Second Quarter 2025 Earnings Call July 29, 2025

Forward-Looking Statements Certain statements contained in this presentation may

constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. This presentation may contain “forward-looking statements” with respect to our business, results of operations and financial

condition, and our expectations or beliefs concerning future events and conditions. You can identify forward-looking statements because they contain words such as, but not limited to, “believes,” “expects,” “may,” “should,” “approximately,”

“anticipates,” “estimates,” “intends,” “plans,” “targets,” likely,” “will,” “would,” “could” and similar expressions (or the negative of these terminologies or expressions). All forward-looking statements involve risks and uncertainties. Many

risks and uncertainties are inherent in our industry and markets, while others are more specific to our business and operations. These risks and uncertainties include, but are not limited to: market competition; economic downturn or industry

specific conditions including the impacts of tax and tariff programs, inflation, foreign currency exchange, and industry consolidation; disruption to business operations; natural disasters including severe flooding and other weather-related

events; the conflict between Russia and Ukraine and other geopolitical tensions; the inability to meet customer demand and quality requirements; the loss of key customers, suppliers or other business relationships; supply disruptions; excessive

inflation; the capacity and effectiveness of our hedging policy activities; the loss of key employees; levels of indebtedness which could limit our operating flexibility and opportunities; and other risk factors set forth under the heading

“Risk Factors” in our Annual Report on Form 10-K, and as described from time to time in subsequent reports filed with the U.S. Securities and Exchange Commission. The occurrence of the events described and the achievement of the expected

results depend on many events, some or all of which are not predictable or within our control. Consequently, actual results may differ materially from the forward-looking statements contained in this press release. We undertake no obligation to

update or revise any forward-looking statement as a result of new information, future events or otherwise, except as required by law. Second Quarter 2025 - Earnings Call - 2

Non-GAAP Measures This presentation includes information regarding certain

non-GAAP financial measures, including Adjusted EBITDA, Free Cash Flow and Net debt. These measures are presented because management uses this information to monitor and evaluate financial results and trends and believes this information to

also be useful for investors. Adjusted EBITDA measures are frequently used by securities analysts, investors and other interested parties in their evaluation of Constellium and in comparison to other companies, many of which present an adjusted

EBITDA-related performance measure when reporting their results. Adjusted EBITDA, Free Cash Flow and Net debt are not presentations made in accordance with U.S. GAAP and may not be comparable to similarly titled measures of other companies.

These non-GAAP financial measures supplement our GAAP disclosures and should not be considered an alternative to the GAAP measures. This presentation provides a reconciliation of non-GAAP financial measures to the most directly comparable GAAP

financial measures. For the definitions or Adjusted EBITDA, Free Cash Flow and Net debt, please refer to our accompanying press release. We are not able to provide a reconciliation of Adjusted EBITDA guidance to net income, the comparable GAAP

measure, because certain items that are excluded from Adjusted EBITDA cannot be reasonably predicted or are not in our control. In particular, we are unable to forecast the timing or magnitude of realized and unrealized gains and losses on

derivative instruments, non-cash impact of metal price lag, impairment or restructuring charges, or taxes without unreasonable efforts, and these items could significantly impact, either individually or in the aggregate, our net income in the

future. Second Quarter 2025 - Earnings Call - 3

Jean-Marc Germain Chief Executive Officer

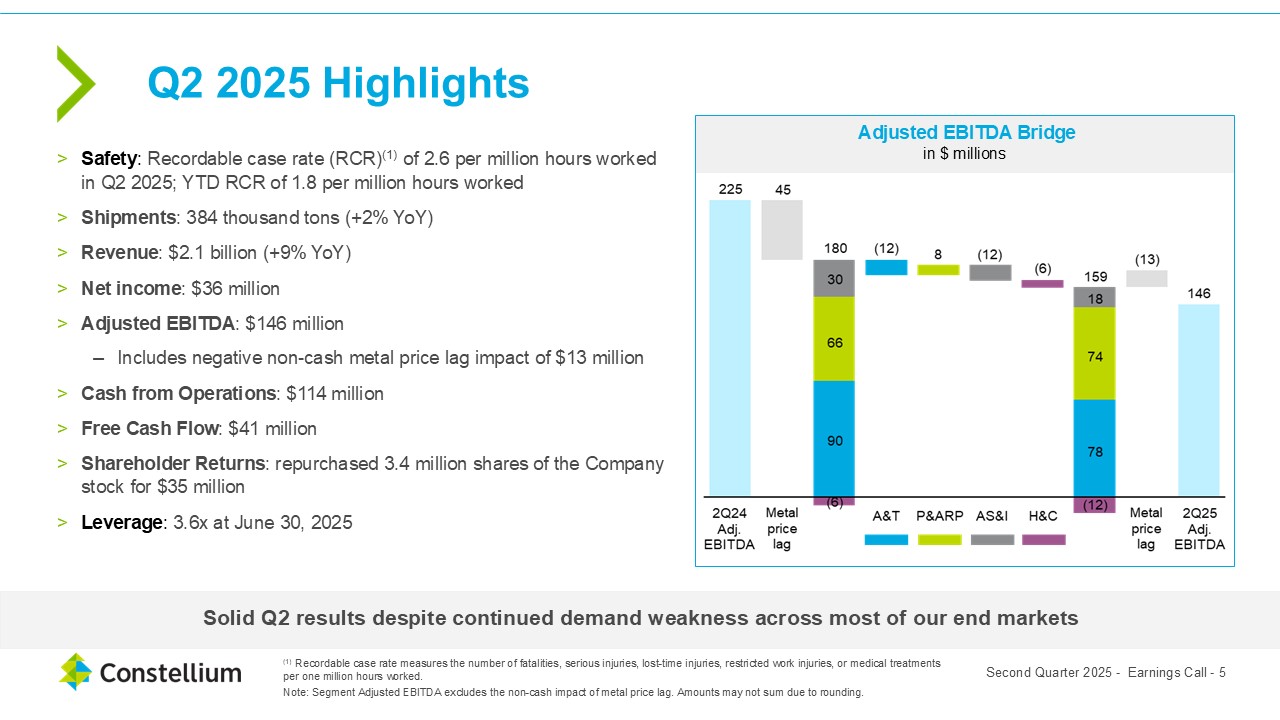

Q2 2025 Highlights Safety: Recordable case rate (RCR)(1) of 2.6 per million

hours worked in Q2 2025; YTD RCR of 1.8 per million hours worked Shipments: 384 thousand tons (+2% YoY) Revenue: $2.1 billion (+9% YoY) Net income: $36 million Adjusted EBITDA: $146 million Includes negative non-cash metal price lag impact

of $13 million Cash from Operations: $114 million Free Cash Flow: $41 million Shareholder Returns: repurchased 3.4 million shares of the Company stock for $35 million Leverage: 3.6x at June 30, 2025 Note: Segment Adjusted EBITDA excludes

the non-cash impact of metal price lag. Amounts may not sum due to rounding. Solid Q2 results despite continued demand weakness across most of our end markets Second Quarter 2025 - Earnings Call - 5 Adjusted EBITDA Bridge in $

millions (1) Recordable case rate measures the number of fatalities, serious injuries, lost-time injuries, restricted work injuries, or medical treatments per one million hours worked.

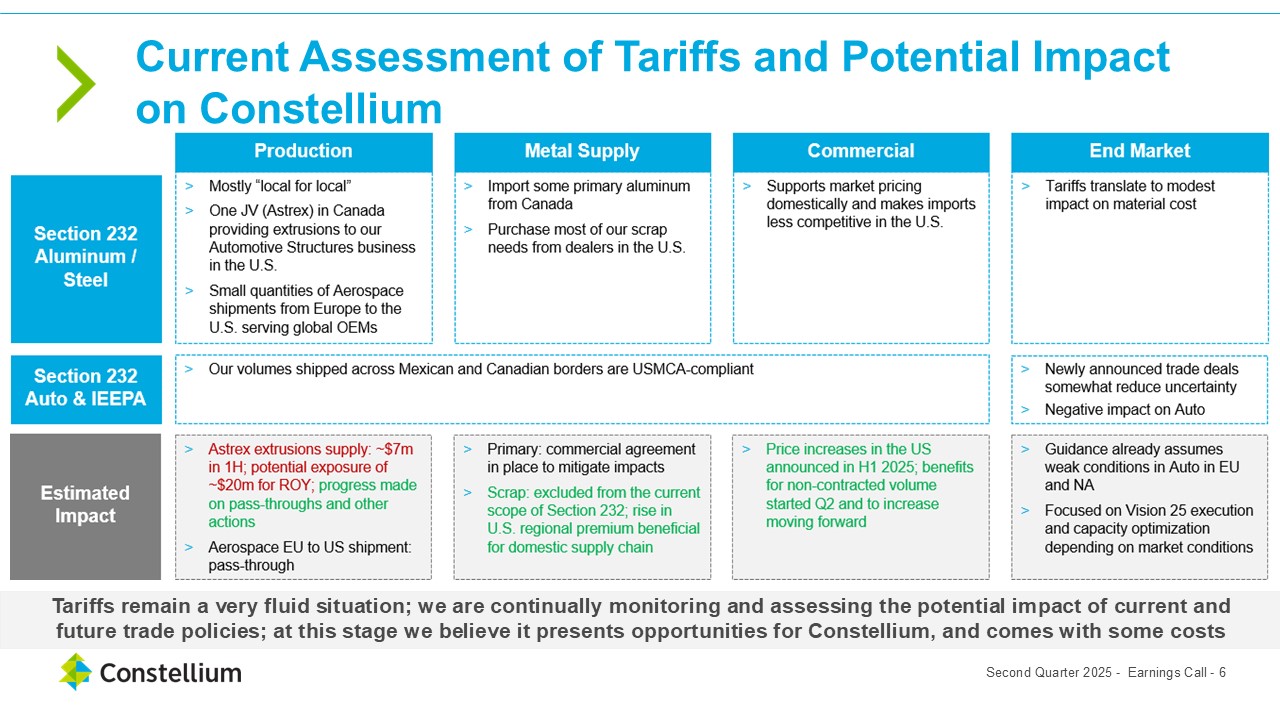

Current Assessment of Tariffs and Potential Impact on Constellium Second Quarter

2025 - Earnings Call - 6 Tariffs remain a very fluid situation; we are continually monitoring and assessing the potential impact of current and future trade policies; at this stage we believe it presents opportunities for Constellium, and

comes with some costs

Jack Guo Chief Financial Officer

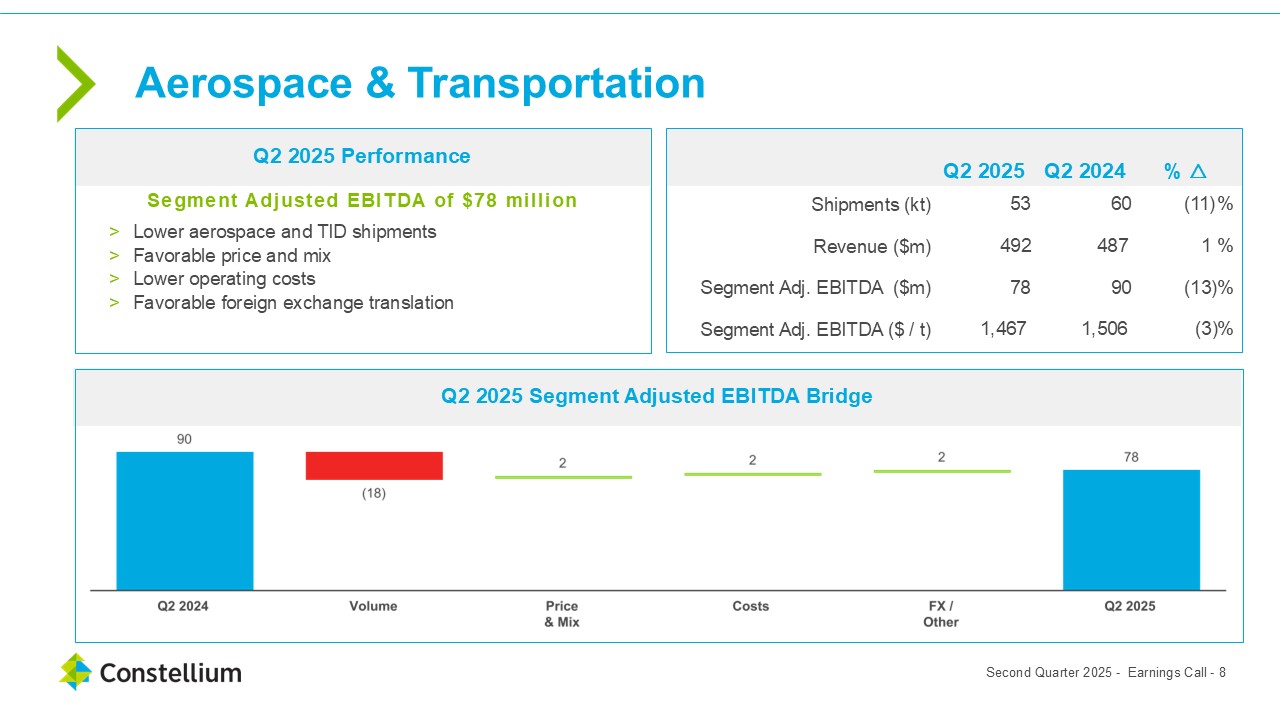

Q2 2025 Q2 2024 % △ Shipments (kt) 53 60 (11) % Revenue ($m) 492 487

1 % Segment Adj. EBITDA ($m) 78 90 (13) % Segment Adj. EBITDA ($ / t) 1,467 1,506 (3) % Aerospace & Transportation Q2 2025 Segment Adjusted EBITDA Bridge Q2 2025 Performance Second Quarter 2025 - Earnings Call - 8 Segment

Adjusted EBITDA of $78 million Lower aerospace and TID shipments Favorable price and mix Lower operating costs Favorable foreign exchange translation

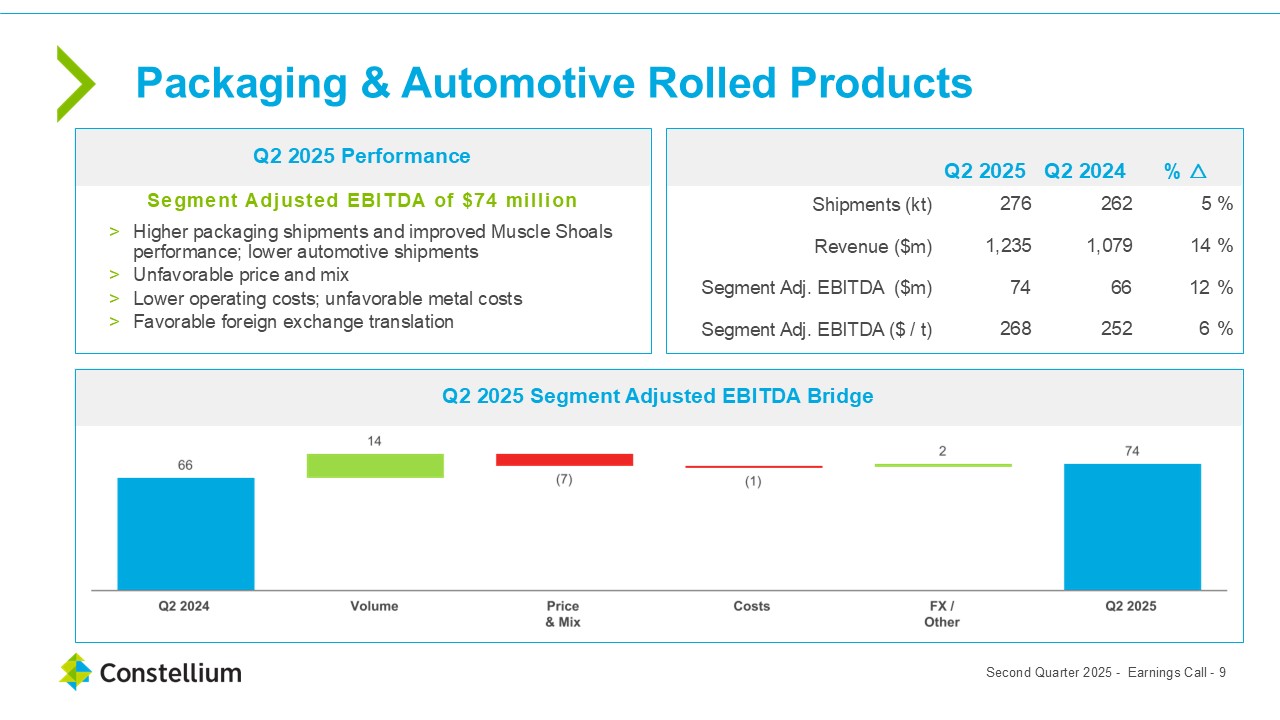

Q2 2025 Q2 2024 % △ Shipments (kt) 276 262 5 % Revenue

($m) 1,235 1,079 14 % Segment Adj. EBITDA ($m) 74 66 12 % Segment Adj. EBITDA ($ / t) 268 252 6 % Packaging & Automotive Rolled Products Q2 2025 Segment Adjusted EBITDA Bridge Q2 2025 Performance Second Quarter 2025 -

Earnings Call - 9 Segment Adjusted EBITDA of $74 million Higher packaging shipments and improved Muscle Shoals performance; lower automotive shipments Unfavorable price and mix Lower operating costs; unfavorable metal costs Favorable

foreign exchange translation

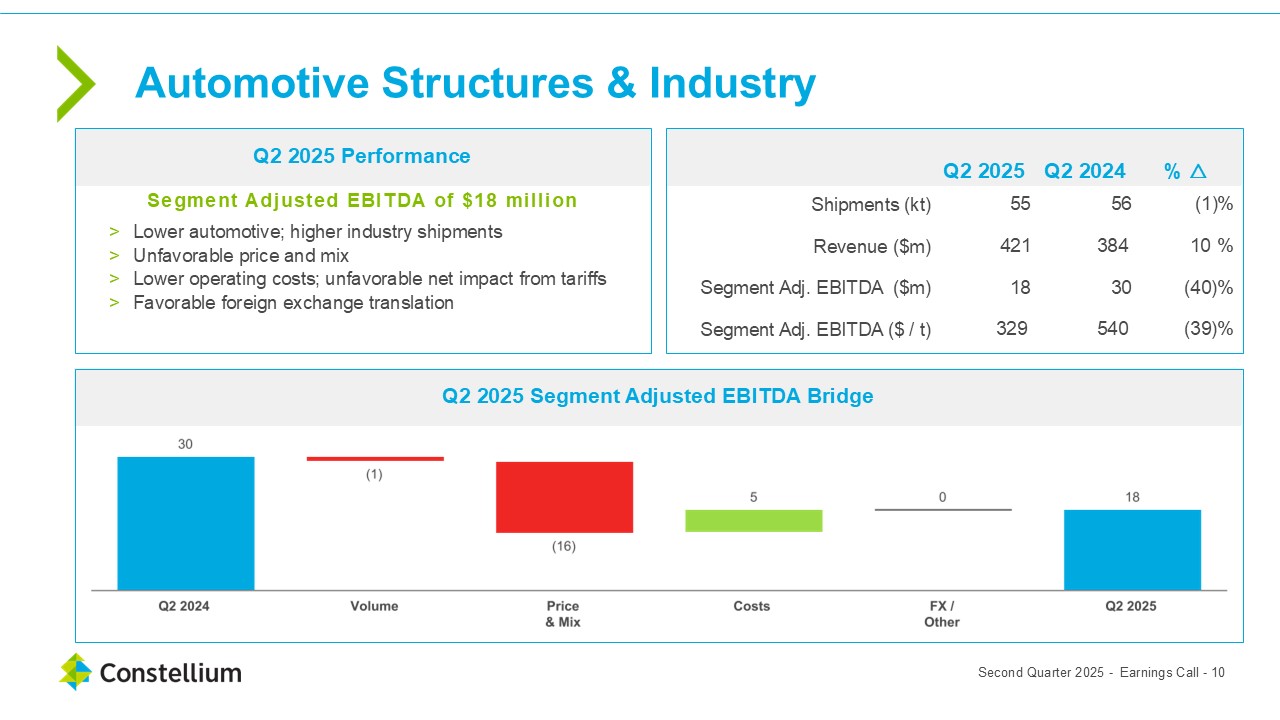

Q2 2025 Q2 2024 % △ Shipments (kt) 55 56 (1) % Revenue ($m) 421 384

10 % Segment Adj. EBITDA ($m) 18 30 (40) % Segment Adj. EBITDA ($ / t) 329 540 (39) % Automotive Structures & Industry Q2 2025 Segment Adjusted EBITDA Bridge Q2 2025 Performance Second Quarter 2025 - Earnings Call -

10 Segment Adjusted EBITDA of $18 million Lower automotive; higher industry shipments Unfavorable price and mix Lower operating costs; unfavorable net impact from tariffs Favorable foreign exchange translation

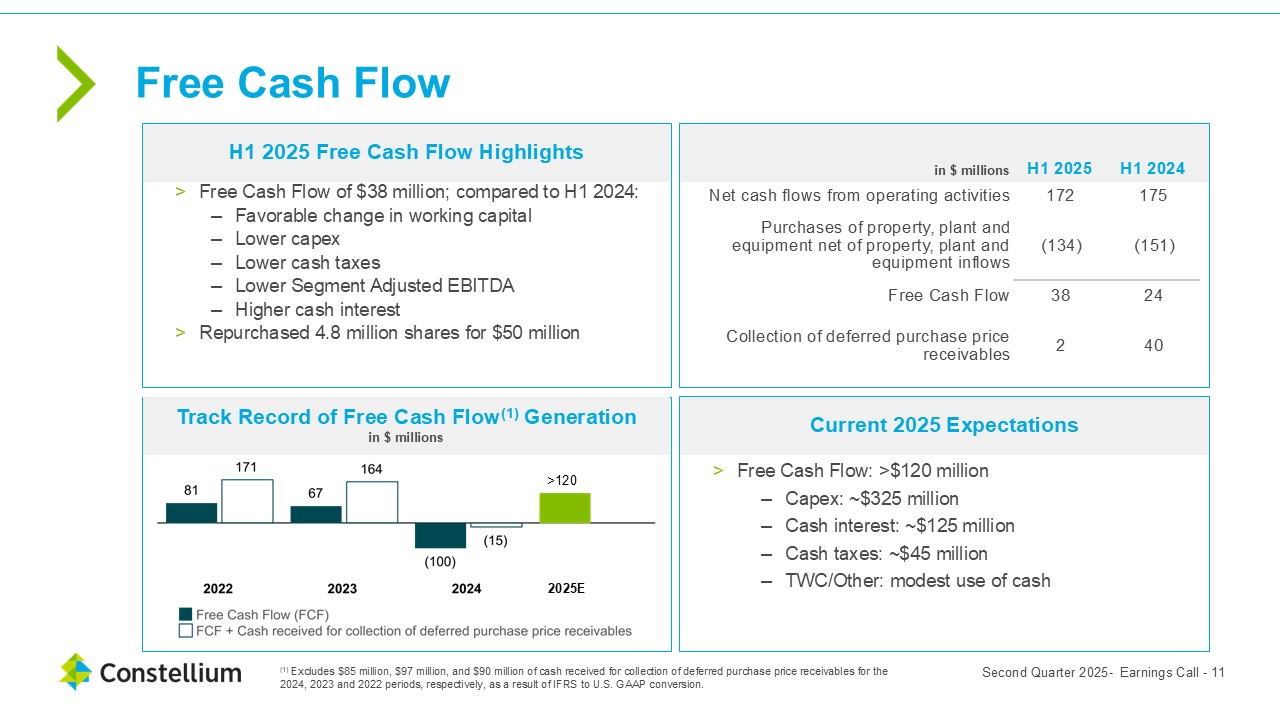

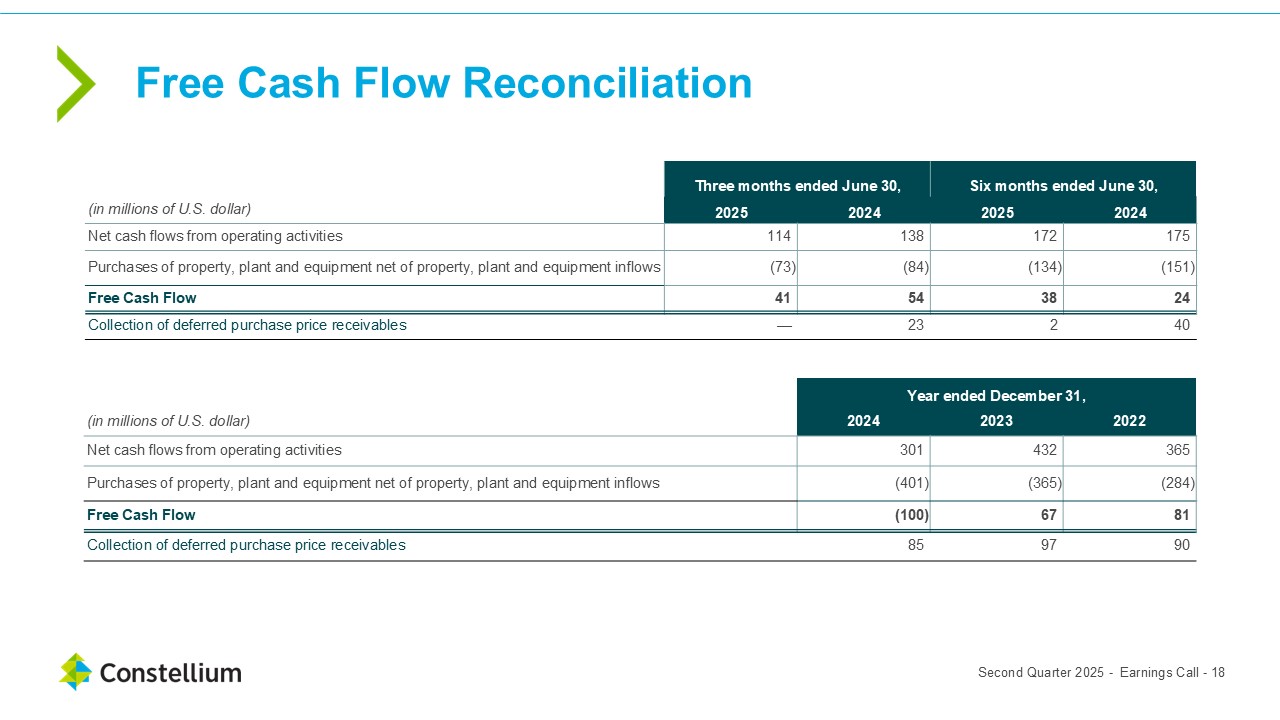

Free Cash Flow of $38 million; compared to H1 2024: Favorable change in working

capital Lower capex Lower cash taxes Lower Segment Adjusted EBITDA Higher cash interest Repurchased 4.8 million shares for $50 million in $ millions H1 2025 H1 2024 Net cash flows from operating activities 172 175 Purchases of

property, plant and equipment net of property, plant and equipment inflows (134) (151) Free Cash Flow 38 24 Collection of deferred purchase price receivables 2 40 Track Record of Free Cash Flow(1) Generation in $ millions H1 2025

Free Cash Flow Highlights Current 2025 Expectations Second Quarter 2025- Earnings Call - 11 (1) Excludes $85 million, $97 million, and $90 million of cash received for collection of deferred purchase price receivables for the 2024, 2023 and

2022 periods, respectively, as a result of IFRS to U.S. GAAP conversion. >120 Free Cash Flow: >$120 million Capex: ~$325 million Cash interest: ~$125 million Cash taxes: ~$45 million TWC/Other: modest use of cash Free Cash

Flow 2025E

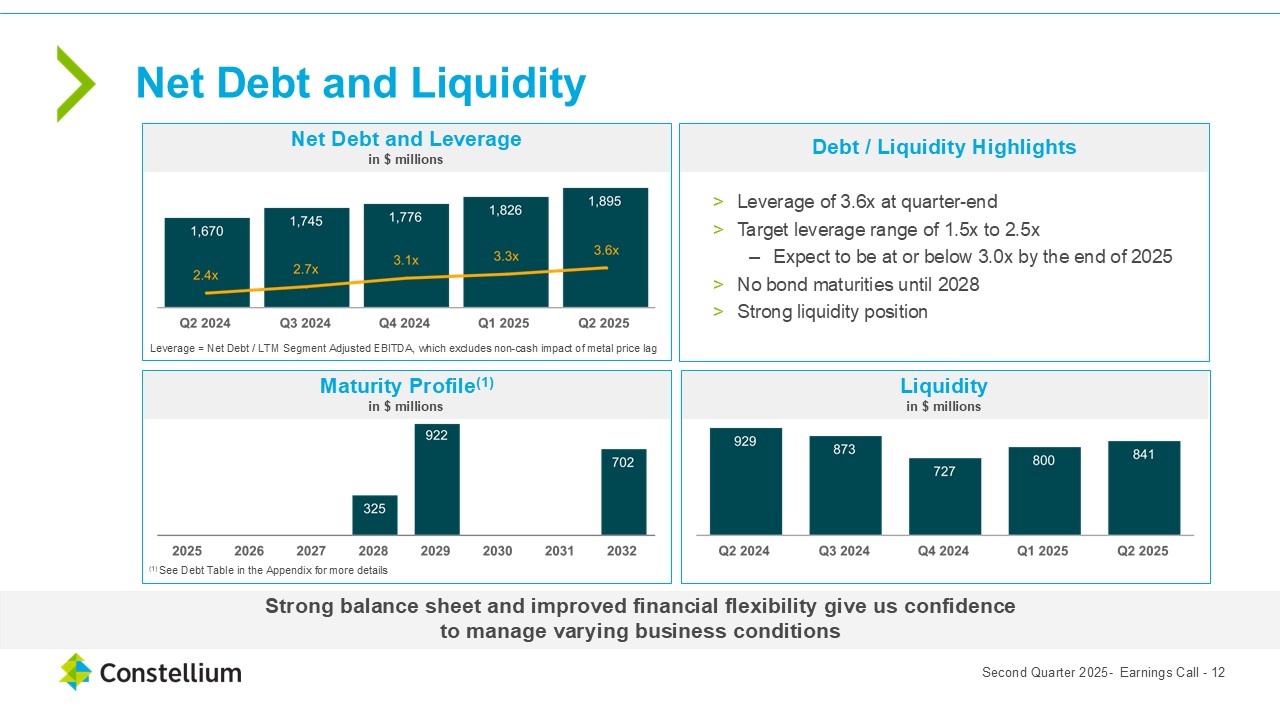

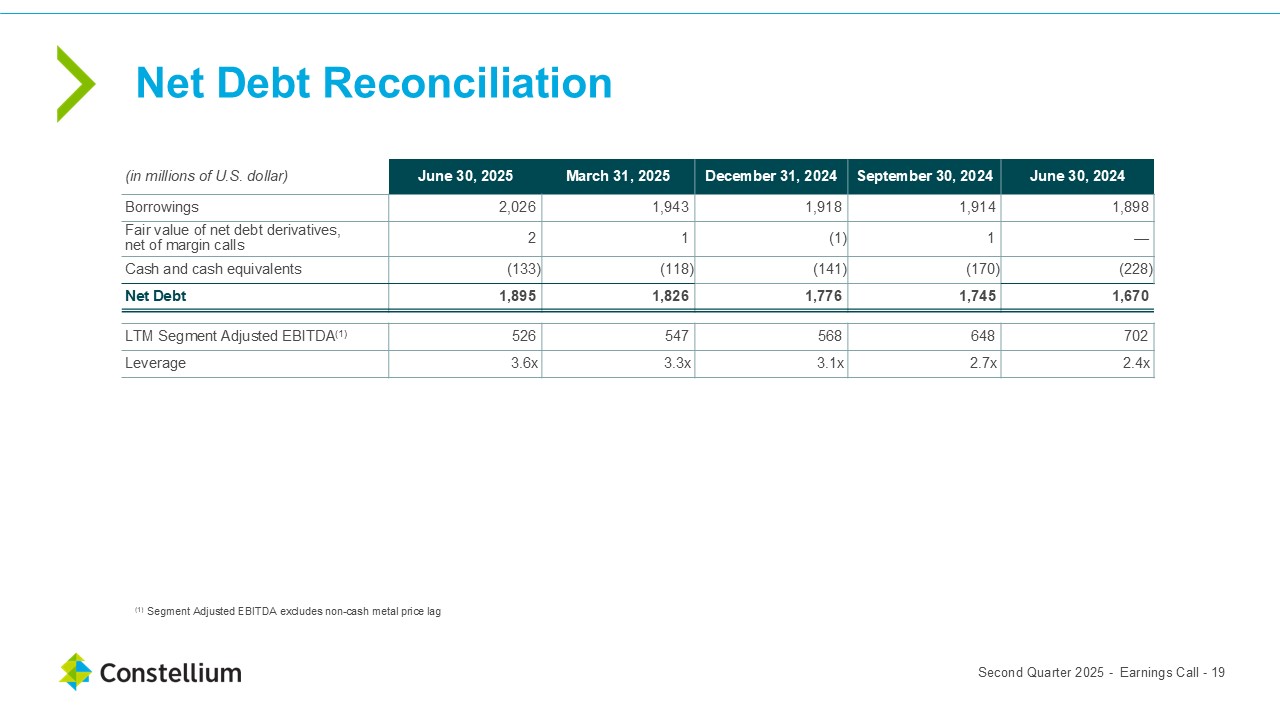

Leverage of 3.6x at quarter-end Target leverage range of 1.5x to 2.5x Expect to

be at or below 3.0x by the end of 2025 No bond maturities until 2028 Strong liquidity position Debt / Liquidity Highlights Net Debt and Liquidity Maturity Profile(1) in $ millions Liquidity in $ millions Net Debt and Leverage in $

millions Strong balance sheet and improved financial flexibility give us confidence to manage varying business conditions Leverage = Net Debt / LTM Segment Adjusted EBITDA, which excludes non-cash impact of metal price lag (1) See Debt

Table in the Appendix for more details Second Quarter 2025- Earnings Call - 12

Jean-Marc Germain Chief Executive Officer

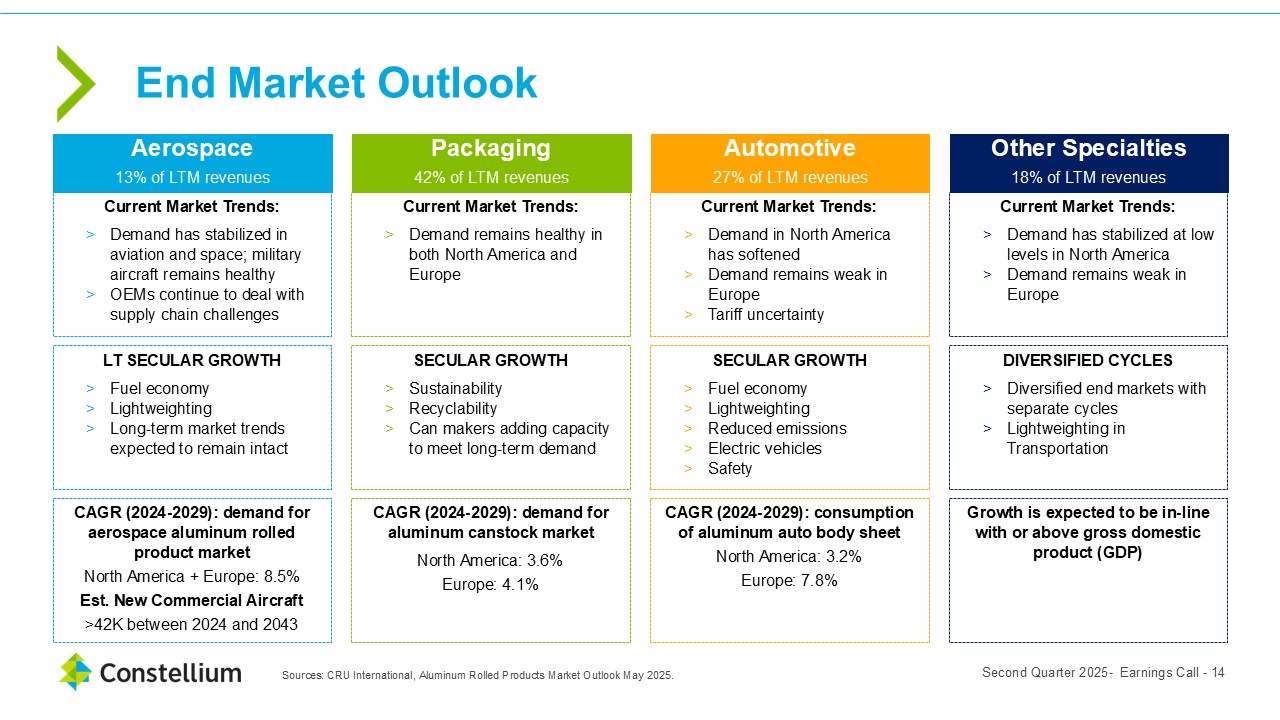

End Market Outlook Second Quarter 2025- Earnings Call - 14 Sources: CRU

International, Aluminum Rolled Products Market Outlook May 2025. Aerospace 13% of LTM revenues Packaging 42% of LTM revenues Automotive 27% of LTM revenues Other Specialties 18% of LTM revenues Current Market Trends: Demand in North

America has softened Demand remains weak in Europe Tariff uncertainty Current Market Trends: Demand has stabilized at low levels in North America Demand remains weak in Europe Current Market Trends: Demand remains healthy in both North

America and Europe Current Market Trends: Demand has stabilized in aviation and space; military aircraft remains healthy OEMs continue to deal with supply chain challenges SECULAR GROWTH Fuel economy Lightweighting Reduced

emissions Electric vehicles Safety DIVERSIFIED CYCLES Diversified end markets with separate cycles Lightweighting in Transportation SECULAR GROWTH Sustainability Recyclability Can makers adding capacity to meet long-term demand LT

SECULAR GROWTH Fuel economy Lightweighting Long-term market trends expected to remain intact CAGR (2024-2029): demand for aluminum canstock market North America: 3.6% Europe: 4.1% CAGR (2024-2029): demand for aerospace aluminum rolled

product market North America + Europe: 8.5% Est. New Commercial Aircraft >42K between 2024 and 2043 CAGR (2024-2029): consumption of aluminum auto body sheet North America: 3.2% Europe: 7.8% Growth is expected to be in-line with or

above gross domestic product (GDP)

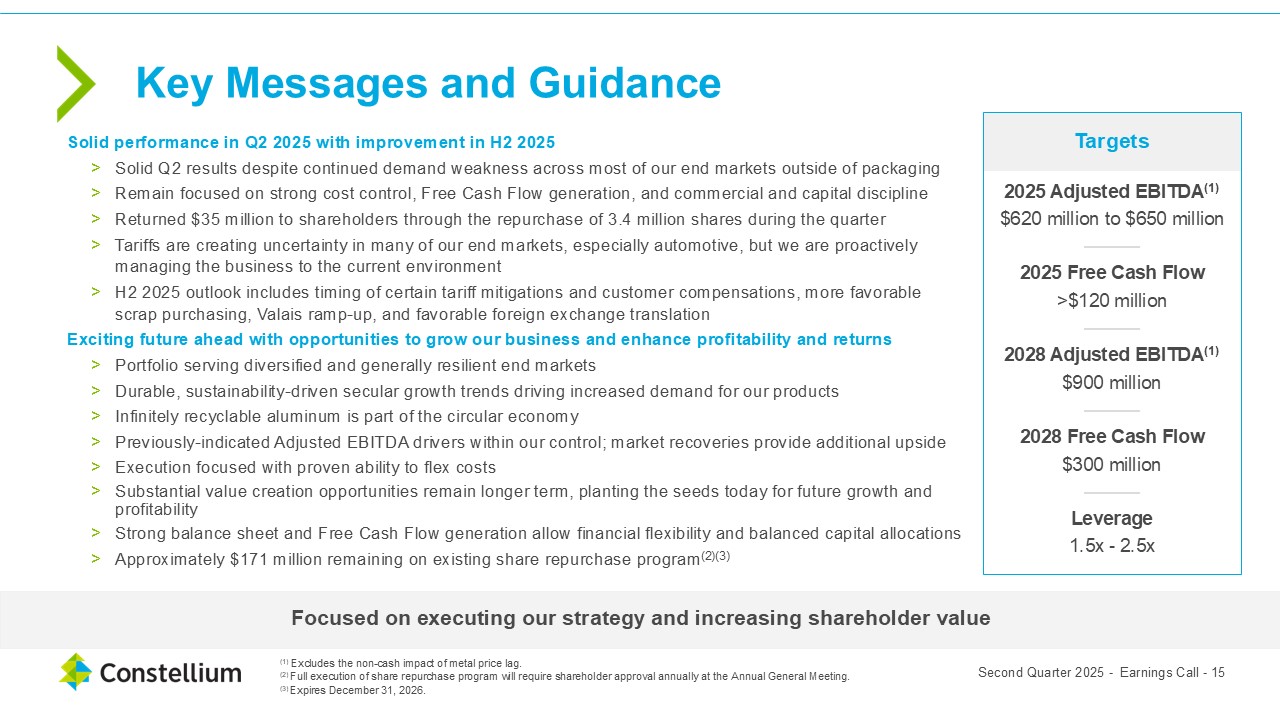

Solid performance in Q2 2025 with improvement in H2 2025 Solid Q2 results despite

continued demand weakness across most of our end markets outside of packaging Remain focused on strong cost control, Free Cash Flow generation, and commercial and capital discipline Returned $35 million to shareholders through the repurchase

of 3.4 million shares during the quarter Tariffs are creating uncertainty in many of our end markets, especially automotive, but we are proactively managing the business to the current environment H2 2025 outlook includes timing of certain

tariff mitigations and customer compensations, more favorable scrap purchasing, Valais ramp-up, and favorable foreign exchange translation Exciting future ahead with opportunities to grow our business and enhance profitability and

returns Portfolio serving diversified and generally resilient end markets Durable, sustainability-driven secular growth trends driving increased demand for our products Infinitely recyclable aluminum is part of the circular

economy Previously-indicated Adjusted EBITDA drivers within our control; market recoveries provide additional upside Execution focused with proven ability to flex costs Substantial value creation opportunities remain longer term, planting

the seeds today for future growth and profitability Strong balance sheet and Free Cash Flow generation allow financial flexibility and balanced capital allocations Approximately $171 million remaining on existing share repurchase

program(2)(3) Key Messages and Guidance Focused on executing our strategy and increasing shareholder value Targets (1) Excludes the non-cash impact of metal price lag. (2) Full execution of share repurchase program will require shareholder

approval annually at the Annual General Meeting. (3) Expires December 31, 2026. Second Quarter 2025 - Earnings Call - 15 2025 Adjusted EBITDA(1) $620 million to $650 million ——— 2025 Free Cash Flow >$120 million ——— 2028 Adjusted

EBITDA(1) $900 million ——— 2028 Free Cash Flow $300 million ——— Leverage 1.5x - 2.5x

Appendix

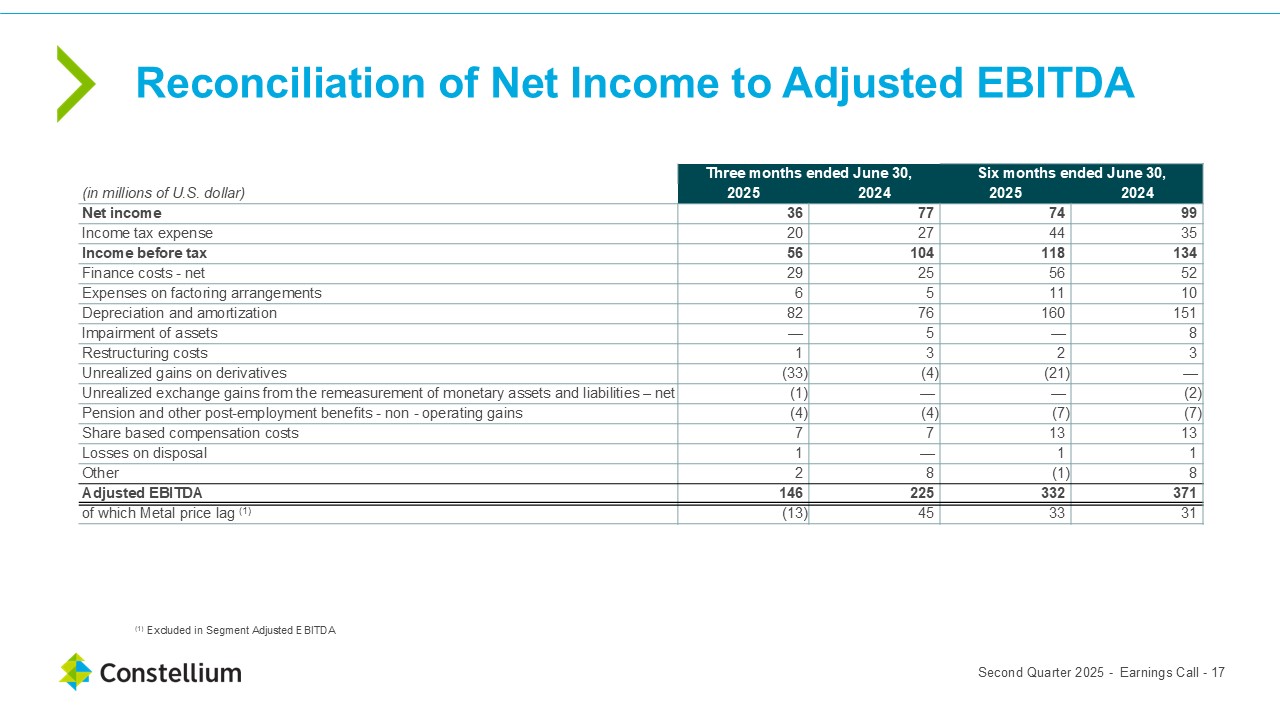

Reconciliation of Net Income to Adjusted EBITDA ≥130 Three months ended June

30, Six months ended June 30, (in millions of U.S. dollar) 2025 2024 2025 2024 Net income 36 77 74 99 Income tax expense 20 27 44 35 Income before tax 56 104 118 134 Finance costs - net 29 25

56 52 Expenses on factoring arrangements 6 5 11 10 Depreciation and amortization 82 76 160 151 Impairment of assets — 5 — 8 Restructuring costs 1 3 2 3 Unrealized gains on

derivatives (33) (4) (21) — Unrealized exchange gains from the remeasurement of monetary assets and liabilities – net (1) — — (2) Pension and other post-employment benefits - non - operating gains (4) (4) (7)

(7) Share based compensation costs 7 7 13 13 Losses on disposal 1 — 1 1 Other 2 8 (1) 8 Adjusted EBITDA 146 225 332 371 of which Metal price lag (1) (13) 45 33 31 Second Quarter

2025 - Earnings Call - 17 (1) Excluded in Segment Adjusted EBITDA

Three months ended June 30, Six months ended June 30, (in millions of U.S.

dollar) 2025 2024 2025 2024 Net cash flows from operating activities 114 138 172 175 Purchases of property, plant and equipment net of property, plant and equipment inflows (73) (84) (134) (151) Free Cash Flow 41

54 38 24 Collection of deferred purchase price receivables — 23 2 40 Year ended December 31, (in millions of U.S. dollar) 2024 2023 2022 Net cash flows from operating activities 301 432 365 Purchases of

property, plant and equipment net of property, plant and equipment inflows (401) (365) (284) Free Cash Flow (100) 67 81 Collection of deferred purchase price receivables 85 97 90 Second Quarter 2025 - Earnings Call -

18 Free Cash Flow Reconciliation

Net Debt Reconciliation ≥130 (in millions of U.S. dollar) June 30, 2025 March

31, 2025 December 31, 2024 September 30, 2024 June 30, 2024 Borrowings 2,026 1,943 1,918 1,914 1,898 Fair value of net debt derivatives, net of margin calls 2 1 (1) 1 — Cash and cash equivalents (133)

(118) (141) (170) (228) Net Debt 1,895 1,826 1,776 1,745 1,670 LTM Segment Adjusted EBITDA(1) 526 547 568 648 702 Leverage 3.6x 3.3x 3.1x 2.7x 2.4x (1) Segment Adjusted EBITDA excludes non-cash

metal price lag Second Quarter 2025 - Earnings Call - 19

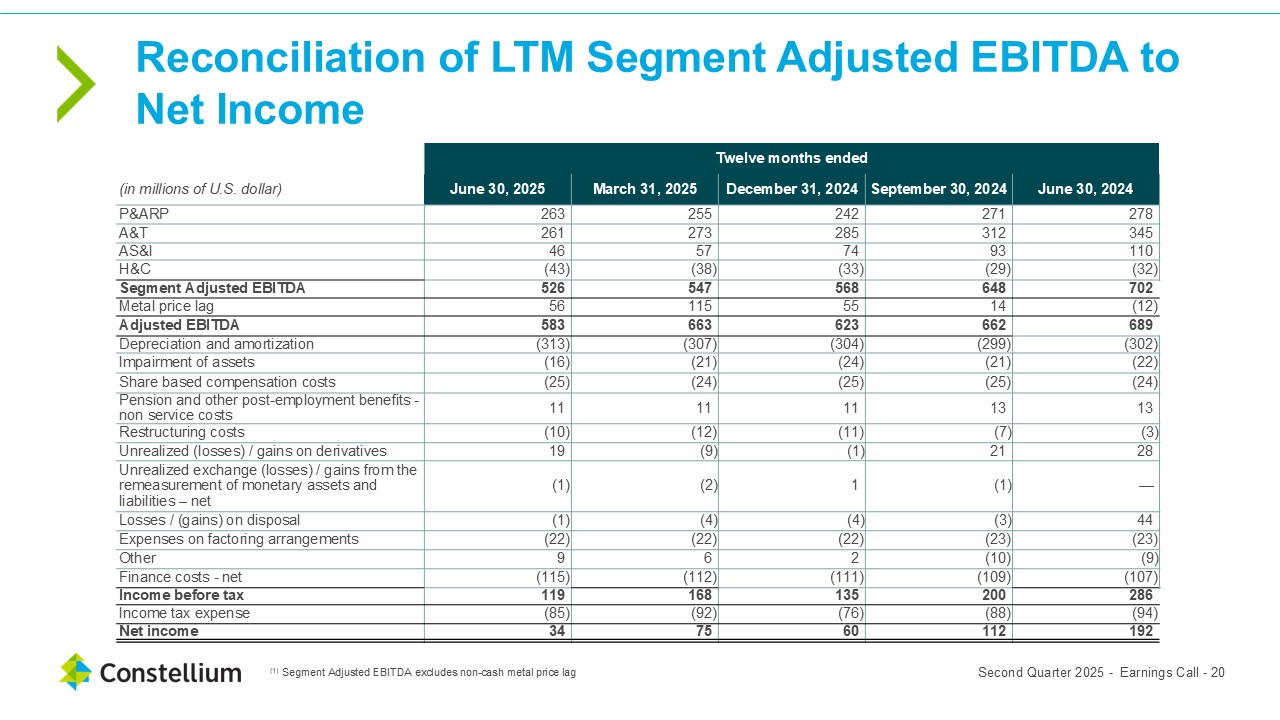

Reconciliation of LTM Segment Adjusted EBITDA to Net Income ≥130 Twelve months

ended (in millions of U.S. dollar) June 30, 2025 March 31, 2025 December 31, 2024 September 30, 2024 June 30, 2024 P&ARP 263 255 242 271 278 A&T 261 273 285 312 345 AS&I 46 57 74 93

110 H&C (43) (38) (33) (29) (32) Segment Adjusted EBITDA 526 547 568 648 702 Metal price lag 56 115 55 14 (12) Adjusted EBITDA 583 663 623 662 689 Depreciation and

amortization (313) (307) (304) (299) (302) Impairment of assets (16) (21) (24) (21) (22) Share based compensation costs (25) (24) (25) (25) (24) Pension and other post-employment benefits - non service costs

11 11 11 13 13 Restructuring costs (10) (12) (11) (7) (3) Unrealized (losses) / gains on derivatives 19 (9) (1) 21 28 Unrealized exchange (losses) / gains from the remeasurement of monetary assets and

liabilities – net (1) (2) 1 (1) — Losses / (gains) on disposal (1) (4) (4) (3) 44 Expenses on factoring arrangements (22) (22) (22) (23) (23) Other 9 6 2 (10) (9) Finance costs - net (115)

(112) (111) (109) (107) Income before tax 119 168 135 200 286 Income tax expense (85) (92) (76) (88) (94) Net income 34 75 60 112 192 (1) Segment Adjusted EBITDA excludes non-cash metal price

lag Second Quarter 2025 - Earnings Call - 20

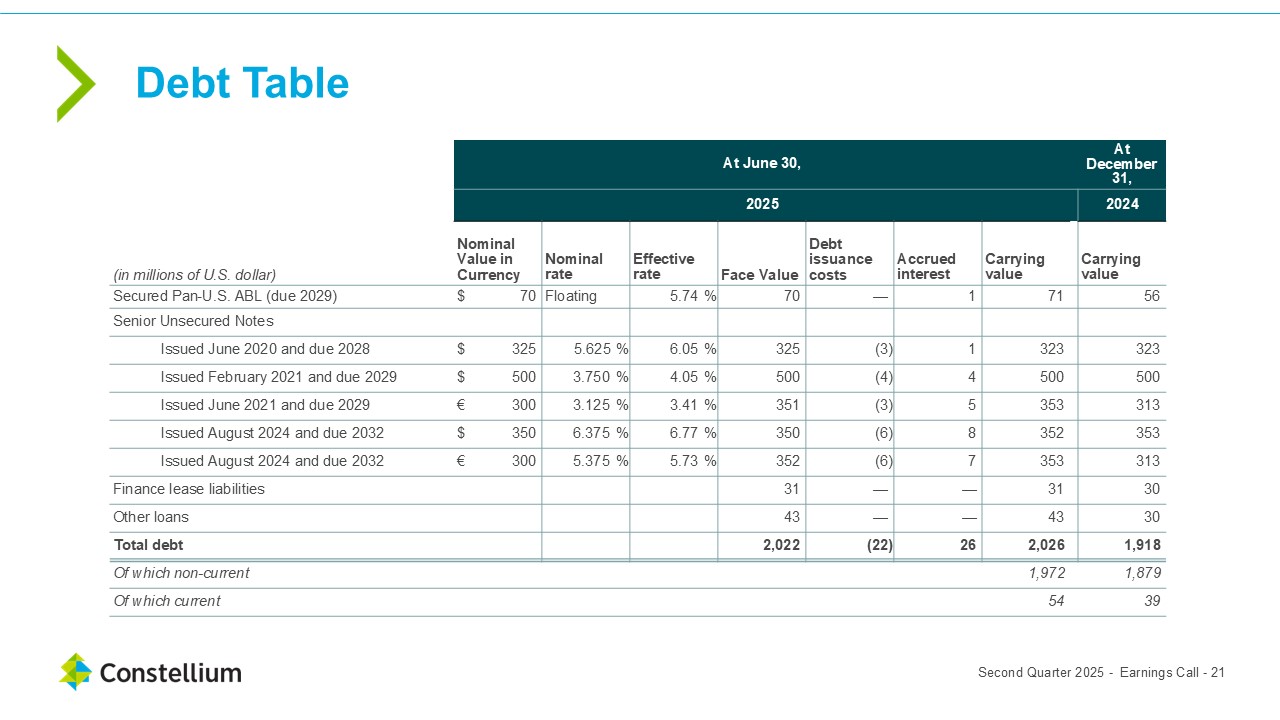

Debt Table ≥130 Second Quarter 2025 - Earnings Call - 21 At June 30, At

December 31, 2025 2024 (in millions of U.S. dollar) Nominal Value in Currency Nominal rate Effective rate Face Value Debt issuance costs Accrued interest Carrying value Carrying value Secured Pan-U.S. ABL (due 2029) $ 70

Floating 5.74 % 70 — 1 71 56 Senior Unsecured Notes Issued June 2020 and due 2028 $ 325 5.625 % 6.05 % 325 (3) 1 323 323 Issued February 2021 and due 2029 $ 500 3.750 % 4.05 % 500 (4) 4

500 500 Issued June 2021 and due 2029 € 300 3.125 % 3.41 % 351 (3) 5 353 313 Issued August 2024 and due 2032 $ 350 6.375 % 6.77 % 350 (6) 8 352 353 Issued August 2024 and due 2032 € 300 5.375

% 5.73 % 352 (6) 7 353 313 Finance lease liabilities 31 — — 31 30 Other loans 43 — — 43 30 Total debt 2,022 (22) 26 2,026 1,918 Of which non-current 1,972 1,879 Of which

current 54 39