Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not

reflected in the table and Examples below.

portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are

held in a taxable account at the shareholder level. These costs, which are not reflected in annual fund operating expenses or in the

example above, affect the Fund’s performance. During the most recent fiscal period ended December 31, 2024, the Fund’s portfolio

turnover rate was 7% of its average value.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all your shares at the end of

those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses

remain the same.

the S&P 500® Index (the “S&P 500”). The foundation of the Fund’s strategy involves buying shares of one or more cost-effective

ETFs that track the S&P 500, providing direct exposure to the broad market's performance. The Fund simultaneously implements a

monthly call option strategy to generate income and a quarterly put option strategy to protect against large declines in the S&P 500. In

strategically buying and selling put and call options on the S&P 500, the Fund seeks to provide a partial buffer against market

downturns, as well as provide additional income in flat to down markets, but resulting in lower upside potential during strong market

rallies.

In implementing its strategy, the Fund employs a methodology similar the MerQube Hedged Premium Income Index (the

“MQKHPI”). The MQKHPI is designed to be 100% invested in the Vanguard S&P 500 ETF (VOO) while selling 1-Month call

options and purchasing 3-Month put options on the SPDR S&P 500 ETF (SPY). The MQKHPI aims to generate income from selling

call spreads while providing downside protection through the purchase of put spreads, maintaining exposure to the U.S. large-cap

equity market.

The Fund will operate similarly to the MQKHPI, but with several differences. For one, while the Fund may elect to purchase VOO

and put and call options on SPY, the Fund will be more flexible in determining which cost-effective S&P 500 ETFs to purchase and

what S&P 500 call and put options to buy and sell. Additionally, unlike the MQKHPI that holds options to expiration, the Fund will

actively manage the risk-to-reward ratio of the Fund’s option strategies. If the perceived reward (premium or cost to close out a

position) is not proportional to the risk (maximum potential loss), the Fund’s Sub-advisor will use its discretion to adjust or close the

position if determined to be advantageous to the portfolio. The Fund’s Sub-adviser will also use independent judgement in

determining what particular option spreads to buy and sell under various market conditions, unlike the fixed spreads used by the

MQKHPI.

Although the Fund’s strategy is not expected to materially change in different interest rate environments, varying levels of market

volatility will impact the relative costs of downside protection and relative option spreads. Additionally, the sequence of investment

returns will affect the various strikes prices, expiration dates, and intended purposes of the options used by the Fund, and could

significantly impact Fund’s overall performance. The Fund, based on current market conditions, seeks to achieve the best balance of

premium income/costs, downside protection, and upside potential to meet its investment objective of current income with the potential

for capital appreciation.

Monthly Call Options Strategy

Call options are derivative instruments that allow the option purchaser to contractually purchase a particular security (or the security

index) from the option issuer at a set price (the “strike price”) up to the expiration date of the options. When the issuer sells the call

option, it receives a premium from the buyer in hopes that the option will not be exercised by the buyer.

The monthly call options strategy consists of a mix of selling and purchasing call options on the S&P 500 (“S&P 500 call options”).

The Fund seeks to generate income from the premiums earned from the sold S&P 500 call options. At the same time, the Fund seeks

to realize capital appreciation from its S&P 500 ETF holdings as the S&P 500 increases in value, but with potentially reduced upside

because of the sold S&P 500 call options it uses to generate premium income. The Fund’s purchased S&P 500 call options, however,

are intended to offset this reduced upside potential and limit the risk of missing out on strong market rallies of the S&P 500.

On a regular basis, typically monthly, the Fund sells S&P 500 call options to generate premium income while simultaneously buying

“out of the money” long S&P 500 call options (i.e., options to purchase at a strike price that is higher than the current price of the

reference security or index) to hedge against the possibility that the sold S&P 500 call options are exercised because the S&P 500

increases above the strike price of the sold S&P 500 call options. For example, as the S&P 500 increases in value during the month,

the holders of the sold S&P 500 call options may be more incentivized to exercise their options which will create some losses for the

Fund. However, if the price of the S&P 500 increases above the strike price of the purchased S&P 500 call options, the Fund will be

protected from larger losses because the Fund will exercise its purchased S&P 500 call options, offsetting a portion of its losses on the

sold S&P 500 call options.

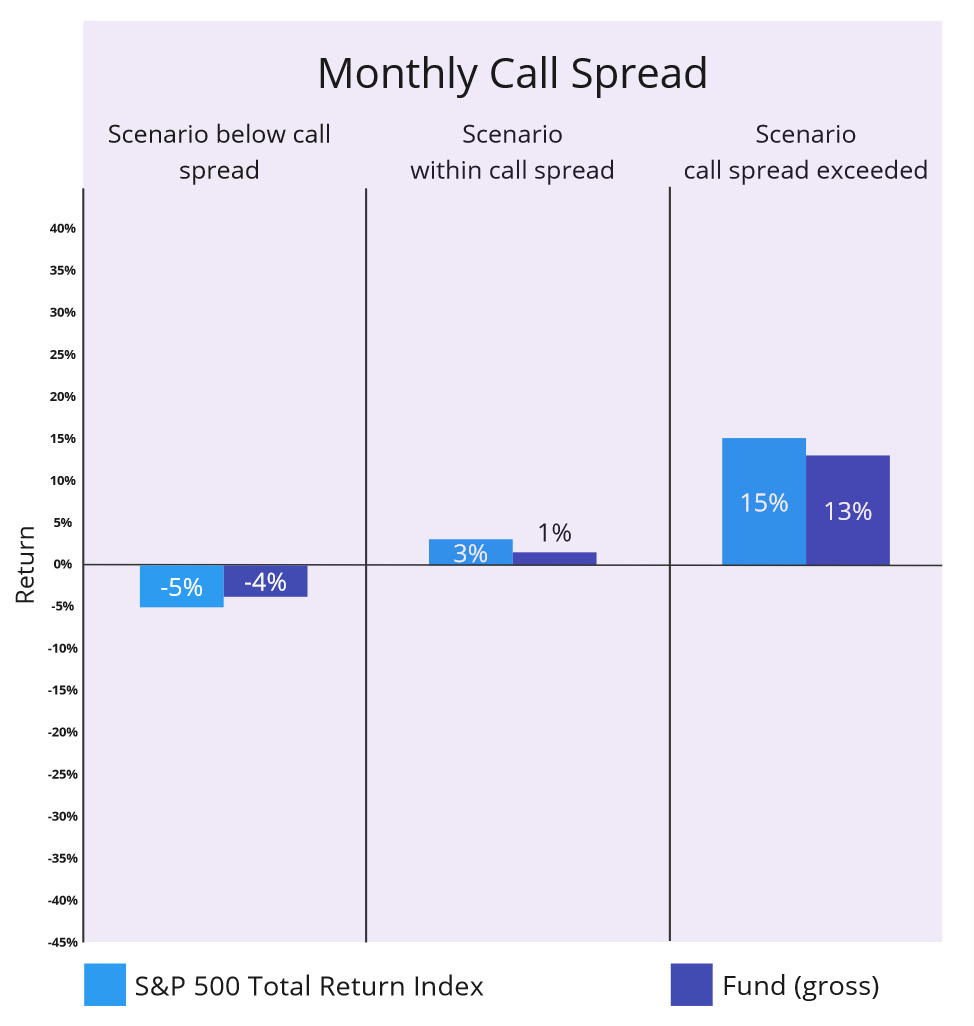

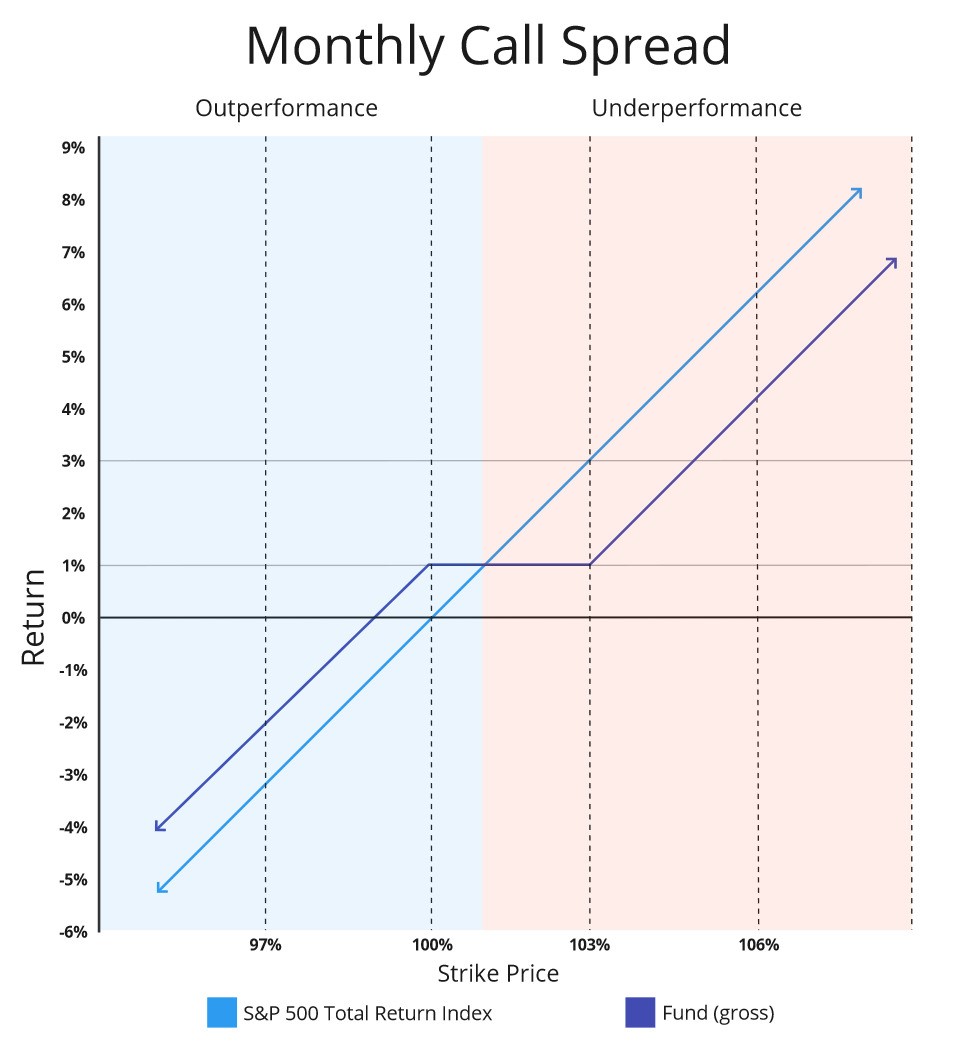

The call option strategy aims to profit from stable or declining S&P 500 prices, with the ideal scenario being the S&P 500 staying

below the strike price of the sold S&P 500 call options. At the same time, the strategy seeks to control and cap the risk of loss from

rapid gains of the S&P 500 with the purchased S&P 500 call options. While the strike prices of the S&P 500 call options may vary, the

Fund will typically sell call options with a strike price between approximately 98-105% of the current value of the S&P 500, and

purchase call options with a strike price between approximately 101-110% of the current value of the S&P 500. Once the S&P 500

appreciates by approximately 5% from its current level (the strike price of the sold call), such call spreads will begin to create a loss.

This loss will, however, will typically be capped at approximately 3% (the difference in strike prices) after the net income from the

call spreads.

Because the call option strategy is typically executed every month, it may have a larger impact on the Fund’s returns than the put

option strategy discussed below that is typically executed on a quarterly basis.

For illustrative purposes only. Figures are approximate and subject to change. Charts assume a quarterly net premium gain of 3%, which results from three

monthly call spreads and one quarterly put spread.

Quarterly Put Options Strategy

Put options are derivative instruments that allow the option purchaser to contractually sell a particular security (or the value of a

security index) to the option issuer at a strike price up to the expiration date of the options. When the issuer sells the put option, it

receives a premium from the buyer in hopes that the buyer will not exercise the option.

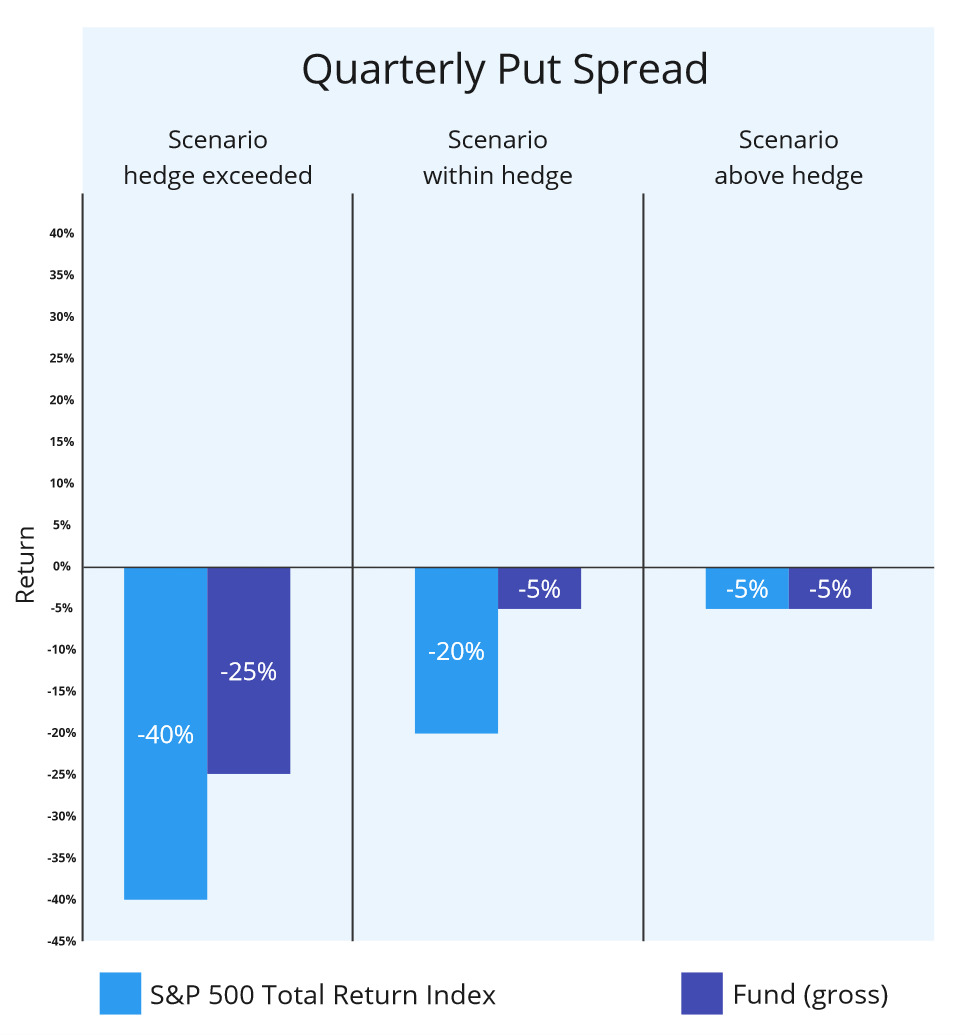

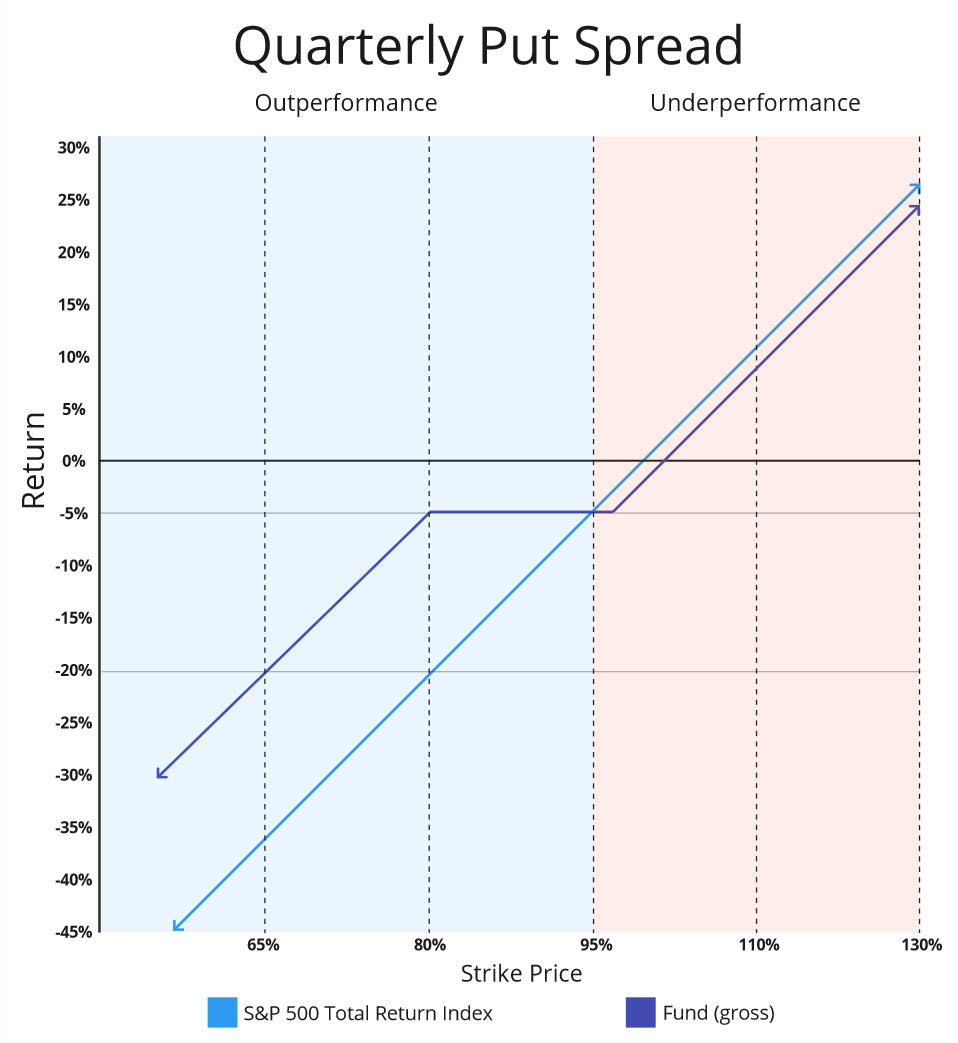

The Fund’s put options strategy, typically executed on a quarterly basis, is designed to protect against large declines in the S&P 500.

The quarterly put options strategy consists of a mix of purchased (or “long”) put options and sold (or “written”) put options on the

S&P 500 Index (“S&P 500 put options”). While the strike prices of the put options may vary, each quarter the Fund typically

purchases S&P 500 put options that are approximately 94-96% of the current S&P 500 level, paying a premium for downside

protection from a large decline in the S&P 500. The Fund simultaneously sells S&P 500 put options with a strike price that is

approximately 75-85% of the current price of the S&P 500 to generate some premium income to offset a portion of the cost of the

purchased put options. The quarterly options strategy of buying a put slightly below the current market price and selling another put

farther below the current market price is designed to protect against significant market downturns at a reduced cost. While the strike

prices of the put options will vary, the put spreads will typically provide a payment to offset losses once the S&P 500 declines by

approximately 5% (the strike price of the purchase put) but will no longer offset losses once the S&P 500 declines by more than an

approximately 20% (the difference in strike prices) after the net costs of the put spreads.

For illustrative purposes only. Figures are approximate and subject to change. Charts assume a quarterly net premium gain of 3%, which results from three

monthly call spreads and one quarterly put spread.

Expected Relative Performance of the Strategy

The Fund’s performance will vary, at times substantially, from the performance of the MQKHPI and the S&P 500. In general,

however, the Fund expects to perform somewhat in line with the MQKHPI, with the Fund’s active decisions around the

implementation of its options strategies intended to improve the Fund’s performance relative to the MQKHPI.

The Fund’s expected performance relative to the S&P 500 under various market conditions can be summarized as follows:

When the S&P 500 is Flat or Declines: Expected Outperformance. In months and quarters where the S&P 500 shows minimal

movement or decreases, the Fund’s overall performance is generally expected to also be flat to negative. However, the Fund would be

positioned to outperform the S&P 500 primarily due to the monthly premium income generated from the monthly call options.

•This anticipated relative outperformance is expected to increase during quarters where the S&P 500 declines by more than

approximately 4-6%, due to the additional downside protection from the quarterly put options.

•If the S&P 500 declines by more than approximately 20% from the purchase price of the put options, the Fund would have no

further downside protection other than the call option premiums. The Fund would participate fully in the decline of the S&P

500 until new put options are purchased.

When the S&P 500 is Up: Expected Underperformance. In months and quarters where the S&P 500 experiences an increase greater

than approximately 1% (the estimated long-term average of option premiums collected), the Fund’s overall performance is generally

expected to be positive. However, the Fund is likely to underperform the S&P 500 primarily be due to the Fund's option strategy that

is intended to sacrifice a portion of the Fund’s upside potential in return for reduced volatility and additional income.

•The underperformance for each monthly call option expiration cycle would be limited to the difference in call option strike

prices (expected to be approximately 3%) and the approximate 1% premium collected.

•If the S&P 500 rises above the strike prices of both call options, the Fund will no longer have capped appreciation until it

sells new call options.”

The Fund is considered to be non-diversified, which means it may invest a high percentage of its assets in a limited number of

investments. Additionally, the Fund’s investment strategies will involve active and frequent purchases and sales of call and put

options, but are not expected to result in high portfolio turnover.

has been in operation for a full calendar year, performance information will be shown here. You should be aware that the Fund’s past

performance (before and after taxes) may not be an indication of how the Fund will perform in the future. Updated performance

information and daily NAV per share is available at no cost by calling toll-free 866-303-8623 and on the Fund’s website at https://

www.kensingtonassetmanagement.com/funds/documents.

particular assets may prove to be incorrect and may not produce the desired results.

sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect

securities markets generally or factors affecting specific industries, sectors, geographic markets, or companies in which the

Fund invests.

◦Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited

number of financial institutions that may act as Authorized Participants (“APs”). In addition, there may be a limited

number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events

occur, shares may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or

otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform

these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business

activities and no other entities step forward to perform their functions.

◦Cash Redemption Risk. While not expected to be a regular occurrence, the Fund’s investment strategy may require it

to redeem shares for cash or to otherwise include cash as part of its redemption proceeds. The Fund may be required

to sell or unwind portfolio investments to obtain the cash needed to distribute redemption proceeds. This may cause

the Fund to recognize a capital gain that it might not have recognized if it had made a redemption in-kind. As a

result, the Fund may pay out higher annual capital gain distributions than if the in-kind redemption process was

used.

◦Costs of Buying or Selling Shares. Due to the costs of buying or selling shares, including brokerage commissions

imposed by brokers and bid-ask spreads, frequent trading of shares may significantly reduce investment results and

an investment in shares may not be advisable for investors who anticipate regularly making small investments.

◦Shares May Trade at Prices Other Than NAV. As with all ETFs, shares may be bought and sold in the secondary

market at market prices. Although it is expected that the market price of shares will approximate the Fund’s NAV,

there may be times when the market price of shares is more than the NAV intra-day (premium) or less than the NAV

intra-day (discount) due to supply and demand of shares or during periods of market volatility. This risk is

heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading

activity for shares in the secondary market, in which case such premiums or discounts may be significant. Because

securities held by the Fund may trade on foreign exchanges that are closed when the Fund’s primary listing

exchange is open, there are likely to be deviations between the current price of a security and the security’s last

quoted price from the closed foreign market. This may result in premiums and discounts that are greater than those

experienced by domestic ETFs.

◦Trading. Although shares are listed for trading on the NYSE Cboe BZX Exchange, Inc. (the “Exchange”) and may

be traded on U.S. exchanges other than the Exchange, there can be no assurance that shares will trade with any

volume, or at all, on any stock exchange. In stressed market conditions, the liquidity of shares may begin to mirror

the liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than shares, and this

could lead to differences between the market price of the shares and the underlying value of those shares.

number of financial institutions that may act as Authorized Participants (“APs”). In addition, there may be a limited

number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events

occur, shares may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or

otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform

these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business

activities and no other entities step forward to perform their functions.

to redeem shares for cash or to otherwise include cash as part of its redemption proceeds. The Fund may be required

to sell or unwind portfolio investments to obtain the cash needed to distribute redemption proceeds. This may cause

the Fund to recognize a capital gain that it might not have recognized if it had made a redemption in-kind. As a

result, the Fund may pay out higher annual capital gain distributions than if the in-kind redemption process was

used.

imposed by brokers and bid-ask spreads, frequent trading of shares may significantly reduce investment results and

an investment in shares may not be advisable for investors who anticipate regularly making small investments.

market at market prices. Although it is expected that the market price of shares will approximate the Fund’s NAV,

there may be times when the market price of shares is more than the NAV intra-day (premium) or less than the NAV

intra-day (discount) due to supply and demand of shares or during periods of market volatility. This risk is

heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading

activity for shares in the secondary market, in which case such premiums or discounts may be significant. Because

securities held by the Fund may trade on foreign exchanges that are closed when the Fund’s primary listing

exchange is open, there are likely to be deviations between the current price of a security and the security’s last

quoted price from the closed foreign market. This may result in premiums and discounts that are greater than those

experienced by domestic ETFs.

be traded on U.S. exchanges other than the Exchange, there can be no assurance that shares will trade with any

volume, or at all, on any stock exchange. In stressed market conditions, the liquidity of shares may begin to mirror

the liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than shares, and this

could lead to differences between the market price of the shares and the underlying value of those shares.

derive at least 90 percent of its gross income each taxable year from qualifying income. Income from certain commodity-

linked derivative instruments in which the Fund invests is not considered qualifying income. The Fund will therefore restrict

its income from direct investments in commodity-linked derivative instruments that do not generate qualifying income, such

as commodity futures, to a maximum of 10 percent of its gross income.

conditions, interest rate levels, and political events affect U.S. and international investment markets. Additionally, unexpected

local, regional or global events, such as war; acts of terrorism; financial, political or social disruptions; natural, environmental

or man-made disasters; the spread of infectious illnesses or other public health issues (such as the global pandemic

coronavirus disease 2020 (COVID-19)); and recessions and depressions could have a significant impact on the Fund and its

investments and may impair market liquidity. Such events can cause investor fear, which can adversely affect the economies

of nations, regions and the market in general, in ways that cannot necessarily be foreseen.

expenses. Each underlying fund is subject to specific risks, depending on the nature of its investment strategy. The manager

of an underlying fund may not be successful in implementing its strategy. ETF shares may trade at a market price that may be

lower (a discount) or higher (a premium) than the ETF’s net asset value. ETFs are also subject to brokerage and/or other

trading costs, which could result in greater expenses to the Fund. Because the value of ETF shares depends on the demand in

the market, the Adviser may not be able to liquidate the Fund’s holdings at the most optimal time, adversely affecting

performance.

loss from a change in the level of the market price of the underlying security (or a basket or index) in a notional amount that

exceeds the amount of cash or assets required to establish or maintain the derivative instrument. Adverse changes in the value

or level of the underlying asset or index, which the Fund may not directly own, can result in a loss to the Fund substantially

greater than the amount invested in the derivative itself. The use of derivative instruments also exposes the Fund to additional

risks and transaction costs. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate

perfectly with the overall securities markets.

◦Options Risk. An option is an agreement that, for a premium payment or fee, gives the option holder (the purchaser) the

right but not the obligation to buy (a “call option”) or sell (a “put option”) the underlying asset (or settle for cash an

amount based on an underlying asset, rate, or index) at a specified price (the “exercise price”) during a period of time or

on a specified date. Investments in options are considered speculative. When the Fund purchases an option, it may lose

the premium paid for it if the price of the underlying security or other assets decreased or remained the same (in the case

of a call option) or increased or remained the same (in the case of a put option). If a put or call option purchased by the

Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund. By

writing put options, the Fund takes on the risk of declines in the value of the underlying instrument, including the

possibility of a loss up to the entire exercise price of each option it sells but without the corresponding opportunity to

benefit from potential increases in the value of the underlying instrument. By writing a call option, the Fund may be

obligated to deliver instruments underlying an option at less than the market price. In the case of an uncovered call

option, there is a risk of unlimited loss.

right but not the obligation to buy (a “call option”) or sell (a “put option”) the underlying asset (or settle for cash an

amount based on an underlying asset, rate, or index) at a specified price (the “exercise price”) during a period of time or

on a specified date. Investments in options are considered speculative. When the Fund purchases an option, it may lose

the premium paid for it if the price of the underlying security or other assets decreased or remained the same (in the case

of a call option) or increased or remained the same (in the case of a put option). If a put or call option purchased by the

Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund. By

writing put options, the Fund takes on the risk of declines in the value of the underlying instrument, including the

possibility of a loss up to the entire exercise price of each option it sells but without the corresponding opportunity to

benefit from potential increases in the value of the underlying instrument. By writing a call option, the Fund may be

obligated to deliver instruments underlying an option at less than the market price. In the case of an uncovered call

option, there is a risk of unlimited loss.

These derivative instruments provide the economic effect of financial leverage by creating additional investment exposure to

the underlying asset, as well as the potential for greater loss. If the Fund uses leverage through activities such as entering into

derivative instruments, the Fund has the risk that losses may exceed the net assets of the Fund. The net asset value of the

Fund while employing leverage will be more volatile and sensitive to market movements.

to attract sufficient assets to operate efficiently.

one or more issuers. The Fund also invests in underlying funds that are non-diversified. The Fund’s performance may be

more sensitive to any single economic, business, political or regulatory occurrence than the value of shares of a diversified

investment company.

| [1] | Kensington Asset Management, LLC (the “Adviser”) has agreed to pay all expenses of the Fund, except for: (i) brokerage expenses and other fees, charges, taxes, levies or expenses incurred in connection with the execution of portfolio transactions or in connection with creation and redemption transactions; (ii) fees or expenses in connection with any arbitration, litigation or pending or threatened arbitration or litigation, including any settlements in connection therewith; (iii) extraordinary expenses; (iv) distribution fees and expenses paid by the Fund under any distribution plan adopted pursuant to Rule 12b-1 under the Investment Company Act of 1940, as amended (“1940 Act”); (v) interest and taxes of any kind or nature; (vi) any fees and expenses related to the provision of securities lending services; (vii) the advisory fee payable to the Adviser; (viii) Acquired Fund Fees and Expenses; and (ix) all costs incurred in connection with shareholder meetings and all proxy solicitations (except for such shareholder meetings and proxy solicitations related to: (a) changes to the Adviser’s investment advisory agreement, (b) changes in control at the Adviser or a sub-adviser, (c) the election of any Board member who is an “interested person” of the Adviser (as that term is defined under Section 2(a)(19) of the 1940 Act), (d) matters initiated by the Adviser, or (e) any other matters that directly benefit the Adviser). |

| [2] | Acquired Fund Fees and Expenses (“AFFE”) are indirect costs of investing in other investment companies. The operating expenses in this fee table do not correlate to the expense ratio in the Fund’s financial highlights because the financial statements include only the direct operating expenses incurred by the Fund and not the indirect costs of investing in other investment companies. |