Clearing Operations

Mar. 31, 2025

We operate six clearing houses, each of which acts as a central counterparty that becomes the buyer to every seller and the seller to every buyer for its clearing members or participants, or Members. Through this central counterparty function, the clearing houses provide financial security for each transaction for the duration of the position by limiting counterparty credit risk.

Our clearing houses are responsible for providing clearing services to each of our futures exchanges, and in some cases to third-party execution venues, and are as follows, referred to herein collectively as "the ICE Clearing Houses":

| Clearing House | Products Cleared | Exchange where Executed | Location | |||||||||||||||||

| ICE Clear Europe | Energy, agricultural, interest rates and equity index futures and options contracts | ICE Futures Europe, ICE Futures U.S., ICE Endex and ICE Futures Abu Dhabi | U.K. | |||||||||||||||||

| ICE Clear U.S. | Agricultural, metals, foreign exchange, or FX, interest rate and equity index futures and/or options contracts | ICE Futures U.S. | U.S. | |||||||||||||||||

| ICE Clear Credit | OTC North American, European, Asian-Pacific and Emerging Market CDS instruments | Creditex and third-party venues | U.S. | |||||||||||||||||

| ICE Clear Netherlands | Derivatives on equities and equity indices traded on regulated markets | ICE Endex | The Netherlands | |||||||||||||||||

| ICE Clear Singapore | Energy, metals and financial futures products | ICE Futures Singapore | Singapore | |||||||||||||||||

| ICE NGX | Physical North American natural gas, environmental commodities and physical and financial electricity | ICE NGX | Canada | |||||||||||||||||

Original and Variation Margin

Each of the ICE Clearing Houses generally requires all Members to deposit collateral in cash or certain pledged assets. The collateral deposits are known as “original margin.” In addition, the ICE Clearing Houses may make intraday original margin calls in circumstances where market conditions require additional protection. The daily profits and losses to and from the ICE Clearing Houses due to the marking-to-market of open contracts is known as “variation margin.” The ICE Clearing Houses mark all outstanding contracts to market, and, with the exception of ICE NGX’s physical natural gas, physical environmental and physical power products discussed separately below, pay and collect variation margin at least once daily.

The amounts that Members are required to maintain are determined by proprietary risk models established by each ICE Clearing House and reviewed by the relevant regulators, independent model validators, risk committees and the boards of directors of the respective ICE Clearing House. The amounts required may fluctuate over time. Each of the ICE Clearing Houses is a separate legal entity and is not subject to the liabilities of the others, or the obligations of Members of the other ICE Clearing Houses.

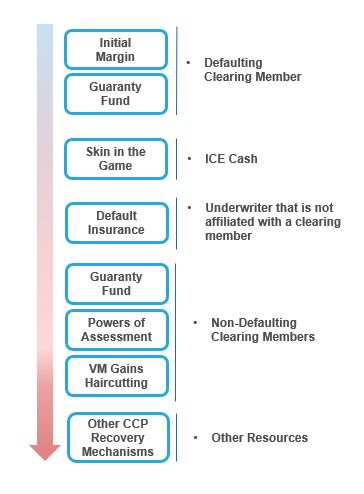

Should a particular Member fail to deposit its original margin or fail to make a variation margin payment, when and as required, the relevant ICE Clearing House may liquidate or hedge the defaulting Member's open positions and use their original margin and guaranty fund deposits to pay any amount owed. In the event that the defaulting Member's deposits are not sufficient to pay the amount owed in full, the ICE Clearing Houses will first use their respective contributions to the guaranty fund, often referred to as Skin In The Game, or SITG, to pay any remaining amount owed. In the event that the SITG is not sufficient, the ICE Clearing Houses may utilize the respective guaranty fund deposits and default insurance or collect limited additional funds from their respective non-defaulting Members on a pro-rata basis, to pay any remaining amount owed.

As of March 31, 2025 and December 31, 2024, the ICE Clearing Houses had received or had been pledged $181.8 billion and $173.1 billion, respectively, in cash and non-cash collateral in original margin and guaranty fund deposits to cover price movements of underlying contracts for both periods.

Guaranty Funds and ICE Contribution

As described above, mechanisms have been created, called guaranty funds, to provide partial protection in the event of a Member default. With the exception of ICE NGX, each of the ICE Clearing Houses requires that each Member make deposits into a guaranty fund.

In addition, we have contributed our own capital that could be used if a defaulting Member’s original margin and guaranty fund deposits are insufficient. Such amounts are recorded as long-term restricted cash and cash equivalents and long-term restricted investments in our balance sheets and are as follows (in millions):

| ICE Portion of Guaranty Fund Contribution | Default insurance | |||||||||||||||||||||||||

| Clearing House | As of March 31, 2025 | As of December 31, 2024 | As of March 31, 2025 | As of December 31, 2024 | ||||||||||||||||||||||

| ICE Clear Europe | $197 | $197 | $100 | $100 | ||||||||||||||||||||||

| ICE Clear U.S. | 75 | 75 | 25 | 25 | ||||||||||||||||||||||

| ICE Clear Credit | 50 | 50 | 75 | 75 | ||||||||||||||||||||||

| ICE Clear Netherlands | 2 | 2 | N/A | N/A | ||||||||||||||||||||||

| ICE Clear Singapore | 1 | 1 | N/A | N/A | ||||||||||||||||||||||

| ICE NGX | 45 | 45 | 200 | 200 | ||||||||||||||||||||||

| Total | $370 | $370 | $400 | $400 | ||||||||||||||||||||||

We also maintain default insurance at ICE Clear Europe, ICE Clear U.S. and ICE Clear Credit as an additional layer of clearing member default protection, which is reflected in the table above. The default insurance was renewed in September 2022 and has a three-year term. The default insurance layer resides after and in addition to the ICE Clear Europe, ICE Clear U.S. and ICE Clear Credit SITG contributions and before the guaranty fund contributions of the non-defaulting Members.

Similar to SITG, the default insurance layer is not intended to replace or reduce the position risk-based amount of the guaranty fund. As a result, the default insurance layer is not a factor that is included in the calculation of the Members' guaranty fund contribution requirement. Instead, it serves as an additional, distinct, and separate default resource that should serve to further protect the non-defaulting Members’ guaranty fund contributions from being mutualized in the event of a default.

As of March 31, 2025, ICE NGX maintained a guaranty fund of $215 million, comprising $15 million in cash and a $200 million letter of credit backed by a default insurance policy of the same amount, discussed below. Separately, ICE NGX has also set aside $30 million of its own capital that could be used for liquidity purposes if a direct participant of the ICE NGX clearing house, or Contracting Party, defaulted.

Below is a depiction of our Default Waterfall which summarizes the lines of defense and layers of protection we maintain for our mutualized clearing houses.

ICE Clearing House Default Waterfall

Cash and Invested Margin Deposits

We have recorded cash and invested margin and guaranty fund deposits and amounts due in our balance sheets as current assets with corresponding current liabilities to the Members. As of March 31, 2025, our cash and invested margin deposits were as follows (in millions):

| ICE Clear Europe | ICE Clear Credit | ICE Clear U.S. | ICE NGX | Other ICE Clearing Houses | Total | ||||||||||||||||||||||||||||||

Original margin | $ | 48,320 | $ | 23,258 | $ | 6,759 | $ | — | $ | 4 | $ | 78,341 | |||||||||||||||||||||||

Unsettled variation margin, net | — | — | — | 1,035 | — | 1,035 | |||||||||||||||||||||||||||||

Guaranty fund | 2,320 | 4,208 | 797 | — | 5 | 7,330 | |||||||||||||||||||||||||||||

Delivery contracts receivable/payable, net | — | — | — | 690 | — | 690 | |||||||||||||||||||||||||||||

Total | $ | 50,640 | $ | 27,466 | $ | 7,556 | $ | 1,725 | $ | 9 | $ | 87,396 | |||||||||||||||||||||||

As of December 31, 2024, our cash and invested margin deposits were as follows (in millions):

| ICE Clear Europe | ICE Clear Credit | ICE Clear U.S. | ICE NGX | Other ICE Clearing Houses | Total | ||||||||||||||||||||||||||||||

Original margin | $ | 45,427 | $ | 23,843 | $ | 7,069 | $ | — | $ | 4 | $ | 76,343 | |||||||||||||||||||||||

Unsettled variation margin, net | — | — | — | 934 | — | 934 | |||||||||||||||||||||||||||||

Guaranty fund | 2,353 | 3,312 | 660 | — | 5 | 6,330 | |||||||||||||||||||||||||||||

Delivery contracts receivable/payable, net | — | — | — | 705 | — | 705 | |||||||||||||||||||||||||||||

Total | $ | 47,780 | $ | 27,155 | $ | 7,729 | $ | 1,639 | $ | 9 | $ | 84,312 | |||||||||||||||||||||||

Our cash and invested margin and guaranty fund deposits are maintained in accounts with national banks and highly-rated financial institutions or secured through direct investments, primarily in U.S. Treasury and other highly-rated foreign government securities, or reverse repurchase agreements with primarily overnight maturities. Reverse repos are valued daily and are subject to collateral maintenance provisions pursuant to which the counterparty must provide additional collateral if the underlying securities lose value in an amount sufficient to maintain collateralization of at least 102%. We primarily use Level 1 inputs when evaluating the fair value of the non-cash equivalent direct investments, as highly-rated government securities are quoted in active markets. The carrying value of these deposits is deemed to approximate fair value.

To provide a tool to address the liquidity needs of our clearing houses and manage the liquidation of margin and guaranty fund deposits held in the form of cash and high quality sovereign debt, ICE Clear Europe, ICE Clear Credit and ICE Clear U.S. have entered into Committed Repurchase Agreement Facilities, or Committed Repo. Additionally, ICE Clear Credit and ICE Clear Netherlands have entered into Committed FX Facilities to support these liquidity needs. As of March 31, 2025, the following facilities were in place:

•ICE Clear Europe: $1.0 billion in Committed Repo to have the ability to convert securities held as collateral into U.S. dollar, euro and pound sterling deposits with same day liquidity.

•ICE Clear Credit: $300 million in Committed Repo (U.S. dollar based) to have the ability to convert U.S. dollar\euro denominated sovereign debt held as collateral into U.S. dollar\euro deposits with same day liquidity, €250 million in Committed Repo (euro based) to have the ability to convert euro\U.S. dollar denominated sovereign debt deposits held as collateral into euro\U.S. dollar denominated deposits with same day liquidity, and €1.9 billion in Committed FX Facilities to have the ability to convert available U.S. dollar denominated cash into euro denominated cash to meet a euro denominated payment obligation with same day liquidity.

•ICE Clear U.S.: $250 million in Committed Repo to have the ability to convert U.S. dollar denominated sovereign debt deposits held as collateral into U.S. dollar deposits with same day liquidity.

•ICE Clear Netherlands: €10 million in Committed FX Facilities to have the ability to convert available non-euro denominated cash into euro denominated cash to meet euro denominated payment obligations with same day liquidity.

Details of our deposits are as follows (in millions):

| Cash and Cash Equivalent Margin Deposits and Guaranty Funds | ||||||||||||||||||||

| Clearing House | Investment Type | As of March 31, 2025 | As of December 31, 2024 | |||||||||||||||||

| ICE Clear Europe | National bank account | $ | 5,757 | $ | 4,817 | |||||||||||||||

| ICE Clear Europe | Reverse repo | 40,278 | 37,276 | |||||||||||||||||

| ICE Clear Europe | Sovereign debt | 2,162 | 4,515 | |||||||||||||||||

| ICE Clear Europe | Demand deposits | 58 | 648 | |||||||||||||||||

| ICE Clear Credit | National bank account | 20,423 | 20,369 | |||||||||||||||||

| ICE Clear Credit | Reverse repo | 3,894 | 4,089 | |||||||||||||||||

| ICE Clear Credit | Demand deposits | 3,149 | 2,697 | |||||||||||||||||

| ICE Clear U.S. | Reverse repo | 7,109 | 7,382 | |||||||||||||||||

| ICE Clear U.S. | Sovereign debt | 447 | 347 | |||||||||||||||||

| Other ICE Clearing Houses | Demand deposits | 9 | 9 | |||||||||||||||||

| Total cash and cash equivalent margin deposits and guaranty funds | $ | 83,286 | $ | 82,149 | ||||||||||||||||

| Invested Deposits, Delivery Contracts Receivable and Unsettled Variation Margin | ||||||||||||||||||||

| Clearing House | Investment Type | As of March 31, 2025 | As of December 31, 2024 | |||||||||||||||||

| ICE NGX | Unsettled variation margin and delivery contracts receivable | $ | 1,725 | $ | 1,639 | |||||||||||||||

| ICE Clear Europe | Invested deposits - sovereign debt | 2,385 | 524 | |||||||||||||||||

| Total invested deposits, delivery contracts receivable and unsettled variation margin | $ | 4,110 | $ | 2,163 | ||||||||||||||||

Other Deposits

In addition to the cash and invested deposits above, the ICE Clearing Houses have also received other assets from Members, which include government obligations, and may include other non-cash collateral such as letters of credit at ICE NGX, European emission allowance certificates or gold at ICE Clear Europe, to mitigate credit risk. For certain deposits, we may impose discount or “haircut” rates to ensure adequate collateral if market values fluctuate. These other deposits are not reflected in our consolidated balance sheets as the risks and rewards of these assets remain with the Members unless the clearing houses have sold or re-pledged the assets or in the event of a clearing member default, where the Member is no longer entitled to redeem the assets. Any income, gain or loss accrues to the Members. The ICE Clearing Houses do not, in the ordinary course, rehypothecate or re-pledge these assets. These pledged assets are not reflected in our balance sheets, and are as follows (in millions):

| As of March 31, 2025 | |||||||||||||||||||||||||||||

ICE Clear Europe | ICE Clear Credit | ICE Clear U.S. | ICE NGX | Total | |||||||||||||||||||||||||

Original margin: | |||||||||||||||||||||||||||||

Government securities at face value | $ | 36,402 | $ | 35,589 | $ | 14,603 | $ | — | $ | 86,594 | |||||||||||||||||||

Letters of credit | — | — | — | 3,360 | 3,360 | ||||||||||||||||||||||||

Emissions certificates at fair value | 819 | — | — | — | 819 | ||||||||||||||||||||||||

ICE NGX cash deposits | — | — | — | 862 | 862 | ||||||||||||||||||||||||

| Total | $ | 37,221 | $ | 35,589 | $ | 14,603 | $ | 4,222 | $ | 91,635 | |||||||||||||||||||

Guaranty fund: | |||||||||||||||||||||||||||||

Government securities at face value | $ | 702 | $ | 1,843 | $ | 269 | $ | — | $ | 2,814 | |||||||||||||||||||

| As of December 31, 2024 | |||||||||||||||||||||||||||||

ICE Clear Europe | ICE Clear Credit | ICE Clear U.S. | ICE NGX | Total | |||||||||||||||||||||||||

Original margin: | |||||||||||||||||||||||||||||

Government securities at face value | $ | 33,884 | $ | 31,590 | $ | 15,186 | $ | — | $ | 80,660 | |||||||||||||||||||

Letters of credit | — | — | — | 4,391 | 4,391 | ||||||||||||||||||||||||

Emissions certificates at fair value | 585 | — | — | — | 585 | ||||||||||||||||||||||||

ICE NGX cash deposits | — | — | — | 723 | 723 | ||||||||||||||||||||||||

| Total | $ | 34,469 | $ | 31,590 | $ | 15,186 | $ | 5,114 | $ | 86,359 | |||||||||||||||||||

Guaranty fund: | |||||||||||||||||||||||||||||

Government securities at face value | $ | 747 | $ | 1,389 | $ | 281 | $ | — | $ | 2,417 | |||||||||||||||||||

ICE NGX

ICE NGX owns a clearing house which administers the physical delivery of energy and environmental trading contracts. ICE NGX is the central counterparty to Members on opposite sides of its physically-settled contracts, and the balance related to delivered but unpaid contracts is recorded as a delivery contract net receivable, with an offsetting delivery contract net payable in our balance sheets. Unsettled variation margin equal to the fair value of open contracts is recorded as of each balance sheet date. There is no impact on our consolidated statements of income as an equal amount is recognized as both an asset and a liability. ICE NGX marks all of its outstanding physical natural gas, physical environmental and physical power contracts to market daily and requires full collateralization of net accrued variation losses. Due to the highly liquid nature and the short period of time to maturity, the fair values of our delivery contract net payable and net receivable are determined to approximate carrying value.

ICE NGX requires Members to maintain cash or letters of credit to serve as collateral in the event of default. The cash is maintained in a segregated bank account for the benefit of the Member, and remains the property of the Member and, therefore, it is not included in our consolidated balance sheets. ICE NGX maintains a committed daylight-overnight liquidity facility in the amount of $100 million with an additional $200 million uncommitted with a third-party Canadian chartered bank which provides liquidity in the event of a settlement shortfall, subject to certain conditions.

As of March 31, 2025, ICE NGX maintains a guaranty fund of $215 million funded by a $200 million letter of credit issued by a major Canadian chartered bank and backed by default insurance underwritten by Export Development Canada, or EDC, a Crown corporation operated at arm’s length from the Canadian government, plus $15 million held as restricted cash to fund the first loss amount that ICE NGX is responsible for under the default insurance policy. In the event of a participant default where the Member’s collateral is depleted, the shortfall would be covered by a draw down on the letter of credit following which ICE NGX would file a claim under the default insurance to recover additional losses up to $200 million beyond the $15 million first-loss amount that ICE NGX is responsible for under the default insurance policy. ICE NGX has also set aside $30 million of its own capital that could be used for liquidity purposes in the event of a Contracting Party default.

Clearing House Exposure

Each ICE Clearing House bears financial counterparty credit risk and provides a central counterparty guarantee, or performance guarantee, to its Members. In its guarantor role, each ICE Clearing House has equal and offsetting claims to and from Members on opposite sides of each contract, standing as an intermediary on every contract cleared. To reduce their exposure, the ICE Clearing Houses have a risk management program with both initial and ongoing membership standards. The ICE Clearing Houses mark all outstanding contracts to market and, with the exception of ICE NGX, pay and collect variation margin at least once daily.

Excluding the effects of original and variation margin, guaranty fund and collateral requirements and default insurance, the ICE Clearing Houses’ maximum estimated exposure for this guarantee would be the intra-day or full day change in fair value if all Members who have open positions with unrealized losses simultaneously defaulted, which is an extremely unlikely scenario. The levels of original margin are calibrated such that a portfolio the ICE Clearing House may be required to liquidate post Member default can be closed or auctioned without recourse to resources other than those deposited by the defaulting Member, assuming an appropriate risk confidence level and liquidation period. In addition to the base margin model, each ICE Clearing House, depending on its products, employs a number of margin add-ons related to position concentration, clearing member capital, volatility, spread responses, recovery rate sensitivity, jump-to-default, and wrong-way risk.

We also performed calculations to determine the fair value of our counterparty performance guarantee taking into consideration factors such as daily settlement of contracts, margining and collateral requirements, other elements of our risk management program, historical evidence of default payments, and estimated probability of potential default payouts by the ICE Clearing Houses. Based on these analyses, the estimated counterparty performance guarantee liability was determined to be nominal, and no liability was recorded as of March 31, 2025. The ICE Clearing Houses have never experienced an incident of a clearing member default which has required the use of the guaranty funds of non-defaulting clearing members or the assets of the ICE Clearing Houses.