The following table illustrates the expenses and fees that the Fund expects to incur and that Shareholders can expect to bear directly or indirectly.

| Class I | |

| Maximum Sales Load | None |

| Maximum Early Repurchase Fee (as a percentage of repurchased amount) | 0.00% |

| ANNUAL EXPENSES (as a percentage of net assets attributable to Shares) | |

| Management Fee(1) | 1.40% |

| Fees and Interest Payments on Borrowed Funds | 0.85%(2) |

| Other Expenses(2) | 0.24% |

| Acquired Fund Fees and Expenses(3) | 0.68% |

| Total Annual Fund Operating Expenses | 3.17% |

| Fee Waiver(4) | (0.40)% |

| Total Annual Fund Operating Expenses after Fee Waiver | 2.77% |

(1) The Management Fee is equal to an annual rate of 1.40% on the average daily net assets of the Fund, payable monthly in arrears. Cliffwater has entered into a written agreement providing that it will limit the Management Fee it charges the Fund to 1.00% from July 1, 2025 through June 30, 2026.

(2) “Fees and Interest Payments on Borrowed Funds” and “Other Expenses” are estimated for the Fund’s current fiscal year. “Other Expenses” include, among other things, professional fees and other expenses that the Fund will bear, including ongoing offering costs and fees and expenses of the Administrator, transfer agent and the Fund’s Custodian.

(3) Shareholders also indirectly bear a portion of the asset-based fees, performance or incentive fees or allocations and other expenses incurred by the Fund as an investor in the Portfolio Funds and Underlying Funds. Generally, asset-based fees payable in connection with Portfolio Fund investments will range from 1.00% to 2.00% (annualized) of the commitment amount of the Fund’s investment, and performance or incentive fees or allocations are typically 20% of a Portfolio Fund’s net profits annually, although it is possible that such amounts may be exceeded for certain Portfolio Fund Managers. The “Acquired Fund Fees and Expenses” disclosed above, however, do not reflect any performance-based fees or allocations paid by the Portfolio Funds that are calculated solely on the realization and/or distribution of gains, or on the sum of such gains and unrealized appreciation of assets distributed in kind, as such fees and allocations for a particular period may be unrelated to the cost of investing in the Portfolio Funds. Future acquired funds’ fees and expenses may be substantially higher or lower because certain fees are based on the performance of the acquired funds, which may fluctuate over time. The “Acquired Fund Fees and Expenses” disclosed above are based on estimated amounts for the Fund’s current fiscal year.

(4) Cliffwater has entered into a written fee waiver agreement providing that it will limit the Management Fee it charges the Fund to 1.00% from July 1, 2025 through June 30, 2026.

| You Would Pay the Following | 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Class I Shares | $ 28 | $ 94 | $ 162 | $ 344 |

The purpose of the table above is to assist prospective investors in understanding the various fees and expenses Shareholders will bear directly or indirectly. For a more complete description of the various fees and expenses of the Fund, see “Management Fee,” “Fund Expenses,” “Repurchase of Shares by the Fund” and “Purchasing Shares.”

Investment Objective and Strategies

Investment Objective

The Fund’s investment objective is to generate long-term capital appreciation by investing in a portfolio of private equity, private debt, as well as structured equity securities that have both equity and credit qualities, investments in real assets, including real estate, and any newer instruments such as collateralized fund obligations (together, “Private Capital”); that provide attractive risk-adjusted return potential. Private Capital investments are investments into the equity and/or debt of private companies. The Fund will seek to achieve its objective through exposure to a broad set

of managers, strategies and transaction types across multiple sectors, geographies and vintage years (the first year in which a fund receives capital from investors or starts making investments). Under normal circumstances, the Fund will invest at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in assets representing investments in Private Capital (“Private Capital Assets”). Unfunded commitments are not counted for purposes of calculating the Fund’s 80% policy. This test is applied at the time of investment; later percentage changes caused by a change in the value of the Fund’s assets, including as a result of the issuance or repurchase of Shares, will not require the Fund to dispose of an investment.

Except as otherwise indicated, the Fund may change its investment objective and any of its investment policies, restrictions, strategies, and techniques without Shareholder approval. The investment objective of the Fund is not a fundamental policy of the Fund and may be changed by the Board without the vote of a majority (as defined by the 1940 Act) of the Fund’s outstanding Shares. The Fund will notify Shareholders of any changes to its investment objective or any of its investment policies, restrictions, strategies or techniques.

Investment Strategies

Private Capital refers to investments into the equity and/or debt of private companies. Private Capital investments can follow a variety of strategies including, without limitation, equity investments in which a mature company is acquired from current shareholders (“Buyouts”), equity investments in early stage or other high growth potential companies (“Venture Capital” and “Growth Equity,” respectively), and lending to businesses, broadly defined as providing capital or assets to businesses or individuals in exchange for regular payments (“Private Debt”).

Private Capital Strategy Descriptions

• Buyouts: Control investments (those where the Portfolio Fund has the ability or power to exercise a controlling influence over the management or policies of a company) in established, cash flow positive companies are generally classified as Buyouts. Buyout investments may focus on small-, mid- or large-capitalization companies, and such investments collectively represent a majority of the capital deployed in the overall private equity market. The use of debt financing, or leverage, is prevalent in buyout transactions — particularly in the large-cap segment.

• Venture Capital: Investments in new and emerging companies are usually classified as Venture Capital. Such investments are often in technology, healthcare, or other high growth industries. Companies financed by Venture Capital are often not cash flow positive at the time of investment and may require several rounds of financing before they can be sold privately or taken public. Venture Capital investors may finance companies along the full path of development or focus on certain sub-stages (usually classified as seed, early-stage, and late-stage) and often do so in partnership with other investors.

• Growth Equity: Growth Equity investments are usually minority investments in high growth companies that require additional capital to expand their businesses but are typically more mature than the recipients of traditional Venture Capital. Such companies are typically profitable, breakeven, or near-breakeven and have largely mitigated the basic risk in their business plan. Growth-stage companies range from companies that were previously funded by Venture Capital investors to those businesses with no third-party investors. Unlike buyout transactions, Growth Equity investments typically utilize low or no leverage. Investment returns in Growth Equity are driven by strong organic revenue growth and typically benefit from downside protection through a preferred position in a company’s capital structure. Growth Equity investors are adept in professionalizing and supporting fast-growing companies, adding value through introducing governance procedures, human capital, and industry-specific operating best practices.

• Private Debt: Private Debt strategies entail lending to businesses, broadly defined as providing capital or assets to businesses or individuals in exchange for regular payments, the level of which is commensurate with the probability of loss for each investment or strategy, or through the provision of capital to businesses or individuals by acquiring assets from those businesses or individuals that produce regular cash flows as an alternative to a traditional loan, such as receivables factoring or a sale leaseback of real estate or equipment (“real assets”). In receivables factoring, companies sell their accounts receivable (unpaid invoices) at a discount to a third-party manager (factor) for cash. This manager may create a fund of such transactions in which investors may participate. The factor assumes responsibility of collecting payment from the customers, seeking to generate a payment greater than the negotiated purchase price

(generating a return for investors). Private Debt investments made by the Fund may take the form of secured or unsecured bonds and loans with a fixed or floating coupon, a structured capital instrument with a preference to common equity holders and a stated contractual interest payment or rate of return, assets with fixed lease payments, or other assets with predictable cash flow streams. Investments may be made directly or indirectly through a range of investment vehicles that the Investment Manager believes offer high current income across corporate, real asset and alternative credit opportunities. Private Debt investments made by the Fund may take the form of secured or unsecured bonds and loans with a fixed or floating coupon, a structured capital instrument with a preference to common equity holders and a stated contractual interest payment or rate of return, assets with fixed lease payments, or other assets with predictable cash flow streams. The Fund may invest some, or all, of its Private Debt target allocation in other Closed-End Funds that are also managed by Cliffwater.

Private Capital Investment Structures

The Fund will seek to achieve its investment objective through broad exposure to Private Capital investments, including semi-liquid or listed investments, that may include: (i) direct investments in the equity and/or debt of a private company (“Direct Investments”); (ii) secondary purchases of interests in private funds (each a “Portfolio Fund,” and collectively, the “Portfolio Funds”) managed by third-party managers (“Portfolio Fund Managers”) and other private assets (together, “Secondary Investments” or “secondaries”); (iii) primary fund commitments; (iv) direct or secondary purchases of liquid private equity instruments; (v) other liquid investments, including exchange-traded funds (“ETFs”); (vi) Closed-End Funds and private and public BDCs and (vii) short-term investments, including money market funds and short-term treasuries. Portfolio Funds, mutual funds, ETFs, registered Closed-End Funds and BDCs in which the Fund may invest are collectively referred to as “Underlying Funds.”

The Fund’s investments will typically not be registered with the SEC or any state securities commission and will typically not be listed on any national securities exchange. The amount of public information available with respect to the issuers in which the Fund invests may generally be less extensive than that available for issuers of registered or exchange listed securities.

The Fund’s portfolio will be constructed with investments across the following Private Capital investment structures:

• Primary Investments: Primary investments (“Primary Investments” or “primaries”) are limited partnership interests in newly established private equity funds that are typically acquired by way of subscription during their initial fundraising period. Most private equity fund sponsors raise new funds every two to four years, and many top-performing funds are closed to new investors. Because of the limited windows of opportunity for making primary investments in particular funds, strong relationships with leading fund sponsors are highly important for investors in Primary Investments.

Investors in primaries subscribe for interests during an initial fundraising period, and their capital commitments are then used to fund investments in a number of individual operating companies during a defined investment period and to pay associated management fees and expenses throughout the fund’s term. The investments of the fund are usually unknown at the time of commitment, and investors typically have little or no ability to influence the investments that are made during the fund’s life. Because primary investors must rely on the expertise of the fund manager, an accurate assessment of the manager’s capabilities is essential.

Primary Investments typically exhibit a value development pattern, commonly known as the “J-curve,” in which the fund’s NAV typically declines moderately during the early years of the fund’s life as investment-related fees and expenses are incurred before investment gains have been realized. As the fund matures and portfolio companies are sold, the pattern is expected to reverse with increasing NAV and distributions to fund investors. Primary Investments typically have a full term of ten to thirteen years with an average portfolio company investment hold period of three to eight years. Capital is typically deployed for new investments over the first three to five years, and the portfolio companies are then held for three to eight years before being sold with cash proceeds distributed back to fund investors. The private fund sponsor will often receive performance-based compensation, also called a carried interest allocation, typically entitling it to approximately 20% of net profits on the fund’s investments after meeting a minimum return. After all of the fund’s assets have been disposed, the fund is dissolved.

• Secondary Investments: Secondary Investments are the assumption or purchase of existing limited partner interests, typically in seasoned Private Capital funds or Co-Investments that are acquired in privately negotiated transactions. The original subscriber of the primary investment is often the seller of the asset. The stage of maturity for the asset can vary from early in the investment period of the fund to near full term of the fund.

Pricing for a Secondary Investment is negotiated based on the reported NAV and expected timing of cash flows (capital calls for contributions to the Portfolio Fund, clawbacks of amounts distributed to the Portfolio Fund’s general partner and distributions of returns) of the Portfolio Fund(s) or Co-Investment(s). A majority of available secondaries have existing investments in portfolio companies. As a result, the secondary buyer has greater visibility to the assets being purchased. Investment returns are less impacted by the J-curve pattern (the tendency for a fund’s NAV to decline moderately during the early years of the fund’s life as investment-related fees and expenses are incurred before investment gains have been recognized) expected from a primary investment and distribution patterns may be accelerated as the buyer’s participation is at a later stage in the primary’s life. The secondary buyer does not participate in prior distributions from the acquired limited partnership interest or the previous growth in value of the assets. The Secondary Investment liquidates and dissolves in the same manner as a Primary Investment.

• Co-Investments: Co-investments (“Co-Investments”) are direct investments in specific companies or assets or indirect investments in specific companies or assets through a vehicle managed and controlled by a general partner or sponsor. Co-Investments are typically offered to Private Capital fund investors when the Private Capital fund sponsor believes that there is an attractive investment for the fund, but the total size of the potential holding exceeds the targeted size or allocation for the fund. Co-investors will generally participate in these investments at the same entry valuation as the Private Capital fund sponsor but with respect to any follow-on investment, such investment may be made at a different valuation. Co-investments, unlike investments in primary funds, often do not bear an additional layer of fees or bear significantly reduced fees. Co-investments typically have a three- to eight-year holding period.

• Listed Investments: Listed Private Capital investments gain access to underlying private assets through investments in listed entities that invest in private transactions or private funds or that earn fees and/or carried interest from such assets. Historically, the prices of listed Private Capital investments have been sensitive to economic conditions and, at certain times, could be purchased at discounts relative to similar assets in private transactions.

The Investment Manager will not cause the Fund to engage in co-investments alongside affiliates unless the Fund has received an order granting an exemption from Section 17 of the 1940 Act or unless such investments are not prohibited by Section 17(d) of the 1940 Act or interpretations of Section 17(d) as expressed in SEC no-action letters or other available guidance.

Investment Process Overview

Due Diligence and Selection of Investments

Cliffwater follows a disciplined approval process for the purpose of identifying investment opportunities within a consistent framework. Cliffwater’s philosophy is that a repeatable process and consistent team engagement leads to better investment outcomes, and the due diligence process is designed to evaluate opportunities against these criteria. Throughout due diligence, Cliffwater maintains a collaborative decision-making process designed to encourage frequent input from its investment committee and other investment professionals.

Manager/Fund Selection

Throughout the course of due diligence on a Fund investment (each a “Fund Investment” and collectively, the “Fund Investments”), Cliffwater focuses on assessing several important attributes of the sponsor, including (i) track record benchmarking and analysis (including a fundamental analysis around key indicators of the sponsor’s historical value creation and a revaluation of the unrealized portfolio), (ii) team quality, experience, continuity, and depth, (iii) consistency and attractiveness of strategy, investment parameters and an ability to deploy capital in the size of assets in which the sponsor has a demonstrable track record of success, and (iv) economic alignment (allocation of carry and the size of

the general partner commitment). The fundamental track record benchmarking analysis includes evaluating a sponsor’s ability to drive an increase in a company’s or a portfolio’s value through operational and financial improvements. This also includes analyzing a sponsor’s ability to grow revenue and earnings before interest, taxes, depreciation and amortization, leading to an increase in enterprise value. Some of the key indicators of value creation include growing the customer base/reducing customer concentration, strengthening management teams, completing accretive or strategic acquisitions, optimizing pricing, improving marketing and branding, expanding into additional markets and product segments, and using prudent levels of debt. Taking these and other factors into consideration, the Investment Manager determines if the current value of an asset or portfolio is appropriate or if an adjustment is required. Valuations are assessed through a combination of reviewing audited financials, valuation policies of sponsors, and comparing public and private comparable transactions or current values. Cliffwater’s operations team also conducts operational due diligence on the sponsor and Cliffwater’s legal due diligence team conducts legal due diligence on the fund documents.

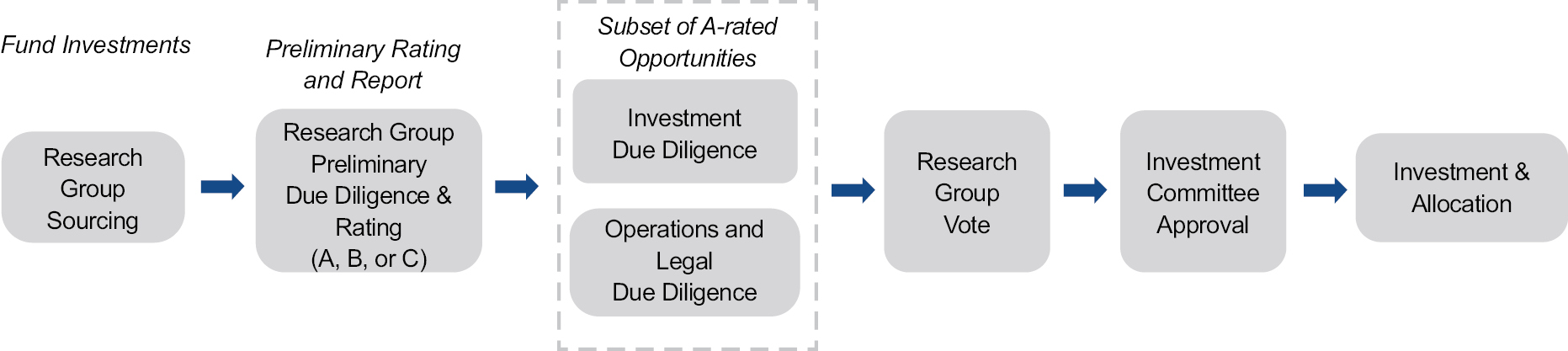

Cliffwater believes that investors benefit by selecting management firms that specialize in each strategy. Cliffwater maintains a global database exceeding 4,800 Private Capital fund managers, conducting due diligence, and giving an A, B, or C-rating to each fund.

The Fund investment selection process is illustrated by the diagram below.

• Sourcing. Cliffwater’s Private Capital research team is responsible for sourcing investment opportunities and funds. These professionals are responsible for primary fund opportunities across a wide spectrum of private equity, Private Debt, and private real asset opportunities and managers. Each has developed sector specialization and manager knowledge from their years of experience, which extends globally. The manager relationships lead to origination of co-investment and secondary opportunities.

• Rating. Each research team member then rates (A, B, or C) investments and fund opportunities and prepares a preliminary due diligence report supporting their rating. A-ratings generally comprise a small fraction 10-20% of the universe of opportunities. Ratings can change as the research team re-evaluates over time.

• Due Diligence. Cliffwater next conducts thorough due diligence on the top A-rated investments and fund opportunities. This involves separate investment and operations due diligence teams and separate investment and operational reports that further describe and assess the opportunity. In addition, Cliffwater expects to regularly communicate with private equity general partnerships (“GPs”) and limited partners (“LPs”) of Private Capital funds (collectively referred to as “Private Equity Investors”), managers and other personnel about statistical and factual information regarding economic factors and trends to utilize in making the investment decisions for the Fund. This interaction facilitates ongoing portfolio analysis and may help to address potential issues, such as loss of key team members or proposed changes in constituent documents. It also provides ongoing due diligence feedback, as additional Co-Investments with a particular GP are considered. Cliffwater may also perform background and reference checks on investment fund personnel.

Key value drivers in Cliffwater’s investment due diligence process include:

i. Organization: Evaluation of the Portfolio Managers, as defined below, and the backing provided by their platform.

ii. Investment process: Assessment of repeatable and differentiated processes for sourcing investment opportunities, transaction analysis, and overall investment strategy; consistency in strategy, investment parameters and an ability to deploy capital in the size of assets in which the sponsor has a demonstrable track record of success.

iii. Portfolio construction: Transaction mix (capital structure, industry, sector, geography, etc.), position sizing, financing sources, economic alignment (allocation of carry and the size of the general partner commitment), and expenses.

iv. Track record: Demonstrable track record of successfully originating, underwriting, and securing deals, and meeting return targets; fundamental analysis around key indicators of the sponsor’s historical value creation.

Separately, Cliffwater’s operations due diligence team conducts an independent assessment of the operational risks of the investment opportunity.

Key value drivers in Cliffwater’s operations due diligence process include:

i. Governance: Evaluation of the regulatory and compliance program, role of the advisory board, and business risk management practices.

ii. Infrastructure: Assessment of the non-investment personnel, segregation of duties and cash controls, service provider selection, and technology infrastructure.

iii. Processes: Review of financing arrangements, investor transparency and disclosures, and ongoing investor communication.

iv. Valuation: Evaluation of the valuation methodology, valuation review procedures, accounting processes, and fund expenses.

• Approval — Research Group. The research team next votes to approve the investment or requests additional information if appropriate.

• Final Approval — Investment Committee. Cliffwater’s Investment Committee approves all final investments/funds. If approved by the research team, the appropriate research professional will present the investment opportunity, with supporting reports, to the Investment Committee for final approval.

• Ongoing Monitoring. Following the close of an investment, Cliffwater implements a diligent monitoring process that includes frequent meetings or calls with underlying investment managers, review of quarterly reports and annual audited financial statements, ongoing monitoring of key performance indicators related to portfolio holdings and underlying exposures, and performance analysis using a wide array of analytical tools and systems.

Co-Investment Selection

Throughout the course of due diligence on a Co-Investment, Cliffwater focuses on evaluating various key aspects of each opportunity, which involves (i) performing an analysis of the sponsor that is leading the transaction, (ii) assessing the underlying sectors and industries where the investment operates and competes, (iii) understanding the target investment’s operating model, historical financial information and business plans, (iv) producing base case (projected return in light of assumptions most likely to occur) and downside cases (projected return after considering additional factors that could negatively impact the investment) as well as developing sensitivities around key drivers, and (v) conducting a detailed review of the proposed transaction terms, including valuation, capital structure, legal, tax and governance.

Portfolio Construction & Liquidity Management

In addition to asset selection, Cliffwater believes that portfolio construction is critical to the successful execution of the Fund’s investment strategy. Additionally, Cliffwater has established portfolio parameters to manage exposure across Primary Investments, Secondary Investments, and Co-Investments. These parameters are set with an understanding of the return, risk and cash flow attributes of each investment type, while also considering the portfolio effect provided by diverse investment opportunities, in an effort to (i) mitigate the “J-curve” (the tendency for a fund’s NAV to decline moderately during the early years of the fund’s life as investment-related fees and expenses are incurred before investment gains have been realized), (ii) reduce blind-pool risk (the risk associated with the wide flexibility and broad

investment mandate afforded to certain pooled investment vehicles at the time the investment is made by the Fund), (iii) deploy investor capital in an efficient manner based on investment opportunity, (iv) grow and return investor capital sooner than typical illiquid, private equity structures, (v) manage portfolio volatility, and (vi) deliver superior risk-adjusted returns to its investors.

By tracking certain features, such as commitments, capital calls, distributions and valuations, Cliffwater will use a range of techniques to balance total returns with reoccurring distributions and liquidity targets, including (i) diversifying commitments across Private Capital Assets at different parts of fund lifecycles through the use of Primary Investments, Secondary Investments and Co-Investments, (ii) actively managing cash and liquid assets, and (iii) modeling and actively monitoring cash flows to mitigate cash drag and maintain appropriate levels of committed capital. In addition, the Fund may seek to establish credit lines to provide liquidity to satisfy Shareholder tender requests.

To enhance the Fund’s liquidity, particularly in times of possible net outflows through the tender of Shares by shareholders, Cliffwater may from time to time determine to sell certain of the Fund’s assets. The Fund may also invest in liquid assets that may include both fixed income and equity assets as well as public and private vehicles that derive their investment returns from fixed income and equity securities, including publicly listed companies that pursue the business of private equity investing; publicly listed companies that invest in private equity transactions or funds; alternative asset managers, holding companies, investment trusts, ETFs, closed-end funds, financial institutions and other vehicles whose primary purpose is to invest in, lend capital to or provide services to privately held companies; and certain derivatives, such as options and futures.

There can be no assurance that the objective of the Fund with respect to liquidity management will be achieved or that the Fund’s portfolio design strategies will be successful. Prospective investors should refer to the discussion of the risks associated with the investment strategy and structure of the Fund found under “General risks” and “Limits of Risk Disclosure.”

Portfolio Monitoring

Cliffwater monitors each investment, including performance measurement relative to initial investment expectations, frequent interactions and periodic in-person visits with the sponsors and attendance of annual general meetings and advisory board meetings. The ongoing monitoring process measures key performance indicators, transactional milestones, investment pacing, volatility metrics, investment consistency relative to the stated strategy, qualitative factors on the sponsor and its professionals, reporting quality and various macro factors.

Description of the Investment Manager’s Experience with Private Capital

The Investment Manager has been advising on private equity and private equity funds since its founding in 2004. It has been recommending such investments to its advisory clients since that time. The Investment Manager has dedicated significant resources to developing its expertise in Private Capital and cultivating relationships with investment advisers that it believes to be top-tier. The Investment Manager brings to the management of the Fund its expertise, experience and access in Private Capital.

The Investment Manager’s research also shows that there is no single investment style that is demonstrably better than others, and the Investment Manager believes that a superior outcome can be achieved when experienced investment advisers of different styles are combined.

Geographic Regions and Foreign Currency Exposure

The Fund may, directly or indirectly, make investments outside of the United States, including in emerging markets. The Fund’s non-U.S. investments are expected to be primarily in Europe, Asia, and Canada and, to a lesser extent in Latin America and the Middle East. Emerging market countries are those countries included in the MSCI Emerging Markets Index.

The Fund’s investment and strategies will involve exposure to foreign currencies. The Fund may seek to hedge all or a portion of the Fund’s foreign currency risk. Depending on market conditions and the views of the Investment Manager, the Fund may or may not hedge all or a portion of its currency exposures.

Subsidiaries

The Fund may make investments through direct and indirect wholly owned subsidiaries (each a “Subsidiary” and collectively, the “Subsidiaries”). Such Subsidiaries will not be registered under the 1940 Act; however, the Fund will wholly own and control any Subsidiaries. The Board has oversight responsibility for the investment activities of the Fund, including its investment in any Subsidiary, and the Fund’s role as sole direct or indirect shareholder of any Subsidiary. To the extent applicable to the investment activities of a Subsidiary, the Subsidiary will follow the same compliance policies and procedures as the Fund. The Fund would “look through” any such Subsidiary to determine compliance with its investment policies.

Borrowing by the Fund

Cliffwater believes the Fund’s investment strategy favors a modest amount of leverage consistent with the statutory limitations. Accordingly, the Fund may utilize leverage from borrowings, including through borrowings by one or more special purpose vehicles (“SPVs”) that are Subsidiaries of the Fund, to enhance yield within the 300% asset coverage (up to 50% of the Fund’s net assets) requirements of an interval fund. Certain investments may be held by these SPVs. The Fund is authorized to borrow cash in connection with its investment activities, to satisfy repurchase requests from Fund shareholders, and to otherwise provide the Fund with temporary liquidity. Borrowings will be limited to 33.33% of the Fund’s assets (50% of its net assets).

On September 26, 2024, the Fund’s wholly owned subsidiary, CPCF Holdings (D1) LLC, (“CPEFX SPV”), entered into a secured revolving credit facility (the “Facility”), with JPMorgan Chase Bank N.A. (the “Lender”). The Facility, as amended effective June 20, 2025, provides for borrowings on a committed basis in an aggregate principal amount up to $800,000,000, and may be increased further from time to time upon mutual agreement by the Lender and CPEFX SPV. The Facility matures on September 26, 2027 and may be extended further from time to time. See “Credit Facility” for information on its effect on the Fund’s leverage.

Other Information Regarding Investment Strategy

The Fund may, from time to time, take temporary defensive positions that are inconsistent with the Fund’s principal investment strategy in attempting to respond to adverse market, economic, political or other conditions. During such times, Cliffwater may determine that a large portion of the Fund’s assets should be invested in cash or cash equivalents, including money market instruments, prime commercial paper, repurchase agreements, municipal bonds, bank accounts, Treasury bills and other short-term obligations of the U.S. Government, its agencies or instrumentalities and other high-quality debt instruments maturing in one year or less from the time of investment. In these and in other cases, the Fund may not achieve its investment objective. Cliffwater may invest the Fund’s cash balances in any investments it deems appropriate.

The frequency and amount of portfolio purchases and sales (known as the “portfolio turnover rate”) of the Fund may vary from year to year. The Fund’s portfolio turnover rate will not be a limiting factor when Cliffwater deems portfolio changes appropriate. The Fund may engage in short-term trading strategies, and securities may be sold without regard to the length of time held when, in the opinion of Cliffwater, investment considerations warrant such action. These policies may have the effect of increasing the annual rate of portfolio turnover of the Fund. If securities are not held for the applicable holding periods, dividends paid on them will not qualify for the advantageous federal tax rates.

No guarantee or representation is made that the investment program of the Fund will be successful, that the various Fund Investments selected will produce positive returns, or that the Fund will achieve its investment objective.

General Risks

The following are certain risk factors that relate to the operations and terms of the Fund. These considerations, which do not purport to be a complete description of any of the particular risks referred to or a complete list of all risks involved in an investment in the Fund, should be carefully evaluated before determining whether to invest in the Fund.

An investment in the Fund involves a considerable amount of risk. An investor may lose money. Before making an investment decision, a prospective investor should (i) consider the suitability of this investment with respect to their investment objectives and personal situation and (ii) consider factors such as their personal net worth, income, age, risk tolerance and liquidity needs. The Fund is an illiquid investment. Shareholders have no right to require the Fund to redeem their Shares of the Fund.

The Shares are speculative and illiquid securities involving substantial risk of loss. An investment in the Fund is appropriate only for those investors who do not require a liquid investment, for whom an investment in the Fund does not constitute a complete investment program, and who fully understand and are capable of assuming the risks of an investment in the Fund.

Limited Operating History Risk. The Fund has limited operating history. The Fund is subject to all of the business risks and uncertainties associated with any new business, including the risk that the Fund will not achieve its investment objective and that the value of Shares could decline.

Market Risk. An investment in the Fund is subject to investment risk, including the possible loss of the entire principal amount invested. An investment in the Fund represents an indirect investment in the securities owned by the Fund. The value of these securities, like other market investments, may move up or down, sometimes rapidly and unpredictably. The value of your shares at any point in time may be worth less than the value of your original investment, even after taking into account any reinvestment of dividends and distributions.

Borrowing, Use of Leverage. The Fund leverages and may continue to leverage its investments, including through borrowings by one or more SPVs that are Subsidiaries of the Fund. Certain Fund investments may be held by such SPVs. The use of leverage increases both risk of loss and profit potential. The Fund is subject to the 1940 Act requirement that an investment company satisfy an asset coverage requirement of 300% of its indebtedness, including amounts borrowed (including through one or more SPVs that are Subsidiaries of the Fund), measured at the time the investment company incurs the indebtedness (the “Asset Coverage Requirement”). This means that at any given time the value of the Fund’s total indebtedness may not exceed one-third the value of its total assets (including such indebtedness). The Fund may be required to dispose of assets on unfavorable terms if market fluctuations or other factors reduce the Fund’s asset coverage to less than the prescribed amount. The interests of persons with whom the Fund (or SPVs that are Subsidiaries of the Fund) enters into leverage arrangements will not necessarily be aligned with the interests of the Fund’s Shareholders and such persons will have claims on the Fund’s assets that are senior to those of the Fund’s Shareholders. In addition to the risks created by the Fund’s use of leverage, the Fund is subject to the additional risk that it would be unable to timely, or at all, obtain leverage borrowing. The Fund might also be required to de-leverage, selling securities at a potentially inopportune time and incurring tax consequences. Further, the Fund’s ability to generate income from the use of leverage would be adversely affected.

Under the 1940 Act, the Fund is not permitted to issue preferred stock unless immediately after such issuance, the value of the Fund’s total assets (including the proceeds of such issuance) less all liabilities and indebtedness not represented by senior securities is at least equal to 200% of the total of the aggregate amount of senior securities representing indebtedness plus the aggregate liquidation value of any outstanding preferred stock. Stated another way, the Fund may not issue preferred stock that, together with outstanding preferred stock and debt securities, has a total aggregate liquidation value and outstanding principal amount of more than 50% of the value of the Fund’s total assets, including the proceeds of such issuance, less liabilities and indebtedness not represented by senior securities. In addition, the Fund is not permitted to declare any distribution on its common stock, or purchase any of the Fund’s shares of common stock (through repurchase offers or otherwise) unless the Fund would satisfy this 200% asset coverage requirement test

after deducting the amount of such distribution or share price, as the case may be. The Fund may, as a result of market conditions or otherwise, be required to purchase or redeem preferred stock, or sell a portion of its investments when it may be disadvantageous to do so, in order to maintain the required asset coverage. Common stockholders would bear the costs of issuing additional preferred stock, which may include offering expenses and the ongoing payment of distributions. Under the 1940 Act, the Fund may only issue one class of preferred stock.

On September 26, 2024, the Fund’s wholly owned subsidiary, CPCF Holdings (D1) LLC, (“CPEFX SPV”), entered into a secured revolving credit facility (the “Facility”), with JPMorgan Chase Bank N.A. (the “Lender”). The Facility, as amended effective June 20, 2025, provides for borrowings on a committed basis in an aggregate principal amount up to $800,000,000, and may be increased further from time to time upon mutual agreement by the Lender and CPEFX SPV. The Facility matures on September 26, 2027 and may be extended further from time to time. See “Credit Facility” for information on its effect on the Fund’s leverage.

Dependence on the Investment Manager Risk. The success of the Fund depends upon the ability of the Investment Manager to develop and implement investment strategies that achieve the investment objective of the Fund. Shareholders will have no right or power to participate in the management or control of the Fund.

Dependence on Key Personnel Risk. The Investment Manager may be dependent upon the experience and expertise of certain key personnel in providing services with respect to the Fund’s investments. If the Investment Manager were to lose the services of these individuals, its ability to service the Fund could be adversely affected. As with any managed fund, the Investment Manager may not be successful in selecting the best-performing securities or investment techniques for the Fund’s portfolio, and the Fund’s performance may lag behind that of similar funds. The Investment Manager has informed the Fund that its investment professionals are actively involved in other investment activities not concerning the Fund and will not be able to devote all of their time to the Fund’s business and affairs. In addition, individuals not currently associated with the Investment Manager may become associated with the Fund, and the performance of the Fund may also depend on the experience and expertise of such individuals.

Concentration of Investments Risk. The value of the investments of a fund that focuses its investments in a particular industry or market sector will be highly sensitive to financial, economic, political and other developments affecting that industry or market sector, and conditions that negatively impact that industry or market sector will have a greater impact on the fund as compared with a fund that does not have its holdings concentrated in a particular industry or market sector. Events negatively affecting the market sectors in which the Fund has invested are therefore likely to cause the value of the Fund’s shares to decrease, perhaps significantly. At times, the performance of investments in those industries may lag the performance of other sectors or the market as a whole.

Management Risk. The NAV of the Fund changes daily based on the performance of the securities in which it invests. The Investment Manager’s judgments about the attractiveness, value and potential appreciation of a particular sector and securities or the financial performance of portfolio companies in which the Fund invests may prove to be incorrect and may not produce the desired results.

Portfolio Fund Risk. The Fund will incur higher and duplicative expenses, including advisory fees, when it invests in shares of mutual funds (including money market funds), BDCs, Closed-End Funds, ETFs and other registered and private investment funds (“Portfolio Funds”). There is also the risk that the Fund may suffer losses due to the investment practices of the Portfolio Funds (such as the use of derivatives). The ETFs in which the Fund invests that attempt to track an index may not be able to replicate exactly the performance of the indices they track, due to transactions costs and other expenses of the ETFs. The existence of extreme market volatility or potential lack of an active trading market for an ETF’s shares could result in such shares trading at a significant premium or discount to their NAV. The shares of listed closed-end funds may also frequently trade at a discount to their NAV. There can be no assurance that the market discount on shares of any closed-end fund purchased by the Fund will ever decrease, and it is possible that the discount may increase. The Fund may invest in other registered closed-end management investment companies advised by Cliffwater that are considered affiliates of the Fund. Cliffwater has agreed to reimburse the Fund for the investment management fees paid on these investments, although the Fund will be subject to asset-based and other non-management fees charged by such funds.

The Fund may invest in the securities of other investment companies to the extent that such investments are consistent with the Fund’s investment objectives and permissible under the 1940 Act. Under one provision of the 1940 Act, the Fund may not acquire the securities of other investment companies if, as a result, (i) more than 10% of the Fund’s total assets would be invested in securities of other investment companies, (ii) such purchase would result in more than 3%

of the total outstanding voting securities of any one investment company being held by the Fund or (iii) more than 5% of the Fund’s total assets would be invested in any one investment company. In some instances, the Fund may invest in an investment company in excess of these limits. For example, the Fund may invest in other registered investment companies, such as mutual funds, closed-end funds and ETFs, and in BDCs in excess of the statutory limits imposed by the 1940 Act in reliance on Rule 12d1-4 under the 1940 Act. These investments would be subject to the applicable conditions of Rule 12d1-4, which in part would affect or otherwise impose certain limits on the investments and operations of the underlying fund. Accordingly, if the Fund serves as an “underlying fund” to another investment company, the Fund’s ability to invest in other investment companies, private funds and other investment vehicles may be limited and, under these circumstances, the Fund’s investments in other investment companies, private funds and other investment vehicles will be consistent with applicable law and/or exemptive relief obtained from the SEC. The requirements of Rule 12d1-4 have been implemented by the Fund with respect to its fund of funds arrangements.

Private Investment Funds Risk. The Fund invests in private investment funds that are not registered as investment companies. As a result, the Fund as an investor in these funds would not have the benefit of certain protections afforded to investors in registered investment companies. The Fund may not have the same amount of information about the identity, value, or performance of the private investment funds’ investments as such private investment funds’ managers. Investments in private investment funds generally will be illiquid and generally may not be transferred without the consent of the fund. The Fund may be unable to liquidate its investment in a private investment fund when desired (and may incur losses as a result), or may be required to sell such investment regardless of whether it desires to do so. Upon its withdrawal of all or a portion of its interest in a private investment fund, the Fund may receive securities that are illiquid or difficult to value. The Fund may not be able to withdraw from a private investment fund except at certain designated times, thereby limiting the ability of the Fund to withdraw assets from the private fund due to poor performance or other reasons. The fees paid by private investment funds to their advisers and general partners or managing members often are higher than those paid by registered funds and generally include a percentage of gains. The Fund will bear its proportionate share of the management fees and other expenses that are charged by a private investment fund in addition to the management fees and other expenses paid by the Fund.

The success of the Fund depends in part upon the ability of the Portfolio Fund Managers to develop and implement strategies that achieve their investment objectives. The Investment Manager does not control the investments or operations of the Portfolio Funds. A Portfolio Fund Manager may employ investment strategies that differ from its past practices and are not fully disclosed to the Investment Manager and that involve risks that are not anticipated by the Investment Manager. Some Portfolio Fund Managers may have a limited operating history and some may have limited experience in executing one or more investment strategies to be employed for a Portfolio Fund. Furthermore, there is no guarantee that the information given to the Administrator and reports given to the Investment Manager will not be fraudulent, inaccurate or incomplete.

Portfolio Funds may target or concentrate their investments in particular markets, sectors or industries. As a result, the NAVs of such Portfolio Funds may be subject to greater volatility than those of investment companies that are subject to diversification requirements and this may negatively impact the NAV of the Fund.

In addition, it is expected that the Fund will be able to make investments in particular Portfolio Funds only at certain times, and commitments to Portfolio Funds may not be accepted (in part or in their entirety). As a result, the Fund may hold cash or invest any portion of its assets that is not invested in Portfolio Funds in cash equivalents, short-term securities or money market securities pending investment in Portfolio Funds. To the extent that the Fund’s assets are not invested in Portfolio Funds, the Fund may be unable to meet its investment objective.

Illiquid Portfolio Investments Risk. The Fund is expected to invest in securities that are subject to legal or other restrictions on transfer or for which no liquid market exists. A Portfolio may make investments that may become less liquid in response to market developments or geopolitical events such as sanctions, trading halts or wars, or adverse investor perceptions. The market prices, if any, for such securities may be volatile and the Fund may not be able to sell them when the Investment Manager desires to do so or to realize what the Investment Manager perceives to be their fair value in the event of a sale. The sale of restricted and illiquid securities often requires more time and results in higher brokerage charges or dealer discounts and other selling expenses than does the sale of securities eligible for trading on national securities exchanges or in the over the counter markets. Restricted securities may sell at prices that are lower than similar securities that are not subject to restrictions on resale.

Investors acquiring direct loans hoping to recoup their entire principal must generally hold their loans through maturity. Direct loans may not be registered under the Securities Act of 1933, as amended (the “Securities Act”) and are not listed on any securities exchange. Accordingly, those loan investments may not be transferred unless they are first registered under the Securities Act and all applicable state or foreign securities laws or the transfer qualifies for an exemption from such registration. A reliable secondary market has yet to develop, nor may one ever develop for direct loans and, as such, these investments should be considered illiquid. Until an active secondary market develops, the Fund intends to primarily hold its direct loans until maturity. The Fund may not be able to sell any of its direct loans even under circumstances when the Investment Manager believes it would be in the best interests of the Fund to sell such investments. In such circumstances, the overall returns to the Fund from its direct loans may be adversely affected. Moreover, certain direct loans may be subject to certain additional significant restrictions on transferability. Although the Fund may attempt to increase its liquidity by borrowing from a bank or other institution, its assets may not readily be accepted as collateral for such borrowing.

Valuation Risk. Unlike publicly traded common stock which trades on national exchanges, there is no central place or exchange for most of the Fund’s investments to trade. Due to the lack of centralized information and trading, the valuation of loans or fixed-income instruments may result in more risk than that of common stock. Uncertainties in the conditions of the financial market, unreliable reference data, lack of transparency and inconsistency of valuation models and processes may lead to inaccurate asset pricing. In addition, other market participants may value securities differently than the Fund. As a result, the Fund may be subject to the risk that when an instrument is sold in the market, the amount received by the Fund is less than the value of such loans or fixed-income instruments carried on the Fund’s books.

Shareholders should recognize that valuations of illiquid assets involve various judgments and consideration of factors that may be subjective. As a result, the NAV of the Fund, as determined based on the fair value of its investments, may vary from the amount ultimately received by the Fund from its investments. This could adversely affect Shareholders whose Shares are repurchased as well as new Shareholders and remaining Shareholders. For example, in certain cases, the Fund might receive less than the fair value of its investment, resulting in a dilution of the value of the Shares of Shareholders who do not tender their Shares in any coincident repurchase offer and a windfall to tendering Shareholders; in other cases, the Fund might receive more than the fair value of its investment, resulting in a windfall to Shareholders remaining in the Fund, but a shortfall to tendering Shareholders.

Valuation of the Fund’s Investment in Other Investment Funds Risk. The valuation of the Fund’s investments in investment funds is typically based on valuations provided by Portfolio Fund Managers on a quarterly basis. Prior to investing in any other investment fund, the Investment Manager will generally conduct a due diligence review of the valuation methodology used by the Portfolio Fund Manager. In addition to quarterly valuations provided by the Portfolio Fund Managers, the Fund undertakes daily valuations and the daily issuance of Shares. A significant portion of the Fund’s invested securities may lack a readily available market price and, therefore, require fair valuation by the Portfolio Fund Manager. In this context, the Investment Manager may encounter a conflict of interest when valuing these securities, as their value can impact the Investment Manager’s compensation or their capacity to raise additional funds. There are no guarantees or assurances regarding the valuation methodology employed or the adequacy of systems utilized by any Portfolio Fund Manager. Additionally, there is no assurance regarding the accuracy of valuations provided by the Portfolio Fund Managers, their compliance with internal policies or procedures for record-keeping and valuation, or the stability of their policies, procedures, and systems without prior notice to the Fund. Consequently, it is possible that a Portfolio Fund Manager’s valuation of securities may not align with the ultimate realized amount upon the disposition of such securities. The information provided by a Portfolio Fund Manager may be subject to inaccuracy due to fraudulent activity, misvaluation, or inadvertent errors. It is important to note that the Fund may not identify valuation errors for a significant period of time, if at all.

Valuation Adjustments in Investment Funds Risk. The Fund calculates its NAV on a daily basis using the quarterly valuations provided by the Portfolio Fund Managers. However, it is important to note that these valuations may not capture market changes or other events that take place after the end of the quarter. The Fund will adjust the valuation of its holdings in investment funds to account for such events, in accordance with its valuation policies. However, it is important to note that there is no guarantee that the Fund will accurately determine the fair value of these investments. Furthermore, it is possible that the valuations reported by the Portfolio Fund Managers may be subject to subsequent adjustments or revisions. Since such adjustments or revisions to the NAV of the Fund are based on information available only at the time of the adjustment or revision, they may not impact the amount of repurchase proceeds received by Shareholders who had their Shares repurchased before these adjustments occurred. Consequently, if the

subsequent adjusted valuations from the Portfolio Fund Managers or revisions to the NAV of an investment fund have an adverse impact on the Fund’s NAV, the remaining outstanding Shares may be negatively affected due to prior repurchases. This may result in a potential benefit for Shareholders who had their Shares repurchased at a NAV higher than the adjusted amount. Contrarily, any increases in the NAV resulting from such subsequent adjustments may exclusively benefit the outstanding Shares, potentially disadvantaging Shareholders who had previously had their Shares repurchased at a NAV lower than the adjusted amount. These principles also extend to the purchase of Shares, meaning that new Shareholders may be similarly affected.

Non-Qualification As A Regulated Investment Company Risk. If for any taxable year the Fund were to fail to qualify as a RIC under Subchapter M of Subtitle A, Chapter 1, of the Code, all of its taxable income would be subject to tax at regular corporate rates without any deduction for distributions. To qualify as a RIC, the Fund must meet three numerical requirements each year regarding (i) the diversification of the assets it holds, (ii) the income it earns, and (iii) the amount of taxable income that it distributes to Shareholders. These requirements and certain additional tax risks associated with investments in the Fund are discussed in “TAX MATTERS” in the SAI.

Operational Risk. An investment in the Fund, like any fund, can involve operational risks arising from factors such as processing errors, human errors, inadequate or failed internal or external processes, failures in systems and technology, changes in personnel and errors caused by third-party service providers. The occurrence of any of these failures, errors or breaches could result in a loss of information, regulatory scrutiny, reputational damage or other events, any of which could have a material adverse effect on the Fund. While the Fund seeks to minimize such events through controls and oversight, there may still be failures that could cause losses to the Fund.

Reliance on Technology. The Fund’s business is highly dependent on the communications and information systems of the Investment Manager. In addition, certain of these systems are provided to the Investment Manager by third-party service providers. Any failure or interruption of such systems, including as a result of the termination of an agreement with any such third-party service provider, could cause delays or other problems in the Fund’s activities. This, in turn, could have a material adverse effect on the Fund’s operating results.

General Economic and Market Conditions Risk. The success of the Fund’s investment program may be affected by general economic and market conditions, such as interest rates, availability of credit, inflation rates, economic uncertainty, changes in laws, threatened or actual imposition of tariffs, and national and international political circumstances. These factors may affect the level and volatility of securities prices and the liquidity of investments held by the Fund. Unexpected volatility or illiquidity could impair the Fund’s profitability or result in losses. The value of a security may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions or adverse investor sentiment generally. The value of a security may also decline due to factors that affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. During a general downturn in the securities markets, multiple asset classes may decline in value simultaneously.

Interest rates in the United States and many other countries have risen in recent periods and may continue to rise in the future. See “Interest Rate Risk” below for more information. Additionally, as a result of increasing interest rates, reserves held by banks and other financial institutions in bonds and other debt securities could face a significant decline in value relative to deposits and liabilities, which coupled with general economic headwinds resulting from a changing interest rate environment, creates liquidity pressures at such institutions. As a result, certain sectors of the credit markets could experience significant declines in liquidity, and it is possible that the Fund will not be able to manage this risk effectively.

Additionally, market risk includes the risk that geopolitical and other events will disrupt the economy on a national or global level. For instance, war, terrorism, social unrest, recessions, supply chain disruptions, market manipulation, government defaults, government shutdowns, political changes, diplomatic developments or the imposition of sanctions and other similar measures, public health emergencies (such as the spread of infectious diseases, pandemics and epidemics), natural/environmental disasters, climate-change and climate related events can all negatively impact the securities markets, which could cause the Fund to lose value. These events could reduce consumer demand or economic output, result in market closures, changes in interest rates, inflation/deflation, travel restrictions or quarantines, and significantly adversely impact the economy. In addition, the current contentious domestic political environment, as well as political and diplomatic events within the United States and abroad could have an adverse impact on a Fund’s investments and operations.

The United Kingdom (“UK”) left the European Union (“EU”) on January 31, 2020, and a transition period during which the UK and EU negotiated terms of departure ended on December 31, 2020. The departure is commonly referred to as “Brexit.” The UK and EU reached an agreement, effective January 1, 2021, on the terms of their future trading relationship, which principally relates to the trading of goods. Further insecurity in EU membership or the abandonment of the euro could exacerbate market and currency volatility and negatively impact investments in securities issued by companies located in EU countries. Brexit also may cause additional member states to contemplate departing the EU, which would likely perpetuate political and economic instability in the region and cause additional market disruption in global financial markets. As a result, markets in the UK, Europe and globally could experience increased volatility and illiquidity, and potentially lower economic growth which in return could potentially have an adverse effect on the value of the Fund’s investments. Market disruption in the EU and globally may have a negative effect on the value of the Fund’s investments. Additionally, there could be additional risks if one or more additional EU member states seek to leave the EU. Additionally, various countries have seen significant internal conflicts and in some cases, civil wars may have had an adverse impact on the securities markets of the countries concerned. In addition, the occurrence of new disturbances due to acts of war or terrorism or other political developments cannot be excluded. Nationalization, expropriation or confiscatory taxation, currency blockage, political changes, government regulation, political, regulatory or social instability or uncertainty or diplomatic developments, including the imposition of sanctions or other similar measures, could adversely affect the Fund’s investments. Recent examples of the above include conflict, loss of life and disaster connected to ongoing armed conflict in Europe and the Middle East. The extent, duration and impact of these conflicts, related sanctions and retaliatory actions are difficult to ascertain, but could be significant and have severe adverse effects on the region, including significant adverse effects on the regional or global economies and the markets for certain securities and commodities. These impacts could negatively affect the Fund’s investments in securities and instruments that are economically tied to the applicable region, and include (but are not limited to) declines in value and reductions in liquidity. In addition, to the extent new sanctions are imposed or previously relaxed sanctions are reimposed (including with respect to countries undergoing transformation), complying with such restrictions may prevent the Fund from pursuing certain investments, cause delays or other impediments with respect to consummating such investments or divestments, require divestment or freezing of investments on unfavorable terms, render divestment of underperforming investments impracticable, negatively impact the Fund’s ability to achieve their investment objectives, prevent the Fund from receiving payments otherwise due, increase diligence and other similar costs to the Fund, render valuation of affected investments challenging, or require the Fund to consummate an investment on terms that are less advantageous than would be the case absent such restrictions. Any of these outcomes could adversely affect the Fund’s performance with respect to such investments, and thus the Fund’s performance as a whole.

The Fund cannot predict the effects or likelihood of such events on the U.S. and global economies, the value of the Shares or the NAV of the Fund. The issuers of securities, including those held in the Fund’s portfolio, could be materially impacted by such events, which may, in turn, negatively affect the value of such securities or such issuers’ ability to make interest payments or distributions to the Fund. These risks may be magnified if certain events or developments adversely interrupt the global supply chain; in these and other circumstances, such risks might affect companies worldwide due to increasingly interconnected global economies and financial markets.

Recently, the United States has enacted or proposed to enact significant new tariffs, and various federal agencies have been directed to further evaluate key aspects of U.S. trade policy, which could potentially lead to significant changes to current policies, treaties, and tariffs. Significant uncertainty continues to exist about the future relationship between the U.S. and other countries with respect to such trade policies, treaties and tariffs. These developments, or the perception that any of them could occur, may have a material adverse effect on global trade, in particular, trade between the impacted nations and the U.S.; the stability of global financial markets; and global economic conditions.

Recent technological developments in, and the increasingly widespread use of, artificial intelligence technologies may pose risks to the Fund. For instance, the economy may be significantly impacted by the advanced development and increased regulation of artificial intelligence technologies. As artificial intelligence technologies are used more widely, the profitability and growth of Fund holdings may be impacted, which could significantly impact the overall performance of the Fund. The legal and regulatory frameworks within which artificial intelligence technologies operate continue to rapidly evolve, and it is not possible to predict the full extent of current or future risks related thereto.

Economic Recession or Downturn Risk. Many of the Fund’s investments may be issued by companies susceptible to economic slowdowns or recessions. Therefore, the Fund’s non-performing assets are likely to increase, and the value of its portfolio is likely to decrease, during these periods. A prolonged recession may result in losses of value

in the Fund’s portfolio and a decrease in the Fund’s revenues, net income and NAV. Unfavorable economic conditions also could increase the Fund’s funding costs, limit the Fund’s access to the capital markets or result in a decision by lenders not to extend credit to it on terms it deems acceptable. These events could prevent the Fund from increasing investments and harm the Fund’s operating results.

Sourcing Investment Opportunities Risk. On an ongoing basis, it cannot be certain that the Investment Manager will be able to continue to locate a sufficient number of suitable investment opportunities to allow the Fund to fully implement its investment strategy. In addition, privately negotiated investments generally, and specifically in loans and illiquid securities of private middle-market companies, require substantial due diligence and structuring, and the Fund may not be able to achieve its anticipated investment pace. These factors increase the uncertainty, and thus the risk, of investing in the Fund. To the extent the Fund is unable to deploy its capital, its investment income and, in turn, the results of its operations, will likely be materially adversely affected.

Publicly Traded Private Equity Risk. Publicly traded private equity companies are typically regulated vehicles listed on a public stock exchange that invest in private equity transactions or funds. Such vehicles may take the form of corporations, business development companies, unit trusts, publicly traded partnerships, or other structures, and may focus on mezzanine, infrastructure, buyout or venture capital investments. Publicly traded private equity may also include investments in publicly listed companies in connection with a privately negotiated financing or an attempt to exercise significant influence on the subject of the investment. Publicly traded private equity investments usually have an indefinite duration.

Publicly traded private equity occupies a small portion of the public equity universe, including only a few professional investors who focus on and actively trade such investments. As a result, relatively little market research is performed on publicly traded private equity companies, only limited public data may be available regarding these companies and their underlying investments, and market pricing may significantly deviate from published net asset value. This can result in market inefficiencies and may offer opportunities to specialists that can value the underlying Private Capital investments. Publicly traded private equity vehicles are typically liquid and capable of being traded daily, in contrast to direct investments and private equity funds, in which capital is subject to lengthy holding periods. Accordingly, publicly traded private equity transactions are significantly easier to execute than other types of Private Capital investments, giving investors an opportunity to adjust the investment level of their portfolios more efficiently.

Defaulted Debt Securities and Other Securities of Distressed Companies Risk. The Fund’s Private Capital Assets may include low grade or unrated debt securities (“high yield” or “junk” bonds or leveraged loans) or investments in securities of distressed companies. Such investments involve substantial, highly significant risks. For example, high yield bonds are regarded as being predominantly speculative as to the issuer’s ability to make payments of principal and interest. Issuers of high yield debt may be highly leveraged and may not have available to them more traditional methods of financing. Therefore, the risks associated with acquiring the securities of such issuers generally are greater than is the case with higher rated securities. In addition, the risk of loss due to default by the issuer is significantly greater for the holders of high yield bonds because such securities may be unsecured and may be subordinated to other creditors of the issuer. Similar risks apply to other Private Debt securities. Successful investing in distressed companies involves substantial time, effort and expertise, as compared to other types of investments. Information necessary to properly evaluate a distress situation may be difficult to obtain or be unavailable and the risks attendant to a restructuring or reorganization may not necessarily be identifiable or susceptible to considered analysis at the time of investment.

Fixed-Income Securities Risks. Fixed-income securities in which the Fund may invest are generally subject to the following risks:

Interest Rate Risk. The Fund is subject to the risks of changes in interest rates. A decline in interest rates could reduce the amount of current income the Fund is able to achieve from interest on fixed-income securities and convertible debt. An increase in interest rates could reduce the value of any fixed income securities and convertible securities owned by the Fund. To the extent that the cash flow from a fixed income security is known in advance, the present value (i.e., discounted value) of that cash flow decreases as interest rates increase; to the extent that the cash flow is contingent, the dollar value of the payment may be linked to then prevailing interest rates. Moreover, the value of many fixed income securities depends on the shape of the yield curve, not just on a single interest rate. Thus, for example, a callable cash flow, the coupons of which depend on a short-term rate, may shorten (i.e., be called away) if the long rate decreases. In this way, such securities are exposed to the difference between long rates and short rates.

Variable and floating rate securities generally are less sensitive to interest rate changes but may decline in value if their interest rates do not rise as much, or as quickly, as interest rates in general. Conversely, floating rate securities will not generally increase in value if interest rates decline. When the Fund holds variable or floating rate securities, a decrease in market interest rates will adversely affect the income received from such securities and the NAV of the Fund’s shares.

Interest rates in the United States and many other countries have risen in recent periods and may continue to rise in the future. Because longer-term inflationary pressure may result from the U.S. government’s fiscal policies, the Fund may experience rising interest rates, rather than falling rates, over its investment horizon. To the extent the Fund or a Portfolio Fund borrows money to finance its investments, the Fund’s or the Portfolio Fund’s performance will depend, in part, upon the difference between the rate at which it borrows funds and the rate at which it invests those funds. In periods of rising interest rates, the Fund’s cost of funds could increase. Adverse developments resulting from changes in interest rates could have a material adverse effect on the Fund’s or a Portfolio Fund’s financial condition and results of operations.

In addition, a decline in the prices of the debt the Fund owns could adversely affect the Fund’s NAV. Changes in market interest rates could also affect the ability of operating companies in which the Fund invests to service debt, which could materially impact the Fund, thus impacting the Fund.

• Issuer and Spread Risk. The value of fixed-income securities may decline for a number of reasons which directly relate to the issuer, such as management performance, financial leverage, reduced demand for the issuer’s goods and services, historical and prospective earnings of the issuer and the value of the assets of the issuer. In addition, wider credit spreads and decreasing market values typically represent a deterioration of a debt security’s credit soundness and a perceived greater likelihood of risk or default by the issuer.

• Credit Risk. Credit risk is the risk that one or more fixed-income securities in the Fund’s portfolio will decline in price or fail to pay interest or principal when due because the issuer of the security experiences a decline in its financial status. Credit risk is increased when a portfolio security is downgraded or the perceived creditworthiness of the issuer deteriorates. To the extent the Fund invests in below investment grade securities, it will be exposed to a greater amount of credit risk than a fund that only invests in investment grade securities. In addition, to the extent the Fund uses credit derivatives, such use will expose it to additional risk in the event that the bonds underlying the derivatives default. The degree of credit risk depends on the issuer’s financial condition and on the terms of the securities.

• Prepayment or “Call” Risk. When interest rates decline, fixed income securities with stated interest rates may have their principal paid earlier than expected. This may result in the Fund having to reinvest that money at lower prevailing interest rates, which can reduce the returns of the Fund.

• Inflation/Deflation Risk. Inflation risk is the risk that the value of assets or income from the Fund’s investments will be worth less in the future as inflation decreases the purchasing power and value of payments at future dates. As inflation increases, the real value of the Fund’s portfolio could decline. Inflation rates may change frequently and significantly as a result of various factors, including unexpected shifts in the domestic or global economy and changes in monetary or economic policies (or expectations that these policies may change), and the Fund’s investments may not keep pace with inflation, which would generally adversely affect the real value of Shareholders’ investment in the Fund. Deflation risk is the risk that prices throughout the economy decline over time. Deflation may have an adverse effect on the creditworthiness of issuers and may make issuer default more likely, which may result in a decline in the value of the Fund’s portfolio.