries have been excluded where the total assets of that subsidiary does not exceed 10% of the consolidated assets of Solaris or, for the omitted subsidiaries together, in aggregate of 20% of the consolidated assets of Solaris.

All entities noted in the chart above are 100% owned, except as indicated below:

| 1. | Minera Ricardo Resources Inc. S.A. is 100% owned by Lowell Copper Holdings Inc., except for one share held by Solaris. |

| 2. | Lowell Copper S.A.C. is 100% owned by Lowell Copper Holdings Inc., except for one share held by Solaris. |

3

| 3. | Lowell Mineral Exploration Ecuador S.A. (“Lowell Ecuador”), a subsidiary of Solaris, owns and operates the Warintza Project (as defined below). Solaris’ wholly owned subsidiary, LCH, is the registered trustor of a guarantee trust that owns all of the issued and outstanding common shares of Lowell Ecuador, and holds the sole and exclusive right to claim restitution of the common shares of Lowell Ecuador upon complying with certain terms of the Funding Package. |

| 4. | Minera Gabriella S.A. de C.V. is 100% owned by Lowell Copper Holdings Inc., except for one share registered in the name of J. David Lowell. |

| 5. | Minera Torre de Oro, S.A. de C.V. is 60% owned by Minera Hill 29 SA de CV (an indirect subsidiary of Solaris) and 40% owned by Aur Mexcay Inc., a subsidiary of Teck Resources Limited (“Teck”). |

| 6. | Ascenso Inversiones, S.A. is 100% owned by Lowell Copper Holdings Inc., except for 0.01% of shares held by a legal representative. |

| Item 4: | GENERAL DEVELOPMENT OF THE BUSINESS |

| 4.1 | Three Year History |

Set out below is a summary of how the Company’s business has developed over the last three completed financial years. In accordance with Form 51-102F2 – Annual Information Form, the below summary includes only events, such as acquisitions or dispositions, or conditions that have influenced the general development of the business.

2023

On February 24, 2023, Solaris announced the appointment of Ms. Poonam Puri to the board of directors of the Company (the “Board”).

On June 14, 2023, Solaris announced a new discovery in its first hole drilled at Patrimonio, a new porphyry southwest of Warintza Central.

On November 6, 2023, Solaris announced the appointment of Mr. Javier Toro as Chief Operating Officer of Solaris to lead the advancement of the Warintza Project.

On December 11, 2023, Solaris announced that Solaris and OMF Fund IV SPV D LLC and OMF Fund IV SPV E LLC, entities managed by Orion Mine Finance Management LP (collectively, “Orion”), had entered into definitive agreements with respect to an $80 million financing package for the advancement of the Warintza Project in Ecuador, comprised of a credit agreement dated December 11, 2023 among Solaris, LCH, Lowell Ecuador and OMF Fund IV SPV relating to the Company’s $60 million senior secured term facility (the “Senior Loan”), a subscription for $10 million in equity at a price of C$5.11 per Common Share and a commitment for $10 million in additional equity financing (the “Orion Subscription Agreement”). In connection with the Orion financing, Solaris entered into a copper offtake agreement (the “Copper Offtake Agreement”) and a molybdenum offtake agreement (the “Molybdenum Offtake Agreement” and, collectively, the “Offtakes”) with Orion for the sale of 20% of metals produced from the Warintza Project for a period of 20 years from the start of production, subject to adjustment in accordance with the Offtakes. If prior to the 18-month anniversary of the Senior Loan closing date a change of control transaction (as defined in the Offtakes) is approved by the Board and announced, either party may terminate the offtake agreements prior to the end of the term which will require the Company to then pay $27 million to Orion to terminate the Copper Offtake Agreement and $3 million to terminate the Molybdenum Offtake Agreement.

2024

On January 8, 2024, the Company announced a preview of 2024 plans including the intent to list the Common Shares on the NYSE American LLC (“NYSE American”).

On January 11, 2024, Solaris announced that it had entered into a subscription agreement in respect of an approximately C$130 million private placement of Common Shares by an affiliate of Zijin Mining Group Co., Ltd. at a subscription price of C$4.55 per Common Share (the “Zijin Private Placement”). The Company announced the termination of the Zijin Private Placement on May 21, 2024.

4

On January 22, 2024, Solaris announced the 2024 drill program with a total of six drill rigs at Warintza including the delivery of an updated Mineral Resource estimate (“MRE”) due in late Q2 2024 and ongoing drilling thereafter focused on growth and infill drilling of at least 30 kilometers.

On March 1, 2024, Solaris announced a cooperation agreement with the Interprovincial Federation of Shuar Centers and the Alliance for Entrepreneurship and Innovation of Ecuador.

On April 19, 2024, Solaris’ Common Shares commenced trading on the NYSE American under the symbol “SLSR”. Concurrent with the start of trading on the NYSE American, the Common Shares ceased trading on the OTCQB Venture Market.

On April 17, 2024, Solaris announced it has signed an updated Impact and Benefits Agreement for the Warintza Project (the “IBA”).

On June 10, 2024, Solaris announced it closed a bought deal equity offering for aggregate gross proceeds of C$40,290,250. The Company also issued, on private placement basis, 2,795,102 Common Shares at a price of C$4.90 per Common Share for aggregate gross proceeds of C$13,696,000.

On June 10, 2024, Solaris filed a preliminary short form base shelf prospectus allowing the Company to offer for sale from time to time, for a 25-month period, Common Shares, debt securities, subscription receipts, Common Share purchase contracts, units and warrants in one or more series or issuances, with a total offering price, in the aggregate, of up to $200 million. On June 14, 2024, Solaris filed a final short form base shelf prospectus with the same offering terms.

On July 22, 2024, Solaris announced an updated MRE for the Warintza Project.

On July 26, 2024, Solaris announced the appointment of Mr. Arun Lamba as Vice President, Corporate Development.

On September 9, 2024, Solaris announced it has submitted an Environmental Impact Assessment (“EIA”) to the Ministry of Environment, Water and Ecological Transition for the construction of the Warintza Project.

On November 20, 2024, Solaris announced that the Company would complete its emigration by year-end (the “Emigration”). As part of the final Emigration steps, the Company’s Canadian offices will be closed, the Company and its subsidiaries will have no individuals in Canada who are employed or self-employed in connection with the Company. In connection with the Emigration, the Company announced the appointment of Mr. Matthew Rowlinson as President and Chief Executive Officer of the Company. Solaris also announced the appointment of Mr. Matthew Rowlinson, Mr. Rodrigo Borja, and Mr. Hans Wick to the Board.

2025

On January 8, 2025, Solaris announced the appointment of Mr. Richard Hughes as Chief Financial Officer and Company Secretary, Mr. Patrick Chambers as Vice President, Investor Relations and Mr. Ignacio Shimamoto as Vice President, Finance. The Company further announced that the final Emigration steps were complete, subject to a few administerial matters.

On March 3, 2025, Solaris announced the formation of an Inter-Institutional working group together with the Pueblo Shuar Arutam organization, Solaris’ host communities of Warints and Yawi and the Ecuadorian State.

On April 22, 2025, Solaris announced the completion of a significant drilling campaign at the Warintza Project, comprising over 82,000 metres of infill drilling completed between January 2024 and February 2025, positioning the Company to upgrade a substantial portion of Inferred Resources to the Measured and Indicated categories.

5

On May 21, 2025, Solaris announced that it had entered into a $200 million financing arrangement comprising a gold stream (the “Stream Agreement”) and net smelter return royalty (the “Royalty Agreement”) (collectively the “RG Financing Agreements”) with RGLD Gold AG (“Royal Gold AG”), a subsidiary of Royal Gold, Inc. (“Royal Gold”). Pursuant to the Stream Agreement, Royal Gold will receive gold deliveries equivalent to 20 ounces per 1 million pounds of copper produced from the RGLD Gold AOI (as defined in the Stream Agreement). For each ounce of gold delivered under the Stream Agreement, Royal Gold will pay Solaris a purchase price equal to: (i) 20% of spot price until 90,000 ounces have been delivered; and (ii) 60% of spot price thereafter. Pursuant to the Royalty Agreement, Royal Gold will receive a 0.3% net smelter return (“NSR”) royalty (the “Royalty”) on all metal production from the RGLD Gold Expanded AOI (as defined in the Royalty Agreement). The Royalty will increase annually by 0.0375%, up to a maximum of 0.6%, until the earlier of (i) the first delivery of gold pursuant to the Stream Agreement; or (ii) eight years following the closing date of the RG Financing Agreements. In connection with the entry by Solaris into the RG Financing Agreements, each of the Offtakes were amended pursuant to first amending agreements dated May 21, 2025 in order to, amongst other things, permit entry by Solaris into the RG Financing Agreements (collectively, the “Funding Package”). The funds received from the Funding Package were used, in part, to repay the Senior Loan in full.

On September 11, 2025, Solaris announced the signing of a landmark agreement with the Pueblo Shuar Arutam organization (“PSHA”), marking a major milestone in the Company’s social engagement efforts and reinforcing the strong momentum behind the Warintza Project.

On November 6, 2025, Solaris announced the results of the Technical Report (as defined below) and a maiden MRE for the Warintza Project. The Technical Report supports an average annual copper equivalent (“CuEq”) production of over 300,000 tonnes in the first 5 years and over 240,000 tonnes during the first 15 years and the first quartile all-in sustaining cost of $0.85/lb of payable copper (“Cu”) for the first five years and $1.07/lb of payable Cu during the first 15 years. The MRE incorporates a 312% increase in Measured plus Indicated Mineral Resources, at a cut-off grade of 0.1% Cu and a NSR cut-off value of $6.30/tonnes (“t”), compared with the 2024 MRE.

2026

On January 28, 2026, Solaris announced that Ecuador’s state-owned mining company, Empresa Nacional Minera ENAMI EP, has granted Solaris an option to acquire up to a 100% interest in a new portfolio of highly prospective exploration areas located immediately adjacent to the Warintza Project, expanding Solaris’ footprint by approximately 40,000 hectares.

| Item 5: | DESCRIPTION OF THE BUSINESS |

Summary

Solaris is a copper-gold exploration and development company, committed to a sustainable future by empowering communities and stakeholders through our dedication to participatory and responsible mining. The Warintza Project, a large copper-gold porphyry deposit, is a unique, global scale asset located in southeast Ecuador. The Company also owns a series of grassroot exploration projects with discovery potential in Peru and Chile and a 60% interest in the La Verde joint-venture project with a subsidiary of Teck. The Common Shares trade on the TSX under the symbol “SLS” and on NYSE American under the symbol “SLSR”.

Solaris’ headquarters is located at Neuhofstrasse 5A Baar 6340 Switzerland. Further information is available at www.solarisresources.com.

Specialized Skill and Knowledge

Management is comprised of a team of individuals who have extensive expertise and experience in the mineral exploration industry and exploration finance and are complemented by an experienced Board. See ITEM 13: “Directors and Officers” below.

6

Competitive Conditions

The Company competes with other mineral exploration and mining companies for mineral properties, joint venture partners, equipment and supplies, qualified personnel and exploration and development capital. See ITEM 7: “Risk Factors” below.

Environmental Protection

The current and future operations of the Company are subject to laws and regulations governing exploration, development, tenure, production, taxes, labour standards, occupational health, waste disposal, greenhouse gas emissions, protection and remediation of the environment, reclamation, mine safety, toxic substances and other matters. Specifically, the Warintza Project is being advanced in accordance with Ecuador’s Mining Law, Environmental Organic Code, Mining Environmental Regulations, Unified Text of Secondary Environmental Legislation, and an array of other applicable norms, standards, laws and regulations.

Compliance with such laws and regulations increases costs and may cause delays in planning, designing, drilling and developing the Warintza Project. The Company attempts to diligently apply technically proven and economically feasible measures to advance protection of the environment throughout the exploration and development process, however it is often impossible to anticipate and mitigate all administrative delays. Currently, costs associated with compliance are considered to be normal compared to other South American countries.

Employees

As of December 31, 2025, the Company directly employed 84 employees.

Foreign Operations

The Company’s mineral properties are located in Ecuador, Mexico, Chile and Peru, and its operations are substantially carried out in those countries. See ITEM 7: “Risk Factors” below.

Social or Environmental Policies

Solaris and the local Shuar communities of Warints and Yawi announced the signing of the IBA in September 2020, which was subsequently updated in March 2022 and in April 2024. The IBA provides certainty of community support for the responsible advancement of the project from exploration and development through to production and is a major milestone in the Company’s innovative CSR program. This was the first IBA established in Ecuador and set the precedent for industry best practice for inclusive and mutually-beneficial resource development in partnership with Indigenous Communities. The IBA formalizes commitments toward supporting partner communities in their social and cultural practices. It also provides for eliminating or mitigating adverse impacts, employment, contracting and business opportunities supported by a robust program of education, skills and training together with community infrastructure development and financial benefits to maximize community participation and positive outcomes for Indigenous partners. Solaris continues to work with the applicable regulatory officials in Ecuador and the Shuar Indigenous Community to proceed with further exploration and development of the project, while working to ensure the health and safety of employees, contractors and the community.

| Item 6: | MATERIAL MINERAL PROJECT |

| 6.1 | Current Technical Report |

The Company’s only material mineral project is the Warintza Project. The technical report is titled “Warintza Project Pre-Feasibility Study and Updated Mineral Resource Estimate”, effective November 1, 2025 (filed on SEDAR+ on November 24, 2025) and was prepared by Mary Alejo Hito, P.Eng., Eugene Tucker, P.Eng., Roderick Carlson, FAIG (RPGeo), MAusIMM, Nicholas Szebor, MCSM, M.Sc., B.Sc., CGeol (London), EurGeol, FGS, Gregory Lane, FAusIMM, Guillermo Hernán Barreda Flores, SME Registered Member (the “Technical Report”).

7

The scientific and technical information in this section relating to the Warintza Project is derived from, and in some instances is a direct extract from, and is based on the assumptions, qualifications and procedures set out in, the Technical Report. Such assumptions, qualifications and procedures are not fully described in this AIF and the following summary does not purport to be a complete summary of the Technical Report. Reference should be made to the full text of the Technical Report, which is available for review under the Company’s profile on SEDAR+ at www.sedarplus.com and on EDGAR at www.sec.gov. Capitalized terms used but not otherwise defined in this section have the meanings given to such terms in the Technical Report.

Introduction

The Warintza Project is a copper-molybdenum porphyry deposit located in southeastern Ecuador (“Warintza”, the “Project” or the “Warintza Project”). AMC Mining Consultants (Canada) Ltd. (“AMC”) was commissioned by Solaris to prepare the independent Technical Report summarizing the results of a pre-feasibility study (“PFS”) for the Warintza Project. The Warintza Project is currently 100 percent owned by Solaris and its subsidiary, Lowell Mineral Exploration Ecuador S.A. (“Lowell”). The purpose of the Technical Report is to provide an update to the MRE described in the previous technical report completed in July 2024 (“2024 Technical Report”), and to provide the results of the PFS for the Project. The 2024 Technical Report was titled “Mineral Resource Estimate Update, NI 43-101 Technical Report, Warintza Project, Ecuador”, with an effective date of July 1, 2024.

Drilling conducted between 2020 and 2025 has delineated the Warintza Central, East, and West areas, supporting the generation of a well-developed geological model. Extensive infill drilling, new metallurgical testing, and mine planning studies have been incorporated into the PFS, which includes a simplified process flowsheet and an optimized mine design.

The PFS contemplates a single-phase open pit operation with a planned 22-year life-of-mine (“LOM”), based on flotation of copper sulphide mineralization. The LOM is constrained by the design storage capacity of the Tailings Management Facility (“TMF”), which is limited to 1.3 billion tonnes. This engineering limitation, consistent with the Estudio de Impacto Ambiental - EIA application, defines the maximum processing capacity and, therefore, the reported LOM, rather than the full extent of potentially available Mineral Resources.

Subsequent to the establishment of criteria for the PFS, a conceptual expanded pit optimization exercise was completed in consideration of the possibility for a future increase in TMF capacity and without the limitation of the current Project footprint. The results of the conceptual exercise indicated a shell with a larger mineralized inventory at potentially similar grades to the PFS Mineral Reserves. Were such a shell to be ultimately realized, and contingent on all necessary supporting aspects being favourable, including with respect to any impact on key infrastructure, there could be a possibility to extend the mine life by a timeframe of the order of 25 to 30 years beyond the PFS Mineral Reserves. Improvements to the mine plan could also be possible that would reflect further resource benefit optimization, such as delaying the processing of the low-grade stockpile and deferring closure activities. Solaris again notes the conceptual nature of the expanded pit exercise and that it does not represent any increase in Mineral Reserve estimates over those presented in this 2025 Technical Report.

Property Description and Ownership

The Warintza Project is located within the Warintza property (the “Property”) in southeastern Ecuador. The Project consists of porphyry copper–molybdenum deposits that are proposed to be developed using conventional open-pit mining methods. Mineral processing for the Project is planned to include crushing, grinding, and flotation to produce a copper concentrate, with gold and silver by-products, and a separate molybdenum concentrate.

The Property lies approximately 235 kilometres (“km”) southeast of Quito, Ecuador’s capital, and 85 km east-southeast of the city of Cuenca. The Project is situated within the Limón Indanza and San Juan Bosco cantons of Morona Santiago province, specifically the Parroquia San Carlos de Limón. The geographic coordinates are approximate1y 3°10’ south 1atitude and 78°17’ west 1ongitude, within the Cordi11era de1 Cóndor mountain range, which locally defines the Ecuador–Peru border.

The Property consists of nine metallic mineral concessions covering a total of 26,773 hectares (“ha”) (268 square kilometres (“km2”)) as shown in Table 1. All concessions are registered to Lowell. In April 2024, Solaris announced an option agreement to acquire up to 100% interest in 10 additional concessions adjacent to the Property, totalling approximately ~40 km2, which are considered prospective for porphyry copper and epithermal gold mineralization.

Table 1: Warintza concessions

| Name | Concession number | Area (ha) | Type | Registration date | Good to date |

| CAYA 21 | 101083 | 2,499 | Concession | 25/5/2010 | 31/8/2044 |

| CAYA 22 | 101092 | 2,499 | Concession | 25/5/2010 | 31/8/2044 |

| CURIGEM 9 | 100081 | 4,049 | Concession | 25/5/2010 | 20/5/2045 |

| CURIGEM 9-1 | 10000938 | 949 | Concession | 8/4/2022 | 10/8/2032 |

| CLEMENTE | 90000337 | 1,601 | Concession | 31/3/2017 | 31/3/2042 |

| MAIKI 01 | 90000310 | 4,072 | Concession | 8/3/2017 | 8/3/2042 |

| MAIKI 02 | 90000311 | 4,304 | Concession | 8/3/2017 | 8/3/2042 |

| MAIKI 03 | 90000313 | 2,500 | Concession | 31/3/2017 | 31/3/2042 |

| MAIKI 04 | 90000314 | 4,300 | Concession | 8/3/2017 | 8/3/2042 |

| Grand total | 26,773 | ||||

8

Solaris has signed the IBA with local communities within the Project area. The IBA, originally signed in March 2022 and updated in April 2024, grants surface access and use rights necessary for exploration and development activities.

The EIA application was submitted by Solaris in August 2024 to the Ecuador Ministerio de Ambiente, Agua y Transición Ecológica - Ministry of Environment, Water, and Ecological Transition (the “MAATE”), recently incorporated into the Ministerio de Ambiente y Energía - Ministry of Environment and Energy (the “MAE”). Approval of the EIA will be required before operating and environmental permits can be issued. At the effective date of the Technical Report, the concessions are in good standing, and Solaris holds all permits required to conduct ongoing exploration activities, including Environmental Licenses for advanced exploration in the Caya 21, Caya 22, and Curigem 9 concessions and Environmental Registrations for the remaining concessions.

The concessions are subject to certain obligations and encumbrances. Lowell has entered into a guaranteed assignment agreement regarding mining rights in favour of ANEFI S.A. In addition, a 2% NSR royalty is payable to South32 Royalty Investments Pty Ltd. on the Curigem 9, Curigem 9-1, Caya 21, and Caya 22 concessions. Ecuadorian mining law also applies a 4% NSR royalty to the state, along with corporate income tax (20% of taxable profits), profit-sharing requirements (12% to the state and 3% to employees), and annual concession fees based on hectares held and stage of development.

Solaris has entered into the RG Financing Agreements to support the development of the Warintza Project. Under the terms of the Stream Agreement, Royal Gold will receive 20 ounces of gold for every one million pounds of Cu produced from a specified area of interest, which includes the current pit design. Solaris will receive 20% of the spot gold price for the first 90,000 ounces of gold delivered, after which the payment will increase to 60%. In addition to the Stream Agreement, the RG Financing Agreements include a royalty percentage applied to the post-stream NSR. The post-stream NSR is calculated after accounting for earnings and deductions from the Stream Agreement. The Royalty starts at 0.3% and will increase annually by 0.0375%, reaching a maximum of 0.6%. This escalation continues unless gold delivery begins or eight years elapse. The RG Financing Agreements were entered into in May 2025. Since the commercial production period is set to begin after a three-year construction phase, a 0.45% royalty is applied to the post-stream NSR in the economic analysis. Additionally, Royal Gold will cover the refining charges for the gold received under the Funding Package.

The Warintza Project has a partial offtake agreement with Orion. Under the Offtakes, Orion will purchase the greater of:

| ● | 20% of the copper and molybdenum concentrates produced in each contract year, or |

| ● | The percentage of production of concentrates necessary to ensure a minimum delivery of 30,000 tonnes of copper and 1,500 tonnes of molybdenum in each contract year. |

The Offtakes will remain in effect for 20 years after commercial production begins. If commercial production is not achieved by December 31, 2032, the Offtakes will be extended for the entire duration of the mine’s life, as specified in the Offtakes. Additionally, Solaris will cover all treatment and refining charges for the concentrates under the Offtakes.

No environmental liabilities have been identified on the Property. Existing exploration infrastructure is subject to reclamation obligations under environmental permits, including camp decommissioning, road rehabilitation, and revegetation of disturbed areas. To the extent known, there are no other significant factors or risks that may affect access, title, or the right or ability to perform work on the Property; this includes any significant environmental, social, or permitting issues that would prevent the exploitation of the mineral deposits on the Warintza Project.

Accessibility, climate, local resources, infrastructure, and physiography

The Warintza Project is located 85 km east-southeast of Cuenca, Morona Santiago province, and is accessible by national and provincial highways, with a final 58 km along the Limón–Warints road. An unsealed 550 metre (m) airstrip at Warintza provides supplementary access. Nearby villages, Warintza (~512 people) and Yawi (~210 people), are parties to the IBA with the Company.

Topography is rugged, with elevations between 800 m and 2,700 m above sea level (“masl”) and slopes of 25°–40°. The climate is tropical humid with an average temperature of 22.9°C and annual precipitation of ~1,900 millimetres (“mm”), permitting year-round operations.

On-site infrastructure includes a base camp at Piuntz with capacity for 340 personnel, administrative and technical facilities, accommodation, power generation (diesel), water supply, wastewater treatment, communications, and a core storage facility. The Project has ~19 km of internal access roads linking key drilling areas.

9

The site is not yet connected to the national grid; however, grid connection is planned via a 230 kilovolt (“kV”) double-circuit transmission line to the Bomboiza substation (~52 km).

The region has demonstrated mining viability under similar physiographic and climatic conditions, as evidenced by the nearby Mirador and Fruta del Norte operations.

History

Exploration activities in the Warintza area began in 1994 when Gencor Limited initiated grassroots work on the Pangui Project in southeastern Ecuador. Early programs focused on stream sediment sampling, ridge-based soil geochemistry, geological mapping, and reconnaissance prospecting, which identified multiple porphyry targets, including Warintza Central, East, West, and South.

Between 1997 and 1999, Billiton PLC (“Billiton”) conducted regional geochemical surveys, airborne magnetics-EM, detailed mapping, and soil and rock geochemistry. Initial drilling commenced in 2000 under Corriente Resources Inc. (“Corriente”) after acquiring rights from Billiton. Two campaigns totalling 33 diamond drillholes (“DD”) (6,530 m) confirmed the presence of a copper-molybdenum (“Cu-Mo”) porphyry system enriched by supergene processes at Warintza Central. Concurrent mapping and geochemical sampling expanded knowledge of Warintza West.

Ownership of the Warintza concessions passed from Corriente to Lowell in a swap of Lowell’s 10% interest in Corriente’s Ecuadorian properties for 100% interest in the Property. In a 2013 reverse takeover of Waterloo Resources Ltd., Lowell Copper Ltd. (“Lowell Copper”) was formed. In 2016, Lowell Copper merged with Gold Mountain Mining Corporation and Anthem United Inc. to form a new company, JDL Gold Corp. (“JDL”). In March 2017, JDL merged with Luna Gold Corp. to form Trek Mining Inc. (“Trek”). In December 2017, Trek merged with NewCastle Gold Ltd. and Anfield Gold Corp. to form Equinox Gold Corp. (“Equinox”). In 2018, Equinox spun out its copper assets including the Property to form Solaris.

Surface geochemical datasets compiled by previous operators comprise approximately 981 soil samples, 256 channel samples, 240 rock-chip samples, and 15 panel samples. These defined Cu-Mo anomalies are broadly coincident with the Warintza Central porphyry centre. While systematic grid-based sampling improved resolution over time, several anomalies remain untested by drilling.

Historical MREs

Several historical MREs have been prepared for the Warintza Central deposit. These include non–NI 43-101 compliant estimates in 2001 and 2005, and the earlier of two estimates prepared by Mine Development Associates (“MDA”) in 2006 and 2018. The MDA estimates comprised:

| ● | 2006 (MDA): Inferred Mineral Resource of 195 million tonnes (“Mt”) grading 0.61% CuEq (0.42% Cu, 0.031% Mo) at a 0.3% CuEq cut-off, based on 33 drillholes and 2,142 assays. |

| ● | 2018 (MDA): An update of the 2006 model with identicsal results, prepared for Equinox and Solaris. |

In 2024, Mario E. Rossi, FAusIMM, SME, IAMG, of Geosystems International Inc., prepared an updated MRE for Solaris based on more than 101,000 m of drilling. The estimate reported: Measured and Indicated Mineral Resources: 909 Mt at 0.53% CuEq (0.37% Cu, 0.02% Mo, 0.05 grams per tonne (“g/t”) gold (“Au”)); Inferred Mineral Resources: 1,426 Mt at 0.37% CuEq (0.27% Cu, 0.01% Mo, 0.04 g/t Au).

The estimates listed above prior to 2018 are considered historical MREs. Solaris is not treating them as current Mineral Resources.

The 2018 and 2024 estimates are superseded by the current MRE disclosed in Section 14 of the Technical Report and are not considered material, except for the provision of context.

Historical production

No mining or commercial production has been reported for the Warintza Project.

Geological setting and mineralization

The Warintza Project is located within the Cordillera del Cóndor of southeastern Ecuador, part of the Jurassic-aged Zamora Cu-Au metallogenic belt that hosts multiple porphyry Cu-Mo±Au and skarn systems, including Mirador and Fruta del Norte. The Warintza cluster comprises several discrete to coalescent porphyry centres (Warintza Central, East, Southeast, West, Patrimonio, and South), covering a mineralized footprint of ~30 km2.

A 7 km long prominent east-west-trending corridor of porphyry Cu centres, likely structurally controlled, is defined by the alignment of Warintza West, Warintza Central, and Warintza East. Warintza South is located about 3 km to the south of this trend. All deposits and prospects exhibit geologic characteristics typical of the Cu-Mo association, with variable, often erratic, presence of Au.

10

Regionally, mineralization is related to Late Jurassic subduction-related magmatism associated with the Zamora Batholith and Misahuallí volcanic sequence. U-Pb zircon and Re-Os molybdenite dating indicates mineralization between ~157 and 153 Ma. These intrusions consist of diorite to quartz monzodiorite porphyries and related breccias, with alteration and mineralization styles typical of porphyry Cu-Mo systems.

At Warintza Central, mineralization is associated with composite quartz monzodiorite and diorite stocks cut by porphyry dikes and veinlet assemblages (early dark micaceous, A-, B-, C-, and D-types). Alteration includes early potassic, intermediate biotite–gray mica, and late sericite assemblages, with a gradational transition from hypogene chalcopyrite-pyrite mineralization to immature supergene chalcocite enrichment near surface.

Warintza East hosts a molybdenum-rich rhyodacite porphyry core with peripheral Cu-Mo mineralization in andesitic hosts, while Warintza West comprises porphyry-style stockwork mineralization developed within intermineral tonalite–quartz monzodiorite intrusions. Patrimonio and Warintza South are less advanced but display porphyry-style alteration, veining, and skarn development consistent with the broader cluster.

Overall, the Warintza cluster represents a structurally controlled, east-west-trending corridor of porphyry centres with Cu-Mo±Au mineralization typical of the Zamora Belt.

Deposit type

The Warintza deposit is a Cu-Mo porphyry system associated with calc-alkalic igneous rocks. Mineralization is hosted in multi-phase intrusive complexes, primarily diorite to quartz monzonite porphyries, and in associated hydrothermal breccias. Copper and molybdenum occur as disseminations and in quartz-sulphide veinlet stockworks, as well as within breccia matrix sulphides.

Hydrothermal alteration follows the typical porphyry zonation pattern: a central potassic core (biotite, K-feldspar) associated with higher grades, overprinted by phyllic (quartz–sericite–pyrite) assemblages, and surrounded by a broad propylitic halo (chlorite–epidote). Structural control through fracture networks enhances sulphide emplacement, and supergene processes have contributed to some secondary copper enrichment near surface.

Porphyry Cu-Mo systems are typically large-tonnage, low-grade deposits formed in subduction-related tectonic settings. Their extensive alteration footprints and geochemical zonation provide reliable vectors for exploration, while geophysical methods (induced polarization, magnetics) and hyperspectral scanning of drill core are effective in delineating mineralized centres.

Exploration

Exploration works completed on the Property include surface rock-chip sampling, soil geochemical sampling, and stream sediment sampling. Historical exploration conducted by previous operators, including Billiton, outlined regional porphyry Cu-Mo targets. Solaris has undertaken extensive programs of geological mapping and surface sampling since 2020, including soil grids at 50-100 m spacing and targeted rock-chip sampling of altered and mineralized outcrops.

Geophysical exploration has included the compilation and re-interpretation of historical airborne magnetic and electromagnetic surveys. In 2020, a Z-axis Tipper Electromagnetic Audio Frequency Magnetic and magnetic survey was carried out over the Property. Detailed three-dimensional (“3D”) inversion and modelling of these results were performed by Condor Consulting Inc. in 2021, integrating additional drilling data, geology, weathering, and density models.

Results of the geochemical and geophysical programs show strong correlations between anomalous Cu, Mo, and Au in soils and rocks with high-conductivity zones and magnetic lows interpreted as porphyry centres. Surface sampling and geophysics have effectively identified multiple target areas, including Warintza East, Warintza South, Patrimonio, and regional prospects such as Caya and Mateo, demonstrating the potential for both porphyry and high-sulphidation epithermal mineralization.

The integration of geological mapping, geochemistry, and geophysical data has provided a robust framework for defining drill targets, vectoring towards zones of higher-grade mineralization, and supporting ongoing resource drilling programs.

11

Drilling

Drilling across the Warintza Project has been conducted by multiple operators, most recently by Solaris. Historical drilling includes campaigns undertaken by Lowell and Corriente in 2000 and 2001, which comprised 33 DD totalling 6,530 m focused on Warintza Central. Since February 2020, Solaris has conducted a renewed drilling campaign, resulting in a total of 318 DD holes and 177,118 m of drilling completed at the time of this report. All available drilling has been incorporated into the Mineral Resource model.

Drilling at Warintza has generally been conducted from centralized platforms due to steep, forested terrain, with multiple drillholes completed at various orientations from each platform. As a result, reported intercepts are downhole lengths and may not represent true thicknesses. Collar locations have been surveyed using Real-Time Kinematic differential global positioning system and, where required, total station surveys. Downhole surveys employ the Reflex Gyro Sprint IQTM gyroscopic tool. DD core recovery is considered excellent, ranging from 83% to 100%, with the majority of intervals recovered at 100%.

Since 2020, Solaris has also collected density samples of 10-15 centimetres (“cm”) length from competent core taken at intervals of every 20 m. Density measurements were completed at the Bureau Veritas (“BV”) laboratory in Quito using the paraffin-coated, water-immersion method. Core handling procedures include logging, photographic documentation, structural and geotechnical data collection, and secure storage in the Solaris core facility in Quito.

Drilling has largely targeted Warintza East, Central, West, and Patrimonio / Trinche zones, supporting geological interpretation, resource estimation, and structural modelling. Drillhole spacing varies by deposit, generally ranging from 12 m by 12 m for trial grade control up to 100-200 m by 50 m in less intensively drilled areas. Drilling methods and procedures are consistent with best practices for porphyry copper exploration and are not expected to materially affect the reliability of the MRE. The QP considers that there are no known drilling, sampling, or recovery factors that could impact the accuracy and reliability of the drilling results.

The drilling results are consistent with the conceptual model for large-scale porphyry copper systems. The deposit features a higher-grade core with grades that decrease progressively with distance from the centre. The QP notes that, given the overall scale of the resource, individual drillhole results have limited significance — particularly considering the extensive number of holes now drilled at the Warintza Project.

Sampling, Analysis and Data Verification

Several laboratories have been used for the preparation and analysis of samples from the Warintza Project. Early drilling campaigns (2000-2001) were conducted by Corriente, with sample preparation at Bondar-Clegg in Quito, Ecuador, and analysis at Bondar-Clegg in North Vancouver, Canada. Since 2020, Solaris has used accredited independent laboratories, primarily ALS Minerals in Quito, Ecuador (preparation) and Lima, Peru (analysis), with BV in Quito acting as a secondary “umpire” laboratory.

Sample preparation and analyses have generally involved crushing and pulverizing DD core samples to 75-106 pm, with subsamp1es assayed via fire assay with atomic absorption finish for Au, and three- or four-acid digest with atomic absorption spectroscopy for Cu, Mo, and other elements. Sequential copper analysis and multielement ICP-AES suites have also been applied since 2020, with mercury added in 2024.

Quality assurance and quality control (“QAQC”) procedures have been implemented throughout all drilling campaigns. Historical campaigns included pulp duplicates and reference materials (“CRMs”) for Cu, Mo, and Au, with minimal QAQC documentation. The chain of custody for samples was maintained via physical documentation, but electronic tracking systems were not in use during this period. Sealing bags and controlling shipment ensured sample security, but formalized security protocols were less comprehensive than in later campaigns. Since 2020, QAQC programs have included field and pulp duplicates, coarse and fine blanks, and CRMs sourced from Target Rocks. DD core was typically sampled at fixed 2 m intervals. The DD core was halved along a marked axis using a diamond saw or guillotine (for oxidized zones), with samples taken consistently from the same side. Field duplicates (quarter DD core) were prepared from the half core primary sample (i.e. primary sample is also quarter core), and sample details, QAQC metadata, and weight were recorded. Samples were sealed in bags with plastic ties and transported securely. Umpire checks using BV provided additional verification of laboratory results.

12

Field duplicates show moderate precision for Au, acceptable precision for Cu, and lower precision for Mo, reflecting natural heterogeneity in the deposit. Pulp and coarse reject duplicates demonstrate improved analytical precision. CRM performance indicates acceptable accuracy, with the majority of results within plus or minus (±) 5% of certified values. Blanks show minimal contamination.

The QP undertook a series of independent verification steps as part of the current resource estimation update, including assessment of drillhole collars and survey, core logging and geological interpretation, sampling and QAQC, database and assay verification, and laboratory audits. In addition to current verification steps, the QP has reviewed previous data verification activities completed for the Warintza Project. Previous verification efforts, undertaken between 2000 and 2024 by in-house and independent consultants, included drillhole collar coordinate checks, downhole survey verification, DD core logging audits, sampling review, QAQC assessment, and laboratory inspections.

The sample preparation, security, and analytical methodologies at Warintza conform to industry-standard practices. QAQC results support the reliability of the dataset for the MRE. Minor limitations were noted in the performance of the secondary laboratory and field duplicates for low-grade Mo and Au, reflecting inherent deposit characteristics rather than methodological deficiencies.

Mineral Processing and Metallurgical Testing

Metallurgical testing for the Warintza Project has progressed through several phases. Solaris, in collaboration with Ausenco, initiated a structured PFS test work campaign during 2024 and 2025 that included mineralogy, comminution, flotation, copper-molybdenum separation, tailings characterization, and concentrate quality assessments.

A total of 58 drillhole intervals was selected for testing, with 30 individual interval samples used for comminution and 35 samples for flotation test work. Eight composite samples for development of the flotation test work conditions were formed based on lithology, alteration, assays (with a focus on sulphide sulphur to copper ratios) and projected mine plan timing.

The eight composite samples underwent TIMA mineralogical analysis, which provided information about copper sulphide liberation, gangue associations, and mineral deportment. The samples were ground to a product size P80 of 180 micrometres (“µm”). Chalcopyrite was identified as the dominant copper mineral, while pyrite was significantly more abundant across all samples. Liberation analysis showed 50-82% of copper sulphides were fully liberated, with potassic alteration samples exhibiting the lowest liberation. Pyrite was generally coarse and well liberated. Chalcopyrite had the most significant associations occur in ternaries with hard silicates (quartz / plagioclases / albite / K-feldspar, 4-16%), in binaries with phyllosilicates (0.5-14%), and in other complex associations (0.3-18%). Association with pyrite is minor in binaries (0.6-3%) and ternaries, with phyllosilicates and pyrite accounting for up to 3% of chalcopyrite mass. Composite samples MAJC-02 and MINC-01 (both of Warintza East, with a potassic alteration), and MAJC-04 (a volcanics composite) had an increased proportion of phyllosilicates, epidote, and complex / other associations.

Comminution testing confirmed Warintza mineralized samples are competent (average drop weight index = 9.4 kilowatt hours per cubic metre), moderately hard (average bond weight index (“BWI”) = 13.8 kilowatt hours per tonne), and moderately abrasive (Ai = 0.33 grams (“g”)). Warintza East samples showed higher DWi and BWI values, correlating with magnesium and calcium content, respectively, due to elevated biotite and plagioclase. Warintza Central DWi values increased with depth and showed a consistent BWI-potassium grade trend, likely linked to potassic alteration.

Flotation residence times, reagent requirements, stage configuration, and flowsheet design were first established through open cycle testing. Rougher and cleaner kinetics were evaluated to define a flowsheet comprising a rougher stage, rougher concentrate regrind, three-stage cleaning, and a cleaner scavenger step that was further evaluated in locked cycle testing.

Flotation test work optimal conditions were defined as:

| ● | All flotation test work conducted using tap water sourced from Société Générale de Surveillance SA Lima. |

| ● | Primary grind size P80 of 150 µm. |

13

| ● | Regrind size P80 of 25 µm. |

| ● | Aero 3302 as the primary collector. |

| ● | Lime used to depress pyrite, with rougher pH set at 10.5 and cleaner pH at 11.5. |

| ● | Burner oil used as the molybdenum collector. |

| ● | MIBC and Solvay Oreprep® F-549 employed as frothers. |

The testing conditions were selected to maximize selectivity of copper over pyrite, which was critical for maintaining concentrate quality. Tests conducted under less selective conditions (where pyrite activation was not controlled or pyrite collection was increased to improve gold recovery to concentrate) resulted in poor cleaner performance and reduced concentrate Cu grade and value.

Locked cycle tests on four major composites yielded copper recoveries of 79.3-89.7%, molybdenum recoveries of 72.2-85.1%, and concentrate grades of 21-28% Cu and 0.78-1.14% Mo. The recovery of non-sulphide gangue to concentrate was an issue and this will be an early priority item in future test work.

Preliminary copper-molybdenum separation tests showed high molybdenum recovery but inadequate copper rejection, largely due to test work procedural issues. Prior test work had demonstrated that successful separation is achievable, particularly when molybdenite is well liberated. The molybdenum concentrates were excessively diluted by non-sulphide gangue, highlighting the criticality of non-sulphide gangue rejection in preceding Cu-Mo concentrate flotation.

The Warintza copper concentrates contain low levels of deleterious elements. Fluorine grades, while generally low, correlate with calcium, and the higher grades are likely associated with the high non-sulphide gangue grades. Future flotation work will focus on improving gangue rejection and validating flowsheet conditions.

Recovery estimates were calculated using locked cycle test results applied to the projected mine plan outputs, rather than relying on simple averages. Some models assumed constant tailings grades for recovery projections. It was also assumed that concentrate grades could be improved with minimal impact on copper recovery, based on trends observed in cleaner performance during locked cycle testing.

Average recoveries over the projected mine life are estimated as:

| ● | 84.2% Cu recovery to a copper concentrate of 26.5% Cu. |

| ● | 71.9% Mo recovery to a molybdenum concentrate of 40% Mo. |

| ● | 60.4% Au recovery to a copper concentrate at an average grade of 2.58 g/t Au. |

Tailings test work identified PT-FLOC 1024 as the optimal flocculant, with settling rates exceeding the design criteria values. Rheology tests showed yield stress below 20 pascals at solids densities less than (<) 70 weight per weight percentage solids. Cycloning classification tests confirmed the potential for TMF embankment material, with further refinement planned.

The PFS test work is considered sufficient, and samples are regarded as representative of the primary mineralization for this study phase. Argillic supergene alteration mineralization was not tested as the selected sample head grade was below the likely cut-off grade.

Future work will focus on geometallurgical modelling, mineralogy, flotation flowsheet optimization to address both pyrite and non-sulphide gangue rejection, variability testing, and characterization of ore, concentrate, and tailings to inform feasibility study process plant design and recovery and concentrate grade estimates.

Mineral Resources

Solaris carried out the Warintza deposit MRE, which has subsequently been independently audited by the QP. The QP for the MRE is AMC Global Lead for Geosciences, Nicholas Szebor, who is independent of Solaris, and who takes responsibility for the estimate. The MRE is dated May 1, 2025 and represents an update of the previous MRE, dated July 1, 2024. The data used in this estimate includes the results of all drilling carried out on the Warintza Project to January 31, 2025.

14

The estimation was completed in Hexagon’s MineSightTM Version 16 software package. Ordinary Kriging was used to estimate grades for Cu, Mo, Au, and silver (“Ag”) in the block models, with Simple Kriging used to estimate density.

The MREs are housed in one-block model, with a key field (ZONA) identifying Warintza Central (including Patrimonio and Trinche), East, and West. Warintza Central and East (Warintza Central—East) were combined for estimation purposes, owing to the mineralization domaining associations that extend across both areas. Warintza West has been estimated as a standalone deposit with differing estimation domains to the Warintza Central-East areas.

The results of the 2025 MRE are summarized in Table 2. Copper, molybdenum, and gold are reported within an optimized pit shell (revenue factor of 1), above an open pit cut-off value of US$6.30/t NSR and a cut-off grade of 0.1% Cu.

Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Table 2: Mineral Resources of the Warintza Project 1 May 2025

| Resource | Tonnage (Mt) |

Grade | Contained metal | |||||||

| Classification | Cu (%) |

Mo (%) |

Au (g/t) |

Ag (g/t) |

CuEq (%) |

Cu (Mt) |

Mo (kt) |

Au (Moz) |

Ag (Moz) | |

| Measured | 1,196 | 0.35 | 0.02 | 0.04 | 1.31 | 0.45 | 4.1 | 231 | 1.7 | 51 |

| Indicated | 2,550 | 0.20 | 0.01 | 0.03 | 1.13 | 0.25 | 5.0 | 222 | 2.5 | 93 |

| Measured plus Indicated | 3,746 | 0.24 | 0.01 | 0.04 | 1.19 | 0.32 | 9.1 | 453 | 4.2 | 143 |

| Inferred | 2,092 | 0.16 | 0.01 | 0.02 | 1.11 | 0.20 | 3.3 | 141 | 1.6 | 75 |

| (1) | The MRE was prepared in accordance with CIM Definition Standards, and CIM MRMR Best Practice Guidelines (2019). |

| (2) | Mineral Resources are reported within optimized open pit constraints and an NSR cut-off value of US$6.30/t and 0.1% Cu cut-off grade, based on a US$5.30/t processing cost and US$1.00/t G&A cost, with a mining cost of US$1.50/t + incremental mining costs increasing by US$0.015/t for every bench below the reference level of 1,340 mRL for Warintza West, 1,145 mRL for Warintza Central, and 1,040 mRL for Warintza East; and US$0.010/t for every bench above these reference levels. |

| (3) | Metal prices: copper US$4.00/lb, molybdenum US$20.00/lb, gold US$1,850/troy oz, and silver US$20.00/troy oz. |

| (4) | Respective metal recoveries (Oxide, Mixed, Sulphide): copper 40,85,88%; molybdenum 0,60,65%; gold 0,60,65%; silver 0,60,65%. |

| (5) | Copper-equivalent grade calculation assumes metal prices and recoveries as per above and includes provisions for downstream selling costs: |

| ● | Sulphide CuEq (%) = Cu (%) + 3.94 × Mo (%) + 0.52 × Au (g/t) + 0.01 x Ag (g/t). |

| ● | Mixed CuEq (%) = Cu (%) + 3.76 × Mo (%) + 0.50 × Au (g/t) + 0.005 x Ag (g/t). |

| ● | Oxide CuEq (%) = Cu (%). |

| (6) | Oxide and mixed material account for less than 0.01% of the total Mineral Resources. |

| Mineral Resources are inclusive of | ||

| (7) | Mineral Reserves. |

| (8) | Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. |

| (9) | The MRE was supervised by Mr. Nicholas Szebor, MCSM, MSc (Mining Geology), BSc, CGeol, EurGeol, FGS, Director and Global Lead Geosciences at AMC Consultants (UK) Limited, who takes responsibility for the estimate. Mr. Szebor is an Independent Qualified Person as defined by NI 43-101. Mr. Szebor is a European Chartered Geologist (European Federation of Geologists) and a Chartered Geologist and Fellow of the Geological Society of London. |

| (10) | The QP is not aware of any known environmental, permitting, legal, taxation, socio-economic, marketing, political or other relevant factors which could materially affect the stated Mineral Resources. |

| (11) | All figures are rounded to reflect the relative accuracy of the estimate and, therefore, may not appear to add precisely; this includes the rounding of Au and Mo to two decimal places. |

| (12) | The effective date of the MRE is May 1, 2025. |

15

Mineral Reserves

The Mineral Reserves estimate has been prepared in accordance with NI 43-101 and CIM Definition Standards.

The Mineral Reserves estimates were developed by Minsys Mining Systems LLC (“Minsys”) and Solaris, under the supervision of the QP, Eugene Tucker of AMC, who is independent of Solaris and Minsys, and who takes responsibility for the estimates. The Mineral Reserves estimates for the Project assume open pit mining and are summarized in Table 3. They cover the Warintza Central and East areas and are composed of 1.3 billion tonnes of combined Proven and Probable Reserves with an average copper grade of 0.31% and an average molybdenum grade of 0.02%. Of the 1.3 billion tonnes of ore, 797 Mt, or approximately 61%, are in the Proven category, and 503 Mt, or approximately 39%, are in the Probable category. The effective date of the Mineral Reserve statement is May 1, 2025.

| ● | Resource base: Mineral Reserves are based on Measured and Indicated Resources; Inferred Resources are excluded. |

| ● | Block model: Reserve block model derived from the Resource block model; regularized to 25 m × 25 m × 15 m blocks for mining selectivity. |

| ● | Pit optimization: conducted using Hexagon MinePlanTM; NSR calculated per block considering metal grades, metallurgical recoveries, metal prices, transportation, treatment / refining charges, and royalties. |

| ● | Classification of material types: material types defined by copper soluble ratio (“CSR”): oxide (greater than (>) 50%), mixed (30–50%), sulphide (<30%). |

| ● | Selected pit shell: revenue factor of 0.45, respecting 1.3 billion tonnes tailings storage capacity. |

| ● | Economic cut-off: NSR-based cut-off of US$6.30/t and copper cut-off grade of 0.1%. |

| ● | Ore loss and dilution: 1.0% dilution and 0.6% ore loss from block model regularization; no additional modifying factors applied. The QP considers the ore loss and dilution associated with the regularization are appropriate. |

| ● | Mine design and phasing: ultimate pit divided into eight phases; design includes pit slopes, haul roads, and catch benches to support LOM scheduling. |

| ● | Economic viability: Project is considered economically viable under current assumptions, with potential for larger pit size if additional tailings storage capacity becomes available. |

Table 3: Mineral Reserve Estimate as of May 1, 2025

| Classification | Tonnes | Grade | Contained metal | |||||||

| (Mt) | Cu (%) |

Mo (%) |

Au (g/t) |

Ag (g/t) |

Copper Equivalent (%) |

Cu (Mt) |

Mo (kt) |

Au (Moz) |

Ag (Moz) | |

| Proven | 797 | 0.37 | 0.02 | 0.05 | 1.37 | 0.49 | 3.0 | 171 | 1.2 | 35.0 |

| Probable | 503 | 0.22 | 0.01 | 0.03 | 1.19 | 0.28 | 1.1 | 43 | 0.6 | 19.2 |

| Total | 1,300 | 0.31 | 0.02 | 0.04 | 1.30 | 0.41 | 4.1 | 214 | 1.8 | 54.1 |

| (1) | CIM Definition Standards (2014) were used for reporting the Mineral Reserves. |

| (2) | The Qualified Person is Eugene Tucker, P.Eng. of AMC. |

| (3) | A NSR cut-off value of US$6.30/tonne and 0.1% copper cut-off grade were used. |

| (4) | Metal prices: copper US$4.00/lb, molybdenum US$20.00/lb, gold US$1,850/troy oz, and silver US$20.00/troy oz. |

| (5) | Respective metallurgical recoveries (oxide, mixed, sulphide): copper 40,85,88%; molybdenum 0,60,65%; gold 0,60,65%; silver 0,60,65%. |

| (6) | Respective payable metal: copper 96.5%, gold 91%, silver 91%, molybdenum 100%. |

16

| (7) | Copper-equivalent grade calculation assumes metal prices and recoveries as per above and includes provisions for downstream selling costs: |

| ● | Sulphide CuEq (%) = Cu (%) + 3.94 × Mo (%) + 0.52 × Au (g/t) + 0.01 x Ag (g/t). |

| ● | Mixed CuEq (%) = Cu (%) + 3.76 × Mo (%) + 0.50 × Au (g/t) + 0.005 x Ag (g/t). |

| ● | Oxide CuEq (%) = Cu (%). |

| (8) | Oxide and mixed material account for less than 0.02% of the total Mineral Reserves. |

| (9) | Mineral Reserves are converted from Mineral Resources through the process of pit optimization, pit design, and production scheduling, and are supported by a positive cash flow model. |

| (10) | Numbers may not compute exactly due to rounding. |

| (11) | Probable Mineral Reserves are based on Indicated Mineral Resources only. |

| (12) | Proven Mineral Reserves are based on Measured Mineral Resources only. |

| (13) | Mineral Reserve estimates are as of May 1, 2025. Mineral Reserve estimates are limited to the portion of the Measured and Indicated Resource estimates scheduled for milling and included in the financial model of the Technical Report. |

The following items could result in material changes to the estimated Mineral Reserves:

| ● | The assumed ore loss and dilution factors will need to be achieved. An on-going reconciliation process should be conducted, with factors adjusted based on the reconciliation information. |

| ● | The estimated metallurgical recoveries will need to be achieved. The assumed recoveries are based on currently available information from a limited amount of test work. As the Project evolves and additional information becomes available, the recovery assumptions should be reviewed and updated if required. |

| ● | The geological interpretation of mineralization geometry and the continuity of mineralization zones are based on the currently available information. |

| ● | Changes in metal prices will have an impact on the Mineral Reserve estimate. The projected impact of metal price change on the overall Project economics is highlighted in Section 22 of the Technical Report. |

| ● | The assumed capital and operating costs may change due to the impact of inflation and operational factors. |

| ● | The assumed geotechnical and hydrogeological parameters may change, impacting the design of the pit walls, tailings storage facility, and waste rock storage facility. Change in pit wall angle assumptions has the most direct impact on the estimate for Mineral Reserves. |

| ● | The Project is currently at the PFS stage, where some of the environmental and permitting conditions have yet to be realized. These conditions may result in changes to the designs of key infrastructure, which may impact the Mineral Reserve estimation. |

Mining Methods

Mining at Warintza will be undertaken by conventional open-pit, truck-and-shovel methods, with support from loaders for narrower working areas and stockpile reclaim. The operation will be developed through two main pits, Warintza Central and Warintza East, subdivided into eight phases to optimize grade sequencing and maintain low strip ratios in the early years of operation. Peak total material movement is estimated at ~160 million tonnes per year (“Mt/y”), with steady-state ore production of ~60.2 Mt/y to support a mine life of approximately 22 years.

17

The geotechnical design parameters for the open pit are based on the geotechnical site investigation program conducted by Solaris under the guidance of KP and the subsequent geotechnical evaluation completed by KP in 2024 and 2025. The following data sources were referenced in the pit slope design and optimization work:

| ● | Lithology models. |

| ● | Regional structural (faults) models. |

| ● | Structural data such as joint sets from the geotechnical site investigation. |

| ● | Rock mass property information. |

| ● | Rock strength data. |

| ● | Hydrogeological data. |

The LOM production schedule is developed with Hexagon’s Mine Plan Strategic OptimizerTM, where the software balances the series of constraints while maximizing the net present value (“NPV”) of the schedule.

A key constraint on mine scheduling is the permitted storage capacity of the TMF, which is limited to 1.3 billion tonnes in accordance with the approved EIA. This restriction governs the maximum amount of ore that can be processed during the mine life.

The mining fleet will be owner-operated following a two-year pre-stripping period. Primary equipment will include 120-ton class cable shovels, 70-ton wheel loaders, and 320-ton haul trucks, supported by dozers, graders, and water trucks. Pit designs incorporate bench heights of 15-30 m, dual-lane haul roads at 40 m width, and slope angles ranging from 36° to 47°, depending on geotechnical domains. Drilling and blasting will be carried out on 15 m benches using 311 mm diameter holes, with annual explosives consumption ranging from 46,000-58,000 t at peak production.

The production schedule emphasizes high-grade ore delivery in the initial years, supported by the use of stockpiles. Approximately 221 Mt of low-grade ore is projected to be stockpiled for processing in the later years, with remaining low-grade balances constrained by tailings storage limits. Waste rock will be placed in engineered facilities designed to meet stability standards under static, pseudo-static, and post-earthquake conditions. In the final years of the mine life, ore supply will transition to be primarily from stockpile reclaim before progressing to closure and reclamation activities. The projected annual production is summarized in Table 4.

Table 4: Annual production quantities

| Year | Mill Feed | Stockpile movement | Waste (Mt) |

Total Material moved (Mt) | |||||||

| Ore (Mt) |

Cu (%) |

Mo (%) |

Au (g/t) |

Ag (g/t) |

High-grade Stockpile (in) |

High-grade Stockpile (out) |

Low-grade Stockpile (in) |

Low-grade Stockpile (out) | |||

| (Mt) | (Mt) | (Mt) | (Mt) | ||||||||

| Yr-2 | 4.16 | 4.16 | |||||||||

| Yr-1 | 8.35 | 29.26 | - | 38.23 | 75.84 | ||||||

| Yr1 | 54.20 | 0.43 | 0.02 | 0.05 | 1.45 | 14.81 | 3.55 | 41.54 | - | 49.45 | 160.00 |

| Yr2 | 60.23 | 0.51 | 0.03 | 0.05 | 2.22 | 48.21 | - | 26.35 | - | 25.22 | 160.00 |

| Yr3 | 60.23 | 0.45 | 0.02 | 0.06 | 1.74 | 22.54 | 17.80 | 36.07 | - | 41.16 | 160.00 |

| Yr4 | 60.23 | 0.44 | 0.03 | 0.05 | 1.26 | 33.52 | 9.77 | 46.49 | - | 19.76 | 160.00 |

| Yr5 | 60.23 | 0.35 | 0.02 | 0.05 | 1.30 | - | 27.00 | 54.47 | - | 45.30 | 160.00 |

| Yr6 | 60.23 | 0.37 | 0.02 | 0.05 | 1.18 | - | - | 48.32 | - | 51.45 | 160.00 |

| Yr7 | 60.23 | 0.38 | 0.02 | 0.05 | 1.18 | - | - | 32.81 | - | 36.97 | 130.00 |

| Yr8 | 60.23 | 0.33 | 0.02 | 0.04 | 1.30 | - | 13.09 | 23.43 | - | 36.35 | 120.00 |

| Yr9 | 60.23 | 0.33 | 0.02 | 0.04 | 1.40 | - | 20.00 | 26.85 | - | 13.75 | 100.82 |

| Yr10 | 60.23 | 0.29 | 0.02 | 0.04 | 1.57 | - | 25.00 | 15.29 | - | 24.48 | 100.00 |

| Yr11 | 60.23 | 0.24 | 0.01 | 0.04 | 1.04 | - | 5.00 | 13.18 | - | 26.59 | 100.00 |

| Yr12 | 60.23 | 0.25 | 0.01 | 0.04 | 1.08 | - | 3.00 | 1.22 | - | 28.55 | 90.00 |

| Yr13 | 60.23 | 0.32 | 0.02 | 0.04 | 1.19 | - | 3.00 | 2.96 | - | 21.82 | 85.00 |

| Yr14 | 60.23 | 0.33 | 0.02 | 0.04 | 1.12 | - | 0.23 | 0.00 | - | 19.77 | 80.00 |

| Yr15 | 60.23 | 0.32 | 0.02 | 0.04 | 1.18 | - | - | 0.05 | - | 13.31 | 73.58 |

| Yr16 | 60.23 | 0.26 | 0.01 | 0.04 | 1.22 | - | - | - | - | 9.77 | 70.00 |

| Yr17 | 60.23 | 0.27 | 0.01 | 0.04 | 1.19 | - | - | - | - | 4.15 | 64.37 |