Exhibit 99.1

English translation

for courtesy purposes only. In case of discrepancies between the Italian version

and the English version, the Italian version shall prevail

OFFER DOCUMENT

VOLUNTARY PUBLIC EXCHANGE OFFER

pursuant to Articles 102 and 106, paragraph 4, of Legislative Decree No. 58 of 24 February 1998, as subsequently amended and supplemented

concerning the ordinary shares of

ISSUER

OFFEROR

Financial Instruments subject to the Offer

maximum of No. 833,279,689 ordinary shares of MEDIOBANCA – Banca di Credito Finanziario Società per Azioni, as well as maximum of No. 16,178,862 additional shares of MEDIOBANCA – Banca di Credito Finanziario Società per Azioni which may be allocated under certain existing incentive plans

Unit consideration offered

No. 2.533 newly issued ordinary shares of Banca Monte dei Paschi di Siena S.p.A. admitted to trading on Euronext Milan, a regulated market organized and managed by Borsa Italiana S.p.A. for each ordinary share of Mediobanca – Banca di Credito Finanziario Società per Azioni tendered in acceptance of the Offer, subject to any further adjustments as set out in Section E of this Offer Document

Duration of the Offer acceptance period agreed with Borsa Italiana S.p.A.

from 8:30 a.m. (Italian time) on 14 July 2025 to 5:30 p.m. (Italian time) on 8 September 2025, both dates inclusive (unless the acceptance period is extended)

Consideration payment date

15 September 2025, unless the acceptance period is extended

Financial advisors to the Offeror

Intermediaries appointed to coordinate the collection of acceptances

Global Information Agent

The approval of the Offer Document, issued with CONSOB resolution No. 23623 on 2 July 2025, does not entail any opinion by CONSOB on the advisability to accept the Offer and regarding the data and information contained in this document.

3 July 2025

Disclaimer

The shares to be issued in connection with the Offer may not be offered or sold in the United States except pursuant to an effective registration statement under the U.S. Securities Act of 1933 (the “U.S. Securities Act”) or pursuant to a valid exemption from registration.

The Offer is being made for the shares of the Issuer by the Offeror, each of which is a company incorporated in Italy. Information distributed in connection with the Offer is subject to Italian disclosure requirements that are different from those of the United States. Financial statements and financial information included in the Offer Document or the Exemption Document, if any, have been prepared in accordance with the international accounting standards issued by the International Accounting Standards Board and may not be comparable to the financial statements or financial information of U.S. companies.

It may be difficult for you to enforce your rights and any claim you may have arising under U.S. federal securities laws in respect of the Offer, since the Offeror and the Issuer are located in Italy, and some or all of their officers and directors may be residents of Italy or other countries outside the U.S. You may not be able to sue a company incorporated outside the U.S. or its officers or directors in a non-U.S. court for violations of U.S. securities laws. It may be difficult to compel a company incorporated outside the U.S. and its affiliates to subject themselves to a U.S. court’s judgment.

The Offer will not be submitted to the review or registration procedures of any regulator outside of Italy and has not been approved or recommended by any governmental securities regulator. The Offer will be made in the U.S. pursuant to the exemptions from (i) the “U.S. tender offer rules” under the United States Securities Exchange Act of 1934 (the “U.S. Exchange Act”) provided by Rule 14d-1(c) thereunder and (ii) the registration requirements of the U.S. Securities Act provided by Rule 802 thereunder. These exemptions permit a bidder to satisfy certain substantive and procedural U.S. Exchange Act rules governing tender offers by complying with home jurisdiction law or practice, and exempt the bidder from compliance with certain other U.S. Exchange Act rules. As a result, the Offer will be made in accordance with the applicable regulatory, disclosure and procedural requirements under Italian law, including with respect to withdrawal rights, offer timetable, settlement procedures and timing of payments, that are different from those applicable in the U.S. To the extent that the Offer is subject to the U.S. securities laws, such laws only apply to holders of the Mediobanca Shares in the U.S. and no other person has any claims under such laws.

To the extent permissible under applicable law or regulation in Italy, and pursuant to the exemptions available under Rule 14e-5(b) under the U.S. Exchange Act, the Offeror and its affiliates or brokers (acting as agents for the Offeror or its affiliates, as applicable) may from time to time, and other than pursuant to the Offer, directly or indirectly purchase, or arrange to purchase, the Mediobanca Shares, that are the subject of the Offer or any securities that are convertible into, exchangeable for or exercisable for such shares, including purchases in the open market at prevailing prices or in private transactions at negotiated prices outside the U.S. To the extent information about such purchases or arrangements to purchase is made public in Italy, if any such purchases are made, such information will be disclosed by means of a press release or other means reasonably calculated to inform U.S. shareholders of the Issuer of such information. In addition, the financial advisors to the Offeror, may also engage in

2

ordinary course trading activities in securities of the Issuer, which may include purchases or arrangements to purchase such securities.

Since the announcement of the Offer, the Offeror and certain of its affiliates have engaged, and intend to continue to engage throughout the Acceptance Period, in various asset management, brokerage, banking-related, collateral-taking, estates and trusts services, and custody-related activities involving the Offeror common shares outside the United States. Among other things, the Offeror or one or more of its affiliates intends to engage in trades in the Offeror common shares for the accounts of its customers for the purpose of effecting brokerage transactions for its customers and other customer facilitation transactions in respect of the Offeror common shares. Further, certain of Offeror’s asset management affiliates may buy and sell the Offeror common shares or indices including the Offeror common shares, outside the United States as part of their ordinary, discretionary investment management activities on behalf of their customers. Certain of Offeror’s affiliates may continue to (a) engage in the marketing and sale to customers of funds that include the Offeror common shares, providing investment advice and financial planning guidance to customers that may include information about the Offeror common shares, (b) transact in the Offeror common shares as trustees and/or personal representatives of trusts and estates, (c) provide custody services relating to the Offeror common shares and (d) engage in accepting the Offeror common shares as collateral for loans.

These activities occur outside of the United States and the transactions in the Offeror common shares may be effected on the Euronext Milan, other exchanges or alternative trading systems and in the over-the-counter market.

3

| INDEX | |

| LIST OF MAIN DEFINITIONS | 9 |

| RECITALS | 21 |

| 1. | Subject of the Offer | 21 | |

| 2. | Legal assumptions and characteristics of the Offer | 22 | |

| 3. | The voluntary public exchange offer promoted by Mediobanca on Banca Generali S.p.A. | 25 | |

| 4. | Reasons for the Offer and overview of future plans | 26 | |

| 5. | Table of key events relating to the Offer | 32 | |

| 6. | Markets on which the Offer is promoted | 38 |

| A. | WARNINGS | 39 |

| A.1. | Conditions of Effectiveness of the Offer | 39 |

| A.1.1. | Conditions of Effectiveness | 39 | |

| A.1.2. | Preliminary Authorizations and Other Authorizations | 41 | |

| A.1.3. | Antitrust Condition | 48 | |

| A.1.4. | Threshold Condition and Minimum Threshold Condition | 48 | |

| A.1.5. | Relevant Acts Condition | 50 | |

| A.1.6. | MAE Condition | 51 | |

| A.1.7. | Amendment or Waiver to the Conditions of Effectiveness | 51 | |

| A.2. | Financial reports and interim financial statements of the Issuer | 52 | |

| A.3. | Related Parties | 53 | |

| A.4. | Evaluation criteria underlying the determination of the Consideration | 54 | |

| A.5. | The Capital Increase Reserved to the Offer | 58 |

| A.5.1. | Corporate procedure applicable to the Capital Increase Reserved to the Offer | 58 | |

| A.5.2. | Absence of effects on the Offer Consideration | 61 | |

| A.5.3. | Possible unavailability of MPS Shares offered as Consideration | 62 |

| A.6. | Treatment of fractions of MPS Shares offered as Consideration | 62 | |

| A.7. | Reasons for the Offer and summary of the Offeror’s future plans in relation to the Issuer | 63 | |

| A.8. | Transactions upon completion of the Offer | 66 | |

| A.9. | Communications and authorizations for the carrying out of the Offer | 67 | |

| A.10. | Reopening of the Acceptance Period | 67 | |

| A.11. | Declaration by the Offeror regarding the possible restoration of the free float and the sell-out pursuant to Article 108, paragraph 2, of the TUF | 68 | |

| A.12. | Declaration by the Offeror regarding the fulfilment of the sell-out pursuant to Article 108, paragraph 1, of the TUF and the simultaneous squeeze-out pursuant to Article 111 of the TUF | 69 | |

| A.13. | Possible shortage of the free float | 71 | |

| A.14. | Potential conflicts of interest | 72 |

4

| A.15. | Possible alternative scenarios for Mediobanca shareholders | 74 |

| A.15.1. | Scenarios in case of completion of the Offer | 74 |

| A.15.1.1. | Acceptance of the Offer | 74 | |

| A.15.1.2. | Non-acceptance of the Offer | 75 |

| (A) | Achievement of a shareholding equal to or less than 90% of the Issuer’s share capital | 75 | |

| (B) | Achievement of a shareholding of more than 90% but less than 95% of the Issuer’s share capital | 75 | |

| (C) | Achievement of a shareholding of at least 95% of the Issuer’s ordinary share capital | 76 | |

| (D) | Transaction upon completion of the Offer | 76 | |

| A.15.2 | Scenarios in the event of failure of the Offer | 78 | |

| A.16. | Rights of Mediobanca shareholders who tendered in acceptance of the Offer the Shares Subject to the Offer | 78 | |

| A.17. | The voluntary public exchange offer promoted by Mediobanca on Banca Generali S.p.A. | 79 | |

| A.18. | Issuer’s Communication | 80 | |

| A.19. | Critical issues related to the national and international macroeconomic context | 80 |

| B. | PARTIES INVOLVED IN THE TRANSACTION | 82 |

| B.1. | The Offeror | 82 | |

| B.1.1. | Name, legal form, registered office and trading market | 82 | |

| B.1.2. | Incorporation and lifetime | 82 | |

| B.1.3. | Applicable law and jurisdiction | 82 | |

| B.1.4. | Corporate purpose | 82 | |

| B.1.5. | Share Capital | 83 | |

| B.1.6. | Major shareholders | 83 | |

| B.1.7. | Management and control bodies | 84 | |

| B.1.8. | Activities of the Offeror and brief description of the MPS Group | 88 | |

| B.1.9. | Accounting Standards | 90 | |

| B.1.10. | Consolidated financial information | 91 | |

| B.1.11. | Recent trend | 91 | |

| B.2. | Issuer of the financial instruments subject to the Offer | 105 |

| B.2.1. | Name, legal form, registered office and trading market | 105 | |

| B.2.2. | Share Capital | 105 | |

| B.2.3. | Significant shareholders and shareholders’ agreements | 114 | |

| B.2.4. | Management and control bodies | 115 | |

| B.2.5. | Activities of the Issuer and brief description of the Mediobanca Group | 119 | |

| B.2.6. | Key financial information | 122 | |

| B.2.6.1. | Balance sheet and income statement of Mediobanca as of 30 June 2024 | 123 | |

| B.2.6.2. | Mediobanca’s balance sheet and income statement as of 31 December 2024 | 129 |

5

| B.2.7. | Recent trend and outlooks | 135 |

| B.3. | Intermediaries | 135 | |

| B.4. | Global Information Agent | 136 |

| C. | CATEGORIES AND QUANTITIES OF THE FINANCIAL INSTRUMENTS SUBJECT TO THE OFFER | 137 |

| C.1. | Category of the financial instruments subject to the Offer and related quantities and percentages | 137 | |

| C.2. | Authorizations | 137 |

| D. | FINANCIAL INSTRUMENTS OF THE ISSUER OR HAVING AS UNDERLYING ASSETS SUCH INSTRUMENTS HELD BY THE OFFEROR, INCLUDING THROUGH TRUST COMPANIES OR INDERMEDIARIES | 146 |

| D.1. | Number and categories of financial instruments of the Issuer held by the Offeror (including through trust companies or intermediaries) and by persons acting in concert | 146 | |

| D.2. | Repurchase agreements, securities lending agreements, usufruct and pledge rights, or other commitments with the Issuer’s shares as underlying asset | 146 |

| E. | UNIT CONSIDERATION FOR THE FINANCIAL INSTRUMENTS AND RELATED JUSTIFICATION | 147 |

| E.1. | Indication of the unit Consideration and related determination | 147 | |

| E.2. | Total countervalue of the Offer | 153 | |

| E.3. | Comparison of the Pre-Adjustment Consideration with certain indicators relating to the Issuer | 154 | |

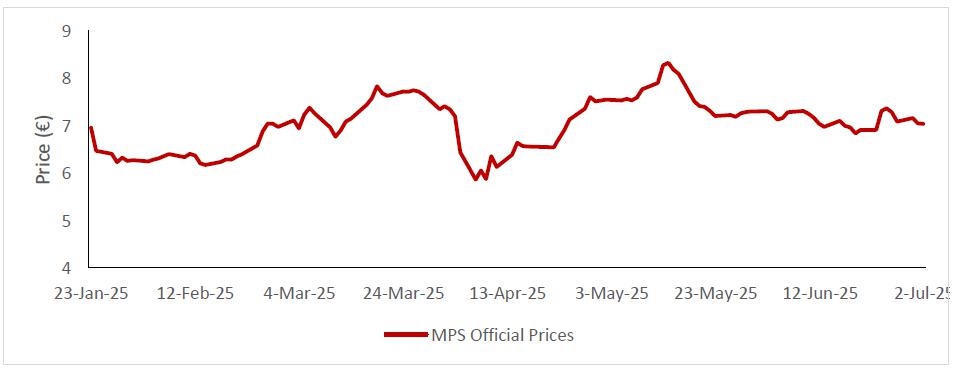

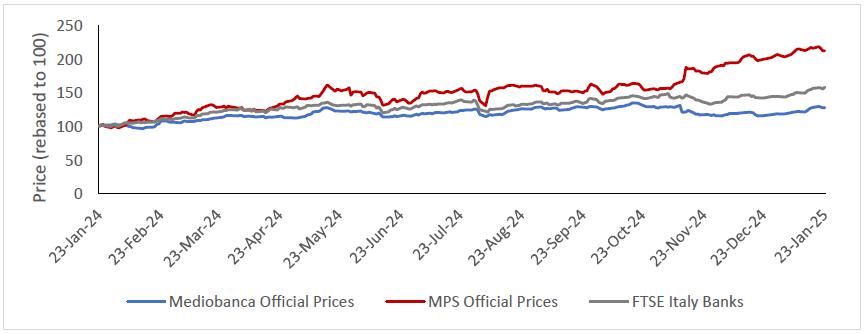

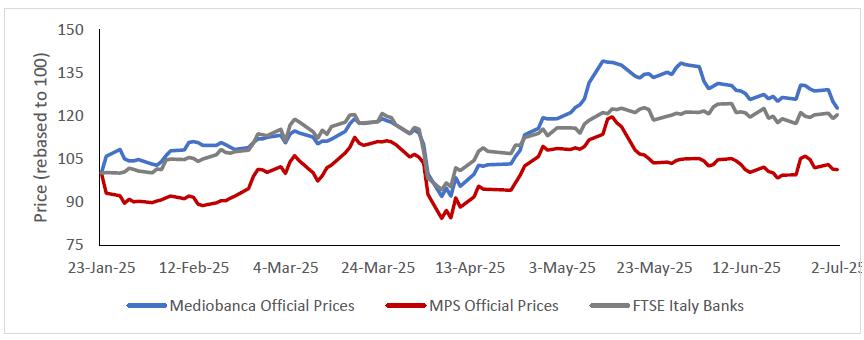

| E.4. | Monthly arithmetic and weighted average of the official prices recorded by the Issuer’s shares in the twelve months prior to the promotion of the Offer | 155 | |

| E.5. | Indication of the values attributed to the Issuer’s shares in financial transactions carried out in the last financial year and in the current financial year | 161 | |

| E.6. | Indication of the values at which the Offeror and the parties acting in concert with it have carried out transactions involving the sale and purchase of the shares subject to the Offer in the last twelve months, indicating the number of financial instruments sold and purchased | 161 |

| F. | TERMS AND CONDITIONS FOR ACCEPTING THE OFFER, DATES AND METHODS OF PAYMENT OF THE CONSIDERATION AND RETURN OF THE SECURITIES SUBJECT TO THE OFFER | 162 |

| F.1. | Terms and conditions for accepting the Offer and for depositing the Shares Subject to the Offer | 162 |

| F.1.1. | Acceptance Period and possible reopening of the acceptance period | 162 | |

| F.1.2. | Methods of acceptance and deposit of the Shares Subject to the Offer | 163 |

| F.2. | Ownership and exercise of administrative and economic rights relating to the Shares tendered in acceptance of, and during, the Offer | 165 | |

| F.3. | Communications regarding the progress and results of the Offer | 165 | |

| F.4. | Markets on which the Offer is promoted | 166 |

| F.4.1. | Italy | 166 | |

| F.4.2. | United States of America | 167 | |

| F.4.3. | Other countries | 168 |

6

| F.4.4. | Canada | 169 | |

| F.4.5. | Japan | 170 | |

| F.4.6. | Australia | 170 |

| F.5. | Consideration Payment Date | 171 | |

| F.6. | Methods of payment of the Consideration | 172 | |

| F.7. | Indication of the governing law of the contracts entered into between the Offeror and the holders of the Issuer’s financial instruments and relevant jurisdiction | 173 | |

| F.8. | Methods and terms for the return of the Shares Subject to the Offer tendered in acceptance of the Offer in the event the Offer being ineffective and/or allocation | 173 |

| G. | METHODS OF FINANCING, PERFORMANCE GUARANTEE AND OFFEROR’S FUTURE PLANS | 174 |

| G.1. | Methods of financing of the Offer and performance guarantee | 174 | |

| G.2. | Rationale of the Offer and future plans drawn up in relation to the Issuer | 174 |

| G.2.1. | Rationale of the Offer | 174 | |

| G.2.2. | Programmes relating to the management of activities | 176 | |

| G.2.2.1. | Strategic and Industrial objectives of the integration of the Issuer into the MPS Group | 176 | |

| G.2.2.2. | Synergies resulting from the Issuer’s strategic and business objectives within the MPS Group upon completion of the Offer | 178 |

| G.2.3. | Investments and future sources of financing | 181 | |

| G.2.4. | Transaction upon completion of the Offer | 181 | |

| G.2.5. | Planned changes in the composition of the corporate bodies and related remuneration | 182 | |

| G.2.6. | Amendments to the By-laws | 182 | |

| G.3. | Restoration of the free float | 182 |

| H. | ANY AGREEMENTS AND TRANSACTIONS BETWEEN THE OFFEROR, PARTIES ACTING IN CONCERT WITH THE OFFEROR AND THE ISSUER OR ITS SHAREHOLDERS OR MEMBERS OF THE ISSUER’S MANAGEMENT AND CONTROL BODIES | 185 |

| H.1. | Financial and/or commercial agreements and transactions that have been executed or approved in the twelve months prior to the publication of the Offer, which may have or have had a significant effect on the business of the Offeror and/or the Issuer | 185 | |

| H.2. | Agreements concerning the exercise of voting rights or the transfer of Shares and/or other financial instruments of the Issuer | 185 |

| I. | FEES TO INTERMEDIARIES | 186 |

| L. | ALLOCATION HYPOTHESIS | 187 |

| M. | ANNEXES | 188 |

| M.1. | Offeror’s Communication | 188 |

| N. | DOCUMENTS MADE AVAILABLE BY THE OFFEROR TO THE PUBLIC AND PLACES WHERE SUCH DOCUMENTS ARE AVAILABLE | 189 |

| N.1. | Documents relating to the Offeror | 189 | |

| N.2. | Documents relating to the Issuer | 189 |

7

| DECLARATION OF RESPONSIBILITY | 190 |

8

LIST OF MAIN DEFINITIONS

Below is a list of the main definitions used in this Offer Document. Where the context requires, terms defined in the singular shall have the same meaning in the plural and vice versa.

| Mediobanca Interim Dividend | The interim dividend based on the results as of 31 December 2024, which Mediobanca’s Board of Directors, on 8 May 2025, resolved to distribute, amounting to Euro 0.56 per each Mediobanca shares outstanding and entitled to the dividend payment, with ex-dividend date on 19 May 2025, record date on 20 May and payment date on 21 May 2025. | |

| Tendering Shareholders | The holders of the Shares Subject to the Offer who are entitled to accept the Offer and have validly tendered in acceptance of the Offer the Shares Subject to the Offer in accordance with the Offer Document. | |

| AGCM | The Italian Competition and Market Authority, with headquarters in Rome, Piazza G. Verdi No. 6/a. | |

| Offeror’s Shareholder Meeting | The Offeror’s shareholders’ meeting of 17 April 2025 which granted the Delegation to the Board of Directors of the Offeror for the execution of the Capital Increase Reserved to the Offer. | |

| Capital Increase Reserved to the Offer | The paid share capital increase of MPS reserved to the Offer, in divisible form and also in one or more tranches, to be paid-in through (and in exchange for) the contribution in kind of the Issuer’s Shares (and any Additional Shares) tendered in acceptance of the Offer (or otherwise transferred to MPS in execution of the Reopening of the Acceptance Period and/or the procedure for the fulfilment of the Sell-Out pursuant to Article 108, paragraph 2, of the TUF and/or the Joint Procedure, where applicable), therefore excluding the option right pursuant to Article 2441, paragraph 4, of the Italian Civil Code, resolved by the Offeror’s Board of Directors on 26 June 2025 – in exercise of the Delegation granted to it by the Offeror’s Shareholder’s Meeting on 17 April 2025, pursuant to Article 2443 of the Italian Civil Code – to be carried out through the issuance of a maximum of No. 2,230,000,000 MPS Shares, to be paid-in through the contribution in kind of the Shares Subject to the Offer tendered in acceptance of the Offer, even as possibly revised and/or modified. | |

| Additional Shares | The maximum No. 16,178,862 shares that may be issued by Mediobanca prior to completion of the Offer in favour of the beneficiaries of certain Incentive Plans |

9

|

(as defined below), if such Incentive Plans are revised by the competent bodies of Mediobanca to provide for their acceleration, where envisaged by the individual Incentive Plans, even though some of them envisage the possibility of using – instead of the Additional Shares – even Mediobanca’s treasury shares held in portfolio and without prejudice to the underlying limitations on the issue of Additional Shares under the Plans. | ||

| Mediobanca Shares or Issuer’s Shares | Each of the No. 833,279,689 ordinary shares of Mediobanca (including the Treasury Shares), without nominal value and admitted to trading on Euronext Milan, a regulated market organized and managed by Borsa Italiana S.p.A., with ISIN Code IT0000062957, in dematerialised form pursuant to Article 83-bis of the TUF and representing the entire share capital of the Issuer as of the Offer Document Date. | |

| Shares Subject to the Offer | Each of the maximum No. 833,279,689 Mediobanca Shares (including the Treasury Shares) and the maximum No. 16,178,862 Additional Shares (in the event that they are issued), subject to the Offer, amounting to a total of No. 849,458,551 ordinary shares of the Issuer, representing its entire share capital. | |

| MPS Shares | The maximum No. 2,230,000,000 newly issued ordinary shares of MPS resulting from the Capital Increase Reserved to the Offer, without nominal value, with regular dividend rights, and having the same features as the ordinary shares of MPS outstanding at the issue date, which will be listed on Euronext Milan, a regulated market organized and managed by Borsa Italiana S.p.A.. The above number was calculated as a matter of extreme caution and in accordance with a highly conservative approach and, therefore, as better specified in this Offer Document, without prejudice to any restructuring and/or changes to the content and/or structure of the Offer and/or possible further adjustments of the Consideration, it will not be necessary to issue all the MPS Shares. | |

| Treasury Shares | The treasury shares of the Issuer, which - as of the Offer Document Date - amount to No. 26,914,597 treasury shares, equal to approximately 3.2% of the share capital of the Issuer as of the Offer Document Date. |

10

| Banca Akros | Banca Akros S.p.A. – Banco BPM Group, with registered office in Milan, Viale Eginardo 29, share capital equal to Euro 39,433,803 fully paid-in, registered with the Companies’ Register of Milan-Monza-Brianza-Lodi, tax code No. 03064920154, listed in the Register of Banks under No. 5328, member of the Interbank Deposit Protection Fund and the National Guarantee Fund, part of the Banco BPM Banking Group, and subject to the management and coordination of Banco BPM S.p.A., pursuant to Articles 2497 et seq. of the Italian Civil Code. | |

| Bank of Italy | The Bank of Italy, with headquarters in Rome, Via Nazionale No. 91. | |

| European Central Bank or ECB | The European Central Bank, with headquarters in Frankfurt (Germany), Sonnemannstrasse No. 20. | |

| Borsa Italiana | Borsa Italiana S.p.A., the company that organizes and manages the regulated market Euronext Milan, with registered office in Milan, Piazza degli Affari No. 6. | |

| Italian Civil Code | The Italian Civil Code, approved by Royal Decree No. 262 of March 1942, as subsequently amended and supplemented. | |

| Corporate Governance Code | The Corporate Governance Code for listed companies published in January 2020 by the Corporate Governance Committee, in the version in force as of the Offer Document Date. | |

| Committee for Related Parties Transactions or Committee | The Committee for Related Parties Transactions of MPS, established pursuant to the MPS Regulation. | |

| Common Equity Tier 1 or CET1 | Pursuant to Article 26 of Regulation (EU) 575/2013, the elements of entities’ common equity tier 1 are the following: (a) capital instruments, as long as the conditions set out in Article 28 of Regulation (EU) 575/2013 or, where applicable, Article 29 are met; (b) share premium reserves relating to instruments referred to in item (a); (c) undistributed profits; (d) other cumulative components of total income; (e) other reserves; and (f) provisions for general banking risks.

Items from (c) to (f) are recognised as Common Equity Tier 1 only if they can be used without restriction and without delay by the entity to cover risks or losses when such risks or losses occur. In general, as clarified by Article 50 of Regulation (EU) 575/2013, an entity’s common equity tier 1 consists of the elements of its |

11

| common equity tier 1 after the application of the adjustments prescribed in Articles 32 to 35 of Regulation (EU) 575/2013, the deductions pursuant to Article 36 of Regulation (EU) 575/2013 and the exemptions and alternatives referred to in Articles 48, 49 and 79 of Regulation (EU) 575/2013. | ||

| CET1 Ratio or Common Equity Tier 1 Ratio | Solvency coefficient expressed by the ratio between Common Equity Tier I and RWA calculated pursuant to the provisions of Regulation (EU) 575/2013, Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 and Bank of Italy Circular No. 285 of 17 December 2013, as subsequently amended and supplemented. | |

| Issuer’s Communication | The press release that the Board of Directors of the Issuer will be required to publish, pursuant to the provisions of Article 103, paragraphs 3 and 3-bis, of the TUF and Article 39 of the Issuers’ Regulation, containing all useful information for the assessment and evaluation of the Offer. | |

| Communication on the Final Results of the Offer | The press release relating to the final results of the Offer, which will be disseminated, pursuant to Article 41, paragraph 6, of the Issuers’ Regulation. | |

| Communication on the Final Results of the Reopening of the Acceptance Period | The press release relating to the final results following the possible Reopening of the Acceptance Period, which will be disseminated by the Offeror pursuant to Article 41, paragraph 6, of the Issuers’ Regulation in the event of a Reopening of the Acceptance Period, as voluntarily applied by the Offeror. | |

| Communication on the Provisional Results of the Offer | The press release relating to the provisional results of the Offer, which will be disseminated by the Offeror pursuant to Article 36, paragraph 3 of the Issuers’ Regulation. | |

| Communication of the Provisional Results of the Reopening of the Acceptance Period | The press release relating to the provisional results of the Offer following the possible Reopening of the Acceptance Period, which will be disseminated pursuant to Article 36, paragraph 3, of the Issuers’ Regulation, in the event of the Reopening of the Acceptance Period, as voluntarily applied by the Offeror. | |

| Communication 102 or Offeror’s Communication | The Offeror’s press release required by Articles 102, paragraph 1 of the TUF and 37, paragraph 1, of the Issuers’ Regulation, disseminated on the Communication Date and published on the Offeror’s |

12

| website, attached to this Offer Document as Annex M.1. | ||

| Conditions of Effectiveness of the Offer | The conditions described in Section A, Paragraph A.1, of this Offer Document, upon whose fulfilment (or waiver by the Offeror, of all or some of them, if provided) the completion of the Offer is conditional. | |

| Financial Advisors | J.P. Morgan Securities plc, with registered office at 25 Bank Street, Canary Wharf, London, United Kingdom; UBS Europe SE, with registered office at Bockenheimer Landstrasse 2-4, Frankfurt, Germany; and Jefferies GmbH, with registered office at Bockenheimer Landstrasse 24, 60323 Frankfurt, Germany. | |

| Consob | The National Commission for Listed Companies and the Stock Exchange, with headquarters in Rome, Via G.B. Martini No. 3. | |

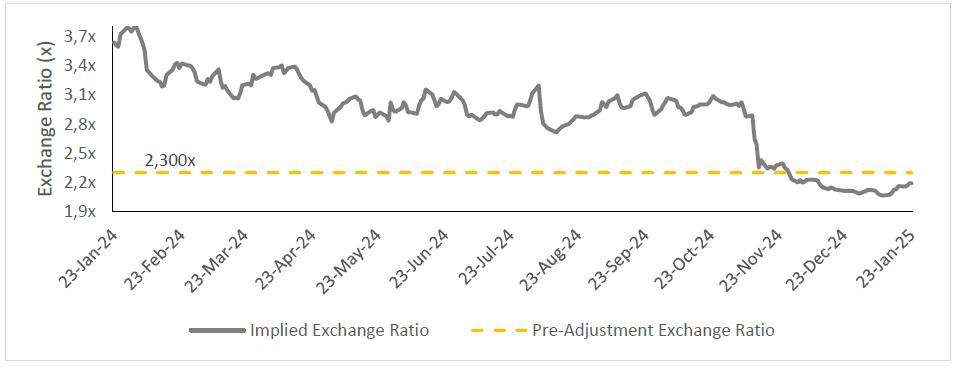

| Consideration | The unit consideration that will be paid by the Offeror to the Tendering Shareholders for each Mediobanca Share (or Additional Share) tendered in acceptance of the Offer, equal to, based on the Exchange Ratio, if there are no further adjustments, No. 2.533 MPS Shares for each Share Subject to the Offer tendered in acceptance of the Offer. | |

| Pre-Adjustment Consideration | The unit consideration as determined by the Offeror and indicated in the Offeror’s Communication, prior to adjustment, equal to 2.300 MPS Shares for each Share Subject to the Offer tendered in acceptance of the Offer. | |

| Full Cash Consideration | The cash consideration referred to in Article 50-ter of the Issuers’ Regulation, which will be offered by the Offeror, as an alternative to the Consideration, in the event that, within the procedure for complying with the Sell-Out pursuant to Article 108, paragraph 2, of the TUF and/or the Joint Procedure, one or more shareholders of Mediobanca request, pursuant to Article 108, paragraph 5, of the TUF, the payment of a full cash consideration, which will be determined: (i) by valuing the MPS Shares based on the weighted average of the official prices recorded in the five Open Market Days preceding the Consideration Payment Date, in the event that, within the Sell-Out pursuant to Article 108, paragraph 1, of the TUF or the Sell-Out pursuant to Article 108, paragraph 2, of the TUF, the purchase price of the Shares Subject to the Offer is equal to the Consideration pursuant to Article 108, paragraph 3, of |

13

| the TUF and Article 50-ter of the Issuers’ Regulation; or (ii) in an amount equal to the monetary valuation made by Consob, in the event that, within the Sell-Out pursuant to Article 108, paragraph 1, of the TUF or the Sell-Out pursuant to Article 108, paragraph 2, of the TUF, the purchase price of the Shares Subject to the Offer is determined by Consob pursuant to Article 108, paragraph 4, of the TUF and Articles 50 and 50-bis of the Issuers’ Regulation. | ||

| Offer Document Date | 3 July 2025, i.e., the date of publication of the Offer Document. | |

| Communication Date | 24 January 2025, the date on which the Offeror’s Communication was disseminated. | |

| Payment Date | The date on which the Consideration will be paid to the Tendering Shareholders for each Share Subject to the Offer tendered in acceptance of the Offer and on which the transfer of the Shares Subject to the Offer to the Offeror will take place, corresponding to the fifth Trading Day following the last day of the Acceptance Period, and, therefore, 15 September 2025 (subject to any extension of the Acceptance Period, in accordance with applicable law), without prejudice to the provisions relating to any Fractional Shares and the related payment of the Fractional Cash Amount (as defined in Section F, Paragraph F.6, of the Offer Document). | |

| Payment Date of the Reopening of the Acceptance Period | The date on which the Consideration will be paid to the Tendering Shareholders who have accepted the Offer during the possible Reopening of the Acceptance Period, corresponding to the fifth Trading Day following the end of the Reopening of the Acceptance Period, and, therefore, 29 September 2025 (unless the Acceptance Period is extended, in accordance with applicable law), without prejudice to the provisions regarding any Fractional Shares and the related payment of the Fractional Cash Amount. | |

| Delegation | The delegation granted, pursuant to Article 2443 of the Italian Civil Code, to the Board of Directors of MPS by the Offeror’s Shareholders’ Meeting for the purpose of executing the Capital Increase Reserved to the Offer. | |

| Delisting | The delisting of the Shares Subject to the Offer from Euronext Milan. | |

| Squeeze-Out | The right of the Offeror to purchase the remaining Shares Subject to the Offer, pursuant to Article 111, |

14

| paragraph 1, of the TUF, in the event that the Offeror were to hold – as a result of the acceptances of the Offer and/or purchases potentially made outside the Offer itself in accordance with applicable regulations, during the Acceptance Period, as possibly extended, and/or during the possible Reopening of the Acceptance Period, as well as during, and/or in accordance with, the procedure for complying with the Sell-Out pursuant to Article 108, paragraph 2, of the TUF – a total shareholding of at least 95% of the Issuer’s share capital. | ||

| MPS Dividend | The dividend approved by the ordinary shareholders’ meeting of MPS on 17 April 2025, equal to Euro 0.86 per MPS share outstanding and entitled to the dividend payment, with ex-dividend date on 19 May 2025, record date on 20 May 2025 and payment date on 21 May 2025. | |

| Exemption Document | The exemption document pursuant to Article 34-ter, paragraph 02, letter a), of the Issuers’ Regulation, prepared by the Offeror for the purposes of the exemption from the obligation to publish the prospectus referred to in Article 1, paragraph 4, letter f) and paragraph 6-bis, letter a) of Regulation (EU) 2017/1129 of the European Parliament and of the Council of 14 June 2017, and published on 3 July 2025. | |

| Offer Document | This offer document, prepared by the Offeror pursuant to Articles 102 et seq. of the TUF, and the applicable provisions of the Issuers’ Regulation. | |

| Issuer or Mediobanca | MEDIOBANCA – Banca di Credito Finanziario Società per Azioni, an Italian joint stock company, with registered office in Milan, Piazzetta Enrico Cuccia, 1, Registration number at the Companies’ Register of Milan and Tax Code No. 00714490158, listed in the Register of Banks held by the Bank of Italy under number 4753, data processing code 10631 and, as the parent company of the Mediobanca Banking Group, in the Register of Banking Groups under number 10631, and a member of the Interbank Deposit Protection Fund (Fondo Interbancario di Tutela dei Depositi) and the National Guarantee Fund (Fondo Nazionale di Garanzia). | |

| Euronext Milan | The Italian regulated market Euronext Milan, organized and managed by Borsa Italiana S.p.A. |

15

| Trading Day | Each day on which the Italian regulated markets are open according to the trading calendar established by Borsa Italiana S.p.A. on an annual basis. |

| Global Information Agent | Georgeson S.r.l., with registered office in Rome, Via Emilia 88, in its capacity as the entity responsible for providing the information relating to the Offer to all Mediobanca shareholders. |

| Mediobanca Group | The “Mediobanca Banking Group” registered with the Register of Banking Groups with the number 10631, headed by the Issuer. |

| MPS Group | The “Monte dei Paschi di Siena Banking Group” registered with the Register of Banking Groups with the number 1030, headed by the Offeror. |

| Depositary Intermediaries | The authorized depositary intermediaries participating in the centralized management system at Monte Titoli (as banks, securities brokerage firms, investment companies, stockbrokers) with which the Shares Subject to the Offer are deposited from time to time. |

| Appointed Intermediaries | The intermediaries in charge of collecting the acceptances of the Offer, as indicated in Section B, Paragraph B.3, of the Offer Document. |

| Intermediaries Appointed to Coordinate the Collection of Acceptances | Banca Monte dei Paschi di Siena S.p.A., together with Banca Akros S.p.A. |

| Stock Exchange Instructions | The instructions to the Stock Exchange Regulations, in force as of the Offer Document Date. |

| MAR | The Regulation (EU) No. 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse, as subsequently amended, in force as of the Offer Document Date. |

| Monte Titoli | Monte Titoli S.p.A., with registered office in Piazza degli Affari No. 6, Milan (Italy). |

| Sell-Out pursuant to Article 108, paragraph 1, of the TUF | The obligation of the Offeror to purchase the remaining Shares Subject to the Offer from those who request it, pursuant to Article 108, paragraph 1, of the TUF, in the event that the Offeror were to hold – as a result of the acceptances of the Offer, and/or purchases potentially made outside the Offer itself in accordance with applicable regulations during the Acceptance Period, as possibly extended, and/or the possible Reopening of the Acceptance Period, as well as during, and/or in accordance with, the procedure for complying with the |

16

| Sell-Out pursuant to Article 108, paragraph 2, of the TUF – a total shareholding equal to at least 95% of the Issuer’s share capital. |

| Sell-Out pursuant to Article 108, paragraph 2, of the TUF | The obligation of the Offeror to purchase the remaining Shares Subject to the Offer from those who request it, pursuant to Article 108, paragraph 2, of the TUF, in the event that the Offeror were to hold – as a result of the acceptances of the Offer and/or purchases potentially made outside the Offer itself in accordance with applicable regulations during the Acceptance Period, as possibly extended, and/or during the possible Reopening of the Acceptance Period – a total shareholding exceeding 90%, but less than 95% of the Issuer’s share capital. |

| Offeror or MPS or BMPS | Banca Monte dei Paschi di Siena S.p.A., an Italian joint stock company, with registered office in Piazza Salimbeni, 3, Siena, registration number at the Companies’ Register of Arezzo – Siena and Tax Code No. 00884060526, listed in the Register of Banks held by the Bank of Italy under number 5274, data processing code 1030 and, as the parent company of the Monte dei Paschi di Siena Banking Group, in the Register of Banking Groups under number 1030, and a member of the Interbank Deposit Protection Fund (Fondo Interbancario di Tutela dei Depositi) and the National Guarantee Fund (Fondo Nazionale di Garanzia). |

| Offer | The voluntary public exchange offer concerning all the Mediobanca Shares and any Additional Shares, promoted by the Offeror, pursuant to Articles 102 and 106, paragraph 4, of the TUF, as well as the applicable implementing provisions contained in the Issuers’ Regulation, as described in this Offer Document. |

| Excluded Countries | Japan, Canada, Australia and any other country where the promotion of the Offer or the participation therein would not comply with financial markets laws and regulations or other local laws and regulations or would not be permitted without prior registration, approval or filing with the relevant supervisory authorities. |

| Fractional Share | The fractional share of decimal numbers resulting from the application of the Exchange Ratio to the Shares Subject to the Offer tendered in acceptance of the Offer by individual Tendering Shareholders. |

| Acceptance Period | The period for the acceptance of the Offer, which will be agreed upon with Borsa Italiana, corresponding to |

17

| No. 40 (forty) Trading Days, which shall commence at 8:30 a.m. (Italian time) on 14 July 2025 and shall end at 5:30 p.m. (Italian time) on 8 September 2025, both dates inclusive, unless extended in accordance with applicable law. |

| Incentive Plans | The following incentive plans approved by Mediobanca: |

| - | 2015 Performance Shares Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2015 (and updated by the ordinary shareholders’ meeting on 28 October 2019); |

| - | 2019-2023 Long Term Incentive Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2019; |

| - | 2021-2025 Performance Shares Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2020 (and partially revoked by the ordinary shareholders’ meeting on 28 October 2021); |

| - | 2022 Performance Shares Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2021; |

| - | 2023 Performance Shares Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2022; |

| - | 2023-2024 Performance Shares Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2023; |

| - | 2024-2025 Performance Shares Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2024; |

| - | 2023-2026 Long Term Incentive Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2023; and |

| - | 2023-2026 Broad-based Share Ownership and Co-investment Plan, approved by the ordinary shareholders’ meeting of Mediobanca on 28 October 2023. |

| Joint Procedure | The joint procedure for (i) complying with the Sell-Out pursuant to Article 108, paragraph 1, of the TUF, and (ii) exercising the Squeeze-Out, agreed upon with Consob and Borsa Italiana pursuant to Article 50-quinquies, paragraph 1, of the Issuers’ Regulation. |

| Exchange Ratio | Means the ratio of No. 2.533 MPS Shares for each Share Subject to the Offer, following the adjustment of the Pre-Adjustment Exchange Ratio due to the detachment |

18

| of the MPS Dividend coupon and the detachment of the Mediobanca Interim Dividend coupon, as better described in Section E, Paragraph E.1, of the Offer Document. |

| Pre-Adjustment Exchange Ratio | Means the ratio of No. 2.300 MPS Shares for each Share Subject to the Offer tendered in acceptance of the Offer, set forth in the Offeror’s Communication, before the adjustment, as better described in Section E, Paragraph E.1, of the Offer Document. |

| Stock Exchange Regulations | The Regulations of the Markets Organized and Managed by Borsa Italiana and in force as of the Offer Document Date. |

| Issuers’ Regulation | The Regulation adopted by Consob by resolution No. 11971 of 14 May 1999, as subsequently amended and integrated, in force as of the Offer Document Date. |

| MPS Regulation | The “Group Regulation on the management of prescriptive requirements relating to related parties, related subjects and Bank officers’ obligations” adopted by the Board of Directors of BMPS and in force as of the Offer Document Date. |

| Related Parties Regulation | Consob Regulation No. 17221 of 12 March 2010, as amended and supplemented, in force as of the Offer Document Date. |

| Regulation (EU) 575/2013 | The Regulation (EU) No. 575/2013 of the European Parliament and the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms, as subsequently amended and supplemented, in force as of the Offer Document Date. |

|

Reopening of the Acceptance Period |

The possible reopening of the Acceptance Period for 5 Trading Days (specifically, unless the Acceptance Period is extended, for the trading sessions of 16, 17, 18, 19 and 22 September 2025) pursuant to Article 40-bis, paragraph 1, letter a), of the Issuers’ Regulation, as voluntarily applied by the Offeror and described more in detail in Section F, Paragraph F.1.1, of the Offer Document. |

| RWA | Risk-weighted assets (including credit risks, operational risks and other risks), in accordance with banking regulations issued by supervisory authorities for the calculation of solvency coefficients. |

| Acceptance Form | The acceptance form for the Offer, which the Tendering Shareholders must sign and deliver to an Appointed Intermediary, duly completed in all its parts, while |

19

| simultaneously depositing the Mediobanca Shares (and any Additional Shares) with the said Appointed Intermediary. |

| TUB or Consolidated Law on Banking | Legislative Decree No. 385 of 1 September 1993 – Consolidated Law on Banking and Credit, as subsequently amended and supplemented, in force as of the Offer Document Date. |

| TUF or Consolidated Law on Finance | Legislative Decree No. 58 of 24 February 1998, as subsequently amended and supplemented, in force as of the Offer Document Date. |

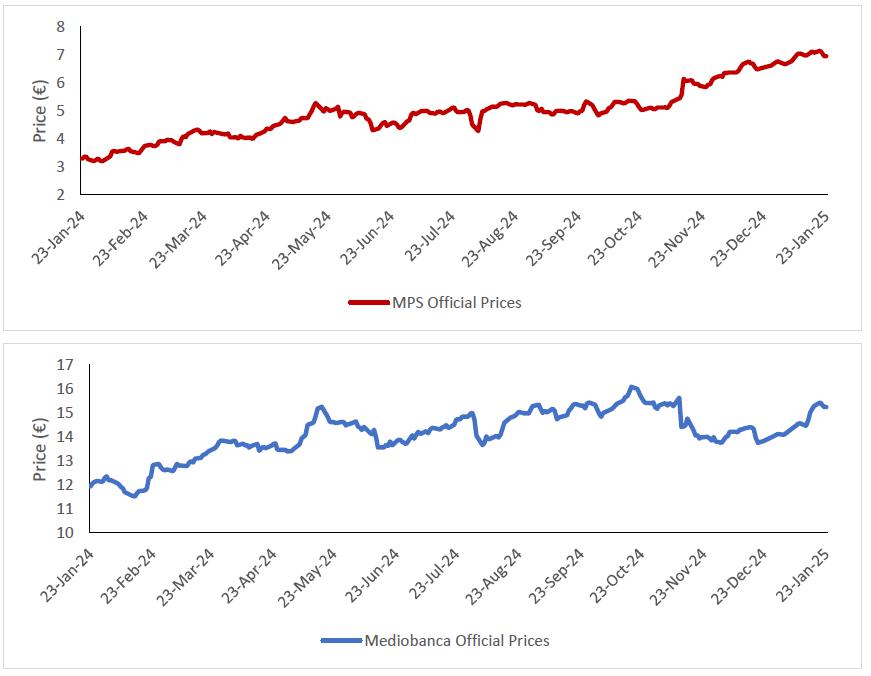

| Unit Market Value of the MPS Share Prior to the Offer Document Date | Euro 7.036 attributed (for illustrative purposes only in the Offer Document) to each MPS Share and corresponding to the official price of MPS ordinary shares on the last Trading Day prior to the Offer Document Date. |

| Unit Market Value of the Pre-Adjustment Consideration Prior to the Communication Date | Euro 15.992 attributed (for illustrative purposes only in the Offer Document) to each Mediobanca Share and corresponding to the official price of MPS ordinary shares on the last Trading Day prior to the Communication Date (i.e., 23 January 2025), namely Euro 6.953 multiplied by 2.300 (corresponding to the Pre-Adjustment Exchange Ratio). |

| Unit Market Value of the Pre-Adjustment Consideration Prior to the Offer Document Date | Euro 16.184 attributed (for illustrative purposes only in the Offer Document) to the Consideration payable for each Share Subject to the Offer tendered in acceptance of the Offer, equal to the Unit Market Value of the MPS Share Prior to the Offer Document Date multiplied by 2.300 (corresponding to the Pre-Adjustment Exchange Ratio). |

20

RECITALS

The following Recitals briefly describe the transaction which is the subject matter of this offer document (the “Offer Document”).

For a complete assessment of the terms and conditions of the transaction, please read Section A “Warnings” carefully and, in any case, the entire Offer Document.

The Offer Document must be read in conjunction with (ad as a mutual integration of) the Exemption Document available, inter alia, on the Offeror’s website.

The data and information relating to the Issuer (and the Mediobanca Group) contained in this Offer Document are exclusively based on data and information available to the public on the Offer Document Date (including those available on Mediobanca’s website, www.mediobanca.com/en).

1. Subject of the Offer

The transaction described in the Offer Document consists of a voluntary public exchange offer (the “Offer” or the “Transaction”), promoted by Banca Monte dei Paschi di Siena S.p.A. (the “Offeror” or “MPS” or “BMPS”) – pursuant to and for the purposes of Articles 102 and 106, paragraph 4, of Legislative Decree No. 58 of 24 February 1998, as subsequently amended and supplemented (the “TUF”), as well as the applicable implementing provisions contained in the regulation on issuers, adopted by Consob with Resolution No. 11971 of 14 May 1999, as subsequently amended and supplemented (the “Issuers’ Regulation”) – on all the ordinary shares of MEDIOBANCA – Banca di Credito Finanziario Società per Azioni (“Mediobanca” or the “Issuer”), a joint stock company with shares listed on Euronext Milan (“Euronext Milan”), a regulated market organized and managed by Borsa Italiana S.p.A. (“Borsa Italiana”), and namely a total maximum of:

| (i) | No. 833,279,689 ordinary shares of Mediobanca (the “Mediobanca Shares” or the “Issuer’s Shares”), i.e., all of the ordinary shares issued by Mediobanca as of the Offer Document Date, including the No. 26,914,597 treasury shares held by the Issuer on the Offer Document Date, corresponding to approximately 3.2% of the Issuer’s share capital as of the Offer Document Date (the “Treasury Shares”), as well as |

| (ii) | No. 16,178,862 ordinary shares of Mediobanca (the “Additional Shares”) that the Issuer may issue prior to the completion of the Offer in favour of the beneficiaries of certain Incentive Plans, as a result of the review by the competent bodies of Mediobanca to provide for their acceleration, where envisaged by the individual Incentive Plans, even though some of them envisage the possibility of using – instead of the Additional Shares – Mediobanca’s Treasury Shares held in portfolio, (collectively, the “Shares Subject to the Offer”). |

Therefore, as of the Offer Document Date, the Offer – assuming the issuance of all Additional Shares – covers a maximum of No. 849,458,551 shares of the Issuer.

As of the Offer Document Date, the Offeror directly holds No. 31,996 Issuer’s shares, representing 0.004% of the Issuer’s share capital as of the Offer Document Date. It should be noted that, this calculation does not include Mediobanca Shares held by investment funds and/or other collective investment undertakings managed by companies of the MPS Group

21

in full autonomy from the latter and in the interests of their clients. For further details on the Shares Subject to the Offer, see Section C, Paragraph C.1, of the Offer Document.

Without prejudice to the Offeror’s decisions regarding the fulfilment (or non-fulfilment) of the Threshold Condition within the terms set out in Section A, Paragraph A.1.4 below, the objective of the Offer, in light of the reasons and future plans relating to the Issuer, as further specified in Section G, Paragraph G.2.1, of the Offer Document, is to acquire the entire share capital of the Issuer and to delist the Shares Subject to the Offer from Euronext Milan. The Offeror believes that Delisting will help MPS and Mediobanca to achieve their goals of integration, creation of synergies, and growth.

The Offer was announced by means of a communication issued by the Offeror on 24 January 2025 (the “Communication Date”), pursuant to Articles 102, paragraph 1, of the TUF and 37, paragraph 1, of the Issuers’ Regulation and Article 17 of the MAR (the “Communication 102” or the “Offeror’s Communication”).

In particular, the Communication 102 announced, among other things, the Offeror’s decision to proceed with the Offer, pursuant to the resolution passed by the Offeror’s Board of Directors on 23 January 2025 (subject to the issuance, on the same date, of a favourable, reasoned and binding opinion by the Committee for Related Parties Transactions), which simultaneously approved, inter alia, to convene the extraordinary shareholders’ meeting of MPS on 17 April 2025 to resolve on the proposal to delegate to the administrative body of MPS, pursuant to Article 2443 of the Italian Civil Code, the execution of the Capital Increase Reserved to the Offer.

Furthermore, on 24 January 2025, MPS published a presentation to the market regarding the Offer, available on the Offeror’s website (www.gruppomps.it/en, Investor Relations section).

2. Legal assumptions and characteristics of the Offer

The Offer is being promoted in Italy pursuant to Articles 102 and 106, paragraph 4, of the TUF.

On 23 January 2025, the Board of Directors of the Offeror (subject to the issue on the same date of a favourable, reasoned and binding opinion by the Committee for Related Parties Transactions) decided to promote the Offer. This decision was therefore communicated to Consob and to the market on 24 January 2025, before the opening of the markets, through the Offeror’s Communication.

Furthermore, on 24 January 2025, pursuant to and for the purposes of Article 102, paragraph 2, of the TUF, the Offeror informed the workers’ representatives of the publication of the Offeror’s Communication.

On 13 February 2025, pursuant to and for the purposes of Article 16 of Law No. 287 of 10 October 1990, the Offeror filed an application for antitrust authorization with the Italian Competition and Market Authority (“AGCM”), as it could potentially give rise to a concentration transaction subject to notification. On the same date, the Offeror also submitted the notification to the European Commission pursuant to and for the purposes of Regulation (EU) 2022/2560 on foreign subsidies distorting the internal market.

Also on 13 February 2025, the Offeror filed with the Presidency of the Council of Ministers the notification required by Article 2 of Decree Law No. 21 of 15 March 2012, on the exercise of special powers in relation to investments in strategic sectors, converted with amendments

22

by Law No. 56 of 11 May 2012, as amended, supplemented and/or modified from time to time (the “Golden Power Decree”), concerning the Offer and the acquisition of exclusive control of the Issuer following completion of the Offer. On the same date, the Offeror filed a request for authorization with the Directorate General for International Trade and Investments – Ministry of Economy, Trade and Enterprise (Direccion General de Comercio Internacional e Inversiones – Ministerio de Economía, Comercio y Empresa) in accordance with Spanish legislation on foreign investments, pursuant to Article 7-bis of Law 19/2003 on the legal regime governing capital movements (Ley 19/2003 sobre régimen jurídico de los movimientos de capitales).

On 12 and 13 February 2025, the Offeror also filed applications with the competent authorities to obtain the Preliminary Authorizations. For further details, please refer to Section A.1.2 of the Offer Document.

On 13 February 2025, the Offeror filed the Offer Document with Consob pursuant to Article 102, paragraph 3, of the TUF and notified the market by means of a press release pursuant to Article 37-ter, paragraph 3, of the Issuers’ Regulation.

The Offer is subject to the Condition of Effectiveness as described in Section A, Paragraph A.1, of the Offer Document and is addressed to all shareholders of the Issuer, without distinction and on equal terms, without prejudice to the provisions of Section F, Paragraph F.4, of the Offer Document.

The Offeror will pay each Tendering Shareholder a unit consideration consisting of No. 2.533 newly issued ordinary shares of MPS resulting from the Capital Increase Reserved to the Offer, with no nominal value, with regular dividend rights and the same characteristics as the ordinary shares of MPS already outstanding as of the issue date, which will be listed on Euronext Milan, a regulated market organized and managed by Borsa Italiana (the “MPS Shares”), for each Share Subject to the Offer tendered in acceptance of the Offer (the “Consideration”). In this regard, it should be noted that (as better explained below), the Pre-Adjustment Exchange Ratio, originally provided for in the Offeror’s Communication, was equal to 2.300 MPS Shares for each Share Subject to the Offer. The Offeror’s Communication indeed provided as follows “If, prior to the Payment Date (as defined below), the Issuer and/or the Offeror should pay(s) a dividend (including an interim dividend) and/or make a distribution of reserves to its shareholders, or in any event the ex coupon (cedola) relating to dividends resolved upon but not yet paid by the Issuer and/or MPS, as the case may be, is detached from the Mediobanca Shares and/or the MPS shares, the Consideration shall be adjusted to take into account the dividend distributed (or the interim dividend) or the reserve distributed”.

Therefore, on 20 May 2025, MPS announced to the market that, following the detachment of the coupons and the subsequent payments of the MPS Dividend and the Mediobanca Interim Dividend, it had made the resulting technical adjustment to the Pre-Adjustment Exchange Ratio, equal to 0.233 MPS Shares. As of the Offer Document Date, the Consideration (following the mentioned technical adjustment) - without prejudice to any further adjustments based on the provisions of the Communication 102 and/or any restructuring and/or changes to the content and/or structure of the Offer - is therefore equal to 2.533 MPS Shares for each Share Subject to the Offer tendered in acceptance of the Offer.

As a result, by way of example, for every No. 1,000 (one thousand) Shares Subject to the Offer tendered in acceptance of the Offer, No. 2,533 (two thousand five hundred and thirty-three)

23

MPS Shares will be exchanged. Acceptance of the Offer may take place, as further specified in Section F of the Offer Document, even if the number of Shares Subject to the Offer tendered in acceptance of the Offer is less than 1,000 (one thousand) or the number of Shares Subject to the Offer is not a whole multiple of 1,000 (one thousand).

Any further adjustments to the Consideration as a result of the provisions of the Communication 102 will be disclosed in the manner and within the time frames required by applicable law. For further details on the additional circumstances that would trigger a further adjustment to the Consideration, please refer to the Offeror’s Communication.

The MPS Shares issued in connection with the Offer derive from the Capital Increase Reserved to the Offer approved by the Board of Directors of the Offeror on 26 June 2025, in exercise of the Delegation granted by the Extraordinary Shareholders’ Meeting of the Offeror held on 17 April 2025. For further details on the resolutions passed by the Shareholders’ Meeting of the Offeror and by the Board of Directors, please refer to the press releases issued by the Offeror to the market on 17 April 2025 and on 26 June 2025, respectively, available on the MPS website, as well as the shareholders’ meeting and board of directors’ meeting documentation made available to the public on the MPS website at www.gruppomps.it/en, Investor Relations section.

In the event of full acceptance of the Offer, i.e., if all Mediobanca Shares and any Additional Shares are tendered in acceptance of the Offer, even during the Reopening of the Acceptance Period (or in any case transferred to MPS in execution of the procedure for the fulfilment of the Sell-Out pursuant to Article 108, paragraph 2, of the TUF and/or the Joint Procedure, where applicable) and without prejudice to any further adjustments based on the provisions of the Communication 102 and/or any restructuring and/or changes to the content and/or structure of the Offer, a total of No. 2,151,678,510 MPS Shares resulting from the Capital Increase Reserved to the Offer will be allocated to the Tendering Shareholders, based on the Consideration, corresponding to – as of the Offer Document Date – approximately 63% of the shares of the Offeror on the basis of the shares of MPS issued as of the Offer Document Date. Alternatively, in the event that the percentage of acceptances of the Offer would be equal to the Threshold Condition (i.e., 66.67% of Mediobanca’s share capital), the dilution for MPS’ shareholders would be equal to 53%.

It should be noted that the Capital Increase Reserved to the Offer is subject to the provisions of Articles 2440 and 2343-ter, et seq., of the Italian Civil Code, concerning capital increases to be paid by contributions in kind.

The Offeror has therefore appointed KPMG Corporate Finance, a division of KPMG Advisory S.p.A., as an independent expert pursuant to Article 2343-ter, paragraph 2, letter b) of the Italian Civil Code (the “Independent Expert”) to prepare the valuation of the Shares Subject to the Offer.

On 14 March 2025, the Independent Expert issued its appraisal on the valuation of the Shares Subject to the Offer (the “Appraisal”). In the Appraisal, the Independent Expert concluded that, as of 14 March 2025, based on the financial and equity position as of 31 December 2024 and the elements and methods described in its appraisal, the fair value of the shares of Mediobanca is not less than Euro 16.406 per Mediobanca share, cum dividend, or Euro 15.852 per Mediobanca share, ex dividend.

24

Subsequently, on 26 June 2025, the Independent Expert, upon request of the Offeror, issued the Appraisal updated taking into account the data and information available as of 31 March 2025, which therefore constitutes the new reference date. Specifically, in the updated Appraisal, the Independent Expert concluded that, as of 26 June 2025, based on the economic and financial position as of 31 March 2025, and the elements and methods described in the update Appraisal, the fair value of the shares of Mediobanca is not less than Euro 17.395 per each share of Mediobanca, ex dividend, i.e., net of Mediobanca’s Interim Dividend.

In accordance with the law, the value attributed, for the purpose of determining the share capital and the share premium, to the Shares Subject to the Offer tendered in acceptance of the Offer must be equal to or less than the value indicated in the aforementioned updated Appraisal of the Independent Expert.

For further information on the Capital Increase Reserved to the Offer, please refer to Section A, Paragraph A.5, of the Offer Document.

For the sake of completeness, it should be noted that the above will apply, mutatis mutandis, if the conditions for the Reopening of the Acceptance Period and/or for the fulfilment of the Sell-Out pursuant to Article 108, paragraph 2, of the TUF and/or for the fulfilment of the Joint Procedure are met.

3. The voluntary public exchange offer promoted by Mediobanca on Banca Generali S.p.A.

On 28 April 2025, pursuant to and for the purposes of Article 102, paragraph 1, of the TUF, as well as Article 37 of the Issuers’ Regulation, Mediobanca notified the market that, on 27 April 2025 it had decided to promote a voluntary public exchange offer pursuant to and for the purposes of Articles 102 and 106, paragraph 4, of the TUF for all the ordinary shares of Banca Generali S.p.A. (“Banca Generali”) admitted to trading on Euronext Milan, organised and managed by Borsa Italiana (the “Mediobanca-Banca Generali Offer”).

The Mediobanca-Banca Generali Offer therefore concerns the maximum No. 116,851,637 ordinary shares of Banca Generali (i.e., all the shares issued by Banca Generali as of that date), including treasury shares held by Banca Generali itself (equal to No. 2,907,907 as reported in Banca Generali’s financial statements as of 31 December 2024).

Mediobanca will pay – for each share of Banca Generali tendered in acceptance of the Mediobanca-Banca Generali Offer – a unit consideration equal to No. 1.70 ordinary shares of Assicurazioni Generali S.p.A. (“Assicurazioni Generali”) held by Mediobanca (the “Mediobanca-Banca Generali Offer Consideration”).

Considering the pending Offer, on 27 April 2025, Mediobanca’s Board of Directors resolved, inter alia, to submit to the ordinary shareholders’ meeting of Mediobanca – convened for 16 June 2025 – a proposal to approve the Mediobanca-Banca Generali Offer pursuant to and for the purposes of Article 104 of the TUF, which allows the shareholders’ meeting to grant power to the Board of Directors in derogation from the provisions of that Article.

On 15 June 2025, Mediobanca’s Board of Directors resolved to postpone the date of the ordinary shareholders’ meeting for the approval of the Mediobanca-Banca Generali Offer, originally convened for 16 June 2025, in accordance with Article 104 of the TUF, to 25

25

September 2025. For further details, please refer to the press release made available to the market by Mediobanca on 15 June 2025.

It should be noted that – in the event that the Offer and the Mediobanca-Banca Generali Offer are completed – taking into account that the Mediobanca-Banca Generali Offer provides, as the Mediobanca-Banca Generali Offer Consideration, the allocation to the tendering shareholders of ordinary shares of Assicurazioni Generali held by Mediobanca in portfolio, depending on the scenarios of acceptance of the Mediobanca-Banca Generali Offer, Mediobanca could reduce (or even sell completely) its interest in Assicurazioni Generali held as of the Offer Document Date.

In terms of timing, based on the information provided by Mediobanca in the press release issued on the date of announcement of the Mediobanca-Banca Generali Offer (the “Mediobanca Communication 102”) and confirmed in the aforementioned press release published on 15 June 2025, the execution of this offer is expected to be completed by October 2025, therefore after the completion of the Offer, based on the information available as of the Offer Document Date.

As described in this Offer Document, the Offer promoted by MPS on Mediobanca is aimed at creating the third largest national banking operator in terms of total assets, customer loans, direct deposits and financial assets, leveraging Mediobanca’s distinctive expertise in Wealth Management, Corporate & Investment Banking and Consumer Finance, and MPS’ experience in Retail and Commercial Banking, areas characterized by strong complementarities.

Given the above objective, Mediobanca’s interest in Assicurazioni Generali has always been considered a financial investment to be evaluated over time according to a risk/return approach. Following completion of the Transaction, this interest will reduce its weight on the overall profitability of the new group.

Therefore, since not all the terms of the Mediobanca-Banca Generali Offer have been disclosed to the market as of the Offer Document Date, also considering the postponement of Mediobanca’s ordinary shareholders’ meeting pursuant to Article 104 of the TUF, the Offeror reserves the right to fully evaluate the Mediobanca-Banca Generali Offer in light of all relevant information that will made available from time to time. It should also be noted that, while the Mediobanca-Banca Generali Offer would potentially appear to be consistent with the strategic rationale of the Offer, the information currently available to the Offeror is not sufficient to allow for a comprehensive analysis, given that Mediobanca’s shareholders’ meeting has been postponed due to the incomplete nature of the available information.

4. Reasons for the Offer and overview of future plans

Over the last three years, MPS has consistently strengthened its fundamentals, consolidating the sustainability of its business model and improving its risk profile, thereby achieving solid levels of profitability. Furthermore, the MPS Group has managed to exceed most of the targets set out in its 2022-2026 business plan two years ahead of schedule and with one of the strongest balance sheets in Europe, laying solid foundations to play an active role in the broader consolidation of the Italian banking sector.

The aggregation between MPS and Mediobanca, which will be carried out in accordance with the principles of sound and prudent management, business continuity and risk control, aims to create a New National Champion, combining two leading brands in the financial services

26

market, with the objective of strengthening the sustainability of its business model, ensuring solid levels of profitability in the medium/long-term.

MPS believes that the Offer represents an ideal opportunity for further development and growth for both institutions and offers significant value creation for the shareholders of both companies and for all stakeholders.

The combination with Mediobanca, to the extent that it is completed, will create the third largest national banking operator in terms of total assets, loans to customers, direct deposits and total financial assets, and a highly diversified, resilient player with distinctive and complementary capabilities in each business area and a significant degree of innovation and support for growth, with the ability to compete with the main Italian and European banking institutions, through the full optimisation of existing human capital.

In a market undergoing consolidation, MPS intends to play an active role, and this proposed aggregation represents a unique opportunity to strengthen its position in certain key areas and sectors, also to better seize future growth opportunities. This will increase support for households and businesses, strengthening overall support for the former, both in terms of financing needs and the protection and management of savings, and supporting the latter in capturing growth opportunities at domestic and international level. The benefits will also extend to local communities and the Italian economy.

The new group will be able to rely on Mediobanca’s distinctive expertise in Wealth Management, Corporate & Investment Banking and Consumer Finance, and MPS’ expertise in Retail and Commercial Banking. Furthermore, the shareholding held in Assicurazioni Generali will also positively contribute to the diversification of the new MPS Group’s revenues and will be managed in the same way as the other business lines, in accordance with a careful capital optimization policy and a strong risk-adjusted profitability approach. In light of the Mediobanca-Banca Generali Offer recently announced to the market, the Offeror reserves the right to fully evaluate it once any further relevant information becomes available.

The aggregation will also offer employees of each institution the opportunity to develop their careers in a larger organization, enhancing their talent thanks to opportunities for mutual enrichment and integration.

At the same time, it will help attract new high-profile resources, enhancing their skills and professionalism to consolidate a sustainable and competitive growth model.

The combination is fully consistent with MPS’ strategic guidelines set out in its 2024-2028 business plan (the “2024-28 Business Plan”) and will generate significant revenue growth and important cost and funding synergies, with an effective implementation path.

With regard to the revenues, the Transaction will generate synergies of approximately Euro 0.3 billion per year, thanks to the enrichment of the product and service offering for households and businesses, the development of an integrated offering across the respective customer bases and increased penetration and expansion of the reference markets. In particular, through:

| § | Retail Banking – introducing MPS products to the customer base of Compass Banca S.p.A. (“Compass”) and Mediobanca Premier S.p.A. (“Mediobanca Premier”), making the MPS branch network available to facilitate scalable service delivery and deeper market penetration. Examples of growth drivers include: |

27

| o | Accounts and Cards – for the so-called daily banking; |

| o | Mortgages – leveraging the proven commercial capabilities of the MPS network, including in meeting the needs of customers for related insurance products; |

| o | Bancassurance – extension of the insurance offering to Mediobanca Premier customers; |

| o | Consumer Finance – expanding the distribution by making the MPS branch network available, enriching the offering with insurance products and internationalizing the value proposition towards new markets; |

| § | Private Banking – extending Mediobanca’s best practices to MPS customers, including through Mediobanca’s asset management products (e.g., alternative investments); |

| § | Asset Gathering (1) – integration of Mediobanca Premier and Banca Widiba S.p.A. (“Widiba”) to create a network of financial advisors already comprehensively structured to compete with key players, supported by a distinctive digital platform, with the introduction of an integrated offering of asset management products and enhancement of MPS’ capabilities in the insurance sector; |

| § | Corporate & Investment Banking – combining MPS’ balance sheet potential with Mediobanca’s Investment Banking business and launching an intensive development programme to support the growth of companies throughout the country. Similarly, leveraging Mediobanca’s specialized experience in Advisory and Markets to extend its reach to MPS’ corporate customers. |

The Transaction will also generate significant cost synergies in terms of administrative expenses and enable targeted optimization of overlapping functions. This will be complemented by savings from the rationalization of the combined investment plans of the two banks, thereby avoiding duplication of investments in areas affected by the combination.

The expected savings amount to approximately Euro 0.3 billion per year. By way of example, the levers include:

| · | centralization of procurement from large suppliers and extension of best practices in terms of cost governance; |

| · | optimization of IT investments and digital transformation for common areas, such as the MPS consumer finance platform; |

| · | optimization of wealth management support activities for both Private Banking and Asset Gathering; |

| · | combined development of the platform for corporate customers and optimization of product factories (e.g., MBFACTA and MPS Factoring); |

| · | optimization of duplication of central functions, both in operational and resource terms. |

Furthermore, the aggregation will enable funding synergies of approximately Euro 0.1 billion per year to be achieved thanks to a more balanced funding mix, leveraging MPS’ commercial funding capacity and optimizing the combined entity’s wholesale funding position.

1 i.e., the activity carried out by a financial institution with the aim of providing advice, collection, administration, and management services in respect of client assets through specific networks of financial advisors.

28

It should also be noted that if, upon completion of the Offer, the Offeror comes to hold a shareholding in Mediobanca’s share capital equal to or greater than the Threshold Condition (i.e., 66.67% of the Issuer’s share capital), it is expected that approximately 50% of the total synergies will be achieved in 2026, increasing to approximately 85% in 2027 and fully implemented in 2028.

The business project, which stands out for the significant complementarity of the two business models (which significantly reduces the execution risk), will be implemented through a simple integration, with one-off integration costs estimated at approximately Euro 0.6 billion before tax, which can be expensed in the first year.

It should be noted that, the cost and funding synergies, the expansion of revenue sources and related synergies, and the advantages deriving from the complementary nature of the business models of MPS and Mediobanca, as well as the strategic objectives of the Offer, will be achievable not only through the acquisition of legal control, but also in scenarios other than the acquisition of legal control (de facto control), albeit with possible variations and delays in their implementation, all as further specified in Section A, Paragraph A.1.4.

The Transaction also aims to accelerate the utilization of Deferred Tax Assets (“DTAs”) held by MPS, by leveraging a higher consolidated tax base and recording Euro 1.3 billion of DTAs (currently off-balance sheet) on the balance sheet, bringing the total to Euro 2.9 billion. Over the next six years, the utilization of these DTAs will generate a significant capital benefit (Euro 0.5 billion per year), in addition to the net result.

For the sake of completeness, it should be noted that, the aforementioned acceleration in the use of DTAs is subject to the Offeror acquiring a shareholding of more than 50% in the share capital of Mediobanca. By relying on the provisions of Articles 117 et seq. of the Consolidated Law on Income Tax (Presidential Decree No. 917 of 22 December 1986), Mediobanca may join the national tax consolidation scheme of Banca Monte dei Paschi di Siena S.p.A., starting from the tax period following that in which such shareholding was acquired (2). As a result, the consequent increase in the MPS Group’s future consolidated tax base will allow for the immediate recording in the financial statements of almost all DTAs from past consolidated tax losses, up to Euro 2.9 billion, and, compared to the current situation, will accelerate the utilization process of these DTAs with the related benefit in capital terms.

Otherwise, in the event that, upon completion of the Offer and following the potential waiver of the Threshold Condition, the Offeror comes to hold a shareholding equal to or less than 50% of the share capital of Mediobanca, the latter, even in a de facto control scenario, may not be included in the national tax consolidation scheme of Banca Monte dei Paschi di Siena S.p.A.; in such a case, MPS may continue to use the past consolidated tax losses to compensate the taxable income generated by the companies currently participating in the national tax consolidation scheme and, both the recording of Euro 1.3 billion of DTAs (currently off-balance sheet) as assets and the benefits deriving from the use of the DTAs will still be achieved, even if over a longer period of time. Specifically, the expected benefits would be achieved in 2036 with an average annual use of DTAs equal to approximately Euro 0.3

2 In accordance with the requirement set forth in Article 119, paragraph 1, letter “a” of the Consolidated Law on Income Tax (“alignment of the financial year of each subsidiary with that of the parent company or controlling entity”), Mediobanca’s financial year (which, on the Offer Document Date, ends on 30 June) shall be aligned with that of the Offeror.

29

billion, also due to the projected increase in the tax base resulting from the synergies generated by the Transaction.

The combined group will be strengthened, with a diversified revenue stream and strong resilience to successfully compete in different scenarios, also enabling significant value creation for all shareholders, supported by higher profitability than the standalone businesses and capable of generating double-digit growth in earnings per share.

Shareholders will benefit from a sustainable dividend policy over time, with a payout ratio of up to 100% of the net profit, with growth in dividends per share, while confirming MPS’ solid capital position (projected consolidated fully loaded Common Equity Tier 1 ratio as of 31 March 2025 for the resulting Group following completion of the Offer equal to 17.8% (3) upon completion of the transaction in the event of 100% acceptance of the Offer).

Finally, the two banks’ sustainability strategies will be consolidated, leveraging their respective ESG capabilities to strengthen the combined entity’s positioning and promote its commitment to the communities and territories where they are based.

MPS’ high governance standards will be maintained throughout the integration and post-integration process, ensuring transparency, accountability and a balanced approach towards all stakeholders, thus contributing to the creation of a sustainable and competitive long-term model.

Industrial and strategic aspects