Exhibit 99.1

Exhibit 99.1

February 2, 2026

Boards of Directors

Columbia Bank MHC

Columbia Financial, Inc.

Columbia Bank

19-01 Route 208 North

Fair Lawn, New Jersey 07410

Members of the Boards of Directors:

At your request, RP® Financial, LC. (“RP Financial”) has completed and hereby provides an independent appraisal (“Appraisal”) of the estimated pro forma market value of the common stock which is to be issued in connection with the two-part transaction whereby (1) Columbia Bank MHC (the “MHC”), the parent mutual holding company and majority shareholder of Columbia Financial, Inc. (the “Company” or “CLBK”), the mid-tier holding company and sole owner of Columbia Bank (the “Bank”), will reorganize by completing a second-step mutual-to-stock conversion to full public ownership (“second-step conversion”), and (2) Northfield Bancorp, Inc., Woodbridge, New Jersey (“Northfield Bancorp” or “NFBK”), will merge into the Company and its wholly-owned Northfield Bank will merge into the Bank (the “Merger”). As a result of the second-step conversion, the Company will be succeeded by a new Maryland corporation, also named Columbia Financial, Inc., and the MHC will be merged with the Company and no longer exist (also referred to herein as the “Company” and CLBK”). As of December 31, 2025, CLBK’s shares were owned 73.1% by the MHC and 26.9% by public shareholders (including stock benefit plans). The Company’s public shares are traded on the Nasdaq Global Select Market (“NasdaqGS”) under the ticker symbol “CLBK.” The Company and Bank will continue as the surviving entities following the Merger. The Company’s Plan of Conversion and Reorganization and Agreement (“Plan of Conversion”) and Plan of Merger (“Plan of Merger”) with NFBK, dated January 31, 2026, are incorporated herein by reference.1

This Appraisal is furnished pursuant to the requirements stipulated in the Code of Federal Regulations and has been prepared in accordance with the 1994 “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” (“Valuation Guidelines”) and applicable regulatory interpretations thereof. These Valuation Guidelines were issued by the Office of Thrift Supervision (“OTS”) and are accepted by the Federal Reserve Board (“FRB”), the Office of the Comptroller of the Currency (“OCC”), and the Federal Deposit Insurance Corporation (“FDIC”). The Valuation Guidelines limit valuation peer group selection to relatively comparable publicly-traded savings institutions. RP Financial requested FRB permission to include publicly-traded commercial banks in the valuation peer group given that (1) there is an insufficient number of public thrifts comparable to the Company in its asset size class and (2) on October 15, 2020 the Bank elected to operate as a “Covered Savings Association,” per Section 5A of the Home Owners’

| 1 | The summary description of the second-step conversion and merger contained herein is not intended to be a complete description of these transactions. |

| Washington Headquarters 1311-A Dolley Madison Blvd., Suite 2A McLean, VA 22101 www.rpfinancial.com |

Telephone: (703) 528-1700 Fax No.: (703) 528-1788 E-Mail: mail@rpfinancial.com |

Boards of Directors

February 2, 2026

Page 2

Loan Act (“HOLA”), enabling it to have the same rights and privileges as national banks and continue its commercial bank transitioning. On January 23, 2026, the FRB indicated that it did not object to our inclusion of public commercial banking companies in the valuation peer group given the limited number of public thrifts comparable to the Company’s profile and characteristics.

Summary of Second-Step Conversion and Merger

Pursuant to the Plan of Conversion, (1) CLBK’s publicly-held shares of common stock will be exchanged for shares in the converted Company to retain the current ownership interest at the time the conversion is completed, subject to an adjustment for net MHC assets to be consolidated with the Company (described below), and (2) shares of common stock, representing the MHC’s majority ownership, will be offered in (a) a subscription offering to Eligible Account Holders, Tax-Qualified Employee Benefit Plans including the Bank’s employee stock ownership plan (the “ESOP”), Supplemental Eligible Account Holders and Other Members, and (b) in a community offering and a stand-by firm commitment offering led by Keefe, Bruyette & Woods, a Stifel Company, if any shares remain after the subscription offering.

NFBK’s issued and outstanding shares of common stock will be converted at the election of the holder into the right to receive either shares of the Company (“Stock Consideration”) or cash (“Cash Consideration”) provided that no more than 30% of the NFBK shares will be converted into Cash Consideration. The Stock Consideration and the Cash Consideration will be dependent upon the “Final Valuation” determined by RP Financial at the closing of the second-step conversion and merger, as follows: (1) if the Final Valuation (full conversion value) is less than $2.3 billion, NFBK shareholders may elect to receive 1.425 shares of CLBK’s common stock, based on a $10.00 per share offering price, or $14.25 in cash for each share of NFBK common stock; (2) if the Final Valuation is equal to or greater than $2.3 billion and less than $2.6 billion, NFBK shareholders may elect to receive 1.450 shares of CLBK’s common stock, based on a $10.00 per share offering price, or $14.50 in cash for each share of Northfield Bancorp common stock; or (3) if the Final Valuation is equal to or greater than $2.6 billion, NFBK shareholders may elect to receive 1.465 shares of CLBK’s common stock, based on a $10.00 per share offering price, or $14.65 in cash for each share of NFBK common stock. Based on the midpoint of the conversion offering range and a 1.425x exchange ratio, the aggregate merger consideration is approximately $597.1 million.

RP® Financial, LC.

RP Financial is a financial consulting firm serving the financial services industry nationwide that, among other things, specializes in financial valuations and analyses of business enterprises and securities, including the pro forma valuation for savings institutions converting from mutual-to-stock form. Our background and experience is detailed in Exhibit V-1. We believe that, except for the fee we will receive for the Appraisal, we are independent of the Company and NFBK. RP Financial is independent from the legal, investment, accounting, and other advisors retained by the Company and NFBK in connection with the second-step conversion and Merger. While RP Financial has previously provided conversion and other valuation services to both the Company and NFBK, at the time of engagement RP Financial was not engaged to provide any services to the Company or NFBK.

Boards of Directors

February 2, 2026

Page 3

Valuation Methodology

In preparing our Appraisal, we have reviewed the Company’s regulatory applications, including the draft prospectus, as filed with the FRB and the Securities and Exchange Commission (“SEC”). We have conducted a financial analysis of the Company that included a review of audited financial information for the five years ended December 31, 2025, recent unaudited information, regulatory, and internal financial reports through December 31, 2025, and related discussions with the Company’s management. We have discussed the conversion and Merger transactions with the Company’s advisors – KPMG LLP, independent auditor; Kilpatrick Townsend & Stockton LLP, conversion counsel; and Keefe Bruyette & Woods, Inc., investment banker. We have reviewed the pro forma financial impact of the Merger based on data and information in the prospectus, NFBK’s audited financial information for the five years ended December 31, 2025, various unaudited, regulatory, and internal financial reports through December 31, 2025, and related discussions with NFBK’s management. We have incorporated the structural aspects of the second-step conversion and merger into our Appraisal analysis, including but not limited to offering range, transaction expenses, stock benefit plan purchases, merger fair value adjustments, after-tax reinvestment rate, and other accounting adjustments. Our Appraisal conclusion was reached independently from such discussions. In addition, where appropriate, we have considered data and information based on other available published sources that we believe are reliable, however we cannot guarantee the accuracy and completeness of such data and information.

We have considered the competitive, economic and demographic characteristics of the Company’s primary market and operating environment. We have assessed the Company’s relative strengths and weaknesses to the industry and the valuation peer group. We have kept abreast of the changing regulatory and legislative environment for financial institutions and analyzed the potential impact on the Company and the industry as a whole. We have analyzed the potential effects of the second-step conversion and the merger on Company’s financial and operating characteristics. We have incorporated the financial and exchange ratio impact of the contribution of the MHC assets to the Company. We have compared the Company’s financial performance and condition incorporating the NFBK merger with the selected valuation peer group and other publicly-traded financial institutions. In selecting the valuation peer group, we excluded those subject to announced or rumored acquisition or have unusual characteristics. We have reviewed current conditions in the securities markets in general and the market for financial institution stocks and the valuation peer group as well as the market for publicly-traded financial institutions and those that recently completed stock conversions. We have also considered the stock price and trading activity of CLBK’s shares prior to and since the announcement of the second-step conversion and merger.

The Appraisal is based on the Company’s representation that the information contained in the regulatory applications and prospectus and additional data and information furnished to us by the Company, NFBK and their respective advisors are truthful, accurate and complete. We did not independently verify the financial statements and other data and information provided by the Company, NFBK, and their respective independent advisors nor did we independently value the individual assets or liabilities of the Company and NFBK. Our Appraisal is predicated on the Company completing the second-step conversion and merger in a manner consistent that are set forth in the regulatory applications and prospectus. Our Appraisal considers the Company only as a going concern and should not be considered as an indication of liquidation or acquisition value.

Boards of Directors

February 2, 2026

Page 4

Our appraised value is predicated on a continuation of the current operating environment for the Company, NFBK, and for all financial institutions and their holding companies. Changes in the local, state and national economy, the legislative and regulatory environment for financial institutions and holding companies, the stock market, interest rates, and other external forces (such as natural disasters or significant world events) may occur from time to time, often with great unpredictability and may materially impact the value of financial institution stocks as a whole or the value of the Company’s stock alone. To the extent that such factors can be foreseen, they have been factored into our analysis. It is our understanding that CLBK has no current plans to sell control following completion of the second-step conversion and merger.

The estimated pro forma market value is defined as the price at which CLBK’s common stock, immediately upon completion of the second-step conversion and merger, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

Valuation Conclusion

It is our opinion that, as of February 2, 2026, the estimated aggregate pro forma value of CLBK’s shares of common stock to be issued and outstanding upon completing the conversion offering – including (1) newly-issued shares representing the MHC’s current ownership interest in the Company and (2) exchange shares issued to CLBK’s public shareholders – was $2,291,268,770 at the midpoint, equal to 229,126,877 shares at $10.00 per share. The resulting range of value and pro forma shares, based on $10.00 per share, is: $1,947,578,450 or 194,757,845 shares at the minimum and adjusted minimum; and $2,634,959,080 or 263,495,908 shares at the maximum.

The resulting midpoint offering amount, based on the MHC’s ownership, is $1,675,000,000, or 1,675,000,000 shares at $10.00 per share, resulting in an offering range, based on $10.00 per share, of: $1,423,750,000 or 142,375,000 shares at the minimum and $1,926,250,000 or 192,625,000 shares at the maximum. If there are unsubscribed offering shares below the minimum of the offering range, the Company may apply up to 41,800,140 of the merger shares to the offering (“adjusted minimum”). Accordingly, at the adjusted minimum of the offering range, the indicated public offering is $1,005,748,600, or 100,574,860 shares at $10.00 per share, with merger shares applied to the offering up to $418,001,140, or 41,800,140 shares at $10.00 per share.

The following table reflects the conversion offering shares, exchange shares for minority shareholders, and merger shares issued to NFBK’s shareholders at the maximum, midpoint and minimum of the range, and the full application of merger shares to the offering in the event of an undersubscribed offering, all based on a $10.00 per share price.

Boards of Directors

February 2, 2026

Page 5

| Shares Conclusion |

2nd Step Offering Shares |

2nd Step Exchange Shares |

Full Conversion Shares |

Shares Issued To Target |

Shares Applied to Offering |

Total Market Capitalization Shares |

Exchange Ratio |

Merger Shares Pct. Of Total |

||||||||||||||||||||||||

| Maximum |

192,625,000 | 70,870,908 | 263,495,908 | 42,973,477 | 0 | 306,469,385 | 2.5340 | 14.02 | % | |||||||||||||||||||||||

| Midpoint |

167,500,000 | 61,626,877 | 229,126,877 | 41,800,140 | 0 | 270,927,017 | 2.2035 | 15.43 | % | |||||||||||||||||||||||

| Minimum |

142,375,000 | 52,382,845 | 194,757,845 | 41,800,140 | 0 | 236,557,985 | 1.8729 | 17.67 | % | |||||||||||||||||||||||

| Adusted Minimum(4) |

100,574,860 | 52,382,845 | 194,757,845 | 0 | 41,800,140 | 194,757,845 | 1.8729 | 21.46 | % | |||||||||||||||||||||||

| Market Value Conclusion |

2nd Step Offering Value |

2nd Step Exchange Shares Value |

Full Conversion Value |

Merger Shares Value |

Merger Shares Applied to Offering |

Total Market Capitalization Value |

||||||||||||||||||

| Maximum |

$ | 1,926,250,000 | $ | 708,709,080 | $ | 2,634,959,080 | $ | 429,734,770 | 0 | $ | 3,064,693,850 | |||||||||||||

| Midpoint |

$ | 1,675,000,000 | $ | 616,268,770 | $ | 2,291,268,770 | $ | 418,001,400 | 0 | $ | 2,709,270,170 | |||||||||||||

| Minimum |

$ | 1,423,750,000 | $ | 523,828,450 | $ | 1,947,578,450 | $ | 418,001,400 | 0 | $ | 2,365,579,850 | |||||||||||||

| Adjusted Minimum(4) |

$ | 1,005,748,600 | $ | 523,828,450 | $ | 1,947,578,450 | $ | 0 | 418,001,400 | $ | 1,947,578,450 | |||||||||||||

Board Establishment of Exchange Ratio

The conversion regulations provide that in second-step conversion the mid-tier company’s minority stockholders are entitled to exchange their shares for newly-issued shares in the fully converted company so as to preserve their current ownership ratio. The exchange ratio for minority shareholders is determined by the Board at the close of the offering based on the total shares issued in the second-step conversion per the final appraisal and the offering price per share determined by the Board. The indicated exchange ratio is then subject to FRB policy potentially leading to minority shareholder dilution with the consolidation of the MHC’s net assets with the issuer’s equity at closing. In the Company’s case, however, the MHC has net liabilities of $48,000, leading to a nominal reduction of equity. Accordingly, no adjustment to the minority shareholder exchange ratio per the FRB policy is applicable in the Company’s second-step conversion. Based on the valuation conclusion herein and resulting offering range and the Board’s determination of a $10.00 per share offering price, the indicated minority exchange ratio is as follows: maximum – 2.5340 shares; midpoint – 2.2035 shares; minimum – 1.8729 shares; and minimum, as adjusted – 1.8729 shares.

Limiting Factors and Considerations

The valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the common stock. Moreover, because such valuation is determined in accordance with applicable regulatory guidelines and is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the conversion offering, or prior to that time, will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the estimated pro forma market value thereof. The Appraisal reflects only a valuation range as of this date for the pro forma market value of the Company immediately upon issuance of the stock and does not take into account any trading activity with respect to the purchase and sale of common stock in the secondary market on the date of issuance of such securities or at anytime thereafter following the completion of the second-step conversion.

Boards of Directors

February 2, 2026

Page 6

RP Financial’s valuation was based on the financial condition, operations and shares outstanding of CLBK and NFBK as of December 31, 2025, the date of the financial data included in the prospectus. The proposed exchange ratio to be received by the current public stockholders of CLBK and the exchange of the public shares for newly issued shares of the Company’s common stock as a full public company was determined independently by CLBK’s Boards of Directors incorporating the required FRB adjustment for MHC assets.

RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees, from purchasing stock of its client institutions.

This Appraisal may be updated as provided for in the conversion regulations and guidelines. These updates will consider, among other things, any developments or changes in the financial performance and condition of the Company and NFBK, management policies, and current conditions in the equity markets for thrift shares, both existing issues and new issues. These updates may also consider changes in other external factors which impact value including but not limited to: various changes in the legislative and regulatory environment for financial institutions, the stock market and the market for financial institution stocks, and interest rates. Should any such new developments or changes be material, in our opinion, to the valuation of the shares, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in the update at the date of the release of the update. The Appraisal will also be updated concurrent with the completion of stock offering and merger.

| Respectfully submitted, |

| RP® FINANCIAL, LC. |

|

| Ronald S. Riggins |

| Managing Director |

|

| Gregory E. Dunn |

| Director |

| RP® Financial, LC. | TABLE OF CONTENTS i |

TABLE OF CONTENTS

COLUMBIA FINANCIAL, INC.

COLUMBIA BANK

Fair Lawn, New Jersey

| DESCRIPTION |

PAGE |

|||

| CHAPTER ONE OVERVIEW AND FINANCIAL ANALYSIS |

| |||

| Introduction |

I.1 | |||

| Plan of Conversion |

I.2 | |||

| Acquisition of Northfield Bancorp, Inc. |

I.2 | |||

| Strategic Overview |

I.4 | |||

| Reasons for the Acquisition of Northfield Bancorp, Inc. |

I.5 | |||

| Reasons for the Second-Step Conversion and Use of Proceeds |

I.6 | |||

| Balance Sheet Trends |

I.7 | |||

| Pro Forma Balance Sheet Impact of Northfield Bancorp Acquisition |

I.11 | |||

| Income and Expense Trends |

I.11 | |||

| Pro Forma Earnings Impact of Northfield Bancorp Acquisition |

I.14 | |||

| Interest Rate Risk Management |

I.15 | |||

| Lending Activities and Strategy |

I.16 | |||

| Asset Quality |

I.19 | |||

| Funding Composition and Strategy |

I.20 | |||

| Subsidiaries |

I.21 | |||

| Legal Proceedings |

I.23 | |||

| CHAPTER TWO MARKET AREA ANALYSIS |

| |||

| Introduction |

II.1 | |||

| National Economic Factors |

II.1 | |||

| Market Area Demographics |

II.5 | |||

| Local Economy |

II.9 | |||

| Unemployment Trends |

II.11 | |||

| Market Area Deposit Characteristics and Competition |

II.12 | |||

| CHAPTER THREE PEER GROUP ANALYSIS |

| |||

| Peer Group Selection |

III.1 | |||

| Financial Condition |

III.6 | |||

| Income and Expense Components |

III.9 | |||

| Loan Composition |

III.11 | |||

| Interest Rate Risk |

III.13 | |||

| Credit Risk |

III.15 | |||

| Summary |

III.15 | |||

| RP® Financial, LC. | TABLE OF CONTENTS ii |

TABLE OF CONTENTS

COLUMBIA FINANCIAL, INC.

COLUMBIA BANK

Fair Lawn, New Jersey

(continued)

| DESCRIPTION |

PAGE NUMBER |

|||

| CHAPTER FOUR VALUATION ANALYSIS |

| |||

| Introduction |

IV.1 | |||

| Appraisal Guidelines |

IV.1 | |||

| RP Financial Approach to the Valuation |

IV.1 | |||

| Valuation Analysis |

IV.2 | |||

| 1. Financial Condition |

IV.3 | |||

| 2. Profitability, Growth and Viability of Earnings |

IV.4 | |||

| 3. Asset Growth |

IV.6 | |||

| 4. Primary Market Area |

IV.6 | |||

| 5. Dividends |

IV.8 | |||

| 6. Liquidity of the Shares |

IV.8 | |||

| 7. Marketing of the Issue |

IV.9 | |||

| A. The Public Market |

IV.9 | |||

| B. The New Issue Market |

IV.14 | |||

| C. The Acquisition Market |

IV.15 | |||

| D. Trading in CLBK’s Stock |

IV.17 | |||

| 8. Management |

IV.18 | |||

| 9. Effect of Government Regulation and Regulatory Reform |

IV.18 | |||

| Summary of Adjustments |

IV.18 | |||

| Valuation Approaches |

IV.19 | |||

| 1. Price-to-Earnings (“P/E”) |

IV.21 | |||

| 2. Price-to-Book (“P/B”) |

IV.23 | |||

| 3. Price-to-Assets (“P/A”) |

IV.23 | |||

| Comparison to Recent Offerings |

IV.24 | |||

| Valuation Conclusion |

IV.24 | |||

| Establishment of the Exchange Ratio |

IV.25 | |||

| RP® Financial, LC. | LIST OF TABLES iii |

LIST OF TABLES

COLUMBIA FINANCIAL, INC.

COLUMBIA BANK

Fair Lawn, New Jersey

| TABLE | ||||||

| NUMBER | DESCRIPTION | PAGE | ||||

| 1.1 | Historical Balance Sheet Data | I.8 | ||||

| 1.2 | Historical Income Statements | I.12 | ||||

| 2.1 | Summary Demographic Data | II.6 | ||||

| 2.2 | Primary Market Area Employment Sectors | II.10 | ||||

| 2.3 | Top Employers in Market Area | II.10 | ||||

| 2.4 | Unemployment Trends | II.11 | ||||

| 2.5 | Deposit Summary | II.13 | ||||

| 2.6 | Market Area Deposit Competitors | II.14 | ||||

| 3.1 | Peer Group of Publicly-Traded Banks and Thrifts | III.3 | ||||

| 3.2 | Balance Sheet Composition and Growth Rates | III.7 | ||||

| 3.3 | Income as a % of Average Assets and Yields, Costs, Spreads | III.10 | ||||

| 3.4 | Loan Portfolio Composition and Related Information | III.12 | ||||

| 3.5 | Interest Rate Risk Measures and Net Interest Income Volatility | III.14 | ||||

| 3.6 | Credit Risk Measures and Related Information | III.16 | ||||

| 4.1 | Market Area Unemployment Rates | IV.7 | ||||

| 4.2 | Pricing Characteristics and After-Market Trends | IV.16 | ||||

| 4.3 | Pro Forma Market Pricing Versus Peer Group | IV.22 | ||||

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.1 |

I. OVERVIEW AND FINANCIAL ANALYSIS

Introduction

Columbia Bank (the “Bank”), founded in 1927, is a federally chartered stock savings bank headquartered in Fairlawn, New Jersey. The Bank serves the state of New Jersey and the suburbs surrounding the New York City and Philadelphia metropolitan areas through its headquarters office and 71 full service branch offices, all of which are located in the state of New Jersey. The Bank is subject to regulation and oversight by the Office of the Comptroller of the Currency (the “OCC”). On October 15, 2020 the Bank elected to operate as a “Covered Savings Association”, per section 5A of the Homeowners’ Loan Act (“HOLA”), enabling it to have the same rights and privileges as national banks and continue its commercial bank transitioning. The Bank is a member of the Federal Home Loan Bank (“FHLB”) system, and its deposits are insured up to the regulatory limits by the Federal Deposit Insurance Corporation (the “FDIC”).

Columbia Financial, Inc. (“CLBK”) is the mid-tier holding company of the Bank and owns 100% of the outstanding common stock of the Bank. CLBK is a Delaware corporation that was organized on March 1997 and has since been engaged primarily in the business of holding the common stock of the Bank. Columbia Bank, MHC (the “MHC”) was also organized in March 1997 and is the federally-chartered mutual holding company parent of CLBK. CLBK completed its initial public offering (“IPO”) on April 19, 2018, pursuant to which it sold 49,832,345 shares or 43.0% of its outstanding common stock to the public and issued 62,580,155 shares or 54.0% of its common stock outstanding to the MHC. Additionally, CLBK issued 3,476,675 shares of common stock or 3.0% of its common stock outstanding to the Columbia Bank Foundation. Since the IPO, stock repurchase programs conducted by CLBK have reduced the total number of public shares outstanding, while shares issued to the MHC in connection with acquisitions completed by CLBK of other mutual holding companies and their bank subsidiaries have increased the number of MHC shares outstanding. The MHC and CLBK are subject to supervision and regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve Board” or the “FRB”). At December 31, 2025, CLBK had total consolidated assets of $11.0 billion, deposits of $8.4 billion and equity of $1.2 billion or 10.53% of total assets. Excluding goodwill and core deposit intangibles of $117.7 million, CLBK’s tangible equity equaled $1.0 billion or 9.47% of total assets at December 31, 2025. CLBK’s audited financial statements for the most recent period are included by reference as Exhibit I-1.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.2 |

Plan of Conversion

On January 31, 2026, the respective Boards of Directors of the MHC and CLBK adopted the Plan of Conversion whereby the MHC will convert to stock form. As a result of the conversion, CLBK, which currently owns all of the issued and outstanding common stock of the Bank, will be succeeded by a new Maryland corporation with the name of Columbia Financial, Inc. (“Columbia Financial” or the “Company”). Following the conversion, the MHC will no longer exist. For purposes of this document, the existing consolidated entity will hereinafter also be referred to as Columbia Financial or the Company, unless otherwise identified as CLBK. As of December 31, 2025, the MHC had a majority ownership interest in, and its principal asset consisted of, approximately 73.10% of the common stock (the “MHC Shares”) of CLBK. The remaining 26.90% of CLBK’s common stock was owned by public shareholders.

Pursuant to the Plan of Conversion, it is our understanding that Columbia Financial will offer its stock representing the majority ownership interest held by the MHC in a subscription offering to Eligible Account Holders, Tax-Qualified Employee Plans including the Bank’s employee stock ownership plan (the “ESOP”), Supplemental Eligible Account Holders and Other Members, as such terms are defined for purposes of applicable federal regulatory requirements governing mutual-to-stock conversions. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to the general public in a community offering and a firm commitment offering. Upon completing the mutual-to-stock conversion and stock offering (the “second-step conversion”), the Company will be 100% owned by public shareholders, the publicly-held shares of CLBK will be exchanged for shares in the Company at a ratio that retains their ownership interest at the time the conversion is completed and the MHC assets will be consolidated with the Company.

Acquisition of Northfield Bancorp, Inc.

In connection with the second-step conversion, the Boards of Directors of CLBK, Columbia Financial and the MHC entered into an Agreement and Plan of Merger (the “Agreement”) with Northfield Bancorp, Inc., Woodbridge, New Jersey (“Northfield Bancorp”). Pursuant to the Agreement, Northfield Bancorp will merge with and into Columbia Financial, with Columbia Financial as the surviving entity (the “Merger”). Immediately following the Merger, Northfield Bank, a federal savings bank and a wholly owned subsidiary of Northfield Bancorp, will merge with and into Columbia Bank with Columbia Bank as the surviving entity.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.3 |

As set forth in Agreement, if the Final Independent Valuation (full conversion value) is less than $2.3 billion, Northfield Bancorp shareholders may elect to receive 1.425 shares of Columbia Financial common stock, based on a $10.00 per share offering price, or $14.25 in cash for each share of Northfield Bancorp common stock. If the Final Independent Valuation is equal to or greater than $2.3 billion and less than $2.6 billion, Northfield Bancorp shareholders may elect to receive 1.450 shares of Columbia Financial common stock, based on a $10.00 per share offering price, or $14.50 in cash for each share of Northfield Bancorp common stock. If the Final Independent Valuation is equal to or greater than $2.6 billion, Northfield Bancorp shareholders may elect to receive 1.465 shares of Columbia Financial common stock, based on a $10.00 per share offering price, or $14.65 in cash for each share of Northfield Bancorp common stock. The proration procedures set forth in the Agreement require that the cash consideration shall not be greater than 30% of the total merger consideration. The aggregate transaction value of the merger consideration, based on an exchange ratio of 1.425x which is the exchange ratio at the midpoint of the offering range, is approximately $597.1 million. Based on Northfield Bancorp’s consolidated balance sheet at December 31, 2025 and estimated fair value accounting adjustments, total intangible assets resulting from the acquisition have been estimated to equal $73.3 million.

Northfield Bancorp, Inc.

Northfield Bancorp is a Delaware corporation and is the bank holding company for Northfield Bank, which is the primary asset of Northfield Bancorp. Northfield Bancorp’s common stock is listed on the NASDAQ Global Market under the symbol “NFBK”. As of December 31, 2025, Northfield Bancorp reported consolidated assets of $5.8 billion, net loans receivable of $3.8 billion, deposits of $4.0 billion, borrowings of $900.2 million, subordinated debt of $61.7 million and stockholders’ equity of $690.1 million, equal to 11.99% of total assets. Northfield Bancorp reported earnings for the year ended December 31, 2025 of $790,000 equal to 0.01% of average assets. Earnings for 2025 were negatively impacted by a $41.0 million charge for impairment of goodwill.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.4 |

Northfield Bank

Northfield Bank was organized in 1887 and is a federally chartered savings bank. Northfield Bank conducts business from its operations center located in Woodbridge, New Jersey, its home office located at a branch in Staten Island, New York and its 36 additional branch offices located in Staten Island, Brooklyn, and the New Jersey counties of Hunterdon, Mercer, Middlesex and Union. Northfield Bank is subject to regulation, examination and supervision by the OCC.

Strategic Overview

Columbia Financial maintains a local community banking emphasis with a primary strategic objective of meeting the borrowing and savings needs of consumers and businesses throughout its market area. The Company considers its market area to be the state of New Jersy and the suburbs surrounding the New York City and Philadelphia metropolitan areas. In recent years, the Company has pursued a strategy of evolving its business model into that of a full service community bank through growing a diversified loan portfolio, increasing core deposits, building non-interest revenue sources and expansion and diversification of the bank franchise through acquisitions. In addition to offering traditional community bank financial services, Columbia Bank maintains wholly owned subsidiaries that offer title insurance and insurance products and investment solutions including personal and business lines of insurance. The Company also offers wealth management services through a third-party relationship.

Columbia Financial’s earnings base is largely dependent upon net interest income and operating expense levels. After experiencing net interest margin compression in 2023 and 2024, the Company’s net interest margin increased in 2025. Net interest margin compression in 2023 and 2024 was due to a more significant increase in the cost of interest-bearing liabilities relative to the increase in yield earned on interest-earning assets, while the increase in the net interest margin during 2025 was facilitated by a balance sheet repositioning transaction completed in the fourth quarter of 2024. During the fourth quarter of 2024, the Company sold $352.3 million of lower yielding available for sale investment securities and the proceeds from the sale were used to fund loan growth, purchase higher yielding investment securities and prepay higher cost borrowings. Operating expenses and revenues derived from sources of non-interest operating income have been maintained at relatively low levels as percent of average assets, while credit loss provisions have generally been a limited factor in the Company’ earnings. Non-operating income and losses were a more significant factor in the Company earnings during 2023 and 2024, which was due to losses recorded on investment securities transactions.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.5 |

Beginning in 2019, the Company has supplemented organic growth through the acquisition of four financial institutions and an insurance agency:

| • | On November 1 2019, the Company completed the acquisition of Stewardship Financial Corporation (“Stewardship Financial”) and its wholly-owned subsidiary, Atlantic Stewardship Bank, a $964 million bank based in Midland Park, New Jersey. |

| • | On April 1, 2020, the Company completed the acquisition of RSB Bancorp, MHC, RSB Bancorp, Inc. and its wholly-owned subsidiary Roselle Bank, a $422 million bank based in Roselle, New Jersey. |

| • | On December 1, 2021, the Company completed the acquisition of Freehold Bancorp, MHC, Freehold Bancorp, Inc. and its wholly owned subsidiary Freehold Bank, a $294 million bank based in Freehold, New Jersey. |

| • | On May 1, 2022, the Company completed the acquisition of RSI Bancorp, M.H.C., RSI Bancorp, Inc. and its wholly owned subsidiary RSI Bank, a $621 million bank based in Rahway, New Jersey. |

| • | On September 17, 2025, the Company completed the acquisition of Jeanne S. Frey Insurance Agency, Inc., a provider of insurance brokerage services based in Newfoundland, New Jersey. |

Reasons for the Acquisition of Northfield Bancorp

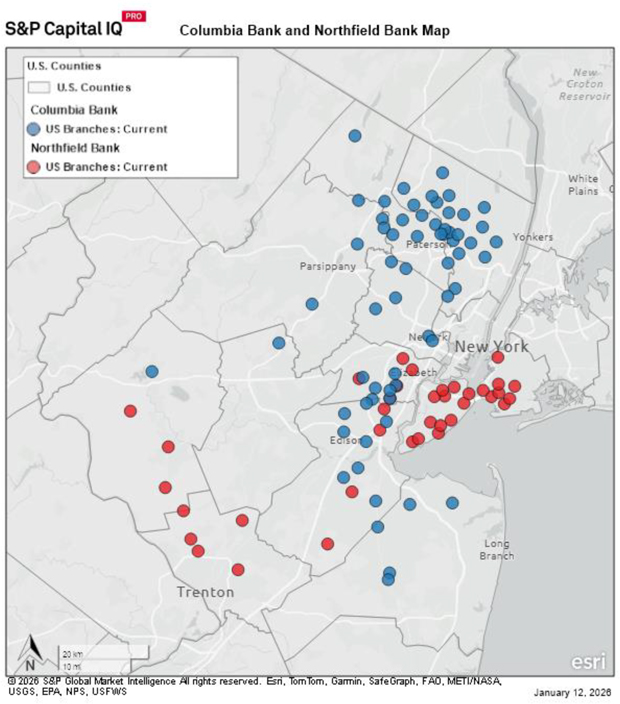

Through the acquisition of Northfield Bancorp, the Company will increase its market presence in certain New Jersey markets and provide an expansion of the Company’s markets into the New York City markets of Staten Island and Brooklyn. A map of the Company’s branch network following the acquisition of Northfield Bancorp is set forth in Exhibit I-2. Other reasons for the merger are set forth below.

| • | The combined entity is expected to meaningfully increase net income and return on assets. |

| • | The merger effectively leverages a portion of the capital raised in the offering. |

| • | The larger branch network and expanded geographic presence will enhance customer convenience and facilitate opportunities for growth at all of the Company’s branches. |

| • | The combined entity will have a larger customer base for purposes of cross-selling the Company’s products and services. |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.6 |

| • | The larger asset size, geographic presence and market capitalization that will result from the acquisition will better position the Company to pursue other strategic acquisitions. |

| • | The combined entity will enhance infrastructure resources to facilitate broadening of products and services capabilities, as well as improve product delivery and efficiency. |

| • | Certain operating synergies, net of certain consolidation costs, are anticipated as a result of the merger, including: |

| — | Elimination of certain duplicative professional services, such as legal, audit and tax and consulting; and |

| — | Spreading securities, shareholder reporting and regulatory reporting and examination expenses over a larger asset base. |

Reasons for Second-Step Coversino and Use of Proceeds

A key component of the Company’s business plan is to complete a second-step conversion offering. The second-step offering will strengthen the Company’s capital position and support growth for purposes of building shareholder value, most notably through the acquisition of Northfield Bancorp. A portion of the conversion proceeds will be utilized to fund the cash consideration to be paid for the acquisition and other merger costs. Additionally, the second-step conversion and increased capital resources that will result from the sale and issuance of common stock will support: (1) expansion of lending and deposit gathering activities with a broader geographic distribution and larger lending platform; (2) potential expansion and diversification of operations through acquisitions of other financial institutions or de novo branching as opportunities arise; (3) strengthening of competitive position; (4) earnings enhancements that will be realized from the combined institutions through leveraging of infrastructure and implementation of operating efficiencies; (5) increasing stockholder returns through higher earnings and more flexible capital management strategies, including elimination of the current limitations imposed by the mutual holding company structure on dividend payments; and (6) as a fully-converted stock holding company, there will be a more liquid and active trading market for the Company’s stock and the Company will have greater flexibility to access capital markets through possible future equity and debt offerings. The projected use of proceeds is highlighted below.

| • | Columbia Financial. The Company is expected to retain up to 50% of the net offering proceeds. At present, funds at the Company level, net of the loan to the ESOP, will be used to fund the cash portion of the merger consideration and other related merger costs incurred to facilitate the acquisition of Northfield Bancorp. The remaining balance of cash is expected to be invested into a |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.7 |

| deposit at the Bank. The approximate cash cost to be paid for the acquisition is $179.1 million, assuming an acquisition exchange ratio of 1.425x and 30% of the consideration is cash. Over time, the funds held in a deposit at the Bank may be utilized for various corporate purposes, possibly including acquisitions, infusing additional equity into the Bank, repurchases of common stock and the payment of cash dividends. |

| • | Columbia Bank. Approximately 50% of the net offering proceeds will be infused into the Bank. Cash proceeds infused into the Bank will initially become part of general funds, the substantial portion of which will be deployed into loans and investments. Under the terms of the merger agreement, Northfield Bank will be merged into Columbia Bank. |

Overall, it is the Company’s objective to pursue controlled growth that will serve to increase returns, while continuing to emphasize management of the overall risk associated with Columbia Financial’s operations.

Balance Sheet Trends

Table 1.1 shows the Company’s historical balance sheet data for the past five years through December 31, 2025, as well as the Company’s pro forma balance sheet at December 31, 2025. The pro forma balance sheet reflects the acquisition of Northfield Bancorp before incorporating the capital to be raised in the stock offering. The following discussion describes the historical balance sheet trends for Columbia Financial on a pre-acquisition basis. The pro forma balance sheet impact of the acquisition of Northfield Bancorp will be discussed at the end of this section.

Asset growth trends from yearend 2021 through yearend 2025 show asset growth was stronger in 2022 and 2025, while total assets declined in 2024. The stronger asset growth recorded in 2022 was in part attributable to acquisition-related growth. Loan growth was the main driver of the Company’s asset growth, with a combination of deposit growth and increased utilization of borrowings constituting the primary funding sources for the asset growth. Overall, the Company’s assets increased from $9.2 billion at yearend 2021 to $11.0 billion at yearend 2025, which provided for an annual growth rate of 4.54%. A summary of Columbia Financial’s key operating ratios for the past five years is presented in Exhibit I-3.

Columbia Financial’s loans receivable portfolio increased at a 6.90% annual rate from yearend 2021 through yearend 2025, in which the loans receivable balance trended higher throughout the period with the strongest growth occurring in 2022 and 2025. Net loans receivable at December 31, 2015 totaled $8.2 billion, versus $6.3 billion at December 31, 2021.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.8 |

Table 1.1

Columbia Financial, Inc.

Historical Balance Sheet Data

| 12/31/21- | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| At December 31, | 12/31/25 Annual. Growth Rate |

Pro Forma Combined(2) At December 31, |

||||||||||||||||||||||||||||||||||||||||||||||||||

| 2021 | 2022 | 2023 | 2024 | 2025 | 2025 | |||||||||||||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Pct | Amount | Pct(1) | ||||||||||||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | (%) | ($000) | (%) | ||||||||||||||||||||||||||||||||||||||||

| Total Amount of: |

||||||||||||||||||||||||||||||||||||||||||||||||||||

| Assets |

$ | 9,224,097 | 100.00 | % | $ | 10,408,169 | 100.00 | % | $ | 10,645,568 | 100.00 | % | $ | 10,475,493 | 100.00 | % | $ | 11,018,793 | 100.00 | % | 4.54 | % | $ | 16,488,131 | 100.00 | % | ||||||||||||||||||||||||||

| Cash and cash equivalents |

70,963 | 0.77 | % | 179,228 | 1.72 | % | 423,249 | 3.98 | % | 289,223 | 2.76 | % | 340,806 | 3.09 | % | 48.04 | % | 297,219 | 1.80 | % | ||||||||||||||||||||||||||||||||

| Investment securities |

2,136,291 | 23.16 | % | 1,753,541 | 16.85 | % | 1,498,790 | 14.08 | % | 1,425,009 | 13.60 | % | 1,525,052 | 13.84 | % | -8.08 | % | 2,965,497 | 17.99 | % | ||||||||||||||||||||||||||||||||

| Loans receivable, net |

6,297,912 | 68.28 | % | 7,624,761 | 73.26 | % | 7,819,441 | 73.45 | % | 7,856,970 | 75.00 | % | 8,224,809 | 74.64 | % | 6.90 | % | 11,863,328 | 71.95 | % | ||||||||||||||||||||||||||||||||

| Bank owned life insurance |

247,474 | 2.68 | % | 264,854 | 2.54 | % | 268,362 | 2.52 | % | 274,908 | 2.62 | % | 283,094 | 2.57 | % | 3.42 | % | 465,922 | 2.83 | % | ||||||||||||||||||||||||||||||||

| FHLB stock |

23,141 | 0.25 | % | 58,114 | 0.56 | % | 81,022 | 0.76 | % | 60,387 | 0.58 | % | 64,604 | 0.59 | % | 29.26 | % | 111,172 | 0.67 | % | ||||||||||||||||||||||||||||||||

| Goodwill and intangible assets |

90,538 | 0.98 | % | 124,222 | 1.19 | % | 121,870 | 1.14 | % | 119,679 | 1.14 | % | 117,661 | 1.07 | % | 6.77 | % | 190,926 | 1.16 | % | ||||||||||||||||||||||||||||||||

| Deposits |

7,570,216 | 82.07 | % | 8,001,159 | 76.87 | % | 7,846,556 | 73.71 | % | 8,096,149 | 77.29 | % | 8,444,079 | 76.63 | % | 2.77 | % | 12,458,526 | 75.56 | % | ||||||||||||||||||||||||||||||||

| Borrowings |

377,309 | 4.09 | % | 1,127,047 | 10.83 | % | 1,528,695 | 14.36 | % | 1,080,600 | 10.32 | % | 1,183,472 | 10.74 | % | 33.08 | % | 2,145,504 | 13.01 | % | ||||||||||||||||||||||||||||||||

| Equity |

1,079,081 | 11.70 | % | 1,053,595 | 10.12 | % | 1,040,335 | 9.77 | % | 1,080,376 | 10.31 | % | 1,160,728 | 10.53 | % | 1.84 | % | 1,567,325 | 9.51 | % | ||||||||||||||||||||||||||||||||

| Tangible equity |

988,543 | 10.72 | % | 929,373 | 8.93 | % | 918,465 | 8.63 | % | 960,697 | 9.17 | % | 1,043,067 | 9.47 | % | 1.35 | % | 1,376,399 | 8.35 | % | ||||||||||||||||||||||||||||||||

| Loans/Deposits |

83.19 | % | 95.30 | % | 99.65 | % | 97.05 | % | 97.40 | % | 95.22 | % | ||||||||||||||||||||||||||||||||||||||||

| Full Service Banking Offices Open |

62 | 66 | 65 | 68 | 71 | 108 | ||||||||||||||||||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of ending assets. |

| (2) | Includes fair value accounting adjustments for the acquisition of Northfield Bancorp. |

Sources: Columbia Financial’s prospectus, Columbia Financial’s and Northfield Bancorp’s audited & unaudited financial statements, Columbia Bank’s and Northfield Bank’s FDIC Call Reports and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.9 |

The Company’s higher loan growth rate compared to its asset growth rate provided for an increase in the loans-to-assets ratio from 68.28% at yearend 2021 to 74.64% at yearend 2025.

Trends in the Company’s loan portfolio composition during 2025 show that the concentration of 1-4 family mortgage loans decreased, equaling 34.4% and 31.0% of total loans at year ends 2024 and 2025, respectively. The decrease in the concentration of 1-4 family loans during 2025 was offset by increases in the concentrations of multi-family loans (18.6% to 20.4%), commercial real estate loans (29.7% to 30.5%) and commercial business loans (7.9% to 9.3%). The remaining loan composition trends for 2025 showed that the concentration of construction loans decreased from 6.0% of total loans to 5.7% of total loans and consumer loans decreased from 3.3% of total loans to 3.1% of total loans.

The intent of the Company’s investment policy is to provide adequate liquidity and to generate a favorable return within the context of supporting Columbia Financial’s overall credit and interest rate risk objectives. It is anticipated that proceeds retained at the holding company level, net of the proceeds used to fund the acquisition of Northfield Bancorp, will primarily be invested into short-term liquid funds held as a deposit at the Bank. Over the past five years, the Company’s level of cash and investment securities (inclusive of FHLB stock) ranged from a low of 16.94% of assets at yearend 2024 to a high of 24.18% of assets at yearend 2021 and equaled 17.52% of assets at yearend 2025. As previously noted, the Company sold $352.3 million of investment securities during the fourth quarter of 2024 to facilitate net interest margin expansion and improve future earnings. Mortgage-backed securities and collateralized mortgage obligations totaling $1.0 billion comprised the most significant component of the Company’s investment portfolio at December 31, 2025. Other investments held by the Company at December 31, 2025 consisted of U.S. government and agency obligations ($443.3 million), corporate debt securities ($66.6 million), equity securities ($6.8 million) and municipal bonds ($2.0 million). As of December 31, 2025, investments designated as held to maturity totaled $396.2 million and investments designated as available for sale totaled 1.122 billion. Investments maintained as available-at December 31, 2025 had a net unrealized loss of $78.2 million. Exhibit I-4 provides historical detail of the Company’s investment portfolio. As of December 31, 2025, the Company also held $340.8 million of cash and cash equivalents and $64.6 million of FHLB stock.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.10 |

The Company also maintains an investment in bank-owned life insurance (“BOLI”) policies, which covers the lives of certain key employees and non-employee directors of the Company. The life insurance policies earn tax-exempt income through cash value accumulation and death proceeds. As of December 31, 2025, the cash surrender value of the Company’s BOLI equaled $283.1 million or 2.57% of assets.

Over the past five fiscal years, Columbia Financial’s funding needs have been addressed through a combination of deposits, borrowings, and internal cash flows. From December 31, 2021 through December 31, 2025, the Company’s deposits increased at a 2.77% annual rate with three of the past four years showing an increase in deposits. Overall, deposits increased from $7.570 billion or 82.07% of assets at December 31, 2021 to $8.444 billion or 76.63% of assets at December 31, 2025. Deposit composition trends from yearend 2023 through yearend 2025 reflect that deposit growth was primarily driven by growth of certificates of deposit (“CDs”), which provided for a decrease in the concentration of transaction and savings accounts comprising total deposits. Transaction and savings account deposits comprised 68.31% of total deposits at December 31, 2023 and 66.22% of total deposits at December 31, 2025.

Borrowings serve as an alternative funding source for the Company to address funding needs for growth and to support management of funding costs and interest rate risk. From December 31, 2021 through December 31, 2025, borrowings increased at an annual rate of 33.08%. Overall, borrowings increased from $377.3 million or 4.09% of assets at December 31, 2021 to $1.183 billion or 10.74% of assets at December 31, 2025. Borrowings currently held by the Company consist substantially of FHLB advances and include a small balance of junior subordinated debt that was acquired in the Stewardship Financial merger.

The Company’s equity increased at a 1.84% annual rate from yearend 2021 through yearend 2025, which was largely attributable to retention of earnings being somewhat offset by an increase in treasury stock and an increase in the adjustment for accumulated other comprehensive loss. Stronger asset growth relative to equity growth provided for a decline in the Company’s equity-to-assets ratio from 11.70% at December 31, 2021 to 10.53% at December 31, 2025. Similarly, the Company’s tangible equity-to-assets ratio declined from 10.72% at December 31, 2021 to 9.47% at December 31, 2025. Goodwill and other intangibles totaled $117.7 million or 1.07% of assets at December 31, 2025, consisting of $110.7 million of goodwill and $6.9 million of core deposit intangibles. The Bank maintained capital surpluses relative to all of its regulatory capital requirements at December 31, 2025. The addition of stock proceeds will serve to strengthen the Company’s capital position, as well as support growth opportunities. At the same time, the significant increase in Columbia Financial’s pro forma capital position will initially depress its ROE.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.11 |

Pro Forma Balance Sheet Impact of Northfield Bancorp Acquisition

The pro forma balance sheet impact of the Northfield Bancorp acquisition is shown in Table 1.1 as of December 31, 2025. On the asset side of the balance sheet, the ratio of loans-to-assets will decrease and the level of cash and investments comprising total assets will increase before factoring in the infusion of the net conversion proceeds. The increase in the pro forma level of cash and investments includes the impact of funding the cash consideration and related acquisition costs, which have been estimated to total $221.4 million in the pro forma adjustments. Intangible assets increased from $117.7 million or 1.07% of assets to $190.9 million or 1.16% of assets on a pro forma combined basis. Pro forma intangible assets consisted of $110.7 million of goodwill and $80.2 million of core deposit intangibles. On the liability side of the balance sheet, deposits decrease from 76.63% of assets to 75.56% of assets on a pro forma combined basis, while borrowings increase from 10.74% of assets to 13.01% of assets on a pro forma combined basis. Before factoring in the impact of the second-step stock offering proceeds, the Company’s equity-to-asset ratio decreases from 10.53% to 9.51% on a pro forma combined basis and the tangible equity-to-assets ratio decreases from 9.47 to 8.35% on a pro forma combined basis.

Income and Expense Trends

Table 1.2 shows the Company’s historical income statements for the past five years, as well as on a pro forma income basis for the twelve months ended December 31, 2025 giving effect to the acquisition of Northfield Bancorp. The following discussion describes the historical income statements of Columbia Financial on a pre-acquisition basis. The pro forma income statement impact of the acquisition of Northfield Bancorp is discussed at the end of this section.

Over the past five years, the Company’s reported earnings ranged from a net loss of $11.7 million or 0.11% of average assets in 2024 to net income of $92.0 million or 1.01% of average assets in 2021. For 2025, the Company reported net income of $51.8 million or 0.48% of average assets. Net interest income and operating expenses represent the primary components of the Company’s earnings. Non-interest operating income has been a stable and somewhat limited source of earnings for the Company. Credit loss provisions have fluctuated over the past five years but generally have not had a significant impact on earnings. Non-operating income and losses had a more significant impact on the Company’s earnings in 2023 and 2024, which stemmed from losses recorded on investment securities transactions.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS Page I.12 |

Table 1.2

Columbia Financial, Inc.

Historical Income Statements

| Pro Forma Combined | ||||||||||||||||||||||||||||||||||||||||||||||||

| For the Year Ended December 31, | For the 12 months Ended 12/31/25(5) |

|||||||||||||||||||||||||||||||||||||||||||||||

| 2021 | 2022 | 2023 | 2024 | 2025 | ||||||||||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | |||||||||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | |||||||||||||||||||||||||||||||||||||

| Interest income |

$ | 270,150 | 2.97 | % | $ | 309,670 | 3.18 | % | $ | 394,978 | 3.81 | % | $ | 451,426 | 4.24 | % | $ | 470,951 | 4.37 | % | $ | 755,580 | 4.69 | % | ||||||||||||||||||||||||

| Interest expense |

(37,016 | ) | -0.41 | % | (42,893 | ) | -0.44 | % | (189,102 | ) | -1.82 | % | (273,444 | ) | -2.57 | % | (249,317 | ) | -2.32 | % | ($ | 361,464 | ) | -2.24 | % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net interest income |

$ | 233,134 | 2.56 | % | $ | 266,777 | 2.74 | % | $ | 205,876 | 1.99 | % | $ | 177,982 | 1.67 | % | $ | 221,634 | 2.06 | % | $ | 394,116 | 2.45 | % | ||||||||||||||||||||||||

| Provision for credit losses |

9,953 | 0.11 | % | (5,485 | ) | -0.06 | % | (4,787 | ) | -0.05 | % | (14,451 | ) | -0.14 | % | (9,822 | ) | -0.09 | % | ($ | 17,224 | ) | -0.11 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net interest income after provisions |

$ | 243,087 | 2.67 | % | $ | 261,292 | 2.68 | % | $ | 201,089 | 1.94 | % | $ | 163,531 | 1.53 | % | $ | 211,812 | 1.97 | % | $ | 376,892 | 2.34 | % | ||||||||||||||||||||||||

| Non-interest operating income |

$ | 38,598 | 0.42 | % | $ | 30,591 | 0.31 | % | $ | 37,531 | 0.36 | % | $ | 35,151 | 0.33 | % | $ | 35,906 | 0.33 | % | $ | 50,220 | 0.31 | % | ||||||||||||||||||||||||

| Non-interest operating expense |

(154,915 | ) | -1.70 | % | (172,006 | ) | -1.77 | % | (181,811 | ) | -1.75 | % | (179,670 | ) | -1.69 | % | (180,678 | ) | -1.68 | % | (281,676 | ) | -1.75 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net operating income |

$ | 126,770 | 1.39 | % | $ | 119,877 | 1.23 | % | $ | 56,809 | 0.55 | % | $ | 19,012 | 0.18 | % | $ | 67,040 | 0.62 | % | $ | 145,436 | 0.90 | % | ||||||||||||||||||||||||

| Non-Operating Income(Loss) |

||||||||||||||||||||||||||||||||||||||||||||||||

| Gain (loss) on securities |

$ | 2,025 | 0.02 | % | $ | 210 | 0.00 | % | ($ | 10,847 | ) | -0.10 | % | ($ | 35,851 | ) | -0.34 | % | $ | 290 | 0.00 | % | $ | 290 | 0.00 | % | ||||||||||||||||||||||

| Change in fair value of equity securities |

(1,792 | ) | -0.02 | % | (401 | ) | 0.00 | % | 695 | 0.01 | % | 2,594 | 0.02 | % | 873 | 0.01 | % | 2,567 | 0.02 | % | ||||||||||||||||||||||||||||

| Merger related expenses/Goodwill impairment |

(822 | ) | -0.01 | % | (2,810 | ) | -0.03 | % | (606 | ) | -0.01 | % | (1,665 | ) | -0.02 | % | (214 | ) | 0.00 | % | (41,226 | ) | -0.26 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net non-operating income |

(589 | ) | -0.01 | % | ($ | 3,001 | ) | -0.03 | % | ( | $10,758 | ) | -0.10 | % | ($ | 34,922 | ) | -0.33 | % | $ | 949 | 0.01 | % | ($ | 38,369 | ) | -0.24 | % | ||||||||||||||||||||

| Net income before tax |

$ | 126,181 | 1.39 | % | $ | 116,876 | 1.20 | % | $ | 46,051 | 0.44 | % | ($ | 15,910 | ) | -0.15 | % | $ | 67,989 | 0.63 | % | $ | 107,067 | 0.66 | % | |||||||||||||||||||||||

| Income tax provision |

(34,132 | ) | -0.37 | % | (30,703 | ) | -0.32 | % | (9,965 | ) | -0.10 | % | 4,257 | 0.04 | % | (16,223 | ) | -0.15 | % | ($ | 38,530 | ) | -0.24 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net income (loss) |

$ | 92,049 | 1.01 | % | $ | 86,173 | 0.88 | % | $ | 36,086 | 0.35 | % | ($ | 11,653 | ) | -0.11 | % | $ | 51,766 | 0.48 | % | $ | 68,537 | 0.43 | % | |||||||||||||||||||||||

| Adjusted Earnings |

||||||||||||||||||||||||||||||||||||||||||||||||

| Net income |

$ | 92,049 | 1.01 | % | $ | 86,173 | 0.88 | % | $ | 36,086 | 0.35 | % | ($ | 11,653 | ) | -0.11 | % | $ | 51,766 | 0.48 | % | $ | 68,537 | 0.43 | % | |||||||||||||||||||||||

| Add(Deduct): Net non-operating income |

589 | 0.01 | % | 3,001 | 0.03 | % | 10,758 | 0.10 | % | 34,922 | 0.33 | % | (949 | ) | -0.01 | % | 38,369 | 0.24 | % | |||||||||||||||||||||||||||||

| Tax effect (2) |

(159 | ) | 0.00 | % | (810 | ) | -0.01 | % | (2,905 | ) | -0.03 | % | (9,429 | ) | -0.09 | % | 256 | 0.00 | % | (10,360 | ) | -0.06 | % | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Adjusted earnings |

$ | 92,479 | 1.02 | % | $ | 88,364 | 0.91 | % | $ | 43,939 | 0.42 | % | $ | 13,840 | 0.13 | % | $ | 51,073 | 0.47 | % | $ | 96,546 | 0.60 | % | ||||||||||||||||||||||||

| Expense Coverage Ratio (3) |

1.50x | 1.55x | 1.13x | 0.99x | 1.23x | 1.40x | ||||||||||||||||||||||||||||||||||||||||||

| Efficiency Ratio (4) |

57.05 | % | 57.84 | % | 74.69 | % | 84.50 | % | 70.29 | % | 63.41 | % | ||||||||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of average assets. |

| (2) | Assumes a 27.0% effective tax rate. |

| (3) | Expense coverage ratio calculated as net interest income before provisions for loan losses divided by operating expenses. |

| (4) | Efficiency ratio calculated as operating expenses divided by the sum of net interest income before provisions for loan losses plus non-interest operating income. |

| (5) | Reflects pro forma impact of Northfield Bancorp acquisition. |

| Sources: | Columbia Financial’s prospectus, Columbia Financial’s and Northfield Bancorp’s audited & unaudited financial statements, Columbia Bank’s and Northfield Bank’s FDIC Call Reports and RP Financial caluclations. |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.13 |

From 2021 through 2025, the Company’s net interest income to average assets ratio ranged from a low of 1.67% during 2024 to a high of 2.74% during 2022. For 2025, the net interest income to average assets ratio increased to 2.06%. The decrease in the net interest income ratio during 2023 and 2024 was due to a more significant increase in the interest expense ratio relative to the interest income ratio, which was attributable to interest rate spread compression resulting from a more significant increase in funding costs relative to the increase in the yield earned on interest-earning assets. Comparatively, a higher interest income ratio and a lower interest expense ratio facilitated the increase in the net interest income ratio for 2025, as a higher yield on interest-earning assets and a lower cost of interest-bearing liabilities contributed to an increase in the Company’s interest rate spread during 2025. The Company’s historical net interest rate spreads and yields and costs are set forth in Exhibits I-3 and I-5.

Non-interest operating income has been a limited contributor to the Company’s earnings over the past five years. Throughout the period shown in Table 1.2, non-interest operating income ranged from a low of $30.6 million or 0.31% of average assets during 2022 to a high of $38.6 million or 0.42% of average assets during 2021. For 2025, non-interest operating income amounted to $35.9 million or 0.33% of average assets. Demand deposit account fees, BOLI income, loan fees and service charges and title insurance fees are the primary contributors to the Company’s non-interest operating income.

Operating expenses represent the other major component of the Company’s earnings, which have been maintained at less than 2.00% of average assets over the past five years. Operating expenses totaled $180.7 million or 1.68% of average assets for 2025, versus total operating expenses of $154.9 million or 1.70% of average assets for 2021. The Company’s relatively low operating expense ratio is in part facilitated by maintaining a high ratio of assets per employee, which is supported by the relatively low staffing requirements associated with (1) the Company’s lending strategy that has emphasized growth of higher balance commercial real estate loans and multi-family loans and (2) limited diversification into other products and services that would provide additional sources of non-interest operating income and have a limited impact on increasing assets. As of December 31, 2025, the Company’s ratio of assets per full time equivalent employee equaled $14.310 million.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.14 |

Overall, during the past five years, the Company’s expense coverage ratios (net interest income divided by operating expenses) ranged from a low of 0.99x during 2024 to a high of 1.55x during fiscal year 2022 and equaled 1.23x during 2025. Comparatively, the Company’s efficiency ratio (operating expenses as a percent of the sum of net interest income and other operating income) ranged from a high of 84.50% during 2024 to a low of 57.05% during 2021 and equaled 70.29% during 2025.

During the period covered in Table 1.2, the amount of credit loss provisions established ranged from a recovery of $10.0 million or 0.11% of average assets during 2021 to loss provisions of $14.5 million or 0.14% of average assets during 2024. For 2025, the Company reported credit loss provisions of $9.8 million or 0.09% of average assets. The reduction in credit loss provisions established in 2025 was primarily attributable to a decrease in net charge-offs, which decreased from $9.6 million during 2024 to $5.8 million during 2025. As of December 31, 2025 the Company maintained credit loss allowances of $67.2 million, equal to 0.82% of total loans and 176.84% of non-accruing loans. Exhibit I-6 sets forth the Company’s allowance for credit losses activity for the past three years.

Non-operating income and losses were a more significant factor in the Company’s earnings during 2023 and 2024, as the result of loss on investments securities transactions to facilitate repositioning of the balance sheet. Net non-operating income and losses over the past five years ranged from a net non-operating loss of $34.9 million or 0.33% of average assets during 2024, which included a $35.9 million loss on investment securities, to net non-operating income of $949,000 or 0.01% of average assets during 2025. Overall, the various items that comprise the Company’s non-operating income/expense are not viewed to be part of the Company’s core or recurring earnings base.

The Company’s effective tax rate ranged from a benefit of 26.76% during 2024 to an expense of 27.05% during 2021 and equaled an expense of 23.86% during 2025. As set forth in the prospectus, the Company’s marginal effective tax rate is 27.0%.

Pro Forma Earnings Impact of Northfield Bancorp Acquisition

The pro forma income statement impact of the Northfield Bancorp acquisition is shown in Table 1.2 for the twelve-month period ended December 31, 2025. Pro forma net interest income reflects the yield adjustments for interest rate sensitive assets and liabilities, based on fair value adjustments on Northfield Bancorp’s balance sheet as of December 31, 2025. Non-interest

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.15 |

expense was adjusted to account for the amortization of core deposit intangibles. On a pro forma basis, before factoring in the reinvestment of conversion proceeds, Columbia Financial’s earnings increase from $51.8 million or 0.48% of average assets to $68.5 million or 0.43% of average assets. The increase in the Company’s pro forma return on average assets reflects higher net interest income (increasing from 2.06% of average assets to 2.45% of average assets), which is partially offset by higher operating expenses (increasing from 1.68% of average assets to 1.75% of average assets). Approximately $35.1 million of the increase in net interest income was attributable to the net earnings impact of Northfield Bancorp’s fair value accounting adjustments. As a percent of pro forma assets, pro forma non-interest operating income decreased slightly (0.33% to 0.31%), pro forma credit loss provisions increased slightly (0.09% to 0.11%) and pro forma non-operating income/losses decreased (0.01% non-operating income to 0.24% non-operating loss). The pro forma non-operating loss was substantially related to the goodwill impairment charge of $41.0 million that was recorded by Northfield Bancorp. The pro forma earnings do not reflect any potential cost savings in merger synergies that may be realized, as such estimates are considered to be speculative and therefore are not disclosed in the pro forma financial statements set forth in the prospectus.

Interest Rate Risk Management

The Company pursues a number of strategies to manage interest rate risk, particularly with respect to seeking to limit the repricing mismatch between interest rate sensitive assets and liabilities. The Company manages interest rate risk from the asset side of the balance sheet through investing in investment securities with short-terms or adjustable interest rates, maintaining most of the investment portfolio as available for sale, selling originations of longer term 1-4 family fixed rate loans and diversifying into other types of lending beyond 1-4 family permanent mortgage loans which consist primarily of adjustable rate or shorter term fixed rate loans. The Company also hedges a portion of its fixed rate commercial business loan portfolio with interest rate swap contracts. As of December 31, 2025, of the Company’s total loans due after December 31, 2026, adjustable rate loans comprised 38.94% of total loans receivable (see Exhibit I-7). On the liability side of the balance sheet, management of interest rate risk has been pursued through emphasizing growth of lower costing and less interest rate sensitive transaction and savings account deposits and utilizing fixed rate FHLB advances with laddered maturities extending out to more than four years. Transaction and savings account deposits comprised 66.22% of the Company’s total deposits at December 31, 2025. In addition, the Company executes interest rate swaps with third parties in order to hedge the interest rate risk of short-term FHLB advances.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.16 |

As of December 31, 2025, an analysis of the Company’s net portfolio value (“NPV”) and net interest income indicated that in the event of an instantaneous parallel 200 basis point increase in market interest rates NPV would decrease by 13.85% and net interest income would decrease by 9.06% in year one, which were within policy guidelines (see Exhibit I-8).

The infusion of stock proceeds will serve to further limit the Company’s interest rate risk exposure, as most of the net proceeds will be redeployed into interest-earning assets, including shorter-to-intermediate term investments and adjustable rate loans, and the increase in the Company’s capital position will lessen the proportion of interest rate sensitive liabilities funding assets.

Lending Activities and Strategy

Columbia Financial’s lending activities have emphasized mortgage-based lending, which has provided for a loan portfolio composition that is concentrated in commercial real estate and muti-family loans, followed by 1-4 family residential loans. Other areas of lending for the Company include commercial business loans, construction loans and home equity loans and advances. Going forward, the Company’s lending strategy will continue to emphasize commercial real estate and multi-family lending, as well as pursuing lending diversification that will emphasize growth of commercial business loans. Comparatively, Northfield Bancorp’s loan portfolio is more concentrated in commercial real estate/multi-family loans, with the balance of the loan portfolio consisting of home equity loans and lines of credit, 1-4 family mortgage loans, commercial business loans, construction and land loans and other consumer loans. Exhibit I-9 and Exhibit I-9A provide historical detail of Columbia Financial’s and Northfield Bancorp’s loan portfolio compositions, respectively. Exhibit I-10 provides the contractual maturity of the Company’s loan portfolio by loan type as of December 31, 2025.

Commercial Real Estate and Multi-Family Loans. Commercial real estate and multi-family loans consist largely of loans originated by the Company, which are generally collateralized by properties in the Company’s regional lending area. On a limited basis, the Company supplements originations of commercial real estate and multi-family loans with purchased loan participations from local banks. Loan participations are subject to the same underwriting criteria and loan approvals as applied to loans originated by the Company.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.17 |

Columbia Financial generally originates commercial real estate loans up to a loan-to-value (“LTV”) ratio of 75% and multi-family loans up to a LTV ratio of 80%. Commercial real estate and multi-family loans generally require a minimum debt-coverage ratio of 1.2 times. Commercial real estate and multi-family loans are generally originated for terms of up to ten years and with amortization schedules of up to 25 years for commercial properties and up to 30 years for multi-family and industrial commercial real estate properties. Loan terms offered on commercial real estate and multi-family loans include fixed rate and adjustable rate loans. Adjustable rate loans are typically fixed from three to ten years. Properties securing the commercial real estate and multi-family loan portfolio include non-medical office buildings, industrial/warehouse facilities, retail shopping centers, medical office buildings, hotels, assisted-living facilities and apartment buildings. At December 31, 2025, the Company’s largest commercial real estate loan was a $30.6 million participation loan and was secured by a retail shopping center. At December 31, 2025, this loan was performing in accordance with its original terms. At December 31, 2025, the Company’s largest multi-family loan had an outstanding balance of $48.7 million and was secured by three garden style apartment buildings. At December 31, 2025, this loan was performing in accordance with its original terms. As of December 31, 2025, the Company’s outstanding balance of commercial real estate and multi-family loans totaled $4.2 billion, equal to 51.39% of total loans outstanding, and consisted of $2.5 billion of commercial real estate loans and $1.7 billion of multi-family loans. As of December 31, 2025, Northfield Bancorp’s outstanding balance of commercial real estate and multi-family loans totaled $3.3 billion, equal to 84.86% of total loans outstanding, and consisted of $911.4 million of commercial real estate loans and $2.4 billion of multi-family loans.

1-4 Family Residential Loans. Columbia Financial offers both fixed rate and adjustable rate 1-4 family permanent mortgage loans with terms of up to 30 years. Loans are generally underwritten to secondary market guidelines, so as to allow for the sale of such loans if such a strategy is warranted for purposes of interest rate risk management. Adjustable rate loans offered by the Company have initial repricing terms of up to seven years and then reprice annually for the balance of the loan term. Adjustable rate loans are indexed to the U.S. Treasury security index. As of December 31, 2025, the Company’s outstanding balance of 1-4 family loans totaled $2.6 billion equal to 31.03% of total loans outstanding. As of December 31, 2025, Northfield Bancorp’s outstanding balance of 1-4 family loans totaled $165.1 million equal to 4.28% of total loans outstanding.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.18 |

Home Equity Loans and Advances. The Company’s 1-4 family lending activities include home equity loans and advances. Home equity loans are offered as fixed rate loans with terms of up to 20 years. Home equity advances have adjustable rates and are indexed to the prime rate as published in The Wall Street Journal. Home equity advances can have repayment schedules of both principal and interest or interest only paid monthly The Company will generally originate home equity loans and advances up to a combined maximum LTV ratio of 80%. As of December 31, 2025, the Company’s outstanding balance of home equity loans and advances totaled $255.1 million equal to 3.09% of total loans outstanding. As of December 31, 2025, Northfield Bancorp’s outstanding balance of home equity loans and lines of credit totaled $198.6 million equal to 5.15% of total loans outstanding.