Exhibit 99.1

| Global Net Lease Second Quarter 2025 Investor Presentation Adobe Garamond Pro Font throughout Footnotes Calibri (Body), 7pt R = 27 G = 117 B = 188 R = 242 G = 242 B = 242 R = 16 G = 37 B = 63 Titles= 20% Tint Pictured – McLaren Campus in Woking, U.K. |

| 1 FORWARD LOOKING STATEMENTS This presentation contains statements that are not historical facts and may be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the timing, ability to consummate and consideration related to our anticipated acquisitions and dispositions (including the proposed closing of the encumbered properties portion of the Multi-Tenant Portfolio), the intent, belief or current expectations of us, our operating partnership and members of our management team, as well as the assumptions on which such statements are based, and generally are identified by the use of words such as “may,” “will,” “seeks,” “anticipates,” “believes,” “expects,” “estimates,” “projects,” “potential,” “predicts,” “plans,” “intends,” “would,” “could,” “should” or similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These forward-looking statements are subject to risks, uncertainties, and other factors, many of which are outside of our control, which could cause actual results to differ materially from the results contemplated by the forward-looking statements. These risks and uncertainties include the risks that any potential future acquisition or disposition by us is subject to market conditions, capital availability and timing considerations and may not be identified or completed on favorable terms, or at all. Some of the risks and uncertainties, although not all risks and uncertainties, that could cause our actual results to differ materially from those presented in our forward-looking statements are set forth under “Risk Factors” and “Quantitative and Qualitative Disclosures about Market Risk” sections in our Annual Report on Form 10-K, our Quarterly Reports on Form 10- Q and our other filings with the U.S Securities and Exchange Commission (“SEC”) as such risks, uncertainties and other important factors may be updated from time to time in our subsequent reports. Further, forward-looking statements speak only as of the date they are made, and we undertake no obligation to update or revise any forward-looking statement to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time, unless required by law. |

| 2 This presentation also includes estimated projections of future operating results. These projections are not prepared in accordance with published guidelines of the SEC or the guidelines established by the American Institute of Certified Public Accountants for preparation and presentation of financial projections. This information is not fact and should not be relied upon as being necessarily indicative of future results; the projections were prepared in good faith by management and are based on numerous assumptions that may prove to be wrong. All such statements, including but not limited to estimates of value accretion, synergies, run-rate or annualized figures and results of future operations after making adjustments to give effect to assumed future operations reflect assumptions as to certain business decisions and events that are subject to change. As a result, actual results may differ materially from those contained in the estimates. Accordingly, there can be no assurance that the estimates will be realized, or that the projections described in this presentation will be realized at all. This presentation also contains estimates and information concerning our industry and tenants, including market position, market size and growth rates of the markets in which we operate, that are based on industry publications and other third-party reports. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to these estimates. We have not independently verified the accuracy or completeness of the data contained in these publications and reports. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Quantitative and Qualitative Disclosures about Market Risk” sections of the Company’s Annual Report on Form 10-K, and all of its other filings with the SEC, as such risks, uncertainties and other important factors may be updated from time to time in the Company’s subsequent reports. Credit Ratings A securities rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time. Each rating agency has its own methodology of assigning ratings and, accordingly, each rating should be evaluated independently of any other rating. Non-GAAP Financial Measures This presentation includes various performance indicators and non-GAAP financial measures that we use to help us evaluate our ability to incur and service debt, financial condition and results of operations. NOI and Adjusted EBITDA and pro forma presentations of the foregoing are financial measures that are calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles in the United States of America (“GAAP”). Reconciliations of such non-GAAP measures to their nearest comparable GAAP measures can be found, with respect to the quarterly information regarding 2Q24, 3Q24 and 4Q24 in the Company’s supplemental information for the quarter ended December 31, 2024, furnished as exhibit 99.2 to the Current Report on Form 8-K filed with the SEC on February 27, 2025, and with respect to the quarterly information regarding 1Q25 in the Company’s supplemental information for the quarter ended March 31, 2025, furnished as exhibit 99.2 to the Current Report on Form 8-K filed with the SEC on May 7, 2025, accessible at: https://www.sec.gov/ix?doc=/Archives/edgar/data/1526113/000152611325000010/gnl-20250507.htm and https://www.sec.gov/ix?doc=/Archives/edgar/data/1526113/000152611325000005/gnl-20250227.htm which are incorporated by reference herein. Any non-GAAP financial measures used in this presentation are in addition to, and not meant to be considered superior to, or a substitute for, the Company’s financial statements prepared in accordance with GAAP. Additional information with respect to the Company is contained in its filings with the SEC and is available at the SEC's website, www.sec.gov, and on the Company’s website, https://www.globalnetlease.com/. PROJECTIONS |

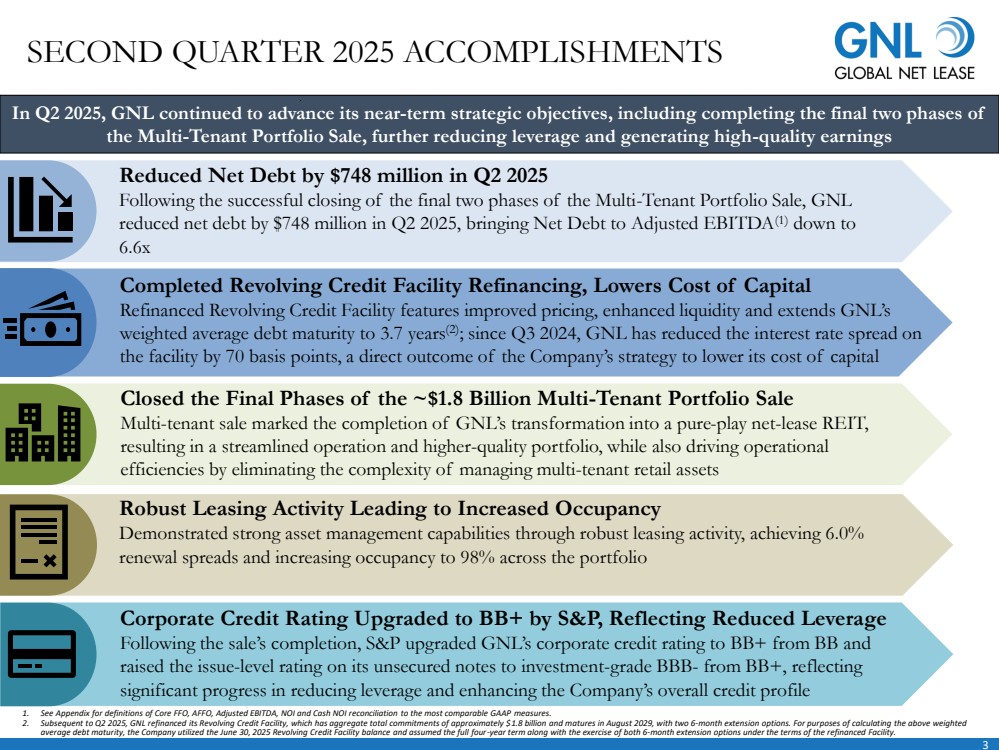

| 3 SECOND QUARTER 2025 ACCOMPLISHMENTS In Q2 2025, GNL continued to advance its near-term strategic objectives, including completing the final two phases of the Multi-Tenant Portfolio Sale, further reducing leverage and generating high-quality earnings Reduced Net Debt by $748 million in Q2 2025 Following the successful closing of the final two phases of the Multi-Tenant Portfolio Sale, GNL reduced net debt by $748 million in Q2 2025, bringing Net Debt to Adjusted EBITDA(1) down to 6.6x Completed Revolving Credit Facility Refinancing, Lowers Cost of Capital Refinanced Revolving Credit Facility features improved pricing, enhanced liquidity and extends GNL’s weighted average debt maturity to 3.7 years(2); since Q3 2024, GNL has reduced the interest rate spread on the facility by 70 basis points, a direct outcome of the Company’s strategy to lower its cost of capital Closed the Final Phases of the ~$1.8 Billion Multi-Tenant Portfolio Sale Multi-tenant sale marked the completion of GNL’s transformation into a pure-play net-lease REIT, resulting in a streamlined operation and higher-quality portfolio, while also driving operational efficiencies by eliminating the complexity of managing multi-tenant retail assets Robust Leasing Activity Leading to Increased Occupancy Demonstrated strong asset management capabilities through robust leasing activity, achieving 6.0% renewal spreads and increasing occupancy to 98% across the portfolio 1. See Appendix for definitions of Core FFO, AFFO, Adjusted EBITDA, NOI and Cash NOI reconciliation to the most comparable GAAP measures. 2. Subsequent to Q2 2025, GNL refinanced its Revolving Credit Facility, which has aggregate total commitments of approximately $1.8 billion and matures in August 2029, with two 6-month extension options. For purposes of calculating the above weighted average debt maturity, the Company utilized the June 30, 2025 Revolving Credit Facility balance and assumed the full four-year term along with the exercise of both 6-month extension options under the terms of the refinanced Facility. Corporate Credit Rating Upgraded to BB+ by S&P, Reflecting Reduced Leverage Following the sale’s completion, S&P upgraded GNL’s corporate credit rating to BB+ from BB and raised the issue-level rating on its unsecured notes to investment-grade BBB- from BB+, reflecting significant progress in reducing leverage and enhancing the Company’s overall credit profile |

| 4 Revolving Credit Facility Refinance: The refinancing provides an immediate 35 basis point reduction in interest rate spread, enhances liquidity to over $1 billion(1) and extends weighted average debt maturity to 3.7 years(2) Credit Rating Upgrade: S&P upgraded GNL’s Corporate Credit Rating to BB+ and raised GNL’s issue-level rating on its unsecured notes to investment-grade BBB-INVESTMENT HIGHLIGHTS Launched Share Repurchase Program: Repurchased 10.2 million shares for a total of $77 million, taking advantage of the compelling opportunity to buy back shares at an AFFO yield of approximately 12% Strengthened Balance Sheet: Since Q2’24, reduced net debt by $2 billion and improved Net Debt to Adjusted EBITDA(3) from 8.1x to 6.6x Single-Tenant Focused: Pure-play net lease REIT with best-in-class portfolio of single-tenant assets 1. Liquidity represents cash, cash equivalents and borrowing availability under our recently refinanced Revolving Credit Facility, utilizing the value of our applicable assets as of June 30, 2025 for the borrowing base calculation and the June 30, 2025 existing Revolver balance. 2. Subsequent to Q2 2025, GNL refinanced its Revolving Credit Facility, which has aggregate total commitments of approximately $1.8 billion and matures in August 2029, with two 6-month extension options. For purposes of calculating the above weighted average debt maturity, the Company utilized the June 30, 2025 Revolving Credit Facility balance and assumed the full four-year term along with the exercise of both 6-month extension options under the terms of the refinanced Facility. 3. See Appendix for definitions of Core FFO, AFFO, Adjusted EBITDA, NOI and Cash NOI reconciliation to the most comparable GAAP measures. |

| 5 STRATEGIC BENEFITS OF THE COMPLETED MULTI-TENANT PORTFOLIO SALE The successful completion of the Multi-Tenant Portfolio Sale in Q2 2025 accelerated GNL’s progress on debt reduction and strengthened its foundation for anticipated future growth Transformed GNL into a Pure-Play Net Lease REIT 1 Simplified Operations and Enhanced Portfolio Metrics 2 Significantly Reduced Leverage and Improved Liquidity Position 3 Positions GNL well for Long-Term Growth 4 |

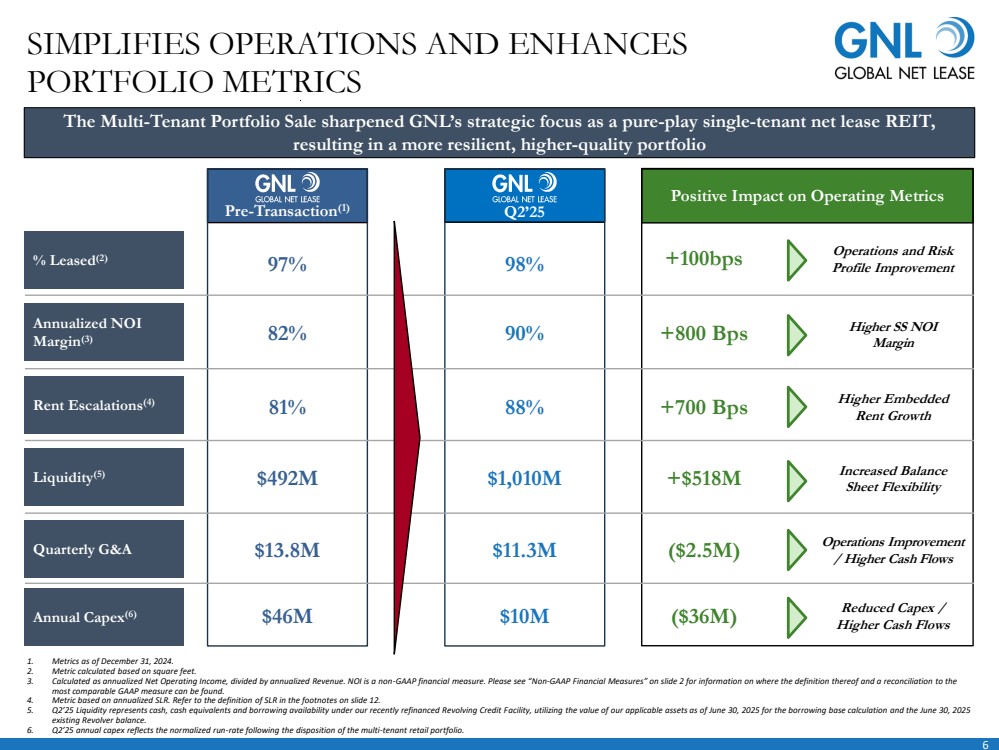

| Operations Improvement / Higher Cash Flows Increased Balance Sheet Flexibility Positive Impact on Operating Metrics % Leased(2) 97% 98% Operations and Risk Profile Improvement Annualized NOI Margin(3) 82% 90% Higher SS NOI Margin Rent Escalations(4) 81% 88% Higher Embedded Rent Growth Liquidity(5) $492M $1,010M Quarterly G&A $13.8M $11.3M Annual Capex(6) $46M $10M Reduced Capex / Higher Cash Flows Pre-Transaction(1) SIMPLIFIES OPERATIONS AND ENHANCES PORTFOLIO METRICS 1. Metrics as of December 31, 2024. 2. Metric calculated based on square feet. 3. Calculated as annualized Net Operating Income, divided by annualized Revenue. NOI is a non-GAAP financial measure. Please see “Non-GAAP Financial Measures” on slide 2 for information on where the definition thereof and a reconciliation to the most comparable GAAP measure can be found. 4. Metric based on annualized SLR. Refer to the definition of SLR in the footnotes on slide 12. 5. Q2’25 Liquidity represents cash, cash equivalents and borrowing availability under our recently refinanced Revolving Credit Facility, utilizing the value of our applicable assets as of June 30, 2025 for the borrowing base calculation and the June 30, 2025 existing Revolver balance. 6. Q2’25 annual capex reflects the normalized run-rate following the disposition of the multi-tenant retail portfolio. Q2’25 +100bps +800 Bps +700 Bps +$518M ($2.5M) ($36M) The Multi-Tenant Portfolio Sale sharpened GNL’s strategic focus as a pure-play single-tenant net lease REIT, resulting in a more resilient, higher-quality portfolio 6 |

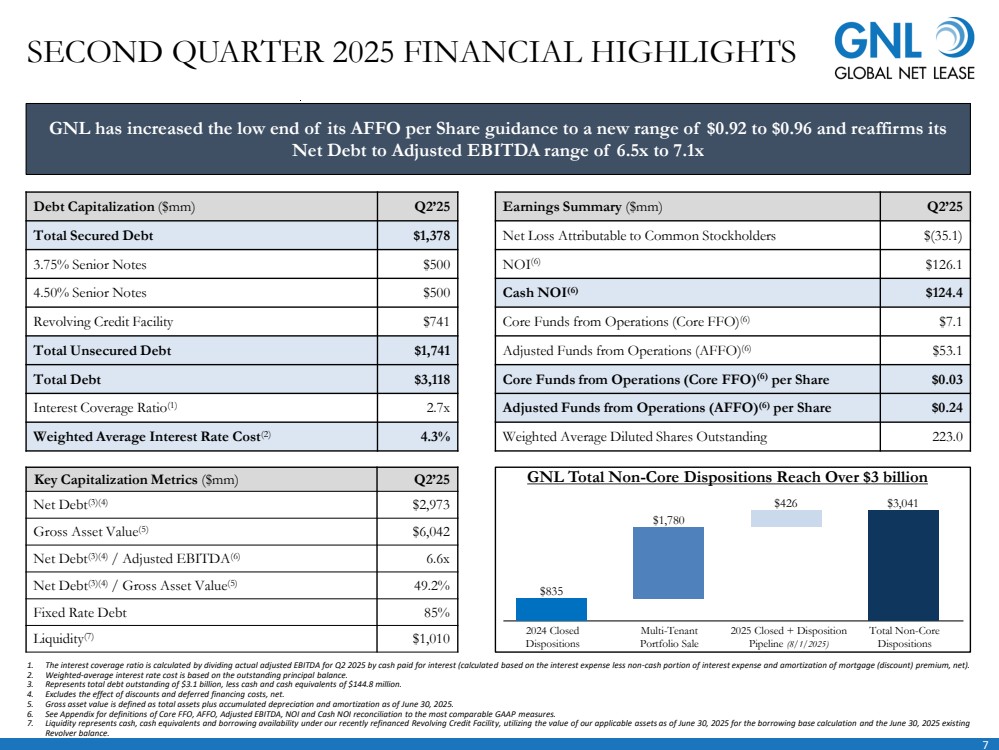

| 7 Earnings Summary ($mm) Q2’25 Net Loss Attributable to Common Stockholders $(35.1) NOI(6) $126.1 Cash NOI(6) $124.4 Core Funds from Operations (Core FFO)(6) $7.1 Adjusted Funds from Operations (AFFO) (6) $53.1 Core Funds from Operations (Core FFO)(6) per Share $0.03 Adjusted Funds from Operations (AFFO)(6) per Share $0.24 Weighted Average Diluted Shares Outstanding 223.0 SECOND QUARTER 2025 FINANCIAL HIGHLIGHTS Key Capitalization Metrics ($mm) Q2’25 Net Debt(3)(4) $2,973 Gross Asset Value(5) $6,042 Net Debt(3)(4) / Adjusted EBITDA(6) 6.6x Net Debt(3)(4) / Gross Asset Value(5) 49.2% Fixed Rate Debt 85% Liquidity(7) $1,010 Debt Capitalization ($mm) Q2’25 Total Secured Debt $1,378 3.75% Senior Notes $500 4.50% Senior Notes $500 Revolving Credit Facility $741 Total Unsecured Debt $1,741 Total Debt $3,118 Interest Coverage Ratio(1) 2.7x Weighted Average Interest Rate Cost(2) 4.3% GNL has increased the low end of its AFFO per Share guidance to a new range of $0.92 to $0.96 and reaffirms its Net Debt to Adjusted EBITDA range of 6.5x to 7.1x 1. The interest coverage ratio is calculated by dividing actual adjusted EBITDA for Q2 2025 by cash paid for interest (calculated based on the interest expense less non-cash portion of interest expense and amortization of mortgage (discount) premium, net). 2. Weighted-average interest rate cost is based on the outstanding principal balance. 3. Represents total debt outstanding of $3.1 billion, less cash and cash equivalents of $144.8 million. 4. Excludes the effect of discounts and deferred financing costs, net. 5. Gross asset value is defined as total assets plus accumulated depreciation and amortization as of June 30, 2025. 6. See Appendix for definitions of Core FFO, AFFO, Adjusted EBITDA, NOI and Cash NOI reconciliation to the most comparable GAAP measures. 7. Liquidity represents cash, cash equivalents and borrowing availability under our recently refinanced Revolving Credit Facility, utilizing the value of our applicable assets as of June 30, 2025 for the borrowing base calculation and the June 30, 2025 existing Revolver balance. 2024 Closed Dispositions Total Non-Core Dispositions Multi-Tenant Portfolio Sale 2025 Closed + Disposition Pipeline (8/1/2025) GNL Total Non-Core Dispositions Reach Over $3 billion $835 $1,780 $426 $3,041 |

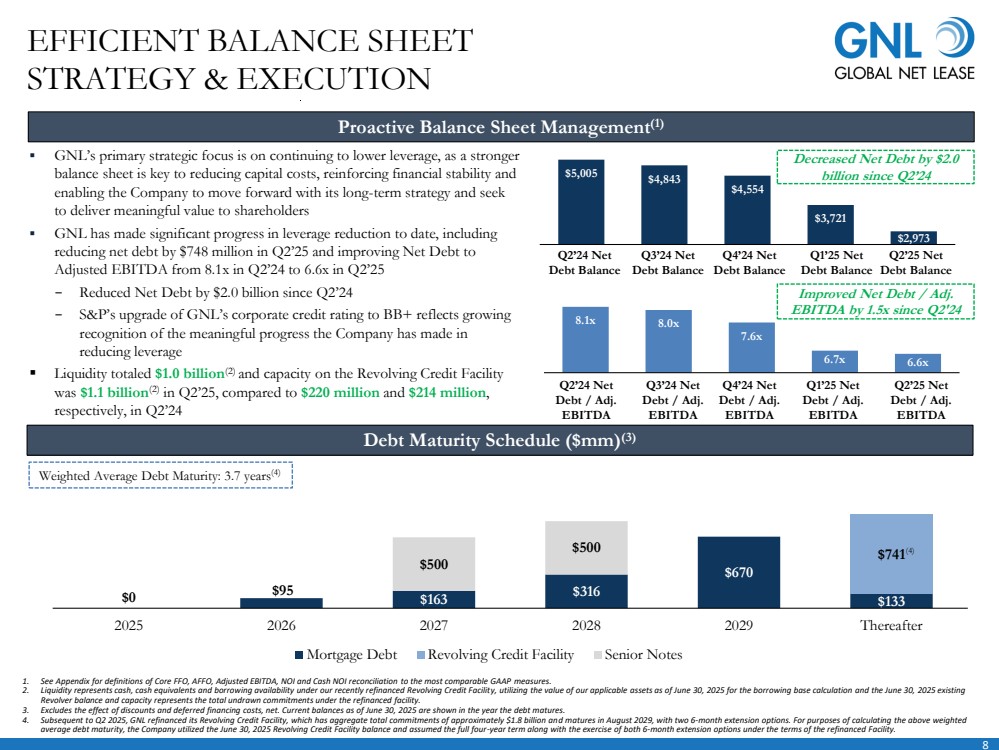

| 8 $0 $95 $163 $316 $670 $133 $741 $500 $500 2025 2026 2027 2028 2029 Thereafter Mortgage Debt Revolving Credit Facility Senior Notes 8.1x 8.0x 7.6x 6.7x 6.6x $5,005 $4,843 $4,554 $3,721 $2,973 ▪ GNL’s primary strategic focus is on continuing to lower leverage, as a stronger balance sheet is key to reducing capital costs, reinforcing financial stability and enabling the Company to move forward with its long-term strategy and seek to deliver meaningful value to shareholders ▪ GNL has made significant progress in leverage reduction to date, including reducing net debt by $748 million in Q2’25 and improving Net Debt to Adjusted EBITDA from 8.1x in Q2’24 to 6.6x in Q2’25 − Reduced Net Debt by $2.0 billion since Q2’24 − S&P’s upgrade of GNL’s corporate credit rating to BB+ reflects growing recognition of the meaningful progress the Company has made in reducing leverage ▪ Liquidity totaled $1.0 billion(2) and capacity on the Revolving Credit Facility was $1.1 billion(2) in Q2’25, compared to $220 million and $214 million, respectively, in Q2’24 EFFICIENT BALANCE SHEET STRATEGY & EXECUTION Debt Maturity Schedule ($mm) (3) 1. See Appendix for definitions of Core FFO, AFFO, Adjusted EBITDA, NOI and Cash NOI reconciliation to the most comparable GAAP measures. 2. Liquidity represents cash, cash equivalents and borrowing availability under our recently refinanced Revolving Credit Facility, utilizing the value of our applicable assets as of June 30, 2025 for the borrowing base calculation and the June 30, 2025 existing Revolver balance and capacity represents the total undrawn commitments under the refinanced facility. 3. Excludes the effect of discounts and deferred financing costs, net. Current balances as of June 30, 2025 are shown in the year the debt matures. 4. Subsequent to Q2 2025, GNL refinanced its Revolving Credit Facility, which has aggregate total commitments of approximately $1.8 billion and matures in August 2029, with two 6-month extension options. For purposes of calculating the above weighted average debt maturity, the Company utilized the June 30, 2025 Revolving Credit Facility balance and assumed the full four-year term along with the exercise of both 6-month extension options under the terms of the refinanced Facility. Weighted Average Debt Maturity: 3.7 years(4) Q3’24 Net Debt Balance Q2’24 Net Debt Balance Q4’24 Net Debt Balance Q1’25 Net Debt Balance Decreased Net Debt by $2.0 billion since Q2’24 Proactive Balance Sheet Management(1) Q2’25 Net Debt Balance Q2’24 Net Debt / Adj. EBITDA Q3’24 Net Debt / Adj. EBITDA Q4’24 Net Debt / Adj. EBITDA Q1’25 Net Debt / Adj. EBITDA Q2’25 Net Debt / Adj. EBITDA Improved Net Debt / Adj. EBITDA by 1.5x since Q2'24 (4) |

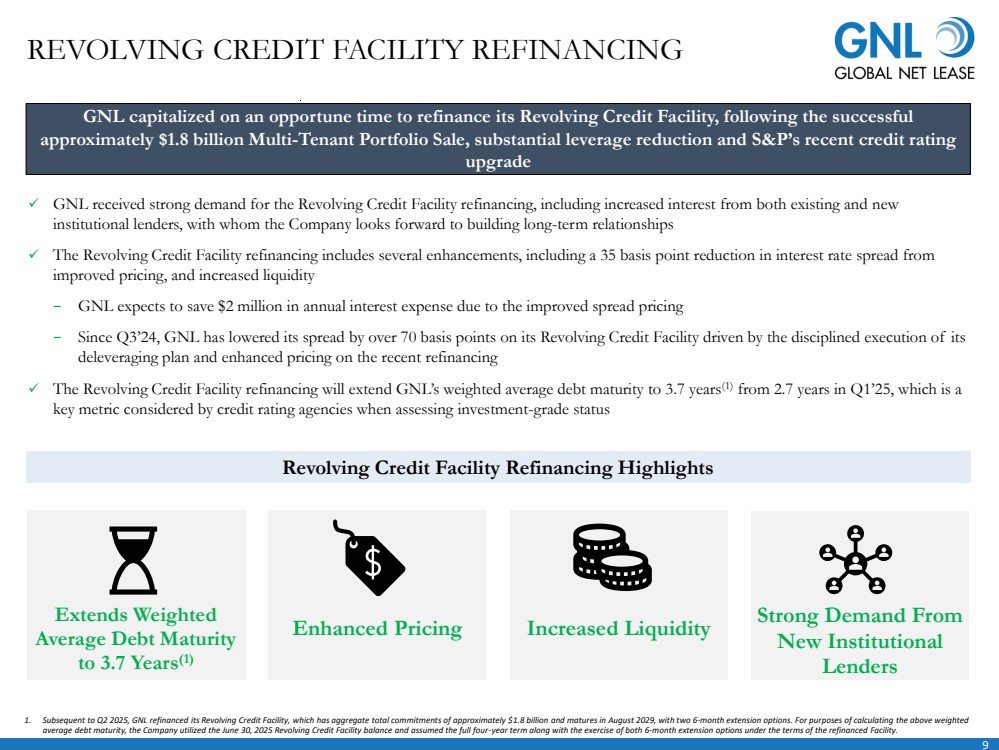

| 9 REVOLVING CREDIT FACILITY REFINANCING Extends Weighted Average Debt Maturity to 3.7 Years(1) Enhanced Pricing Strong Demand From New Institutional Lenders Increased Liquidity ✓ GNL received strong demand for the Revolving Credit Facility refinancing, including increased interest from both existing and new institutional lenders, with whom the Company looks forward to building long-term relationships ✓ The Revolving Credit Facility refinancing includes several enhancements, including a 35 basis point reduction in interest rate spread from improved pricing, and increased liquidity − GNL expects to save $2 million in annual interest expense due to the improved spread pricing − Since Q3’24, GNL has lowered its spread by over 70 basis points on its Revolving Credit Facility driven by the disciplined execution of its deleveraging plan and enhanced pricing on the recent refinancing ✓ The Revolving Credit Facility refinancing will extend GNL’s weighted average debt maturity to 3.7 years(1) from 2.7 years in Q1’25, which is a key metric considered by credit rating agencies when assessing investment-grade status GNL capitalized on an opportune time to refinance its Revolving Credit Facility, following the successful approximately $1.8 billion Multi-Tenant Portfolio Sale, substantial leverage reduction and S&P’s recent credit rating upgrade 1. Subsequent to Q2 2025, GNL refinanced its Revolving Credit Facility, which has aggregate total commitments of approximately $1.8 billion and matures in August 2029, with two 6-month extension options. For purposes of calculating the above weighted average debt maturity, the Company utilized the June 30, 2025 Revolving Credit Facility balance and assumed the full four-year term along with the exercise of both 6-month extension options under the terms of the refinanced Facility. Revolving Credit Facility Refinancing Highlights |

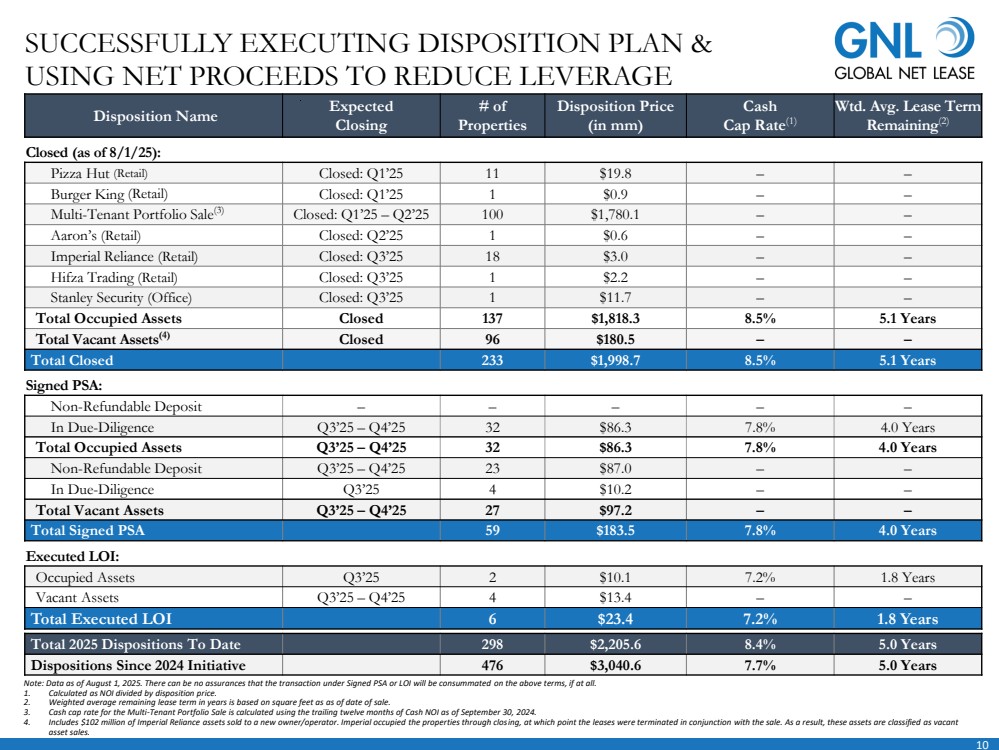

| 10 Disposition Name Expected Closing # of Properties Disposition Price (in mm) Cash Cap Rate(1) Wtd. Avg. Lease Term Remaining(2) Closed (as of 8/1/25): Pizza Hut (Retail) Closed: Q1’25 11 $19.8 – – Burger King (Retail) Closed: Q1’25 1 $0.9 – – Multi-Tenant Portfolio Sale(3) Closed: Q1’25 – Q2’25 100 $1,780.1 – – Aaron’s (Retail) Closed: Q2’25 1 $0.6 – – Imperial Reliance (Retail) Closed: Q3’25 18 $3.0 – – Hifza Trading (Retail) Closed: Q3’25 1 $2.2 – – Stanley Security (Office) Closed: Q3’25 1 $11.7 – – Total Occupied Assets Closed 137 $1,818.3 8.5% 5.1 Years Total Vacant Assets(4) Closed 96 $180.5 – – Total Closed 233 $1,998.7 8.5% 5.1 Years Signed PSA: Non-Refundable Deposit – – – – – In Due-Diligence Q3’25 – Q4’25 32 $86.3 7.8% 4.0 Years Total Occupied Assets Q3’25 – Q4’25 32 $86.3 7.8% 4.0 Years Non-Refundable Deposit Q3’25 – Q4’25 23 $87.0 – – In Due-Diligence Q3’25 4 $10.2 – – Total Vacant Assets Q3’25 – Q4’25 27 $97.2 – – Total Signed PSA 59 $183.5 7.8% 4.0 Years Executed LOI: Occupied Assets Q3’25 2 $10.1 7.2% 1.8 Years Vacant Assets Q3’25 – Q4’25 4 $13.4 – – Total Executed LOI 6 $23.4 7.2% 1.8 Years Total 2025 Dispositions To Date 298 $2,205.6 8.4% 5.0 Years Dispositions Since 2024 Initiative 476 $3,040.6 7.7% 5.0 Years Note: Data as of August 1, 2025. There can be no assurances that the transaction under Signed PSA or LOI will be consummated on the above terms, if at all. 1. Calculated as NOI divided by disposition price. 2. Weighted average remaining lease term in years is based on square feet as as of date of sale. 3. Cash cap rate for the Multi-Tenant Portfolio Sale is calculated using the trailing twelve months of Cash NOI as of September 30, 2024. 4. Includes $102 million of Imperial Reliance assets sold to a new owner/operator. Imperial occupied the properties through closing, at which point the leases were terminated in conjunction with the sale. As a result, these assets are classified as vacant asset sales. SUCCESSFULLY EXECUTING DISPOSITION PLAN & USING NET PROCEEDS TO REDUCE LEVERAGE |

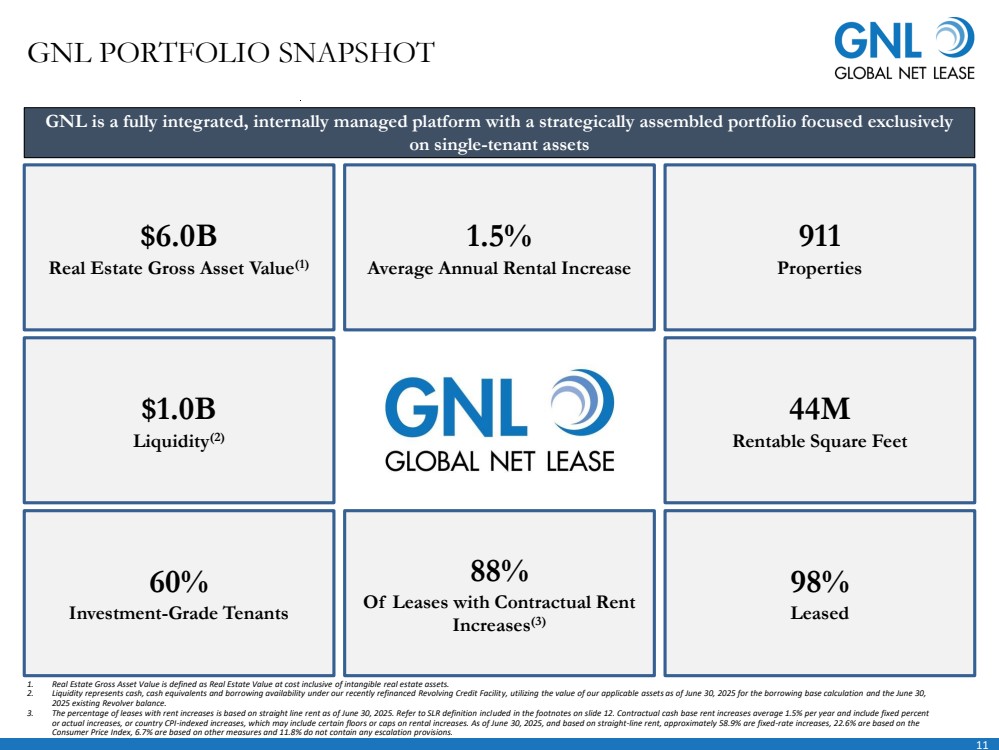

| $6.0B Real Estate Gross Asset Value(1) 1.5% Average Annual Rental Increase 911 Properties 98% Leased 44M Rentable Square Feet $1.0B Liquidity(2) 60% Investment-Grade Tenants 88% Of Leases with Contractual Rent Increases(3) GNL PORTFOLIO SNAPSHOT 1. Real Estate Gross Asset Value is defined as Real Estate Value at cost inclusive of intangible real estate assets. 2. Liquidity represents cash, cash equivalents and borrowing availability under our recently refinanced Revolving Credit Facility, utilizing the value of our applicable assets as of June 30, 2025 for the borrowing base calculation and the June 30, 2025 existing Revolver balance. 3. The percentage of leases with rent increases is based on straight line rent as of June 30, 2025. Refer to SLR definition included in the footnotes on slide 12. Contractual cash base rent increases average 1.5% per year and include fixed percent or actual increases, or country CPI-indexed increases, which may include certain floors or caps on rental increases. As of June 30, 2025, and based on straight-line rent, approximately 58.9% are fixed-rate increases, 22.6% are based on the Consumer Price Index, 6.7% are based on other measures and 11.8% do not contain any escalation provisions. GNL is a fully integrated, internally managed platform with a strategically assembled portfolio focused exclusively on single-tenant assets 11 |

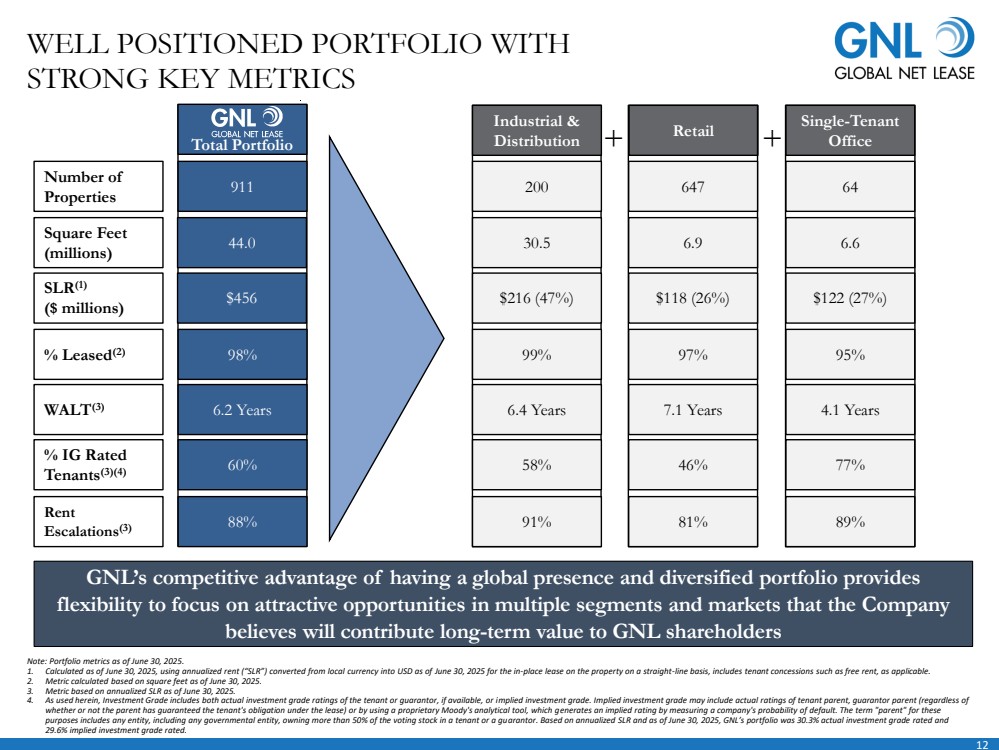

| 12 Retail WELL POSITIONED PORTFOLIO WITH STRONG KEY METRICS Note: Portfolio metrics as of June 30, 2025. 1. Calculated as of June 30, 2025, using annualized rent (“SLR”) converted from local currency into USD as of June 30, 2025 for the in-place lease on the property on a straight-line basis, includes tenant concessions such as free rent, as applicable. 2. Metric calculated based on square feet as of June 30, 2025. 3. Metric based on annualized SLR as of June 30, 2025. 4. As used herein, Investment Grade includes both actual investment grade ratings of the tenant or guarantor, if available, or implied investment grade. Implied investment grade may include actual ratings of tenant parent, guarantor parent (regardless of whether or not the parent has guaranteed the tenant's obligation under the lease) or by using a proprietary Moody's analytical tool, which generates an implied rating by measuring a company's probability of default. The term "parent" for these purposes includes any entity, including any governmental entity, owning more than 50% of the voting stock in a tenant or a guarantor. Based on annualized SLR and as of June 30, 2025, GNL’s portfolio was 30.3% actual investment grade rated and 29.6% implied investment grade rated. + Number of Properties Square Feet (millions) SLR(1) ($ millions) % Leased(2) WALT(3) % IG Rated Tenants(3)(4) + Industrial & Distribution 200 30.5 $216 (47%) 99% 6.4 Years 58% 647 6.9 $118 (26%) 97% 7.1 Years 46% Single-Tenant Office 64 6.6 $122 (27%) 95% 4.1 Years 77% Total Portfolio 911 44.0 $456 98% 6.2 Years 60% Rent Escalations(3) 88% 91% 81% 89% GNL’s competitive advantage of having a global presence and diversified portfolio provides flexibility to focus on attractive opportunities in multiple segments and markets that the Company believes will contribute long-term value to GNL shareholders |

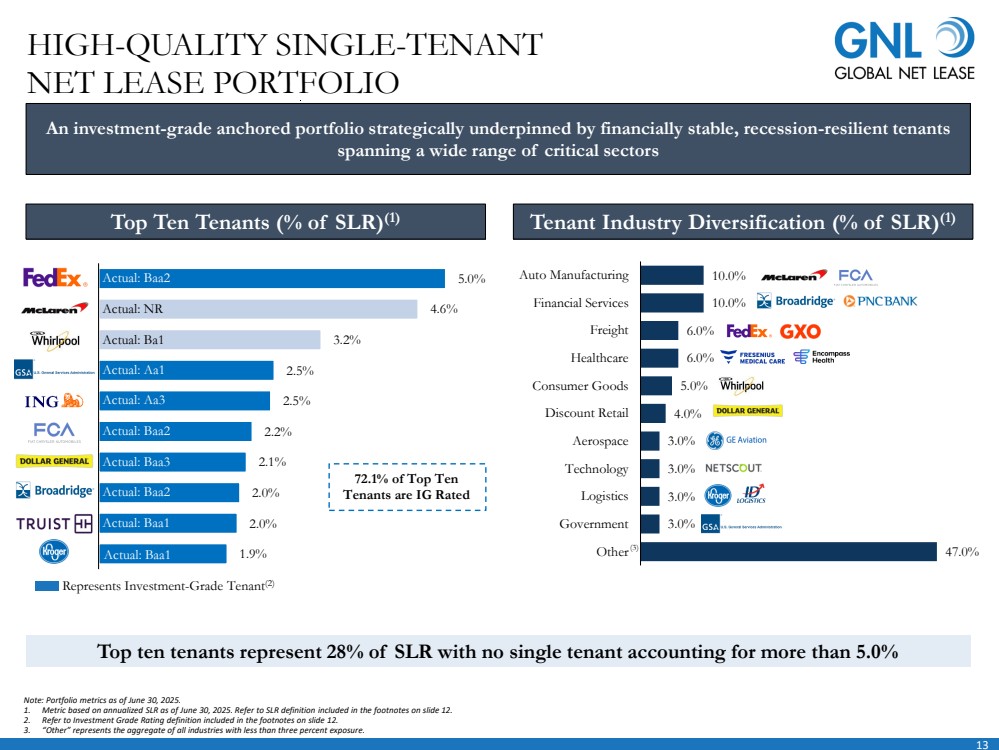

| 13 47.0% 3.0% 3.0% 3.0% 3.0% 4.0% 5.0% 6.0% 6.0% 10.0% 10.0% Other Government Logistics Technology Aerospace Discount Retail Consumer Goods Healthcare Freight Financial Services Auto Manufacturing 1.9% 2.0% 2.0% 2.1% 2.2% 2.5% 2.5% 3.2% 4.6% 5.0% Tenant Industry Diversification (% of SLR) Top Ten Tenants (1) (% of SLR)(1) Note: Portfolio metrics as of June 30, 2025. 1. Metric based on annualized SLR as of June 30, 2025. Refer to SLR definition included in the footnotes on slide 12. 2. Refer to Investment Grade Rating definition included in the footnotes on slide 12. 3. “Other” represents the aggregate of all industries with less than three percent exposure. HIGH-QUALITY SINGLE-TENANT NET LEASE PORTFOLIO (3) An investment-grade anchored portfolio strategically underpinned by financially stable, recession-resilient tenants spanning a wide range of critical sectors Top ten tenants represent 28% of SLR with no single tenant accounting for more than 5.0% Actual: Baa2 Actual: NR Actual: Ba1 Actual: Aa1 Actual: Aa3 Actual: Baa2 Actual: Baa3 Actual: Baa2 Actual: Baa1 Actual: Baa1 Represents Investment-Grade Tenant(2) 72.1% of Top Ten Tenants are IG Rated |

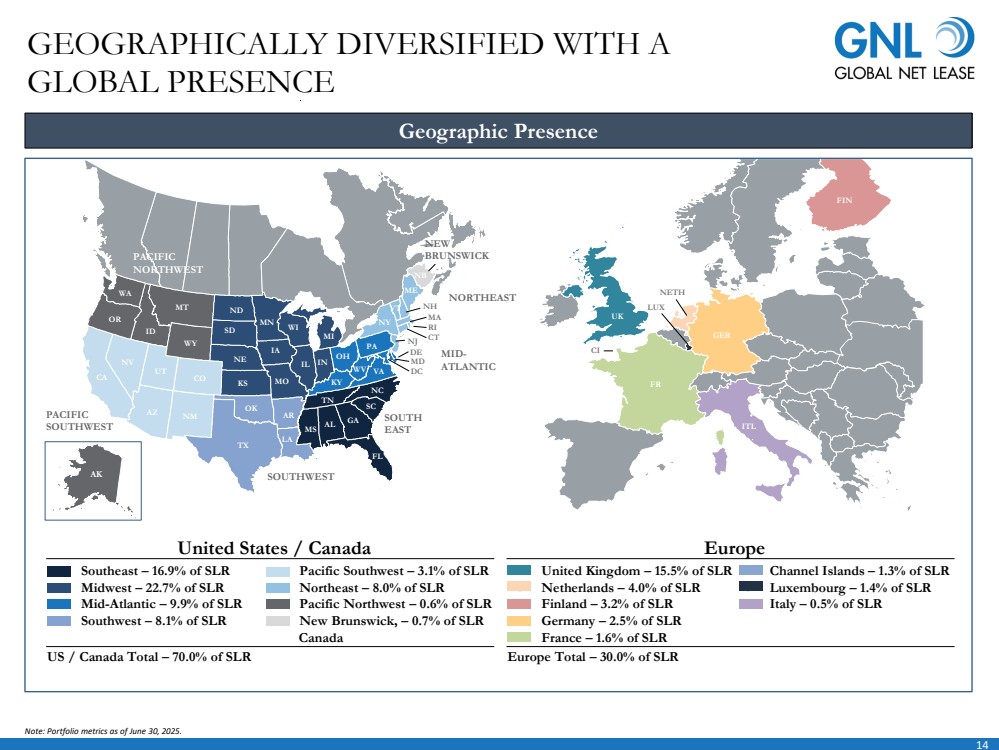

| 14 MIDWEST NC FL GA AL MS LA TX NM AZ CA NV UT OR WA ID MT WY CO ND SD NE KS OK AR MO IA MN WI MI IL IN OH KY TN SC NC WV VA PA NY VT NH ME MA NJ CT MD DE DC RI NB PACIFIC SOUTHWEST SOUTHWEST MID-ATLANTIC NEW PACIFIC BRUNSWICK NORTHWEST SOUTH EAST AK NORTHEAST GEOGRAPHICALLY DIVERSIFIED WITH A GLOBAL PRESENCE Geographic Presence Note: Portfolio metrics as of June 30, 2025. FR UK ITL GER LUX NETH FIN CI United States / Canada US / Canada Total – 70.0% of SLR ⚫ Southeast – 16.9% of SLR ⚫ Midwest – 22.7% of SLR ⚫ Mid-Atlantic – 9.9% of SLR ⚫ Southwest – 8.1% of SLR ⚫ Pacific Southwest – 3.1% of SLR ⚫ Northeast – 8.0% of SLR ⚫ Pacific Northwest – 0.6% of SLR ⚫ New Brunswick, – 0.7% of SLR Canada Europe Europe Total – 30.0% of SLR ⚫ United Kingdom – 15.5% of SLR ⚫ Netherlands – 4.0% of SLR ⚫ Finland – 3.2% of SLR ⚫ Germany – 2.5% of SLR ⚫ France – 1.6% of SLR ⚫ Channel Islands – 1.3% of SLR ⚫ Luxembourg – 1.4% of SLR ⚫ Italy – 0.5% of SLR |

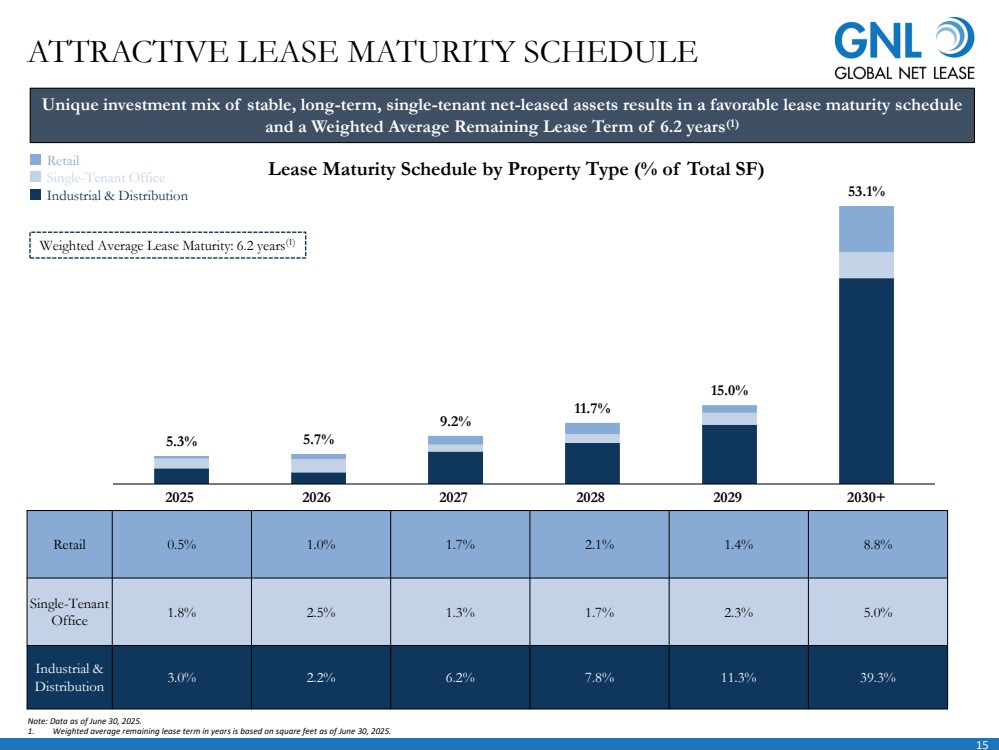

| 15 5.3% 5.7% 9.2% 11.7% 15.0% 53.1% 2025 2026 2027 2028 2029 2030+ Lease Maturity Schedule by Property Type (% of Total SF) ATTRACTIVE LEASE MATURITY SCHEDULE Unique investment mix of stable, long-term, single-tenant net-leased assets results in a favorable lease maturity schedule and a Weighted Average Remaining Lease Term of 6.2 years(1) Note: Data as of June 30, 2025. 1. Weighted average remaining lease term in years is based on square feet as of June 30, 2025. Retail 0.5% 1.0% 1.7% 2.1% 1.4% 8.8% Single-Tenant Office 1.8% 2.5% 1.3% 1.7% 2.3% 5.0% Industrial & Distribution 3.0% 2.2% 6.2% 7.8% 11.3% 39.3% Retail Single-Tenant Office Industrial & Distribution Weighted Average Lease Maturity: 6.2 years(1) |

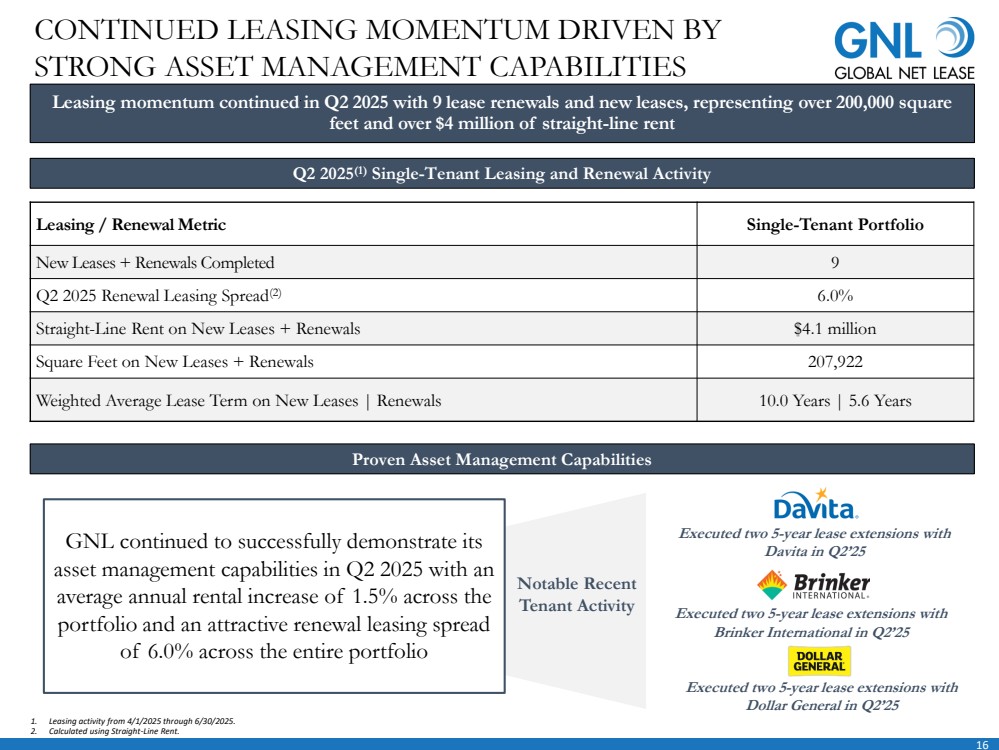

| 16 Leasing momentum continued in Q2 2025 with 9 lease renewals and new leases, representing over 200,000 square feet and over $4 million of straight-line rent Q2 2025(1) Single-Tenant Leasing and Renewal Activity Leasing / Renewal Metric Single-Tenant Portfolio New Leases + Renewals Completed 9 Q2 2025 Renewal Leasing Spread(2) 6.0% Straight-Line Rent on New Leases + Renewals $4.1 million Square Feet on New Leases + Renewals 207,922 Weighted Average Lease Term on New Leases | Renewals 10.0 Years | 5.6 Years 1. Leasing activity from 4/1/2025 through 6/30/2025. 2. Calculated using Straight-Line Rent. CONTINUED LEASING MOMENTUM DRIVEN BY STRONG ASSET MANAGEMENT CAPABILITIES Proven Asset Management Capabilities GNL continued to successfully demonstrate its asset management capabilities in Q2 2025 with an average annual rental increase of 1.5% across the portfolio and an attractive renewal leasing spread of 6.0% across the entire portfolio Notable Recent Tenant Activity Executed two 5-year lease extensions with Dollar General in Q2’25 Executed two 5-year lease extensions with Davita in Q2’25 Executed two 5-year lease extensions with Brinker International in Q2’25 |

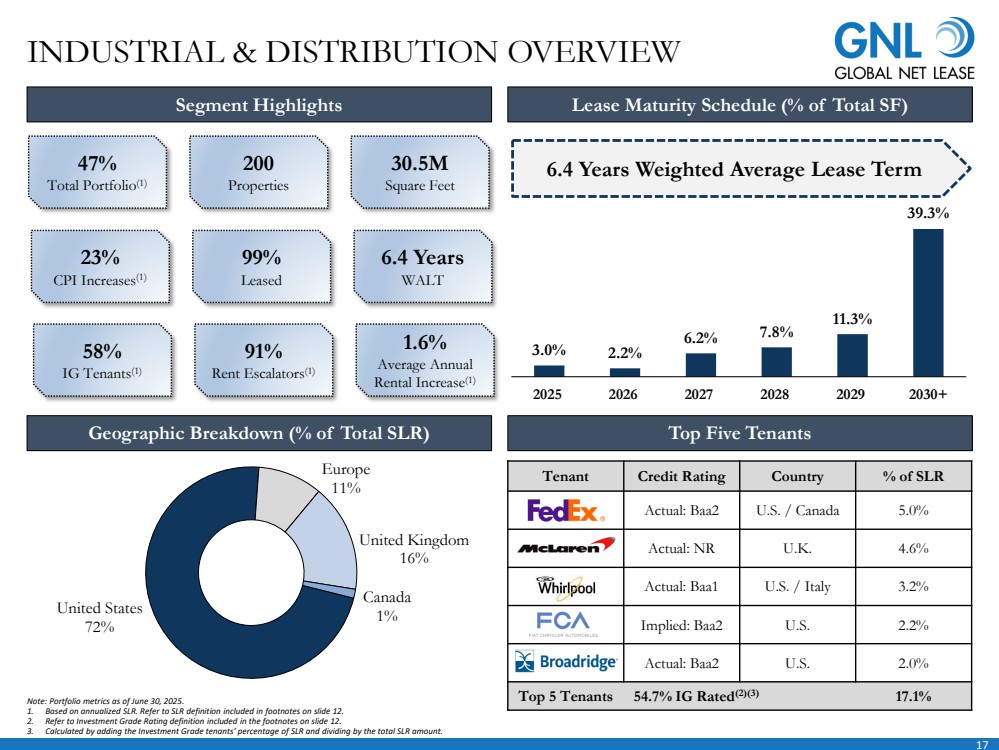

| 17 3.0% 2.2% 6.2% 7.8% 11.3% 39.3% 2025 2026 2027 2028 2029 2030+ United States 72% Europe 11% United Kingdom 16% Canada 1% Tenant Credit Rating Country % of SLR Actual: Baa2 U.S. / Canada 5.0% Actual: NR U.K. 4.6% Actual: Baa1 U.S. / Italy 3.2% Implied: Baa2 U.S. 2.2% Actual: Baa2 U.S. 2.0% Top 5 Tenants 54.7% IG Rated(2)(3) 17.1% Segment Highlights Lease Maturity Schedule (% of Total SF) Geographic Breakdown (% of Total SLR) Top Five Tenants 47% Total Portfolio(1) 200 Properties 30.5M Square Feet 23% CPI Increases(1) 99% Leased 6.4 Years WALT 58% IG Tenants(1) 91% Rent Escalators(1) 1.6% Average Annual Rental Increase(1) Note: Portfolio metrics as of June 30, 2025. 1. Based on annualized SLR. Refer to SLR definition included in footnotes on slide 12. 2. Refer to Investment Grade Rating definition included in the footnotes on slide 12. 3. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount. INDUSTRIAL & DISTRIBUTION OVERVIEW 6.4 Years Weighted Average Lease Term |

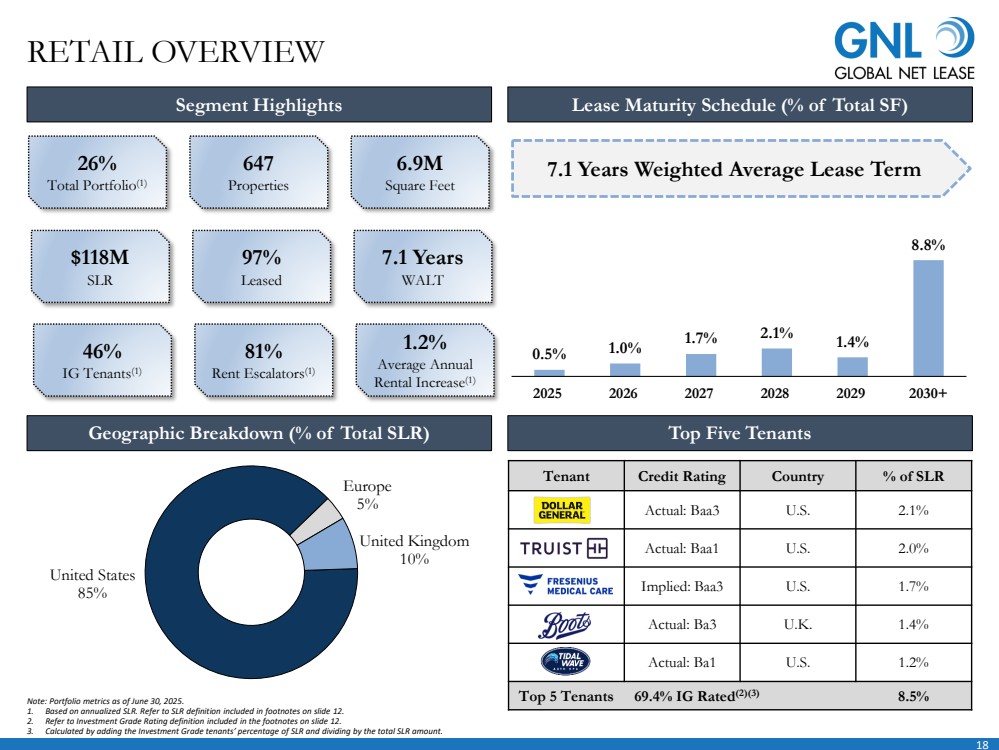

| 18 0.5% 1.0% 1.7% 2.1% 1.4% 8.8% 2025 2026 2027 2028 2029 2030+ United States 85% Europe 5% United Kingdom 10% RETAIL OVERVIEW Tenant Credit Rating Country % of SLR Actual: Baa3 U.S. 2.1% Actual: Baa1 U.S. 2.0% Implied: Baa3 U.S. 1.7% Actual: Ba3 U.K. 1.4% Actual: Ba1 U.S. 1.2% Top 5 Tenants 69.4% IG Rated(2)(3) 8.5% Segment Highlights Lease Maturity Schedule (% of Total SF) Geographic Breakdown (% of Total SLR) Top Five Tenants 26% Total Portfolio(1) 647 Properties 6.9M Square Feet $118M SLR 97% Leased 7.1 Years WALT 46% IG Tenants(1) 81% Rent Escalators(1) 1.2% Average Annual Rental Increase(1) Note: Portfolio metrics as of June 30, 2025. 1. Based on annualized SLR. Refer to SLR definition included in footnotes on slide 12. 2. Refer to Investment Grade Rating definition included in the footnotes on slide 12. 3. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount. 7.1 Years Weighted Average Lease Term |

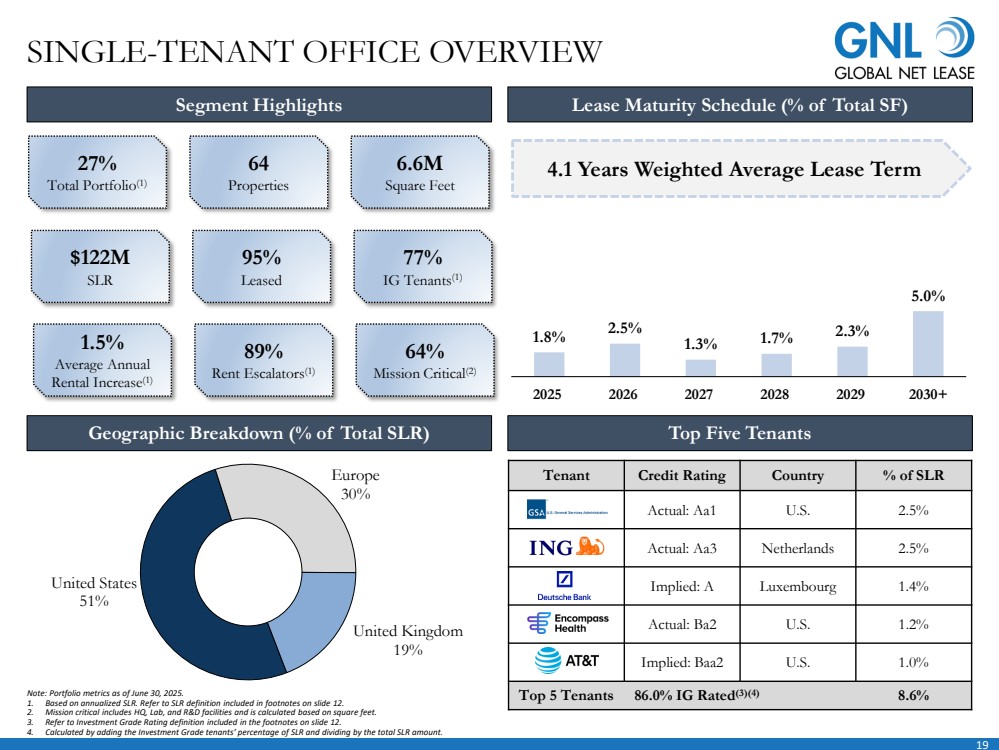

| 19 United States 51% Europe 30% United Kingdom 19% SINGLE-TENANT OFFICE OVERVIEW Tenant Credit Rating Country % of SLR Actual: Aa1 U.S. 2.5% Actual: Aa3 Netherlands 2.5% Implied: A Luxembourg 1.4% Actual: Ba2 U.S. 1.2% Implied: Baa2 U.S. 1.0% Top 5 Tenants 86.0% IG Rated(3)(4) 8.6% Segment Highlights Lease Maturity Schedule (% of Total SF) 27% Total Portfolio(1) 64 Properties 6.6M Square Feet $122M SLR 95% Leased 77% IG Tenants(1) 1.5% Average Annual Rental Increase(1) 89% Rent Escalators(1) 64% Mission Critical(2) Geographic Breakdown (% of Total SLR) Top Five Tenants Note: Portfolio metrics as of June 30, 2025. 1. Based on annualized SLR. Refer to SLR definition included in footnotes on slide 12. 2. Mission critical includes HQ, Lab, and R&D facilities and is calculated based on square feet. 3. Refer to Investment Grade Rating definition included in the footnotes on slide 12. 4. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount. 4.1 Years Weighted Average Lease Term 1.8% 2.5% 1.3% 1.7% 2.3% 5.0% 2025 2026 2027 2028 2029 2030+ |

| 20 LEADERSHIP OVERVIEW Management Board of Directors Michael Weil, Director Refer to “Management” section for Michael Weil’s biography Michael Weil, Chief Executive Officer & President Previously served as CEO of The Necessity Retail REIT Member of the Board of Directors of Global Net Lease, Inc. since 2012 Served as President of the Board of Directors of the Real Estate Investment Securities Association Chris Masterson, Chief Financial Officer Previously served as Chief Accounting Officer of GNL Past experience includes accounting positions with Goldman Sachs and KPMG Edward Rendell, Independent Director Previously served as the 45th Governor of the Commonwealth of Pennsylvania and as the Mayor of Philadelphia, and previously served as a member of the board of directors of The Necessity Retail REIT Lisa Kabnick, Independent Director Retired Partner at Troutman Pepper Hamilton Sanders LLP, and previously served as a member of the board of directors of The Necessity Retail REIT Therese Antone, Independent Director Currently serves as the Chancellor of Salve Regina University since her appointment in 2009 Leslie Michelson, Independent Director Currently serves as lead independent director of Franklin BSP Franklin Lending Corporation, and previously served as a member of the board of directors of The Necessity Retail REIT Stanley Perla, Independent Director Previously served as a member of the board of directors and the chair of the audit committee of Madison Harbor Balanced Strategies, Inc, and previously served as a member of the board of directors of The Necessity Retail REIT Directors Jesse Galloway, Executive Vice President & General Counsel Joined GNL in September 2023 25 years of legal experience representing large real estate companies and financial institutions, including 10 years as General Counsel and 15 years in private practice Jason Slear, Executive Vice President Responsible for sourcing, negotiating, and closing GNL’s real estate acquisitions and dispositions Oversaw the acquisition of over $3.5 billion of real estate assets and the lease-up of over 10 million square feet during professional career Ori Kravel, Chief Operating Officer Responsible for corporate development and business strategy Executed over $12 billion of capital market transactions and over $25 billion of M&A transactions Rob Kauffman, Non-Executive Chairperson of the Board of Directors Co-founder of Fortress Investment Group and previously worked as a Managing Director at UBS, a Principal at BlackRock Financial and at Lehman Brothers Michael J.U. Monahan, Independent Director Currently serves as a CBRE Vice Chair and previously served as a Senior Director at Jones Lang Wootton and a Vice President at Cushman & Wakefield Leon Richardson, Independent Director Founder, President and Chief Operating Officer of The Chemico Group, one of the largest minority-owned chemical management and distribution companies in the US Sue Perrotty, Independent Director Previously served as President and Chief Executive Officer of AFM Financial Services and Tower Health |

| 21 APPENDIX: FINANCIAL DEFINITIONS Non-GAAP Financial Measures This section discusses non-GAAP financial measures we use to evaluate our performance, including Funds from Operations (“FFO”), Core Funds from Operations (“Core FFO”), Adjusted Funds from Operations (“AFFO”), Adjusted Earnings before Interest, Taxes, Depreciation and Amortization (“Adjusted EBITDA”), Net Operating Income (“NOI”), Cash Net Operating Income (“Cash NOI”) and Cash Paid for Interest. While NOI is a property-level measure, AFFO is based on total Company performance and therefore reflects the impact of other items not specifically associated with NOI such as, interest expense, general and administrative expenses and operating fees to related parties. Additionally, NOI as defined herein, does not reflect an adjustment for straight-line rent but AFFO does include this adjustment. A description of these non-GAAP measures and reconciliations to the most directly comparable GAAP measure, which is net income, is provided below. Caution on Use of Non-GAAP Measures FFO, Core FFO, AFFO, Adjusted EBITDA, NOI, Cash NOI and Cash Paid for Interest should not be construed to be more relevant or accurate than the current GAAP methodology in calculating net income or in its applicability in evaluating our operating performance. The method utilized to evaluate the value and performance of real estate under GAAP should be construed as a more relevant measure of operational performance and considered more prominently than the non-GAAP measures. Other REITs may not define FFO in accordance with the current National Association of Real Estate Investment Trusts (“NAREIT”) definition (as we do), or may interpret the current NAREIT definition differently than we do, or may calculate Core FFO or AFFO differently than we do. Consequently, our presentation of FFO, Core FFO and AFFO may not be comparable to other similarly-titled measures presented by other REITs. We consider FFO, Core FFO and AFFO useful indicators of our performance. Because FFO, Core FFO and AFFO calculations exclude such factors as depreciation and amortization of real estate assets and gain or loss from sales of operating real estate assets (which can vary among owners of identical assets in similar conditions based on historical cost accounting and useful-life estimates), FFO, Core FFO and AFFO presentations facilitate comparisons of operating performance between periods and between other REITs in our peer group. Funds from Operations, Core Funds from Operations and Adjusted Funds from Operations Funds From Operations Due to certain unique operating characteristics of real estate companies, as discussed below, NAREIT, an industry trade group, has promulgated a measure known as FFO, which we believe to be an appropriate supplemental measure to reflect the operating performance of a REIT. FFO is not equivalent to net income or loss as determined under GAAP. We calculate FFO, a non-GAAP measure, consistent with the standards established over time by the Board of Governors of NAREIT, as restated in a White Paper approved by the Board of Governors of NAREIT effective in December 2018 (the “White Paper”). The White Paper defines FFO as net income or loss computed in accordance with GAAP, excluding depreciation and amortization related to real estate, gain and loss from the sale of certain real estate assets, gain and loss from change in control and impairment write-downs of certain real estate assets and investments in entities when the impairment is directly attributable to decreases in the value of depreciable real estate held by the entity. Adjustments for unconsolidated partnerships and joint ventures are calculated to exclude the proportionate share of the non-controlling interest to arrive at FFO, Core FFO, AFFO and NOI attributable to stockholders, as applicable. Our FFO calculation complies with NAREIT’s definition. FFO includes adjustments related to the treatment of the sale of Multi-Tenant Retail Portfolio as a discontinued operation, which includes adjustments for depreciation and amortization and loss (gain) on dispositions of real estate investments. |

| 22 The historical accounting convention used for real estate assets requires straight-line depreciation of buildings and improvements, and straight-line amortization of intangibles, which implies that the value of a real estate asset diminishes predictably over time. We believe that, because real estate values historically rise and fall with market conditions, including inflation, interest rates, unemployment and consumer spending, presentations of operating results for a REIT using historical accounting for depreciation and certain other items may be less informative. Historical accounting for real estate involves the use of GAAP. Any other method of accounting for real estate such as the fair value method cannot be construed to be any more accurate or relevant than the comparable methodologies of real estate valuation found in GAAP. Nevertheless, we believe that the use of FFO, which excludes the impact of real estate related depreciation and amortization, among other things, provides a more complete understanding of our performance to investors and to management, and, when compared year over year, reflects the impact on our operations from trends in occupancy rates, rental rates, operating costs, general and administrative expenses, and interest costs, which may not be immediately apparent from net income. Funds from Operations, Core Funds from Operations and Adjusted Funds from Operations (Cont’d) Core Funds From Operations In calculating Core FFO, we start with FFO, then we exclude certain non-core items such as merger, transaction and other costs, as well as certain other costs that are considered to be non-core, such as debt extinguishment or modification costs. The purchase of properties, and the corresponding expenses associated with that process, is a key operational feature of our core business plan to generate operational income and cash flows in order to make dividend payments to stockholders. In evaluating investments in real estate, we differentiate the costs to acquire the investment from the subsequent operations of the investment. We also add back non-cash write-offs of deferred financing costs, prepayment penalties and certain other costs incurred with the early extinguishment or modification of debt which are included in net income but are considered financing cash flows when paid in the statement of cash flows. We consider these write-offs and prepayment penalties to be capital transactions and not indicative of operations. By excluding expensed acquisition, transaction and other costs as well as non-core costs, we believe Core FFO provides useful supplemental information that is comparable for each type of real estate investment and is consistent with management’s analysis of the investing and operating performance of our properties. Core FFO includes adjustments related to the treatment of the sale of Multi-Tenant Retail Portfolio as a discontinued operation, which includes adjustments for acquisition and transaction costs and loss on extinguishment of debt. Adjusted Funds From Operations In calculating AFFO, we start with Core FFO, then we exclude certain income or expense items from AFFO that we consider more reflective of investing activities, other non-cash income and expense items and the income and expense effects of other activities or items, including items that were paid in cash that are not a fundamental attribute of our business plan or were one time or non-recurring items. These items include for example early extinguishment or modification of debt and other items excluded in Core FFO as well as unrealized gain and loss, which may not ultimately be realized, such as gain or loss on derivative instruments, gain or loss on foreign currency transactions, and gain or loss on investments. In addition, by excluding non-cash income and expense items such as amortization of above-market and below-market leases intangibles, amortization of deferred financing costs, straight-line rent and equity-based compensation from AFFO, we believe we provide useful information regarding income and expense items which have a direct impact on our ongoing operating performance. We also exclude revenue attributable to the reimbursement by third parties of financing costs that we originally incurred because these revenues are not, in our view, related to operating performance. We also include the realized gain or loss on foreign currency exchange contracts for AFFO as such items are part of our ongoing operations and affect our current operating performance. APPENDIX: FINANCIAL DEFINITIONS |

| 23 Funds from Operations, Core Funds from Operations and Adjusted Funds from Operations (Cont’d) Adjusted Funds From Operations (cont’d) In calculating AFFO, we also exclude certain expenses which under GAAP are characterized as operating expenses in determining operating net income. All paid and accrued acquisition, transaction and other costs (including prepayment penalties for debt extinguishments or modifications and merger related expenses) and certain other expenses, including expenses related to our European tax restructuring and transition costs related to the RTL merger and internalizations, negatively impact our operating performance during the period in which expenses are incurred or properties are acquired and will also have negative effects on returns to investors, but are excluded by us as we believe they are not reflective of our on-going performance. Further, under GAAP, certain contemplated non-cash fair value and other non-cash adjustments are considered operating non-cash adjustments to net income. In addition, as discussed above, we view gain and loss from fair value adjustments as items which are unrealized and may not ultimately be realized and not reflective of ongoing operations and are therefore typically adjusted for when assessing operating performance. Excluding income and expense items detailed above from our calculation of AFFO provides information consistent with management’s analysis of our operating performance. Additionally, fair value adjustments, which are based on the impact of current market fluctuations and underlying assessments of general market conditions, but can also result from operational factors such as rental and occupancy rates, may not be directly related or attributable to our current operating performance. By excluding such changes that may reflect anticipated and unrealized gain or loss, we believe AFFO provides useful supplemental information. By providing AFFO, we believe we are presenting useful information that can be used to, among other things, assess our performance without the impact of transactions or other items that are not related to our portfolio of properties. AFFO presented by us may not be comparable to AFFO reported by other REITs that define AFFO differently. Furthermore, we believe that in order to facilitate a clear understanding of our operating results, AFFO should be examined in conjunction with net income (loss) calculated in accordance with GAAP as presented in our consolidated financial statements. AFFO should not be considered as an alternative to net income (loss) as an indication of our performance or to cash flows as a measure of our liquidity or ability to make distributions. Adjusted Earnings before Interest, Taxes, Depreciation and Amortization, Net Operating Income, Cash Net Operating Income and Cash Paid for Interest. We believe that Adjusted EBITDA, which is defined as earnings before interest, taxes, depreciation and amortization adjusted for acquisition, transaction and other costs, other non-cash items and including our pro-rata share from unconsolidated joint ventures, is an appropriate measure of our ability to incur and service debt. We also exclude revenue attributable to the reimbursement by third parties of financing costs that we originally incurred because these revenues are not, in our view, related to operating performance. All paid and accrued acquisition, transaction and other costs (including prepayment penalties for debt extinguishments or modifications) and certain other expenses, including expenses related to our European tax restructuring and transition costs related to the Merger and Internalization, negatively impact our operating performance during the period in which expenses are incurred or properties are acquired and will also have negative effects on returns to investors, but are not reflective of on-going performance. Adjusted EBITDA should not be considered as an alternative to cash flows from operating activities, as a measure of our liquidity or as an alternative to net income (loss) as calculated in accordance with GAAP as an indicator of our operating activities. Other REITs may calculate Adjusted EBITDA differently and our calculation should not be compared to that of other REITs. EBITDA includes adjustments related to the treatment of the sale of the Multi-Tenant Retail Portfolio as a discontinued operation, which includes adjustments for depreciation and amortization and interest expense. Adjusted EBITDA includes adjustments related to the treatment of the sale of the Multi-Tenant Retail Portfolio as a discontinued operation, which includes adjustments for merger, transaction and other costs, (loss) gain on dispositions of real estate investments, loss (gain) on derivative instruments, loss on extinguishment of debt and other income (expense). APPENDIX: FINANCIAL DEFINITIONS |

| 24 NOI is a non-GAAP financial measure equal to net income (loss), the most directly comparable GAAP financial measure, less discontinued operations, interest, other income and income from preferred equity investments and investment securities, plus corporate general and administrative expense, acquisition, transaction and other costs, depreciation and amortization, other noncash expenses and interest expense. We use NOI internally as a performance measure and believe NOI provides useful information to investors regarding our financial condition and results of operations because it reflects only those income and expense items that are incurred at the property level. Therefore, we believe NOI is a useful measure for evaluating the operating performance of our real estate assets and to make decisions about resource allocations. Further, we believe NOI is useful to investors as a performance measure because, when compared across periods, NOI reflects the impact on operations from trends in occupancy rates, rental rates, operating costs and acquisition activity on an unlevered basis, providing perspective not immediately apparent from net income. NOI excludes certain components from net income in order to provide results that are more closely related to a property’s results of operations. For example, interest expense is not necessarily linked to the operating performance of a real estate asset and is often incurred at the corporate level as opposed to the property level. In addition, depreciation and amortization, because of historical cost accounting and useful life estimates, may distort operating performance at the property level. NOI presented by us may not be comparable to NOI reported by other REITs that define NOI differently. We believe that in order to facilitate a clear understanding of our operating results, NOI should be examined in conjunction with net income (loss) as presented in our consolidated financial statements. NOI should not be considered as an alternative to net income (loss) as calculated in accordance with GAAP as an indication of our performance or to cash flows as a measure of our liquidity. Cash NOI is a non-GAAP financial measure that is intended to reflect the performance of our properties. We define Cash NOI as net operating income (which is separately defined herein) excluding amortization of above/below market lease intangibles and straight-line rent adjustments that are included in GAAP lease revenues. We believe that Cash NOI is a helpful measure that both investors and management can use to evaluate the current financial performance of our properties and it allows for comparison of our operating performance between periods and to other REITs. Cash NOI should not be considered as an alternative to net income (loss) as calculated in accordance with GAAP as an indication of our financial performance, or to cash flows as a measure of liquidity or our ability to fund all needs. The method by which we calculate and present Cash NOI may not be directly comparable to the way other REITs calculate and present Cash NOI. Cash NOI includes all of the adjustments described above for Adjusted EBITDA related to the treatment of the sale of the Multi-Tenant Retail Portfolio as a discontinued operation, as well as adjustments for general and administrative expenses. Cash Paid for Interest is calculated based on the interest expense less non-cash portion of interest expense and amortization of mortgage (discount) premium, net. Management believes that Cash Paid for Interest provides useful information to investors to assess our overall solvency and financial flexibility. Cash Paid for Interest should not be considered as an alternative to interest expense as determined in accordance with GAAP or any other GAAP financial measures and should only be considered together with and as a supplement to our financial information prepared in accordance with GAAP. APPENDIX: FINANCIAL DEFINITIONS |

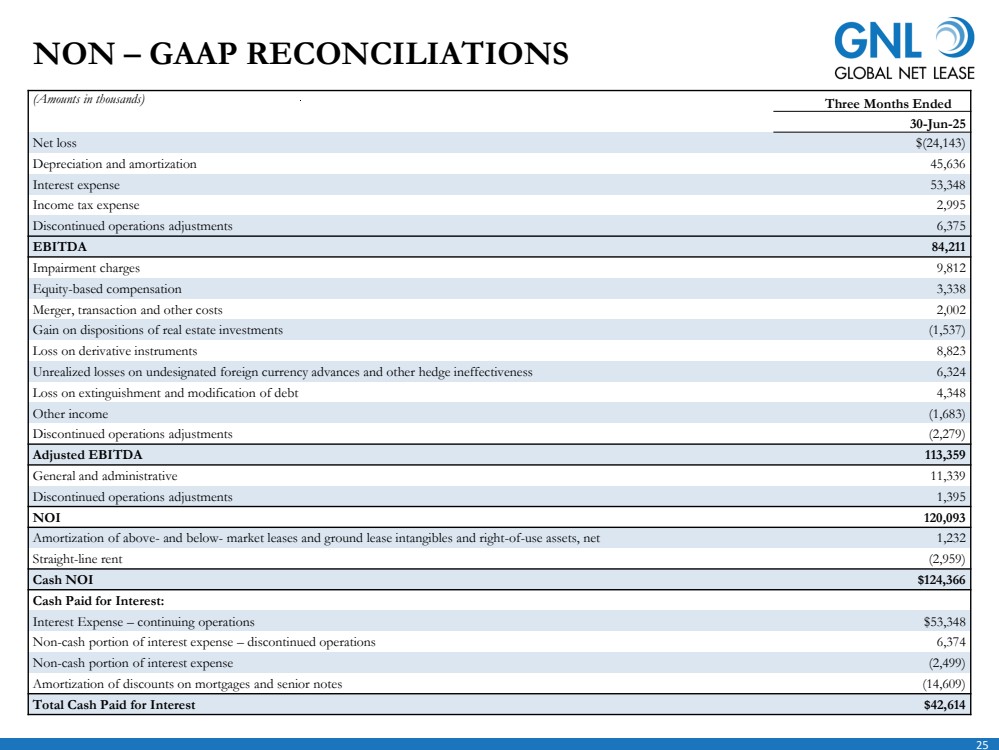

| 25 NON – GAAP RECONCILIATIONS (Amounts in thousands) Three Months Ended 30-Jun-25 Net loss $(24,143) Depreciation and amortization 45,636 Interest expense 53,348 Income tax expense 2,995 Discontinued operations adjustments 6,375 EBITDA 84,211 Impairment charges 9,812 Equity-based compensation 3,338 Merger, transaction and other costs 2,002 Gain on dispositions of real estate investments (1,537) Loss on derivative instruments 8,823 Unrealized losses on undesignated foreign currency advances and other hedge ineffectiveness 6,324 Loss on extinguishment and modification of debt 4,348 Other income (1,683) Discontinued operations adjustments (2,279) Adjusted EBITDA 113,359 General and administrative 11,339 Discontinued operations adjustments 1,395 NOI 120,093 Amortization of above- and below- market leases and ground lease intangibles and right-of-use assets, net 1,232 Straight-line rent (2,959) Cash NOI $124,366 Cash Paid for Interest: Interest Expense – continuing operations $53,348 Non-cash portion of interest expense – discontinued operations 6,374 Non-cash portion of interest expense (2,499) Amortization of discounts on mortgages and senior notes (14,609) Total Cash Paid for Interest $42,614 |

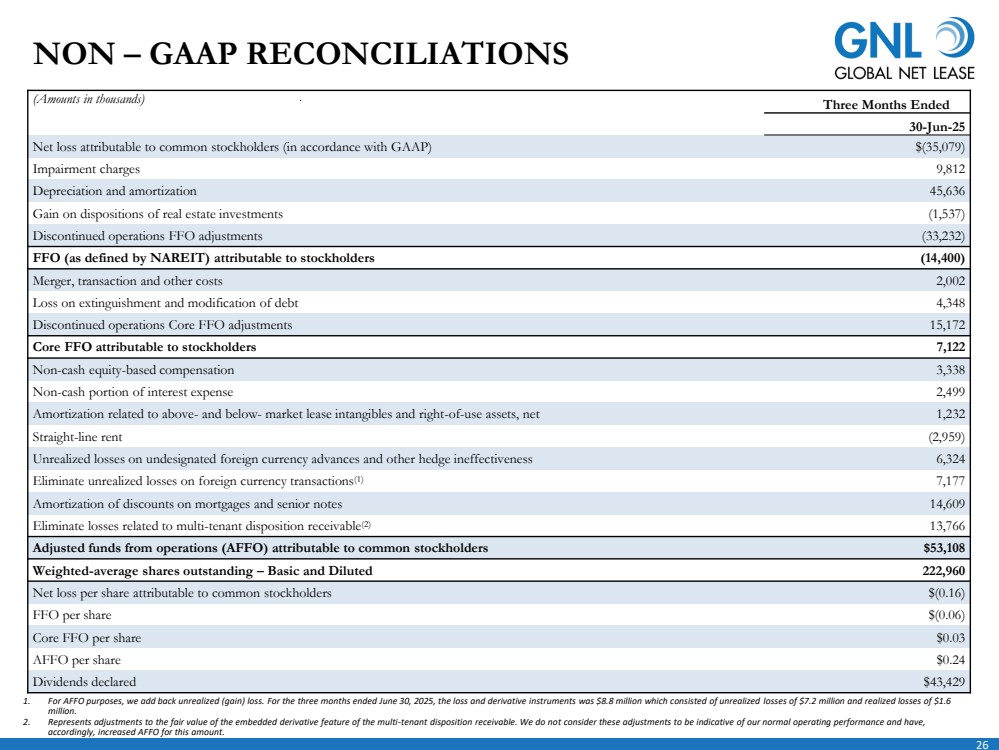

| 26 (Amounts in thousands) Three Months Ended 30-Jun-25 Net loss attributable to common stockholders (in accordance with GAAP) $(35,079) Impairment charges 9,812 Depreciation and amortization 45,636 Gain on dispositions of real estate investments (1,537) Discontinued operations FFO adjustments (33,232) FFO (as defined by NAREIT) attributable to stockholders (14,400) Merger, transaction and other costs 2,002 Loss on extinguishment and modification of debt 4,348 Discontinued operations Core FFO adjustments 15,172 Core FFO attributable to stockholders 7,122 Non-cash equity-based compensation 3,338 Non-cash portion of interest expense 2,499 Amortization related to above- and below- market lease intangibles and right-of-use assets, net 1,232 Straight-line rent (2,959) Unrealized losses on undesignated foreign currency advances and other hedge ineffectiveness 6,324 Eliminate unrealized losses on foreign currency transactions(1) 7,177 Amortization of discounts on mortgages and senior notes 14,609 Eliminate losses related to multi-tenant disposition receivable(2) 13,766 Adjusted funds from operations (AFFO) attributable to common stockholders $53,108 Weighted-average shares outstanding – Basic and Diluted 222,960 Net loss per share attributable to common stockholders $(0.16) FFO per share $(0.06) Core FFO per share $0.03 AFFO per share $0.24 Dividends declared $43,429 NON – GAAP RECONCILIATIONS 1. For AFFO purposes, we add back unrealized (gain) loss. For the three months ended June 30, 2025, the loss and derivative instruments was $8.8 million which consisted of unrealized losses of $7.2 million and realized losses of $1.6 million. 2. Represents adjustments to the fair value of the embedded derivative feature of the multi-tenant disposition receivable. We do not consider these adjustments to be indicative of our normal operating performance and have, accordingly, increased AFFO for this amount. |