Exhibit 99.(H)(23)

WisdomTree Rules-Based Methodology

| Last Updated February 2026 |

The 2026 reconstitution schedule is set as noted below:

| · | The screening date for the Global (including Emerging Markets), ex-State-Owned Enterprises and Developed International Equity Indexes will be September 30, 2026 |

| o | The International Weighting Date will be October 6, 2026 and the International Reconstitution Date will be October 15, 2026. |

| o | The Emerging Market and Global Weighting Dates will be October 16, 2026 and the Emerging Market and Global Reconstitution Dates will be October 27, 2026. |

| · | The screening date for the India, U.S. Dividend and Core Equity Indexes will be November 30, 2026 |

| o | The U.S. Weighting Date will be December 9, 2026 and the U.S. Reconstitution Date will be December 16, 2026. |

| o | The India Weighting Date will be December 4, 2026 and the India Reconstitution Date will be December 15, 2026. |

| Page 1 of 192 |

| U.S. DIVIDEND INDEXES | 4-16 |

| WisdomTree U.S. Dividend Index | |

| WisdomTree U.S. LargeCap Dividend Index | |

| WisdomTree U.S. MidCap Dividend Index | |

| WisdomTree U.S. SmallCap Dividend Index | |

| WisdomTree U.S. High Dividend Index | |

| WisdomTree U.S. Quality Dividend Growth Index | |

| WisdomTree U.S. SmallCap Quality Dividend Growth Index |

| CORE EQUITY INDEXES | 17-24 |

| WisdomTree U.S. LargeCap Index | |

| WisdomTree U.S. MidCap Index | |

| WisdomTree U.S. SmallCap Index |

| U.S. MULTIFACTOR INDEX | 25-30 |

| WisdomTree U.S. Multifactor Index |

| INTERNATIONAL DIVIDEND INDEXES | 31-53 |

| WisdomTree International Equity Index | |

| WisdomTree Dynamic International Equity Index | |

| WisdomTree International High Dividend Index | |

| WisdomTree True Developed International Index | |

| WisdomTree International MidCap Dividend Index | |

| WisdomTree International SmallCap Dividend Index | |

| WisdomTree Dynamic International SmallCap Equity Index | |

| WisdomTree International Quality Dividend Growth Index | |

| WisdomTree International Hedged Quality Dividend Growth Index | |

| WisdomTree Europe Equity Index | |

| WisdomTree Europe Hedged Equity Index | |

| WisdomTree Europe SmallCap Equity Index | |

| WisdomTree Europe Hedged SmallCap Equity Index | |

| WisdomTree Europe SmallCap Dividend Index | |

| WisdomTree Europe Quality Dividend Growth Index | |

| WisdomTree Japan Dividend Index | |

| WisdomTree Japan Hedged Equity Index | |

| WisdomTree Japan SmallCap Dividend Index | |

| WisdomTree Japan SmallCap Equity Index | |

| WisdomTree Japan Hedged SmallCap Equity Index |

| EMERGING MARKETS DIVIDEND INDEXES | 54-64 |

| WisdomTree Emerging Markets Dividend Index | |

| WisdomTree Emerging Markets High Dividend Index | |

| WisdomTree Emerging Markets SmallCap Dividend Index |

| Page 2 of 192 |

| EX-STATE-OWNED ENTERPRISES INDEXES | 65-74 |

| WisdomTree Emerging Markets ex-State-Owned Enterprises Index | |

| WisdomTree China ex-State-Owned Enterprises Index | |

| WisdomTree True Emerging Markets Index |

| INDIA INDEXES | 75-87 |

| WisdomTree India Earnings Index | |

| WisdomTree India Equity Index | |

| WisdomTree India Hedged Equity Index |

| GLOBAL DIVIDEND INDEXES | 88-97 |

| WisdomTree Global Dividend Index |

| WisdomTree Global High Dividend Index |

| GLOBAL EX–US QUALITY INDEX | 98-105 |

| Global ex–US Quality Growth Index |

| CYBERSECURITY INDEX | 106-112 |

| WisdomTree Team8 Cybersecurity Index |

| BIOREVOLUTION INDEX | 113-118 |

| WisdomTree BioRevolution Index |

| ARTIFICIAL INTELLIGENCE & INNOVATION INDEX | 119-126 |

| WisdomTree Artificial Intelligence & Innovation Index | |

| BATTERY VALUE CHAIN AND INNOVATION INDEX | 127-1344 |

| WisdomTree Battery Value Chain and Innovation Index |

| QUALITY GROWTH INDEXES | 135-141 |

| WisdomTree U.S. Quality Growth Index | |

| WisdomTree U.S. MidCap Quality Growth Index | |

| WisdomTree U.S. SmallCap Quality Growth Index |

| NEW ECONOMY REAL ESTATE INDEX | 142-147 |

| WisdomTree New Economy Real Estate Index |

| WISDOMTREE OPPORTUNITIES INDEXES | 148-162 |

| WisdomTree European Opportunities Equity Index | |

| WisdomTree European Opportunities Index | |

| WisdomTree Japan Opportunities Equity Index |

| WisdomTree Japan Opportunities Index |

| WisdomTree GeoAlpha Opportunities Index |

| Page 3 of 192 |

| WISDOMTREE DEFENSE INDEXES | 163-172 |

| WisdomTree European Defense Index | |

| WisdomTree Asia Defense Index | |

| WisdomTree Global Defense Index |

| QUANTUM COMPUTING INDEX | 173-179 |

| WisdomTree Quantum Computing Index |

| INTERNATIONAL LARGECAP INDEX | 180-184 |

| WisdomTree U.S. Adaptive Moving Average Index |

| ADAPTIVE MOVING AVERAGE INDEXES | 185-190 |

| WisdomTree U.S. Adaptive Moving Average Index | |

| WisdomTree International Adaptive Moving Average Index |

| Page 4 of 192 |

Methodology Guide for US Dividend Indexes

| 1. | Overview and Description |

WisdomTree U.S. Dividend Index (“DI”), WisdomTree U.S. LargeCap Dividend Index (“LargeCap Dividend Index”), WisdomTree U.S. MidCap Dividend Index (“MidCap Dividend Index”),WisdomTree U.S. SmallCap Dividend Index (“SmallCap Dividend Index”), WisdomTree U.S. High Dividend Index (“High Dividend Index”), WisdomTree U.S. Quality Dividend Growth Index (“Quality Dividend Growth Index”) and WisdomTree U.S. SmallCap Quality Dividend Growth Index (“SmallCap Quality Dividend Growth Index”) (collectively, the “Domestic Dividend Indexes”) were developed by WisdomTree, Inc. (“WT”) to define the dividend-paying segments of the U.S. stock market and to serve as performance benchmarks for equity income investors.

| · | The DI measures the performance of investable U.S.-based companies that pay regular cash dividends on shares of common stock. All of the other Domestic Dividend Indexes, defined below, are derived from the DI. |

| · | The LargeCap Dividend Index is comprised of dividend-paying companies from the large-capitalization segment of the DI. |

| · | The MidCap Dividend Index is comprised of dividend-paying companies from the mid-capitalization segment of the DI. |

| · | The SmallCap Dividend Index is comprised of dividend-paying companies from the small-capitalization segment of the DI. |

| · | The High Dividend Index is comprised of the high-yielding companies within the DI. |

| · | The Quality Dividend Growth Index is comprised of dividend-paying stocks with growth characteristics. |

| · | The SmallCap Quality Dividend Growth Index is comprised of dividend-paying companies from the small-capitalization segment of the DI with growth characteristics. |

Each Index is reconstituted annually, at which time each component’s weight is adjusted, if necessary, to reflect its dividend-weighting in the Index. Dividend weighting is defined as each component’s projected cash dividends to be paid over the coming year divided by the sum of the projected cash dividends to be paid by all the components in the Index over the same period. This quotient is the percentage weight assigned to each component in the Index at the annual reconstitution. Projected cash dividends to be paid is calculated by multiplying a company’s indicated annual dividend per share by common shares outstanding. Each Index is calculated to seek to capture price appreciation and total return, which assumes dividends are reinvested in the components of the Index. Each Index is calculated using available primary market prices.

| Page 5 of 192 |

| 2. | Index Governance |

The Indexes are overseen by the WisdomTree U.S. Dividend Index Committee (the “Committee”), a standing index committee of WisdomTree, Inc. (“WisdomTree”), ticker WT. The Committee will be composed of not less than three members. The Committee is responsible for making broad decisions with respect to the implementation, ongoing management, operation, and administration of the Index. WisdomTree designed this methodology to achieve the Index’s objective. The primary function of the Committee is to seek to ensure the Index methodology is implemented correctly. In such role, the Index Committee selects all constituents meeting the eligibility criteria described herein in its discretion. In addition, any changes to or deviations from this methodology are intended to enable the Index to continue to achieve its objective and will be made in the sole judgment and discretion of the Index Committee.

The Committee meetings generally will be held at a semi-annual cadence or as needed in relation to the reconstitution and/or rebalance frequency of the Index or as circumstances require. The composition of the Committee may be changed from time to time.

| 3. | Key Features |

| 3.1. | Membership Criteria |

To be eligible for inclusion in the Domestic Dividend Indexes, a company must list its shares on a U.S. stock exchange, conduct its Primary Business Activities1 in the United States and pay regular cash dividends on shares of its common stock in the 12 months preceding the annual reconstitution, which takes place in December. Companies must have a market capitalization of at least $100 million by the “Screening Date” (i.e., after the close of trading on the last trading day in November) and shares of such companies must have had a median daily trading dollar volume of at least $100,000 for the three months preceding the Screening Date.

1 The country in which a company conducts its Primary Business Activities is determined based on the following factors: country of organization or incorporation, country in which a company’s headquarters is located, the country to which a company has the greatest risk exposure (“Country of Risk”), and the country from which a company generates the most significant portion of its revenue or to which it allocates the greatest resources. WT may determine to consider additional or different factors depending on the nature of a company’s business and operations.

| Page 6 of 192 |

Common stocks, REITs, tracking stocks, and holding companies are eligible for inclusion in the Domestic Dividend Indexes. ADRs, GDRs, EDRs, limited partnerships, limited liability companies, royalty trusts, and Business Development Companies (BDCs), preferred stocks, closed-end funds, exchange-traded funds, and derivative securities such as warrants and rights are not eligible for inclusion in the Indexes.2 The publicly traded security for WisdomTree, Inc. (NYSE: WT), is also not eligible for inclusion in any of WisdomTree’s equity indexes.

In addition, companies that fall within the bottom decile of a composite risk factor score are not eligible for inclusion in the Domestic Dividend Indexes. The composite risk factor score is used to eliminate potentially higher risk companies that would have otherwise been eligible for inclusion in the Indexes. The composite risk factor score is an equally weighted score of the two factors described below.

| 1) | Quality Factor – determined by static observations and trends of return on equity (ROE), return on assets (ROA), gross profits over assets and cash flows over assets. Scores are calculated within industry groups. |

| 2) | Momentum Factor – determined by stocks’ risk adjusted total returns over historical periods (6 and 12 months) |

Companies that fall within the top 5% ranked by dividend yield and also the bottom ½ of the composite risk factor score are not eligible for inclusion.

| 3.2. | Base Date and Base Value |

Indexes covering entire regions were established with a base value of 300 on May 31, 2006. Market-cap segment and high dividend indexes were established with a base value of 200 on May 31, 2006.

The WisdomTree U.S. Quality Dividend Growth Index and WisdomTree U.S. SmallCap Quality Dividend Growth Index were established with a base value of 200 on April 11, 2013.

| 3.3. | Calculation and Dissemination |

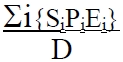

The following formula is used to calculate the index levels for the Domestic Dividend Indexes:

2 Beginning with the December 2006 reconstitution, Mortgage REITs will no longer be eligible for inclusion in the WisdomTree Domestic and International Dividend Indexes.

| Page 7 of 192 |

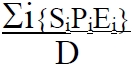

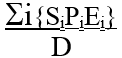

Si = Number of shares in the index for security i.

Pi = Price of security i

D = Divisor

The Domestic Dividend Indexes are calculated whenever the US exchanges are open for trading.

If trading is suspended while one of the exchanges is still open, the last traded price for that stock is used for all subsequent Index computations until trading resumes. If trading is suspended before the opening, the stock’s adjusted closing price from the previous day is used to calculate the Index. Until a particular stock opens, its adjusted closing price from the previous day is used in the Index computation. Index values are calculated on both a price and total-return basis, in U.S. dollars. The price Index is updated on a real time basis, while the total return Index is calculated and disseminated on an end-of-day basis. Price index values are calculated and disseminated every 15 seconds to the Securities Industry Automation Corporation (SIAC) so that such Index Values can print to the Consolidated Tape.

| 3.4 | Weighting |

The Domestic Dividend Indexes are modified capitalization-weighted Indexes that employ a transparent weighting formula to magnify the effect that dividends play in the total return of the Indexes. The initial weight of a component in the Index at the annual reconstitution is equal to the dollar value of the company’s cash dividends to be paid in the coming year based on the company’s indicated annual dividend per share. To calculate the weighting factor – Cash Dividends to be paid – indicated annual dividend per share is multiplied by common shares outstanding.3 Thus, each component’s weight in the Index at the “U.S. Weighting Date” (defined below) reflects its share of the total Dividend Stream projected to be paid in the coming year by all of the component companies in the Index. The dividend stream will be adjusted for constituents with dividend yields greater than 12% at the screening date. The dividend stream of these capped securities will be their market cap multiplied by 12%.

For the size segment dividend indexes (total, large, mid and small caps) and high dividend cuts of the market, companies that fall within the top two deciles of the composite risk factor will have their dividend stream multiplied by 1.5 while all other dividends will remain unadjusted.

Companies will be weighted in the index based on this adjusted dividend stream.

3 Special Dividends are not included in the computation of Index weights.

| Page 8 of 192 |

The U.S. Weighting Date is when component weights are set, and it occurs immediately after the close of trading on the relevant date. New components and component weights take effect before the opening of trading the day following the “U.S. Reconstitution Date.” Please refer to the Reconstitution Schedule on page 1 for specific dates.

Should any company achieve a weighting equal to or greater than 24.0% of the Index, its weighting will be reduced to 20.0% at the close of the current calendar quarter, and the weights of all other components in the Index will be rebalanced proportionally. Moreover, should the “collective weight” of Index component securities whose individual current weights equal or exceed 5.0% of the Index, when added together, equal or exceed 50.0% of the Index, the weightings in those component securities will be reduced so that their collective weight equals 40.0% of the Index at the close of the current calendar quarter, and other components in the Index will be rebalanced proportionally to reflect their relative weights before the adjustment. Further iterations of these adjustments may occur until no company or group of companies violates these rules.

The capping rules described below are applied concurrently and, in a manner, designed to seek to minimize deviation from a component’s initial or intended weighting in an Index.

The following capping rule applies to all Domestic Dividend Indexes, unless specified otherwise below:

| · | Should the components assigned to any sector (except the Real Estate sector) achieve an aggregate weight greater than 25% of an Index, the aggregate weight of the component companies will be reduced to 25% as of the annual Screening Date. The Real Estate sector will be capped at 10%. |

In the case of the WisdomTree U.S. Dividend Index the following caps apply:

| · | The Real Estate sector will be capped at 5%. |

| · | Should the ratio of a component company’s weight relative to its weight in a market capitalization weighted version of the Index exceed 3x or fall below 0.33x, the weight of the company will be reduced or increased to meet the 3x or 0.33x thresholds, respectively. |

In the case of the WisdomTree U.S. LargeCap Dividend Index the following caps apply:

| · | Should the ratio of a security’s weight relative to its weight in a market capitalization weighted version of the index reach above 3x or fall below 0.33x, the weight of the company will be reduced or increased to meet the 3x or 0.33x thresholds, respectively. |

| Page 9 of 192 |

In the case of the WisdomTree U.S. MidCap Dividend Index and the U.S. SmallCap Dividend Index the following caps apply:

| · | Should the ratio of a security’s weight relative to its weight in a market capitalization weighted version of the index reach above 2.5x or fall below 0.4x, the weight of the company will be reduced or increased to meet the 2.5x or 0.4x thresholds, respectively. |

In the case of the WisdomTree U.S. High Dividend Index the following caps apply:

| · | The maximum weight of any individual component is capped at 5% on the annual rebalance. |

| · | Should the ratio of a security’s weight relative to its weight in a market capitalization weighted version of the index reach above 3x or fall below 0.33x, the weight of the company will be reduced or increased to meet the 3x or 0.33x thresholds, respectively. |

| · | Sector exposures will be capped at the lesser of 25% or 3x their weight in a market capitalization version of the initial universe of eligible securities prior to the final selection of highest dividend yielding companies as detailed in section 5.5 below. The Real Estate sector will be capped at 5%. |

In the case of the WisdomTree U.S. Quality Dividend Growth Index, the following capping rules are applied:

| · | The maximum weight of any individual security is capped at 8% on the annual rebalance prior to the introduction of sector caps and the weights of all other components will be adjusted. |

| · | Should the ratio of a security’s weight relative to its weight in a market capitalization weighted version of the index reach above 3x or fall below 0.33x, the weight of the company will be reduced or increased to meet the 3x or 0.33x thresholds, respectively. |

| · | Sector exposures will be capped at the lesser of 20% or 2x their weight in a market capitalization version of the initial universe of eligible securities prior to the final selection of 300 companies as detailed in section 5.6 below. The Information Technology sector will be capped at 30%. The Real Estate sector will be capped at 10%. |

| Page 10 of 192 |

In the case of the WisdomTree U.S. SmallCap Quality Dividend Growth Index the following caps apply:

| · | The maximum weight of any individual security is capped at 2% on the annual rebalance and the weights of all other components will be adjusted. |

| · | Should the ratio of a security’s weight relative to its weight in a market capitalization weighted version of the index reach above 2.5x or fall below 0.4x, the weight of the company will be reduced or increased to meet the 2.5x or 0.4x thresholds, respectively. |

| · | Should any sector achieve a weight equal to or greater than 25% of the Index, weight of companies will be reduced to 25% as of the annual Screening Date. Real Estate sector will be capped at 10%. |

The weights of individual components or groups of components may fluctuate above or below the specified caps during the year intra annual rebalance dates. The weights will be reset at each annual rebalance date.

The following liquidity adjustment factors will be applied to all Indexes after the capping rules described above have been applied:

A further volume screen requires that a calculated volume factor (the median daily dollar volume for three months preceding the Screening Date / weight of security in each index) shall be greater than $200 million to be eligible for each index. If a security’s volume factor falls below $200 million at the annual screening, but is currently in the Index, it will remain in the Index. The securities’ weight will be adjusted downwards by an adjustment factor equal to its volume factor divided by $400 million.

In the event a security has a calculated volume factor (average daily volume traded over the preceding three months / weight in the index) that is less than $400 million, its weight will be reduced such that weight after volume adjustment = weight before adjustment x calculated volume factor

/ $400 million. The implementation of the volume factor may cause an increase in the holding, sector and country weights above the specified caps.

| Page 11 of 192 |

| 3.5 | Dividend Treatment |

Normal dividend payments are not taken into account in the price Index, whereas they are reinvested and accounted for in the total return Index. Special dividends are reinvested and accounted for in the total return Index.

| 3.6 | Multiple Share Classes |

In the event a component company issues multiple classes of shares of common stock, each class of share will be included in any broad-based Index, provided that dividends are paid on that share of stock. In the event such a component company qualified for inclusion in the “High Dividend” cut from these broad-based Indexes, only the share class of that company with the highest dividend yield would be selected for inclusion. Conversion of a share class into another share class results in the deletion of the share class being phased out and an increase in shares of the surviving share class, provided that the surviving share class is in the Index. For all Mid and Small cap cuts, if a security has multiple listed share classes and the total market capitalization of the listed share classes is greater than largest market capitalization cutoff of that index, the security would not be eligible for that index. At least one share class will be eligible for inclusion in either large, mid or small size cut based on total market value of the company.

| 4. | Index Maintenance |

Index Maintenance includes monitoring and implementing the adjustments for company deletions, stock splits, stock dividends, spin-offs, or other corporate actions. Some corporate actions, such as stock splits, stock dividends, and rights offerings require changes in the index shares and the stock prices of the component companies in the Domestic Dividend Indexes. Some corporate actions, such as stock issuances, stock buybacks, warrant issuances, increases or decreases in dividend per share between reconstitutions, do not require changes in the index shares or the stock prices of the component companies in the Domestic Dividend Indexes. Other corporate actions, such as special dividends, may require Index divisor adjustments. Any corporate action, whether it requires divisor adjustments or not, will be implemented after the close of trading on the day prior to the ex-date of such corporate action. Whenever possible, changes to the Index’s components, such as deletions as a result of corporate actions, will be announced at least two business days prior to their implementation date.

| Page 12 of 192 |

| 4.1. | Component Changes |

Additions

Additions to the Domestic Dividend Indexes are made at the annual reconstitution according to the inclusion criteria defined above. Changes are implemented before the opening of trading on the first trading day following the “U.S. Reconstitution Date.” Please refer to the Reconstitution Schedule on page 1 for specific dates.

In the case of the WisdomTree U.S. Dividend Index and the WisdomTree U.S. LargeCap Dividend Index:

The DI will check for dividend initiators on a quarterly basis (following the close of trading in February, May and August), in addition to the annual screening in November. If initiators are within the 300 largest component companies by market capitalization, they will be added to the Indexes within the first 8 trading days of the following month. Added components will be weighted as specified in section 2.4. with weights of existing components adjusted proportionally.

In the case of the WisdomTree U.S. Quality Dividend Growth Index:

Dividend initiators to be included in the DI on a quarterly basis, will be ranked using the criteria specified in section 5.6. Companies that rank in the top 300 by this criteria will be added to the Index within the first 8 trading days of the following month. Added components will be weighted as specified in section 2.4. with weights of existing components adjusted proportionally.

No additions are made to any of the remaining Domestic Dividend Indexes between annual reconstitutions.

Deletions

Shares of companies that are de-listed or acquired by a company outside of the Index are deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in composition of the Index. A component company that cancels its dividend payment is deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in the composition of the Index. A component company that files for bankruptcy is deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in the composition of the Index. If a component company is acquired by another company in the Index for stock, the acquiring company’s shares and weight in the Index are adjusted to reflect the transaction after the close of trading on the day prior to the execution date.4 A component company that is no longer primarily listed in the U.S. or that no longer conducts its Primary Business Activities in the U.S. will be removed from the Index and the weights of the remaining components will be adjusted proportionately to reflect the change in the composition of the Index. Component companies that reclassify their shares (e.g., that convert multiple share classes into a single share class) remain in the Index, although index shares are adjusted to reflect the reclassification.

4 Companies being acquired will be deleted from the WisdomTree Indexes immediately before the effective date of the acquisition or upon notice of a suspension of trading in the stock of the company that is being acquired. In cases where an effective date is not publicly announced in advance, or where a notice of suspension of trading in connection with an acquisition is not announced in advance, WisdomTree reserves the right to delete the company being acquired based on best available market information.

| Page 13 of 192 |

Spin-Offs and IPOs

Should a company be spun-off from an existing component company and pay a regular cash dividend, it will be ineligible for inclusion in the Domestic Dividend Indexes until the next annual reconstitution, provided it meets all other Index eligibility requirements. Spin-off shares of publicly traded companies that are included in the same Indexes as their parent company are increased to reflect the spin-off and the weights of the remaining components will be adjusted proportionately to reflect the change in the composition of the Index. Companies that go public in an Initial Public Offering (IPO), pay a regular cash dividend, and meet all other eligibility requirements may be considered for inclusion in a Domestic Dividend Index at the next annual reconstitution of such Index.

| 5. | Index Divisor Adjustments |

Changes in the Index’s market capitalization due to changes in composition, weighting or corporate actions result in a divisor change to maintain the Index’s continuity. By adjusting the divisor, the Index value retains its continuity before and after the event. Corporate actions that require divisor adjustments will be implemented prior to the opening of trading on the effective date. In certain instances where information is incomplete, or the completion of an event is announced too late to be implemented prior to the ex-date, the implementation will occur as of the close of the following day or as soon as practicable thereafter. For corporate actions not described herein, or combinations of different types of corporate events and other exceptional cases, WisdomTree reserves the right to determine the appropriate implementation method.

Companies that are acquired, de-listed, file for bankruptcy, move their Primary Business Activities outside of the U.S. or that cancel their dividends in the intervening weeks between the Screening Date and the U.S. reconstitution date are not included in the Domestic Dividend Indexes, and the weights of the remaining components are adjusted accordingly.

| Page 14 of 192 |

| 6. | Selection Parameters for the Domestic Dividend Indexes |

| 6.1. | Selection parameters for the WisdomTree U.S. Dividend Index are defined in 3.1. Companies that pass this selection criteria as of the Screening Date are included in the DI. The component companies are assigned weights in the Index as defined in section 3.4. and annual reconstitution of the Index takes effect as defined in section 4.1. |

| 6.2. | The WisdomTree U.S. LargeCap Dividend Index is created by selecting the 300 largest component companies of the DI by market capitalization. The component companies are assigned weights in the Index as defined in section 3.4, and annual reconstitution of the Index takes effect as defined in section 4.1. |

| 6.3. | The WisdomTree U.S. MidCap Dividend Index is created based on a defined percentage of the remaining market capitalization of the DI, once the 300 largest companies by market capitalization have been removed. The companies that comprise the top 75% of the remaining market capitalization are selected for inclusion in the MidCap Dividend Index. The component companies are assigned weights in the Index as defined in section 3.4., and annual reconstitution of the Index takes effect as defined in section 4.1. |

| 6.4. | The WisdomTree U.S. SmallCap Dividend Index is created based on a defined percentage of the remaining market capitalization of the DI, once the 300 largest companies by market capitalization have been removed. The companies that comprise the bottom 25% of the remaining market capitalization are selected for inclusion in the SmallCap Dividend Index. The component companies are assigned weights in the Index as defined in section 3.4., and annual reconstitution of the Index takes effect as defined in section 4.1. |

| 6.5. | The WisdomTree U.S. High Dividend Index is comprised of the highest-yielding companies within the DI. On the Screening Date, companies within the DI with market capitalizations of at least $200 million and median daily dollar volumes of at least $200,000 for the prior three months are eligible for inclusion. Component companies are split into Real Estate and ex-Real Estate groups according to their GICS sector classification and then ranked by indicated annual dividend yield within those two groups. Companies that rank in the top 30% by indicated annual dividend yield are selected for inclusion. To be deleted from the Index, companies must rank outside of the top 35% by dividend yield. The component companies are assigned weights in the Index as defined in section 3.4., and annual reconstitution of the Index takes effect as defined in section 4.1. |

| Page 15 of 192 |

| 6.6. | The WisdomTree U.S. Quality Dividend Growth Index is created as a subset of the DI. On the Screening Date, companies within the DI with market capitalizations of at least $2 billion and an earnings yield greater than the dividend yield are eligible for inclusion. Eligible companies are ranked on a composite score of two fundamental factors: growth and quality, which are equally weighted. The growth factor is determined by a company's ranking based on a 50% weight in its median analyst earnings growth forecast, a 25% weight in its trailing 5-year earnings growth and a 25% weight in its trailing 5-year sales growth. The quality factor is determined by a company’s ranking based on 50% its historical three-year average return on equity and 50% its historical three-year average return on assets. Companies with negative equity and therefore undefined return on equity will be given a median score as long as they’ve shown dividend growth over the past 5 years. Companies that rank in the top 250 companies by this combined ranking will be selected for inclusion, the number of securities will be further reduced to 200 removing the smallest 50 by initial weighting as defined in section 3.4. Eligible companies for the WisdomTree U.S. Quality Dividend Growth Index must not be a member of the WisdomTree U.S. SmallCap Dividend Index. |

| 6.7. | The WisdomTree U.S. SmallCap Quality Dividend Growth Index is created as a subset of the WisdomTree U.S. SmallCap Dividend Index (WTSDI). On the Screening Date, companies with earnings yield greater than the dividend yield are eligible for inclusion. These companies are ranked using a weighted combination of three ranking factors: 50% weighted to the rank of medium-term estimated earnings growth, 25% weighted to the rank of the historical three-year average return on equity, and 25% weighted to rank of the historical three-year average return on assets. Companies with negative equity and therefore undefined return on equity will be given a median score as long as they’ve shown dividend growth over the past 5 years. Companies that rank in the top 50% by this combined ranking will be selected for inclusion. Companies that lack medium-term earnings growth estimates will be eligible for the Index but their composite rank for ultimate selection in the index will be the average ranks of their Return on Equity (ROE) and Return on Assets (ROA). |

| Page 16 of 192 |

Methodology Guide for Core Equity Methodology

| 1. | Overview and Description |

WisdomTree U.S. LargeCap Index (“LargeCap Index”), WisdomTree U.S. MidCap Index (“MidCap Index”) and WisdomTree U.S. SmallCap Index (“SmallCap Index”) (collectively, the “Core Equity Indexes”) were developed by WisdomTree, Inc. (“WT”) to define the universe of profitable companies in the U.S. stock market.

| · | The LargeCap Index is comprised of companies with positive earnings from the large-capitalization segment of the investment universe. |

| · | The MidCap Index is comprised of companies with positive earnings from the mid-capitalization segment of the investment universe. |

| · | The SmallCap Index is comprised of companies with positive earnings from the small-capitalization segment of the investment universe. |

Each Index is reconstituted annually, at which time each component’s weight is adjusted, if necessary, to reflect its share of the Earnings Stream during the prior four fiscal quarters. The Earnings Stream is defined as cumulative earnings over the prior four fiscal quarters for each component in the Index. The percentage weight assigned to each component in the Index at the annual reconstitution is calculated by dividing the cumulative earnings each component company has generated in its last four reported fiscal quarters by the sum of all the earnings generated by all the component companies in the Index over the same period. Each Index is calculated to seek to capture price appreciation and total return, which assumes dividends are reinvested in the components of the Index. Each Index is calculated using available primary market prices.

| Page 17 of 192 |

| 2. | Index Governance |

| 2.1. | The WisdomTree Core Equity Indexes are overseen by the WisdomTree Core Equity Index Committee (the “Committee”), a standing index committee of WisdomTree, Inc. (“WisdomTree”), ticker WT. The Committee will be composed of not less than 3 members. The Committee is responsible for making broad decisions with respect to the implementation, ongoing management, operation and administration of the Index. The primary function of the Committee is to make sure the Index rules are implemented correctly and comprehensively, provided that the published Index composition shall be as determined by the Committee. Furthermore, the Committee may determine to rebalance each Index more frequently in response to volatility in the market, shifts in exposure away from underlying earnings, or other similar circumstances. |

The Committee meetings will generally be held on an annual basis or such frequency in relation to the reconstitution and/or rebalance frequency of the Index, and may be held more frequently as circumstances require.

The composition of the Committee may from time to time be changed to reflect changes in market conditions.

| 3. | Key Features |

| 3.1. | Membership Criteria |

To be eligible for inclusion in the Core Equity Indexes, a company must be under coverage by the market management team of the third party independent index calculation agent, must list its shares on a U.S. stock exchange, conduct its Primary Business Activities5 in the United States and have positive cumulative earnings over the four fiscal quarters preceding the annual reconstitution, which takes place in December.

Companies must have a market capitalization of at least $100 million by the “Screening Date” (after the close of trading on the last trading day in November); shares of such companies need to have had a median daily trading dollar volume of at least $200,000 for each of the six months preceding the Screening Date; and component companies need to have had a P/E ratio of at least 2 as of the Screening Date.

5 The country in which a company conducts its Primary Business Activities is determined based on the following factors: country of organization or incorporation, country in which a company’s headquarters is located, the country to which a company has the greatest risk exposure (“Country of Risk”), and the country from which a company generates the most significant portion of its revenue or to which it allocates the greatest resources. WT may determine to consider additional or different factors depending on the nature of a company’s business and operations.

| Page 18 of 192 |

Common stocks, REITs, tracking stocks and holding companies are eligible for inclusion in the Core Equity Indexes. ADRs, GDRs and EDRs, limited partnerships, limited liability companies, royalty trusts, and Business Development Companies (BDCs), preferred stocks, closed-end funds, exchange-traded funds, and derivative securities such as warrants and rights are not eligible for inclusion in the Indexes. The publicly traded security for WisdomTree, Inc. (NYSE: WT), is also not eligible for inclusion in any of WisdomTree’s equity indexes.

In addition, companies that fall within the bottom decile of a composite risk factor score are not eligible for inclusion in the Core Equity Indexes. The composite risk factor is used to eliminate potentially higher risk companies that would have otherwise been eligible for inclusion in the Indexes. The composite risk factor score is an equally weighted score of the two factors described below.

| 1) | Quality Factor – determined by static observations and trends of return on equity (ROE), return on assets (ROA), gross profits over assets and cash flows over assets. Scores are calculated within industry groups. |

| 2) | Momentum Factor – determined by stocks’ risk adjusted total returns over historical periods (6 and 12 months) |

| 3.2 | Base Date and Base Value |

The WisdomTree U.S. LargeCap Index, the WisdomTree U.S. MidCap Index and the WisdomTree U.S. SmallCap Index were established with a base value of 200 on January 31, 2007.

| 3.3 | Calculation and Dissemination |

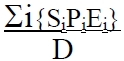

The following formula is used to calculate the index levels for the Core Equity Indexes:

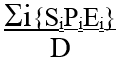

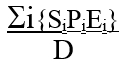

Si = Number of shares in the index for security i.

Pi = Price of security i

D = Divisor

The Core Equity Indexes are calculated every weekday.

| Page 19 of 192 |

If trading is suspended while one of the exchanges is still open, the last traded price for that stock is used for all subsequent Index computations until trading resumes. If trading is suspended before the opening, the stock’s adjusted closing price from the previous day is used to calculate the Index. Until a particular stock opens, its adjusted closing price from the previous day is used in the Index computation. Index values are calculated on both a price and total-return basis, in U.S. dollars. The price Index is updated on a real time basis, while the total return Index is calculated and disseminated on an end-of-day basis. Price index values are calculated and disseminated every 15 seconds.

| 3.4 | Weighting |

The Core Equity Indexes are modified capitalization-weighted Indexes that employ a transparent weighting formula to magnify the effect that earnings play in the total return of the Indexes. The initial weight of a component in the Index at the annual reconstitution is based on the companies’ earnings stream during the last four fiscal quarters. To calculate the weighting factor – Earnings Stream – WisdomTree uses cumulative earnings generated over the prior four reported quarters, as of November 30th of each year. Thus, each component’s weight in the Index at the “U.S. Weighting Date” (defined below) reflects its share of the total Earnings Stream recorded over the prior four quarters by all of the component companies in the Index. The U.S. Weighting Date is when component weights are set, and it occurs immediately after the close of trading on the relevant date. New components and component weights take effect before the opening of trading the day following the “U.S. Reconstitution Date.” Please refer to the Reconstitution Schedule on page 1 for specific dates.

Should any company achieve a weighting equal to or greater than 24.0% of the Index, its weighting will be reduced to 20.0% at the close of the current calendar quarter, and the weights of all other components in the Index will be rebalanced proportionally. Moreover, should the “collective weight” of Index component securities whose individual current weights equal or exceed 5.0% of the Index, when added together, equal or exceed 50.0% of the Index, the weightings in those component securities will be reduced so that their collective weight equals 40.0% of the Index at the close of the current calendar quarter, and other components in the Index will be rebalanced proportionally to reflect their relative weights before the adjustment. Further iterations of these adjustments may occur until no company or group of companies violates these rules.

The capping rules described below are applied concurrently and, in a manner, designed to seek to minimize deviation from a component’s initial or intended weighting in an Index.

| Page 20 of 192 |

The following capping rule applies to all Core Equity Indexes, unless specified otherwise below:

| · | Should any sector achieve a weight that is more than 5% above or below the weight of the sector in a market capitalization weighted version of the index, the weight of the companies will be reduced or increased to meet the +/-5% threshold, respectively. |

Should the ratio of a component company’s initial weight relative to its weight in a market capitalization weighted version of the index exceed 3x or fall below 0.33x, the weight of the company will be reduced or increased to meet the 3x or 0.33x thresholds, respectively. The weights may fluctuate above the specified caps during the year but will be reset at each annual rebalance date.

The following liquidity adjustment factors will be applied to all Indexes after the capping rules described above have been applied:

| · | A further volume screen requires that a calculated volume factor (the median daily dollar volume for three months preceding the Screening Date / weight of security in each index) is greater than $200 million to be eligible for each index. If a security’s volume factor falls below $200 million at the annual screening, but is currently in the Index, it will remain in the Index. The securities’ weight will be adjusted downwards by an adjustment factor equal to its volume factor dividend by $400 million. |

| · | In the event a security has a calculated volume factor (average daily volume traded over the preceding three months / weight in the index) that is less than $400 million, its weight will be reduced such that weight after volume adjustment = weight before adjustment x calculated volume factor / $400 million. The implementation of the volume factor may cause an increase in the sector weights above the specified caps. |

| Page 21 of 192 |

| 3.5 | Dividend Treatment |

Normal dividend payments are not taken into account in the price Index, whereas they are reinvested and accounted for in the total return Index. However, special dividends require index divisor adjustments to prevent the distribution from distorting the price Index.

| 3.6 | Multiple Share Classes |

In the event a component company issues multiple classes of shares of common stock, the most liquid share class, based on the average daily trading volume as described in section 2.1, will be included in the index. Conversion of a share class in the Index into another share class not in the Index results in the conversion of the share class being phased out into the surviving share class. For all Mid and Small cap cuts, if a security has multiple listed share classes and the total market capitalization of the listed share classes is greater than largest market capitalization cutoff of that index, the security would not be eligible for that index. At least one share class will be eligible for inclusion in either large, mid or small size cut based on total market value of the company.

| 4. | Index Maintenance |

Index Maintenance includes monitoring and implementing the adjustments for company deletions, stock splits, stock dividends, spins-offs, or other corporate actions. Some corporate actions, such as stock splits, stock dividends, and rights offerings require changes in the index shares and the stock prices of the component companies in the Core Equity Indexes. Some corporate actions, such as stock issuances, stock buybacks, warrant issuances, increases or decreases in earnings between reconstitutions, restatements of earnings between reconstitutions, do not require changes in the index shares or the stock prices of the component companies in the Core Equity Indexes. Other corporate actions, such as special dividends, may require Index divisor adjustments. Any corporate action, whether it requires divisor adjustments or not, will be implemented after the close of trading on the day prior to the ex-date of such corporate action, or when the Index Calculation Agent typically applies such corporate actions. Whenever possible, changes to the Index’s components, such as deletions as a result of corporate actions, will be announced at least two business days prior to their implementation date.

| 4.1. | Component Changes |

Additions

Additions to the Core Equity Indexes are made at the annual reconstitution according to the inclusion criteria defined above. Changes are implemented before the opening of trading on the first business day following the “U.S. Reconstitution Date.” Please refer to the Reconstitution Schedule on page 1 for specific dates. No additions are made to any of the Core Equity Indexes between annual reconstitutions, except in the cases of certain spin-off companies, defined below.

| Page 22 of 192 |

Deletions

Shares of companies that are de-listed or acquired by a company outside of the Index are deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in composition of the Index. A component company that files for bankruptcy is deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in the composition of the Index. If a component company is acquired by another company in the Index for stock, the acquiring company’s shares and weight in the Index are adjusted to reflect the transaction after the close of trading on the day prior to the execution date. A component company that is no longer primarily listed in the U.S. or that no longer conducts its Primary Business Activities in the U.S. will be removed from the Index and the weights of the remaining components will be adjusted proportionately to reflect the change in the composition of the Index. Component companies that reclassify their shares (e.g., that convert multiple share classes into a single share class) remain in the Index, although index shares are adjusted to reflect the reclassification.

Spin-Offs and IPOs

Should a company be spun-off from an existing component company, it is allowed to stay in the Core Equity Index that its parent company is in until the next annual reconstitution. Companies that go public in an Initial Public Offering (IPO) and have positive cumulative earnings after four fiscal quarters of operations and meet all other eligibility requirements may be considered for inclusion in a Core Equity Index at the next annual reconstitution of such Index.

Index Divisor Adjustments

Changes in the Index’s market capitalization due to changes in composition, weighting or corporate actions result in a divisor change to maintain the Index’s continuity. By adjusting the divisor, the Index value retains its continuity before and after the event. Corporate actions that require divisor adjustments will be implemented prior to the opening of trading on the effective date. In certain instances where information is incomplete, or the completion of an event is announced too late to be implemented prior to the ex-date, the implementation will occur as of the close of the following day or as soon as practicable thereafter. For corporate actions not described herein, or combinations of different types of corporate events and other exceptional cases, WisdomTree reserves the right to determine the appropriate implementation method.

| Page 23 of 192 |

Companies that are acquired, de-listed, file for bankruptcy, move their Primary Business Activities outside of the U.S. or that cancel their dividends in the intervening weeks between the Screening Date and the U.S. reconstitution date are not included in the Core Equity Indexes, and the weights of the remaining components are adjusted accordingly.

| 5. | Selection Parameters for the Core Equity Indexes |

| 5.1. | The WisdomTree U.S. LargeCap Index is created by selecting the 500 largest component companies of the TI by market capitalization. The component companies are assigned weights in the Index as defined in section 2.4, and the annual reconstitution of the Index takes effect as defined in section 3.1 |

| 5.2. | The WisdomTree U.S. MidCap Index is created based on a defined percentage of the remaining market capitalization of the TI, once the 500 largest companies by market capitalization have been removed. The companies that comprise the top 75% of the remaining market capitalization are selected for inclusion in the MidCap Index. The component companies are assigned weights in the Index as defined in section 2.4., and the annual reconstitution of the Index takes effect as defined in section 3.1. |

| 5.3. | The WisdomTree U.S. SmallCap Index is created based on a defined percentage of the remaining market capitalization of the TI, once the 500 largest companies by market capitalization have been removed. The companies that comprise the bottom 25% of the remaining market capitalization are selected for inclusion in the SmallCap Index. The component companies are assigned weights in the Index as defined in section 2.4., and the annual reconstitution of the Index takes effect as defined in section 3.1. |

| Page 24 of 192 |

Methodology Guide for U.S. Multifactor Index

| 1. | Index Overview and Description |

The WisdomTree U.S. Multifactor Index [referred to as “the Index”] was developed by WisdomTree, Inc. (WT). WisdomTree U.S. Multifactor Index is comprised of 200 U.S. companies with the highest composite scores based on two fundamental factors, value and quality measures, and two technical factors, momentum and correlation.

The Index is reconstituted on a quarterly basis (following the close of trading on the eighth business day in March, June, September and December).

The Index is calculated to capture price appreciation and total return, which assumes dividends are reinvested into the Index. The Index is calculated using primary market prices and calculated in U.S. dollars.

| 2. | Key Features |

| 2.1. | Membership Criteria |

To be eligible for inclusion in the Index, component companies must be under coverage by the market management team of the third-party independent index calculation agent, must list shares on a U.S. stock exchange, conduct its Primary Business Activities6 in the United States. Companies must have had a median daily dollar volume of at least $1,000,000 for each of the three months preceding the Screening Date (after the close of trading on the last trading day in February, May, August, November). Common stocks, REITs, tracking stocks and holding companies are eligible for inclusion. ADRs, GDRs and EDRs, limited partnerships, limited liability companies, royalty trusts, and Business Development Companies (BDCs), preferred stocks, closed-end funds, exchange-traded funds, and derivative securities such as warrants and rights are not eligible. Companies that have pending acquisitions or mergers are excluded from the initial universe. The publicly traded security for WisdomTree, Inc. (NYSE: WT), is also not eligible for inclusion in any of WisdomTree’s equity indexes.

6 The country in which a company conducts its Primary Business Activities is determined based on the following factors: country of organization or incorporation, country in which a company’s headquarters is located, the country to which a company has the greatest risk exposure (“Country of Risk”), and the country from which a company generates the most significant portion of its revenue or to which it allocates the greatest resources. WT may determine to consider additional or different factors depending on the nature of a company’s business and operations.

| Page 25 of 192 |

Top 800 companies by market capitalization that meet the selection criteria are assigned a score for each of the following factors. Factors are equal-weighted at 25%.

| 1) | Value Factor – determined by fundamental valuation ratios, i.e. sales to price, book to price, earnings to price, estimated earnings to price, EBITDA to enterprise value, operating cash flow to price. Scores are calculated within industry groups. |

| 2) | Quality Factor – determined by static observations and trends of return on equity (ROE), return on assets (ROA), gross profits over assets and cash flows over assets. Scores are calculated within industry groups. |

| 3) | Momentum Factor – determined by stocks’ risk adjusted total returns over historical periods (6 and 12 months) |

| 4) | Low Correlation Factor – incorporates diversification potential of stocks that are less correlated to the market over historical periods (6 and 12 months). |

The score for each factor is used to calculate an overall factor score that is used to rank and select the top 25% for inclusion into the Index. The highest ranking multifactor scoring companies will be selected, subject to maximum and minimum constraints on number of components within a sector in seeking sector diversification.

| 2.2 | Base Date and Base Value |

The WisdomTree U.S. Multifactor Index was established with a base value of 200 on June 9, 2017.

| 2.3 | Calculation and Dissemination |

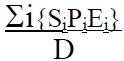

The following formula is used to calculate the index levels for the U.S. Multifactor Index:

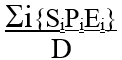

Si = Number of shares in the index for security i.

Pi = Price of security i

Ei = Cross rate of currency of Security i vs. USD. If security price in USD, Ei = 1

D = Divisor

| Page 26 of 192 |

The Index is calculated whenever the U.S. stock exchanges are open. If trading is suspended while the exchange the component company trades on is still open, the last traded price for that stock is used for all subsequent Index computations until trading resumes. If trading is suspended before the opening, the stock’s adjusted closing price from the previous day is used to calculate the Index. Until a particular stock opens, its adjusted closing price from the previous day is used in the Index computation. Index values are calculated on both a price and total-return basis, in U.S. dollars. The price Index and total return Indexes are calculated and disseminated on an end-of-day basis.

| 2.4 | Weighting |

The WisdomTree U.S. Multifactor Index is weighted by a combination of the company overall factor score and inverse volatility over the prior 12 months.

The Weighting Date is when component weights are set, and it occurs after the close of the third business day of the rebalance month. The changes will go into effect after the close of trading on the eighth business day of the rebalance month.

The Index will be modified should the following occur. Should any company achieve a weighting equal to or greater than 24.0% of its Index, its weighting will be reduced to 20.0% at the close of the current calendar quarter, and other components in the Index will be rebalanced. Moreover, should the “collective weight” of Index component securities whose individual current weights equal or exceed 5.0% of the Index, when added together, equal or exceed 50.0% of the Index, the weightings in those component securities will be reduced so that their collective weight equals 40.0% of the Index at the close of the current calendar quarter, and other components in the Index will be rebalanced to reflect their relative weights before the adjustment. Further iterations of these adjustments may occur until no company or group of companies violates these rules.

The following capping rules are applied in this order:

| · | The maximum weight of any individual security is capped at 4% on the quarterly rebalance prior to the introduction of sector caps and the weights of all other components will be adjusted proportionally. |

| · | Sectors are weighted to be sector neutral relative to the sector weights in the starting universe. |

| Page 27 of 192 |

The following liquidity adjustment factors will be applied after the capping rules above have been applied:

A further volume screen requires that a calculated volume factor (the median daily dollar volume for three months preceding the Screening Date / weight of security in each index) shall be greater than $200 million to be eligible for each index. If a security’s volume factor falls below $200 million at the annual screening, but is currently in the Index, it will remain in the Index. The securities’ weight will be adjusted downwards by an adjustment factor equal to its volume factor divided by $400 million.

In the event a security has a calculated volume factor (average daily volume traded over the preceding three months / weight in the index) that is less than $400 million, its weight will be reduced such that weight after volume adjustment = weight before adjustment x calculated volume factor

/ $400 million. The implementation of the volume factor may cause an increase in the holding, sector and country weights above the specified caps.

| 2.5 | Dividend Treatment |

Normal dividend payments are not taken into account in the price Index, whereas they are reinvested and accounted for in the total return Index. However, special dividends that are not reinvested in the total return index require index divisor adjustments to prevent the distribution from distorting the price index.

| 2.6 | Multiple Share Classes |

In the event a component company issues multiple classes of shares of common stock, the share class with the highest average daily volume will be included. Conversion of a share class into another share class results in the deletion of the share class being phased out and an increase in shares of the surviving share class, provided that the surviving share class is in the Index.

| 3. | Index Maintenance |

Index Maintenance includes monitoring and implementing the adjustments for company deletions, stock splits, stock dividends, spins-offs, or other corporate actions. Some corporate actions, such as stock splits, stock dividends, and rights offerings require changes in the index shares and the stock prices of the component companies in the Indexes. Some corporate actions, such as stock issuances, stock buybacks, warrant issuances, increases or decreases in dividend per share between reconstitutions, do not require changes in the index shares or the stock prices of the component companies in the Index. Other corporate actions, such as special dividends and entitlements, may require Index divisor adjustments. Any corporate action, whether it requires divisor adjustments or not, will be implemented after the close of trading on the day prior to the ex-date of such corporate actions. Whenever possible, changes to the Index’s components, such as deletions as a result of corporate actions, will be announced at least two business days prior to their implementation date.

| Page 28 of 192 |

| 3.1. | Component Changes |

Additions

Additions to the Indexes are made at the reconstitution according to the inclusion criteria defined above. Changes are implemented following the close of trading on the eighth business day in March, June, September and December. No additions are made to the Index between reconstitutions, except in the cases of certain spin-off companies defined below.

Deletions

Shares of companies that are de-listed or acquired by a company outside of the Indexes are deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in composition of the Index. A component company that files for bankruptcy is deleted from the Index and the weights of the remaining components are adjusted proportionately to reflect the change in the composition of the Index. If a component company is acquired by another company in the Index for stock, the acquiring company’s shares and weight in the Index are adjusted to reflect the transaction after the close of trading on the day prior to the execution date.7 Component companies that reclassify their shares (i.e. that convert multiple share classes into a single share class) remain in the Index, although index shares are adjusted to reflect the reclassification.

| 3.2. | Spin-Offs and IPOs |

Should a company be spun-off from an existing component company, it is allowed to stay in the Index that its parent company is in until the next reconstitution. Spin-off shares of publicly traded companies that are included in the same indexes as their parent company are increased to reflect the spin-off and the weights of the remaining components will be adjusted proportionately to reflect the change in the composition of the Index. Companies that go public in an Initial Public Offering (IPO) and meet all other eligibility requirements may be considered for inclusion in the Index at the next reconstitution.

7 Companies being acquired will be deleted from the WisdomTree indexes immediately before the effective date of the acquisition or upon notice of a suspension of trading in the stock of the company that is being acquired. In cases where an effective date is not publicly announced in advance, or where a notice of suspension of trading in connection with an acquisition is not announced in advance, WisdomTree reserves the right to delete the company being acquired based on best available market information.

| Page 29 of 192 |

| 4. | Index Divisor Adjustments |

Changes in the Index’s market capitalization due to changes in composition, weighting or corporate actions result in a divisor change to maintain the Index’s continuity. By adjusting the divisor, the Index value retains its continuity before and after the event. Corporate actions that require divisor adjustments will be implemented prior to the opening of trading on the effective date. In certain instances where information is incomplete, or the completion of an event is announced too late to be implemented prior to the ex-date, the implementation will occur as of the close of the following day or as soon as practicable thereafter. For corporate actions not described herein, or combinations of different types of corporate events and other exceptional cases, WisdomTree reserves the right to determine the appropriate implementation method.

Companies that are acquired, de-listed, file for bankruptcy, or move their Primary Business Activities outside of the U.S. in the intervening weeks between the Screening Date and the Reconstitution Date are not included in the Indexes, and the weights of the remaining components are adjusted accordingly.

| 5. | Selection Parameters |

Selection parameters for the WisdomTree U.S. Multifactor Index are defined in section 2.1. Companies that pass these selection criteria as of the Screening Date are included in the Index. The component companies are assigned weights in the Index as defined in section 2.4., and reconstitution of the Index takes effect as defined in section 3.1.

| Page 30 of 192 |

Methodology Guide for International Dividend Indexes

| 1. | Index Overview and Description |

WT has created a family of international indexes that track the performance of dividend-paying companies in developed markets.

The International developed market indexes are sometimes referred to as the “International Dividend Indexes.”

| · | WisdomTree International Equity Index measures the stock performance of investable companies that pay regular cash dividends on shares of common stock and that conduct its Primary Business Activities8 in Japan, the 15 European countries, Australia, Israel, Hong Kong and Singapore. |

| · | The WisdomTree Dynamic International Equity Index is designed to remove from index performance the impact of changes to the value of foreign currencies relative to U.S. dollar with a hedge ratio ranging from 0 to 100% on a monthly basis. |

| · | The WisdomTree International High Dividend Index comprises high dividend yielding stocks from the WisdomTree International Equity Index. |

| · | The WisdomTree True Developed International Index is comprised of the dividend-paying companies from the large-capitalization segment of the WisdomTree International Equity Index and eligible dividend-paying companies with Primary Business Activities9 in South Korea, Poland, and Taiwan. |

| · | The WisdomTree International MidCap Dividend Index is comprised of the dividend-paying companies from the mid-capitalization segment of the WisdomTree International Equity Index. |

| · | The WisdomTree International SmallCap Dividend Index is comprised of the dividend-paying companies from the small-capitalization segment of the WisdomTree International Equity Index. |

8 The country in which a company conducts its Primary Business Activities is determined based on the following factors: country of organization or incorporation, country in which a company’s headquarters is located, the country to which a company has the greatest risk exposure (“Country of Risk”), and the country from which a company generates the most significant portion of its revenue or to which it allocates the greatest resources. WT may determine to consider additional or different factors depending on the nature of a company’s business and operations.

9 The country in which a company conducts its Primary Business Activities is determined based on the following factors: country of organization or incorporation, country in which a company’s headquarters is located, the country to which a company has the greatest risk exposure (“Country of Risk”), and the country from which a company generates the most significant portion of its revenue or to which it allocates the greatest resources. WT may determine to consider additional or different factors depending on the nature of a company’s business and operations.

| Page 31 of 192 |

| · | The WisdomTree Dynamic International SmallCap Equity Index is designed to remove from index performance the impact of changes to the value of foreign currencies relative to U.S. dollar with a hedge ratio ranging from 0 to 100% on a monthly basis. |

| · | The WisdomTree International Quality Dividend Growth Index comprises dividend-paying developed market companies with growth characteristics. |

| · | The WisdomTree International Hedged Quality Dividend Growth Index is designed to remove from index performance the impact of changes to the value of foreign currencies relative to U.S. dollar. |

| · | The WisdomTree Europe Equity Index comprises of dividend-paying companies included in the WisdomTree International Equity Index that conduct their Primary Business Activities in Europe, traded in Euros and derive at least 50% of their revenue from countries outside of Europe. To be deleted from the Index, companies must derive less than 47% of their revenue from countries outside of Europe. |

| · | The WisdomTree Europe Hedged Equity Index is designed to remove from index performance the impact of changes to the value of Euro relative to U.S. dollar. |

| · | WisdomTree Europe SmallCap Equity Index comprises of dividend-paying companies included in the WisdomTree International Equity Index that conduct their Primary Business Activities in Europe and traded in Euros. |

| · | The WisdomTree Europe Hedged SmallCap Equity Index is designed to remove from index performance the impact of changes to the value of Euro relative to |

U.S. dollar.

| · | The WisdomTree Europe SmallCap Dividend Index (“ESC”) is comprised of the dividend-paying companies from the small-capitalization segment of the European companies in the WisdomTree International Equity Index. |

| · | The WisdomTree Europe Quality Dividend Growth Index is derived from the WisdomTree International Equity Index and is comprised of dividend paying European companies with growth characteristics. |

| · | The WisdomTree Japan Dividend Index (“JDI”) measures the performance of investable Japanese companies that pay regular cash dividends on shares of common stock and have less than 80% of revenue come from Japan. |

| · | The WisdomTree Japan Hedged Equity Index is designed to remove from index performance the impact of changes to the value of Japanese Yen relative to U.S. dollar. |

| Page 32 of 192 |

| · | The WisdomTree Japan SmallCap Dividend Index (“JSC”) is comprised of the dividend-paying companies from the small-capitalization segment of the Japanese companies within the WisdomTree International Equity Index. |

| · | The WisdomTree Japan SmallCap Equity Index is comprised of the dividend-paying companies from the small-capitalization segment of the Japanese companies within the WisdomTree International Equity Index. |

| · | The WisdomTree Japan Hedged SmallCap Equity Index is designed to remove from index performance the impact of changes to the value of Japanese Yen relative to U.S. dollar. |

At the International Reconstitution Date each year, the International Dividend Indexes are reconstituted, with each components’ weight adjusted, if necessary, to reflect its dividend-weighting in its respective Index.

All of the International Dividend Indexes are calculated to seek to capture price appreciation and total return, which assumes dividends are reinvested in the components of the Index. The International Dividend Indexes will be calculated using available primary market prices. The International Dividend Indexes are calculated in U.S. dollars.

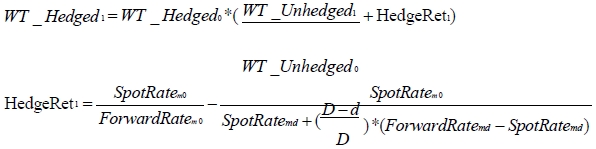

Hedged Equity Indexes

For U.S. investors, international equity investments include two components of return. The first is the return attributable to stock prices in the non-U.S. market or markets in which an investment is made. The second is the return attributable to the value of non-U.S. currencies in these markets relative to U.S. dollar. Hedged Equity Indexes are designed to remove from index performance the impact of their respective currencies relative to U.S. dollar.

In this sense, the Indexes “hedge” against fluctuations in the relative value of non-

U.S. currencies against the U.S. dollar. The Indexes are designed to have higher returns than their equivalent non-currency hedged indexes when the U.S. Dollar is going up in value relative to foreign currencies. Conversely, the Indexes are designed to have lower returns than their equivalent non-hedged indexes when the U.S. dollar is falling in value relative to foreign currencies (e.g., Euro is rising relative to U.S. dollar). Calculation of the Indexes is discussed in section 2.3.

Dynamic Hedged Equity Indexes

The Dynamic Hedged Equity Indexes described above are designed to add a dynamic currency hedge that ranges from 0 to 100% for each currrency.

| Page 33 of 192 |

On a monthly basis the hedge ratio for any individual currency can be adjusted to either 0.00%, 16.7%, 33.3%, 50%, 66.67%, 83.3%, or 100% and are determined by the following signals10:

| · | Momentum: 16.7% of the total hedge ratio is determined by momentum. When the one-month average of the currency’s spot price versus U.S. dollar is weaker than that of the three-month (i.e. the targeted currency is depreciating), the hedge ratio of 16.7% is applied. |

| · | Interest Rate Differentials: 16.7% of the total hedge ratio is determined by measuring the difference in interest rates, as implied in one month FX forwards, between each currency and U.S. dollar. If the implied interest rate in the United States is higher than that within the targeted currency, a further 16.7% hedge ratio is applied for that currency on this signal. |

| · | Low Volatility: 16.7% of the total hedge ratio is determined by a volatility signal that provides unhedged exposure to the lowest volatility currencies. |

| o | The full 16.7% hedge ratio for this signal is applied for the top two thirds currencies with the highest 24-month return volatilities. |

| o | There is no hedge ratio applied for the remaining currencies. |

| · | Time-series momentum: 50% of the total hedge ratio for all currencies is determined by the overall broad trend in the U.S. dollar. |

| o | A hedge ratio of 0% is applied to all currencies if the weighted average momentum of all currencies is below 33% (i.e. less than 33% of the weight of the Index has a Momentum hedge signal). |

| o | A hedge ratio of 50% is applied to all currencies if the weighted average momentum of all currencies is above 66%. (i.e. more than 66% of the weight of the Index has a Momentum hedge signal) |

| o | A hedge ratio of 25% is applied to all currencies otherwise. |

When the dynamic hedges are added, the Indexes are designed to have higher (or similar subject to costs) returns than their equivalent non-currency hedged indexes when U.S. Dollar is going up in value relative to foreign currencies. Conversely, the Indexes are designed to have lower (or similar subject to costs) returns than their equivalent non-hedged indexes when U.S. dollar is falling in value relative to foreign currencies (e.g., foreign currencies are rising relative to U.S. dollar). Calculation of the Indexes is discussed in section 2.3.

10 Israeli Shekels (ILS) and Singapore Dollars (SGD) are hedged at 50% and Hong Kong Dollars (HKD) hedged at 0% on a monthly basis.

| Page 34 of 192 |

| 2. | Key Features |

| 2.1. | Membership Criteria |

To be eligible for inclusion in the above mentioned International Dividend Indexes, component companies must be under coverage by the market management team of the third-party independent index calculation agent and must meet the minimum liquidity requirements established by WT. To be included in any of the International Dividend Indexes, shares of such component securities must have traded at least 250,000 shares per month for each of the six months preceding the “International Screening Date” (after the close of trading on the last trading day in September).

In addition, companies that fall within the bottom decile of a composite risk factor score are not eligible for inclusion in the Domestic Dividend Indexes. The composite risk factor score is used to eliminate potentially higher risk companies that would have otherwise been eligible for inclusion in the Indexes. The composite risk factor score is an equally weighted score of the two factors described below.

| 1) | Quality Factor – determined by static observations and trends of return on equity (ROE), return on assets (ROA), gross profits over assets and cash flows over assets. Scores are calculated within industry groups. |

| 2) | Momentum Factor – determined by stocks’ risk adjusted total returns over historical periods (6 and 12 months) |

Companies that fall within the top 5% ranked by dividend yield and also the bottom ½ of the composite risk factor score are not eligible for inclusion.

The score for each factor is used to calculate an overall factor score, i.e. composite risk score, that is used to eliminate potentially higher risk companies that would have otherwise been eligible for inclusion.