Exhibit 99.1

|

Annual Report 2025

March 5, 2026

Exhibit 99.1

|

Annual Report 2025

March 5, 2026

Page 1 |

Thomson Reuters Annual Report 2025 |

Information in this annual report is provided as of March 4, 2026 unless otherwise indicated.

Certain statements in this annual report are forward-looking. These forward-looking statements are based on certain assumptions and reflect our current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Some of the factors that could cause actual results to differ materially from current expectations are discussed in the “Risk Factors” section of this annual report as well as in materials that we from time to time file with, or furnish to, the Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission. There is no assurance that any forward-looking statements will materialize. You are cautioned not to place undue reliance on forward-looking statements, which reflect expectations only as of the date of this annual report. Except as may be required by applicable law, we disclaim any intention or obligation to update or revise any forward-looking statements.

The following terms in this annual report have the following meanings, unless otherwise indicated:

Term |

|

Definition |

AI |

|

Artificial intelligence |

“Big 3” segments |

|

Our combined Legal Professionals, Corporates and Tax, Audit & Accounting Professionals segments |

bp |

|

Basis points – one basis point is equal to 1/100th of 1%,“100bp” is equivalent to 1% |

C$ |

|

Canadian dollars |

constant currency |

|

A non-IFRS measure derived by applying the same foreign currency exchange rates to the financial results of the current and equivalent prior-year period |

EBITDA |

|

Earnings before interest, tax, depreciation and amortization |

EPS |

|

Earnings per share |

IASB |

|

International Accounting Standards Board |

IFRS |

|

International Financial Reporting Standards |

LSEG |

|

London Stock Exchange Group plc |

ML |

|

Machine learning |

n/a |

|

Not applicable |

n/m |

|

Not meaningful |

Nasdaq |

|

The Nasdaq Stock Market LLC |

organic or organically |

|

A non-IFRS measure that represents changes in revenues of our existing businesses at constant currency. The metric excludes the distortive impacts of acquisitions and dispositions from not owning the business in both comparable periods |

SEC |

|

U.S. Securities and Exchange Commission |

TSX |

|

Toronto Stock Exchange |

Woodbridge |

|

The Woodbridge Company Limited, our principal and controlling shareholder |

$ and US$ |

|

U.S. dollars |

Non-IFRS financial measures are defined and reconciled to the most directly comparable measure in the “Management’s Discussion and Analysis” section of this annual report. See Appendix A of the Management’s Discussion and Analysis for a description of our non-IFRS financial measures, including an explanation of why we believe they are useful measures of our performance. See Appendices B and C of the Management’s Discussion and Analysis for reconciliations of our non-IFRS financial measures to the most directly comparable IFRS measures. Non-IFRS measures do not have standardized meanings prescribed by IFRS and therefore are unlikely to be comparable to the calculation of similar measures used by other companies and should not be viewed as alternatives to measures of financial performance calculated in accordance with IFRS.

For information regarding our disclosure requirements under applicable Canadian and U.S. laws and regulations, please see the “Cross Reference Tables” section of this annual report.

Information contained on our website or any other websites identified in this annual report is not part of this annual report. All website addresses listed in this annual report are intended to be inactive, textual references only. The Thomson Reuters logo and our other trademarks, trade names and service names mentioned in this annual report are the property of Thomson Reuters.

Front cover photo credit: REUTERS/Karen Toro; Page 11 photo credit: REUTERS/Evelyn Hockstein; and Page 17 photo credit: REUTERS/Navesh Chitrakar

Thomson Reuters Annual Report 2025 |

|

|

2 |

|

|

2 |

|

|

5 |

|

|

5 |

|

|

6 |

|

|

7 |

|

|

8 |

|

|

8 |

|

Key Products |

|

9 |

|

11 |

|

|

11 |

|

|

11 |

|

|

11 |

|

|

12 |

|

|

12 |

|

|

13 |

|

|

13 |

|

|

13 |

|

|

14 |

|

|

15 |

|

|

18 |

|

|

19 |

|

|

33 |

|

|

96 |

|

|

160 |

|

|

160 |

|

|

163 |

|

|

166 |

|

|

167 |

|

|

168 |

|

|

168 |

|

|

169 |

|

Presiding Directors at Meetings of Non-Management and Independent Directors |

|

170 |

|

170 |

|

|

170 |

|

|

171 |

|

|

171 |

|

|

172 |

|

|

172 |

|

|

174 |

|

|

174 |

|

|

175 |

|

|

178 |

|

Interests of Experts |

|

179 |

|

179 |

|

|

181 |

|

Annual Information Form (Form 51-102F2) Cross Reference Table |

|

181 |

|

182 |

Thomson Reuters Annual Report 2025 |

|

Business

Overview

Who We Are and What We Do

Thomson Reuters powers business-critical professions with AI they can trust in the moments that matter. We unite unparalleled expertise, proprietary content, and seamless workflows to help our customers move with speed, think with clarity, and lead with confidence. Across our products, we combine highly specialized software and insights to empower professionals with the data, intelligence and solutions needed to make informed decisions, and to help institutions in their pursuit of justice, truth and transparency. Reuters, part of Thomson Reuters, is a world leading provider of trusted journalism and news. Thomson Reuters shares are listed on the Toronto Stock Exchange and the Nasdaq (symbol: TRI). Our website is thomsonreuters.com.

We are organized as five reportable segments, reflecting how our products and services are managed and offered to target customers.

|

Legal Professionals Serves law firms and governments with research and workflow products powered by AI-enabled technology, focusing on intuitive legal research and integrated legal workflow solutions that combine content, tools and analytics. |

|

|

|

Corporates Serves corporations, ranging from small businesses to multinational organizations, including the seven largest global accounting firms, with our full suite of content-driven products, powered by AI-enabled technology and integrated compliance workflow solutions to help them achieve their business outcomes. |

|

|

|

Tax, Audit & Accounting Professionals Serves tax, audit and accounting firms (other than the seven largest, which are served by our Corporates segment) with research and workflow products powered by AI-enabled technology. |

|

|

|

Reuters Supplies business, financial and global news and data to the world’s media organizations, professionals and news consumers through Reuters News Agency, Reuters.com, Reuters Events, Thomson Reuters products and to financial firms exclusively via LSEG products. |

|

|

|

Global Print Provides legal and tax information primarily in print format to customers around the world and provides commercial printing services to a wide range of book publishers. |

Our businesses are supported by a corporate center that manages our commercial and technology operations, including those around our sales capabilities, digital customer experience, and product and content development, as well as our global facilities. Costs relating to these activities are allocated to our business segments. We also report “Corporate costs”, which includes expenses for certain centrally managed functions such as finance, legal, human resources and the executive office. These costs are not allocated to the segments and are included in consolidated adjusted EBITDA.

Page 2 |

Thomson Reuters Annual Report 2025 |

Our Business Model and Key Operating Characteristics

We derive a significant portion of our revenues from selling information and software solutions, mostly on a recurring subscription basis. Our professional-grade solutions are built on comprehensive proprietary content and deep domain expertise with software, embedded AI capabilities and automation tools. We believe our workflow solutions make our customers more productive by streamlining how they operate, enabling them to focus on higher value activities. Many of our customers use our solutions deeply integrated into their workflows, which has led to strong customer retention. We believe that our customers trust us because of our decades serving high-stakes workflows, where accuracy and reliability are non-negotiable, our enterprise-grade security and governance built for regulated environments, and our deep understanding of their businesses and industries. They rely on our services for navigating a rapidly changing and increasingly complex digital and global landscape. Over the years, our business model has proven to be capital efficient and cash flow generative, and it has enabled us to maintain leading and scalable positions in our chosen market segments.

Some of our key business and operating characteristics are:

Attractive Industry |

Balanced and Diversified Leadership |

Attractive Business Model |

Strong Competitive Positioning |

Disciplined Financial Policies |

• Currently our “Big 3” segments operate in an estimated $31 billion market expected to grow between 8% and 11% over the next 5 years • Legal, Tax & Risk markets are prime for content-driven innovation |

• A leader in our "Big 3" and Reuters segments • Resilient businesses, historically stable, through periods of macroeconomic uncertainty • Approximately 450,000 customers; largest customer is approximately 5% of revenues* |

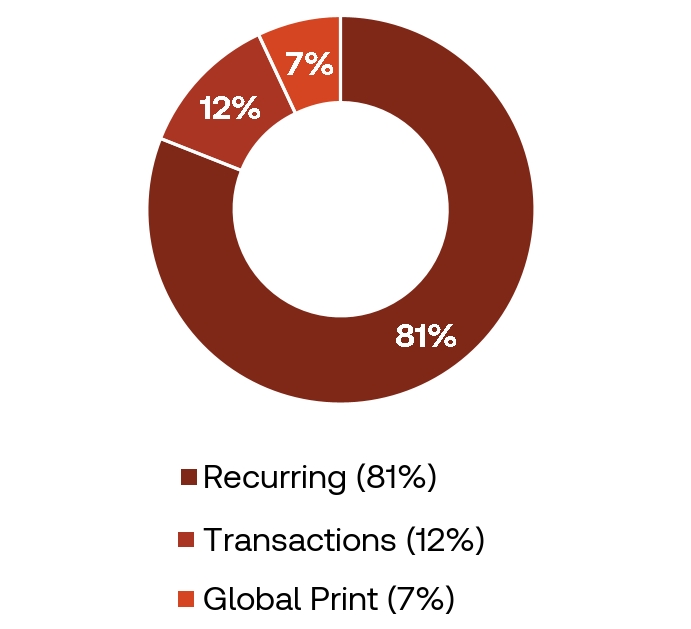

• 81% of revenues were recurring in 2025 • Fixed cost model supports operating leverage as we grow • Strong and consistent cash generation capabilities

|

• Proprietary content plus data and human expertise combined with AI and ML are key differentiators • Products deeply embedded in customers’ daily workflows • 92% retention rate in 2025

|

• Focused and incentivized on organic revenue growth and free cash flow growth • Balance investing in business and returning capital to shareholders • Committed to maintaining investment grade rating with stable capital structure • Significant potential capital capacity affords optionality

|

* The news agreement with the Data & Analytics business of LSEG.

Thomson Reuters Annual Report 2025 |

Page 3 |

Our Strategy and Key Priorities

We strive to be the leading content-driven technology company that empowers professionals to navigate complex legal, tax, audit, accounting, compliance, government, corporate and media environments. We do this through professional-grade solutions specifically designed for high-stakes work, leveraging the depth and breadth of our proprietary content, which is meticulously curated and continually enhanced by thousands of subject matter experts and legal editors.

Because our data and insights are built on this uniquely curated intellectual capital, our content reflects a high level of quality and expertise that supports our customers’ professional needs, underpinned by enterprise-grade security and governance. This strong foundation enables us to be positioned to combine next-generation AI technologies with our existing strengths to serve customers in new and differentiated ways centered on four core pillars that guide our strategies:

The rapid pace of AI innovation continues to drive significant transformation across the industries we serve, reinforcing the importance of our strategy and our priorities for 2026:

Page 4 |

Thomson Reuters Annual Report 2025 |

Three-Year History

Customer Segments

Our business is a customer-focused structure organized in five reportable customer segments: Legal Professionals, Corporates, Tax, Audit & Accounting Professionals, Reuters and Global Print. This structure allows us to focus on the customer so we can partner with them to solve challenges that they face in their businesses. For additional information about the financial results of our customer segments, please see the “Management’s Discussion and Analysis” section of this annual report.

Legal Professionals

Our Legal Professionals segment delivers professional-grade, agentic AI-enabled solutions for customers across law firms, courts and government. Our next generation AI solution, CoCounsel Legal, with Deep Research grounded in Westlaw and Practical Law, is purpose-built to deliver rigorous, end-to-end legal research results and workflow automation.

Today, legal professionals are navigating a period of significant transformation. Regulation and compliance requirements continue to grow in complexity, increasing the operational burden on legal teams. At the same time, corporate legal departments are becoming more sophisticated and cost-conscious purchasers of legal services, prompting law firms to focus on delivering measurable value through improved processes and the latest technology. Meanwhile, new associates are demonstrating a strong appetite for solutions that enable them to work effectively and sustainably, and legal career pathways are set to evolve as AI adoption grows.

Against this backdrop, it is critical that the legal profession is equipped with AI solutions that deliver defensible results, safeguard confidential data, and operate inside professional and regulatory frameworks. Thomson Reuters is well positioned to meet this need through our unparalleled legal content: 1.9 billion documents in the Westlaw database from over 3,500 authoritative sources, enhanced by 1,500 attorney editors who create 1.6 million editorial updates per year.

We are also building our first vertical-specific legal Large Language Model (LLM) which will be trained on our content, data and expertise. This includes our legal-specific data with validation frameworks such as the West Key Number System, our proprietary taxonomy of the law, and KeyCite with 1.4 billion citation relationships, providing AI outputs that meet professional standards.

Thomson Reuters Annual Report 2025 |

Page 5 |

We will continue to scale our agentic AI capabilities, combining proprietary legal content, deep domain expertise, and professional-grade AI to help legal teams work with greater speed, precision, and confidence, supported by robust privacy commitments.

In addition to law firms, we also serve government customers, including federal, state, and local organizations, with solutions that support mission-critical workflows where security, reliability, and accuracy are essential. This includes helping courts run more efficiently and productively and helping government organizations undertake risk management and tackle fraud.

We also serve legal professionals across Europe, Asia-Pacific, Latin America, and the Middle East with solutions that combine global platform capabilities with jurisdiction-specific content, local expertise and AI-enabled workflows tailored to regional legal frameworks.

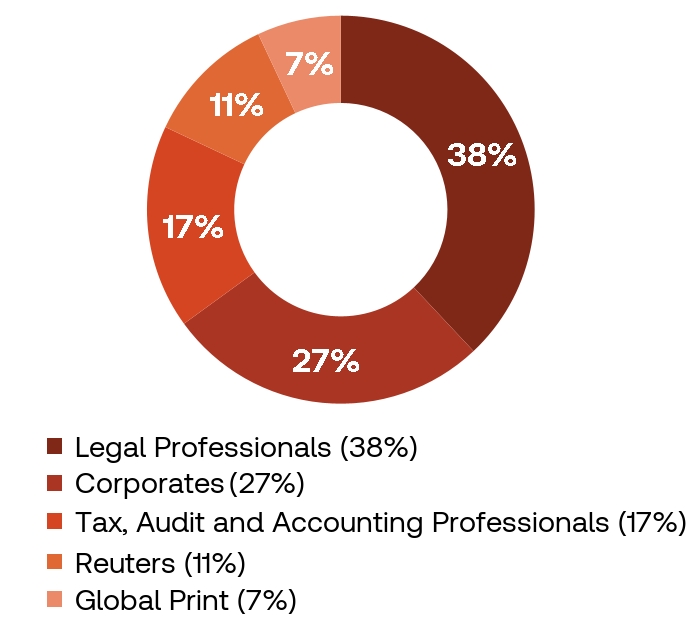

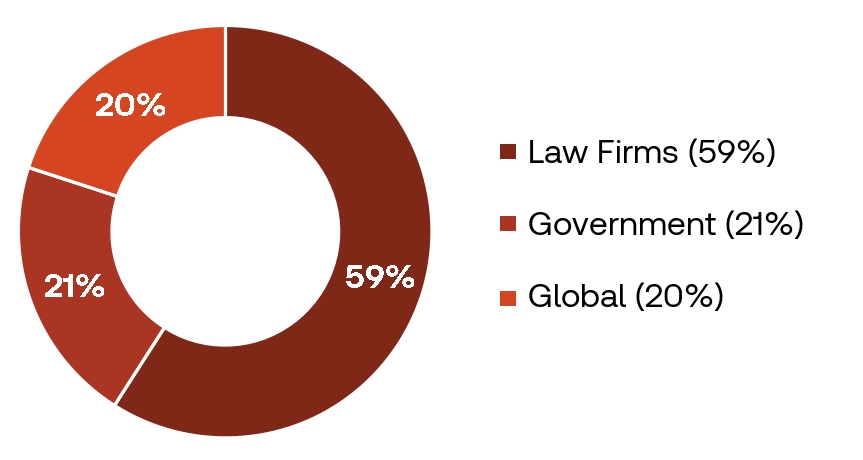

The following provides a summary of Legal Professionals’ 2025 revenues by type of customer.

Legal Professionals’ primary global competitors are LexisNexis (which is owned by RELX Group) and Wolters Kluwer. Legal Professionals also competes with other companies that provide legal and regulatory information, legal workflow and drafting software providers, and with AI-enabled software companies that support legal professionals.

Corporates

Our Corporates segment serves a range of customers, from small businesses to multinational organizations, including the seven largest global accounting firms, with our full suite of content-driven products, powered by leading-edge technologies, including AI, and integrated compliance workflow solutions to help them achieve their business outcomes.

Our Corporates customers operate in an environment of sustained regulatory change, evolving technology, expanding reporting obligations and heightened expectations for speed, productivity and precision. Evolving compliance requirements—such as Environmental, Social and Governance reporting, sanctions and tariffs, and enhanced "know your counterparty" practices, are increasing the volume and complexity of compliance and risk decisions. At the same time, compliance teams across tax, trade, legal and risk are being asked to do more with constrained resources, as tax departments face greater demands for efficiency and productivity and many general counsels navigate growing regulatory complexity. Digital mandates, including global minimum tax developments and the continued rollout of e-invoicing and other continuous transaction control regimes, are accelerating the shift toward cloud-based, data-driven compliance and workflow transformation.

We believe these dynamics create the opportunity for Thomson Reuters to serve as a trusted partner for Corporates customers by helping them navigate regulatory complexity, improve operational efficiency and manage risk with greater confidence. Our strategy is built around Thomson Reuters ONESOURCE+, which unifies tax, trade, legal and risk functions through an intelligent compliance network. We combine proprietary content and domain expertise with AI-driven workflow software and analytics, including CoCounsel AI and agentic technology, that are embedded in customers' day-to-day processes. Our approach focuses on embedding AI in workflows, connecting data across compliance functions and delivering intelligent automation to help customers drive efficiency, reduce risk and cost and unlock growth for businesses.

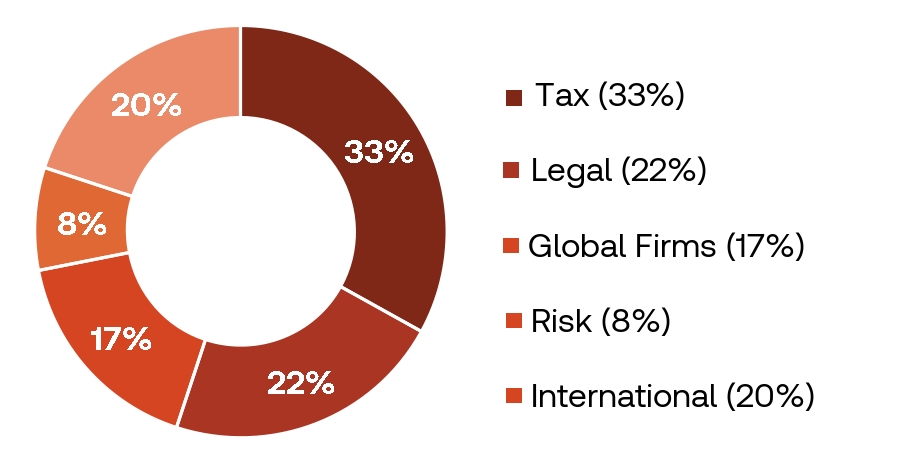

The following provides a summary of Corporates’ 2025 revenues by type of customer.

Page 6 |

Thomson Reuters Annual Report 2025 |

Corporates’ primary global competitors include LexisNexis, Wolters Kluwer and Bloomberg. Corporates also competes with focused software providers such as Avalara, Mitratech, Vertex and Sovos and at times with large technology companies, enterprise resource planning software solution companies, and highly focused and venture capital-backed startups. While the largest global accounting firms are significant customers of Thomson Reuters, they can also be competitors.

Tax, Audit & Accounting Professionals

Our Tax, Audit & Accounting Professionals segment serves tax, audit and accounting professionals with AI-powered research and workflow solutions. We introduced agentic AI into our core offerings, which use advanced reasoning models paired with an AI assistant that orchestrates complex work, backed by Checkpoint’s comprehensive proprietary content and deep domain expertise from our tax editors and subject matter experts. Our customers range from sole practitioners to the largest global firms providing tax compliance, audit, advisory and accounting services.

The profession faces an unprecedented talent shortage, which defines the strategic imperative for our business. The pipeline of qualified professionals has contracted sharply, with fewer graduates pursuing accounting certification even as demand intensifies. Simultaneously, regulatory complexity continues to increase as tax codes grow, cross-jurisdictional requirements expand and audit standards tighten. Meanwhile, client expectations have moved beyond compliance focused tasks to include higher-value advisory services. These converging pressures require firms to deliver more with constrained resources while maintaining high quality and accuracy. Our solutions address this imperative by streamlining the end-to-end process, from research and compliance to workflow automation and client advisory.

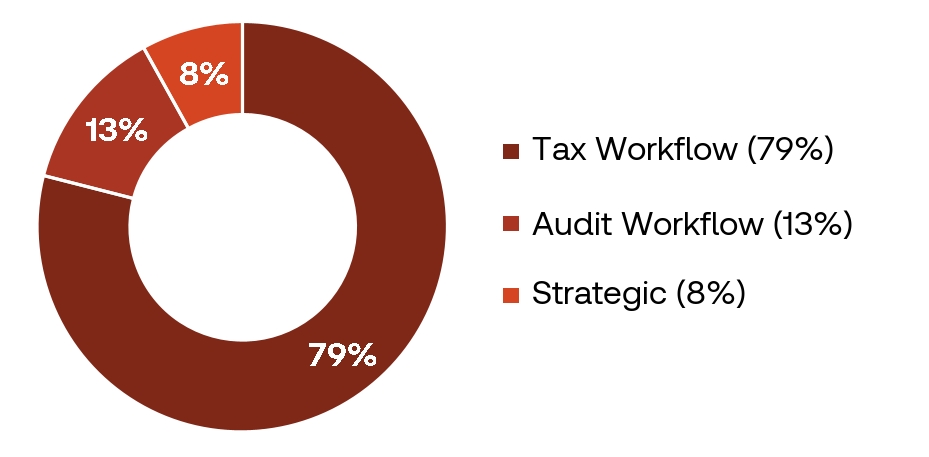

The following provides a summary of Tax, Audit & Accounting Professionals’ 2025 revenues by type of customer.

Strategic customers represent the largest firms across Tax and Audit workflows.

Tax Workflow

We provide end-to end workflows to streamline the entirety of the tax lifecycle, from client onboarding and data gathering through document processing, tax planning, and filing. Strategic acquisitions, including Materia, SafeSend and Additive, have expanded our platform capabilities. In 2025, we launched CoCounsel for Tax and Audit, Ready to Review and Ready to Advise. Ready to Review introduced agentic tools that automate and enhance tax research and return preparation workflows. Ready to Advise, our AI-enabled tax planning solution built on the CoCounsel platform, leverages authoritative Checkpoint content and deep tax expertise to analyze client data and identify tailored planning strategies, ranked by relevance and potential impact. It delivers step-by-step guidance backed by authoritative knowledge and integrated workflow tools, enabling firms to scale advisory services efficiently and generate incremental revenue.

Audit Workflow

We provide audit firms with a suite of cloud-based tools designed to streamline engagement workflows, enhance accuracy, and elevate client service through AI-enabled automation. Our newest solutions include CoCounsel Audit, Audit Intelligence Analyze, and Audit Intelligence Test. Audit Intelligence Analyze uses AI to accelerate transaction analysis, identify items for review, optimize sample selection, and direct attention toward higher-risk areas. Audit Intelligence Test reduces manual effort during testing by automating the matching of selected samples to supporting evidence, validating collected amounts, and maintaining documentation within the workflow.

Tax, Audit & Accounting Professionals' competitors include Wolters Kluwer's CCH business, Bloomberg Industry Group, Intuit, Drake Software, and CaseWare, as well as emerging technology startups serving the profession.

Thomson Reuters Annual Report 2025 |

Page 7 |

Reuters

Reuters is a leading provider of trusted news, insight and analysis. Founded in 1851, it brings together world-class journalism, industry expertise and cutting-edge technology with unparalleled speed, reliability and accuracy to enable people to make better decisions. Reuters is committed to the Thomson Reuters Trust Principles, including that of independence, integrity and freedom from bias, and is an essential source of business, financial and world news delivered to financial firms exclusively via LSEG products, to the world’s media organizations, and to professionals via industry events and Reuters.com. In 2025, Reuters delivered approximately 3.6 million unique news stories, 829,000 pictures and images and 142,000 video stories and numerous industry events.

For more information on the Thomson Reuters Trust Principles, please see the “Additional Information – Material Contracts – Thomson Reuters Trust Principles and Thomson Reuters Founders Share Company” section of this annual report.

Reuters’ primary global competitors include Bloomberg, the Associated Press, Agence France-Presse and Getty.

Global Print

Global Print is a leading provider of information, primarily in print format, to legal and tax professionals, government (including federal, state and local government lawyers and judges), law schools and corporations. Global Print also leverages its capabilities through offering commercial printing services to a wide range of book publishers including those in trade, government, associations, faith-based organizations, universities and children’s books. The business serves customers primarily in the United States, Canada and the United Kingdom. Global Print’s primary global competitors are LexisNexis and Wolters Kluwer.

Page 8 |

Thomson Reuters Annual Report 2025 |

Key Products

Our customer-focused structure enables us to have broader conversations with our customers, with a more cohesive go-to-market approach. We believe that this focus will create opportunities to deepen relationships with customers on more of our products and services across their organizations, increase sales to existing customers, improve retention and attract new customers. The following table provides information about our key products and target customers.

Product |

Description |

Legal Professionals |

Corporates |

Tax, Audit & Accounting Professionals |

Audit Intelligence (Analyze and Test) |

AI-powered solution that automates transaction analysis and substantive testing, identifying high-risk transactions, selecting samples, and validating them against bank and source documents to improve audit efficiency and quality.

|

|

|

|

Checkpoint Checkpoint Edge

|

Integrated tax, audit and accounting research solution that delivers news, editorial insights, advisory tools and authoritative content. |

|

|

|

CLEAR CLEAR Risk Inform CLEAR ID Confirm CLEAR Adverse Media Sanctions PeopleMap |

US-based public records platform providing risk, fraud, and investigative solutions to authorized businesses and government agencies limited to legally permissible purposes including investigating crimes and locating victims, performing due diligence and preparing for litigation and detecting fraud and mitigating risk. |

|

|

|

Cloud Audit Suite |

End-to-end solution providing accuracy and efficiency throughout the audit process through a suite of tools including: engagement management and trial balance capabilities, guided assurance with assisted decision making, online confirmations and embedded disclosure examples. |

|

|

|

CoCounsel Legal |

Next-generation agentic AI platform that brings together legal research, essential workflow automation, intelligent document search and drafting, and AI-powered legal assistance within one unified solution including CoCounsel, CoCounsel Drafting, Westlaw and Practical Law. |

|

|

|

CoCounsel for Legal |

Generative AI platform built for legal professionals, leveraging proprietary content and trained by domain experts. Enables more efficient research, document review, deposition preparation, correspondence drafting, contract analysis and policy compliance with a growing library of skills. |

|

|

|

CoCounsel for Tax & Audit

|

Generative AI platform for intelligent tax and accounting automation using large language models with tax and accounting content. Provides AI-powered document analysis, data extraction, research assistance, and content generation through a natural language interface for tax and accounting questions. |

|

|

|

Thomson Reuters Annual Report 2025 |

Page 9 |

Dominio |

Complete, fully integrated suite for Brazilian accounting firms, automating routine operations including tax calculations, payroll and generation of electronic files for eSocial, EFD and ECD. Integrates with Brazilian government systems ensuring compliance at municipal, state, and federal levels, with a client portal and firm management tools. |

|

|

|

ONESOURCE

Direct Tax |

Global cloud-based tax and trade solutions managing direct and indirect tax compliance, indirect tax determination, statutory reporting, trust taxation, tax information reporting, tax planning, trade compliance, trade operations, trade special programs, trade regulatory content and overall data and process management. |

|

|

|

Practical Law Practical Law Connect Practical Law Dynamic Tool Set |

Legal know-how, current awareness and workflow tools with embedded guidance from expert practitioners. |

|

|

|

Ready to Advise |

Provides step-by-step guidance supporting authoritative knowledge and workflow tools that enable CPA firms to take a scalable approach to tax advisory services, generating incremental revenue for their businesses. |

|

|

|

Ready to Review |

Automates the creation of the first draft of a tax return, extracting and mapping data, running that data through our tax engines and diagnosing and resolving errors. |

|

|

|

UltraTax & CS Professional Suite |

Scalable, integrated suite of desktop and online software applications that encompass key aspects of a professional accounting firm’s operations, from collecting client data and preparing and filing tax returns to the overall management of the accounting practice. |

|

|

|

Westlaw, Westlaw Edge Westlaw Advantage |

Westlaw is our primary online legal research delivery platform. Westlaw offers authoritative content, powerful search functionality and research organization, team collaboration features and navigation tools to find and share specific points of law and search for analytical commentary. |

|

|

|

Page 10 |

Thomson Reuters Annual Report 2025 |

Additional Business Information

Corporate Center

Our corporate center seeks to foster a group-wide approach to management while allowing our business segments sufficient operational flexibility to serve their customers effectively. Our corporate center centrally manages our Operations & Technology group, our commercial operations and certain functions such as finance, legal and human resources.

The Role of Thomson Reuters Enterprise Centre

The Thomson Reuters Enterprise Centre in Switzerland has a pivotal role in our business operations and strategic initiatives. Key decisions on company-wide strategy and global commercial policies are led by a senior Executive Leadership team in Switzerland representing multiple functions across Strategy, Product, Operations & Technology, Engineering, Labs, Legal, Risk & Compliance and Finance. This strengthens our speed of innovation, collaboration and direction setting across our global business.

Operations & Technology

Our Operations & Technology group consolidates essential corporate functions into a cohesive team, encompassing product engineering, technology delivery and service, data and analytics, AI innovation, digital transformation, customer service, procurement, real estate, collections and content operations. This unified approach provides a strong foundation for accelerating our scale and growth strategies, allowing us to focus resources effectively on key priorities. In 2026, we will continue to advance our products and service through AI innovation.

Thomson Reuters Annual Report 2025 |

Page 11 |

We aim to deliver AI enhancements across our product suite, enabling the agility and speed that our customers demand, while simultaneously improving margin through AI-driven process optimization.

Our commitment to transformation ensures our content, products and services evolve to meet customer needs, while we continue to focus on securing customer data and global systems as part of our ongoing security program enhancements.

Innovation, Research and Development

Innovation remains a cornerstone of our strategy and a key driver of competitive advantage. In 2025, we advanced our commitment to applied research and technology development through Thomson Reuters Labs—our dedicated research and innovation arm. Building on the momentum from 2024, we expanded the Labs’ capabilities and deepened its integration with product engineering, accelerating delivery of AI-powered solutions across our portfolio.

For over three decades, Thomson Reuters Labs has been at the forefront of emerging technologies in high-stakes professional domains. In 2025, Labs delivered new AI capabilities across Westlaw, Practical Law, CoCounsel for Legal, CoCounsel for Tax, CLEAR, ONESOURCE+ and Reuters. These innovations enable legal professionals to perform complex, multi‑step research and analyze large volumes of litigation documents in a fraction of the time previously required. For tax and accounting, Labs developed solutions that automate return preparation and help firms surface and deliver personalized advisory strategies at scale. The organization continues to advance the state of the art in professional‑grade AI through active engagement with the global research community, participating in nearly 30 AI conferences and contributing around 70 articles, patents, workshops, and peer‑reviewed publications.

In addition to organic development, we strengthened our innovation pipeline through strategic acquisitions. These investments brought in specialized capabilities in areas such as workflow automation, advanced legal research and AI-driven analytics, enabling us to accelerate product development and deliver integrated solutions faster. By combining these new technologies with our trusted content and human expertise, we are creating a more connected ecosystem that supports professionals across tax, legal, compliance and risk domains.

As we progress toward our ambition to become the world’s leading content-driven technology company, innovation is not just a function—it is a mindset. By combining cutting-edge technology with human expertise, we continue to redefine how trusted answers are delivered in an ever-changing world.

Go to Market

In 2025, we continued to modernize and unify our go-to-market model to reflect how professionals evaluate, buy, and adopt technology today. Our approach combines direct sales, digital commerce, partner channels and proactive customer success motions, supported by expanding AI capabilities and a more integrated global commercial organization.

We primarily sell our products and services directly to our customers through our sales team. We enhanced coordination across go-to-market, marketing, customer success and partnerships to deliver a more consistent and connected customer experience. Teams leveraged AI-powered insights and improved revenue insight technology to better identify opportunities, prioritize accounts, and support cross-portfolio selling. This enabled more integrated conversations around our solutions, reflecting customers’ increasing preference for connected capabilities rather than point products.

In addition, we sell some of our products and services online directly to customers. In 2025, we expanded our digital commerce capabilities, offering more of our solutions online and scaling guided self-serve pathways. Customers could trial, purchase and manage products more easily through enhanced onboarding flows, improved in-product support and AI-driven recommendations that helped accelerate adoption and value realization. These investments broadened our reach across smaller firms and emerging customer segments while also reducing acquisition and servicing costs.

Partnerships remained a strategic growth driver. We expanded our relationships across system integrators, resellers, referral partners and technology providers, opening new routes to market and accelerating our reach across

geographies and customer segments. New partner programs supported joint solutions, co-marketing initiatives and Application Program Interface (API)-based integrations.

APIs allow our software platforms to connect with those of other companies, providing customers with data and access to the services of both companies. We continued to advance our API capabilities as customers increasingly looked to integrate Thomson Reuters content and AI into their existing technology stacks. Enhanced APIs across our portfolio improved interoperability with third-party platforms, expanded workflow automation and opened new opportunities for embedded use cases. This ecosystem approach supports customers' end-to-end processes and creates more flexible deployment models for our solutions. As our capabilities related to APIs continue to grow, it will further enable our ability to provide more robust solutions in collaboration with our partners to solve our customers’ business challenges.

In 2025, we expanded and formalized our customer success organization to create a scalable, proactive engagement

Page 12 |

Thomson Reuters Annual Report 2025 |

model focused on adoption, value realization and long-term outcomes. Standardized playbooks, digital success programs and data‑driven health insights enabled us to support customers more efficiently and consistently. This work lays the foundation for continued improvements in retention, net revenue retention and cross-portfolio expansion.

Our 2025 go-to-market progress strengthened our commercial foundation and improved how we serve customers across their lifecycle. With enhanced digital buying experiences, a deeper partner ecosystem, expanded API connectivity and a unified customer success model, we continue to evolve our go-to-market approach to meet the needs of modern professionals and support sustained growth in 2026 and beyond.

Intellectual Property

Our products and services primarily consist of information and original content distributed across multiple platforms. We protect these offerings and their underlying content through a comprehensive intellectual property (IP) portfolio. Our IP strategy relies on four key elements: patents and trade secrets that safeguard our innovative content creation and delivery methods; trademarks that protect our brand identity; and copyrights that secure our proprietary content, databases and software source code. We believe our current IP holdings adequately support our business operations.

To strengthen our IP position, we employ both technical and commercial safeguards within our content distribution systems. We actively expand our patent portfolio through global patent applications and acquisitions of patent-holding companies. Our online presence is protected through registered domain names, while our trademarks and copyrights are maintained through strategic registrations and active enforcement against potential infringers. Corporate acquisitions further enhance our IP assets, typically adding trademarks, copyrights, patents, and web domains to our portfolio.

We continuously assess how emerging AI regulations and concepts intersect with intellectual property law to protect our technology, source code, and content. For additional details on IP‑related risks, please refer to the "Risk Factors" section of this annual report.

Acquisitions and Dispositions

Acquisitions – Acquired businesses can strengthen our offerings and enable us to extend our platform with new capabilities that we believe will provide opportunities to expand our positions, better serve our customers and supplement our organic revenue growth. Generally, the businesses that we acquire initially have lower margins than our existing businesses, largely reflecting their stage of development and the costs of integration.

In January 2025, we acquired SafeSend, a United States-based cloud-native provider of technology for tax and accounting professionals. SafeSend automates the ‘last‑mile’ of the tax return, including assembly, review, taxpayer e‑signature and delivery. In July 2025, we acquired TimeBase, a leading provider of Australian legislative information, offering a comprehensive platform for legal professionals to find, search, track and understand legislation. In August 2025, we acquired the commercial and licensing operations of Imagn Images, a US-based sports photography agency. In September 2025, we acquired Additive AI, a San Francisco‑based startup, founded in 2023, that uses cutting‑edge AI to automate tax document processing for tax and accounting professionals. More recently, in February 2026, we acquired Noetica, Inc., a New York-based AI-native start-up that transforms transaction-deal data into structured market intelligence for deal professionals.

We expect that acquisitions will continue to play an important role in our strategy going forward and we expect to continue to make acquisitions from time to time that we believe will strengthen our positions in key growth segments. See the “Liquidity and Capital Resources” section of the "Management’s Discussion and Analysis" for additional information about our capital strategy.

Dispositions – As part of our continuing strategy to optimize our portfolio of businesses and ensure that we are investing in parts of our business that offer the greatest opportunities to achieve growth and returns, we have sold a number of non-core businesses and product lines during the last several years which were not compatible with our strategy.

For more information on acquisitions and dispositions that we made in the last two years, please see the “Management’s Discussion and Analysis” section of this annual report.

Thomson Reuters Venture Fund

During 2025, Thomson Reuters Ventures deepened its commitment to investing in AI‑powered innovation that helps professionals operate more productively and with greater insight. Beyond investing, Thomson Reuters Ventures stayed active in the ecosystem through programming that convenes founders, investors and partners to discuss the evolving AI‑driven startup and professional landscape. Thomson Reuters Ventures prioritizes companies building practical solutions that align with Thomson Reuters customers' needs to reduce friction in core workflows and deliver faster, complementary trusted outcomes.

Thomson Reuters Annual Report 2025 |

Page 13 |

Human Capital Management

Employees

The following table sets forth information on the approximate number of employees by region and unit as of December 31, 2025.

By Region |

|

|

|

Americas |

|

14,400 |

|

Asia Pacific |

|

8,600 |

|

Europe, Middle East and Africa (EMEA) |

|

4,100 |

|

By Unit |

|

|

|

Legal Professionals |

|

800 |

|

Corporates |

|

2,100 |

|

Tax, Audit & Accounting Professionals |

|

800 |

|

Global Print |

|

800 |

|

Government |

|

600 |

|

Reuters |

|

3,700 |

|

Product & Editorial |

|

3,600 |

|

Operations & Technology |

|

9,400 |

|

Corporate Center (Enabling Functions) |

|

1,400 |

|

Commercial Functions(1) |

|

1,200 |

|

Other(2) |

|

2,700 |

|

Thomson Reuters |

|

27,100 |

|

We believe that we generally have good relations with our employees, unions and works councils, although we have had disputes from time to time with the various unions that represent some of our employees. Our senior management team is committed to maintaining good relations with our employees, unions and works councils.

Overview

Our human capital practices and initiatives are designed to attract, develop and retain talented employees across our global business. At Thomson Reuters, our global team fuels innovation through their curiosity and ambition. We foster a values-driven culture that attracts top talent, empowers our people to grow and lets them do the work that matters most. We aim to ensure employees feel valued, have meaningful opportunities to develop and are empowered to succeed. Our priorities span key areas including compensation and benefits, culture and engagement, talent acquisition, learning and development and inclusion and belonging.

We are continuing to build talent for the future by integrating AI into day-to-day work, strengthening business acumen and deepening knowledge of our evolving product portfolio and customers. In 2025, we launched refreshed values to support how we work and guide our decisions and behaviors for how we deliver for our customers and colleagues.

We remain committed to career development through Grow My Way, an initiative that supports continuous skill building and enables leaders to deploy talent effectively as business needs change. As our AI capabilities mature, we are shifting from measuring AI tool adoption alone to capturing the operational and business impacts enabled, such as improved cycle times, quality, customer outcomes and productivity.

Supporting and developing people leaders remains a priority. In 2025, we focused on building skills around critical conversations and leading through ambiguity. We will continue broadening people leader development through the introduction of Leading at TR, with upskilling focus areas around setting clear goals, delivering quality feedback, improving empowerment and decision making and leading change. This leadership program is designed to strengthen leadership effectiveness at all levels, accelerate performance and reinforce a culture of accountability, collaboration and results.

Page 14 |

Thomson Reuters Annual Report 2025 |

Our investments in learning, career development and AI are reflected in employee feedback. In our most recent organizational health survey, scores related to learning and innovation increased and remain top quartile, with:

We voluntarily publish a range of human capital metrics in our securities filings and on our website, including our Social Impact & ESG Report. Certain metrics are not publicly disclosed due to competitive considerations. We expect human capital management to remain an important focus area for management and the Board of Directors, supporting strong stewardship of the organization, advancing societal objectives and contributing to our strategic advantage in the marketplace.

For additional information on our human capital management practices, please see the “Environmental, Social and Governance (ESG)” section below.

Environmental, Social and Governance (ESG)

Our company is dedicated to serving institutions and businesses that keep the wheels of commerce turning, uphold justice and taxation systems, fight fraud, support law enforcement and report on world events with impartiality, as an important source of unbiased news globally. We pursue ESG initiatives because they contribute to value creation for our customers, employees, shareholders and other stakeholders. The Board and its committees oversee different ESG-related areas that are of the greatest importance to the organization and our stakeholders to achieve our long-term strategic objectives. Ultimately, though, our ESG-related initiatives require employees who take on responsibility for them and are empowered to achieve them.

Our ESG-related workstreams include sustainability, inclusion and belonging, community relations and volunteerism. ESG factors are considered in our Enterprise Risk Management (ERM) processes. Our financial support of the Thomson Reuters Foundation also contributes to our ongoing ESG efforts.

We post a Social Impact & ESG Report annually on our website, www.thomsonreuters.com/social-impact-report, which summarizes our strategy, includes stories of progress and tracks performance, tying our efforts to our business strategy and commercial expertise. We encourage you to review the Social Impact & ESG Report to gain a better understanding of our accomplishments and practices in these areas. |

We believe in the power of collaboration with the international business community, so we are signatories of the United Nations Global Compact (UNGC), a non-binding United Nations (U.N.) pact to encourage businesses and firms worldwide to adopt sustainable and socially responsible policies. We are also aligned with the United Nations Guiding Principles on Business and Human Rights (UNGPs), which augment our longstanding commitment to the UNGC, the U.N. Declaration on Human Rights and other international standards.

In 2025, we updated our ESG double materiality assessment to ensure the continued alignment of our ESG initiatives with our business strategy and to comply with new global regulations. This assessment enables us to identify and prioritize the ESG issues that are most likely to impact our business and stakeholders in the short and long-term, and establishes a robust foundation for our ongoing sustainability reporting and management processes. In 2025, we also completed our second company-wide human rights impact assessment (HRIA) of our global operations, products and services. This assessment examined potential impacts across stakeholder groups and helped us to identify salient human rights risks which were then mapped against the expectations of the UNGPs and which now inform our human rights strategy and roadmap. Our commitment to respecting human rights throughout our operations will continue to guide our work and the recommendations from this comprehensive ESG assessment will continue to help us identify, assess and proactively respond to salient and material risks across our enterprise. Finally, in March 2023, we released our human rights policy, which informs our colleagues, customers, shareholders and those in the communities where we operate and do business, of our commitment and approach to human rights.

Our 2025 Social Impact & ESG Report, which we anticipate publishing later in 2026, will contain more information about our ESG strategy and results and will be available on our website at thomsonreuters.com.

Environmental Practices

We aim to continue to reduce our environmental impact globally. We continue to source renewable energy for 100% of our operations. We have achieved this largely by purchasing renewable energy credits to match our electricity use. We are also working closely with our suppliers to drive lower emissions within our supply chain. We will continue to measure and manage our own emissions and environmental impacts and continue to find ways to further assess, monitor and improve our carbon footprint.

Thomson Reuters Annual Report 2025 |

Page 15 |

Social Practices

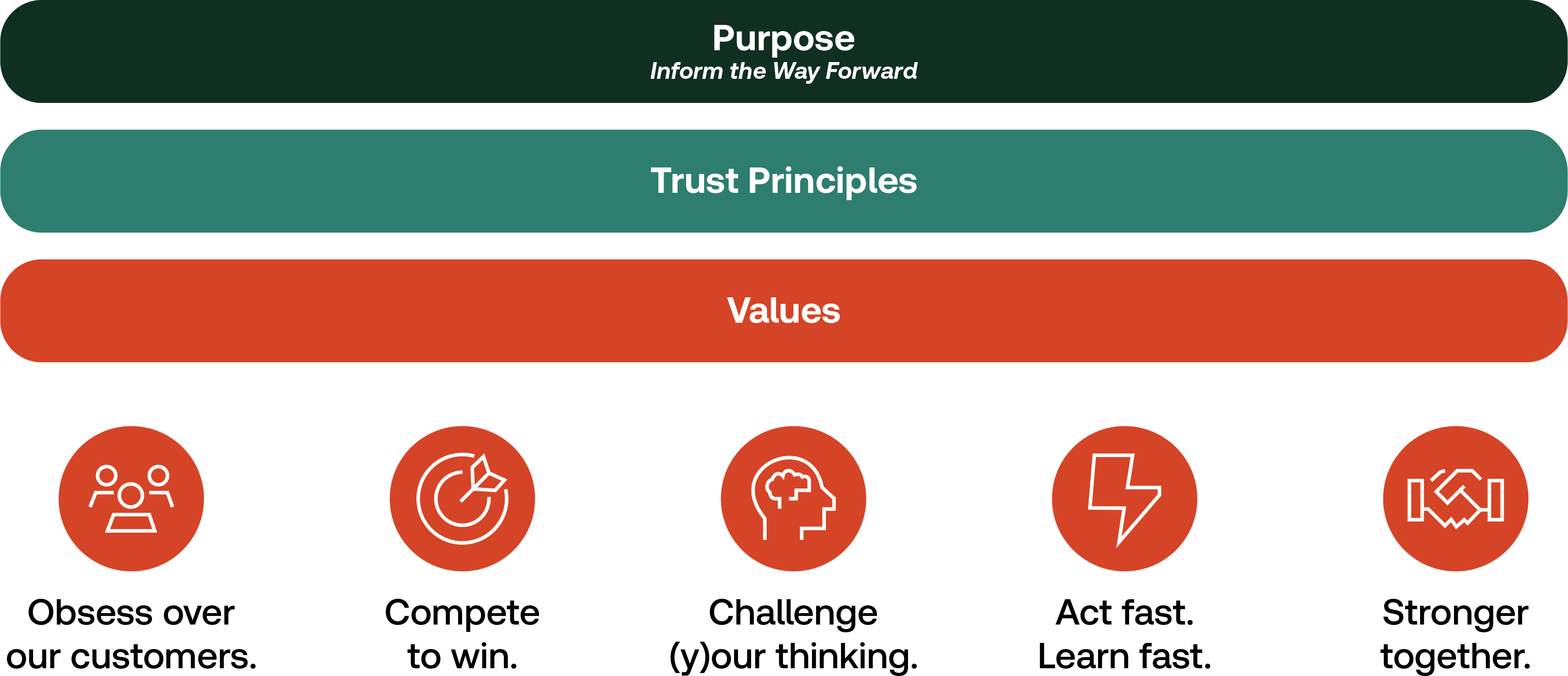

Our values and culture

At Thomson Reuters, our team is committed to solving big challenges for our customers and supporting skill building for colleagues to thrive in an AI-enabled future. In 2025, we introduced new company values that are rooted in our purpose to Inform the Way Forward and the Thomson Reuters Trust Principles. These values elevate us to a higher standard of customer excellence, product innovation, teamwork and success.

Inclusion and Belonging

As a global company with employees located around the world, inclusion and belonging are core to our purpose and values, fostering an inclusive workplace where people with varied backgrounds, perspectives and experiences can grow and thrive. We believe this gives us access to the broadest talent pool, leads to better decision making and fosters greater innovation.

Health and Wellbeing

Our people remain our greatest asset and we are steadfast in our commitment to fostering a supportive and empowering workplace environment. We offer employee benefit plans, tools, resources and workplace practices that promote mental, physical, financial and social wellbeing.

Central to our employee experience is a strong focus on mental health and wellbeing. Our Mindful Leadership Training is a key component of our Managing at TR program, ensuring that all new managers are equipped to lead effectively. Additionally, we offer global resources such as employee assistance programs, meditation apps and mindfulness discussions, highlighted during our May and October Mental Health campaigns.

Thomson Reuters upholds its commitment to flexibility through our hybrid working policy and the “Flex My Way” initiative. These global flexible workplace policies enable employees to balance family and customer needs effectively. With offerings like Bereavement Leave, Caregiver Paid Time Off, Sabbatical Leave, Parental Leave, Work From Anywhere policy and local paid and unpaid time off policies, we ensure our employees can take the time they need, when they need it. Together, these efforts underline our unwavering dedication to cultivating a physically, mentally, financially and socially healthy workplace for all.

Community and Social Impact

Thomson Reuters annually provides 16 hours of paid volunteer time off (VTO) to every employee and provides an additional 20 hours of paid VTO to a subset of employees with law degrees to provide legal pro bono aid to not-for-profit organizations.

In 2025, our employees logged a total of approximately 63,000 volunteer hours, including over 10,000 hours in total pro bono support to not-for-profit organizations around the world. In addition to VTO, Thomson Reuters offers a global Corporate Match program to match eligible employee donations as well as a Volunteer Rewards Program in which an employee earns corporate funding for reaching 20 hours of volunteering. In 2025, donations by our employees together with our corporate matching and rewards donations totaled approximately $2.2 million to over 1,900 not-for-profits in 26 countries.

Page 16 |

Thomson Reuters Annual Report 2025 |

Finally, we provide some of our products and services free of charge to various not-for-profit organizations to support their initiatives, including access to our Westlaw, Practical Law, HighQ and CoCounsel products. For example, since 2010, Thomson Reuters has made our CLEAR product available to the National Center for Missing and Exploited Children. Additionally, through our AI for Justice legal aid initiative, not-for-profit legal organizations can utilize CoCounsel, our premier AI-powered legal assistant.

The Thomson Reuters Foundation

The Thomson Reuters Foundation works to bolster the resilience of independent media, strengthen access to the law and promote responsible business practices. It leverages its unique combination of media and legal expertise, together with data intelligence, to inform, connect and empower professionals and civil society to strengthen free, fair and informed societies. It delivers its work through capacity-building programs, legal support, research, news, data-driven products and events, including its flagship annual forum, the Trust Conference.

Additional information on the Foundation can be found at www.trust.org.

Governance Practices

Our Board and its committees oversee ESG initiatives. The Corporate Governance Committee of the board of directors evaluates our ESG strategy and progress and is updated regularly by our management. We remain committed to our values and ethics through our governance practices, which include our Code of Business Conduct and Ethics.

Thomson Reuters Annual Report 2025 |

Page 17 |

Properties and Facilities

We own and lease office space and facilities around the world to support our businesses. We believe that our properties are in good condition and are adequate and suitable for our present purposes. The following table provides summary information about our principal properties as of December 31, 2025.

Facility |

|

Owned/Leased |

|

Principal Use |

|

|

|

|

|

|

|

|

|

|

|

|

|

610 Opperman Drive, |

|

Owned |

|

Global Print operating facility |

|

|

|

|

|

|

|

|

|

|

|

|

|

2900 Ames Crossing Rd. |

|

Subleased |

|

Legal Professionals operating facility |

|

|

|

|

|

|

|

|

|

|

|

|

|

6300 Interfirst Drive, |

|

Owned |

|

Tax, Audit & Accounting Professionals operating facility |

|

|

|

|

|

|

|

|

|

|

|

|

|

Knowledge Court, |

|

Leased |

|

Thomson Reuters shared services center |

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Canada Square, |

|

Subleased |

|

Legal Professionals, Tax, Audit & Accounting Professionals and |

|

|

|

|

|

|

|

|

|

|

|

|

|

Hyderabad, Bldg. 11 Madhapur, Hyderabad, India |

|

Leased |

|

Global shared service center |

|

|

|

|

|

|

|

|

|

|

|

|

|

19 Duncan Street Toronto, Ontario, Canada |

|

Leased |

|

Thomson Reuters headquarters |

|

|

|

|

|

|

|

|

|

|

|

|

|

Reforma Cuarzo |

|

Leased |

|

Global shared service center |

|

|

|

|

|

|

|

|

|

|

|

|

|

6160 Warren Parkway |

|

Leased |

|

Tax, Audit & Accounting Professionals and Corporates operating facility |

|

|

|

|

|

|

|

|

|

|

|

|

|

3 Times Square, New York, New York, United States |

|

Owned/leased(1) |

|

Reuters, Legal Professionals and Corporates operating facility |

|

|

|

|

|

|

|

|

|

|

|

|

|

Landis & Gyr 3, Zug, Switzerland |

|

Leased |

|

Enterprise Centre |

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 18 |

Thomson Reuters Annual Report 2025 |

Risk Factors

The risks and uncertainties below represent the risks that our management believes could be material. If any of the events or developments discussed below actually occurs, our business, financial condition or results of operations could be adversely affected. Other factors not presently known to us or that we presently believe are not material could also affect our future business and operations. The risks below are organized by categories and are not necessarily listed in the order of priority to our company.

Risk Category |

Page |

19 |

|

23 |

|

25 |

|

27 |

|

30 |

|

32 |

Strategic Risks

We operate in highly competitive markets and may be adversely affected by this competition.

The markets for our information, software, services and news are highly competitive and are subject to rapid technological changes and evolving customer demands and needs, including, as an example, the ongoing transformation brought on by the development and use of AI and the capabilities it offers across the spectrum of how businesses operate. Our customers increasingly look to us for solutions to help them adapt, improve efficiency and demonstrate value through leveraging technology to deliver a differentiated work product. If we fail to compete effectively and with speed to market, we may not retain key customers and our revenues, profitability and cash flows could be adversely affected.

We face more competition from fast-moving and agile competitors as AI continues to be integrated into the markets in which we compete. The rapid advancements in coding tools may enable new and existing competitors to create competing offerings rapidly, or they may incorporate AI into their products and solutions sooner and more successfully than we do, resulting in greater, faster and more effective adoption by customers, which could impair our ability to compete effectively and adversely affect our business, financial condition and results of operations. If we are not able to provide products, services and solutions that compete effectively, we could experience reduced sales and our business could be adversely affected. Our established, principal competitors have substantial resources, with recognized brands, technological expertise and market experience. With the acceleration of AI technologies there is a risk of our deep domain expertise and content-driven technology focus being undermined by competitors who evolve to provide comparable information and services to our customer base. Our business may be adversely impacted by risks such as the following:

Thomson Reuters Annual Report 2025 |

Page 19 |

We may be adversely affected by uncertainty, downturns and changes in the markets that we serve, particularly in the legal, tax, audit and accounting industries.

We operate in a dynamic external environment that is rapidly shifting due to innovations in technology, evolving global regulation and information proliferation. Uncertainty, downturns and changes that impact our business can also arise as a result of conditions in global financial markets, changes in macroeconomic factors, changes in laws and regulations, trade policy uncertainty, political conditions and election outcomes, political and social unrest, wars and conflicts, terrorist acts, cyber-attacks, economic and regulatory sanctions, natural disasters and public health crises and other factors over which we have no control.

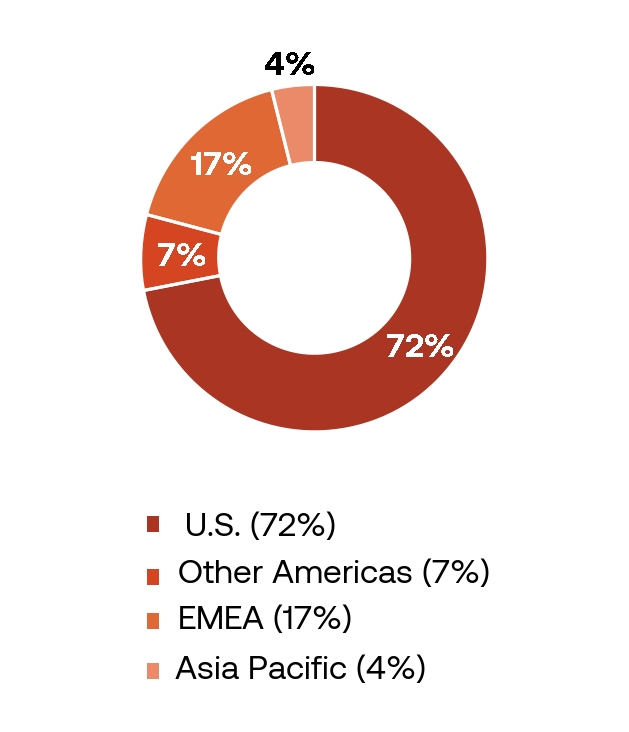

Our performance depends on the financial health and strength of our customers, which in turn is primarily dependent on the general economy in the United States (72% of our 2025 revenues) and secondarily on the general economies in the U.K., Canada, Brazil and other economies of Europe, Asia Pacific and Latin America. The global economy continues to experience substantial disruption and uncertainty due to persisting geopolitical tensions, ongoing protectionism measures (including the imposition of new tariffs, as well as related retaliatory measures), weaker global demand, an evolving interest rate and inflationary backdrop, supply chain disruptions, labour shortages and other events. These factors may create unprecedented economic conditions, including the possibility of an economic recession that may last substantially longer than expected and create stress on economic growth and market volatility. These conditions could lead to limited business opportunities for our customers, creating significant cost pressures for some of them, which could lead to lower demand for our products and services. We are unable to predict the extent of impact or duration of any such economic conditions, or their ultimate impact on demand for our products and services. In 2025, we derived 82% of our revenues from our Legal Professionals, Corporates and Tax, Audit & Accounting Professionals businesses. Global uncertainty and changing economic conditions can impact these industries.

The profitability of our products and services relies on our customers’ demand for and usage of our products and services. While we endeavour to accurately predict these trends, with the impact of changing technology on our customers’ business models, it has become difficult to accurately predict our customers’ demand for our products and services. Cost-cutting, reduced spending or reduced activity by customers may decrease demand for and usage of some of our products and services. This could adversely affect our business, financial condition and results of operations by reducing our revenues, which could in turn reduce the profitability of some of our products and services. Some of our customers may also slow down decision-making or delay planned renewals or implementations because of economic conditions and rapidly changing technology such as AI, which may disrupt historical spending patterns.

Page 20 |

Thomson Reuters Annual Report 2025 |

Trends in the industries we serve may change the way our customers operate and thus may impact our business. We have noted the following trends:

We may not be successful in our AI initiatives, and AI may expose us to certain risks, which could adversely affect our business, reputation, or financial condition and results of operations.

We are making significant investments in AI-based initiatives, including generative and agentic AI. As with other investments, there are significant risks involved in the development and application of AI and there can be no assurance that the usage of AI will enhance our products or services, meet the needs and expectations of our customers, or be beneficial to our business, including our efficiency or profitability.

The development of AI technologies is complex and evolving and there are technical challenges associated with achieving desired levels of accuracy, efficiency and reliability. AI algorithms, models and data may have limitations, including inherent human biases, errors, or inability to handle certain data types or scenarios. Failure of our AI technologies to produce accurate results may have a negative impact on our reputation and adversely affect our business and we may be subject to legal and regulatory scrutiny and increased litigation. Given that the development, adoption and use of AI technologies remains fast-paced, it is not possible to predict all the risks related to the use of AI and the impact they may have on the company.

If we are unable to keep pace with rapid technological developments to provide new products, services, applications and functionalities to meet our customers’ needs, attract new customers and retain existing ones, expand into new geographic markets and identify areas of higher growth, our ability to generate revenues or achieve higher levels of revenue growth in the future may be adversely affected.

Our growth strategy involves enhancing our current products and developing innovative new products, product features, and services in a timely and cost-effective manner to meet our customers’ needs. This includes anticipating and responding to industry trends and technological changes, expanding into new geographic markets and maintaining a strong position in the sectors that we serve.

Technologies such as AI, ML, data synthesis and user-generated capabilities have created the need to adapt rapidly to the shifting landscape and to generate insights from these technologies to increase the value that our solutions and services bring to our customers. While we are focused on these changes to the technological landscape, if we fail to adapt, or do not adapt quickly enough, our business, financial condition and results of operations could be adversely impacted.

We continue to focus on driving growth through more collaboration and stronger relationships with both established and emerging companies and incubators. We are also continuing to increase our focus on partnerships and APIs. Some of these initiatives combine another company’s technology, data or other capabilities with our products and services. These initiatives involve a number of risks, including the risk that the expected synergies will not be realized, that they may require substantial expenditures and take considerable time and that the expected results may ultimately not be achieved, that a new initiative may conflict or detract from our existing businesses, or that security measures may not be adequate or could adversely impact our brand and reputation. In addition, our ability to adopt new services and develop new technologies may be inhibited by industry-wide standards, new laws and regulations, resistance to change from our customers, limitations in technological ability or third parties’ IP rights. While we believe

Thomson Reuters Annual Report 2025 |

Page 21 |

these initiatives will be attractive to our customers, allow us to innovate more quickly and build sales channels in segments that we could not have reached as quickly on our own, we are unable to provide any assurances that these initiatives will increase our revenue growth.

Over the last few years, we have made significant investments designed to improve and enhance the functionality and performance of several of our key products, such as Westlaw, CoCounsel, HighQ, Legal Tracker, CLEAR, Checkpoint Edge, Practical Law, ONESOURCE and SurePrep. We have also successfully migrated customers from legacy offerings to our current propositions and continued to enhance the reliability and resiliency of the technology infrastructure that we use to deliver products and services. However, if our customers’ adoption rates for existing and new products and services are lower than our expectations, our revenues may be lower and our results of operations may be adversely affected.

We may be unable to derive fully the anticipated benefits from our existing or future acquisitions, dispositions, or other strategic transactions, including joint ventures and investments.

While we are focused on growing our businesses organically, acquisitions and other strategic transactions remain an important part of our growth strategy to expand and enhance our products, services and customer base and to enter new geographic areas.

In 2025, we acquired SafeSend, a United States-based cloud-native provider of technology for tax and accounting professionals. We also acquired Additive AI, a San Francisco-based startup, founded in 2023, which uses cutting-edge AI to automate tax document processing for tax and accounting professionals, as well as TimeBase, a leading provider of Australian legislative information, offering a comprehensive platform for legal professionals to find, search, track and understand legislation. Lastly, we acquired the commercial and licensing operations of Imagn Images, a US-based sports photography agency.

In the future, we may not be able to successfully identify attractive acquisitions or other strategic transaction opportunities or make acquisitions or other strategic transactions on terms that are satisfactory to our company from a commercial perspective. In addition, competition for acquisitions in the industries in which we operate during recent years has escalated and may increase the price of acquisitions or other strategic transactions, which could cause us to refrain from making certain acquisitions. Our ability to execute on opportunities may also be affected by factors beyond our control, including without limitation, commercial or regulatory changes that may subject us to increased regulatory scrutiny from competition and antitrust authorities in connection with acquisitions and other strategic transactions. Achieving the expected returns and synergies from existing and future acquisitions or other strategic transactions will depend in part upon our ability to integrate the products and services, technology, administrative functions and personnel of these businesses into our segments in an efficient and effective manner. We cannot guarantee that we will be able to do so, or that our acquired businesses, joint ventures or investments will perform at anticipated levels or that we will be able to obtain these synergies. Management resources may also be diverted from operating our existing businesses to certain acquisition and other strategic transaction integration challenges. If we are unable to successfully integrate acquired businesses and other strategic transactions, as applicable, our anticipated revenues and profits may be lower. Our profit margins may also be lower, or diluted, following the acquisition of, or strategic transactions involving, companies whose profit margins are less than those of our existing businesses. Certain acquisitions may initially incur losses which would reduce our earnings per share in certain periods.

We have also historically decided from time to time to dispose of assets or businesses that are no longer aligned with strategic objectives or our current business portfolio. These transactions may involve challenges and risks. There can be no assurance that future divestitures will occur, or if a transaction does occur, there can be no assurance as to the potential value created by the transaction. The process of exploring strategic alternatives or selling a business could also negatively impact customer decision-making and cause uncertainty and negatively impact our ability to attract, retain and motivate key employees. Any failures or delays in completing divestitures, including separation activities, could have an adverse effect on our business, financial condition and results of operations and on our ability to execute our strategy. Although we have established procedures and processes to mitigate these risks, there is no assurance that those procedures and processes will be effective or that these transactions will be successful. In addition, we expend costs and management resources to complete divestitures and manage post-closing arrangements. Completed divestitures may also result in continued financial involvement in the divested business, such as through guarantees, indemnifications, transition services arrangements or other financial arrangements, following the transaction.

Our brands and reputation are important company assets and are key to our ability to remain a trusted source of information and news.

The integrity of our brands and reputation is key to our ability to remain a trusted source of information and news and to attract and retain customers. Negative publicity regarding our company or actual, alleged or perceived issues regarding one of our products or services could harm our relationship with customers.

Page 22 |

Thomson Reuters Annual Report 2025 |

Failure to protect our brands or a failure by our company to uphold the Thomson Reuters Trust Principles may also adversely impact our credibility as a trusted supplier of content and may have a negative impact on our information and news business.

There is a focus from some stakeholders on corporate responsibility, specifically relating to ESG initiatives and corporate sustainability reporting. We pursue ESG initiatives because they contribute to value creation for our customers, employees, shareholders and other stakeholders. In 2025, we completed our second ESG double materiality assessment to comply with new global regulations. We have set a number of targets related to these initiatives and identified and prioritized ESG issues, risks and opportunities. Standards for tracking and reporting ESG matters continue to evolve and we may not be able to implement new and changing standards in ways that meet the expectations of all of our stakeholders. If we fail to satisfy the expectations of investors, customers, vendors, employees, regulators and other stakeholders related to our ESG performance and in our corporate sustainability reporting or our ESG initiatives are not executed as planned, it could adversely affect our reputation, business, share price, financial condition or results of operations. Due to the shifting legal and policy landscape, as well as changing stakeholder expectations, our reputation also may be harmed by negative perceptions that our customers, employees and other stakeholders may have about our action or inaction on social, ethical, or political issues.

Social and ethical issues relating to the use of new and evolving technologies, such as AI, in our products and services could adversely affect our business, financial condition or results of operations.

Many of our products and services use new and evolving technologies, such as AI. These often present social and ethical risks and challenges that could affect their adoption and therefore our business. For example, the use of AI in our products may give rise to risks related to harmful content, inaccuracy, misinformation, bias, discrimination, IP infringement or misappropriation, defamation, data privacy and cybersecurity, among others. We may not have insight into, or control over, the practices of third parties who utilize AI technologies. As such, we cannot guarantee that third parties will not use AI technologies for improper purposes. If we enable or offer AI solutions, or enter into partnerships with third parties or engage third party vendors in respect of AI technologies, that result in any of the foregoing or otherwise draw controversy due to their perceived or actual impact on society, we may experience brand or reputational harm, competitive harm or legal liability and regulatory scrutiny.

Evolving government regulation related to AI use and ethics, or requirements from third-party groups, such as local bar associations or tax licensing boards, may also increase the burden and cost of research and development in this area and failure to properly remediate AI usage or ethics issues may cause public confidence in AI to be undermined, which could slow adoption of AI in our products and services. The rapid evolution of AI will require the application of resources to develop, test and maintain our products and services to help ensure that AI is implemented ethically in order to minimize unintended, harmful impacts. If we do not maintain ethical and transparent policies and procedures related to AI, this could result in reputational harm and legal liability, which could adversely affect our business, financial condition or results of operations.

Technology and Data Risks

We and our third-party providers face risks related to cybersecurity threats and incidents that could adversely affect our reputation, business, results of operations, and financial condition.