Exhibit 99.2 ____

.

_

_

Forward-Looking Statements

These earnings supplemental materials contain forward-looking statements including, but not limited to, statements about management’s plans, goals, expectations, and guidance and assumptions with respect to future financial performance of the Company. Any statements in these supplemental materials that are not statements of historical facts are forward-looking statements. When used in these supplemental materials, the words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “project,” “will,” “positions,” “confidence,” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such words. Forward-looking statements relate to our future plans, objectives, expectations, and intentions and are not historical facts and accordingly involve known and unknown risks and uncertainties and other factors that may cause the actual results or performance to be materially different from future results or performance expressed or implied by these forward-looking statements. The following factors, among others, could cause actual results to differ materially from those contained in forward-looking statements made in these supplemental materials and in oral statements made by our authorized officers:

•the impact of fluctuations in the amount of fuel purchased and sold by our customers and retail partners, respectively, fuel price volatility, and the actual price of fuel, including fuel spreads in the Company’s international markets, and the resulting impact on the Company’s results, including margins, revenues, and net income;

•the effects of general economic conditions and the amount of business activity in the economies in which we operate, particularly in the U.S., Europe, and the United Kingdom, including, but not limited to, conditions resulting from an economic recession, the impact of tariffs or international trade wars, increasing unemployment, and declining consumer confidence, which may lead to, among other things, a decline or stagnation in demand for fuel, corporate payment services, travel related services, or employee benefits related products and services;

•the failure to comply with the applicable requirements of Mastercard or Visa contracts and rules;

•the extent to which unpredictable events in the locations in which the Company or the Company’s customers operate or elsewhere may adversely affect the Company’s employees, ability to conduct business, results of operations and financial condition;

•the impact and size of credit losses, including fraud losses, and other adverse effects if the Company fails to adequately assess and monitor credit risk or fraudulent use of our payment cards or systems;

•the impact of changes to the Company’s credit standards;

•limitations on, or compression of, interchange fees;

•the effect of adverse financial conditions affecting the banking system;

•the impact of increasing scrutiny with respect to our environmental, social and governance practices;

•failure to implement new technologies and products;

•the failure to realize or sustain the expected benefits from our cost and organizational operational efficiencies initiatives;

•the failure to compete effectively in order to maintain or renew key customer and partner agreements and relationships, or to maintain volumes under such agreements;

•the ability to attract and retain employees;

•the ability to execute the Company’s business expansion and acquisition efforts and realize the benefits of acquisitions we have completed;

•the failure to achieve commercial and financial benefits as a result of our strategic minority equity investments;

•the impact of foreign currency exchange rates on the Company’s operations, revenue and income and other risks associated with our operations outside the United States;

•the failure to adequately safeguard custodial HSA assets;

•the incurrence of impairment charges if the Company’s assessment of the fair value of certain of its reporting units changes;

•the uncertainties of investigations and litigation;

•the ability of the Company to protect its intellectual property and other proprietary rights;

•the impact of regulatory capital requirements and other regulatory requirements on the operations of WEX Bank or its ability to make payments to WEX Inc.;

•the impact of the Company’s debt instruments on the Company’s operations;

•the impact of increased leverage on the Company’s operations, results or borrowing capacity generally;

•changes in interest rates, including those which we must pay for our deposits, those which we earn on our investment securities, and the resultant potential impacts to our debt securities subject to early call provisions;

•the ability to refinance certain indebtedness or obtain additional financing;

•the actions of regulatory bodies, including tax, banking and securities regulators, or possible changes in tax, banking or financial regulations impacting the Company’s industrial bank, the Company as the corporate parent or other subsidiaries or affiliates;

•the failure to comply with the Treasury Regulations applicable to non-bank custodians;

•the impact from breaches of, or other issues with, the Company’s technology systems or those of its third-party service providers and any resulting negative impact on the Company’s reputation, liabilities or relationships with customers or merchants;

•the impact of regulatory developments with respect to privacy and data protection;

•the impact of any disruption to the technology and electronic communications networks we rely on;

•the ability to adopt, implement and use artificial intelligence technologies across our business successfully and ethically;

•the ability to maintain effective systems of internal controls;

•the failure to repurchase shares at favorable prices, if at all;

•the impact of provisions in our charter documents, Delaware law and applicable banking laws that may delay or prevent our acquisition by a third party; as well as

•other risks and uncertainties identified in Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2024, filed with the Securities and Exchange Commission on February 20, 2025 and subsequent filings with the Securities and Exchange Commission.

The forward-looking statements speak only as of the date of the initial filing of these earnings supplemental materials and undue reliance should not be placed on these statements. The Company disclaims any obligation to update any forward-looking statements as a result of new information, future events, or otherwise.

Non-GAAP Information:

For additional important information and disclosure regarding our use of non-GAAP metrics, specifically, adjusted net income, adjusted net income per diluted share, total segment adjusted operating income and margin, and adjusted free cash flow, please see our most recent earnings release issued on April 30, 2025. In addition, see the Appendix to this earnings supplement for an explanation and reconciliation of (i) GAAP operating income to non-GAAP total segment adjusted operating income and adjusted operating income, (ii) GAAP net income to non-GAAP adjusted net income, (iii) GAAP net income per diluted share to non-GAAP adjusted net income per diluted share, and (iv) GAAP operating cash flow to non-GAAP adjusted free cash flow.

Note:

The Company rounds amounts to millions within tables and text (unless otherwise specified), and calculates all percentages and per-share data from underlying whole-dollar amounts. As a result, certain amounts may not foot, crossfoot, or recalculate based on reported numbers due to rounding. Within the tables below, we present the impact of FX and PPG changes on various financial metrics. To determine the estimated earnings impact of FX on revenue and expenses from entities whose functional currency is not denominated in U.S. dollars, as well as revenue and variable expenses from purchase volume transacted in non-U.S. denominated currencies, amounts were translated using the weighted average exchange rates for the same period in the prior year, net of tax, exclusive of revenue and expenses derived from acquisitions for one year following the acquisition dates. To determine the estimated earnings impact of PPG, revenue and certain variable expenses impacted by changes in fuel prices were adjusted based on the average retail price of fuel for the same period in the prior year for the portion of our business that earns revenue based on a percentage of fuel spend, net of applicable taxes, exclusive of revenue and expenses derived from acquisitions for one year following the acquisition dates. For the portions of our business that earn revenue based on margin spreads, revenue was adjusted to the comparable margin from the prior year, net of non-controlling interests and applicable taxes.

Financial Results

•Total revenue for Q1 2025 decreased $16.1 million compared to Q1 2024 driven by a net $8.5 million unfavorable impact from fuel prices and spreads and a $2.5 million unfavorable impact from foreign exchange rates.

•Q1 2025 results were largely in line with guidance provided in February. Fuel prices trended slightly higher than anticipated, which increased revenue above the midpoint of the guidance range and adjusted EPS above the guidance range. When adjusted for fuel prices and FX noted above, the underlying revenue growth during the quarter was down 0.8% compared with the prior year while adjusted earnings per share grew 5.2% on the same basis.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | | For the three months ended | | | For the twelve months ended | |

| (in millions except per share amounts) | | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 | |

| Revenues | | $ | 612.0 | | $ | 621.4 | | $ | 651.4 | | $ | 663.3 | | $ | 652.7 | | $ | 673.5 | | $ | 665.5 | | $ | 636.5 | | $ | 636.6 | | | | $ | 2,548.0 | | $ | 2,628.1 | | |

| Y/Y Change | | 18.3 | % | 3.9 | % | 5.7 | % | 7.2 | % | 6.7 | % | 8.4 | % | 2.2 | % | (4.0) | % | (2.5) | % | | | 8.4 | % | 3.1 | % | |

| FX Impact vs Prior Year1 | | $ | 4.3 | | $ | (0.3) | | $ | (5.3) | | $ | (0.3) | | $ | (0.7) | | $ | 0.8 | | $ | (2.2) | | $ | 1.3 | | $ | 2.5 | | | | $ | (1.7) | | $ | (0.8) | | |

PPG Impact vs Prior Year1 | | $ | (1.3) | | $ | 53.0 | | $ | 31.9 | | $ | 24.9 | | $ | 20.5 | | $ | 5.4 | | $ | 21.2 | | $ | 26.6 | | $ | 8.5 | | | | $ | 108.4 | | $ | 73.8 | | |

| PPG and FX % Impact on Revenue vs Prior Year | | (0.6) | % | (8.8) | % | (4.3) | % | (4.0) | % | (3.2) | % | (1.0) | % | (2.9) | % | (4.2) | % | (1.7) | % | | | (4.5) | % | (2.9) | % | |

| | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

GAAP Income per Diluted Share2 | | $ | 1.56 | | $ | 2.20 | | $ | 0.42 | | $ | 1.98 | | $ | 1.55 | | $ | 1.83 | | $ | 2.52 | | $ | 1.60 | | $ | 1.81 | | | | $ | 6.16 | | $ | 7.50 | | |

| Y/Y Change3 | | (42.4) | % | NM | NM | (2.0) | % | (0.6) | % | (16.8) | % | NM | (19.2) | % | 16.8 | % | | | 36.9 | % | 21.8 | % | |

| | | | | | | | | | | | | | | |

ANI per Diluted Share2 | | $ | 3.31 | | $ | 3.63 | | $ | 4.05 | | $ | 3.82 | | $ | 3.46 | | $ | 3.91 | | $ | 4.35 | | $ | 3.57 | | $ | 3.51 | | | | $ | 14.81 | | $ | 15.28 | | |

| Y/Y Change | | (5.7) | % | (2.2) | % | 15.4 | % | 11.0 | % | 4.5 | % | 7.7 | % | 7.4 | % | (6.5) | % | 1.4 | % | | | 9.5 | % | 3.2 | % | |

FX Impact per Share vs Prior Year1 | | $ | 0.04 | | $ | (0.02) | | $ | (0.06) | | $ | 0.04 | | $ | — | | $ | — | | $ | (0.05) | | $ | 0.01 | | $ | — | | | | $ | — | | $ | (0.04) | | |

PPG Impact per Share vs Prior Year1 | | $ | (0.03) | | $ | 0.77 | | $ | 0.49 | | $ | 0.39 | | $ | 0.33 | | $ | 0.09 | | $ | 0.33 | | $ | 0.44 | | $ | 0.13 | | | | $ | 1.62 | | $ | 1.19 | | |

| PPG and FX % Impact on Adjusted Earnings Per Share vs Prior Year | | (0.2) | % | (20.4) | % | (12.3) | % | (12.5) | % | (10.0) | % | (2.5) | % | (6.9) | % | (11.8) | % | (3.7) | % | | | (12.0) | % | (7.8) | % | |

(1) Favorable impacts are shown in these tables as negatives, while unfavorable impacts are shown as positive figures.

(2) Diluted earnings per share includes the impact of convertible securities under the “if-converted” method if the effect of such securities would be dilutive and includes the assumed exercise of dilutive options, the assumed issuance of unvested RSUs, performance-based awards for which the performance condition has been met as of the date of determination, and contingently issuable shares that would be issuable if the end of the reporting period was the end of the contingency period, using the treasury stock method unless the effect is anti-dilutive. On August 11, 2023, the Company repurchased all of the outstanding Convertible Notes.

(3) Due to the relative volatility in our GAAP net income per share, many of the changes are not meaningful to the reader and have been marked "NM".

The following table summarizes our financial results by segment for the most recent quarter and for the twelve months ended December 31, 2024, in millions except for margin.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | For the three months ended 3/31/25 | | For the twelve months ended 12/31/24 |

| Mobility | Benefits | Corporate

Payments | Total | | Mobility | Benefits | Corporate Payments | Total |

| Revenues | $ | 333.8 | | $ | 199.3 | | $ | 103.5 | | $ | 636.6 | | | $ | 1,400.8 | | $ | 739.5 | | $ | 487.8 | | $ | 2,628.1 | |

| Segment Revenue % of Total | 52 | % | 31 | % | 16 | % | | | 53 | % | 28 | % | 19 | % | |

| GAAP Operating Income | $ | 99.4 | | $ | 56.5 | | $ | 27.2 | | $ | 157.3 | | | $ | 469.1 | | $ | 173.3 | | $ | 203.5 | | $ | 686.3 | |

| GAAP Operating Income Margin | 29.8 | % | 28.3 | % | 26.3 | % | 24.7 | % | | 33.5 | % | 23.4 | % | 41.7 | % | 26.1 | % |

| Adjusted Operating Income | $ | 131.4 | | $ | 86.9 | | $ | 40.5 | | $ | 233.8 | | | $ | 598.5 | | $ | 307.0 | | $ | 256.2 | | $ | 1,059.7 | |

| Adjusted Operating Income Margin | 39.4 | % | 43.6 | % | 39.1 | % | 36.7 | % | | 42.7 | % | 41.5 | % | 52.5 | % | 40.3 | % |

Within our Mobility segment, operating through North American, Over-the-Road, and International business units, WEX is a leader in fleet payment solutions, transaction processing, and information management. We serve diverse fleet needs globally, from Over-the-Road to locally operated fleets. Our proprietary closed-loop payments network in the U.S. covers more than 90% of fuel and 80% of EV charging locations. Our differentiated network offers enhanced data capture, custom controls, and tailored economics between fleets and merchants, creating customer value. Beyond fuel cards, our portfolio includes SaaS solutions for field service management, telematics, reporting and analytics, cash flow management, and mixed-energy fleets. Powered by payment intelligence and workflow optimization, these solutions deliver transformative value to operators, fleet managers, and business managers. Our solutions simplify our customers' businesses by optimizing costs, streamlining operations, and improving driver and fleet manager satisfaction while advancing sustainability and driving business growth.

Revenue in this segment is derived primarily from payment processing, based on transaction volume or fixed fees, as well as account servicing fees, finance charges, and other ancillary services.

•Mobility segment revenue for the quarter decreased 1.5% compared to the same period a year ago, including a 2.9% drag from lower fuel prices. The Q1 average domestic fuel price of $3.32 was 6 cents higher than our prior guidance, increasing revenue by approximately $4 million relative to consolidated guidance. Compared to the same period in 2024, a $0.24 decline in fuel prices reduced revenue approximately $8.5 million, which also includes a small impact from European fuel price spreads.

•Payment processing transactions were down 1.8% in Q1 2025 compared to Q1 2024. Local fleets in North America were down 2% and Over-the-Road truck fleets were up 0.6%.

•Same-store sales4, which is a measure of the gallons purchased, were down 3.9% compared to last year for local fleets in North America, which was in part due to weather-related issues, while Over-the-Road truck fleets were up 2.5%. The Company believes that this metric is a reflection of the economic demand environment and the long term trend of better vehicle fuel efficiency. Specific to Q1 results, we believe that there was a pull forward of demand for Over-the-Road truck customers in advance of anticipated tariffs. The overall results are in line with our expectations for the quarter and our new sales and retention rates remain strong.

•The net interchange rate in the Mobility segment was 1.30%, flat compared to the same quarter of 2024.

•GAAP operating income margin for the segment was 29.8%, compared to 29.3% in the same prior year period. The Mobility segment's non-GAAP adjusted operating income margin for the quarter was 39.4%, which is up 0.7% compared to last year. This increase was primarily driven by lower credit losses as discussed below.

•The net late fee rate increased by 7 basis points year-over-year, while finance fee revenue increased 7% at $75.2 million. The increase in the net late fee rate was due primarily to pricing changes implemented last year and was offset by a 4% decline in the number of late fee instances charged as well as the declines in fuel prices.

•Credit losses decreased by $6.9 million versus the same period last year, coming in at 12 basis points of spend volume, which was in line with our guidance range of 11-16 basis points and compares to 15 basis points last year. We remain very pleased with our efforts to minimize credit losses to date and will continue to watch this closely.

(4) Same-store sales for the Mobility segment are calculated by comparing fuel gallons purchased by customers who joined the Company in 2023 or earlier, adjusted for the number of business days in the period.

The following table reflects segment results and select other metrics within Mobility. All amounts are in millions, except for per transaction and per gallon data:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | | For the three months ended | | | For the twelve months ended |

| | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 |

| Revenues | | | | | | | | | | | | | | |

| Total Revenues | | $ | 342.3 | | $ | 340.2 | | $ | 350.1 | | $ | 350.1 | | $ | 339.0 | | $ | 359.6 | | $ | 357.2 | | $ | 345.2 | | $ | 333.8 | | | | $ | 1,382.7 | | $ | 1,400.8 | |

| Y/Y Change | | 7.3 | % | (10.3) | % | (7.4) | % | (4.7) | % | (1.0) | % | 5.7 | % | 2.0 | % | (1.4) | % | (1.5) | % | | | (4.2) | % | 1.3 | % |

| FX Impact5 | | $ | 2.5 | | $ | 0.8 | | $ | (0.6) | | $ | (0.9) | | $ | 0.1 | | $ | 0.4 | | $ | (0.5) | | $ | 0.1 | | $ | 1.3 | | | | $ | 1.7 | | $ | — | |

PPG Impact5 | | $ | (1.3) | | $ | 53.0 | | $ | 31.9 | | $ | 24.9 | | $ | 20.5 | | $ | 5.4 | | $ | 21.2 | | $ | 26.6 | | $ | 8.5 | | | | $ | 108.4 | | $ | 73.8 | |

| PPG and FX % Impact on Revenue | | (0.4) | % | (14.2) | % | (8.3) | % | (6.5) | % | (6.0) | % | (1.7) | % | (5.9) | % | (7.6) | % | (2.9) | % | | | (7.6) | % | (5.3) | % |

| | | | | | | | | | | | | | |

| Operating Income (GAAP) | | $ | 111.9 | | $ | 118.6 | | $ | 125.0 | | $ | 117.3 | | $ | 99.3 | | $ | 119.2 | | $ | 136.5 | | $ | 114.1 | | $ | 99.4 | | | | $ | 472.8 | | $ | 469.1 | |

| Operating Income (GAAP) Margin | | 32.7 | % | 34.9 | % | 35.7 | % | 33.5 | % | 29.3 | % | 33.1 | % | 38.2 | % | 33.1 | % | 29.8 | % | | | 34.2 | % | 33.5 | % |

| Adjusted Operating Income | | $ | 138.8 | | $ | 150.3 | | $ | 159.6 | | $ | 150.7 | | $ | 131.0 | | $ | 154.3 | | $ | 167.1 | | $ | 146.1 | | $ | 131.4 | | | | $ | 599.4 | | $ | 598.5 | |

| Adjusted Operating Income Margin | | 40.5 | % | 44.2 | % | 45.6 | % | 43.0 | % | 38.6 | % | 42.9 | % | 46.8 | % | 42.3 | % | 39.4 | % | | | 43.3 | % | 42.7 | % |

| | | | | | | | | | | | | | |

| Select Other Metrics | | | | | | | | | | | |

| Total Volume | | $ | 21,217 | | $ | 20,228 | | $ | 22,220 | | $ | 21,057 | | $ | 19,943 | | $ | 20,849 | | $ | 20,137 | | $ | 18,610 | | $ | 18,751 | | | | $ | 84,721 | | $ | 79,539 | |

| Y/Y Change | | (2.2) | % | (27.3) | % | (12.5) | % | (12.2) | % | (6.0) | % | 3.1 | % | (9.4) | % | (11.6) | % | (6.0) | % | | | (14.3) | % | (6.1) | % |

| Payment Processing Transactions | | 137.5 | | 142.4 | | 144.6 | | 138.1 | | 136.9 | | 144.9 | | 146.5 | | 138.5 | | 134.5 | | | | 562.6 | | 566.8 | |

| Y/Y Change | | 3.7 | % | (0.5) | % | (0.4) | % | (0.8) | % | (0.4) | % | 1.8 | % | 1.3 | % | 0.3 | % | (1.8) | % | | | 0.4 | % | 0.7 | % |

| Payment Processing $ of Fuel | | $ | 14,144 | | $ | 13,780 | | $ | 14,945 | | $ | 13,814 | | $ | 13,061 | | $ | 13,729 | | $ | 13,227 | | $ | 12,003 | | $ | 12,018 | | | | $ | 56,684 | | $ | 52,021 | |

| Y/Y Change | | (1.7) | % | (26.1) | % | (13.1) | % | (13.3) | % | (7.7) | % | (0.4) | % | (11.5) | % | (13.1) | % | (8.0) | % | | | (14.3) | % | (8.2) | % |

| Average U.S. Fuel Price | | $ | 3.86 | | $ | 3.68 | | $ | 3.97 | | $ | 3.76 | | $ | 3.56 | | $ | 3.62 | | $ | 3.45 | | $ | 3.25 | | $ | 3.32 | | | | $ | 3.82 | | $ | 3.47 | |

| Y/Y Change | | (2.3) | % | (26.1) | % | (12.6) | % | (13.4) | % | (7.8) | % | (1.6) | % | (13.1) | % | (13.6) | % | (6.7) | % | | | (14.3) | % | (9.2) | % |

| Payment Processing Gallons | | 3,577 | | 3,664 | | 3,687 | | 3,579 | | 3,568 | | 3,694 | | 3,731 | | 3,601 | | 3,528 | | | | 14,507 | | 14,593 | |

| Y/Y Change | | 0.8 | % | (0.7) | % | (1.1) | % | (0.9) | % | (0.3) | % | 0.8 | % | 1.2 | % | 0.6 | % | (1.1) | % | | | (0.5) | % | 0.6 | % |

| Payment Processing Revenue | | $ | 171.5 | | $ | 172.1 | | $ | 177.1 | | $ | 174.3 | | $ | 170.7 | | $ | 177.2 | | $ | 183.2 | | $ | 163.4 | | $ | 156.4 | | | | $ | 695.0 | | $ | 694.5 | |

| Y/Y Change | | 12.9 | % | (15.0) | % | (6.1) | % | (1.7) | % | (0.5) | % | 3.0 | % | 3.4 | % | (6.3) | % | (8.4) | % | | | (3.5) | % | (0.1) | % |

| Net Payment Processing Rate | | 1.21 | % | 1.25 | % | 1.18 | % | 1.26 | % | 1.31 | % | 1.29 | % | 1.38 | % | 1.36 | % | 1.30 | % | | | 1.23 | % | 1.34 | % |

| Net Late Fee Revenue | | $70.2 | $66.3 | $66.4 | $69.0 | $60.4 | $67.3 | $59.0 | $68.4 | $63.7 | | | $271.8 | $255.1 |

| Y/Y Change | | 11.2 | % | (6.4) | % | (20.2) | % | (23.3) | % | (14.0) | % | 1.5 | % | (11.1) | % | (0.9) | % | 5.5 | % | | | (11.5) | % | (6.1) | % |

| Net Late Fee Rate | | 0.50 | % | 0.48 | % | 0.44 | % | 0.50 | % | 0.46 | % | 0.49 | % | 0.45 | % | 0.57 | % | 0.53 | % | | | 0.48 | % | 0.49 | % |

| Credit Losses, in Basis Points | | 32 | 15 | 7 | 8 | 15 | 14 | 6 | 11 | 12 | | | 15 | 12 |

(5) Favorable impacts are shown in these tables as negatives, while unfavorable impacts are shown as positive figures.

WEX's Benefits segment simplifies employee benefit plan administration through SaaS software integrated with payment solutions. We deliver diverse product offerings including Benefit Administration, Health Savings Accounts, Flexible Spending Accounts, Health Reimbursement Arrangements, COBRA & Direct Billing, and compliance administration. These solutions empower administrators, employers, and participants to make optimal benefits decisions. Our platform's flexibility supports multiple plan types and customizable designs, adapting to market changes. Our solutions streamline processes, reduce costs, and empower employees with greater choice and control. WEX combines healthcare expertise with payment intelligence and workflow optimization to deliver secure, customer-centric solutions. This simplifies daily administration, provides personalized tools, and offers proactive support, ultimately driving better business outcomes through healthier, more engaged employees.

Revenue in this segment is derived from per-participant fees, HSA deposit interest, and debit card interchange. Our business experiences annual seasonality, with Q1 peaking for new account sign-ups and transactions. WEX Inc. also serves as an IRS-designated non-bank custodian, while WEX Bank provides HSA depository services.

•Benefits revenue in Q1 2025 was $199.3 million, a 4.2% increase over the prior year driven by continued strong revenue growth in our HSA business.

•Average SaaS accounts for Q1 increased 6.1% year-over-year to 21.5 million. HSA account growth specifically, including partner channel accounts, was 7% compared to market growth of 5% according to the Devenir Research 2024 Year-end HSA Market Statistics and Trends report.

•Benefits purchase volume increased by 10.2% compared to the prior-year quarter. While our interchange revenues in this segment are a relatively small piece of the total, they generate a steady revenue stream and a strong flow-through to operating income.

•Average custodial cash assets of $4.6 billion, an increase of 9.5% compared to the prior year, generated $55.8 million in revenue that was earned at WEX Bank and at third-party banks compared to $50.5 million last year. The interest yield earned on these investments increased 5 basis points in Q1 at 4.85% compared to the prior year.

•GAAP operating income margin for the segment was 28.3%, compared to 24.4% in the same prior year period. The Benefits segment adjusted operating income margin, which is a non-GAAP metric, was 43.6% compared to 41.5% in 2024. The increase in margin versus last year is driven by the high flow-through of custodial investment income.

The following table reflects segment results and select other metrics within Benefits. All amounts are in millions, except for yields:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | | For the three months ended | | | | For the twelve months ended |

| | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 |

| Revenues | | | | | | | | | | | | | | |

| Total Revenues | | $ | 164.9 | | $ | 159.2 | | $ | 166.1 | | $ | 178.2 | | $ | 191.2 | | $ | 179.8 | | $ | 181.5 | | $ | 186.9 | | $199.3 | | | $ | 668.4 | | $ | 739.5 | |

| Y/Y Change | | 36.2 | % | 34.2 | % | 33.9 | % | 26.7 | % | 15.9 | % | 12.9 | % | 9.3 | % | 4.9 | % | 4.2 | % | | | 32.5 | % | 10.6 | % |

| | | | | | | | | | | | | | |

| Operating Income (GAAP) | | $ | 39.8 | | $ | 29.5 | | $ | 26.5 | | $ | 19.0 | | $ | 46.7 | | $ | 32.5 | | $ | 45.2 | | $ | 48.8 | | $ | 56.5 | | | | $ | 114.8 | | $ | 173.3 | |

| Operating Income (GAAP) Margin | | 24.1 | % | 18.5 | % | 16.0 | % | 10.7 | % | 24.4 | % | 18.1 | % | 24.9 | % | 26.1 | % | 28.3 | % | | | 17.2 | % | 23.4 | % |

| Adjusted Operating Income | | $ | 64.5 | | $ | 59.3 | | $ | 58.8 | | $ | 59.2 | | $ | 79.4 | | $ | 71.1 | | $ | 78.4 | | $ | 78.0 | | $ | 86.9 | | | | $ | 241.8 | | $ | 307.0 | |

| Adjusted Operating Income Margin | | 39.1 | % | 37.2 | % | 35.4 | % | 33.2 | % | 41.5 | % | 39.6 | % | 43.2 | % | 41.7 | % | 43.6 | % | | | 36.2 | % | 41.5 | % |

| | | | | | | | | | | | | | |

| Select Other Metrics | | | | | | | | | | | |

| Average SaaS Accounts | | 20.3 | | 19.5 | | 19.9 | | 19.9 | | 20.3 | | 20.0 | | 20.3 | | 20.4 | | 21.5 | | | | 19.9 | | 20.3 | |

| Y/Y Change | | 13.8 | % | 11.2 | % | 9.2 | % | 7.6 | % | — | % | 2.6 | % | 2.0 | % | 2.5 | % | 6.1 | % | | | 10.6 | % | 2.0 | % |

| Total Volume | | 3,502 | | 3,236 | | 2,880 | | 2,823 | | 3,840 | | 3,496 | | 3,129 | | 3,135 | | 4,196 | | | | 12,442 | 13,600 |

| Y/Y Change | | 14.3 | % | 11.2 | % | 9.3 | % | 8.7 | % | 9.7 | % | 8.0 | % | 8.6 | % | 11.1 | % | 9.3 | % | | | 11.0 | % | 9.3 | % |

| Purchase Volume | | $ | 1,929 | | $ | 1,716 | | $ | 1,501 | | $ | 1,510 | | $ | 2,115 | | $ | 1,865 | | $ | 1,646 | | $ | 1,617 | | $ | 2,330 | | | | 6,656 | | 7,243 | |

| Y/Y Change | | 18.3 | % | 13.3 | % | 11.2 | % | 9.9 | % | 9.6 | % | 8.7 | % | 9.7 | % | 7.1 | % | 10.2 | % | | | 13.4 | % | 8.8 | % |

| Average HSA Custodial Cash Assets | | $ | 3,764 | | $ | 3,878 | | $ | 3,909 | | $ | 3,925 | | $ | 4,209 | | $ | 4,231 | | $ | 4,315 | | $ | 4,366 | | $ | 4,609 | | | | 3,869 | | 4,280 | |

| Y/Y Change | | 25.5 | % | 24.7 | % | 23.0 | % | 13.1 | % | 11.8 | % | 9.1 | % | 10.4 | % | 11.2 | % | 9.5 | % | | | 21.8 | % | 10.6 | % |

| Custodial Investment Revenue - in Other Revenue6 | | $ | 20.0 | | $ | 27.1 | | $ | 29.7 | | $ | 32.2 | | $ | 37.5 | | $ | 40.0 | | $ | 41.2 | | $ | 44.3 | | $ | 44.6 | | | | $ | 109.0 | | $ | 163.0 | |

| Custodial Investment Revenue - in Account Servicing Revenue7 | | $ | 17.1 | | $ | 14.9 | | $ | 14.3 | | $ | 13.1 | | $ | 13.0 | | $ | 11.9 | | $ | 12.5 | | $ | 9.1 | | $ | 11.3 | | | | $ | 59.4 | | $ | 46.5 | |

| Custodial Investment Revenue - Total | | $ | 37.2 | | $ | 42.0 | | $ | 44.0 | | $ | 45.3 | | $ | 50.5 | | $ | 51.9 | | $ | 53.7 | | $ | 53.4 | | $ | 55.8 | | | | $ | 168.5 | | $ | 209.5 | |

| Y/Y Change | | 292.9 | % | 313.9 | % | 177.0 | % | 77.0 | % | 35.8 | % | 23.6 | % | 22.0 | % | 17.9 | % | 10.6 | % | | | 175.8 | % | 24.3 | % |

| HSA Yield8 | | 3.95 | % | 4.33 | % | 4.51 | % | 4.62 | % | 4.80 | % | 4.91 | % | 4.98 | % | 4.89 | % | 4.85 | % | | | 4.36 | % | 4.90 | % |

(6) Represents income earned on available-for-sale securities held and managed by WEX Bank. These amounts are recorded within Other Revenue on our consolidated statement of operations.

(7) Represents income earned for custodial deposits held at third-party banks. These amounts are recorded within Account Servicing Revenue on our consolidated statement of operations.

(8) We calculate HSA yield by dividing Custodial Investment Revenue - Total by Average Custodial Cash Assets.

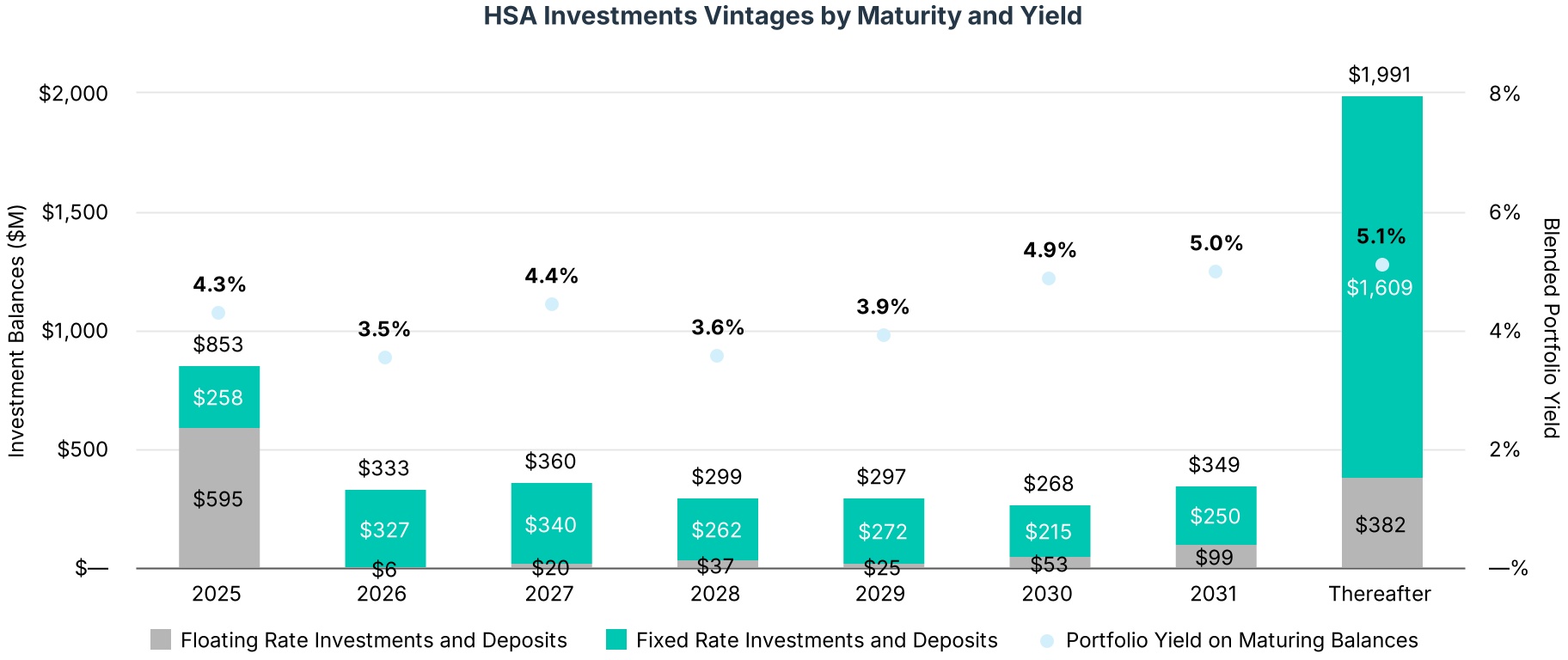

The following chart shows the maturity profile of the investment securities and deposits as of March 31, 2025. The blended portfolio yield shown is the return earned on the balances maturing each year as of March 31, 2025.

Despite benchmark interest rates that have generally trended downward recently, our portfolio management efforts have maintained relatively consistent custodial investment returns.

| | | | | |

| Corporate Payments Segment |

WEX's Corporate Payments segment delivers global B2B payment solutions, powered by payment intelligence and workflow optimization, that enhance security, simplify processes, and drive revenue. Our Direct to Corporate solution automates Accounts Payable (AP) by integrating with ERPs and accounting workflows to maximize virtual payment usage. Our customizable Embedded Payments solution seamlessly integrates virtual payment capabilities into existing workflows, whether payments are core to the business, part of critical operations, or an added customer offering. This versatile solution empowers a broad range of industries, including online travel. We also offer white-label partnerships with financial institutions. Leveraging scale, network incentives, global expertise, and our supplier enablement team, we optimize revenue for our customers.

Revenue in this segment is primarily derived from net interchange, with additional contributions from licensing fees.

•Total segment revenue for the quarter decreased 15.5% to $103.5 million. The revenue decline was driven primarily by the change in revenue model for a major online travel agency (OTA) customer, which we have discussed previously. Our relationship with this customer is strong and we expect to lap the impact of this change starting in Q3 2025. Foreign exchange rates were also unfavorable, reducing revenue by $1.3 million compared to the prior year.

•Total purchase volumes issued by WEX declined 27.8% compared to last year. This was largely due to the OTA revenue model transition mentioned above.

•The net interchange rate decreased 2 basis points sequentially driven primarily by customer volume mix.

•Direct Accounts Payable purchase volume for WEX increased by approximately 25%. While the Direct component of the segment is currently a small portion of volume, it is rapidly growing and its higher revenue yield leads to a relatively outsized revenue impact to the segment. Direct also provides lower quarterly volume volatility due to our direct interaction with the end customer. This book of business currently generates approximately 20% of annual segment revenue.

•Because of the strong potential growth opportunity in our Direct Accounts Payable business, we intend to continue to invest in new product capabilities and additional sales and marketing resources in 2025.

•GAAP operating income margin for the segment was 26.3% compared to 41.7% in the comparable prior year quarter. The non-GAAP adjusted operating income margin in the segment was 39.1%, which is down from 52.7% in the same quarter last year due to lower revenue.

The following table reflects segment results and select other metrics within Corporate Payments. All amounts are in millions: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | For the three months ended | | | For the twelve months ended |

| | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 |

| Revenues | | | | | | | | | | | | | | |

| Total Revenues | | $ | 104.8 | | $ | 121.9 | | $ | 135.2 | | $ | 135.0 | | $ | 122.5 | | $ | 134.1 | | $ | 126.9 | | $ | 104.3 | | $ | 103.5 | | | | $ | 496.9 | | $ | 487.8 | |

| Y/Y Change | | 35.6 | % | 21.4 | % | 18.6 | % | 22.0 | % | 16.9 | % | 10.0 | % | (6.1) | % | (22.7) | % | (15.5) | % | | | 23.5 | % | (1.8) | % |

| FX Impact9 | | $ | 1.8 | | $ | (1.1) | | $ | (4.7) | | $ | 0.6 | | $ | (0.9) | | $ | 0.5 | | $ | (1.7) | | $ | 1.3 | | $ | 1.3 | | | | $ | (3.3) | | $ | (0.9) | |

| | | | | | | | | | | | | | |

| Operating Income (GAAP) | | $ | 36.9 | | $ | 51.7 | | $ | 69.6 | | $ | 60.9 | | $ | 51.1 | | $ | 61.0 | | $ | 56.1 | | $ | 35.4 | | $ | 27.2 | | | | $ | 219.1 | | $ | 203.5 | |

| Operating Income (GAAP) Margin | | 35.2 | % | 42.4 | % | 51.5 | % | 45.1 | % | 41.7 | % | 45.5 | % | 44.2 | % | 33.9 | % | 26.3 | % | | | 44.1 | % | 41.7 | % |

| Adjusted Operating Income | | $ | 49.2 | | $ | 66.3 | | $ | 82.9 | | $ | 78.8 | | $ | 64.6 | | $ | 74.4 | | $ | 71.5 | | $ | 45.7 | | $ | 40.5 | | | | $ | 277.2 | | $ | 256.2 | |

| Adjusted Operating Income Margin | | 46.9 | % | 54.4 | % | 61.3 | % | 58.4 | % | 52.7 | % | 55.5 | % | 56.4 | % | 43.9 | % | 39.1 | % | | | 55.8 | % | 52.5 | % |

| | | | | | | | | | | | | | |

| Select Other Metrics | | | | | | | | | | | |

| Total Volume | | $ | 27,589 | | $ | 31,827 | | $ | 36,780 | | $ | 31,971 | | $ | 33,026 | | $ | 35,792 | | $ | 39,056 | | $ | 30,833 | | $ | 31,109 | | | | $ | 128,168 | | $ | 138,707 | |

| Y/Y Change | | 37.5 | % | 23.2 | % | 24.6 | % | 22.0 | % | 19.7 | % | 12.5 | % | 6.2 | % | (3.6) | % | (5.8) | % | | | 26.1 | % | 8.2 | % |

| Total Purchase Volume | | $ | 18,635 | | $ | 22,901 | | $ | 27,860 | | $ | 22,801 | | $ | 23,948 | | $ | 25,756 | | $ | 23,394 | | $ | 16,541 | | $ | 17,285 | | | | $ | 92,197 | | $ | 89,640 | |

| Y/Y Change | | 57.8 | % | 33.8 | % | 34.9 | % | 33.5 | % | 28.5 | % | 12.5 | % | (16.0) | % | (27.5) | % | (27.8) | % | | | 38.3 | % | (2.8) | % |

| Net Interchange Rate | | 0.48 | % | 0.46 | % | 0.42 | % | 0.52 | % | 0.43 | % | 0.45 | % | 0.45 | % | 0.52 | % | 0.50 | % | | | 0.46 | % | 0.46 | % |

| Payment Solutions Processing Revenue | | 90.1 | | 104.8 | | 115.7 | | 117.4 | | 103.2 | | 116.2 | | 104.8 | | $ | 85.5 | | $ | 85.7 | | | | $ | 428.0 | | $ | 409.7 | |

| Y/Y Change | | 38.4 | % | 18.3 | % | 14.0 | % | 19.2 | % | 14.5 | % | 10.9 | % | (9.4) | % | (27.2) | % | (16.9) | % | | | 21.0 | % | (4.3) | % |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

(9) Favorable impacts are shown in these tables as negatives, while unfavorable impacts are shown as positive figures.

Balance Sheet and Debt

The following table includes a further condensed version of our balance sheet as well as key operating metrics relevant to our balance sheet:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (in millions, except for leverage ratio) | | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 |

| Cash and Cash Equivalents | | $ | 922 | | $ | 901 | | $ | 958 | | $ | 976 | | $ | 780 | | $ | 683 | | $ | 535 | | $ | 599 | | $ | 610 | |

| Accounts Receivable | | 3,400 | | 3,622 | | 4,054 | | 3,429 | | 3,857 | | 3,966 | | 3,770 | | 3,023 | | 3,768 | |

| Long-Term Debt, Net | | 2,631 | | 2,499 | | 2,650 | | 2,828 | | 3,082 | | 2,960 | | 3,143 | | 3,082 | | 4,100 | |

| Corporate Cash | | $ | 149 | | $ | 194 | | $ | 170 | | $ | 172 | | $ | 176 | | $ | 143 | | $ | 123 | | $ | 80 | | $ | 163 | |

| Available Liquidity10 | | $ | 925 | | $ | 1,087 | | $ | 1,095 | | $ | 903 | | $ | 639 | | $ | 947 | | $ | 729 | | $ | 735 | | $ | 770 | |

| Leverage Ratio | | 2.5x | 2.8x | 2.4x | 2.5x | 2.6x | 2.5x | 2.6x | 2.6x | 3.5x |

| Investment Securities at Cost11 | | $ | 2,597 | | $ | 2,789 | | $ | 2,830 | | $ | 3,102 | | $ | 3,411 | | $ | 3,438 | | $ | 3,734 | | $ | 3,875 | | $ | 3,891 | |

We remain in a healthy financial position and ended the quarter with $770 million of available liquidity that includes our available corporate cash and capacity to borrow under our revolving Credit Agreement. Our leverage ratio as of March 31, 2025, as defined in the Credit Agreement, stands at 3.5 times, and remains within our long-term target of 2.5 times to 3.5 times. Our leverage increased in the quarter primarily due to financing for the recently completed Tender Offer. The Company expects to use cash flow generated through the remainder of the year to reduce leverage.

The following table summarizes the Company's long-term debt maturities, excluding our revolver and nominal scheduled principal payments on our term loans:

We have maintained ample access to debt markets and strategically review our debt composition and maturity schedule to align with our long-term objectives. We currently have a three-year runway before our next maturity and believe this provides an appropriate cushion to remain opportunistic in the market.

(10) Available liquidity includes corporate cash, plus the portion of our revolving credit facility undrawn as of the specific balance sheet date.

(11) Our available for sale debt securities are measured and reported at fair value on the face of the balance sheet. We have additionally included the cost basis of these investments to provide greater clarity on the nature and extent of our investing activities.

Cash Flow

The following table presents our operating cash flow and adjusted free cash flow metric:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | | For the three months ended | | |

| (In millions) | | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | | |

| Operating Cash Flow, as reported | | $ | 27.1 | | $ | 72.4 | | $ | 46.5 | | $ | 761.9 | | $ | (153.3) | | $ | (7.0) | | $ | 3.3 | | $ | 638.4 | | $ | (481.6) | | | | | |

| Adjustments to operating cash flow, as reported | | | | | | | | | | | | | | |

| Changes in WEX Bank Cash Balances | | $ | (46.7) | | $ | 71.4 | | $ | (83.5) | | $ | (23.6) | | $ | 188.9 | | $ | 69.6 | | $ | 125.3 | | $ | (104.7) | | $ | 67.7 | | | | | |

| Other | | $ | 1.5 | | $ | — | | $ | — | | $ | (50.0) | | $ | 67.1 | | $ | — | | $ | — | | $ | (33.1) | | $ | 58.8 | | | | | |

| | | | | | | | | | | | | | |

| Net Funding Activity | | $ | 971.8 | | $ | 385.9 | | $ | 294.8 | | $ | (214.4) | | $ | 205.0 | | $ | 214.8 | | $ | 372.2 | | $ | (139.3) | | $ | 375.5 | | | | | |

| Less: Purchases of Current Investment Securities, Net of Sales and Maturities | | $ | (1,026.8) | | $ | (220.8) | | $ | (56.6) | | $ | (256.8) | | $ | (282.9) | | $ | (25.6) | | $ | (276.3) | | $ | (153.2) | | $ | 28.3 | | | | | |

| Less: Capital Expenditures | | $ | (30.6) | | $ | (34.7) | | $ | (36.4) | | $ | (41.9) | | $ | (34.0) | | $ | (39.6) | | $ | (35.0) | | $ | (38.7) | | $ | (32.6) | | | | | |

| Adjusted Free Cash Flow | | $ | (103.7) | | $ | 274.2 | | $ | 164.9 | | $ | 175.2 | | $ | (9.2) | | $ | 212.2 | | $ | 189.5 | | $ | 169.5 | | $ | 16.2 | | | | | |

| | | | | | | | | | | | | | |

| Trailing Twelve Month Adjusted Free Cash Flows | | $ | 460.4 | | $ | 642.5 | | $ | 601.7 | | $ | 510.6 | | $ | 605.0 | | $ | 543.0 | | $ | 567.8 | | $ | 562.0 | | $ | 587.4 | | | | | |

WEX generates a significant amount of cash each year and we utilize an adjusted free cash flow metric, which is prepared on a non-GAAP basis, to describe the cash flow we consider available for investment. Using our definition, Q1 2025 non-GAAP adjusted free cash flow was $16.2 million. Over the trailing twelve months ended March 31, 2025, we generated $587 million, converting a substantial portion of our ANI into adjusted free cash flow. We are able to leverage this strong cash flow generation to deliver on our disciplined capital allocation strategy including ongoing investments in our business.

Capital Allocation

The following table presents our uses of cash over the preceding quarters:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | For the three months ended | |

| (In millions) | | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 |

| Capital Expenditures | | $ | 30.6 | | $ | 34.6 | | $ | 36.4 | | $ | 41.9 | | $ | 34.0 | | $ | 39.6 | | $ | 35.0 | | $ | 38.7 | | $ | 32.6 | |

| Acquisitions12 | | $ | 31.7 | | $ | — | | $ | 180.7 | | $ | 246.3 | | $ | 86.6 | | $ | 5.1 | | $ | 7.1 | | $ | — | | $ | 91.2 | |

| Share Repurchases | | $ | 92.2 | | $ | 3.2 | | $ | 50.0 | | $ | 150.0 | | $ | 73.6 | | $ | 100.0 | | $ | 370.0 | | $ | 106.0 | | $ | 790.0 | |

| Capital Deployed | | $ | 154.5 | | $ | 37.8 | | $ | 267.1 | | $ | 438.2 | | $ | 194.2 | | $ | 144.7 | | $ | 412.1 | | $ | 144.7 | | $ | 913.8 | |

WEX strategically allocates capital through a disciplined and rigorous analytical process, prioritizing investments that deliver strong long-term returns. Our primary uses of cash include growth-focused initiatives, such as investments in technology and customer experience, strategic M&A, and returning capital to shareholders via share repurchases. Our CapEx investments are central to strengthening our competitive edge and delivering greater value to our customers.

The following table presents cash spent on share buybacks and ending undiluted shares outstanding for each of the preceding quarters:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In millions) | For the three months ended |

| 6/30/22 | 9/30/22 | 12/31/22 | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/2413 | 12/31/2413 | 03/31/25 |

| Cash Spent Repurchasing Shares | $ | 80.6 | | $ | 69.0 | | $ | 141.2 | | $ | 92.2 | | $ | 3.2 | | $ | 50.0 | | $ | 150.0 | | $ | 73.6 | | $ | 100.0 | | $ | 370.0 | | $ | 106.0 | | $ | 790.0 | |

| Cumulative Cash Spent | | $ | 149.6 | | $ | 290.8 | | $ | 383.0 | | $ | 386.1 | | $ | 436.1 | | $ | 586.2 | | $ | 659.8 | | $ | 759.8 | | $ | 1,129.8 | | $ | 1,235.8 | | $ | 2,025.8 | |

| Share Repurchased | 0.52 | | 0.43 | | 0.95 | | 0.53 | | 0.02 | | 0.26 | | 0.87 | | 0.35 | | 0.47 | | 1.72 | | 0.77 | | 5.10 | |

| Cumulative Shares Repurchased | | 0.95 | | 1.90 | | 2.43 | | 2.45 | | 2.71 | | 3.58 | | 3.93 | | 4.39 | | 6.12 | | 6.89 | | 11.99 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

On February 26, 2025, the Company commenced a modified “Dutch auction” Tender Offer to repurchase up to $750.0 million worth of its common stock (the “Tender Offer”). On March 31, 2025, the Company completed the Tender Offer and accepted for purchase a total of approximately 4.9 million shares of its common stock at a purchase price of $154 per share. The Company paid $750.0 million in cash to complete the Tender Offer, excluding related costs and fees. The Company incurred approximately $4.1 million of costs and fees related to the Tender Offer, which are recorded along with the cost of the shares repurchased as treasury stock.

(12) This line is presented on a cash basis and includes all consideration transferred in the related quarter, including deferred and contingent payments when they are paid as opposed to when the underlying transaction occurred.

(13) During the third quarter of 2024, we entered into an ASR agreement with JPMorgan to repurchase an aggregate of $300.0 million of the Company’s outstanding common stock. Under the ASR, the Company made a payment of $300.0 million to JPMorgan for which we received an initial delivery of approximately 1.3 million shares of our common stock. For purposes of this table, we have included the full payment amount and the initial delivery of shares in the quarter ended September 30, 2024. During the fourth quarter of 2024, the ASR was settled resulting in the receipt of an additional 0.2 million shares of WEX common stock, which is included in the quarter ended December 31, 2024.

Financial Guidance

The following table presents our expectations for the second quarter and full year 2025:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Financial Guidance | Q2'25 | | Full Year 2025 |

| Current Guidance | | Current Guidance | | Changes from Prior Guide at Midpoint |

| Low | High | | Low | High | | $ Change | % Change | Fuel Price Impact |

| Net Revenue, in millions | $ | 640 | | $ | 660 | | | $ | 2,568 | | $ | 2,628 | | | $ | (32) | | (1) | % | $(30) |

| Adjusted Net Income per Diluted Share14 | $ | 3.60 | | $ | 3.80 | | | $ | 14.72 | | $ | 15.32 | | | $ | 0.07 | | — | % | $(0.53) |

Second quarter and full year 2025 guidance is based on a number of assumptions, including:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Key Guidance Assumptions | Q2'25 | | Full Year 2025 | |

| Current Guidance | | Current Guidance | Change from Prior Guide at Midpoint | % Change | |

| Average US Retail Fuel Prices per Gallon | $3.18 | | $3.10 | $(0.15) | (5)% | |

| Mobility Credit Losses (bps) | 11 | - | 16 | | 12 | - | 17 | 0 | —% | |

| Diluted Shares Outstanding, in millions | 34.5 | | 35.9 | -3.1 | (8)% | |

| | | | | | |

2025 guidance also includes the following assumptions:

•U.S. GDP growth of approximately 2% in 2025; guidance is based upon current trends and does not include the impact of a potential further slowdown in the economy

•No benefits from future M&A activity

•Interest rates in line with the market Fed Funds projections

•Exchange rates are as of the end of March 2025

•Adjusted net income effective tax rate of 25.0% for 2025 (all periods)

•No further share repurchases in 2025

(14) The Company's adjusted net income guidance, which is a non-GAAP measure, excludes unrealized gains and losses on financial instruments, net foreign currency gains and losses, changes in fair value of contingent consideration, acquisition-related intangible amortization, other acquisition and divestiture related items, stock-based compensation, other costs, impairment charges, debt restructuring and debt issuance cost amortization, adjustments attributable to our non-controlling interests, and certain tax related items. We are unable to reconcile our adjusted net income guidance to the comparable GAAP measure without unreasonable effort because of the difficulty in predicting the amounts to be adjusted, including, but not limited to, foreign currency exchange rates, unrealized gains and losses on financial instruments, and acquisition and divestiture related items, which may have a significant impact on our financial results.

The following tables include estimated revenue and ANI per share sensitivities to changes in PPG and interest rates as of the date of this supplement. As a reminder, the impacts of these macro factors can and will change based upon various factors including the composition of our balance sheet. We target maintaining a materially neutral ANI per Share impact from 100bps adjustments to interest rates and can adjust our profile through balance sheet strategies and hedging.

| | | | | | | | | | | | | | | | | |

| Price Per Gallon | | Interest Rates |

| Sensitivities | +$0.10/Gal | -$0.10/Gal | | +100bps | -100bps |

| Impact to Net Revenue, in millions (Approximate) | $ | 20 | | $ | (20) | | | $ | 40 | | $ | (40) | |

| Impact to ANI per Share (Approximate)15 | $ | 0.35 | | $ | (0.35) | | | $ | (0.30) | | $ | 0.35 | |

Note: The ANI per share amounts above have been updated to reflect the share count reduction due to the Tender Offer completed at the end of March.

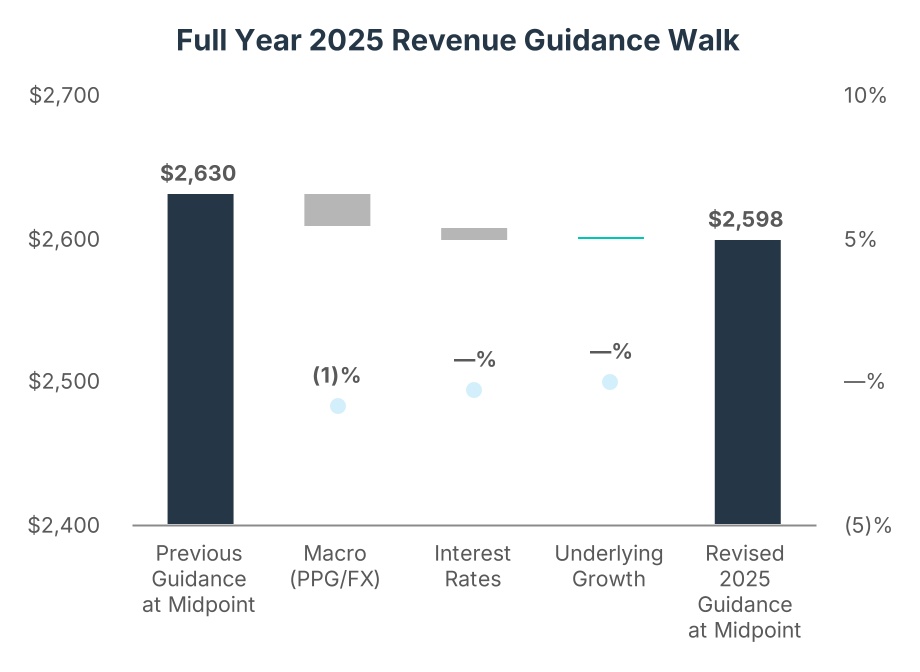

The following charts represent a walk between our most recent guidance and our revised guidance accounting for the primary drivers that have changed. The revised guidance does not contemplate the impact of a recessionary cycle or further economic deterioration that remains uncertain at this time.

(15) The Company's adjusted net income guidance, which is a non-GAAP measure, excludes unrealized gains and losses on financial instruments, net foreign currency gains and losses, changes in fair value of contingent consideration, acquisition-related intangible amortization, other acquisition and divestiture related items, stock-based compensation, other costs, impairment charges, debt restructuring and debt issuance cost amortization, adjustments attributable to our non-controlling interests and certain tax related items. We are unable to reconcile our adjusted net income guidance to the comparable GAAP measure without unreasonable effort because of the difficulty in predicting the amounts to be adjusted, including, but not limited to, foreign currency exchange rates, unrealized gains and losses on financial instruments, and acquisition and divestiture related items, which may have a significant impact on our financial results.

Acronyms and Abbreviations

The acronyms and abbreviations identified below are used in these supplemental materials.

| | | | | |

| Adjusted free cash flow | A non-GAAP measure calculated as cash flows from operating activities, adjusted for net purchases of current investment securities, capital expenditures, net Funding Activity, changes in WEX Bank cash balances, and certain other adjustments. |

| Adjusted net income or ANI | A non-GAAP measure that adjusts net income (loss) to exclude all items excluded in segment adjusted operating income except unallocated corporate expenses, further excluding unrealized gains and losses on financial instruments, net foreign currency gains and losses, debt issuance cost amortization, tax related items and certain other non-operating items, as applicable depending on the period presented. |

| ASR | Accelerated Share Repurchase |

| Average number of SaaS accounts | Represents the average number of active consumer-directed health, COBRA, and billing accounts on our SaaS platforms. HSA accounts for which WEX Inc. serves as the non-bank custodian under designation by the U.S. Department of Treasury are included in this average. |

| BTFP | The Federal Reserve Bank Term Funding Program, which provides liquidity to U.S. depository institutions. |

| Company | WEX Inc. and all entities included in the consolidated financial statements. |

| Convertible notes | Convertible senior unsecured notes due on July 15, 2027 in an aggregate principal amount of $310.0 million with a 6.5 percent interest rate, issued July 1, 2020, which were repurchased by the Company and canceled by the trustee at the instruction of the Company on August 11, 2023. |

| Corporate cash | Calculated in accordance with the terms of our consolidated leverage ratio in the Company’s Amended and Restated Credit Agreement. |

| Credit Agreement | Amended and Restated Credit Agreement entered into on April 1, 2021 (as amended from time to time) by and among the Company and certain of its subsidiaries, as borrowers, and Bank of America, N.A., as administrative agent on behalf of the lenders. |

| |

| |

| FHLB | Federal Home Loan Bank |

| FSA | Flexible Spending Account |

| Funding activity | Includes the change in net deposits, net advances from the FHLB, changes in participation debt, and changes in borrowings under the BTFP and borrowed federal funds. |

| HSA | Health Savings Account |

| Net interchange rate | Represents the percentage of the dollar value of each payment processing transaction that WEX records as revenue from merchants, less certain discounts given to customers and network fees. |

| Net late fee rate | Net late fee rate represents late fee revenue as a percentage of fuel purchased by fleets that have a payment processing relationship with WEX. |

| Net payment processing rate | The percentage of each payment processing $ of fuel that the Company records as revenue from merchants less certain discounts given to customers and network fees. |

| Net working capital | Total current assets less total current liabilities. |

| Operating cash flow | Net cash provided by (used for) operating activities. |

| | | | | |

| Operating interest | Interest expense incurred on the operating debt obtained to provide liquidity for the Company’s short-term receivables or used for investing purposes in fixed income debt securities. |

| Over-the-Road | Typically, heavy trucks traveling long distances. |

| Payment processing $ of fuel | Total dollar value of the fuel purchased by fleets that have a payment processing relationship with WEX. |

| Payment processing transactions | Total number of purchases made by fleets that have a payment processing relationship with the Company where the Company maintains the receivable for the total purchase. |

| Processing costs | Expenses related to processing transactions, servicing customers and merchants, and costs of goods sold related to hardware and other product sales. |

| Purchase volume | Purchase volume in the Corporate Payments segment represents the total dollar value of all WEX-issued transactions that use WEX corporate card products and virtual card products. Purchase volume in the Benefits segment represents the total dollar value of all transactions where interchange is earned by WEX. |

| Revolving Credit Facility | The Company’s secured revolving credit facility under the Amended and Restated Credit Agreement. |

| SaaS | Software-as-a-Service |

| Segment adjusted operating income ("AOI") | A non-GAAP measure that adjusts operating income to exclude specified items that the Company’s management excludes in evaluating segment performance, including unallocated corporate expenses, acquisition-related intangible amortization, other acquisition and divestiture related items, debt restructuring costs, stock-based compensation, other costs and certain non-recurring or non-cash operating charges that are not core to our operations, as applicable depending on the period presented. |

| Segment adjusted operating income ("AOI") margin | Segment adjusted operating income margin is calculated by dividing segment adjusted operating income by segment revenue. |

| Service fees | Costs incurred from third-party networks utilized to deliver payment solutions and other third-parties utilized in performing services directly related to generating revenue. |

| Tender Offer | The Company’s modified “Dutch auction” tender offer, that was completed on March 31, 2025, in which the Company purchased for cash $750 million in value of shares of its common stock upon the terms and subject to the conditions described in that certain Schedule TO and the exhibits thereto, that were originally filed by the Company with the SEC on February 26, 2025 and subsequently amended. |

| Total volume | Includes purchases on WEX-issued accounts as well as purchases issued by others, but using a WEX platform. |

| WEX | WEX Inc., and all of its subsidiaries that are consolidated under accounting principles generally accepted in the United States, unless otherwise indicated or required by the context. |

Exhibit 1

Reconciliation of Non-GAAP Measures

(in millions, except per share data)

(unaudited)

Reconciliation of GAAP Net Income Attributable to Shareholders to Adjusted Net Income Attributable to Shareholders

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | | For the three months ended | | | | For the twelve months ended |

| | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 |

| Net income attributable to shareholders | | $ | 68.0 | | $ | 95.3 | | $ | 18.4 | | $ | 84.9 | | $ | 65.8 | | $ | 77.0 | | $ | 102.9 | | $ | 63.9 | | $ | 71.5 | | | | $ | 266.6 | | $ | 309.6 | |

| Unrealized (gain) loss on financial instruments | | $ | 14.5 | | $ | (2.2) | | $ | 7.8 | | $ | 10.3 | | $ | 0.2 | | $ | 0.2 | | $ | (0.9) | | $ | 0.8 | | $ | (0.4) | | | | $ | 30.4 | | $ | 0.2 | |

| Net foreign currency (gain) loss | | $ | 1.4 | | $ | 0.2 | | $ | 7.8 | | $ | (14.3) | | $ | 12.5 | | $ | 0.4 | | $ | (3.2) | | $ | 16.4 | | $ | 3.1 | | | | $ | (4.9) | | $ | 26.1 | |

| Change in fair value of contingent consideration | | $ | 1.8 | | $ | 1.2 | | $ | 3.2 | | $ | 2.3 | | $ | 1.7 | | $ | 1.7 | | $ | 0.1 | | $ | 3.0 | | $ | 0.8 | | | | $ | 8.5 | | $ | 6.5 | |

| Acquisition-related intangible amortization | | $ | 44.1 | | $ | 44.3 | | $ | 45.2 | | $ | 50.4 | | $ | 50.9 | | $ | 50.5 | | $ | 50.4 | | $ | 49.9 | | $ | 47.8 | | | | $ | 184.0 | | $ | 201.8 | |

| Other acquisition and divestiture related items | | $ | 1.1 | | $ | 1.4 | | $ | 5.1 | | $ | (1.0) | | $ | 3.2 | | $ | 3.8 | | $ | 2.4 | | $ | 2.8 | | $ | 2.5 | | | | $ | 6.6 | | $ | 12.1 | |

| Stock-based compensation | | $ | 26.1 | | $ | 36.5 | | $ | 31.9 | | $ | 37.1 | | $ | 26.7 | | $ | 33.3 | | $ | 29.8 | | $ | 22.1 | | $ | 13.3 | | | | $ | 131.6 | | 111.9 | |

| Other costs | | $ | 4.5 | | $ | 9.0 | | $ | 15.1 | | $ | 17.0 | | $ | 5.8 | | $ | 19.4 | | $ | 12.6 | | $ | 11.1 | | $ | 14.8 | | | | $ | 45.6 | | 48.9 | |

| | | | | | | | | | | | | | |

| Debt restructuring and debt issuance cost amortization | | $ | 4.7 | | $ | 4.8 | | $ | 74.4 | | $ | 5.5 | | $ | 4.5 | | $ | 3.2 | | $ | 4.3 | | $ | 3.9 | | $ | 2.2 | | | | $ | 89.4 | | $ | 15.9 | |

| | | | | | | | | | | | | | |

| Tax related items | | $ | (20.4) | | $ | (31.2) | | $ | (32.1) | | $ | (28.4) | | $ | (24.7) | | $ | (25.5) | | $ | (20.9) | | $ | (31.1) | | $ | (17.2) | | | | $ | (112.1) | | $ | (102.2) | |

| Adjusted net income attributable to shareholders | | $ | 145.8 | | $ | 159.3 | | $ | 176.8 | | $ | 163.9 | | $ | 146.7 | | $ | 164.0 | | $ | 177.5 | | $ | 142.9 | | $ | 138.4 | | | | $ | 645.8 | | $ | 631.0 | |

| ANI per Diluted Share | | $ | 3.31 | | $ | 3.63 | | $ | 4.05 | | $ | 3.82 | | $ | 3.46 | | $ | 3.91 | | $ | 4.35 | | $ | 3.57 | | $ | 3.51 | | | | $ | 14.81 | | $ | 15.28 | |

Reconciliation of GAAP Operating Income to Total Segment Adjusted Operating Income and Adjusted Operating Income

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Unaudited) | | For the three months ended | | | | For the twelve months ended |

| | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 |

| Operating income | | $ | 154.3 | | $ | 159.4 | | $ | 174.9 | | $ | 158.5 | | $ | 164.5 | | $ | 168.1 | | $ | 196.4 | | $ | 157.3 | | $ | 157.3 | | | | $ | 647.1 | | $ | 686.3 | |

| Unallocated corporate expenses | | $ | 22.4 | | $ | 25.3 | | $ | 29.1 | | $ | 26.2 | | $ | 23.6 | | $ | 26.1 | | $ | 24.1 | | $ | 28.3 | | $ | 24.9 | | | | $ | 103.0 | | $ | 102.1 | |

| Acquisition-related intangible amortization | | $ | 44.1 | | $ | 44.3 | | $ | 45.2 | | $ | 50.4 | | $ | 50.9 | | $ | 50.5 | | $ | 50.4 | | $ | 49.9 | | $ | 47.8 | | | | $ | 184.0 | | $ | 201.8 | |

| Other acquisition and divestiture related items | | $ | 1.1 | | $ | 1.4 | | $ | 5.1 | | $ | (1.0) | | $ | 2.4 | | $ | 1.4 | | $ | 1.6 | | $ | 0.3 | | $ | 0.5 | | | | $ | 6.6 | | $ | 5.7 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Stock-based compensation | | $ | 26.1 | | $ | 36.5 | | $ | 31.9 | | $ | 37.1 | | $ | 26.7 | | $ | 33.3 | | $ | 29.8 | | $ | 22.1 | | $ | 13.3 | | | | $ | 131.6 | | 111.9 | |

| Other costs | | $ | 4.5 | | $ | 9.0 | | $ | 15.1 | | $ | 17.5 | | $ | 6.7 | | $ | 20.6 | | $ | 14.8 | | $ | 11.9 | | $ | 14.9 | | | | $ | 46.1 | | 53.9 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Total segment adjusted operating income | | $ | 252.5 | | $ | 275.9 | | $ | 301.3 | | $ | 288.7 | | $ | 274.9 | | $ | 299.9 | | $ | 317.1 | | $ | 269.8 | | $ | 258.7 | | | | $ | 1,118.4 | | $ | 1,161.7 | |

| Unallocated corporate expenses | | $ | (22.4) | | $ | (25.3) | | $ | (29.1) | | $ | (26.2) | | $ | (23.6) | | $ | (26.1) | | $ | (24.1) | | $ | (28.3) | | $ | (24.9) | | | | $ | (103.0) | | $ | (102.1) | |

| Adjusted operating income | | $ | 230.1 | | $ | 250.6 | | $ | 272.2 | | $ | 262.5 | | $ | 251.3 | | $ | 273.9 | | $ | 293.0 | | $ | 241.5 | | $ | 233.8 | | | | $ | 1,015.4 | | $ | 1,059.7 | |

The Company's non-GAAP adjusted operating income excludes acquisition-related intangible amortization, other acquisition and divestiture related items, debt restructuring costs, stock-based compensation, other costs and certain non-recurring or non-cash operating charges that are not core to our operations, as applicable depending on the period presented. Total segment adjusted operating income incorporates these same adjustments and further excludes unallocated corporate expenses.

The Company's non-GAAP adjusted net income, which similarly excludes the impact of all items excluded in adjusted operating income, further excludes unrealized gains and losses on financial instruments, net foreign currency gains and losses, debt issuance cost amortization, tax related items, and certain other non-operating items, as applicable depending on the period presented.

Although adjusted net income, adjusted operating income and total segment adjusted operating income are not calculated in accordance with GAAP, our management team believes these non-GAAP measures are integral to our reporting and planning processes and uses them to assess operating performance because they generally exclude financial results that are outside the normal course of our business operations or management’s control. These measures are also used to allocate capital and resources among our operating segments.

For the periods presented herein, the following items have been excluded in determining one or more non-GAAP measures for the following reasons:

•Exclusion of the non-cash, mark-to-market adjustments on financial instruments, including interest rate swap agreements and investment securities, helps management identify and assess trends in the Company’s underlying business that might otherwise be obscured due to quarterly non-cash earnings fluctuations associated with these financial instruments. Additionally, the non-cash, mark-to-market adjustments on financial instruments are difficult to forecast accurately, making comparisons across historical and future quarters difficult to evaluate;

•Net foreign currency gains and losses primarily result from the remeasurement to functional currency of cash, accounts receivable and accounts payable balances, certain intercompany transactions denominated in foreign currencies and any gain or loss on foreign currency hedges relating to these items. The exclusion of these items helps management compare changes in operating results between periods that might otherwise be obscured due to currency fluctuations;

•The change in fair value of contingent consideration, which is related to the acquisition of certain contractual rights to serve as custodian or sub-custodian to HSAs, is dependent upon changes in future interest rate assumptions and has no significant impact on the ongoing operations of the Company. Additionally, the non-cash, mark-to-market adjustments on financial instruments are difficult to forecast accurately, making comparisons across historical and future quarters difficult to evaluate;

•The Company considers certain acquisition-related costs, including certain financing costs, investment banking fees, warranty and indemnity insurance, certain integration-related expenses and amortization of acquired intangibles, as well as gains and losses from divestitures to be unpredictable, dependent on factors that may be outside of our control and unrelated to the continuing operations of the acquired or divested business or the Company. In addition, the size and complexity of an acquisition, which often drives the magnitude of acquisition-related costs, may not be indicative of such future costs. The Company believes that excluding acquisition-related costs and gains or losses on divestitures facilitates the comparison of our financial results to the Company’s historical operating results and to other companies in our industry;

•Stock-based compensation is different from other forms of compensation as it is a non-cash expense. For example, a cash salary generally has a fixed and unvarying cash cost. In contrast, the expense associated with an equity-based award is generally unrelated to the amount of cash ultimately received by the employee, and the cost to the Company is based on a stock-based compensation valuation methodology and underlying assumptions that may vary over time;

•Other costs are not consistently occurring and do not reflect expected future operating expense, nor do they provide insight into the fundamentals of current or past operations of our business. This also includes non-recurring professional service costs, costs related to certain identified initiatives, including restructuring and technology initiatives, to further streamline the business, improve the Company’s efficiency, create synergies and globalize the Company’s operations, all with an objective to improve scale and efficiency and increase profitability going forward.

•Impairment charges represent non-cash asset write-offs, which do not reflect recurring costs that would be relevant to the Company’s continuing operations. The Company believes that excluding these nonrecurring expenses facilitates the comparison of our financial results to the Company’s historical operating results and to other companies in its industry;

•Debt restructuring and debt issuance cost amortization, which for the year ended December 31, 2023 includes the loss on extinguishment of Convertible Notes, are unrelated to the continuing operations of the Company. Debt restructuring costs are not consistently occurring and do not reflect expected future operating expense, nor do they provide insight into the fundamentals of current or past operations of our business. In addition, since debt issuance cost amortization is dependent upon the financing method, which can vary widely company to company, we believe that excluding these costs helps to facilitate comparison to historical results as well as to other companies within our industry;

•The adjustments attributable to non-controlling interests, including adjustments to the redemption value of a non-controlling interest, have no significant impact on the ongoing operations of the business;

•The tax related items are the difference between the Company’s GAAP tax provision and a non-GAAP tax provision. Beginning in fiscal year 2024, the Company began utilizing a fixed annual projected long-term non-GAAP tax rate in order to provide better consistency across reporting periods. To determine this long-term projected tax rate, the Company performs a pro forma tax provision based upon the Company’s projected adjusted net income before taxes. The fixed annual projected long-term non-GAAP tax rate could be subject to change in future periods for a variety of reasons, including the rapidly evolving global tax environment, significant changes in our geographic earnings mix including due to acquisition activity, or other changes to our strategy or business operations; and

•The Company does not allocate certain corporate expenses to our operating segments, as these items are centrally controlled and are not directly attributable to any reportable segment.

Adjusted net income, adjusted operating income, and total segment adjusted operating income may be useful to investors as a means of evaluating our performance. However, because total segment adjusted operating income and adjusted net income are non-GAAP measures, they should not be considered as a substitute for, or superior to, operating income or net income as determined in accordance with GAAP. Total segment adjusted operating income and adjusted net income as used by WEX may not be comparable to similarly titled measures employed by other companies.

Reconciliation of GAAP Operating Cash Flow to Adjusted Free Cash Flow

The Company’s non-GAAP adjusted free cash flow is calculated as cash flows from operating activities, adjusted for net purchases of current investment securities, capital expenditures, net funding activity including the change in net deposits, net advances from the FHLB, and changes in borrowings under the BTFP and borrowed federal funds, and certain other adjustments. Although non-GAAP adjusted free cash flow is not calculated in accordance with GAAP, WEX believes that adjusted free cash flow is a useful measure for investors to further evaluate our results of operations because (i) adjusted free cash flow indicates the level of cash generated by the operations of the business, which excludes consideration paid on acquisitions, after appropriate reinvestment for recurring investments in property, equipment and capitalized software that are required to operate the business; (ii) net Funding Activity includes fluctuations in deposits and other borrowings primarily used as part of our accounts receivable funding strategy; (iii) purchases of current investment securities are made as a result of deposits gathered operationally; and (iv) WEX Bank cash balances may be increased or decreased for reasons other than matching operating activity. However, because adjusted free cash flow is a non-GAAP measure, it should not be considered as a substitute for, or superior to, operating cash flow as determined in accordance with GAAP. In addition, adjusted free cash flow as used by WEX may not be comparable to similarly titled measures employed by other companies.

The following table reconciles GAAP operating cash flow to adjusted free cash flow for the three and twelve-month periods presented:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | For the three months ended | | | | For the twelve months ended |

| (In millions) | | 3/31/23 | 6/30/23 | 9/30/23 | 12/31/23 | 3/31/24 | 6/30/24 | 9/30/24 | 12/31/24 | 3/31/25 | | | 12/31/23 | 12/31/24 |

| Operating Cash Flow, as reported | | $ | 27.1 | | $ | 72.4 | | $ | 46.5 | | $ | 761.9 | | $ | (153.3) | | $ | (7.0) | | $ | 3.3 | | $ | 638.4 | | $ | (481.6) | | | | $ | 907.9 | | $ | 481.4 | |

| Adjustments to operating cash flow, as reported: | | | | | | | | | | | | | | |

| Changes in WEX Bank Cash Balances | | $ | (46.7) | | $ | 71.4 | | $ | (83.5) | | $ | (23.6) | | $ | 188.9 | | $ | 69.6 | | $ | 125.3 | | $ | (104.7) | | $ | 67.7 | | | | $ | (82.4) | | $ | 279.1 | |

| Other | | $ | 1.5 | | $ | — | | $ | — | | $ | (50.0) | | $ | 67.1 | | $ | — | | $ | — | | $ | (33.1) | | $ | 58.8 | | | | $ | (48.5) | | $ | 34.0 | |

| | | | | | | | | | | | | | |

| Net Funding Activity | | $ | 971.8 | | $ | 385.9 | | $ | 294.8 | | $ | (214.4) | | $ | 205.0 | | $ | 214.8 | | $ | 372.2 | | $ | (139.3) | | $ | 375.5 | | | | $ | 1,438.2 | | $ | 652.7 | |

| Less: Purchases of Current Investment Securities, Net of Sales and Maturities | | $ | (1,026.8) | | $ | (220.8) | | $ | (56.6) | | $ | (256.8) | | $ | (282.9) | | $ | (25.6) | | $ | (276.3) | | $ | (153.2) | | $ | 28.3 | | | | $ | (1,561.0) | | $ | (738.0) | |

| Less: Capital Expenditures | | $ | (30.6) | | $ | (34.7) | | $ | (36.4) | | $ | (41.9) | | $ | (34.0) | | $ | (39.6) | | $ | (35.0) | | $ | (38.7) | | $ | (32.6) | | | | $ | (143.6) | | $ | (147.3) | |

| Adjusted Free Cash Flow | | $ | (103.7) | | $ | 274.2 | | $ | 164.9 | | $ | 175.2 | | $ | (9.2) | | $ | 212.2 | | $ | 189.5 | | $ | 169.5 | | $ | 16.2 | | | | $ | 510.6 | | $ | 562.0 | |