Exhibit (a)(5)(vi)

Weinstein Is ‘Buying Pessimism’ With Discount Bids on Private Assets

Bloomberg

By Loukia Gyftopoulou and Leonard Kehnscherper

March 10, 2026

The hedge-fund manager offers to buy out frustrated investors in Blue Owl and Starwood funds — and says he’s just getting started

Everyday investors have billions of dollars stuck in portfolios of private credit, real estate and other hard-to-value assets. Enter Boaz Weinstein.

As cracks spread through private credit markets in recent weeks, the head of Saba Capital Management began offering investors quick cash for their stakes in such vehicles run by Blue Owl Capital Inc. Now he’s making the same proposal to backers of a Starwood Capital Group real estate fund that has severely curtailed withdrawals for nearly two years.

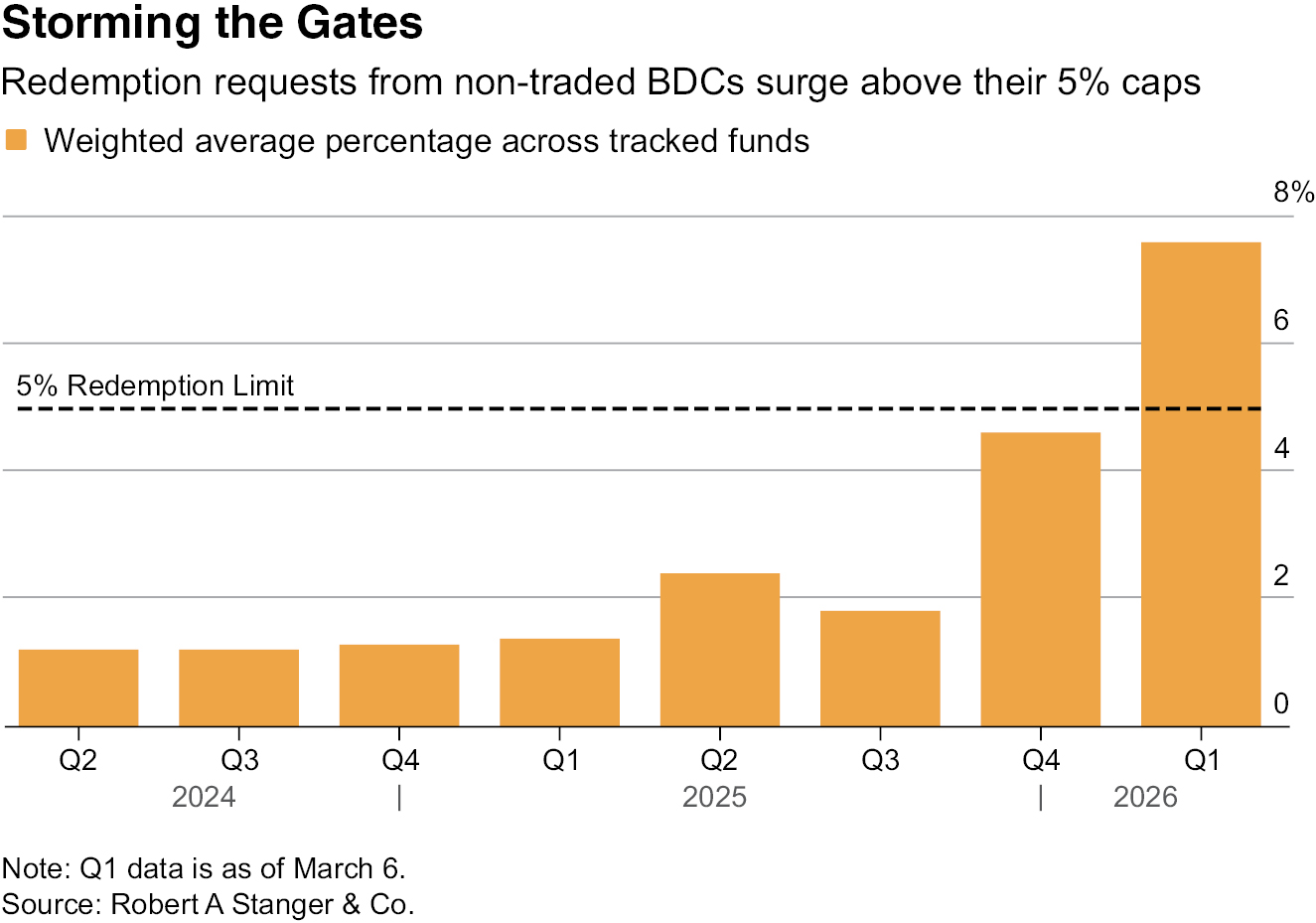

That’s just the beginning, Weinstein says. He’s considering tender offers for similar funds and portfolios that he expects will be hit by more redemption demands than the managers can fulfill. He contends the Starwood trust, known as SREIT, has been flooded with about $1 billion in outstanding requests, but has been able to honor only about 4%. Blue Owl has halted redemptions in favor of selling some assets so it can return cash to investors.

Weinstein is betting that the fear gripping these less-liquid markets will eventually pass, and depressed asset prices will rebound closer to full value. In the meantime, he will pay cash to retail investors who don’t want to wait it out, something that managers of those portfolios can’t or won’t do. Weinstein volunteers he doesn’t know much about businesses like Blue Owl’s — but if he gets more than 30% off the list price, he’ll take his chances.

“I’m effectively buying pessimism,’’ he said in an interview, “and selling optimism at full price.”

Making this happen might be more complex than just buying low and selling high, and possibly very noisy. Weinstein, a chess master in his youth who later got kicked out of the Bellagio casino for counting cards, set up Saba in 2009 and now manages $6 billion across its funds. In 2012, he gained Wall Street fame when he took the other side of outsize bets made by a trader in JPMorgan Chase & Co.’s London chief investment office, the so-called London Whale, which ended up costing the New York-based bank over $6 billion.

1

In recent years, he’s made a name for himself by taking stakes in publicly listed, closed-end funds run by some of the world’s biggest asset managers and then pushing, cajoling and hectoring them to close the gap between the stated value of their assets and their share price. He says his activist agenda won’t be the same for private markets retail funds, at least for now — the accompanying fees are too high and he doesn’t want to hold these strategies for too long.

Buying BDCs

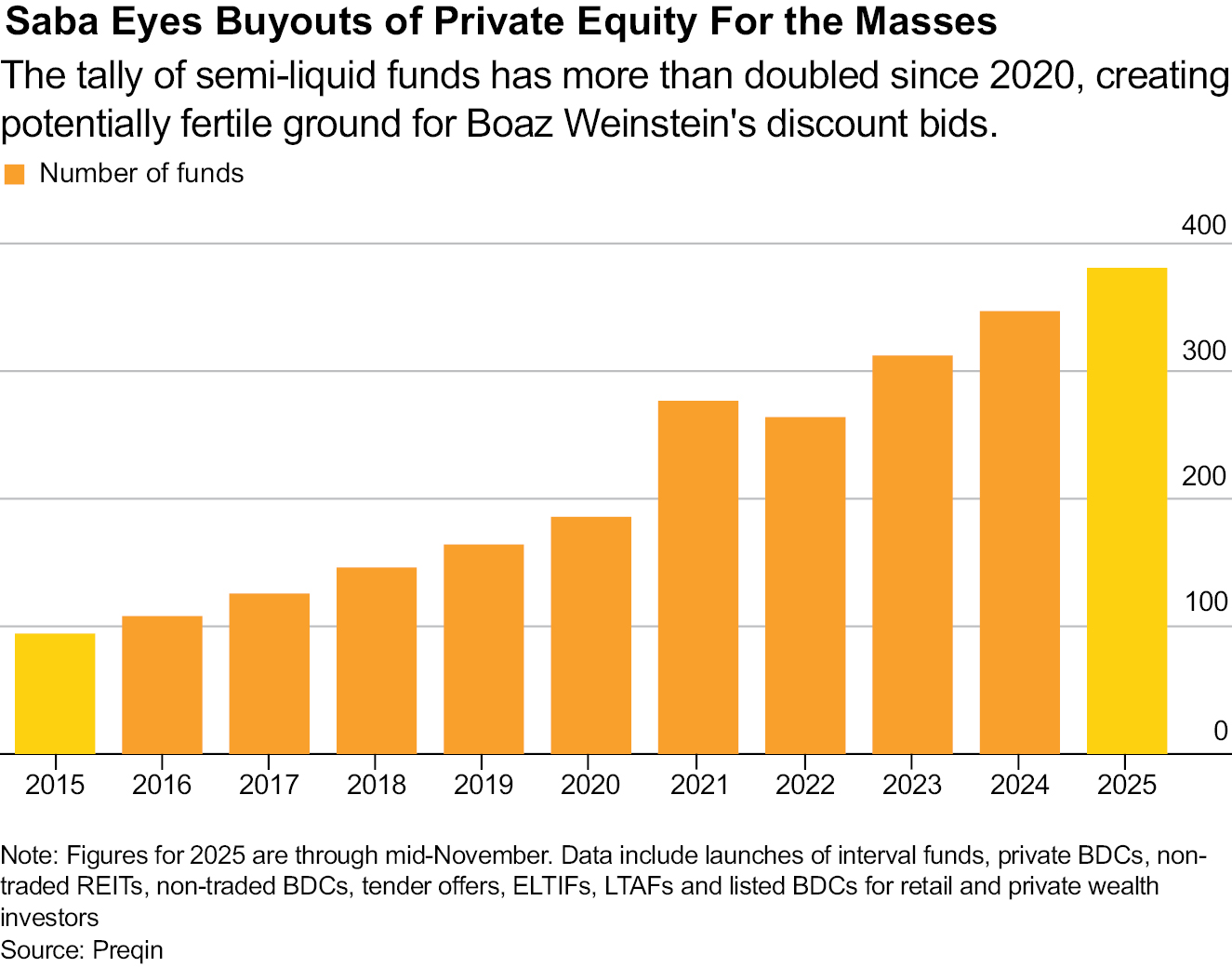

This time, he says, he’s simply offering to buy up shares in Blue Owl’s business development companies or BDCs — listed and unlisted firms that lend to small and midsize businesses — as well as the Starwood Real Estate Income Trust. More will follow. His New York-based Saba hedge fund has teamed with Cox Capital Partners, a Philadelphia firm known for acquiring private stakes from individuals. By one count, BDCs managed about $450 billion at the end of 2025, and his offers have already started to create unease in the industry.

Like with closed-end funds, Weinstein is striking at a moment when the private assets industry is vulnerable. Concerns about liquidity, inflated valuations, defaults and outright borrower fraud in the $1.8 trillion private credit market have spurred doubt about whether the industry’s equity stakes and private loans are really worth what they claim. Unsold holdings have been piling up with fund managers for years because buyers refuse to pay the asking price, making it hard for the funds to generate profits for restive backers. Weinstein says he’s here to help everyday investors whose money is stranded with sponsors that have curtailed redemptions.

The industry’s jitters were amplified this year when two of the biggest players in publicly traded BDCs, BlackRock Inc. and Apollo Global Management Inc., cut their dividends and wrote down weaker assets in some funds, worsening their already dismal stock performance. Managers at Blackstone Inc. pitched in some $150 million of their own money to help finance a record redemption request from retail investors for its flagship private credit fund, and BlackRock jolted the industry by curbing withdrawals from another one of its private credit funds when client requests for redemptions spiked.

2

With that backdrop, it’s small wonder that the average listed BDC was trading at around 77% of net assets as of February, which might make Weinstein’s offer to buy Blue Owl’s BDCs at a 30% discount more palatable to frustrated investors. Any takers would lose future dividends and might be liable for capital gains taxes. His bid for SREIT would mean haircuts to some current holders of more than 28%.

In a March 6 statement, Starwood called Weinstein’s offer an “opportunistic attempt to acquire shares at a significant discount” that he’s using to “exploit SREIT’s structure by seeking redemption through the share repurchase program for immediate profit.”

Weinstein said in the interview Blue Owl favors his intervention and that he has high esteem for its managers. Blue Owl declined to comment, but in a March 6 statement about Weinstein’s tender offer, the firm said it remains “focused on maximizing value for all shareholders” and “protecting their interests.’’

Previous Contests

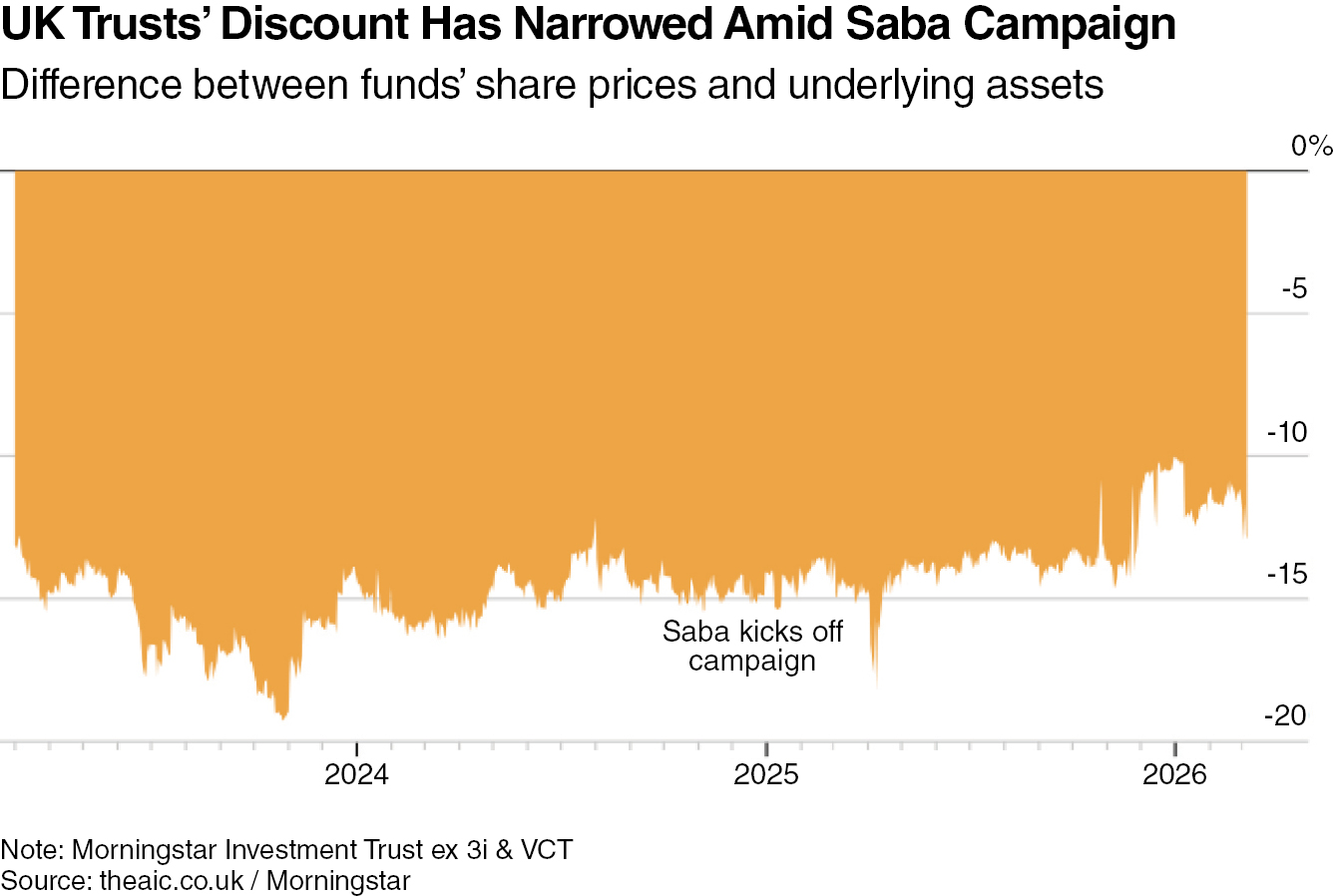

Weinstein’s overtures to investors are reminiscent of his prior run-ins with managers of publicly listed closed-end funds, which sometimes turned ugly as he pushed them to close valuation gaps and occasionally sought control.

In a confrontation with BlackRock two years ago, he called one of the investment giant’s campaigns “intentionally false and misleading.” BlackRock accused Saba of self-serving “bait-and-switch” tactics, larding on new fees for himself and turning in sub-par returns. In a separate campaign that began in 2024, he targeted a batch of UK closed-end funds that he disparaged in one presentation as “The Miserable Seven” and vowed to oust their leaders. Elsewhere, managers and board members say they have felt under personal attack, according to people familiar with the matter, who asked not to be identified discussing non-public information.

3

While some of Weinstein’s campaigns to take control failed, they did succeed in boosting share prices closer to the value of their assets. In one case where Saba did take over management, Weinstein changed the fund’s objectives and added chunky bets on unconventional assets such as crypto and blank-check firms. Investors approved the change and Saba offered those who didn’t want to remain in the fund the chance to exit at close to net asset value.

In the UK, he’s pushed several closed-end funds to give investors a way to cash out in line with the value of their assets, but he’s still fighting for control of some of them. Asset managers and fund boards have complained to regulators about the repeated investor votes Weinstein demanded, as well as Weinstein’s promises about performance, according to people familiar with the matter.

The UK’s Financial Conduct Authority started a review of listing rules for closed-end funds that will include how these “ensure that boards support strong shareholder rights and engagement and manage conflicts of interests.”

The review has arguably come too late for Edinburgh Worldwide, a trust run by Scottish growth investor Baillie Gifford & Co. Having fended off Saba’s attacks for more than a year, it outlined a tender offer on Tuesday that would enable all shareholders to exit.

“While we have galvanized the FCA into action, addressing this systemic problem will take longer than Saba’s repeat smash-and-grab cycle,” Edinburgh Worldwide Chair Jonathan Simpson-Dent said in a statement Tuesday. “Regrettably, we believe it is only a matter of time before Saba succeeds.”

Track Record

Weinstein’s impact has been mixed, according to analysts at Investec Bank. “Having effectively parked its tanks on the lawns of these investment companies, it is only appropriate that Saba’s own track record in terms of alignment with shareholders be subjected to the same level of scrutiny,” wrote Alan Brierley and Elliott Hardy in a report on Weinstein’s ongoing fight in the UK.

By their reckoning — which Weinstein disputes — his campaigns didn’t always benefit shareholders. But the authors conceded his efforts were a “much-needed wake-up call to an industry where an extended bull market had bred pockets of complacency.” Weinstein points to several of the UK funds that recently allowed investors to cash out at higher share prices.

Back in the US, alternative-asset managers are watching. In private, some say the kind of activism that has worked on publicly traded closed-end funds won’t work with unlisted BDCs or other private-market funds. Weinstein insists that, at least for now, this is not what he’s doing. He defended his performance during the interview, insisting his interventions have only been for the benefit of investors.

“I’m proud of the track record,” he said. “We are the good guys.”

4