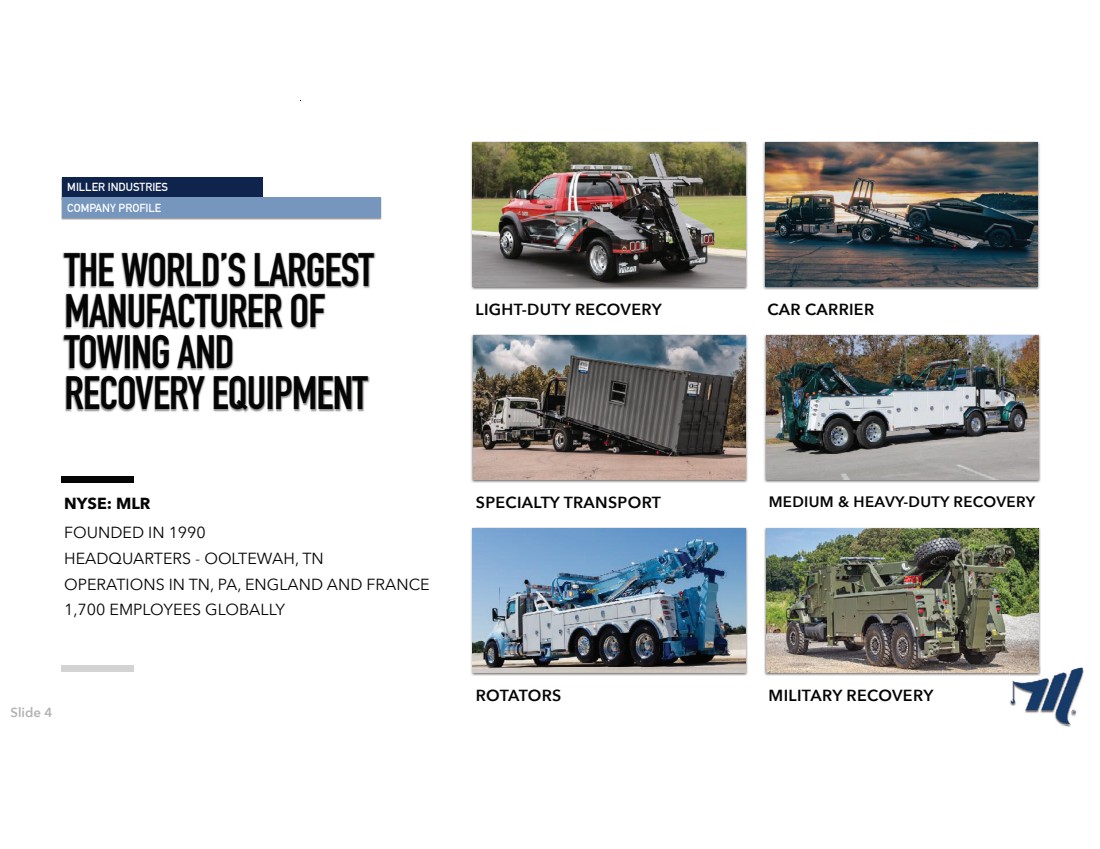

| THE WORLD’S LARGEST MANUFACTURER OF TOWING AND RECOVERY EQUIPMENT |

| MILLER INDUSTRIES FORWARD LOOKING STATEMENTS SAFE HARBOR STATEMENT Certain statements in this presentation may be deemed to be forward-looking statements, as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by the use of words such as “may”, “will”, “should”, “could”, “continue”, “future”, “potential”, “believe”, “project”, “plan”, “intend”, “seek”, “estimate”, “predict”, “expect”, “anticipate” and similar expressions, or the negative of such terms, or other comparable terminology and include, without limitation, any statements relating to our 2025 revenues including on the slide titled “2025 Guidance”, the ability to execute our strategy to reduce field inventory, the potential success of actions taken to address tariff-related uncertainties, the potential success of actions taken to address demand headwinds, including efforts to improve costs, as well as expectations regarding our future cash flow, potential future recovery in retail activity and order intake, inventory channel flow, current or pending federal or state regulations regarding emissions and emissions standards, opportunities in the global military market, and our future performance, revenues, share repurchases or profitability. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. Forward-looking statements also include the assumptions underlying or relating to any of the foregoing statements. Such forward-looking statements are made based on our management’s beliefs as well as assumptions made by, and information currently available to, our management. Our actual results may differ materially from the results anticipated in these forward-looking statements due to, among other things: our dependence upon outside suppliers for component parts, chassis and raw materials, including aluminum, steel, and petroleum-related products leaves us subject to changes in price and availability, the cadence and quantity of deliveries from our suppliers, and delays in receiving supplies of such materials, component parts or chassis; our customers’ and towing operators’ access to capital and credit to fund purchases; the implementation of new or increased tariffs and any resulting trade wars and any resulting macroeconomic uncertainty; the rising costs of equipment ownership, including continuing increases in insurance premiums and elevated interest rates that have added cost pressures to our end users, and fluctuations in the value of used trucks; macroeconomic trends, availability of financing, and changing interest rates; our customers’ ability to fund purchases of our products increases in the cost of skilled labor; the cyclical nature of our industry and changes in consumer confidence and in economic conditions in general; special risks from our sales to U.S. and other governmental entities through prime contractors; changes in fuel and other transportation costs, insurance costs and weather conditions; changes in government regulations, including environmental and health and safety regulations; failure to comply with domestic and foreign anti-corruption laws; competition in our industry and our ability to attract or retain customers; our ability to develop or acquire proprietary products and technology; assertions against us relating to intellectual property rights; changes in the tax regimes and related government policies and regulations in the countries in which we operate; the effects of regulations relating to conflict minerals; the catastrophic loss of one of our manufacturing facilities; environmental and health and safety liabilities and requirements; loss of the services of our key executives; product warranty or product liability claims in excess of our insurance coverage; potential recalls of components or parts manufactured for us by suppliers or potential recalls of defective products; an inability to acquire insurance at commercially reasonable rates; a disruption in, or breach in security of, our information technology systems or any violation of data protection laws; and those other risks discussed in our filings with the Securities and Exchange Commission, including those risks discussed under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2024, as supplemented in our Quarterly Report on Form 10-Q for the quarter ended June 30, 2025, which discussion is incorporated herein by this reference. Such factors are not exclusive. We do not undertake to update any forward-looking statement that may be made from time to time by, or on behalf of, Miller Industries, Inc. This presentation and the associated remarks made during this conference call are integrally related and are intended to be presented and understood together Slide 2 |

| Q2 2025 EARNINGS PRESENTATION Slide 3 |

| MILLER INDUSTRIES COMPANY PROFILE THE WORLD’S LARGEST MANUFACTURER OF TOWING AND RECOVERY EQUIPMENT NYSE: MLR LIGHT-DUTY RECOVERY CAR CARRIER SPECIALTY TRANSPORT MEDIUM & HEAVY-DUTY RECOVERY ROTATORS MILITARY RECOVERY FOUNDED IN 1990 HEADQUARTERS - OOLTEWAH, TN OPERATIONS IN TN, PA, ENGLAND AND FRANCE 1,700 EMPLOYEES GLOBALLY Slide 4 |

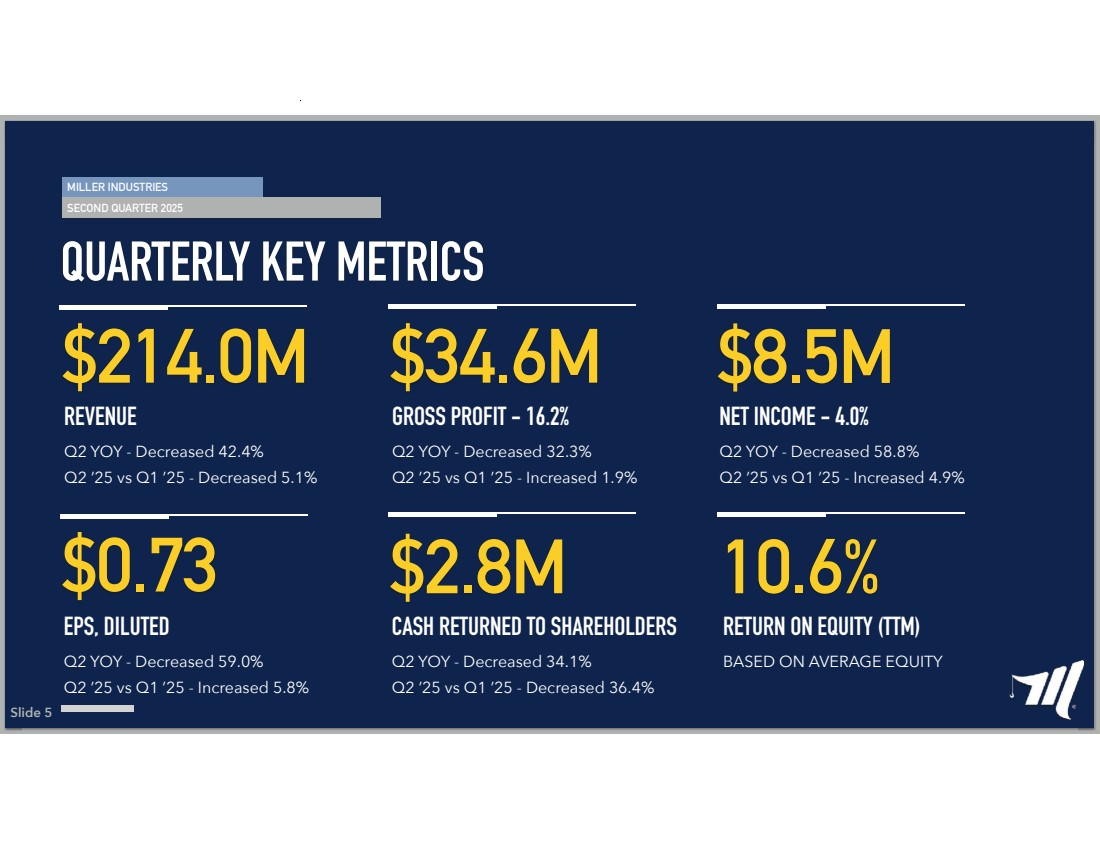

| MILLER INDUSTRIES SECOND QUARTER 2025 QUARTERLY KEY METRICS Q2 YOY - Decreased 42.4% Q2 ’25 vs Q1 ’25 - Decreased 5.1% REVENUE GROSS PROFIT - 16.2% $214.0M $34.6M NET INCOME - 4.0% $8.5M EPS, DILUTED $0.73 $2.8M CASH RETURNED TO SHAREHOLDERS Slide 5 Q2 YOY - Decreased 32.3% Q2 ’25 vs Q1 ’25 - Increased 1.9% Q2 YOY - Decreased 58.8% Q2 ’25 vs Q1 ’25 - Increased 4.9% Q2 YOY - Decreased 59.0% Q2 ’25 vs Q1 ’25 - Increased 5.8% Q2 YOY - Decreased 34.1% Q2 ’25 vs Q1 ’25 - Decreased 36.4% 10.6% RETURN ON EQUITY (TTM) BASED ON AVERAGE EQUITY |

| MILLER INDUSTRIES MARKET OVERVIEW 2025 SECOND HALF OUTLOOK ■ INDUSTRY DEMAND HEADWINDS ■ DISTRIBUTOR INVENTORY REDUCTION ■ RETAIL ACTIVITY / ORDER INTAKE ■ PRODUCTION LEVELS ■ COST REDUCTION INITIATIVES ■ CARB / A.C.T. ■ TARIFFS Slide 6 |

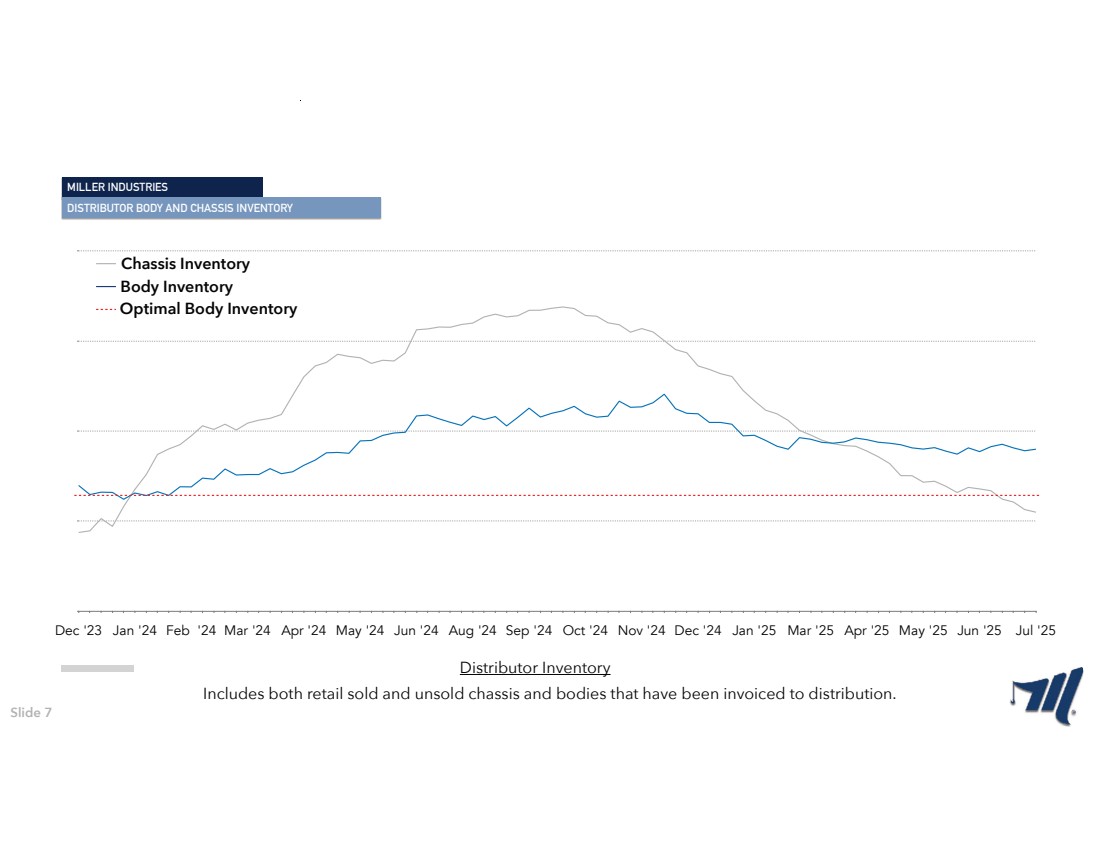

| MILLER INDUSTRIES DISTRIBUTOR BODY AND CHASSIS INVENTORY 3000 3750 4500 5250 6000 Dec '23 Jan '24 Feb '24 Mar '24 Apr '24 May '24 Jun '24 Aug '24 Sep '24 Oct '24 Nov '24 Dec '24 Jan '25 Mar '25 Apr '25 May '25 Jun '25 Jul '25 Chassis Inventory Body Inventory Optimal Body Inventory Distributor Inventory Includes both retail sold and unsold chassis and bodies that have been invoiced to distribution. Slide 7 |

| MILLER INDUSTRIES MARKET OVERVIEW 2025 SECOND HALF AND BEYOND ■ FREE CASH FLOW ■ DEBT REDUCTION ■ COMMERCIAL MARKET RECOVERY ■ MILITARY RFQ’S ■ GROWTH OPPORTUNITIES ■ ENTER 2026 IN A POSITION OF STRENGTH Slide 8 |

| MILLER INDUSTRIES CAPITAL ALLOCATION CAPITAL ALLOCATION STRATEGY ■Quarterly Dividend ■Debt Reduction ■Share Repurchase ■Innovation ■Automation ■Human Capital ■Capacity Expansion Slide 9 |

| MILLER INDUSTRIES 2025 AND BEYOND 2025 GUIDANCE ■ ESTIMATED REVENUE $750M - $800M ■ SUSPENDED EPS GUIDANCE Slide 10 |

| “ MILLER INDUSTRIES CORE PHILOSOPHY WE HAVE THE BEST PEOPLE, THE BEST PRODUCTS, AND THE BEST DISTRIBUTION NETWORK IN THE TOWING AND RECOVERY INDUSTRY.” - BILL MILLER - 1990 Slide 11 |

| MILLER INDUSTRIES Q2 2025 EARNINGS PRESENTATION Q&A Slide 12 |

| Slide 13 THANK YOU |