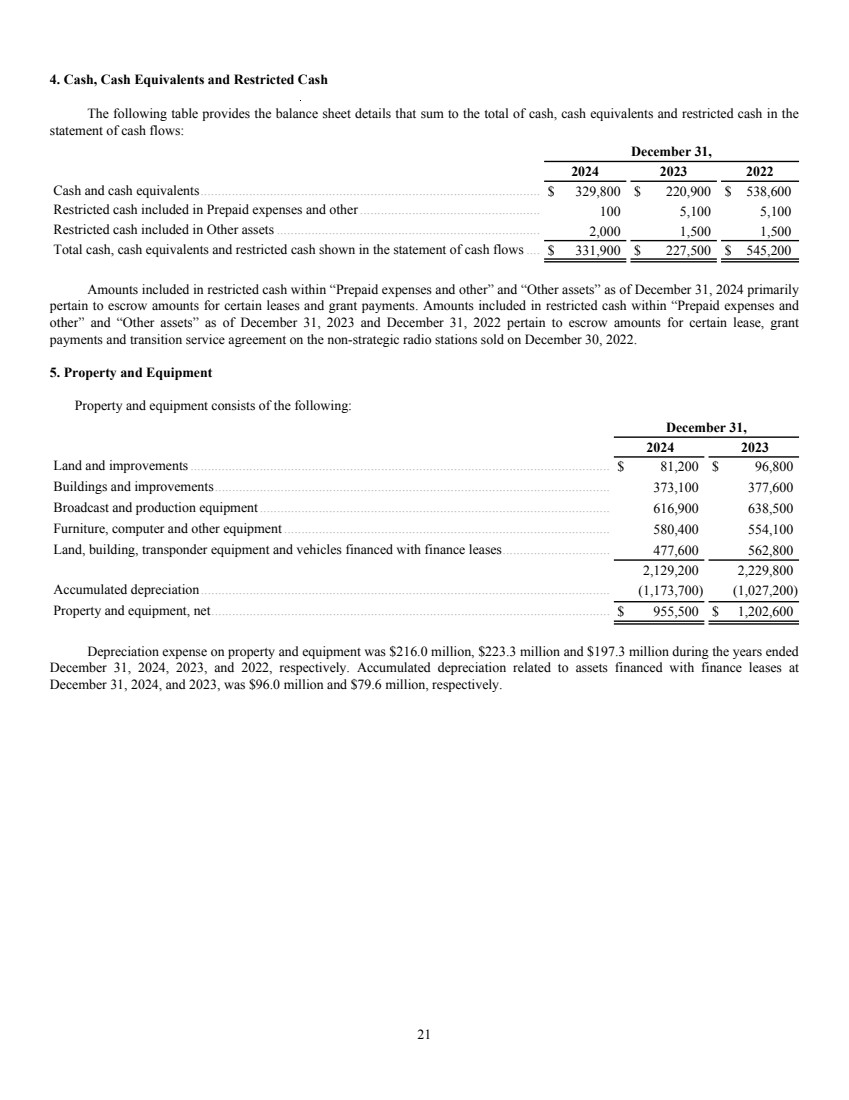

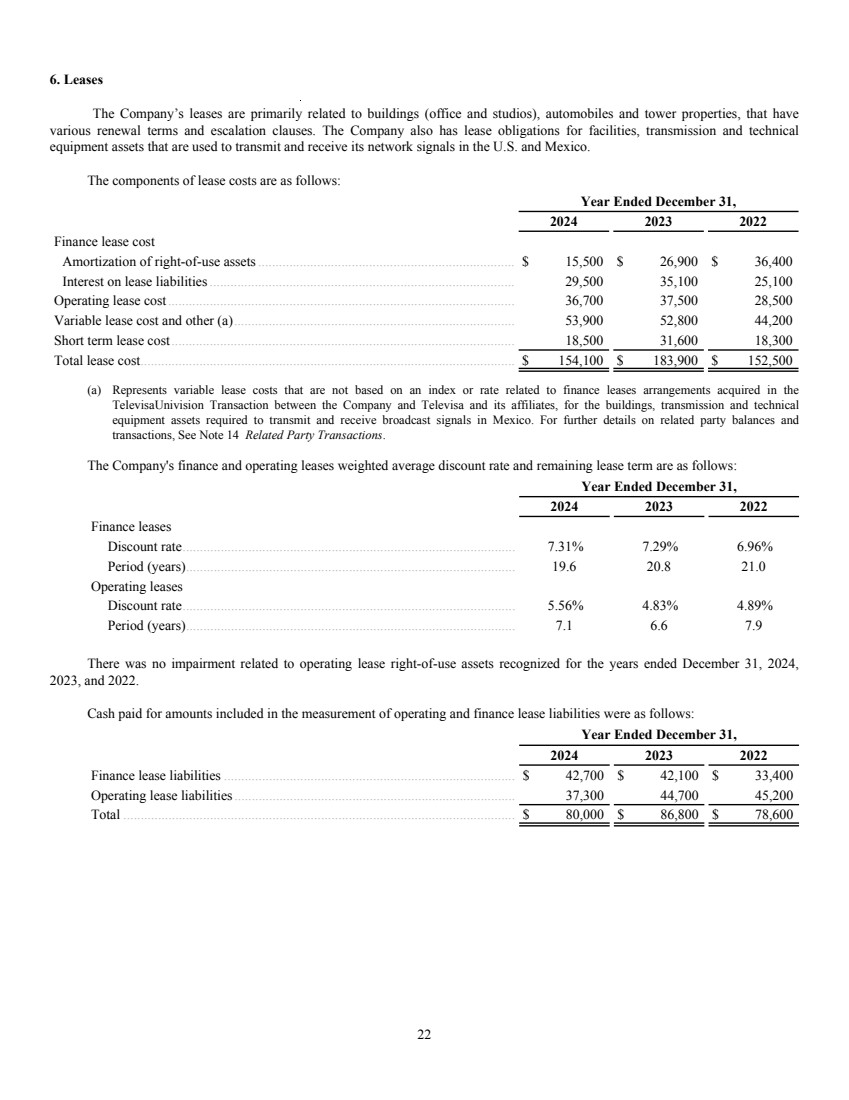

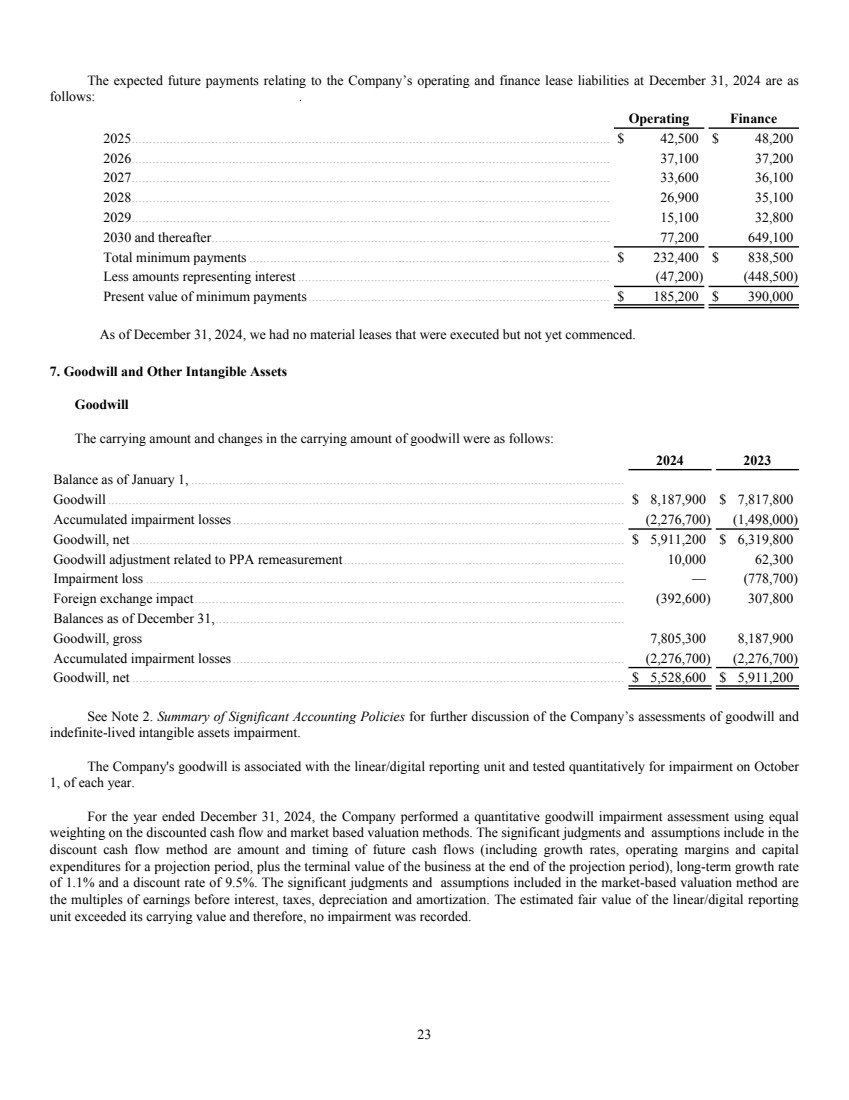

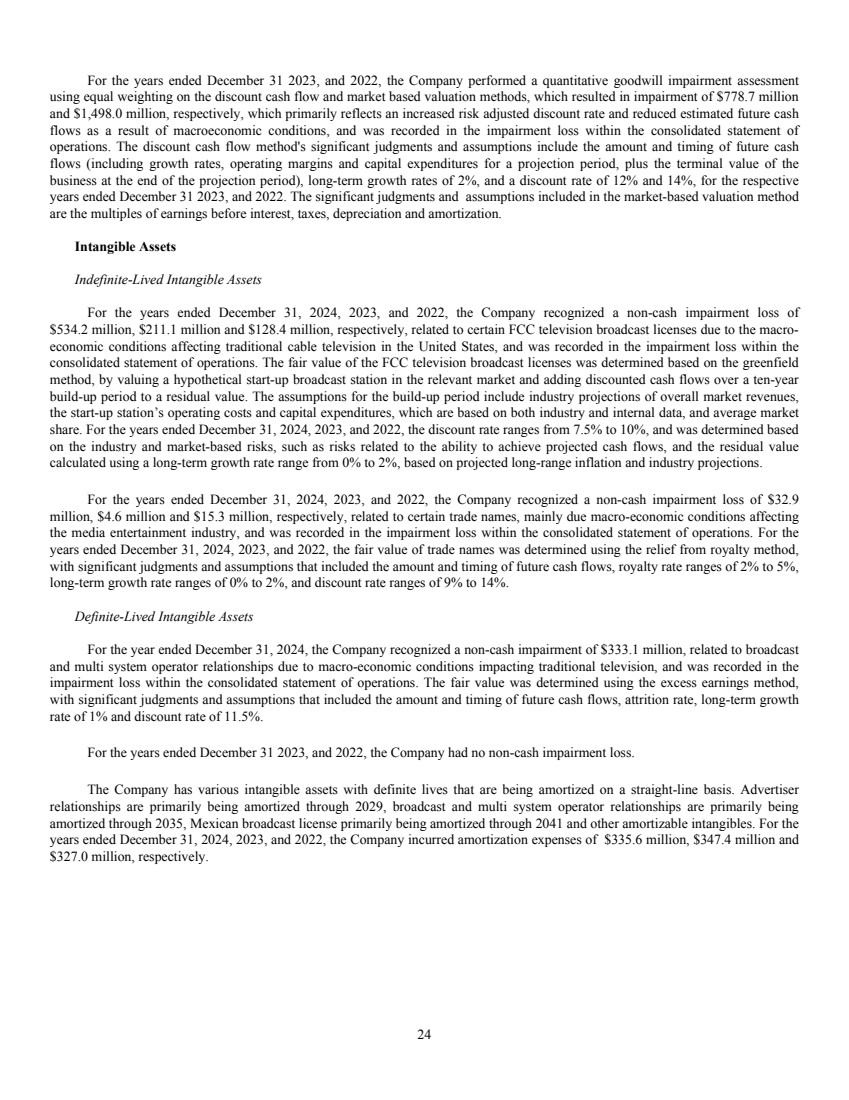

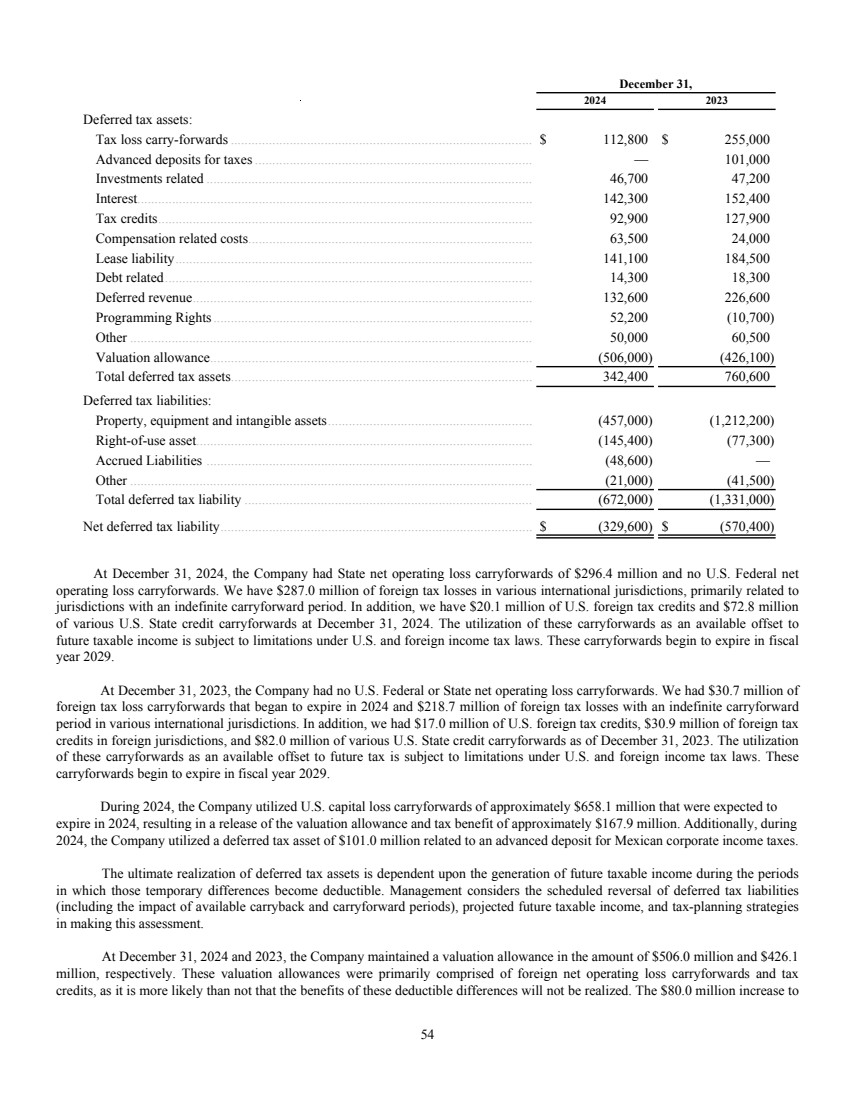

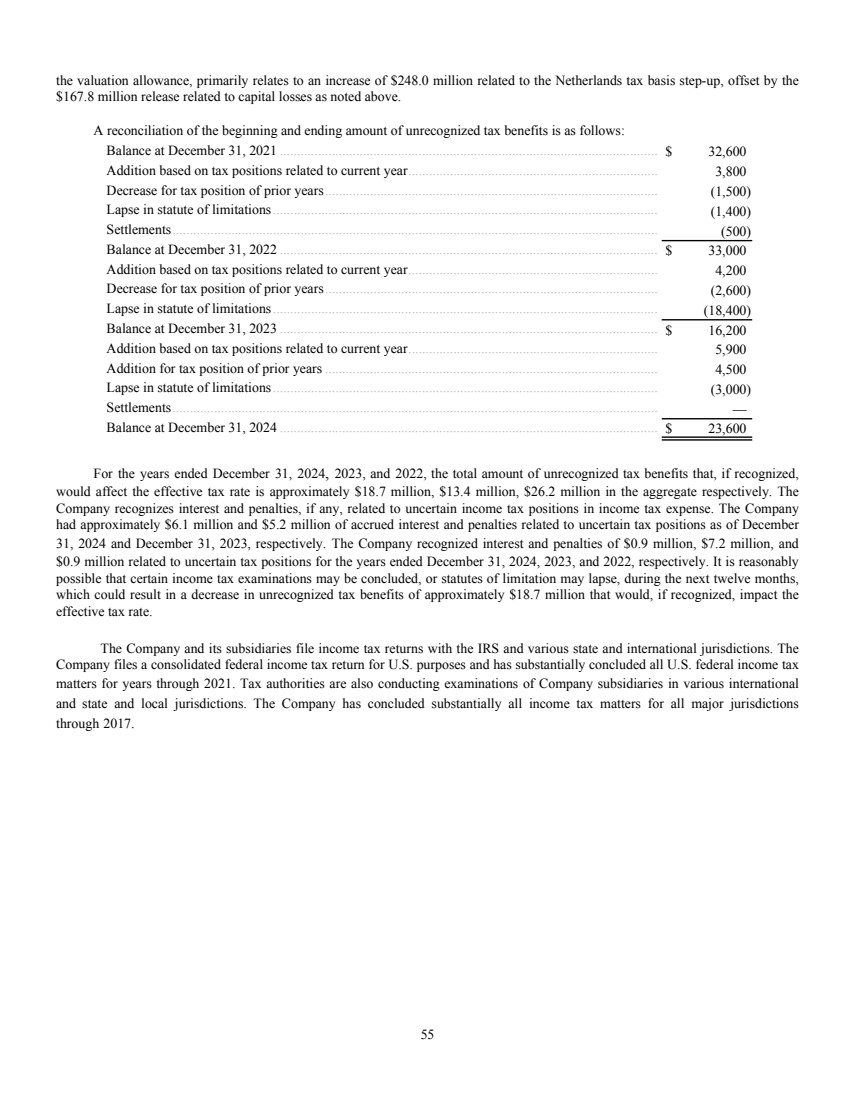

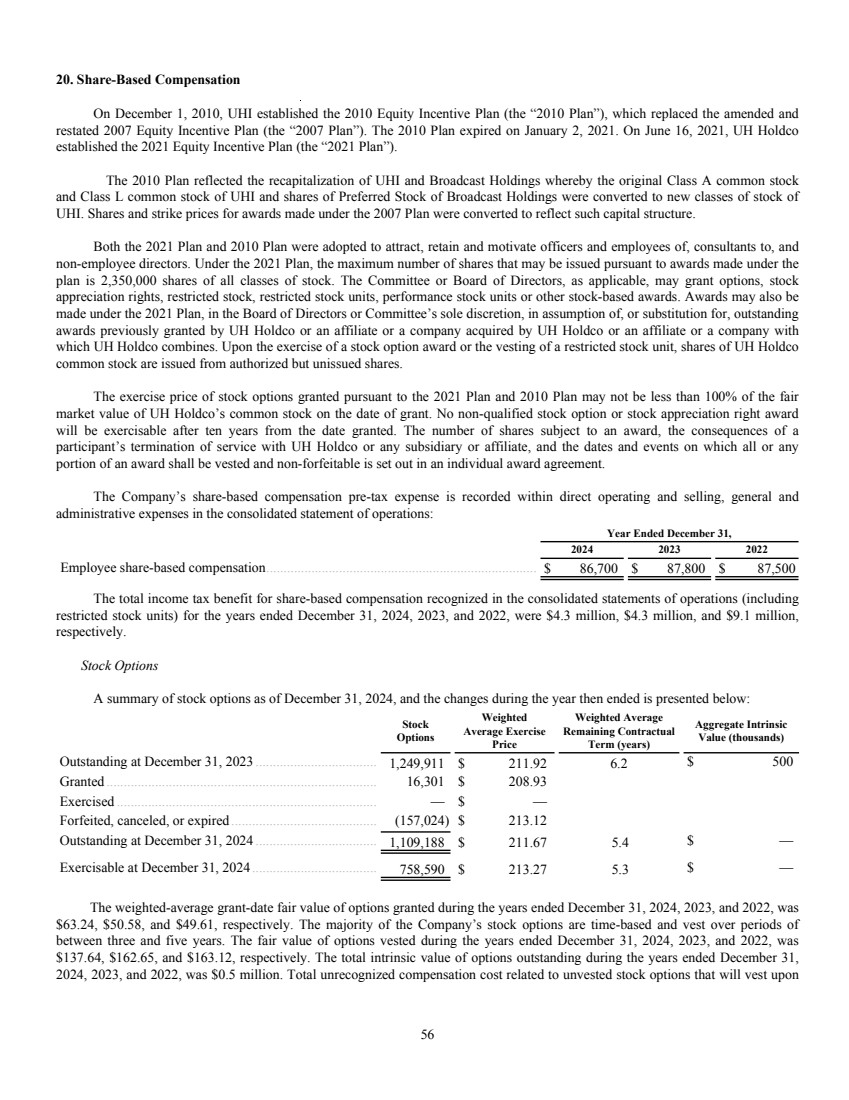

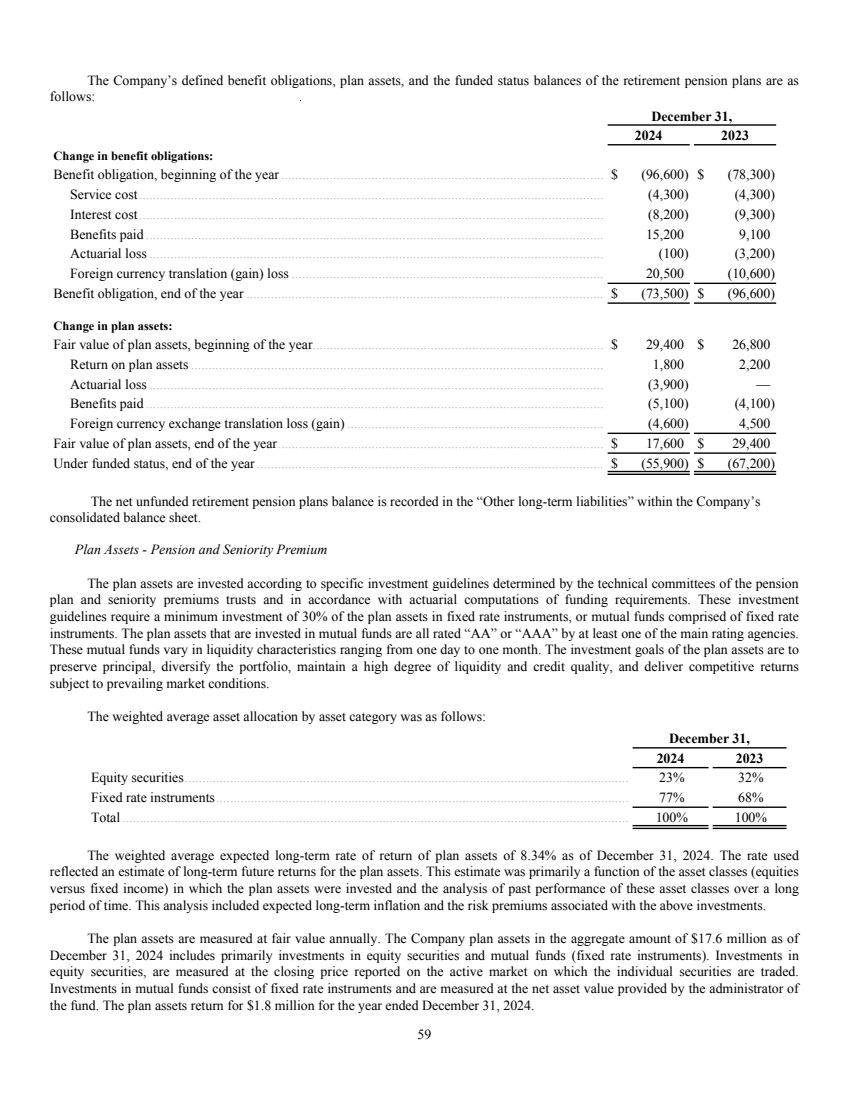

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES 2024 Year End Financial Information |

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES INDEX Page Financial Information: Report of Independent Auditors................................................................................................................................. 3 Consolidated Balance Sheets at December 31, 2024 and December 31, 2023.......................................................... 7 Consolidated Statements of Operations for the years ended December 31, 2024, 2023, and 2022 ......................... 8 Consolidated Statements of Comprehensive Loss for the years ended December 31, 2024, 2023, and 2022 .......... 9 Consolidated Statements of Changes in Redeemable Convertible Preferred Stock and Stockholders' Equity for the years ended December 31, 2024, 2023, and 2022 ............................................................................................... 10 Consolidated Statements of Cash Flows for the years ended December 31, 2024, 2023, and 2022 ........................ 11 Notes to Consolidated Financial Statements.............................................................................................................. 12 2 |

| KPMG LLP Brickell City Centre, Suite 1200 78 SW 7 Street Miami, FL 33130 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. Independent Auditors’ Report The Board of Directors and Stockholders TelevisaUnivision, Inc.: Opinion We have audited the consolidated financial statements of TelevisaUnivision, Inc. and its subsidiaries (the Company), which comprise the consolidated balance sheet as of December 31, 2024, and the related consolidated statement of operations, comprehensive loss, changes in redeemable convertible preferred stock and stockholders’ equity, and cash flows for the year then ended, and the related notes to the consolidated financial statements. In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2024, and the results of its operations and its cash flows for the year then ended in accordance with U.S. generally accepted accounting principles. Basis for Opinion We conducted our audit in accordance with auditing standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are required to be independent of the Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Responsibilities of Management for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with U.S. generally accepted accounting principles, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. In preparing the consolidated financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for one year after the date that the consolidated financial statements are issued. Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the consolidated financial statements. 3 |

| 4 In performing an audit in accordance with GAAS, we: ● Exercise professional judgment and maintain professional skepticism throughout the audit. ● Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. ● Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. Accordingly, no such opinion is expressed. ● Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the consolidated financial statements. ● Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for a reasonable period of time. We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control related matters that we identified during the audit. Miami, Florida March 27, 2025 |

| Ernst & Young LLP 1 Manhattan West New York, NY 10001-2177 Tel: +1 212 773 3000 Fax: +1 212 773 6350 ey.com Report of Independent Auditors Board of Directors and Stockholders of TelevisaUnivision, Inc. and subsidiaries Opinion We have audited the consolidated financial statements of TelevisaUnivision, Inc. and subsidiaries (the Company), which comprise the consolidated balance sheet as of December 31, 2023, and the related consolidated statements of operations, comprehensive loss, changes in redeemable convertible preferred stock and stockholders’ equity and cash flows for the years ended December 31, 2023 and 2022, and the related notes (collectively referred to as the “financial statements”). In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Company at December 31, 2023, and the results of its operations and its cash flows for the years ended December 31, 2023 and 2022 in accordance with accounting principles generally accepted in the United States of America. Basis for Opinion We conducted our audits in accordance with auditing standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of the Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audits. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Responsibilities of Management for the Financial Statements Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error. In preparing the financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for one year after the date that the financial statements are available to be issued. Auditor’s Responsibilities for the Audit of the Financial Statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free of material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the financial statements. In performing an audit in accordance with GAAS, we: 5 |

| • Exercise professional judgment and maintain professional skepticism throughout the audit. • Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. • Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. Accordingly, no such opinion is expressed. • Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the financial statements. • Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for a reasonable period of time. We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control-related matters that we identified during the audit. April 15, 2024 6 |

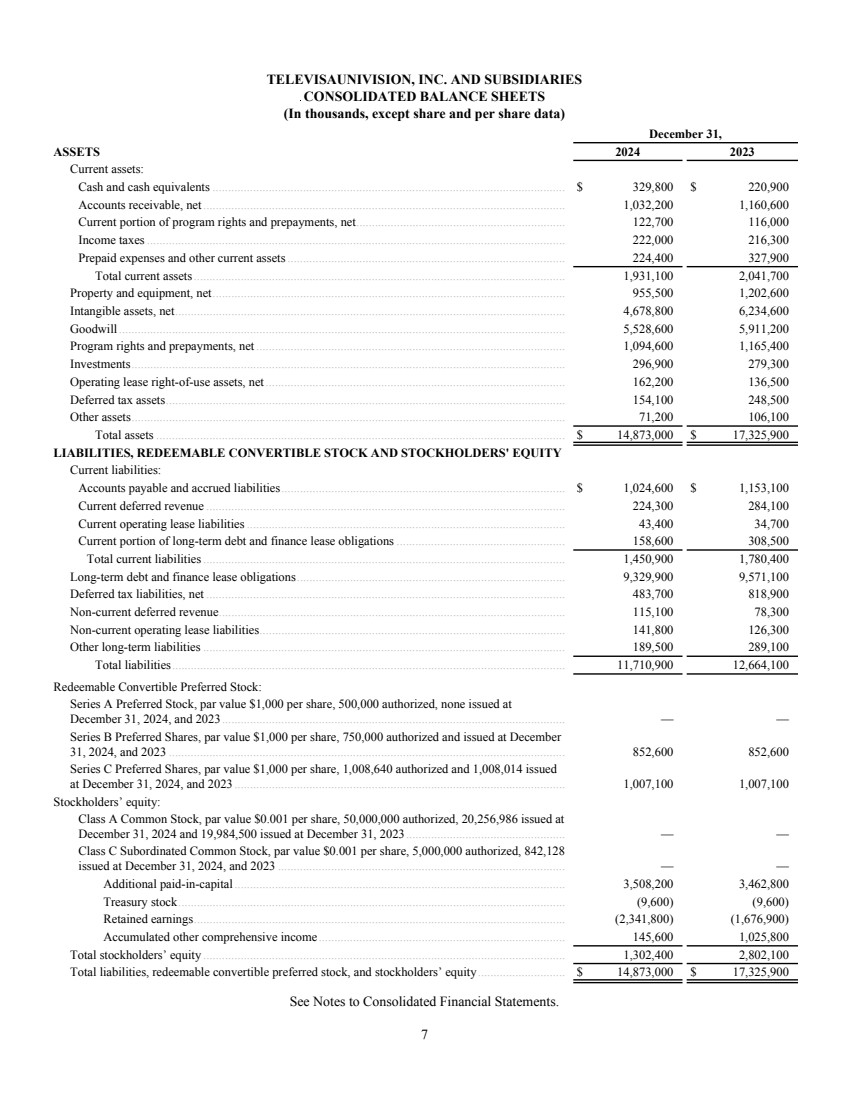

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS (In thousands, except share and per share data) December 31, ASSETS 2024 2023 Current assets: Cash and cash equivalents ................................................................................................................. $ 329,800 $ 220,900 Accounts receivable, net.................................................................................................................... 1,032,200 1,160,600 Current portion of program rights and prepayments, net................................................................... 122,700 116,000 Income taxes...................................................................................................................................... 222,000 216,300 Prepaid expenses and other current assets......................................................................................... 224,400 327,900 Total current assets....................................................................................................................... 1,931,100 2,041,700 Property and equipment, net................................................................................................................. 955,500 1,202,600 Intangible assets, net............................................................................................................................. 4,678,800 6,234,600 Goodwill............................................................................................................................................... 5,528,600 5,911,200 Program rights and prepayments, net ................................................................................................... 1,094,600 1,165,400 Investments........................................................................................................................................... 296,900 279,300 Operating lease right-of-use assets, net................................................................................................ 162,200 136,500 Deferred tax assets................................................................................................................................ 154,100 248,500 Other assets........................................................................................................................................... 71,200 106,100 Total assets ................................................................................................................................... $ 14,873,000 $ 17,325,900 LIABILITIES, REDEEMABLE CONVERTIBLE STOCK AND STOCKHOLDERS' EQUITY Current liabilities: Accounts payable and accrued liabilities........................................................................................... $ 1,024,600 $ 1,153,100 Current deferred revenue ................................................................................................................... 224,300 284,100 Current operating lease liabilities...................................................................................................... 43,400 34,700 Current portion of long-term debt and finance lease obligations ...................................................... 158,600 308,500 Total current liabilities.................................................................................................................... 1,450,900 1,780,400 Long-term debt and finance lease obligations...................................................................................... 9,329,900 9,571,100 Deferred tax liabilities, net ................................................................................................................... 483,700 818,900 Non-current deferred revenue............................................................................................................... 115,100 78,300 Non-current operating lease liabilities.................................................................................................. 141,800 126,300 Other long-term liabilities .................................................................................................................... 189,500 289,100 Total liabilities.............................................................................................................................. 11,710,900 12,664,100 Redeemable Convertible Preferred Stock: Series A Preferred Stock, par value $1,000 per share, 500,000 authorized, none issued at December 31, 2024, and 2023.............................................................................................................. — — Series B Preferred Shares, par value $1,000 per share, 750,000 authorized and issued at December 31, 2024, and 2023 ............................................................................................................................... 852,600 852,600 Series C Preferred Shares, par value $1,000 per share, 1,008,640 authorized and 1,008,014 issued at December 31, 2024, and 2023 .......................................................................................................... 1,007,100 1,007,100 Stockholders’ equity: Class A Common Stock, par value $0.001 per share, 50,000,000 authorized, 20,256,986 issued at December 31, 2024 and 19,984,500 issued at December 31, 2023................................................... — — Class C Subordinated Common Stock, par value $0.001 per share, 5,000,000 authorized, 842,128 issued at December 31, 2024, and 2023 ............................................................................................ — — Additional paid-in-capital.......................................................................................................... 3,508,200 3,462,800 Treasury stock............................................................................................................................ (9,600) (9,600) Retained earnings....................................................................................................................... (2,341,800) (1,676,900) Accumulated other comprehensive income............................................................................... 145,600 1,025,800 Total stockholders’ equity .................................................................................................................... 1,302,400 2,802,100 Total liabilities, redeemable convertible preferred stock, and stockholders’ equity............................ $ 14,873,000 $ 17,325,900 See Notes to Consolidated Financial Statements. 7 |

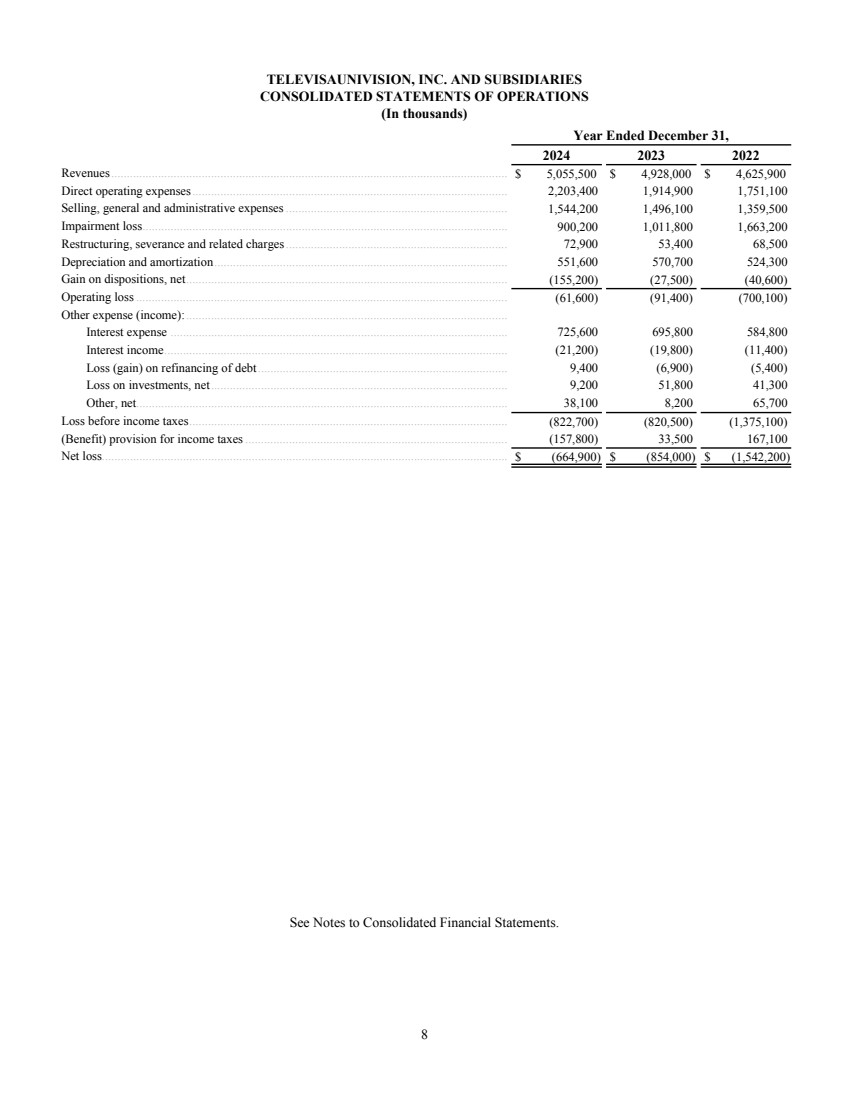

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF OPERATIONS (In thousands) Year Ended December 31, 2024 2023 2022 Revenues............................................................................................................................... $ 5,055,500 $ 4,928,000 $ 4,625,900 Direct operating expenses..................................................................................................... 2,203,400 1,914,900 1,751,100 Selling, general and administrative expenses....................................................................... 1,544,200 1,496,100 1,359,500 Impairment loss..................................................................................................................... 900,200 1,011,800 1,663,200 Restructuring, severance and related charges....................................................................... 72,900 53,400 68,500 Depreciation and amortization.............................................................................................. 551,600 570,700 524,300 Gain on dispositions, net....................................................................................................... (155,200) (27,500) (40,600) Operating loss....................................................................................................................... (61,600) (91,400) (700,100) Other expense (income):....................................................................................................... Interest expense ............................................................................................................ 725,600 695,800 584,800 Interest income.............................................................................................................. (21,200) (19,800) (11,400) Loss (gain) on refinancing of debt................................................................................ 9,400 (6,900) (5,400) Loss on investments, net............................................................................................... 9,200 51,800 41,300 Other, net....................................................................................................................... 38,100 8,200 65,700 Loss before income taxes...................................................................................................... (822,700) (820,500) (1,375,100) (Benefit) provision for income taxes.................................................................................... (157,800) 33,500 167,100 Net loss.................................................................................................................................. $ (664,900) $ (854,000) $ (1,542,200) See Notes to Consolidated Financial Statements. 8 |

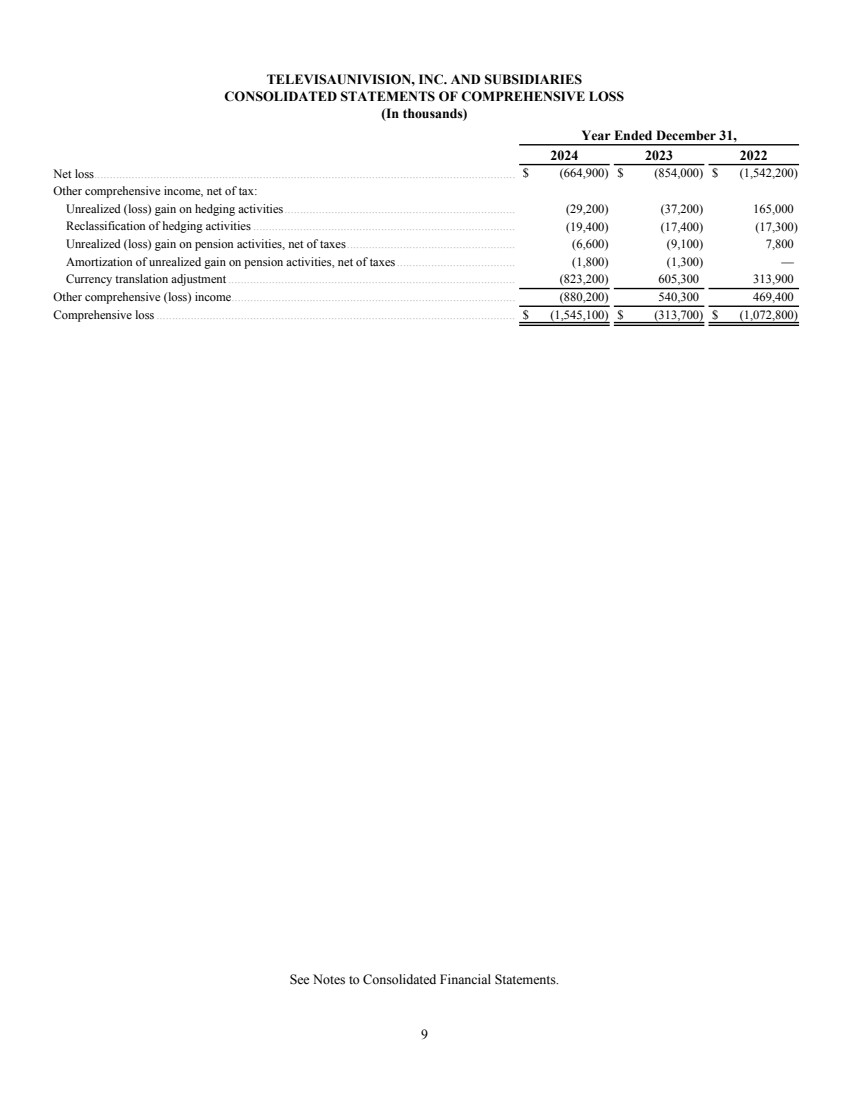

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS (In thousands) Year Ended December 31, 2024 2023 2022 Net loss....................................................................................................................................... $ (664,900) $ (854,000) $ (1,542,200) Other comprehensive income, net of tax: Unrealized (loss) gain on hedging activities.......................................................................... (29,200) (37,200) 165,000 Reclassification of hedging activities.................................................................................... (19,400) (17,400) (17,300) Unrealized (loss) gain on pension activities, net of taxes...................................................... (6,600) (9,100) 7,800 Amortization of unrealized gain on pension activities, net of taxes...................................... (1,800) (1,300) — Currency translation adjustment ............................................................................................ (823,200) 605,300 313,900 Other comprehensive (loss) income........................................................................................... (880,200) 540,300 469,400 Comprehensive loss................................................................................................................... $ (1,545,100) $ (313,700) $ (1,072,800) See Notes to Consolidated Financial Statements. 9 |

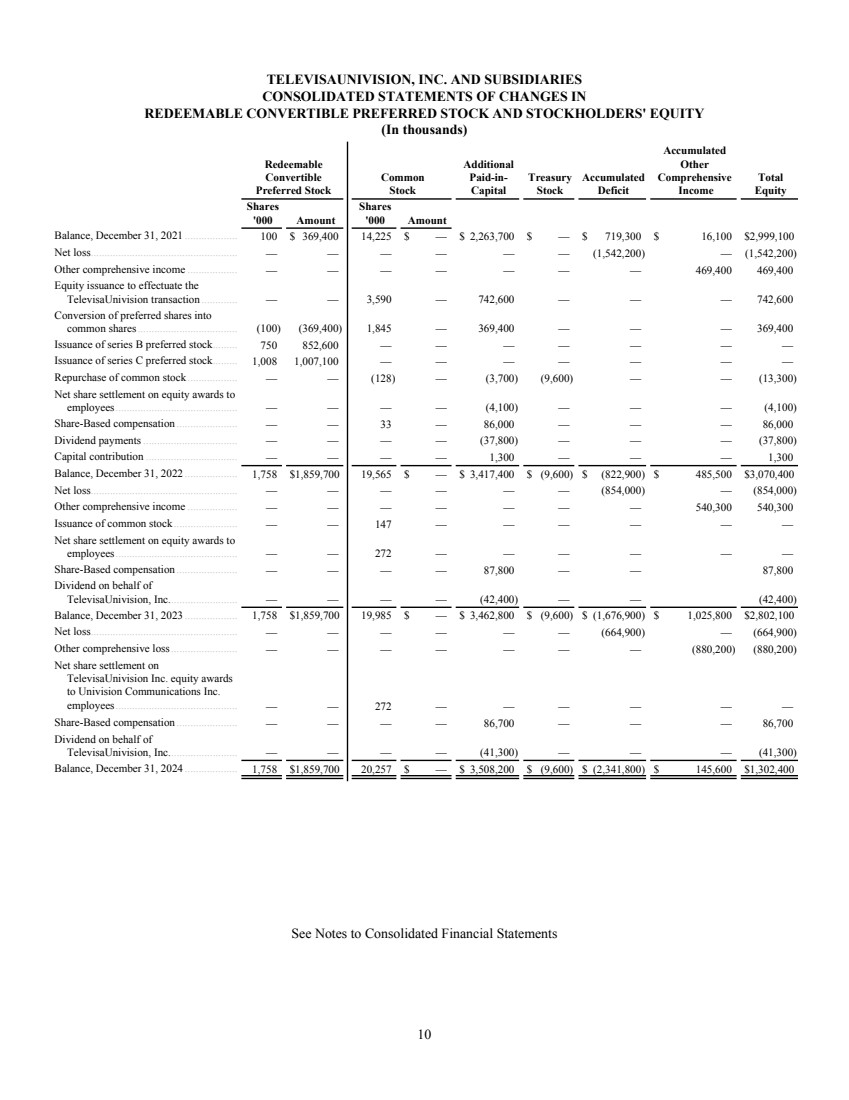

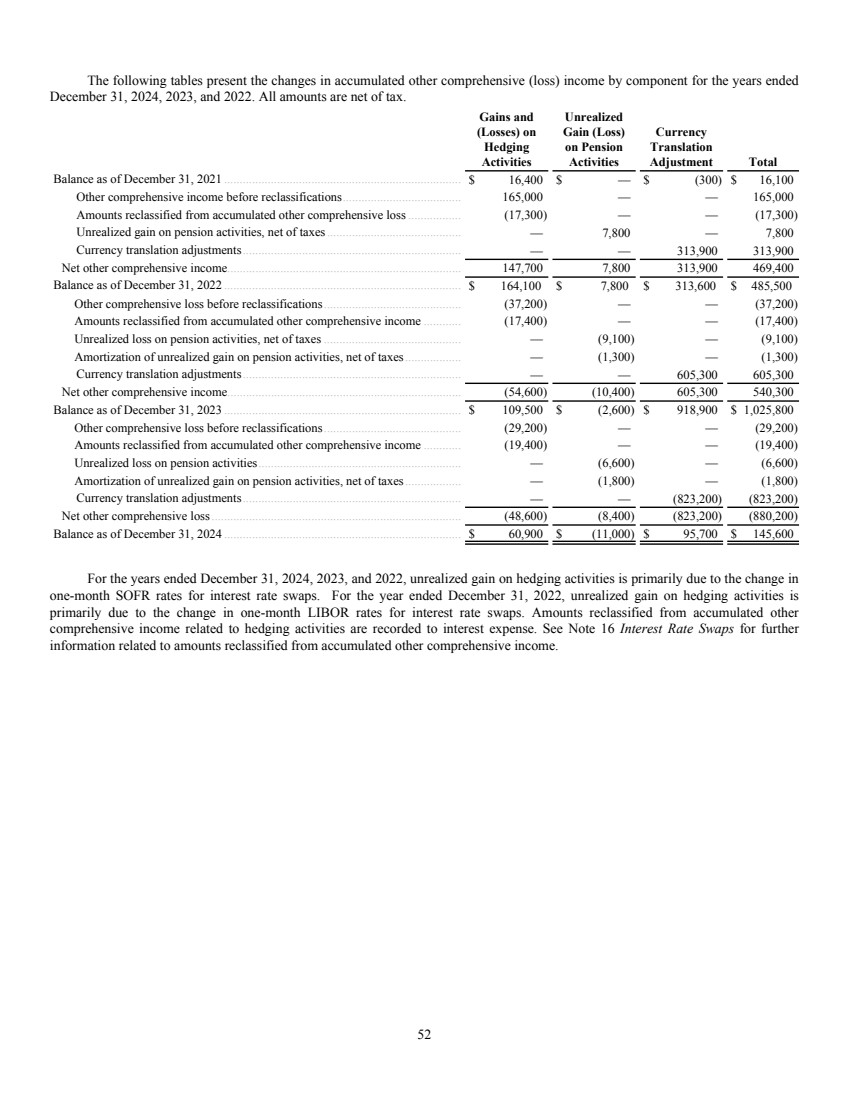

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CHANGES IN REDEEMABLE CONVERTIBLE PREFERRED STOCK AND STOCKHOLDERS' EQUITY (In thousands) Redeemable Convertible Preferred Stock Common Stock Additional Paid-in-Capital Treasury Stock Accumulated Deficit Accumulated Other Comprehensive Income Total Equity Shares '000 Amount Shares '000 Amount Balance, December 31, 2021 ................... 100 $ 369,400 14,225 $ — $ 2,263,700 $ — $ 719,300 $ 16,100 $ 2,999,100 Net loss..................................................... — — — — — — (1,542,200) — (1,542,200) Other comprehensive income .................. — — — — — — — 469,400 469,400 Equity issuance to effectuate the TelevisaUnivision transaction ............. — — 3,590 — 742,600 — — — 742,600 Conversion of preferred shares into common shares.................................... (100) (369,400) 1,845 — 369,400 — — — 369,400 Issuance of series B preferred stock......... 750 852,600 — — — — — — — Issuance of series C preferred stock......... 1,008 1,007,100 — — — — — — — Repurchase of common stock .................. — — (128) — (3,700) (9,600) — — (13,300) Net share settlement on equity awards to employees............................................ — — — — (4,100) — — — (4,100) Share-Based compensation ...................... — — 33 — 86,000 — — — 86,000 Dividend payments.................................. — — — — (37,800) — — — (37,800) Capital contribution ................................. — — — — 1,300 — — — 1,300 Balance, December 31, 2022 ................... 1,758 $ 1,859,700 19,565 $ — $ 3,417,400 $ (9,600) $ (822,900) $ 485,500 $ 3,070,400 Net loss..................................................... — — — — — — (854,000) — (854,000) Other comprehensive income .................. — — — — — — — 540,300 540,300 Issuance of common stock....................... — — 147 — — — — — — Net share settlement on equity awards to employees............................................ — — 272 — — — — — — Share-Based compensation ...................... — — — — 87,800 — — 87,800 Dividend on behalf of TelevisaUnivision, Inc......................... — — — — (42,400) — — (42,400) Balance, December 31, 2023 ................... 1,758 $ 1,859,700 19,985 $ — $ 3,462,800 $ (9,600) $ (1,676,900) $ 1,025,800 $ 2,802,100 Net loss..................................................... — — — — — — (664,900) — (664,900) Other comprehensive loss........................ — — — — — — — (880,200) (880,200) Net share settlement on TelevisaUnivision Inc. equity awards to Univision Communications Inc. employees............................................ — — 272 — — — — — — Share-Based compensation ...................... — — — — 86,700 — — — 86,700 Dividend on behalf of TelevisaUnivision, Inc......................... — — — — (41,300) — — — (41,300) Balance, December 31, 2024 ................... 1,758 $ 1,859,700 20,257 $ — $ 3,508,200 $ (9,600) $ (2,341,800) $ 145,600 $ 1,302,400 See Notes to Consolidated Financial Statements 10 |

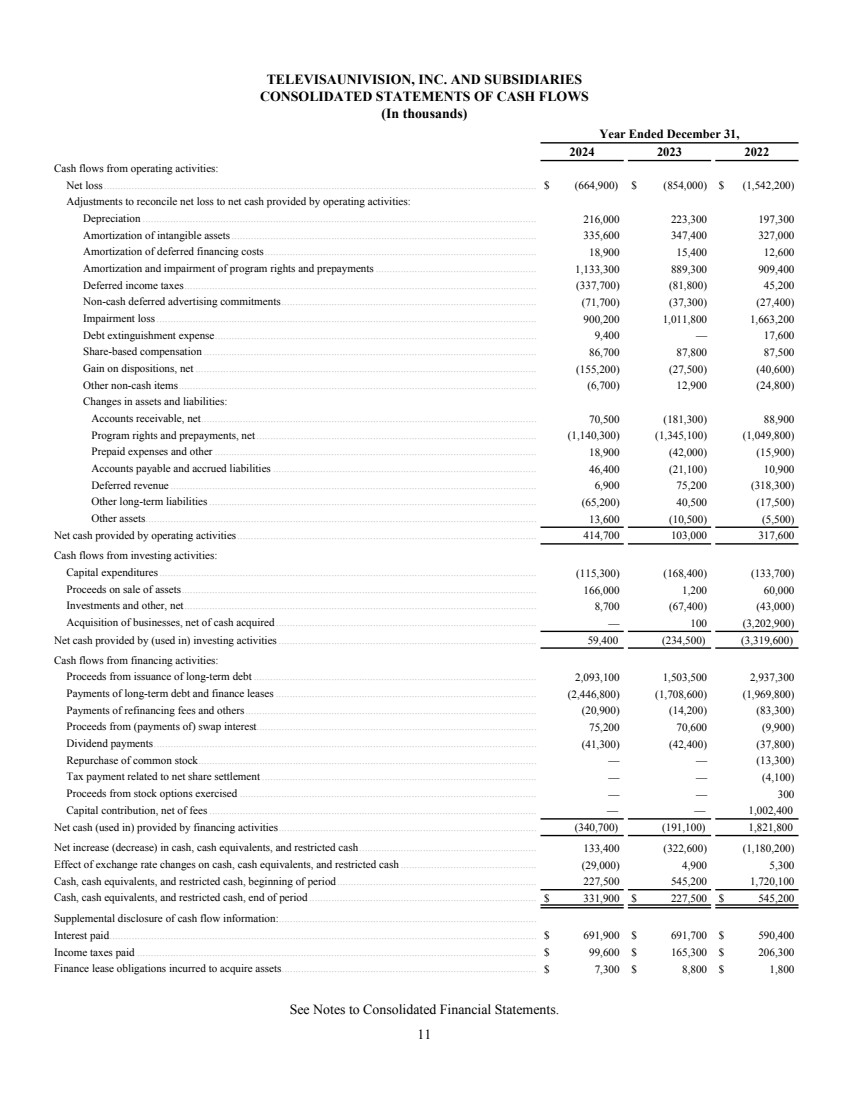

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS (In thousands) Year Ended December 31, 2024 2023 2022 Cash flows from operating activities: Net loss............................................................................................................................................................ $ (664,900) $ (854,000) $ (1,542,200) Adjustments to reconcile net loss to net cash provided by operating activities: Depreciation .............................................................................................................................................. 216,000 223,300 197,300 Amortization of intangible assets.............................................................................................................. 335,600 347,400 327,000 Amortization of deferred financing costs.................................................................................................. 18,900 15,400 12,600 Amortization and impairment of program rights and prepayments.......................................................... 1,133,300 889,300 909,400 Deferred income taxes............................................................................................................................... (337,700) (81,800) 45,200 Non-cash deferred advertising commitments............................................................................................ (71,700) (37,300) (27,400) Impairment loss......................................................................................................................................... 900,200 1,011,800 1,663,200 Debt extinguishment expense.................................................................................................................... 9,400 — 17,600 Share-based compensation ........................................................................................................................ 86,700 87,800 87,500 Gain on dispositions, net ........................................................................................................................... (155,200) (27,500) (40,600) Other non-cash items................................................................................................................................. (6,700) 12,900 (24,800) Changes in assets and liabilities: Accounts receivable, net......................................................................................................................... 70,500 (181,300) 88,900 Program rights and prepayments, net..................................................................................................... (1,140,300) (1,345,100) (1,049,800) Prepaid expenses and other .................................................................................................................... 18,900 (42,000) (15,900) Accounts payable and accrued liabilities............................................................................................... 46,400 (21,100) 10,900 Deferred revenue .................................................................................................................................... 6,900 75,200 (318,300) Other long-term liabilities...................................................................................................................... (65,200) 40,500 (17,500) Other assets............................................................................................................................................. 13,600 (10,500) (5,500) Net cash provided by operating activities............................................................................................................ 414,700 103,000 317,600 Cash flows from investing activities: Capital expenditures........................................................................................................................................ (115,300) (168,400) (133,700) Proceeds on sale of assets................................................................................................................................ 166,000 1,200 60,000 Investments and other, net............................................................................................................................... 8,700 (67,400) (43,000) Acquisition of businesses, net of cash acquired.............................................................................................. — 100 (3,202,900) Net cash provided by (used in) investing activities............................................................................................. 59,400 (234,500) (3,319,600) Cash flows from financing activities: Proceeds from issuance of long-term debt ...................................................................................................... 2,093,100 1,503,500 2,937,300 Payments of long-term debt and finance leases.............................................................................................. (2,446,800) (1,708,600) (1,969,800) Payments of refinancing fees and others......................................................................................................... (20,900) (14,200) (83,300) Proceeds from (payments of) swap interest..................................................................................................... 75,200 70,600 (9,900) Dividend payments.......................................................................................................................................... (41,300) (42,400) (37,800) Repurchase of common stock.......................................................................................................................... — — (13,300) Tax payment related to net share settlement ................................................................................................... — — (4,100) Proceeds from stock options exercised ........................................................................................................... — — 300 Capital contribution, net of fees...................................................................................................................... — — 1,002,400 Net cash (used in) provided by financing activities............................................................................................. (340,700) (191,100) 1,821,800 Net increase (decrease) in cash, cash equivalents, and restricted cash................................................................ 133,400 (322,600) (1,180,200) Effect of exchange rate changes on cash, cash equivalents, and restricted cash ................................................. (29,000) 4,900 5,300 Cash, cash equivalents, and restricted cash, beginning of period........................................................................ 227,500 545,200 1,720,100 Cash, cash equivalents, and restricted cash, end of period .................................................................................. $ 331,900 $ 227,500 $ 545,200 Supplemental disclosure of cash flow information:............................................................................................. Interest paid.......................................................................................................................................................... $ 691,900 $ 691,700 $ 590,400 Income taxes paid ................................................................................................................................................ $ 99,600 $ 165,300 $ 206,300 Finance lease obligations incurred to acquire assets............................................................................................ $ 7,300 $ 8,800 $ 1,800 See Notes to Consolidated Financial Statements. 11 |

| TELEVISAUNIVISION, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS December 31, 2024 (Dollars in thousands, except share and per-share data, unless otherwise indicated) 1. Company Background Nature of operations—TelevisaUnivision, Inc. (“TelevisaUnivision” or "the Company"), (formerly known as Univision Holdings II, Inc. (“UH Holdco”) or Searchlight III UTD L.P. (“Searchlight”)) is a holding company and the ultimate parent of Univision Communications Inc. Searchlight was originally formed on February 19, 2020 and held a 26.04% equity investment in Univision Holdings, Inc. (“UHI”). UH Holdco became the owner of 100% of the issued and outstanding capital stock of UHI on May 18, 2021. UHI owns Broadcast Media Partners Holdings, Inc. (“Broadcast Holdings”) which owns Univision Communications Inc. (together with its subsidiaries, collectively referred to herein as “UCI”), has operations in linear/digital (formerly Media Networks) and radio. UH Holdco was renamed TelevisaUnivision upon the completion of the TelevisaUnivision Transaction (see “TelevisaUnivision Transaction” below). TelevisaUnivision together with its subsidiaries, are collectively referred to herein as the “Company”, except where the context indicates otherwise. TelevisaUnivsion features the largest Spanish-language library of owned content and industry-leading production capabilities that power its streaming, digital and linear television offerings, as well as its radio platforms. The Company’s linear networks include the top-rated broadcast networks Univision and UniMás in the United States (“U.S.”) and Las Estrellas, Foro TV, Canal 5 and Canal 9 in Mexico. TelevisaUnivision is home to 38 Spanish- language cable networks, including Galavisión and TUDN, the No. 1 Spanish-language sports network in the U.S. and Mexico. With the most compelling portfolio of Spanish-language sports rights in the world, the Company has solidified itself as the home of soccer. The Company also owns and manages 59 local television stations across the U.S., and 16 local television stations in Mexico and Videocine studio. The Company is home to premium streaming services ViX, which host over 50,000 hours of high-quality, original Spanish-language programming from distinguished producers and top talent. The Company’s prominent digital assets include Univision.com, Univision NOW, and several top-rated digital apps. The Radio operations, known as the Uforia Audio Network, the Home of Latin Music, which encompasses 35 owned or operated U.S. radio stations, a live event series and a robust digital audio footprint. Additionally, the Company incurs corporate expenses separate from the linear/digital and radio operations which include general corporate overhead and unallocated, shared company expenses related to human resources, finance, legal and executive services which are centrally managed and support the Company’s operating and financing activities. TelevisaUnivision Transaction—On January 31, 2022 Grupo Televisa, S.A.B (“Televisa”; NYSE:TV; BMV:TLEVISA CPO) and UH Holdco (together with its wholly owned subsidiary, UCI) announced the completion of the transaction between Televisa’s media content and production assets and UCI (the “TelevisaUnivision Transaction”). The combined new company, which was named TelevisaUnivision, Inc., created the world’s leading Spanish-language media and content company. TelevisaUnivision produces and delivers premium content for its own platforms and for others, while also providing innovative solutions for advertisers and distributors globally. As a result of the TelevisaUnivision Transaction, TelevisaUnivision reaches nearly 60% of the respective TV audiences in both the U.S. and Mexico. Across television, digital, streaming, and audio, the Company reaches over 100 million Spanish speakers every day, holding leading positions in both markets. Radio Stations Sale - On June 3, 2022, UCI entered into an agreement to sell 18 non-strategic radio stations. On December 30, 2022, UCI completed the sale of 17 non-strategic radio stations. The Company recorded a gain of $28.3 million in “Other, net” within the consolidated statements of operations for the year ended December 31, 2022. Disposition of non-core broadcast tower assets - On September 6, 2024, UCI sold a portion of its non-core broadcast tower portfolio for $166.0 million, and simultaneously entered into an operating lease for the respective broadcast tower assets needed to operate UCI's linear network business (the “Tower Assets Sale”). The disposed non-core broadcast tower assets had a carrying amount of $1.3 million. The Company recorded a gain on disposition related to the Tower Assets Sale of $160.4 million in the consolidated statement of operations. The Company used proceeds from the Tower Assets Sale to make a $150.0 million partial repayment of the 2026 term loans on September 16, 2024. 2. Summary of Significant Accounting Policies Basis of presentation—The accompanying consolidated financial statements have been prepared in accordance with generally accepted accounting principles (“GAAP”) in the United States. 12 |

| Application of Pushdown Accounting—Pushdown accounting means implementing a new basis of accounting for the assets and liabilities based on stepped-up basis to the acquired company in connection with a change-in-control event. UCI implemented pushdown accounting as a result of the change-in-control event that occurred in connection with the May 18, 2021 reorganization when the Company executed a series of transactions that gave UH Holdco 100% ownership and a controlling financial interest in UHI (the “Reorganization”), which was accounted for under the scope of ASC 805, in which UH Holdco was deemed to be the accounting acquirer. The Company’s decision to apply pushdown accounting related to this change-in -control event is irrevocable. Principles of consolidation—The consolidated financial statements include the accounts and operations of the Company and its majority owned and controlled subsidiaries. All intercompany accounts and transactions have been eliminated. Non-controlling interests have been recognized where a controlling interest exists, but the Company owns less than 100% of the controlled entity. Non-controlling interest is recorded for the portion of an investment’s equity which is not controlled by the Company. The Company has consolidated the special purpose entities associated with its accounts receivable facility (see Note 15 Debt). This determination was based on the fact that these special purpose entities lack sufficient equity to finance their activities without additional support from the Company and, additionally, that the Company retains the risks and rewards of their activities. The consolidation of these special purpose entities does not have a significant impact on the Company’s consolidated financial statements. The Company accounts for investments over which it has significant influence but not a controlling financial interest using the equity method of accounting. Under the equity method of accounting, the Company’s share of the earnings and losses of these companies is included in “Other, net” in the accompanying consolidated statements of operations of the Company. For equity investments which are not accounted for under the equity method, the Company measures these investments at fair value, with changes in fair value recognized in earnings. The Company holds equity positions in several small early-stage entities which may not have readily determinable fair values. For such securities, the Company utilizes the measurement alternative to carry these investments at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for identical or similar investments of the same issuer. A security will be considered identical or similar if it has identical or similar rights to the equity securities held by the Company. The Company reviews its investments in equity securities without readily determinable fair values for impairment each reporting period when there are qualitative factors or events that indicate possible impairment. Factors the Company considers in making this determination include negative changes in industry and market conditions, financial performance, business prospects, and other relevant events and factors. When indicators of impairment exist, the Company prepares quantitative assessments of the fair value of its investments in equity securities, which require judgment and the use of estimates. When the Company’s assessment indicates that the fair value of the investment is below its carrying amount, the Company writes down the investment to its fair value and records the corresponding charge in “Other, net”, within the Company’s consolidated statements of operations. Use of estimates—The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses, including impairments, during the reporting period. Actual results could differ from those estimates. Significant items subject to such estimates and assumptions include: estimated credit losses, business combinations, shared-based compensation, the valuation of derivatives, pension and post-retirement benefits, lease assets and liabilities, investments, property, plant and equipment, definite lived intangibles, the recoverability of goodwill and indefinite-lived intangible assets; amortization of program rights and prepayments; the fair value of equity securities without readily determinable fair values; and reserves for income tax uncertainties and other contingencies. Reclassifications— Certain reclassifications have been made to the prior years' financial information to conform to the current year presentation. Foreign Currency—The reporting currency of the Company is the U.S. dollar. The functional currency of most of the Company’s international subsidiaries is the local currency. Financial statements of subsidiaries whose functional currency is not the U.S. dollar are translated at exchange rates in effect at the balance sheet date for assets and liabilities and at average exchange rates for revenues and expenses for the respective periods. Translation adjustments are recorded in accumulated other comprehensive income (loss). Foreign currency transaction gains and losses resulting from the conversion of the transaction currency to functional currency are included in “Other, net”. For the years ended December 31, 2024, 2023, and 2022, the Company recorded total foreign currency transaction loss of $11.7 million, $2.6 million, and $13.6 million within “Other, net” within the Company’s consolidated statement of operations, respectively. Cash equivalents—The Company considers all highly liquid investments with a maturity of three months or less when purchased to be cash equivalents. 13 |

| Fair value measurements—The Company utilizes valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs to the extent possible. The Company determines fair value based on assumptions that market participants would use in pricing an asset or liability in the principal or most advantageous market. When considering market participant assumptions in fair value measurements, the following fair value hierarchy distinguishes between observable and unobservable inputs, which are categorized in one of the following levels: • Level 1 Inputs: Unadjusted quoted prices in active markets for identical assets or liabilities accessible to the reporting entity at the measurement date. • Level 2 Inputs: Other than quoted prices included in Level 1, inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the asset or liability. • Level 3 Inputs: Unobservable inputs for the asset or liability used to measure fair value to the extent that observable inputs are not available, thereby allowing for situations in which there is little, if any, market activity for the asset or liability at measurement date. Revenue—Revenue is recognized upon transfer of control of promised services or goods to customers in an amount that reflects the consideration that the Company expects to receive in exchange for those services or goods. Revenues do not include taxes collected from customers on behalf of taxing authorities such as sales tax and value-added tax. Advertising—The Company generates advertising revenue from the sale of commercial time on broadcast and cable networks, local television and radio stations. The Company also generates revenue from the sale of display, mobile and video advertising, as well as sponsorships, on our various digital properties. In some cases, the network advertising sales are subject to ratings guarantees that require the Company to provide additional advertising time if the guaranteed audience levels are not achieved. Revenues for any audience deficiencies are deferred until the guaranteed audience levels are achieved through the Company' provision of additional advertising time. Advertising contracts, which are generally short-term, are billed monthly, with payments due shortly after the invoice date. Advertising revenue from the sale of advertising on broadcast and cable networks, local television and radio stations is recognized when advertising spots are aired and performance guarantees, if any, are achieved. The achievement of performance guarantees related to U.S. broadcasting operations are based on audience ratings from an independent research company. If there is a guarantee to deliver a targeted audience rating, revenues are recognized based on the proportion of the audience rating delivered compared to the total guaranteed in the contract. For impression-based digital advertising, revenue is recognized when “impressions” are delivered, while revenue from non-impression-based digital advertising (primarily sponsorship) is recognized over the period that the advertisement is run. “Impressions” are defined as the number of times that an advertisement appears in pages viewed by users of the Company’s digital properties. Sponsorship advertisement revenue is recognized ratably over the contract period. Subscription and licensing revenue consist of subscriber fees and program licensing: Subscriber Fees—are charged for the right to view the programming content of the Company’s broadcast networks, cable networks and stations through a variety of distribution platforms and viewing devices. Subscriber fee revenue is principally comprised of fees received from multichannel video programming distributors (“MVPDs”) and third-party live streaming services (“virtual MVPD’s”) for authorizing carriage of the Company’s networks and for retransmission consent of Univision and UniMás broadcast networks aired on the Company’s owned television stations as well as fees for digital content. Typically, the Company’s networks and stations are aired by MVPDs and virtual MVPDs pursuant to multi-year carriage agreements that provide for the level of carriage that the Company’s networks and stations will receive, and if applicable, for annual rate increases. Subscriber fee revenue is largely dependent on market demand for the content that the Company provides, the contractual rate-per-subscriber negotiated in the agreements, and the number of subscribers that receive the Company’s networks or content. Subscriber fees received from cable and satellite MVPDs are recognized as revenue in the period during which services are provided. Additionally, the Company’s subscriber fee revenue includes monthly fees related to access to our Subscription Video on Demand (“SVOD”) global streaming platform. Subscribers are billed on a monthly basis in advance of obtaining access to the platform. Subscription fees related to the SVOD service are recognized ratably over the term of the subscription. The Company also receives retransmission consent fees related to television stations that the Company does not own (referred to as “affiliates”) that are affiliated with Univision and UniMás broadcast networks. The Company has agreements with its affiliates whereby the Company negotiates the terms of retransmission consent agreements for substantially all of its Univision and UniMás stations with MVPDs. As part of these arrangements, the Company shares the retransmission consent fees received with certain of its affiliates and records revenue on a net basis. 14 |

| Program Licensing—The Company licenses programming content for digital streaming and to other cable and satellite providers. Program licensing revenue is recognized when the content is delivered, and all related obligations have been satisfied. For licenses of internally-produced television programming, each individual episode delivered represents a separate performance obligation and revenue is recognized when the episode is made available to the licensee for exhibition and the license period has begun. All revenue is recognized only when it is probable that the Company will collect substantially all of the consideration for the program licensing. Other Revenue—The Company classifies revenue from contractual commitments (including non-cash advertising and promotional revenue) primarily related to Televisa as “Other Revenue”. The Company also recognizes other revenue related to support services provided to joint ventures and related to spectrum access in channel sharing arrangements. From time to time the Company enters into transactions involving its spectrum. Program rights and prepayments—The Company produces and acquires program rights to exhibit programming on its broadcast and cable networks and one digital streaming platform. Program rights principally consist of television series, specials, movies, and sporting events. Program rights aired on the Company’s broadcast and cable networks and digital streaming platforms is sourced from a wide range of third-party producers, wholly-owned production studios, and sports associations. Costs for internally-produced and acquired programming rights, including prepayments for such costs, are recorded within the non-current portion of “Program rights and prepayments, net” on the consolidated balance sheet, with the exception of content acquired with an initial license period of 12 months or less and prepaid sports rights expected to air within 12 months. The Company capitalizes costs for produced program rights, including direct production costs, development costs, and production overhead, of original programs when incurred. For licensed program rights, the costs incurred to acquire programming are capitalized as a program right and prepayment and a corresponding liability payable to the licensor are recorded when (i) the cost of the programming is reasonably determined; (ii) the programming has been accepted in accordance with the terms of the agreement; (iii) the programming is available for its first showing or telecast and (iv) the license period has commenced. Programming rights and prepayments includes advance payments for rights to air sporting events that will take place in the future. For purposes of amortization and impairment, the capitalized content costs are classified based on their predominant monetization strategy. Programs rights are either monetized individually or as part of a film group. The substantial majority of our program rights and prepayments are predominantly monetized as a film group on our broadcast and cable networks and/or digital streaming platform. For programming rights that are predominantly monetized as part of our broadcast and cable networks film group, which includes licensed content and internally-produced television programs, capitalized costs are amortized based on an estimate of the timing of our usage of and benefit from such programming, generally resulting in an accelerated or straight-line amortization pattern. Programming rights that are predominantly monetized as part of our digital streaming platform are generally amortized on a straight-line basis over an initial estimated economic life of six (6) years or the lesser of a license period, if applicable. The Company has limited historical usage pattern or viewership information on its digital platform as it continues to scale subscribers and the current estimated economic life reflects an initial ramp-up period of the digital streaming service. As we obtain more historical information, our estimate used to amortize our programming rights monetized on our digital streaming platform will be adjusted as necessary. Adjustments to projected usage are applied prospectively in the period of the change. Such changes in the future could be material. Programming costs that are predominantly monetized on an individual basis are amortized utilizing an individual-film-forecast-computation method over the title’s life cycle based upon the ratio of current period revenue to estimated remaining total expected revenue. Licensed content for multi-year sports programming arrangements are generally amortized over the license period based on the ratio of current-period direct revenue to estimated remaining total direct revenue over the remaining contract period. Licensed content costs for entertainment programming are generally amortized over the shorter of the estimated period of benefit or licensed period. Amortization expense of program rights and prepayments is included in “Direct Operating Expense,” in the Company’s consolidated statement of operations. All program rights and prepayments on the Company’s balance sheet are subject to regular recoverability assessments. The Company has a three-year development cycle which begins with the initial capitalization of the development costs. Film development costs that have not been set for production are expensed within three years unless they are abandoned earlier, in which case these projects are written down to their estimated fair value in the period the decision to abandon the project is determined. The Company’s predominant monetization strategy determines how the impairment testing is performed for program rights and prepayments whenever events or changes in circumstances indicate that the carrying amount of content monetized on its own or as a film group may exceed its estimated fair value. In addition, a change in the predominant monetization strategy is considered a triggering event for impairment testing before a title is accounted for as part of a film group. If the carrying amount of an individual 15 |

| monetized content or film group, exceeds the estimated fair value, an impairment charge will be recorded in the amount of the difference. For content that is predominately monetized individually, we utilize estimates including ultimate revenues and additional costs to be incurred (including exploitation and participation costs), in order to determine whether the carrying amount of the program rights is impaired. In the event the Company decides not to air a program or substantively abandon content due to lower viewership, an impairment loss reducing the corresponding asset to zero is recorded to reflect the programming asset abandonment. Accounting for goodwill, other intangibles and long-lived assets—Goodwill and other intangible assets with indefinite lives are tested annually for impairment on October 1 or more frequently if circumstances indicate a possible impairment exists. The Company first assesses the qualitative factors for reporting units that carry goodwill. A reporting unit is defined as an operating segment or one level below an operating segment. In performing a qualitative assessment, the Company considers relevant events and circumstances that could affect the reporting unit fair value. These circumstances may include macroeconomic conditions, industry and market considerations, cost factors, overall financial performance, and entity-specific events, business plans, and strategy. The Company considers the totality of these events, in the context of the reporting unit, and determines if it is more likely than not that the fair value of the reporting unit is less than its carrying amount. If the qualitative assessment results in a conclusion that it is more likely than not that the fair value of a reporting unit exceeds the carrying amount, then no further testing is performed for that reporting unit. When a qualitative assessment is not used, or if the qualitative assessment is not conclusive and it is necessary to calculate fair value of a reporting unit, then the impairment analysis for goodwill is performed at the reporting unit level. The quantitative impairment test is used to identify potential impairment by comparing the fair value of a reporting unit with its carrying amount, including goodwill. If the carrying value exceeds the fair value, an impairment charge is recognized equal to the difference between the carrying value of the reporting unit and its fair value, considering the related income tax effect of any goodwill deductible for tax purpose. In performing the quantitative assessment, we measure the fair value of the reporting unit using a combination of the income and market approaches. The assessment requires us to make judgments and involves the use of significant estimates and assumptions. Under the income approach, the Company calculates the present value of the reporting unit’s estimated future cash flows (discounted cash flow analysis). Significant estimates and assumptions include the amount and timing of expected future cash flow, risk-adjusted discount rates based on a weighted-average cost of capital (“WACC”) adjusted for the relevant risk associated with business-specific characteristics and the uncertainty related to the reporting unit’s ability to execute on its projected cash flows. The expected cash flows used in the income approach are based on the Company’s most recent forecast and budget and, for years beyond the budget, the Company’s estimates, which are based, in part, on forecasted growth rates. Assumptions used in the estimate of future cash flows, including the WACC, are assessed based on the reporting units’ current results and forecasted future performance, as well as macroeconomic and industry specific factors. Determining fair value using a market approach considers multiples of financial metrics based on both acquisitions and trading multiples of a selected peer group of companies. From the comparable companies, a representative market multiple is determined which is applied to financial metrics to estimate the fair value of a reporting unit. The Company also has indefinite-lived intangible assets, such as television and radio broadcast licenses and tradenames. The Company’s United States television and radio broadcast licenses have indefinite lives because the Company expects to renew them and renewals are routinely granted with little cost, provided that the licensee has complied with the applicable rules and regulations of the Federal Communications Commission (“FCC”). Historically, all material television and radio licenses that have been up for renewal have been renewed. Indefinite-lived intangible assets are tested for impairment annually or more frequently if circumstances indicate a possible impairment exists. The fair value of the television and radio broadcast licenses is determined using the direct valuation method or greenfield method which is classified as a Level 3 measurement. The Company's broadcast license impairment testing, significant unobservable inputs utilized included discount rates and terminal growth rates. Under the direct valuation method, the fair value of the television and radio broadcast licenses is calculated at the network or market level as applicable. The application of the direct valuation method attempts to isolate the income that is properly attributable to the television and radio broadcast licenses alone (that is, apart from tangible and identified intangible assets). It is based upon modeling a hypothetical “greenfield” build-up to a “normalized” enterprise that, by design, lacks inherent goodwill and whose only other assets have essentially been paid for (or added) as part of the build-up process. Under the direct valuation method, it is assumed that rather than acquiring television and radio broadcast licenses as part of a going concern business, the buyer hypothetically develops television and radio broadcast licenses and builds a new operation with similar attributes from inception. Thus, the buyer incurs start-up costs during the build-up phase. Initial capital costs are deducted from 16 |

| the discounted cash flow model which results in a value that is directly attributable to the indefinite-lived intangible assets. The key assumptions used in the direct valuation method are market revenue growth rates, market share, profit margin, duration and profile of the build-up period, estimated start-up capital costs and losses incurred during the build-up period, the risk-adjusted discount rate and terminal values. The market revenue growth rate assumption is impacted by, among other things, factors affecting the local advertising market for local television and radio stations. This data is populated using industry normalized information representing an average FCC license within a market. Univision Network and UniMás network programming is broadcast on the television stations. FCC broadcast licenses for television stations that are not dependent on network programming are tested for impairment at the local market level. Radio broadcast licenses are tested for impairment at the local market level. The Company has the option to first assess qualitative factors to determine whether it is more likely than not that an indefinite-lived intangible asset is impaired as a basis for determining whether it is necessary to perform the quantitative impairment test. If the qualitative assessment determines that it is more likely than not that the fair value of the intangible asset is more than its carrying amount, then the Company concludes that the intangible asset is not impaired. If the Company does not choose to perform the qualitative assessment, or if the qualitative assessment determines that it is more likely than not that the fair value of the indefinite-lived intangible asset is less than its carrying amount, then the Company calculates the fair value of the intangible asset and compares it to the corresponding carrying value. If the carrying amount of the indefinite-lived intangible asset exceeds its fair value, an impairment loss is recognized for the excess carrying value over the fair value. Long-lived assets, such as property and equipment, intangible assets with definite lives, channel-sharing arrangements and program right prepayments are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to its estimated undiscounted future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated undiscounted future cash flows, an impairment charge is recognized for the amount by which the carrying amount of the asset exceeds the fair value of the asset. Derivative instruments—The Company recognizes all derivative instruments as either assets or liabilities in the consolidated balance sheet at their respective fair values. Derivatives designated and qualifying as a hedge of the exposure to variability in expected future cash flows, or other types of forecasted transactions, are considered cash flow hedges. The Company may enter into derivative contracts that are intended to economically hedge certain of its risks, even though hedge accounting does not apply or the Company elects not to apply hedge accounting. For all hedging relationships, the Company formally documents the hedging relationship and its risk-management objective and strategy for undertaking the hedge, the hedging instrument, the hedged transaction, the nature of the risk being hedged, how the hedging instrument’s effectiveness in offsetting the hedged risk will be assessed prospectively and retrospectively, and a description of the method used to measure ineffectiveness. The Company also formally assesses, both at the inception of the hedging relationship and on an ongoing basis, whether the derivatives that are used in hedging relationships are highly effective in offsetting changes in cash flows of hedged transactions. For derivative instruments that are designated and qualify as part of a cash flow hedging relationship, the gain or loss on the derivative is reported as a component of other comprehensive (loss) income and reclassified into earnings in the same period or periods during which the hedged transaction affects earnings. For derivative instruments not designated as hedging instruments, the derivative is marked to market with the change in fair value recorded directly into interest expense. The Company classifies cash flows from its derivative transactions as cash flow from operating activities in the consolidated statement of cash flows. For derivative transactions that have an other-than-insignificant financing element, all cash flows are classified as cash flows from financing activities in the consolidated statement of cash flows. The Company discontinues hedge accounting prospectively when (i) it determines that the derivative is no longer effective in offsetting cash flows attributable to the hedged risk; (ii) the derivative expires or is sold, terminated, or exercised; (iii) the cash flow hedge is de-designated because a forecasted transaction is not probable of occurring; or (iv) management determines to remove the designation of the cash flow hedge. In all situations in which hedge accounting is discontinued and the derivative remains outstanding, the Company continues to carry the derivative at its fair value on the consolidated balance sheet and recognizes any subsequent changes in its fair value in earnings, and any associated balance in accumulated other comprehensive (loss) income will be reclassified into interest expense in the same periods during which the forecasted transactions that originally were being hedged affect earnings. When it is probable that a forecasted transaction will not occur, the Company discontinues hedge accounting and recognizes immediately in earnings gains and losses that were accumulated in other comprehensive (loss) income related to the hedging relationship. 17 |

| Treasury Stock — When stock is acquired for purposes other than formal or constructive retirement, the purchase price of the acquired stock is recorded in a separate treasury stock account, which is separately reported as a reduction of equity. Property and equipment, net —Property and equipment are carried at historical cost. Depreciation is calculated using the straight-line method over the estimated useful lives of the assets. The Company removes the cost and accumulated depreciation of its property and equipment upon the retirement or disposal of such assets and the resulting gain or loss, if any, is then recognized. Land improvements are depreciated up to 15 years, buildings and improvements are depreciated up to 50 years, broadcast equipment over 5 to 20 years and furniture, computer and other equipment over 3 to 7 years. Property and equipment financed with finance leases are amortized over the shorter of their useful life or the remaining life of the lease. Repairs and maintenance costs are expensed as incurred. Leases —The Company has long-term operating leases expiring on various dates for office, studio, automobile and tower rentals. the Company's operating leases, which are primarily related to buildings and tower properties, have various renewal terms and escalation clauses. The Company also has long-term finance lease obligations for facilities and transmission and technical equipment assets that are used to transmit and receive its network signals in the U.S. and Mexico. Our leases generally have remaining terms ranging from 3 to 45 years and often contain renewal options to extend the lease for periods ranging from 5 years to 25 years. For leases that contain renewal options, we include the renewal period in the lease term if it is reasonably certain that the option will be exercised. We evaluate whether our contractual arrangements contain leases at the inception of such arrangements. Specifically, we consider whether we can control the underlying asset and have the right to obtain substantially all of the economic benefits or outputs from the asset. Contracts containing a lease are further evaluated for classification as an operating or finance lease where the Company is a lessee. Our right-of-use operating lease assets represent our right to use an underlying asset for the lease term, and our operating lease liabilities represent our obligation to make lease payments. The underlying assets under finance leases are recorded as components of property and equipment and the corresponding finance lease liability is recorded as a component of long-term debt and finance lease obligations. Variable lease payments consist primarily of common area maintenance and service related costs, personnel costs, utilities and taxes, which are not included in the recognition of Right-of-Use ("ROU") assets and related lease liabilities. Our lease agreements do not contain any material residual value guarantees or material restrictive covenants. Both the operating lease right to use asset and liability are recognized as of the lease commencement date at the present value of the lease payments over the lease term. Most of our leases do not provide an implicit rate that can readily be determined. Therefore, we use a discount rate based on our incremental borrowing rate, which is determined using secured borrowings of companies with similar credit ratings and adjusted for the Company’s current issuing rates for senior secured debt. The Company combines the lease and non-lease components of lease payments in determining right-of-use assets and related lease liabilities. Lease expense is recognized on a straight-line basis over the term of the lease. As permitted by ASC 842, leases with an initial term of twelve months or less (“short-term leases”) are not recorded on the accompanying consolidated balance sheet. Lease cost for finance leases includes the amortization of the ROU asset included within property and equipment, which is amortized on a straight-line basis and recorded to Depreciation and amortization, and interest expense on the finance lease liability, which is calculated using the interest method and recorded to Interest expense. The Company also has operating subleases which have been accounted for by reference to the underlying asset subject to the lease rather than by reference to their associated right-of-use asset. Deferred financing costs—Deferred financing costs consist of payments made by the Company in connection with its debt offerings, primarily ratings fees, legal fees, accounting fees, private placement fees and costs related to the offering circular and other related expenses. Deferred financing costs are amortized over the life of the related debt using the effective interest method. Advertising and promotional costs—The Company expenses advertising and promotional costs in the period in which they are incurred. The Company recorded advertising and promotional costs of $405.9 million, $380.9 million and $306.1 million for years ended December 31, 2024, 2023, and 2022, respectively. Share-based compensation—Compensation expense relating to share-based payments is recognized in earnings using a fair-value measurement method. The Company uses the straight-line attribution method of recognizing compensation expense over the requisite service period which generally matches the stated vesting schedule. The Company’s stock options vest over periods of between three and five years from the date of grant. The Company’s restricted and performance stock unit awards vest over periods of between three and four years from the date of grant. The fair value of each new stock option award is estimated on the date of grant using the Black-Scholes-Merton option-pricing model. The Black-Scholes-Merton option-pricing model was developed for use in 18 |