| 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade March 3, 2026 Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you (and each of your employees, representatives, and other agents) may disclose to any and all persons the US federal income and state tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. PROPRIETARY & CONFIDENTIAL Project Jewel Discussion Materials DRAFT Preliminary – Subject to Refinement |

| 2 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Disclaimer PROPRIETARY & CONFIDENTIAL CUSTOMIZABLE FIELD FOR TITLE OR SECTION These materials have been prepared by Goldman Sachs on a confidential basis for presentation solely to the special committee (the “Special Committee”) of Jewel (the “Company”) in connection with an informational presentation which Goldman Sachs is making to the Special Committee. These materials and Goldman Sachs’ presentation relating to these materials (collectively, the “Presentation”) may not be disclosed to any third party or circulated or referred to publicly or used for or relied upon for any other purpose without the written consent of Goldman Sachs. The Presentation was not prepared with a view to public disclosure or to conform to any disclosure standards under any state, federal or international securities laws or other laws, rules or regulations, and Goldman Sachs does not take any responsibility for the use of the Presentation by persons other than those set forth above. Notwithstanding anything in this Presentation to the contrary, the Company may disclose to any person the US federal income and state income tax treatment and tax structure of any transaction described herein and all materials of any kind (including tax opinions and other tax analyses) that are provided to the Company relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. The Presentation has been prepared by the Investment Banking Division of Goldman Sachs and is not a product of its research department. Goldman Sachs and its affiliates are engaged in advisory, underwriting and financing, principal investing, sales and trading,research, investment management and other financial and non-financial activities and services for various persons and entities. Goldman Sachs and its affiliates and employees, and funds or other entities they manage or in which they invest or have other economic interest or with which they co-invest, may at any time purchase, sell, hold or vote long or short positions and investments in securities, derivatives, loans, commodities, currencies, credit default swaps and other financial instruments of the Company, any other party to any transaction and any of their respective affiliates or any currency or commodity that may be involved in any transaction. The firm’s clients and counterparties may now or in the future include persons and entities that are the subject of the Presentation and the firm may be, may have been or may become involved in other transactions and assignments with or involving these clients and counterparties and/or may have confidential information relating to these clients or counterparties. The Presentation is neither an expressed nor an implied commitment by Goldman Sachs to act in any capacity with respect to the Special Committee or the Company, which commitment shall only be set forth in an engagement letter to be executed between the Special Committee, the Company and Goldman Sachs, and does not restrict Goldman Sachs from being engaged by, or otherwise acting with, any other party in any capacity. Nothing contained herein shall be deemed to create a fiduciary, advisory, agency or other relationship between Goldman Sachs and the Special Committee, the Company or its stockholders, directors, officers, employees or creditors, nor shall any of the foregoing persons rely on this document or the presentation thereof. The Presentation has been prepared based on historical financial information, forecasts and other information obtained by Goldman Sachs from publicly available sources (other than information regarding the Company, which may have been obtained from the management of the Company). In preparing the Presentation, Goldman Sachs has relied upon and assumed, without assuming any responsibility for independent verification, the accuracy and completeness of all of the financial, legal, regulatory, tax, accounting and other information provided to, discussed with or reviewed by us, and Goldman Sachs does not assume any liability for any such information. Goldman Sachs does not provide accounting, tax, legal or regulatory advice. Goldman Sachs has not made an independent evaluation or appraisal of the assets and liabilities (including any contingent, derivative or off-balance sheet assets and liabilities) of the Company or any other party to any transaction or any of their respective affiliates and has no obligation to evaluate the solvency of the Company or any other party to any transaction under any state or federal laws relating to bankruptcy, insolvency or similar matters. The analyses contained in the Presentation do not purport to be appraisals nor do they necessarily reflect the prices at which businesses or securities actually may be sold or purchased. Any indications of value or synergies in the Presentation are based solely on public information, are for illustrative purposes only, and do not reflect actual values or synergies that may be achieved or realized by the Company or any views of Goldman Sachs with respect to any such values or synergies. The Presentation does not address the underlying business decision of the Special Committee or the Company to engage in any transaction, or the relative merits of any transaction or strategic alternative as compared to any other transaction or alternative that may be available to the Company. The Presentation is necessarily based on economic, monetary, market and other conditions as in effect on, and the information made available to Goldman Sachs as of, the date of such Presentation and Goldman Sachs assumes no responsibility for updating or revising the Presentation based on circumstances, developments or events occurring after such date. The Presentation does not constitute any opinion, nor does the Presentation constitute a recommendation to the Special Committee, the Company, any security holder of the Company or any other person as to how to vote or act with respect to any transaction or any other matter. The Presentation, including this disclaimer, are subject to, and governed by, any written agreement between the Special Committee, the Company and Goldman Sachs. |

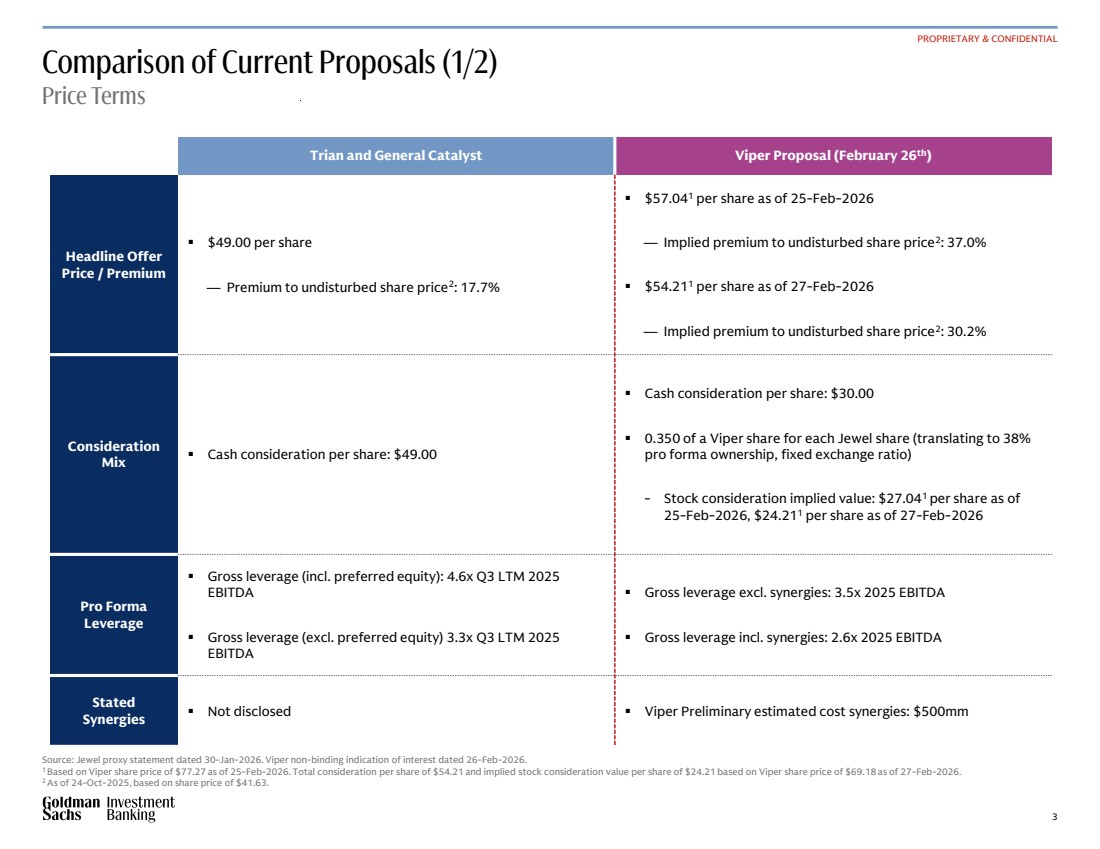

| 3 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Comparison of Current Proposals (1/2) Price Terms Source: Jewel proxy statement dated 30-Jan-2026. Viper non-binding indication of interest dated 26-Feb-2026. 1 Based on Viper share price of $77.27 as of 25-Feb-2026. Total consideration per share of $54.21 and implied stock consideration value per share of $24.21 based on Viper share price of $69.18 as of 27-Feb-2026. 2 As of 24-Oct-2025, based on share price of $41.63. PROPRIETARY & CONFIDENTIAL Trian and General Catalyst Viper Proposal (February 26th) Headline Offer Price / Premium ▪ $49.00 per share — Premium to undisturbed share price2 : 17.7% ▪ $57.041 per share as of 25-Feb-2026 — Implied premium to undisturbed share price2 : 37.0% ▪ $54.211 per share as of 27-Feb-2026 — Implied premium to undisturbed share price2 : 30.2% Consideration Mix ▪ Cash consideration per share: $49.00 ▪ Cash consideration per share: $30.00 ▪ 0.350 of a Viper share for each Jewel share (translating to 38% pro forma ownership, fixed exchange ratio) - Stock consideration implied value: $27.041 per share as of 25-Feb-2026, $24.211 per share as of 27-Feb-2026 Pro Forma Leverage ▪ Gross leverage (incl. preferred equity): 4.6x Q3 LTM 2025 EBITDA ▪ Gross leverage (excl. preferred equity) 3.3x Q3 LTM 2025 EBITDA ▪ Gross leverage excl. synergies: 3.5x 2025 EBITDA ▪ Gross leverage incl. synergies: 2.6x 2025 EBITDA Stated Synergies ▪ Not disclosed ▪ Viper Preliminary estimated cost synergies: $500mm |

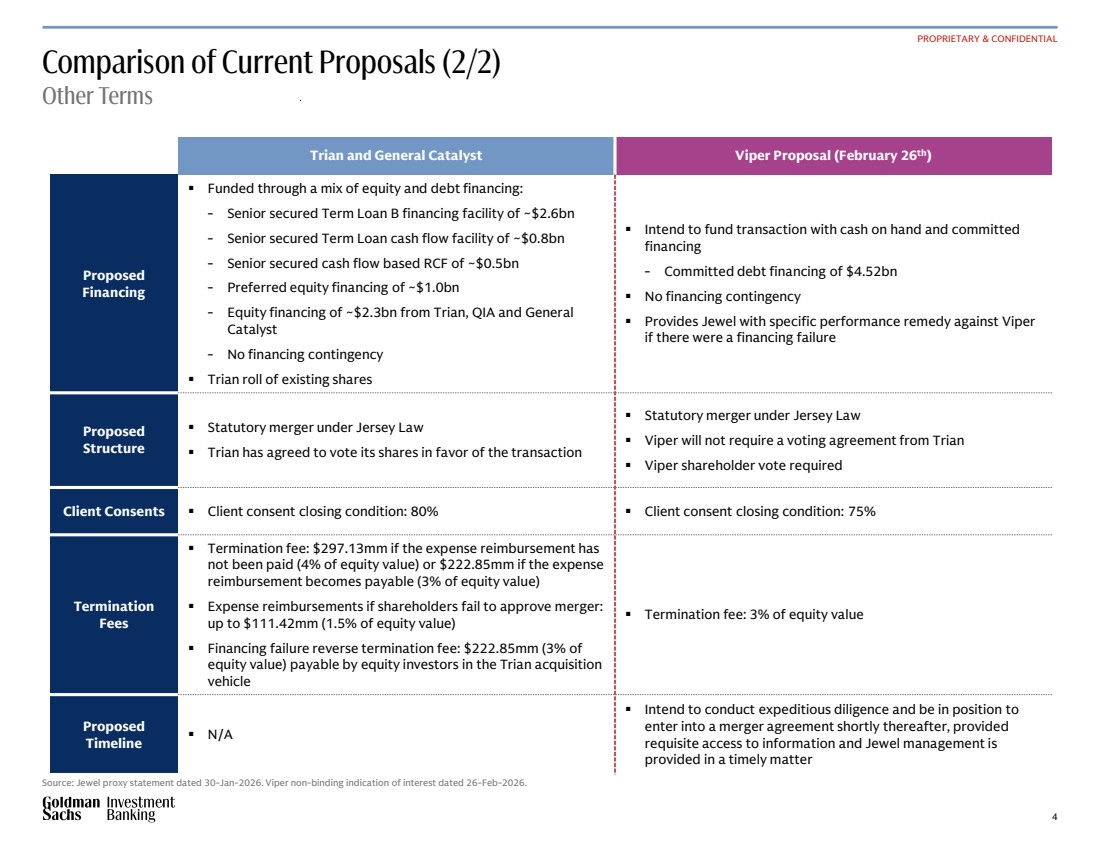

| 4 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Comparison of Current Proposals (2/2) Other Terms Source: Jewel proxy statement dated 30-Jan-2026. Viper non-binding indication of interest dated 26-Feb-2026. PROPRIETARY & CONFIDENTIAL Trian and General Catalyst Viper Proposal (February 26th) Proposed Financing ▪ Funded through a mix of equity and debt financing: - Senior secured Term Loan B financing facility of ~$2.6bn - Senior secured Term Loan cash flow facility of ~$0.8bn - Senior secured cash flow based RCF of ~$0.5bn - Preferred equity financing of ~$1.0bn - Equity financing of ~$2.3bn from Trian, QIA and General Catalyst - No financing contingency ▪ Trian roll of existing shares ▪ Intend to fund transaction with cash on hand and committed financing - Committed debt financing of $4.52bn ▪ No financing contingency ▪ Provides Jewel with specific performance remedy against Viper if there were a financing failure Proposed Structure ▪ Statutory merger under Jersey Law ▪ Trian has agreed to vote its shares in favor of the transaction ▪ Statutory merger under Jersey Law ▪ Viper will not require a voting agreement from Trian ▪ Viper shareholder vote required Client Consents ▪ Client consent closing condition: 80% ▪ Client consent closing condition: 75% Termination Fees ▪ Termination fee: $297.13mm if the expense reimbursement has not been paid (4% of equity value) or $222.85mm if the expense reimbursement becomes payable (3% of equity value) ▪ Expense reimbursements if shareholders fail to approve merger: up to $111.42mm (1.5% of equity value) ▪ Financing failure reverse termination fee: $222.85mm (3% of equity value) payable by equity investors in the Trian acquisition vehicle ▪ Termination fee: 3% of equity value Proposed Timeline ▪ N/A ▪ Intend to conduct expeditious diligence and be in position to enter into a merger agreement shortly thereafter, provided requisite access to information and Jewel management is provided in a timely matter |

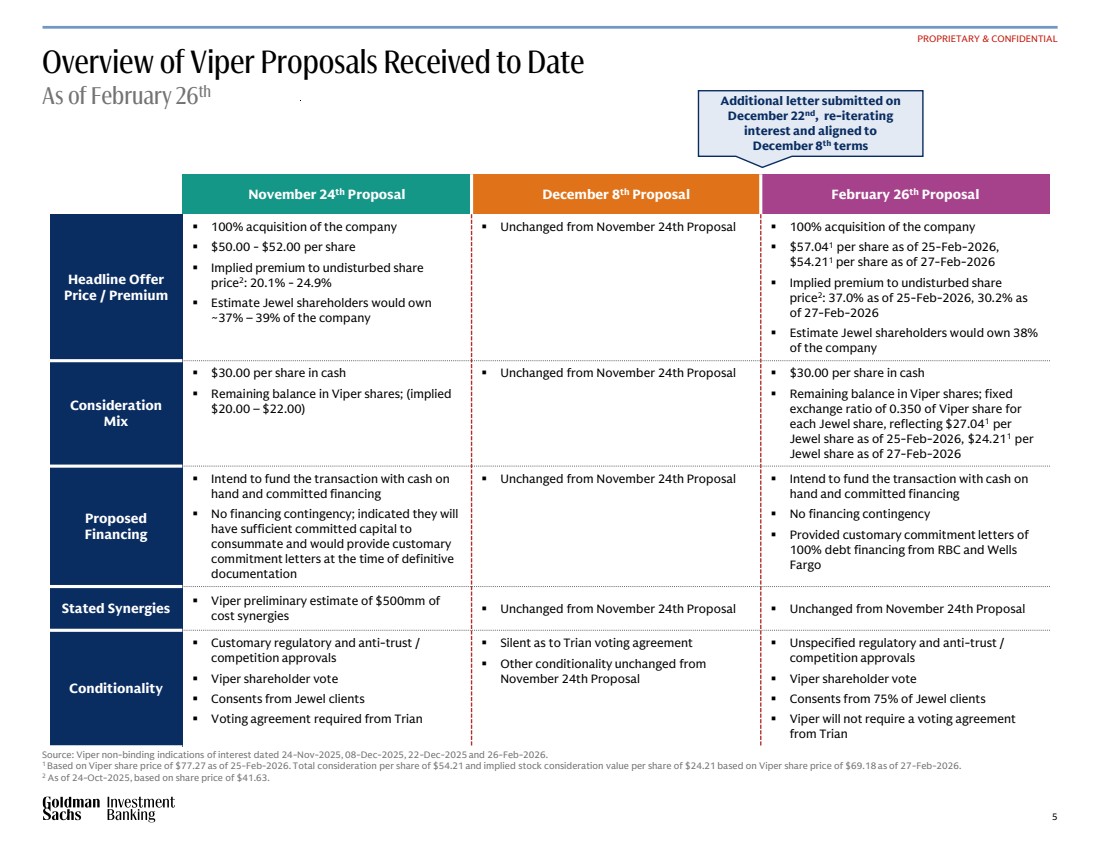

| 5 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Overview of Viper Proposals Received to Date As of February 26th Source: Viper non-binding indications of interest dated 24-Nov-2025, 08-Dec-2025, 22-Dec-2025 and 26-Feb-2026. 1 Based on Viper share price of $77.27 as of 25-Feb-2026. Total consideration per share of $54.21 and implied stock consideration value per share of $24.21 based on Viper share price of $69.18 as of 27-Feb-2026. 2 As of 24-Oct-2025, based on share price of $41.63. PROPRIETARY & CONFIDENTIAL November 24th Proposal December 8th Proposal February 26th Proposal Headline Offer Price / Premium ▪ 100% acquisition of the company ▪ $50.00 - $52.00 per share ▪ Implied premium to undisturbed share price2 : 20.1% - 24.9% ▪ Estimate Jewel shareholders would own ~37% – 39% of the company ▪ Unchanged from November 24th Proposal ▪ 100% acquisition of the company ▪ $57.041 per share as of 25-Feb-2026, $54.211 per share as of 27-Feb-2026 ▪ Implied premium to undisturbed share price2 : 37.0% as of 25-Feb-2026, 30.2% as of 27-Feb-2026 ▪ Estimate Jewel shareholders would own 38% of the company Consideration Mix ▪ $30.00 per share in cash ▪ Remaining balance in Viper shares; (implied $20.00 – $22.00) ▪ Unchanged from November 24th Proposal ▪ $30.00 per share in cash ▪ Remaining balance in Viper shares; fixed exchange ratio of 0.350 of Viper share for each Jewel share, reflecting $27.041 per Jewel share as of 25-Feb-2026, $24.211 per Jewel share as of 27-Feb-2026 Proposed Financing ▪ Intend to fund the transaction with cash on hand and committed financing ▪ No financing contingency; indicated they will have sufficient committed capital to consummate and would provide customary commitment letters at the time of definitive documentation ▪ Unchanged from November 24th Proposal ▪ Intend to fund the transaction with cash on hand and committed financing ▪ No financing contingency ▪ Provided customary commitment letters of 100% debt financing from RBC and Wells Fargo Stated Synergies ▪ Viper preliminary estimate of $500mm of cost synergies ▪ Unchanged from November 24th Proposal ▪ Unchanged from November 24th Proposal Conditionality ▪ Customary regulatory and anti-trust / competition approvals ▪ Viper shareholder vote ▪ Consents from Jewel clients ▪ Voting agreement required from Trian ▪ Silent as to Trian voting agreement ▪ Other conditionality unchanged from November 24th Proposal ▪ Unspecified regulatory and anti-trust / competition approvals ▪ Viper shareholder vote ▪ Consents from 75% of Jewel clients ▪ Viper will not require a voting agreement from Trian Additional letter submitted on December 22nd, re-iterating interest and aligned to December 8th terms |

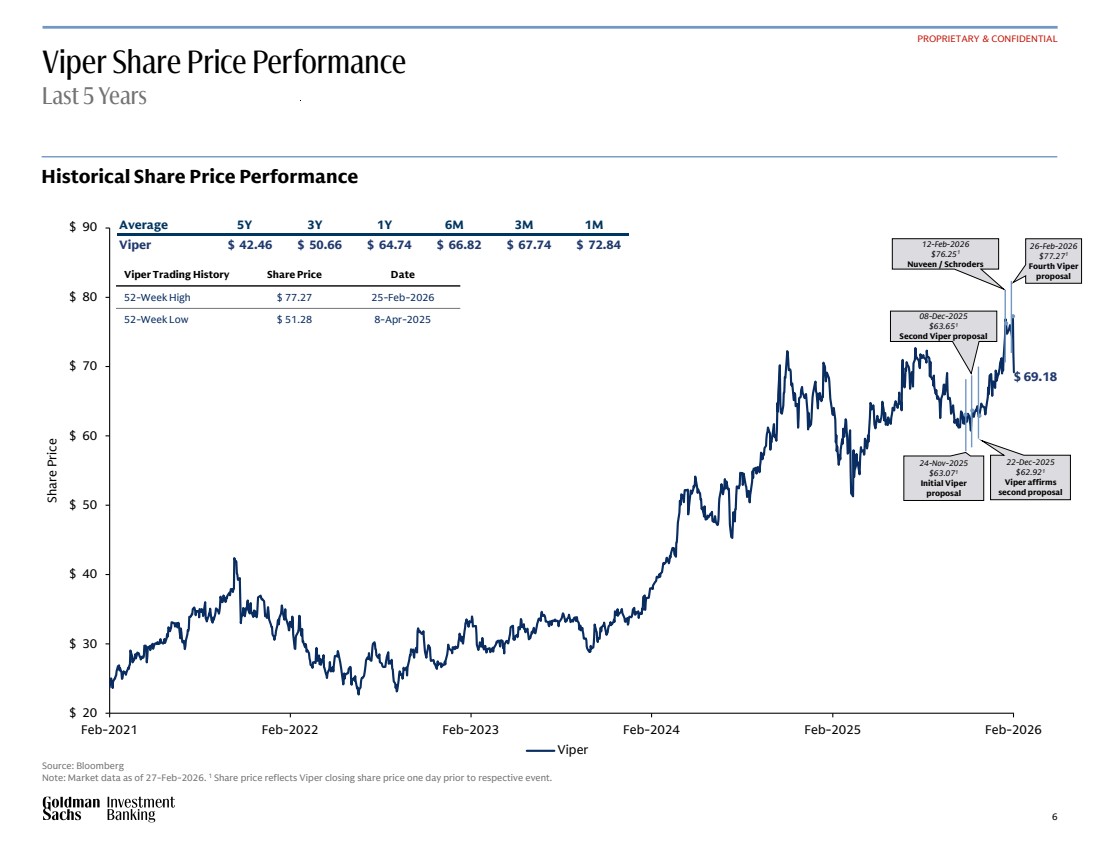

| 6 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade $ 69.18 $ 20 $ 30 $ 40 $ 50 $ 60 $ 70 $ 80 $ 90 Feb-2021 Feb-2022 Feb-2023 Feb-2024 Feb-2025 Feb-2026 Share Price Viper Viper Share Price Performance Last 5 Years Historical Share Price Performance Source: Bloomberg Note: Market data as of 27-Feb-2026. 1 Share price reflects Viper closing share price one day prior to respective event. PROPRIETARY & CONFIDENTIAL 24-Nov-2025 $63.071 Initial Viper proposal 08-Dec-2025 $63.651 Second Viper proposal 22-Dec-2025 $62.921 Viper affirms second proposal 26-Feb-2026 $77.271 Fourth Viper proposal 12-Feb-2026 $76.251 Nuveen / Schroders Viper Trading History Share Price Date 52-Week High $ 77.27 25-Feb-2026 52-Week Low $ 51.28 8-Apr-2025 Average 5Y 3Y 1Y 6M 3M 1M Viper $ 42.46 $ 50.66 $ 64.74 $ 66.82 $ 67.74 $ 72.84 |

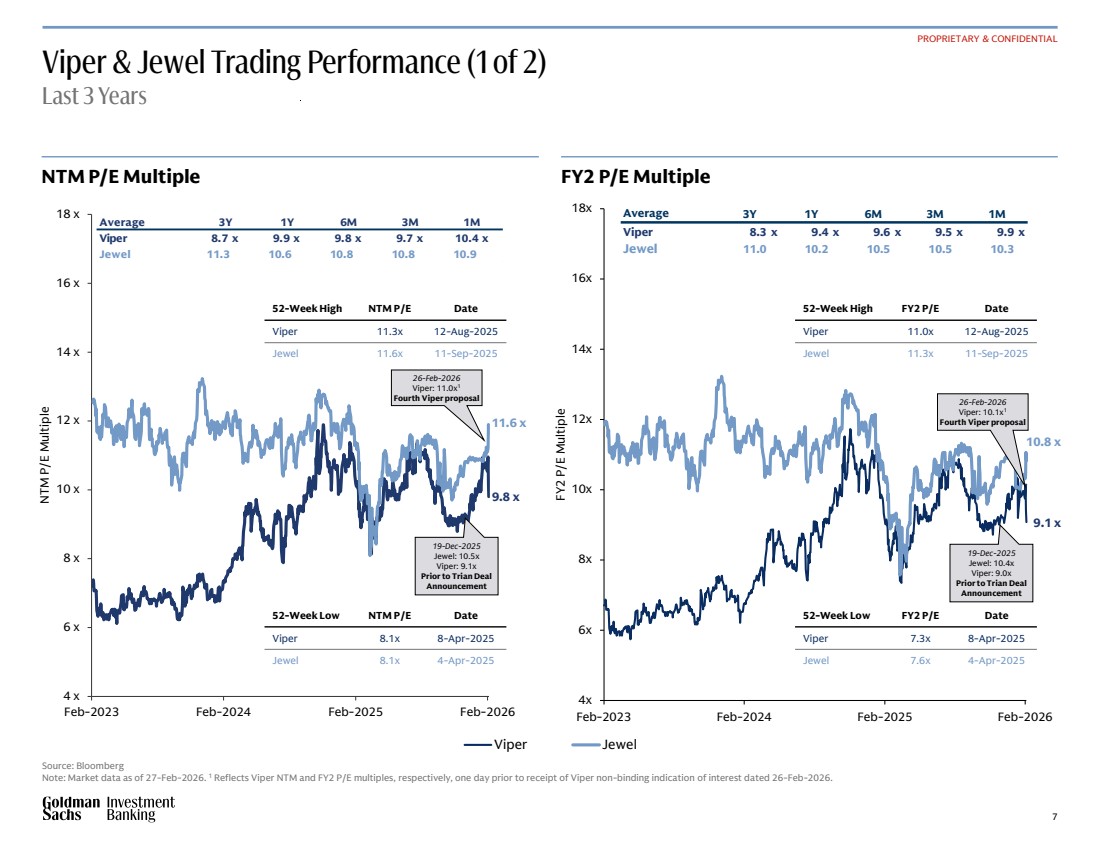

| 7 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade 11.6 x 4 x 6 x 8 x 10 x 12 x 14 x 16 x 18 x Feb-2023 Feb-2024 Feb-2025 Feb-2026 NTM P/E Multiple 9.8 x Average 3Y 1Y 6M 3M 1M Viper 8.7 x 9.9 x 9.8 x 9.7 x 10.4 x Jewel 11.3 10.6 10.8 10.8 10.9 9.1 x 10.8 x 4x 6x 8x 10x 12x 14x 16x 18x Feb-2023 Feb-2024 Feb-2025 Feb-2026 FY2 P/E Multiple Viper & Jewel Trading Performance (1 of 2) Last 3 Years NTM P/E Multiple FY2 P/E Multiple Source: Bloomberg Note: Market data as of 27-Feb-2026. 1 Reflects Viper NTM and FY2 P/E multiples, respectively, one day prior to receipt of Viper non-binding indication of interest dated 26-Feb-2026. PROPRIETARY & CONFIDENTIAL 10.1 x 10.4 x 4x 6x 8x 10x 12x 14x 16x 18x Feb-2021 Feb-2022 Feb-2023 Feb-2024 Feb-2025 Feb-2026 FY1 P/E Multiple Viper Jewel 52-Week High FY2 P/E Date Viper 11.0x 12-Aug-2025 Jewel 11.3x 11-Sep-2025 52-Week Low FY2 P/E Date Viper 7.3x 8-Apr-2025 Jewel 7.6x 4-Apr-2025 52-Week High NTM P/E Date Viper 11.3x 12-Aug-2025 Jewel 11.6x 11-Sep-2025 52-Week Low NTM P/E Date Viper 8.1x 8-Apr-2025 Jewel 8.1x 4-Apr-2025 26-Feb-2026 Viper: 10.1x1 Fourth Viper proposal Average 3Y 1Y 6M 3M 1M Viper 8.3 x 9.4 x 9.6 x 9.5 x 9.9 x Jewel 11.0 10.2 10.5 10.5 10.3 19-Dec-2025 Jewel: 10.4x Viper: 9.0x Prior to Trian Deal Announcement 26-Feb-2026 Viper: 11.0x1 Fourth Viper proposal 19-Dec-2025 Jewel: 10.5x Viper: 9.1x Prior to Trian Deal Announcement |

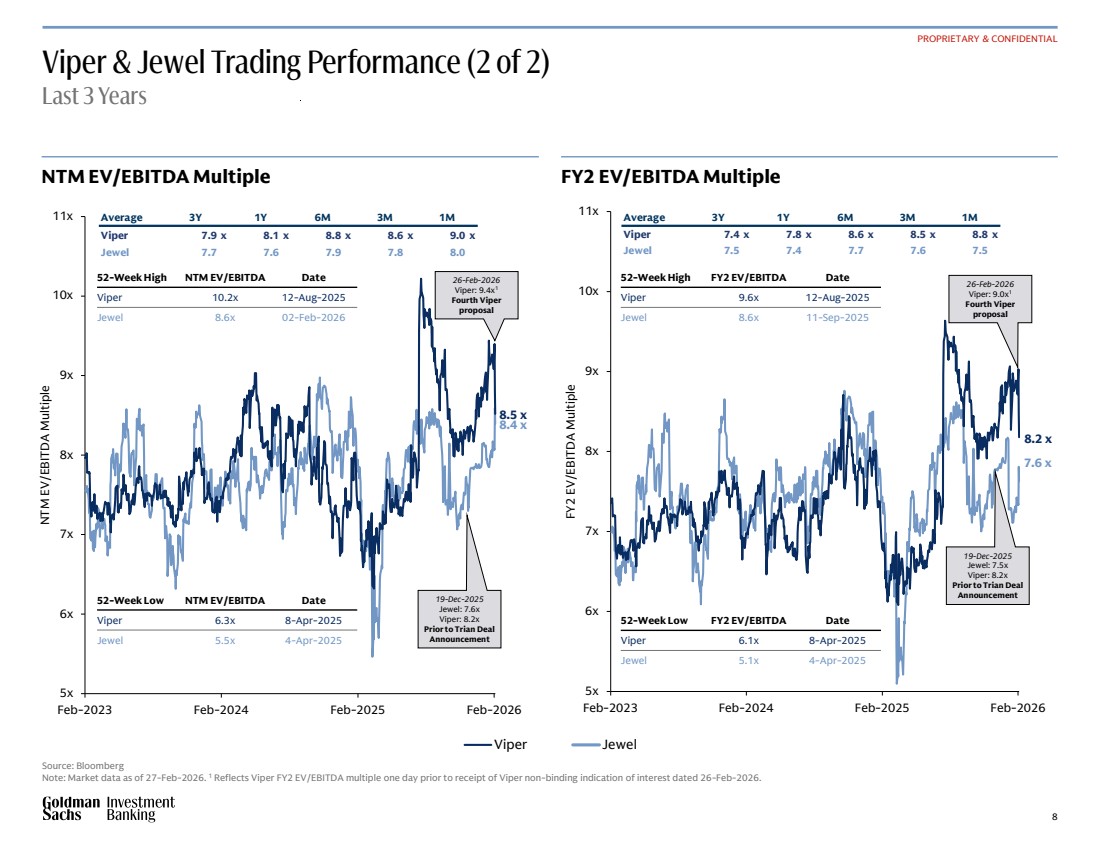

| 8 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade 8.4 x 8.5 x 5x 6x 7x 8x 9x 10x 11x Feb-2023 Feb-2024 Feb-2025 Feb-2026 NTM EV/EBITDA Multiple 7.6 x 8.2 x 5x 6x 7x 8x 9x 10x 11x Feb-2023 Feb-2024 Feb-2025 Feb-2026 FY2 EV/EBITDA Multiple Viper & Jewel Trading Performance (2 of 2) Last 3 Years NTM EV/EBITDA Multiple FY2 EV/EBITDA Multiple Source: Bloomberg Note: Market data as of 27-Feb-2026. 1 Reflects Viper FY2 EV/EBITDA multiple one day prior to receipt of Viper non-binding indication of interest dated 26-Feb-2026. PROPRIETARY & CONFIDENTIAL 10.1 x 10.4 x 4x 6x 8x 10x 12x 14x 16x 18x Feb-2021 Feb-2022 Feb-2023 Feb-2024 Feb-2025 Feb-2026 FY1 P/E Multiple Viper Jewel 52-Week High NTM EV/EBITDA Date Viper 10.2x 12-Aug-2025 Jewel 8.6x 02-Feb-2026 26-Feb-2026 Viper: 9.0x1 Fourth Viper proposal 52-Week Low NTM EV/EBITDA Date Viper 6.3x 8-Apr-2025 Jewel 5.5x 4-Apr-2025 52-Week High FY2 EV/EBITDA Date Viper 9.6x 12-Aug-2025 Jewel 8.6x 11-Sep-2025 52-Week Low FY2 EV/EBITDA Date Viper 6.1x 8-Apr-2025 Jewel 5.1x 4-Apr-2025 19-Dec-2025 Jewel: 7.5x Viper: 8.2x Prior to Trian Deal Announcement Average 3Y 1Y 6M 3M 1M Viper 7.9 x 8.1 x 8.8 x 8.6 x 9.0 x Jewel 7.7 7.6 7.9 7.8 8.0 Average 3Y 1Y 6M 3M 1M Viper 7.4 x 7.8 x 8.6 x 8.5 x 8.8 x Jewel 7.5 7.4 7.7 7.6 7.5 26-Feb-2026 Viper: 9.4x1 Fourth Viper proposal 19-Dec-2025 Jewel: 7.6x Viper: 8.2x Prior to Trian Deal Announcement |

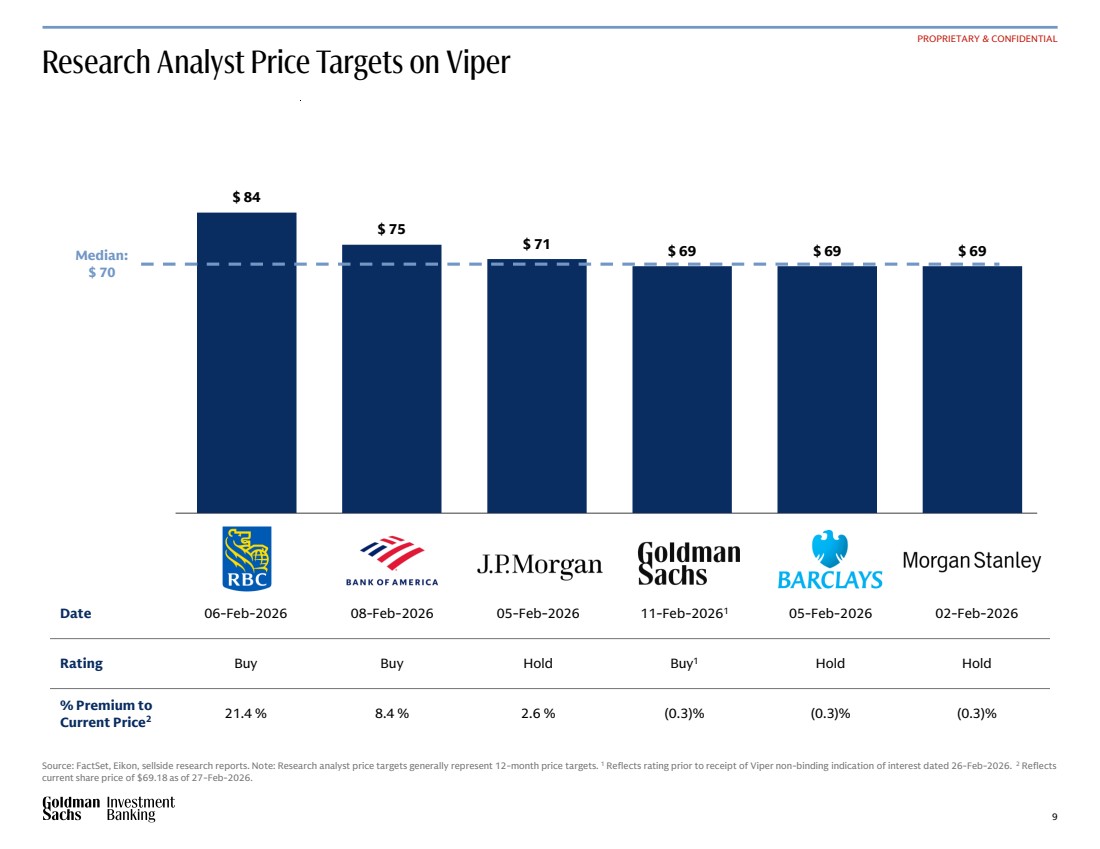

| 9 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Research Analyst Price Targets on Viper Source: FactSet, Eikon, sellside research reports. Note: Research analyst price targets generally represent 12-month price targets. 1 Reflects rating prior to receipt of Viper non-binding indication of interest dated 26-Feb-2026. 2 Reflects current share price of $69.18 as of 27-Feb-2026. PROPRIETARY & CONFIDENTIAL Date 06-Feb-2026 08-Feb-2026 05-Feb-2026 11-Feb-20261 05-Feb-2026 02-Feb-2026 Rating Buy Buy Hold Buy1 Hold Hold % Premium to Current Price2 21.4 % 8.4 % 2.6 % (0.3)% (0.3)% (0.3)% $ 69 $ 69 $ 69 $ 71 $ 75 $ 84 Median: $ 70 |

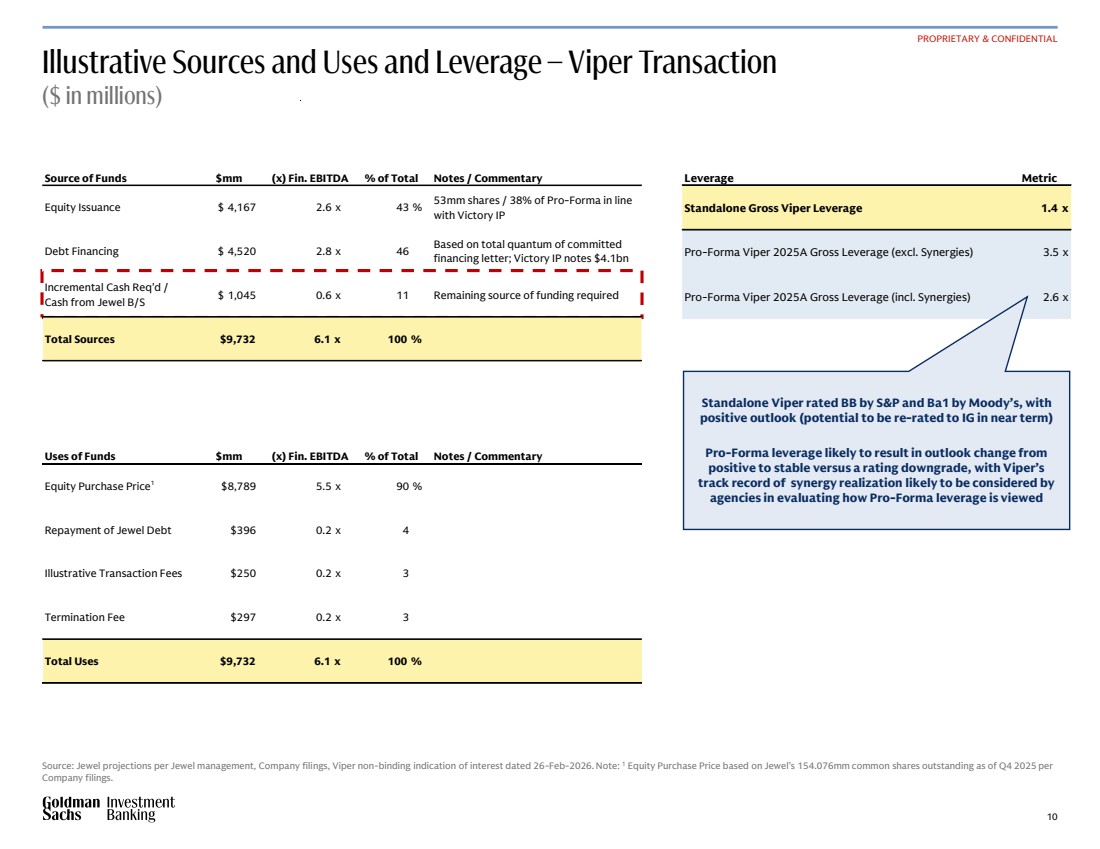

| 10 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Illustrative Sources and Uses and Leverage – Viper Transaction ($ in millions) Source: Jewel projections per Jewel management, Company filings, Viper non-binding indication of interest dated 26-Feb-2026. Note: 1 Equity Purchase Price based on Jewel’s 154.076mm common shares outstanding as of Q4 2025 per Company filings. PROPRIETARY & CONFIDENTIAL Leverage Metric Standalone Gross Viper Leverage 1.4 x Pro-Forma Viper 2025A Gross Leverage (excl. Synergies) 3.5 x Pro-Forma Viper 2025A Gross Leverage (incl. Synergies) 2.6 x Standalone Viper rated BB by S&P and Ba1 by Moody’s, with positive outlook (potential to be re-rated to IG in near term) Pro-Forma leverage likely to result in outlook change from positive to stable versus a rating downgrade, with Viper’s track record of synergy realization likely to be considered by agencies in evaluating how Pro-Forma leverage is viewed Source of Funds $mm (x) Fin. EBITDA % of Total Notes / Commentary Equity Issuance $ 4,167 2.6 x 43 % 53mm shares / 38% of Pro-Forma in line with Victory IP Debt Financing $ 4,520 2.8 x 46 Based on total quantum of committed financing letter; Victory IP notes $4.1bn Incremental Cash Req'd / Cash from Jewel B/S $ 1,045 0.6 x 11 Remaining source of funding required Total Sources $9,732 6.1 x 100 % Uses of Funds $mm (x) Fin. EBITDA % of Total Notes / Commentary Equity Purchase Price1 $8,789 5.5 x 90 % Repayment of Jewel Debt $396 0.2 x 4 Illustrative Transaction Fees $250 0.2 x 3 Termination Fee $297 0.2 x 3 Total Uses $9,732 6.1 x 100 % |

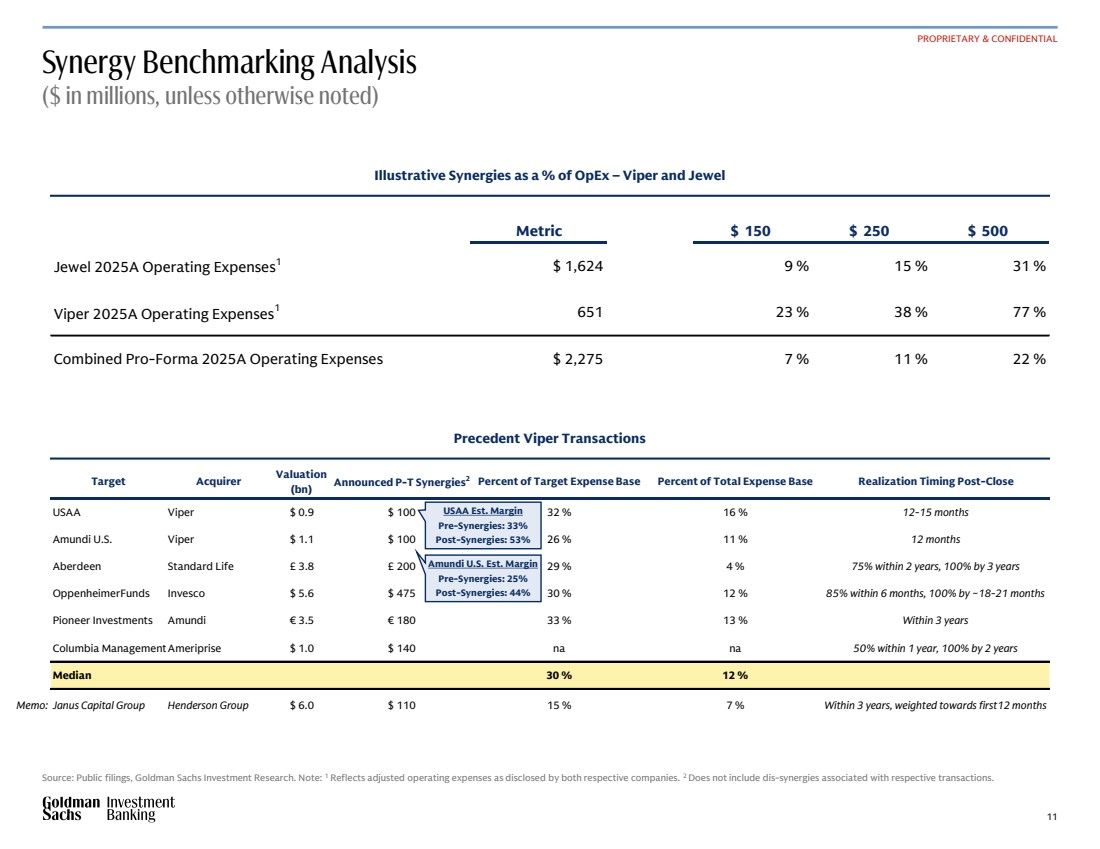

| 11 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Target Acquirer Valuation (bn) Announced P-T Synergies2 Percent of Target Expense Base Percent of Total Expense Base Realization Timing Post-Close USAA Viper $ 0.9 $ 100 32 % 16 % 12-15 months Amundi U.S. Viper $ 1.1 $ 100 26 % 11 % 12 months Aberdeen Standard Life £ 3.8 £ 200 29 % 4 % 75% within 2 years, 100% by 3 years OppenheimerFunds Invesco $ 5.6 $ 475 30 % 12 % 85% within 6 months, 100% by ~18-21 months Pioneer Investments Amundi € 3.5 € 180 33 % 13 % Within 3 years Columbia ManagementAmeriprise $ 1.0 $ 140 na na 50% within 1 year, 100% by 2 years Median 30 % 12 % Janus Capital Group Henderson Group $ 6.0 $ 110 15 % 7 % Within 3 years, weighted towards first12 months Synergy Benchmarking Analysis ($ in millions, unless otherwise noted) Source: Public filings, Goldman Sachs Investment Research. Note: 1 Reflects adjusted operating expenses as disclosed by both respective companies. 2 Does not include dis-synergies associated with respective transactions. PROPRIETARY & CONFIDENTIAL Illustrative Synergies as a % of OpEx – Viper and Jewel Precedent Viper Transactions Amundi U.S. Est. Margin Pre-Synergies: 25% Post-Synergies: 44% https://publishing.gs.com/content/research/en/reports/2024/04/17/452320c2-3430-45f8-ac62- 7510dd81b257.html#_bf7a002b-5eb2-4000-a6eb-268f86fbf000 USAA Est. Margin Pre-Synergies: 33% Post-Synergies: 53% Memo: Metric $ 150 $ 250 $ 500 Jewel 2025A Operating Expenses1 $ 1,624 9 % 15 % 31 % Viper 2025A Operating Expenses1 651 23 % 38 % 77 % Combined Pro-Forma 2025A Operating Expenses $ 2,275 7 % 11 % 22 % |

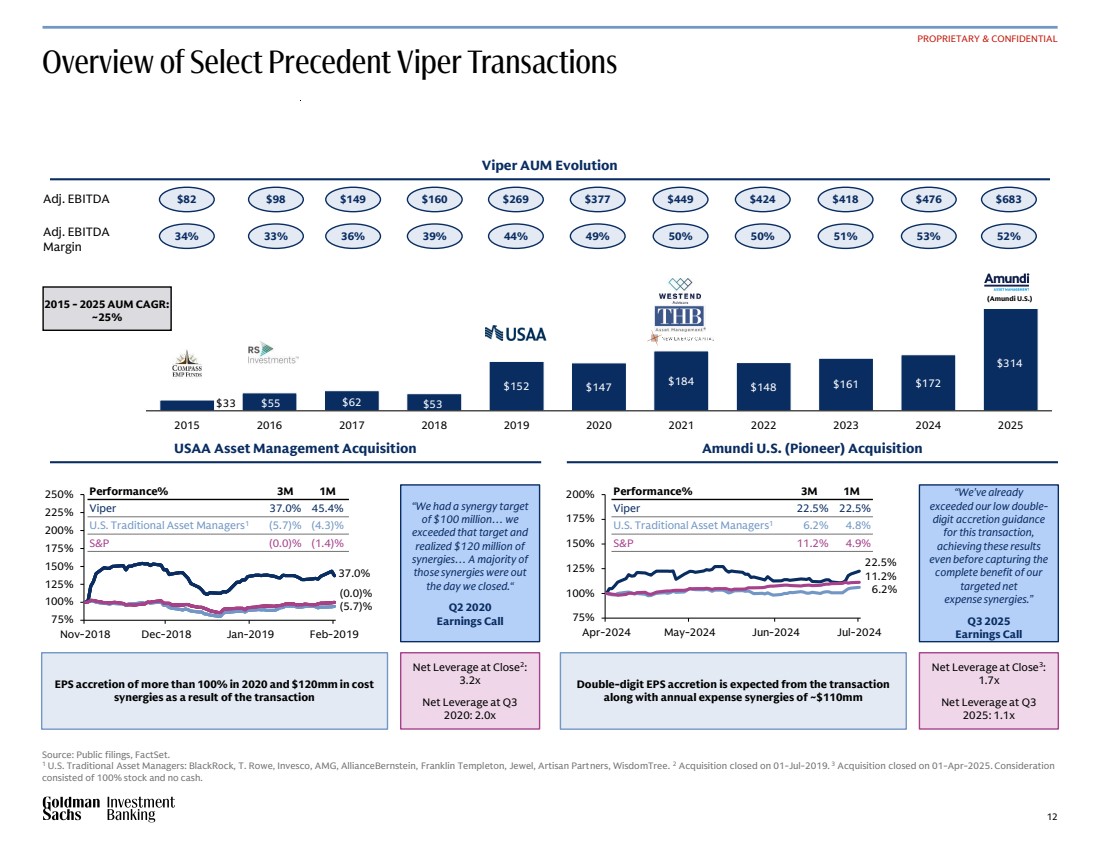

| 12 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Overview of Select Precedent Viper Transactions Source: Public filings, FactSet. 1 U.S. Traditional Asset Managers: BlackRock, T. Rowe, Invesco, AMG, AllianceBernstein, Franklin Templeton, Jewel, Artisan Partners, WisdomTree. 2 Acquisition closed on 01-Jul-2019. 3 Acquisition closed on 01-Apr-2025. Consideration consisted of 100% stock and no cash. PROPRIETARY & CONFIDENTIAL EPS accretion of more than 100% in 2020 and $120mm in cost synergies as a result of the transaction “We had a synergy target of $100 million… we exceeded that target and realized $120 million of synergies… A majority of those synergies were out the day we closed.“ Q2 2020 Earnings Call Net Leverage at Close2 : 3.2x Net Leverage at Q3 2020: 2.0x Double-digit EPS accretion is expected from the transaction along with annual expense synergies of ~$110mm “We've already exceeded our low double-digit accretion guidance for this transaction, achieving these results even before capturing the complete benefit of our targeted net expense synergies.” Q3 2025 Earnings Call Net Leverage at Close3 : 1.7x Net Leverage at Q3 2025: 1.1x 2015 - 2025 AUM CAGR: ~25% Adj. EBITDA Adj. EBITDA Margin $82 $98 $149 $160 $269 $377 $449 $424 $418 $476 $683 34% 33% 36% 39% 44% 49% 50% 50% 51% 53% 52% (Amundi U.S.) 75% 100% 125% 150% 175% 200% 225% 250% Nov-2018 Dec-2018 Jan-2019 Feb-2019 37.0% (5.7)% (0.0)% 75% 100% 125% 150% 175% 200% Apr-2024 May-2024 Jun-2024 Jul-2024 22.5% 6.2% 11.2% Performance% 3M 1M Viper 37.0% 45.4% U.S. Traditional Asset Managers1 (5.7)% (4.3)% S&P (0.0)% (1.4)% Performance% 3M 1M Viper 22.5% 22.5% U.S. Traditional Asset Managers1 6.2% 4.8% S&P 11.2% 4.9% $33 $55 $62 $53 $152 $147 $184 $148 $161 $172 $314 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Viper AUM Evolution USAA Asset Management Acquisition Amundi U.S. (Pioneer) Acquisition |

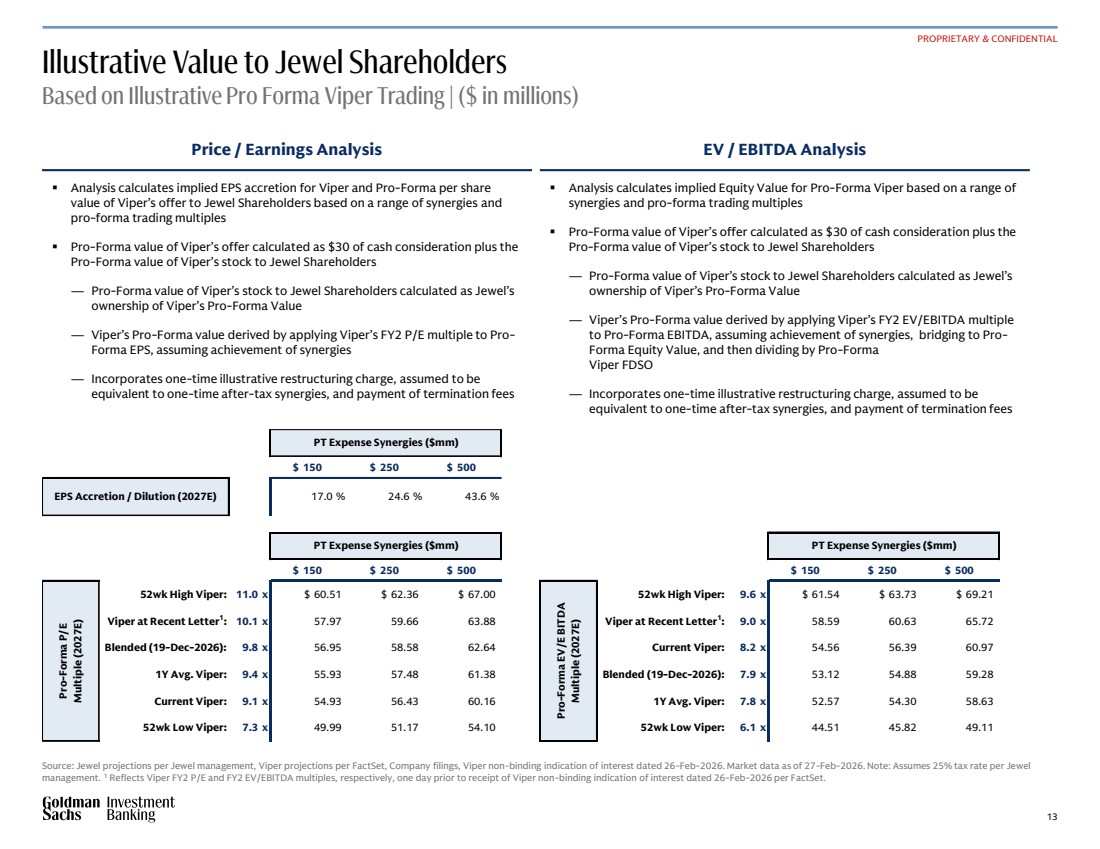

| 13 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade # ### $ 150 $ 250 $ 500 52wk High Viper: 11.0 x $ 60.51 $ 62.36 $ 67.00 Viper at Recent Letter1 : 10.1 x 57.97 59.66 63.88 Blended (19-Dec-2026): 9.8 x 56.95 58.58 62.64 1Y Avg. Viper: 9.4 x 55.93 57.48 61.38 Current Viper: 9.1 x 54.93 56.43 60.16 52wk Low Viper: 7.3 x 49.99 51.17 54.10 Pro-Forma P/E Multiple (2027E) PT Expense Synergies ($mm) # ### $ 150 $ 250 $ 500 52wk High Viper: 9.6 x $ 61.54 $ 63.73 $ 69.21 Viper at Recent Letter1 : 9.0 x 58.59 60.63 65.72 Current Viper: 8.2 x 54.56 56.39 60.97 Blended (19-Dec-2026): 7.9 x 53.12 54.88 59.28 1Y Avg. Viper: 7.8 x 52.57 54.30 58.63 52wk Low Viper: 6.1 x 44.51 45.82 49.11 PT Expense Synergies ($mm) Pro-Forma EV/E BITDA Multiple (2027E) 43.6 % $ 150 $ 250 $ 500 EPS Accretion / Dilution (2027E) 10.1 x 17.0 % 24.6 % 43.6 % PT Expense Synergies ($mm) Illustrative Value to Jewel Shareholders Based on Illustrative Pro Forma Viper Trading | ($ in millions) Source: Jewel projections per Jewel management, Viper projections per FactSet, Company filings, Viper non-binding indication of interest dated 26-Feb-2026. Market data as of 27-Feb-2026. Note: Assumes 25% tax rate per Jewel management. 1 Reflects Viper FY2 P/E and FY2 EV/EBITDA multiples, respectively, one day prior to receipt of Viper non-binding indication of interest dated 26-Feb-2026 per FactSet. PROPRIETARY & CONFIDENTIAL Price / Earnings Analysis EV / EBITDA Analysis ▪ Analysis calculates implied EPS accretion for Viper and Pro-Forma per share value of Viper’s offer to Jewel Shareholders based on a range of synergies and pro-forma trading multiples ▪ Pro-Forma value of Viper’s offer calculated as $30 of cash consideration plus the Pro-Forma value of Viper’s stock to Jewel Shareholders — Pro-Forma value of Viper’s stock to Jewel Shareholders calculated as Jewel’s ownership of Viper’s Pro-Forma Value — Viper’s Pro-Forma value derived by applying Viper’s FY2 P/E multiple to Pro-Forma EPS, assuming achievement of synergies — Incorporates one-time illustrative restructuring charge, assumed to be equivalent to one-time after-tax synergies, and payment of termination fees ▪ Analysis calculates implied Equity Value for Pro-Forma Viper based on a range of synergies and pro-forma trading multiples ▪ Pro-Forma value of Viper’s offer calculated as $30 of cash consideration plus the Pro-Forma value of Viper’s stock to Jewel Shareholders — Pro-Forma value of Viper’s stock to Jewel Shareholders calculated as Jewel’s ownership of Viper’s Pro-Forma Value — Viper’s Pro-Forma value derived by applying Viper’s FY2 EV/EBITDA multiple to Pro-Forma EBITDA, assuming achievement of synergies, bridging to Pro-Forma Equity Value, and then dividing by Pro-Forma Viper FDSO — Incorporates one-time illustrative restructuring charge, assumed to be equivalent to one-time after-tax synergies, and payment of termination fees |

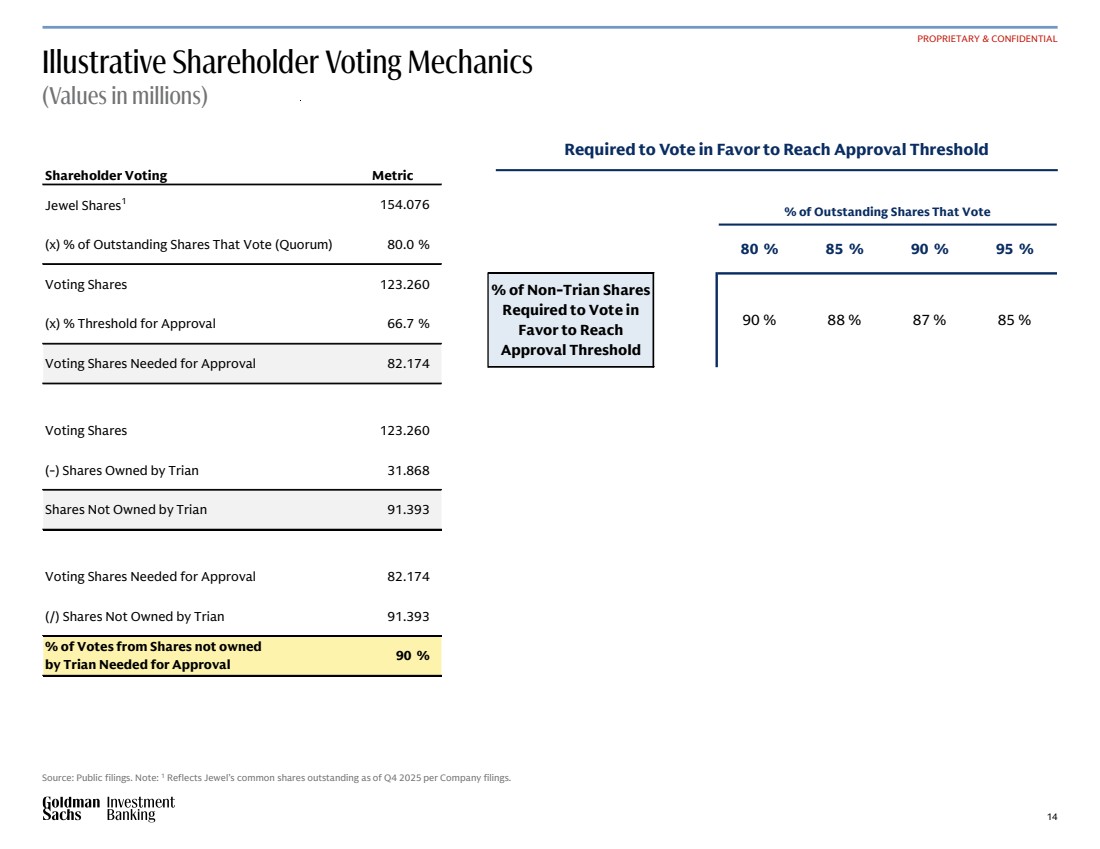

| 14 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Illustrative Shareholder Voting Mechanics (Values in millions) Source: Public filings. Note: 1 Reflects Jewel’s common shares outstanding as of Q4 2025 per Company filings. PROPRIETARY & CONFIDENTIAL Required to Vote in Favor to Reach Approval Threshold % of Outstanding Shares That Vote 89.9 % 80 % 85 % 90 % 95 % % of Non-Trian Shares Required to Vote in Favor to Reach Approval Threshold 66.7 % 90 % 88 % 87 % 85 % Shareholder Voting Metric Jewel Shares1 154.076 (x) % of Outstanding Shares That Vote (Quorum) 80.0 % Voting Shares 123.260 (x) % Threshold for Approval 66.7 % Voting Shares Needed for Approval 82.174 Voting Shares 123.260 (-) Shares Owned by Trian 31.868 Shares Not Owned by Trian 91.393 Voting Shares Needed for Approval 82.174 (/) Shares Not Owned by Trian 91.393 % of Votes from Shares not owned by Trian Needed for Approval 90 % |

| 15 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Appendix A: Supplemental Materials PROPRIETARY & CONFIDENTIAL |

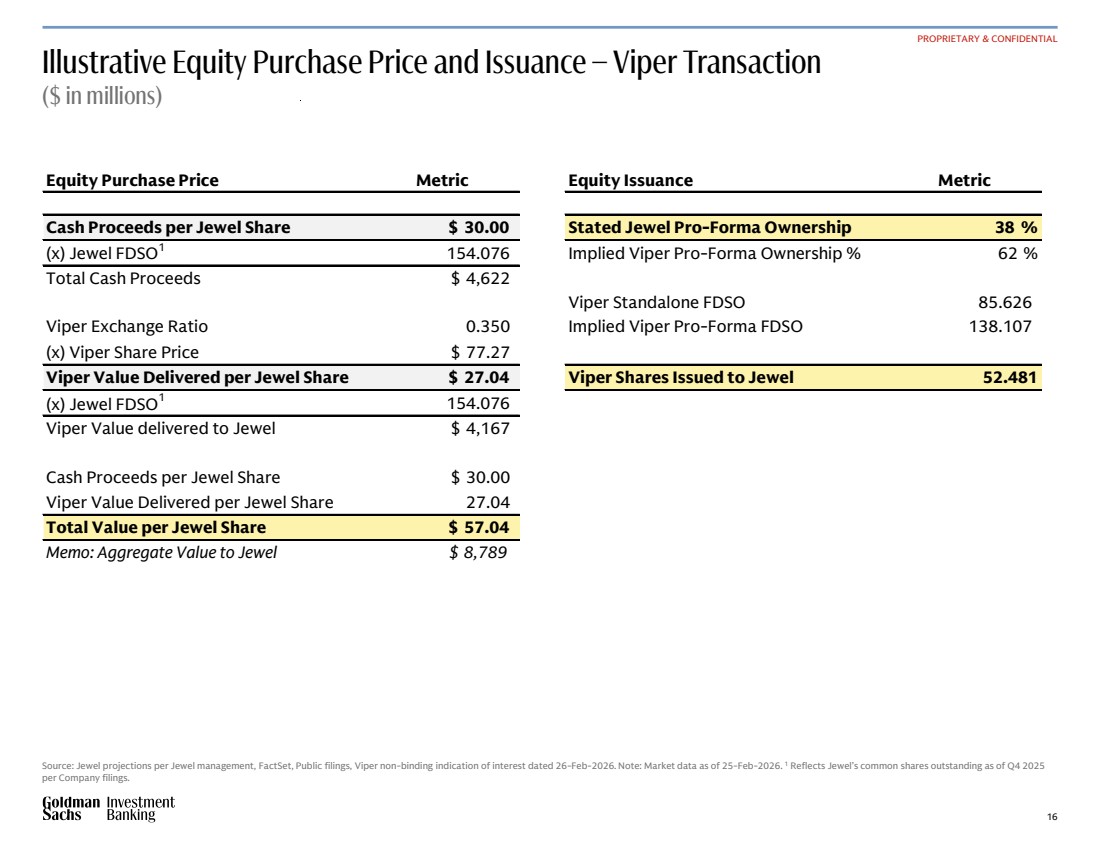

| 16 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Illustrative Equity Purchase Price and Issuance – Viper Transaction ($ in millions) Source: Jewel projections per Jewel management, FactSet, Public filings, Viper non-binding indication of interest dated 26-Feb-2026. Note: Market data as of 25-Feb-2026. 1 Reflects Jewel’s common shares outstanding as of Q4 2025 per Company filings. PROPRIETARY & CONFIDENTIAL Layout Guidance To use this charts and graphs sprite sheet: Ensure chart templates are installed. Copy and paste chart examples from this sprite sheet to the desired slide and edit data. Reapply the chart template by selecting the ‘Chart Design’ tab, ‘Chart Type’, then choosing the correct chart under ‘Template’. Check full chart guidance for details on inserting on-brand charts and graphs. Equity Purchase Price Metric Equity Issuance Metric Cash Proceeds per Jewel Share $ 30.00 Stated Jewel Pro-Forma Ownership 38 % (x) Jewel FDSO1 154.076 Implied Viper Pro-Forma Ownership % 62 % Total Cash Proceeds $ 4,622 Viper Standalone FDSO 85.626 Viper Exchange Ratio 0.350 Implied Viper Pro-Forma FDSO 138.107 (x) Viper Share Price $ 77.27 Viper Value Delivered per Jewel Share $ 27.04 Viper Shares Issued to Jewel 52.481 (x) Jewel FDSO1 154.076 Viper Value delivered to Jewel $ 4,167 Cash Proceeds per Jewel Share $ 30.00 Viper Value Delivered per Jewel Share 27.04 Total Value per Jewel Share $ 57.04 Memo: Aggregate Value to Jewel $ 8,789 |

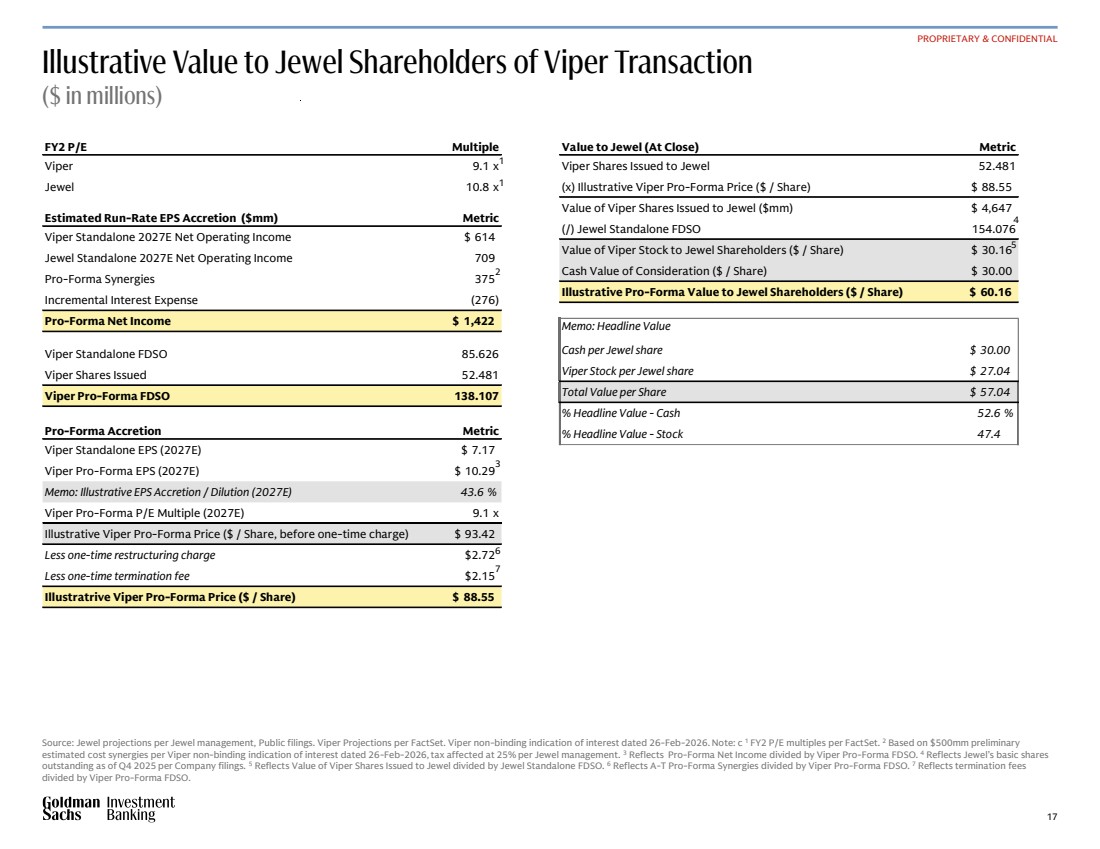

| 17 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Value to Jewel (At Close) Metric Viper Shares Issued to Jewel 52.481 (x) Illustrative Viper Pro-Forma Price ($ / Share) $ 88.55 Value of Viper Shares Issued to Jewel ($mm) $ 4,647 (/) Jewel Standalone FDSO 154.076 Value of Viper Stock to Jewel Shareholders ($ / Share) $ 30.16 Cash Value of Consideration ($ / Share) $ 30.00 Illustrative Pro-Forma Value to Jewel Shareholders ($ / Share) $ 60.16 Memo: Headline Value Cash per Jewel share $ 30.00 Viper Stock per Jewel share $ 27.04 Total Value per Share $ 57.04 % Headline Value - Cash 52.6 % % Headline Value - Stock 47.4 FY2 P/E Multiple Viper 9.1 x Jewel 10.8 x Estimated Run-Rate EPS Accretion ($mm) Metric Viper Standalone 2027E Net Operating Income $ 614 Jewel Standalone 2027E Net Operating Income 709 Pro-Forma Synergies 375 Incremental Interest Expense (276) Pro-Forma Net Income $ 1,422 Viper Standalone FDSO 85.626 Viper Shares Issued 52.481 Viper Pro-Forma FDSO 138.107 Pro-Forma Accretion Metric Viper Standalone EPS (2027E) $ 7.17 Viper Pro-Forma EPS (2027E) $ 10.29 Memo: Illustrative EPS Accretion / Dilution (2027E) 43.6 % Viper Pro-Forma P/E Multiple (2027E) 9.1 x Illustrative Viper Pro-Forma Price ($ / Share, before one-time charge) $ 93.42 Less one-time restructuring charge $2.72 Less one-time termination fee $2.15 Illustratrive Viper Pro-Forma Price ($ / Share) $ 88.55 Illustrative Value to Jewel Shareholders of Viper Transaction ($ in millions) Source: Jewel projections per Jewel management, Public filings. Viper Projections per FactSet. Viper non-binding indication of interest dated 26-Feb-2026. Note: c 1 FY2 P/E multiples per FactSet. 2 Based on $500mm preliminary estimated cost synergies per Viper non-binding indication of interest dated 26-Feb-2026, tax affected at 25% per Jewel management. 3 Reflects Pro-Forma Net Income divided by Viper Pro-Forma FDSO. 4 Reflects Jewel’s basic shares outstanding as of Q4 2025 per Company filings. 5 Reflects Value of Viper Shares Issued to Jewel divided by Jewel Standalone FDSO. 6 Reflects A-T Pro-Forma Synergies divided by Viper Pro-Forma FDSO. 7 Reflects termination fees divided by Viper Pro-Forma FDSO. PROPRIETARY & CONFIDENTIAL Layout Guidance To use this charts and graphs sprite sheet: Ensure chart templates are installed. Copy and paste chart examples from this sprite sheet to the desired slide and edit data. Reapply the chart template by selecting the ‘Chart Design’ tab, ‘Chart Type’, then choosing the correct chart under ‘Template’. Check full chart guidance for details on inserting on-brand charts and graphs. 4 5 1 1 2 6 3 7 |

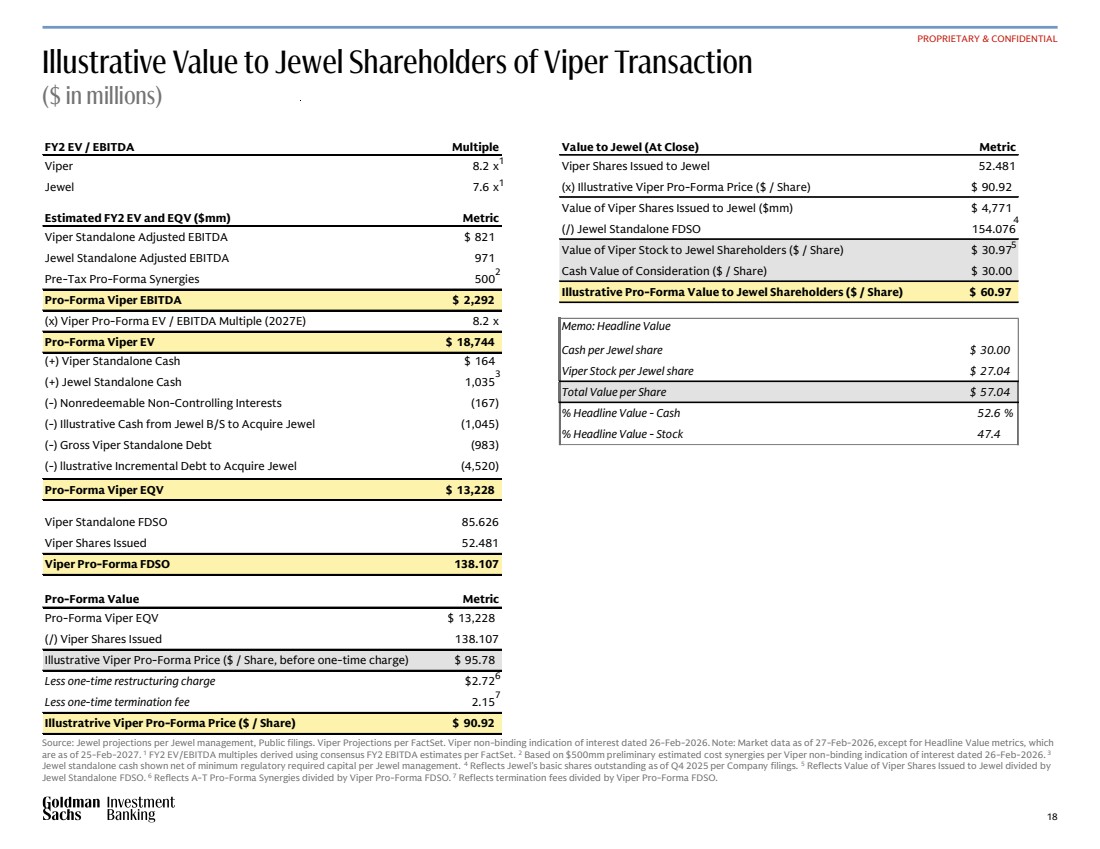

| 18 114:151:197 255:255:255 0:0:0 Brand Colors A. 240:235:230 167:162:157 114:115:117 Brand Grays B. 220:220:224 187:187:191 Background Grays C. 253:243:173 184:208:245 242:203:231 153:224:217 245:208:206 198:233:189 Table Highlight D. E. 0:0:0 114:115:117 Table Borders F. Functional Data Colors G. 194:23:10 243:196:63 57:128:37 Primary Sequence 9:44:97 114:151:197 166:66:140 21:151:136 224:115:26 117:55:173 176:48:48 189:140:0 105.55.14 97:122:39 9:107:96 59:124:222 64:37:56 145:87:196 9:74:171 143:106:4 107:20:20 199:97:172 55:71:19 59:26:89 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. Theme Colors Primary Sequence Secondary Shade Value to Jewel (At Close) Metric Viper Shares Issued to Jewel 52.481 (x) Illustrative Viper Pro-Forma Price ($ / Share) $ 90.92 Value of Viper Shares Issued to Jewel ($mm) $ 4,771 (/) Jewel Standalone FDSO 154.076 Value of Viper Stock to Jewel Shareholders ($ / Share) $ 30.97 Cash Value of Consideration ($ / Share) $ 30.00 Illustrative Pro-Forma Value to Jewel Shareholders ($ / Share) $ 60.97 Memo: Headline Value Cash per Jewel share $ 30.00 Viper Stock per Jewel share $ 27.04 Total Value per Share $ 57.04 % Headline Value - Cash 52.6 % % Headline Value - Stock 47.4 FY2 EV / EBITDA Multiple Viper 8.2 x Jewel 7.6 x Estimated FY2 EV and EQV ($mm) Metric Viper Standalone Adjusted EBITDA $ 821 Jewel Standalone Adjusted EBITDA 971 Pre-Tax Pro-Forma Synergies 500 Pro-Forma Viper EBITDA $ 2,292 (x) Viper Pro-Forma EV / EBITDA Multiple (2027E) 8.2 x Pro-Forma Viper EV $ 18,744 (+) Viper Standalone Cash $ 164 (+) Jewel Standalone Cash 1,035 (-) Nonredeemable Non-Controlling Interests (167) (-) Illustrative Cash from Jewel B/S to Acquire Jewel (1,045) (-) Gross Viper Standalone Debt (983) (-) llustrative Incremental Debt to Acquire Jewel (4,520) Pro-Forma Viper EQV $ 13,228 Viper Standalone FDSO 85.626 Viper Shares Issued 52.481 Viper Pro-Forma FDSO 138.107 Pro-Forma Value Metric Pro-Forma Viper EQV $ 13,228 (/) Viper Shares Issued 138.107 Illustrative Viper Pro-Forma Price ($ / Share, before one-time charge) $ 95.78 Less one-time restructuring charge $2.72 Less one-time termination fee 2.15 Illustratrive Viper Pro-Forma Price ($ / Share) $ 90.92 Illustrative Value to Jewel Shareholders of Viper Transaction ($ in millions) Source: Jewel projections per Jewel management, Public filings. Viper Projections per FactSet. Viper non-binding indication of interest dated 26-Feb-2026. Note: Market data as of 27-Feb-2026, except for Headline Value metrics, which are as of 25-Feb-2027. 1 FY2 EV/EBITDA multiples derived using consensus FY2 EBITDA estimates per FactSet. 2 Based on $500mm preliminary estimated cost synergies per Viper non-binding indication of interest dated 26-Feb-2026. 3 Jewel standalone cash shown net of minimum regulatory required capital per Jewel management. 4 Reflects Jewel’s basic shares outstanding as of Q4 2025 per Company filings. 5 Reflects Value of Viper Shares Issued to Jewel divided by Jewel Standalone FDSO. 6 Reflects A-T Pro-Forma Synergies divided by Viper Pro-Forma FDSO. 7 Reflects termination fees divided by Viper Pro-Forma FDSO. PROPRIETARY & CONFIDENTIAL Layout Guidance To use this charts and graphs sprite sheet: Ensure chart templates are installed. Copy and paste chart examples from this sprite sheet to the desired slide and edit data. Reapply the chart template by selecting the ‘Chart Design’ tab, ‘Chart Type’, then choosing the correct chart under ‘Template’. Check full chart guidance for details on inserting on-brand charts and graphs. 4 5 3 6 7 1 1 2 |