As filed with the Securities and Exchange Commission on January 3, 2024

Registration No. 333-274379

Delaware | | | 1531 | | | 93-1969003 |

(State or other jurisdiction of incorporation or organization) | | | (Primary Standard Industrial Classification Code Number) | | | (I.R.S. Employer Identification No.) |

Marc D. Jaffe Senet Bischoff Benjamin J. Cohen Latham & Watkins LLP 1271 Avenue of the Americas New York, New York 10022 Telephone: (212) 906-1200 Fax: (212) 751-4864 | | | Shane Tintle Michael Kaplan Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 Telephone: (212) 450-4000 |

Large accelerated filer | | | ☐ | | | Accelerated filer | | | ☐ |

Non-accelerated filer | | | ☒ | | | Smaller reporting company | | | ☐ |

Emerging growth company | | | ☒ | | | | |

| | | Per Share | | | Total | |

Initial public offering price | | | $ | | | $ |

Underwriting discount(1) | | | $ | | | $ |

Proceeds, before expenses, to Smith Douglas Homes Corp. | | | $ | | | $ |

(1) | We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See “Underwriting (conflicts of interest).” |

J.P. Morgan | | | BofA Securities | | | RBC Capital Markets | | | Wells Fargo Securities |

Wolfe | Nomura Alliance | | | Zelman Partners LLC | ||||||

Wedbush Securities | | | Fifth Third Securities | | | Regions Securities LLC | | | Whelan Advisory Capital Markets |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

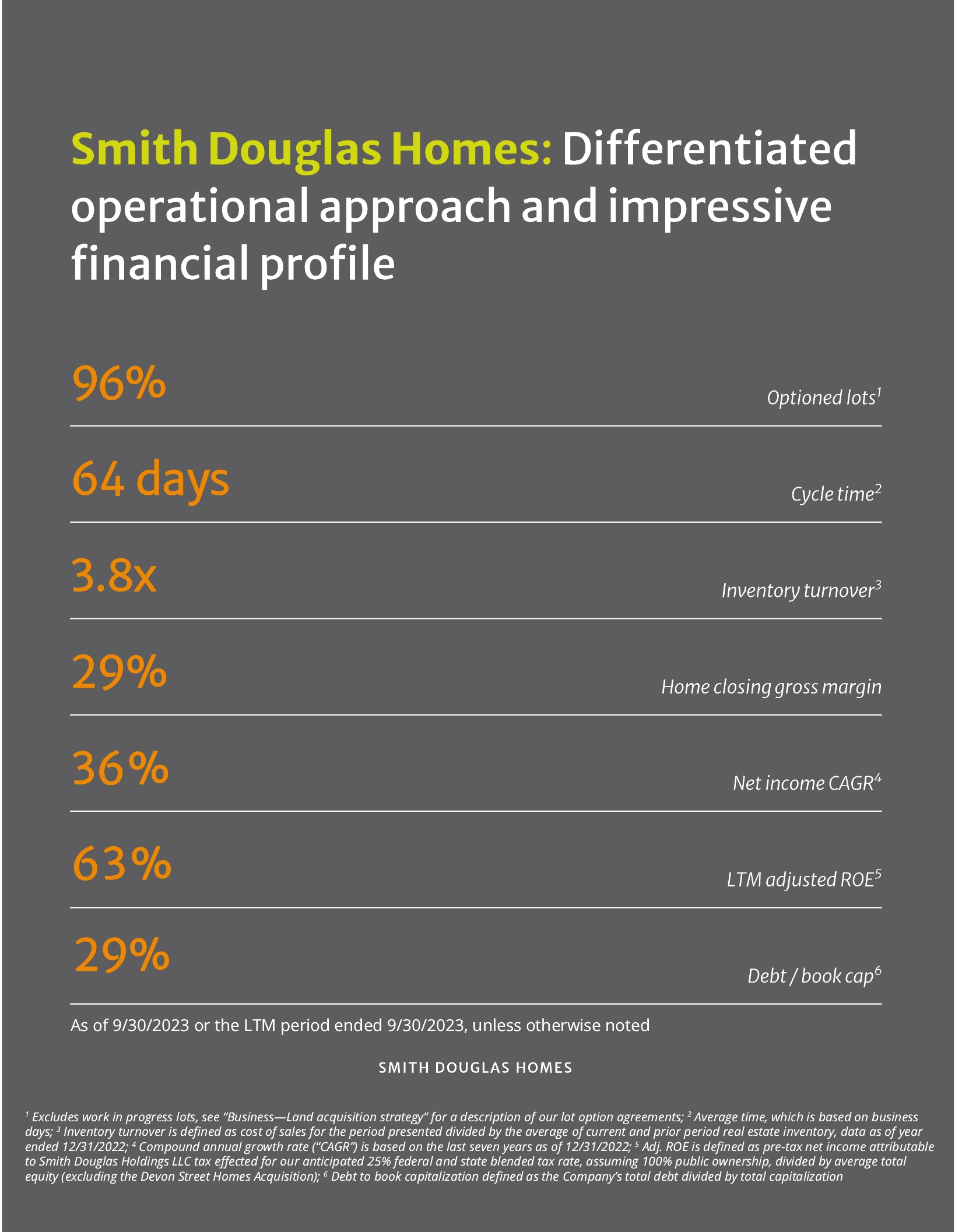

• | “adjusted return on equity” or “adj. ROE” refers, for us, to pre-tax income attributable to Smith Douglas Holdings LLC tax effected for our anticipated 25% federal and state blended tax rate, assuming 100% public ownership to adjust for the impact of taxes on earnings attributable to Smith Douglas Holdings LLC as if Smith Douglas Holdings LLC was a subchapter C corporation in the periods presented, divided by average total equity (excluding the Devon Street Homes Acquisition). For the public company homebuilders, “adjusted return on equity” or “adj. ROE” refers to net income divided by average total equity. |

• | “adjusted return on inventory” refers to, unless stated otherwise, pre-tax income attributable to Smith Douglas Holdings LLC tax effected for our anticipated 25% federal and state blended tax rate, assuming 100% public ownership to adjust for the impact of taxes on earnings attributable to Smith Douglas Holdings LLC as if Smith Douglas Holdings LLC was a subchapter C corporation in the periods presented, divided by the average of current and prior period closing real estate inventory (excluding the Devon Street Homes Acquisition). |

• | “Average sales price” or “ASP” refers to the average sales price of either our homes closed, our new home orders, or our backlog homes (at period end). |

• | “average total equity” refers to average of current and prior period closing total equity. |

• | “Basis Adjustments” refers to an allocable share (and increases thereto) of existing tax basis, in Smith Douglas Holdings LLC’s assets and tax basis adjustments with respect to such assets resulting from (a) Smith Douglas Homes Corp.’s purchase of LLC Interests from Smith Douglas Holdings LLC and each Continuing Equity Owner in connection with the Transactions, as described under “Use of proceeds”, (b) any future redemptions or exchanges of LLC Interests from the Continuing Equity Owners, (c) certain distributions (or deemed distributions) by Smith Douglas Holdings LLC, and (d) payments made under the Tax Receivable Agreement. |

• | “construction cycle time” refers, unless stated otherwise, to the number of business days between the start of the construction of foundations in a home and quality acceptance. |

• | “CAGR” refers to compound annual growth rate. |

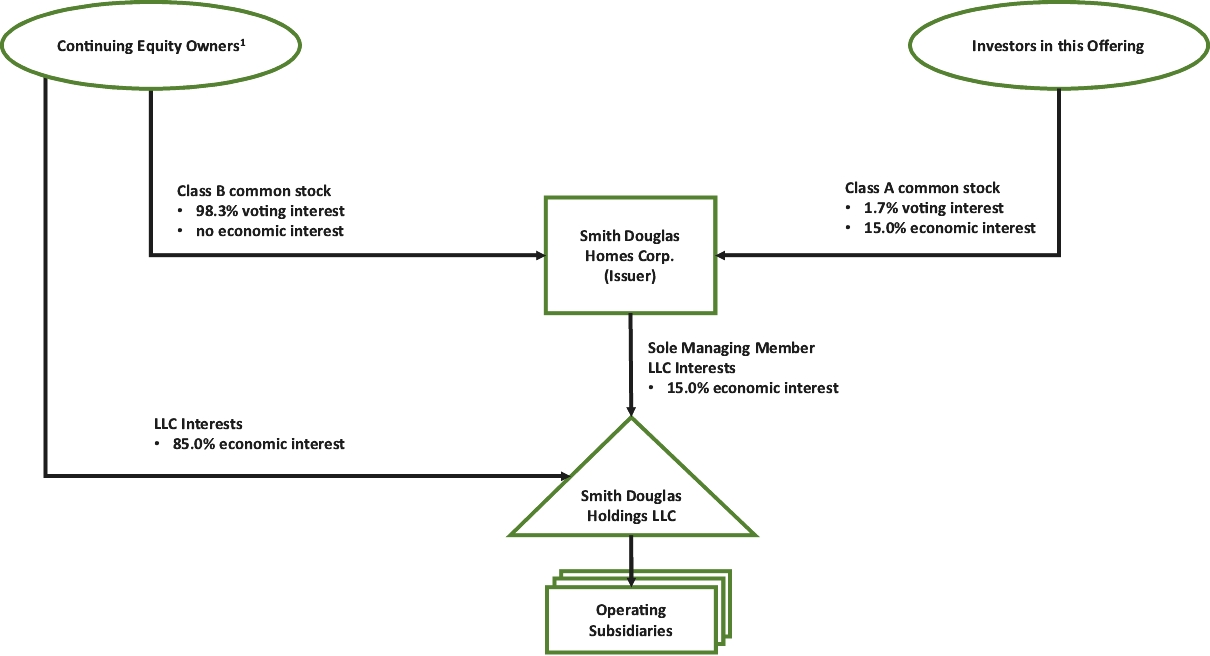

• | “Continuing Equity Owners” refers collectively to the owners of LLC Interests in Smith Douglas Holdings LLC prior to the consummation of the Transactions, who will also be holders of LLC Interests and our Class B common stock immediately following consummation of the Transactions, including the Founder Fund and GSB Holdings, who may, following the consummation of this offering, exchange at each of their respective options, in whole or in part from time to time, their LLC Interests, as applicable, for, at our election (determined solely by our independent directors (within the meaning of the Exchange rules) who are disinterested), cash or newly-issued shares of our Class A common stock as described in “Certain relationships and related person transactions—Smith Douglas LLC Agreement—Agreement in effect upon consummation of the Transactions.” In connection with an exchange of LLC Interests, a corresponding number of shares of Class B common stock shall be immediately and automatically transferred to Smith Douglas Homes Corp. for no consideration and canceled. |

• | “controlled lots” refers to lots that are either owned or held under an option to be acquired for the relevant time frame set forth in the option contracts. |

• | “Devon Street Homes” refers to Devon Street Homes, L.P. |

• | “Devon Street Homes Acquisition” refers to the transaction consummated on July 31, 2023, pursuant to which we acquired substantially all of the assets of Devon Street Homes. See “Management’s discussion and analysis of financial condition and results of operations—Devon Street Homes Acquisition.” |

• | “Exchange” refers to the New York Stock Exchange. |

• | “Founder Fund” refers to The Bradbury Family Trust II A U/A/D December 29, 2015, for which our founder and Executive Chairman, Tom Bradbury, is co-trustee. |

• | “GSB Holdings” refers to GSB Holdings LLC, for which our Chief Executive Officer, President, and Vice Chairman, Greg Bennett, is the sole member. |

• | “inventory turnover” refers, unless stated otherwise, to cost of sales divided by the average of current and prior period real estate inventory. |

• | “LLC Interests” refers to the membership units of Smith Douglas Holdings LLC, including those that we purchase with the net proceeds from this offering. |

• | “pro forma for the Transactions” refers, unless stated otherwise, to the unaudited condensed consolidated financial information of Smith Douglas Homes Corp. giving pro forma effect to the Transactions, including the offering and sale of 7,692,308 shares of Class A common stock in this offering at an initial public offering price of $19.50 per share, which is the midpoint of the price range set forth on the cover page of this prospectus and the proposed use of proceeds. |

• | “public company homebuilders” refers to Beazer Homes USA, Inc., Century Communities, Inc., Dream Finders Homes, Inc., D.R. Horton, Inc., Green Brick Partners, Inc., KB Home, Landsea Homes Corp., Lennar Corporation, LGI Homes, Inc., M.D.C. Holdings, Inc., Meritage Homes Corporation, M/I Homes, Inc., NVR, Inc., PulteGroup, Inc., Taylor Morrison Home Corporation, Toll Brothers, Inc., and TRI Pointe Group, Inc. |

• | “Section 704(c) Allocations” refers to disproportionate allocations (if any) of income and gain from inventory property held by Smith Douglas Holdings LLC as of the date of this offering under Section 704(c) of the Internal Revenue Code of 1986, as amended (the “Code”), resulting from our acquisition of LLC Interests from Smith Douglas Holdings LLC including in connection with the Transactions. |

• | “Sunset Date” refers to the date upon which the aggregate number of shares of Class B common stock then outstanding is less than 10% of the aggregate number of shares of Class A common stock and Class B common stock then outstanding. |

• | “Smith Douglas LLC Agreement” refers, as applicable, to Smith Douglas Holdings LLC’s amended and restated limited liability company agreement, as currently in effect, or to the amended and restated limited liability company agreement effective prior to the consummation of this offering, and as such agreement may thereafter be amended and/or restated. |

• | “Tax Receivable Agreement” refers to the Tax Receivable Agreement to be entered into by and among Smith Douglas Homes Corp., Smith Douglas Holdings LLC and the Continuing Equity Owners in connection with this offering, pursuant to which, among other things, Smith Douglas Homes Corp. will be required to pay to each Continuing Equity Owner 85% of certain tax benefits, if any, that it realizes (or in certain cases is deemed to realize) as a result of the tax benefits provided by Basis Adjustments, Section 704(c) Allocations, and certain other tax benefits (such as interest deductions) covered by the Tax Receivable Agreement as described in “Certain relationships and related person transactions—Tax Receivable Agreement.” |

• | “Transactions” refers to the organizational transactions described in the section titled “Our organizational structure” and this offering, and the application of the net proceeds therefrom. |

• | “we,” “us,” “our,” the “Company,” “Smith Douglas,” and similar references refer: (i) following the consummation of the Transactions, including this offering, to Smith Douglas Homes Corp., and, unless otherwise stated, all of its direct and indirect subsidiaries, including Smith Douglas Holdings LLC, and (ii) prior to the completion of the Transactions, including this offering, to Smith Douglas Holdings LLC. |

• | Smith Douglas Homes Corp. Other than the inception balance sheet, dated as of June 20, 2023 and the interim financial statements as of September 30, 2023, the historical financial information of Smith Douglas Homes Corp. has not been included in this prospectus as it is a newly incorporated entity, has had no business transactions or activities to date, besides our initial capitalization. |

• | Smith Douglas Holdings LLC. Because Smith Douglas Homes Corp. will have no interest in any operations other than those of Smith Douglas Holdings LLC, the historical financial information included in this prospectus is that of Smith Douglas Holdings LLC. |

• | adjusted home closing gross profit, defined as home closing revenue less cost of home closings, excluding capitalized interest charged to cost of home closings, impairment charges and adjustments resulting from the application of purchase accounting included in cost of sales, if applicable; |

• | adjusted home closing gross margin, defined as adjusted home closing gross profit as a percentage of home closing revenue; |

• | adjusted net income, defined as net income adjusted for the income tax expense effect of the pass-through entity taxable income of Smith Douglas Holdings LLC as if Smith Douglas Holdings LLC was a subchapter C corporation in periods presented. This assumption uses an effective tax rate of 25% for pass-through taxable income, which is our anticipated federal and state blended tax rate as a public company; |

• | EBITDA, defined as net income before (i) interest income, (ii) capitalized interest charged to cost of home closings, (iii) interest expense, (iv) income tax expense, and (v) depreciation; and |

• | EBITDA margin, defined as EBITDA as a percentage of home closing revenue. |

(1) | Based on Builder Magazine’s Top 100 list; achievements correspond to the year the ranking was based on. |

(2) | Purchase price of $82.9 million, primarily from cash on hand, availability under the Existing Credit Facility (as defined below), a three-year promissory note in the principal amount of $5.0 million payable to the seller, and approximately $3.0 million contingent consideration to the seller. We do not intend to use the proceeds from this offering for the payment of any outstanding amounts under the APA (as defined below) that may be paid pursuant to the contingent consideration. See “Management’s discussion and analysis of financial condition and results of operations—Devon Street Homes Acquisition.” |

• | our inability to successfully identify, secure, and control an adequate inventory of lots at reasonable prices; |

• | the tightening of mortgage lending standards and mortgage financing requirements; |

• | the housing market may not continue to grow at the same rate, or may decline; |

• | the availability, skill, and performance of trade partners; |

• | a shortage or increase in the costs of building materials could delay or increase the cost of home construction; |

• | efforts to impose joint employer liability on us for labor, safety, or worker’s compensation law violations committed by our trade partners; |

• | volatility in the credit and capital markets may impact our cost of capital and our ability to access necessary financing and the difficulty in obtaining sufficient capital could prevent us from acquiring lots for our development or increase costs and delays in the completion of our homebuilding expenditures; |

• | no market currently exists for our Class A common stock, and an active, liquid trading market for our Class A common stock may not develop, which may cause our Class A common stock to trade at a discount from the initial offering price and make it difficult for you to sell the Class A common stock you purchase; |

• | we cannot predict the effect our dual class structure may have on the market price of our Class A common stock; |

• | the Tax Receivable Agreement requires us to make cash payments to the Continuing Equity Owners in respect of certain tax benefits to which we may become entitled, and we expect that such payments will be substantial; |

• | our organizational structure, including the Tax Receivable Agreement, confers certain benefits upon the Continuing Equity Owners that will not benefit holders of our Class A common stock to the same extent that it will benefit the Continuing Equity Owners; and |

• | the significant influence the Continuing Equity Owners will have over us after the Transactions, including control over decisions that require the approval of stockholders. |

• | we will amend and restate the existing limited liability company agreement of Smith Douglas Holdings LLC, which will become effective prior to the consummation of this offering, to, among other things, (i) recapitalize all existing ownership interests in Smith Douglas Holdings LLC into 44,871,794 LLC Interests (before giving effect to the use of proceeds described below), (ii) appoint Smith Douglas Homes Corp. as the sole managing member of Smith Douglas Holdings LLC upon its acquisition of LLC Interests in connection with this offering, and (iii) provide certain redemption rights to the Continuing Equity Owners; |

• | we will amend and restate Smith Douglas Homes Corp.’s certificate of incorporation to, among other things, provide (i) for Class A common stock, with each share of our Class A common stock entitling its holder to one vote per share on all matters presented to our stockholders generally, (ii) for Class B common stock, with each share of our Class B common stock entitling its holder to ten votes per share on all matters presented to our stockholders generally prior to the Sunset Date and from and after the occurrence of the Sunset Date each share of our Class B common stock will entitle its holder to one vote per share on all matters presented to our stockholders generally, (iii) that shares of our Class B common stock may only be held by the Continuing Equity Owners and their respective permitted transferees as described in “Description of capital stock—Common Stock—Class B common stock;” and (iv) for preferred stock, which can be issued by our board in one or more series without stockholder approval; |

• | we will issue 43,589,743 shares of our Class B common stock (after giving effect to the use of net proceeds as described below and assuming no exercise of the underwriters' option to purchase additional shares of Class A common stock) to the Continuing Equity Owners, which is equal to the number of LLC Interests held by such Continuing Equity Owners, at the time of such issuance of Class B common stock, for nominal consideration; |

• | we will issue 7,692,308 shares of our Class A common stock to the purchasers in this offering (or 8,846,154 shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock) in exchange for net proceeds of approximately $139.5 million (or approximately $160.4 million if the underwriters exercise in full their option to purchase additional shares of Class A common stock) based upon an assumed initial public offering price of $19.50 per share (which is the midpoint of the estimated price range set forth on the cover page of this prospectus), less the underwriting discount; |

• | use of the net proceeds from this offering (i) to purchase 6,410,257 newly issued LLC Interests for approximately $116.3 million directly from Smith Douglas Holdings LLC at a price per unit equal to the initial public offering price per share of Class A common stock in this offering less the underwriting discount; and (ii) to purchase 1,282,051 LLC Interests from the Continuing Equity Owners on a pro rata basis for $23.2 million in aggregate (or 2,435,897 LLC Interests for $44.2 million in aggregate if the underwriters exercise in full their option to purchase additional shares of Class A common stock) at a price per unit equal to the initial public offering price per share of Class A common stock in this offering less the underwriting discount; |

• | Smith Douglas Holdings LLC intends to use the net proceeds from the sale of LLC Interests to Smith Douglas Homes Corp. (i) to repay approximately $71.0 million of borrowings outstanding under our Existing Credit Facility, (ii) redeem all outstanding Class C Units and Class D Units of Smith Douglas Holdings LLC at par in aggregate for $2.6 million, (iii) repay $1.2 million in notes payable to certain related parties and (iv) if any remain, for general corporate purposes as described under “Use of proceeds” and “Certain relationships and related person transactions;” and |

• | Smith Douglas Homes Corp. will enter into (i) the Registration Rights Agreement with our Continuing Equity Owners and (ii) the Tax Receivable Agreement with Smith Douglas Holdings LLC and the Continuing Equity Owners. For a description of the terms of the Registration Rights Agreement and the Tax Receivable Agreement, see “Certain relationships and related person transactions.” |

• | Smith Douglas Homes Corp. will be a holding company and its principal asset will consist of LLC Interests it acquires directly from Smith Douglas Holdings LLC and from each Continuing Equity Owner; |

• | Smith Douglas Homes Corp. will be the sole managing member of Smith Douglas Holdings LLC and will control the business and affairs of Smith Douglas Holdings LLC; |

• | Smith Douglas Homes Corp. will own, directly or indirectly, 7,692,308 LLC Interests of Smith Douglas Holdings LLC, representing approximately 15.0% of the economic interest in Smith Douglas Holdings LLC (or 8,846,154 LLC Interests, representing approximately 17.3% of the economic interest in Smith Douglas Holdings LLC if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

• | the Continuing Equity Owners will own (i) 43,589,743 LLC Interests of Smith Douglas Holdings LLC, representing approximately 85.0% of the economic interest in Smith Douglas Holdings LLC (or 42,435,897 LLC Interests, representing approximately 82.7% of the economic interest in Smith Douglas Holdings LLC if the underwriters exercise in full their option to purchase additional shares of Class A common stock) and (ii) 43,589,743 shares of Class B common stock of Smith Douglas Homes Corp., representing approximately 98.3% of the combined voting power of all of Smith Douglas Homes Corp.’s common stock (or 42,435,897 shares of Class B common stock of Smith Douglas Homes Corp., representing approximately 98.0% of the combined voting power if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

• | the purchasers in this offering will own (i) 7,692,308 shares of Class A common stock of Smith Douglas Homes Corp. (or 8,846,154 shares of Class A common stock of Smith Douglas Homes Corp. if the underwriters exercise in full their option to purchase additional shares of Class A common stock), representing approximately 1.7% of the combined voting power of all of Smith Douglas Homes Corp.’s common stock and 100% of the economic interest in Smith Douglas Homes Corp. (or approximately 2.0% of the combined voting power and 100% of the economic interest if the underwriters exercise in full their option to purchase additional shares of Class A |

• | our Class A common stock and Class B common stock will have what is commonly referred to as a “high/low vote structure,” which means that shares of our Class B common stock will initially have ten votes per share and our Class A common stock will have one vote per share. Upon the occurrence of the Sunset Date, each share of Class B common stock will then be entitled to one vote per share. This high/low vote structure will enable the Continuing Equity Owners to control the outcome of matters submitted to our stockholders for approval, including the election of our directors, as well as the overall management and direction of our company. Furthermore, the Continuing Equity Owners will continue to exert a significant degree of influence, or actual control, over matters requiring stockholder approval. We believe that maintaining this control by the Continuing Equity Owners will help enable them to successfully guide the implementation of our Company’s growth strategies and strategic vision. Meanwhile, holders of our Class A common stock will have economic and voting rights similar to those of holders of common stock of non-Up-C structured public companies that have a high/low vote structure. See “Description of capital stock.” |

(1) | Includes Founder Fund and GSB Holdings. |

• | we are required to have only two years of audited financial statements and only two years of related selected financial data and management’s discussion and analysis of financial condition and results of operations disclosure; |

• | we are not required to engage an auditor to report on our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”); |

• | we are not required to comply with the requirement of the Public Company Accounting Oversight Board (“PCAOB”), regarding the communication of critical audit matters in the auditor’s report on the financial statements; |

• | we are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency,” and “say-on-golden parachutes;” and |

• | we are not required to comply with certain disclosure requirements related to executive compensation, such as the requirement to present a comparison of our Chief Executive Officer’s compensation to our median employee compensation. |

• | gives effect to the amendment and restatement of the Smith Douglas LLC Agreement that converts all existing ownership interests in Smith Douglas Holdings LLC into 44,871,794 LLC Interests, as well as the filing of our amended and restated certificate of incorporation; |

• | gives effect to the other Transactions, including the Refinancing, the consummation of this offering and proposed use of proceeds; |

• | excludes 2,051,282 shares of Class A common stock reserved for issuance under the 2024 Incentive Award Plan (the “2024 Plan”), as described under the caption “Executive compensation—Equity compensation plans—2024 Incentive Award Plan”, including approximately 472,820 shares of Class A common stock issuable pursuant to the settlement of restricted stock units that we will grant to certain of our directors, executive officers and other employees, including certain of our named executive officers, in connection with this offering as described in “Executive compensation—Narrative to summary compensation table—Equity compensation—IPO equity awards”; |

• | assumes an initial public offering price of $19.50 per share of Class A common stock, which is the midpoint of the estimated price range set forth on the cover page of this prospectus; and |

• | assumes no exercise by the underwriters of their option to purchase 1,153,846 additional shares of Class A common stock from us. |

| | | Smith Douglas Homes Corp. Pro Forma(1) | | | Historical Smith Douglas Holdings LLC | |||||||||||||

| | | Nine months ended September 30, | | | Year ended December 31, | | | Nine months ended September 30, | | | Year ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | (In thousands) | | | (Unaudited, in thousands) | | | (In thousands) | ||||||||||

Summary statement of income data: | | | | | | | | | | | | | ||||||

Home closing revenue | | | $594,591 | | | $863,241 | | | $547,304 | | | $531,944 | | | $755,353 | | | $518,863 |

Cost of home closings | | | 426,136 | | | 617,241 | | | 388,983 | | | 377,341 | | | 532,599 | | | 395,917 |

Home closing gross profit | | | 168,455 | | | 246,000 | | | 158,321 | | | 154,603 | | | 222,754 | | | 122,946 |

Selling, general, and administrative costs | | | 71,381 | | | 97,192 | | | 64,901 | | | 56,080 | | | 83,269 | | | 64,231 |

Equity in income from unconsolidated entities | | | (658) | | | (1,120) | | | (658) | | | (789) | | | (1,120) | | | (595) |

Interest expense | | | 808 | | | 1,016 | | | 795 | | | 528 | | | 734 | | | 1,733 |

Other (income) loss, net | | | (213) | | | (473) | | | (217) | | | (352) | | | (573) | | | 188 |

Forgiveness of Paycheck Protection Program Loan | | | — | | | — | | | — | | | — | | | — | | | (5,141) |

Income before income taxes | | | 97,137 | | | 149,385 | | | 93,500 | | | 99,136 | | | 140,444 | | | 62,530 |

Provision for income taxes | | | 3,643 | | | 5,602 | | | — | | | — | | | — | | | — |

Net income | | | 93,494 | | | 143,783 | | | $93,500 | | | $99,136 | | | $140,444 | | | $62,530 |

Net income attributable to noncontrolling interests | | | 79,470 | | | 122,216 | | | | | | | | | ||||

Net income attributable to Smith Douglas Homes Corp. | | | $14,024 | | | $21,567 | | | | | | | | | ||||

Pro forma per share data: | | | | | | | | | | | | | ||||||

Pro forma net income per share: | | | | | | | | | | | | | ||||||

Basic and diluted | | | $1.77 | | | $2.80 | | | | | | | | | ||||

Pro forma weighted-average shares used to compute pro forma net income per share: | | | | | | | | | | | | | ||||||

Basic and diluted | | | 7,908,718 | | | 7,692,308 | | | | | | | | | ||||

| | | Smith Douglas Homes Corp. Pro Forma(1) | | | Historical Smith Douglas Holdings LLC | |||||||

| | | As of September 30, | | | As of September 30, | | | As of December 31, | ||||

| | | 2023 | | | 2023 | | | 2022 | | | 2021 | |

| | | (In thousands) | | | (Unaudited, in thousands) | | | (In thousands) | ||||

Summary balance sheet data: | | | | | | | | | ||||

Cash and cash equivalents | | | $51,938 | | | $10,440 | | | $29,601 | | | $25,340 |

Total assets | | | 375,451 | | | 329,476 | | | 223,372 | | | 201,188 |

Notes payable | | | 5,000 | | | 76,000 | | | 15,000 | | | 72,000 |

Total liabilities | | | 78,585 | | | 141,692 | | | 58,861 | | | 105,672 |

Members’ equity | | | | | 187,784 | | | 164,511 | | | 95,516 | |

Equity attributable to Smith Douglas Homes Corp. | | | 44,537 | | | | | | | |||

Noncontrolling interests | | | 252,329 | | | | | | | |||

Total stockholders’/members’ equity | | | 296,866 | | | 187,784 | | | 164,511 | | | 95,516 |

Total liabilities and stockholders’/members’ equity | | | $375,451 | | | $329,476 | | | $223,372 | | | $201,188 |

| | | Smith Douglas Homes Corp. Pro Forma(1) | | | Historical Smith Douglas Holdings LLC | |||||||||||||

| | | Nine months ended September 30, | | | Year ended December 31, | | | Nine months ended September 30, | | | Year ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | (In thousands) | | | (Unaudited, in thousands) | | | (In thousands) | ||||||||||

Summary statements of cash flows data: | | | | | | | | | | | | | ||||||

Net cash provided by operating activities | | | | | | | $54,958 | | | $58,105 | | | $132,095 | | | $30,870 | ||

Net cash (used in) provided by investing activities | | | | | | | (75,631) | | | 798 | | | 361 | | | 847 | ||

Net cash (used in) provided by financing activities | | | | | | | 1,512 | | | (67,124) | | | (128,195) | | | (38,541) | ||

Net (decrease) increase in cash and cash equivalents | | | | | | | (19,161) | | | (8,221) | | | 4,261 | | | (6,824) | ||

Other financial data(2): | | | | | | | | | | | | | ||||||

Home closing gross profit(3) | | | $168,455 | | | $246,000 | | | $158,321 | | | $154,603 | | | $222,754 | | | $122,946 |

Adj. home closing gross profit(5) | | | $170,170 | | | $249,040 | | | $159,823 | | | $156,444 | | | $225,511 | | | $124,981 |

Home closing gross margin(4) | | | 28.3% | | | 28.5% | | | 28.9% | | | 29.1% | | | 29.5% | | | 23.7% |

Adj. home closing gross margin(4) | | | 28.6% | | | 28.9% | | | 29.2% | | | 29.4% | | | 29.9% | | | 24.1% |

Adj. net income(5) | | | $72,853 | | | $112,039 | | | $70,125 | | | $74,352 | | | $105,333 | | | $46,898 |

EBITDA(5) | | | $100,403 | | | $154,325 | | | $96,479 | | | $102,155 | | | $144,707 | | | $67,284 |

Net income margin | | | 15.7% | | | 16.7% | | | 17.1% | | | 18.6% | | | 18.6% | | | 12.1% |

EBITDA margin(4)(5) | | | 16.9% | | | 17.9% | | | 17.6% | | | 19.2% | | | 19.2% | | | 13.0% |

Other operating data(2): | | | | | | | | | | | | | ||||||

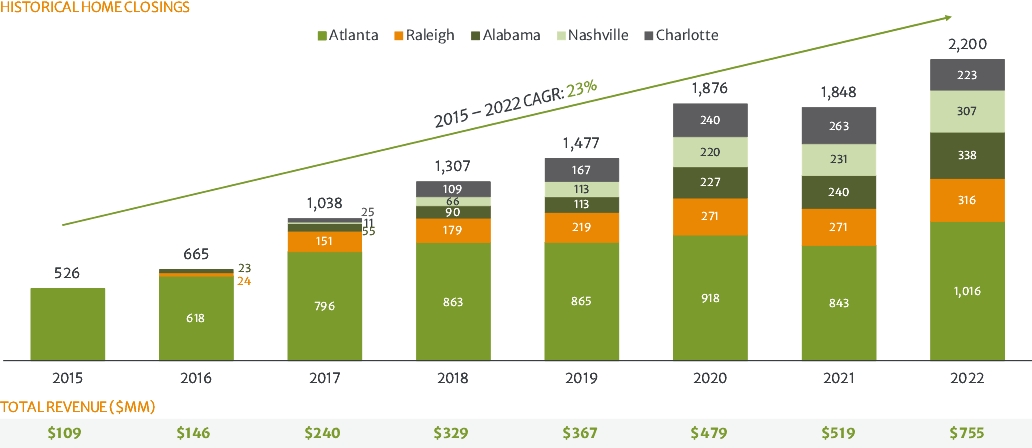

Home closings | | | 1,789 | | | 2,524 | | | 1,643 | | | 1,575 | | | 2,200 | | | 1,848 |

ASP of homes closed | | | $332 | | | $342 | | | $333 | | | $338 | | | $343 | | | $281 |

Net new home orders | | | 1,996 | | | 2,132 | | | 1,844 | | | 1,504 | | | 1,928 | | | 1,920 |

Contract value of net new home orders | | | $663,690 | | | $735,382 | | | $614,683 | | | $535,455 | | | $667,530 | | | $597,761 |

ASP of net new home orders | | | $333 | | | $345 | | | $333 | | | $356 | | | $346 | | | $311 |

Cancellation rate(6) | | | 10.7% | | | 14.7% | | | 9.5% | | | 9.0% | | | 10.9% | | | 6.7% |

Backlog homes (period end)(7) | | | 1,042 | | | 841 | | | 1,042 | | | 972 | | | 771 | | | 1,043 |

Contract value of backlog homes (period end) | | | $350,439 | | | $282,168 | | | $350,439 | | | $349,542 | | | $258,718 | | | $345,521 |

ASP of backlog homes (period end) | | | $336 | | | $336 | | | $336 | | | $360 | | | $336 | | | $331 |

Active communities (period end)(8) | | | 62 | | | 64 | | | 62 | | | 55 | | | 53 | | | 52 |

Controlled lots (period end): | | | | | | | | | | | | | ||||||

Homes under construction | | | 905 | | | 778 | | | 905 | | | 792 | | | 623 | | | 711 |

Owned lots | | | 395 | | | 589 | | | 395 | | | 384 | | | 342 | | | 319 |

Optioned lots | | | 10,279 | | | 8,665 | | | 10,279 | | | 9,390 | | | 7,848 | | | 9,840 |

Total controlled lots | | | 11,579 | | | 10,032 | | | 11,579 | | | 10,566 | | | 8,813 | | | 10,870 |

(1) | Pro forma for the Transactions, including the Refinancing and the Devon Street Homes Acquisition. See “Unaudited pro forma condensed consolidated financial information.” |

(2) | For definitions and further information about how we calculate financial and operating data, including a reconciliation of adjusted home closing gross profit, adjusted net income, EBITDA, adjusted home closing gross margin, and EBITDA margin, please see “Management’s discussion and analysis of financial condition and results of operations—Reorganization transactions—Non-GAAP financial measures.” |

(3) | Home closing gross profit is home closing revenue less cost of home closings. |

(4) | Calculated as a percentage of home closing revenue. |

(5) | Adjusted home closing gross profit, adjusted home closing gross margin, adjusted net income, EBITDA, and EBITDA margin are included in this prospectus because they are non-GAAP financial measures used by management and our board of directors to assess our financial performance. For definitions of adjusted homes closing gross profit, adjusted home closing gross margin, adjusted net income, EBITDA, and EBITDA margin and reconciliations to our most directly comparable financial measures calculated and presented in accordance with GAAP, see “Management’s discussion and analysis of financial condition and results of operations—Reorganization transactions—Non-GAAP financial measures.” Our non-GAAP financial measures should not be considered in isolation from, or as substitutes for, financial information prepared in accordance with GAAP. Adjusted homes closing gross profit, adjusted home closing gross margin, adjusted net income, EBITDA, and EBITDA margin may be different than a similarly titled measure used by other companies. |

(6) | The cancellation rate is the total number of cancellations during the period divided by the total gross new home orders during the period. |

(7) | Backlog homes (period end) is the number of homes in backlog from the previous period plus the number of net new home orders generated during the current period minus the number of homes closed during the current period. |

(8) | A community becomes active once the model is completed or the community has its first sale. A community becomes inactive when it has fewer than two units remaining to sell. |

• | increases in short- and long-term interest rates; |

• | high inflation; |

• | supply-chain disruptions and the cost or availability of building materials; |

• | the availability of trade partners, vendors, or other third parties; |

• | housing affordability; |

• | the availability and cost of financing for homebuyers; |

• | federal and state income and real estate tax laws, including limitations on, or the elimination of, the deduction of mortgage interest or property tax payments; |

• | employment levels, job and personal income growth and household debt-to-income levels; |

• | consumer confidence generally and the confidence of potential homebuyers in particular; |

• | the ability of homeowners to sell their existing homes at acceptable prices; |

• | the U.S. and global financial systems and credit markets, including stock market and credit market volatility; |

• | inclement weather and natural and man-made disasters, including risks associated with global climate change, such as increased frequency or intensity of adverse weather events; |

• | environmental, health, and safety laws and regulations, and the environmental conditions of our properties; |

• | civil unrest, acts of terrorism, other acts of violence, threats to national security, global economic and political instability, and conflicts such as the conflict between Russia and Ukraine and the Israel-Hamas conflict (including any escalation or expansion), escalating global trade tensions, the adoption of trade restrictions, or a public health issue such as COVID-19 or another major epidemic or pandemic; |

• | mortgage financing programs and regulation of lending practices; |

• | housing demand from population growth, household formations and demographic changes (including immigration levels and trends or other costs of home ownership in urban and suburban migration); |

• | demand from foreign homebuyers for our homes; |

• | the supply of available new or existing homes and other housing alternatives; |

• | energy prices; and |

• | the supply of developable land in our markets and in the United States generally. |

• | allocation of expenses to and among different jurisdictions; |

• | changes to our assessment about our ability to realize, or in the valuation of, our deferred tax assets that are based on estimates of our future results, the prudence and feasibility of possible tax planning strategies, and the economic and political environments in which we do business; |

• | expected timing and amount of the release of any tax valuation allowances; |

• | tax effects of stock-based compensation; |

• | costs related to intercompany restructurings; |

• | changes in tax laws, regulations, or interpretations thereof; |

• | the outcome of current and future tax audits, examinations, or administrative appeals; |

• | lower than anticipated future earnings in jurisdictions where we have lower statutory tax rates and higher than anticipated future earnings in jurisdictions where we have higher statutory tax rates; and |

• | limitations or adverse findings regarding our ability to do business in some jurisdictions. |

• | making it more difficult for us to satisfy our obligations with respect to our debt or to our trade or other creditors; |

• | increasing our vulnerability to adverse economic or industry conditions; |

• | limiting our ability to obtain additional financing to fund capital expenditures and acquisitions, particularly when the availability of financing in the capital markets is limited; |

• | requiring a substantial portion of our cash flows from operations and the proceeds from this offering for the payment of interest on our debt and reducing our ability to use our cash flows and the proceeds from this offering to fund working capital, capital expenditures, acquisitions, and general corporate requirements; |

• | limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; and |

• | placing us at a competitive disadvantage to less leveraged competitors. |

• | results of operations that vary from the expectations of securities analysts and investors; |

• | results of operations that vary from those of our competitors; |

• | changes in expectations as to our future financial performance, including financial estimates and investment recommendations by securities analysts and investors; |

• | technology changes, changes in consumer behavior in our industry; |

• | security breaches related to our systems or those of our affiliates or strategic partners; |

• | changes in economic conditions for companies in our industry; |

• | changes in market valuations of, or earnings and other announcements by, companies in our industry; |

• | declines in the market prices of stocks generally, particularly those of residential construction; |

• | strategic actions by us or our competitors; |

• | announcements by us, our competitors or our strategic partners of significant contracts, new products, acquisitions, joint marketing relationships, joint ventures or other unconsolidated entities, other strategic relationships, or capital commitments; |

• | changes in general economic or market conditions or trends in our industry or the economy as a whole and, in particular, in the residential construction environment; |

• | changes in business or regulatory conditions; |

• | future sales of our Class A common stock or other securities; |

• | investor perceptions of the investment opportunity associated with our Class A common stock relative to other investment alternatives; |

• | the public’s response to press releases or other public announcements by us or third parties, including our filings with the SEC; |

• | announcements relating to litigation or governmental investigations; |

• | guidance, if any, that we provide to the public, any changes in this guidance, or our failure to meet this guidance; |

• | the development and sustainability of an active trading market for our stock; |

• | changes in accounting principles; and |

• | other events or factors, including those resulting from system failures and disruptions, natural or man-made disasters, extreme weather events, war, acts of terrorism, an outbreak of highly infectious or contagious diseases, such as COVID-19, or responses to these events. |

• | the ability of our board of directors to issue one or more series of preferred stock without stockholder approval; |

• | at any time prior to the Sunset Date, our stockholders may take action by consent without a meeting, and from and after the occurrence of the Sunset Date, our stockholders may not take action by consent without a meeting, but may only take action at a meeting of stockholders; |

• | vacancies on our board of directors will be able to be filled only by our board of directors and not by stockholders; |

• | advance notice procedures apply for stockholders to nominate candidates for election as directors or to bring matters before an annual meeting of stockholders; |

• | at any time prior to the Sunset Date, the Secretary (or other officer or our board of directors) at the request of any Continuing Equity Owner owning at least 5% of the voting power of all of the then outstanding shares of capital stock entitled to vote thereon may call a special meeting of stockholders, and from and after the occurrence of the Sunset Date, our stockholders will be unable to call a special meeting of stockholders; |

• | no cumulative voting in the election of directors; |

• | prior to the Sunset Date, directors may be removed at any time with or without cause upon the affirmative vote of the holders of a majority of the voting power of our outstanding shares of capital stock entitled to vote thereon, and from and after the occurrence of the Sunset Date, directors may be removed with or without cause and only upon the affirmative vote of holders of at least 66 2/3% of the voting power of our outstanding shares of capital stock entitled to vote thereon; and |

• | that certain provisions of amended and restated certificate of incorporation may be amended only by the affirmative vote of holder of at least 66 2/3% of the voting power of our then-outstanding capital stock entitled to vote thereon. |

• | the last day of its fiscal year following the fifth anniversary of the date of its initial public offering of common equity securities; |

• | the last day of its fiscal year in which it has annual gross revenue of $1.235 billion or more; |

• | the date on which it has, during the previous three-year period, issued more than $1 billion in nonconvertible debt; and |

• | the date on which it is deemed to be a “large accelerated filer,” which will occur at such time as we (i) have an aggregate worldwide market value of common equity securities held by non-affiliates of $700 million or more as of the last business day of its most recently completed second fiscal quarter, (ii) have been required to file annual and quarterly reports under the Exchange, for a period of at least 12 months, and (iii) have filed at least one annual report pursuant to the Exchange Act. |

• | not be required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes Oxley Act; |

• | not be required to hold a nonbinding advisory stockholder vote on executive compensation pursuant to Section 14A(a) of the Exchange Act; |

• | not be required to seek stockholder approval of any golden parachute payments not previously approved pursuant to Section 14A(b) of the Exchange Act; |

• | be exempt from the requirement of the Public Company Accounting Oversight Board (the “PCAOB”) regarding the communication of critical audit matters in the auditor’s report on the financial statements; and |

• | be subject to reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements. |

• | general market conditions, including inflation and rising interest rates; |

• | the market’s perception of our growth potential; |

• | with respect to acquisition and/or development financing, the market’s perception of the value of the land parcels to be acquired and/or developed; |

• | our current debt levels; |

• | our current and expected future earnings; |

• | our cash flow; and |

• | the market price per share of our Class A common stock. |

• | our ability to successfully identify, secure, and control an adequate inventory of lots at reasonable prices; |

• | our market opportunity and the potential growth of that market; |

• | our ability to expand into new regions; |

• | our strategy, expected outcomes, and growth prospects; |

• | trends in our operations, industry, and markets; |

• | our future profitability, indebtedness, liquidity, access to capital, and financial condition; |

• | the effects of seasonal trends on our results of operations; |

• | the increased expenses associated with being a public company; |

• | our ability to remain in compliance with extensive laws and regulations that apply to our business and operations; |

• | the effect our dual class structure may have on the market price of our Class A common stock; |

• | the completion of the concurrent Refinancing and |

• | the future trading prices of our Class A common stock. |

• | we will amend and restate the existing limited liability company agreement of Smith Douglas Holdings LLC, which will become effective prior to the consummation of this offering, to, among other things, (i) recapitalize all existing ownership interests in Smith Douglas Holdings LLC into 44,871,794 LLC Interests (before giving effect to the use of proceeds described below), (ii) appoint Smith Douglas Homes Corp. as the sole managing member of Smith Douglas Holdings LLC upon its acquisition of LLC Interests in connection with this offering, and (iii) provide certain redemption rights to the Continuing Equity Owners; |

• | we will amend and restate Smith Douglas Homes Corp.’s certificate of incorporation to, among other things, provide (i) for Class A common stock, with each share of our Class A common stock entitling its holder to one vote per share on all matters presented to our stockholders generally; (ii) for Class B common stock, with each share of our Class B common stock entitling its holder to ten votes per share on all matters presented to our stockholders generally prior to the Sunset Date and from and after the occurrence of the Sunset Date each share of our Class B common stock will entitle its holder to one vote per share on all matters presented to our stockholders generally; (iii) that shares of our Class B common stock may only be held by the Continuing Equity Owners and their respective permitted transferees as described in “Description of capital stock—Common stock—Class B common stock;” and (iv) for preferred stock, which can be issued by our board in one or more series without stockholder approval; |

• | we will issue 43,589,743 shares of our Class B common stock (after giving effect to the use of net proceeds as described below and assuming no exercise of the underwriters’ option to purchase additional shares of Class A common stock) to the Continuing Equity Owners at the time of such issuance of Class B common stock, which is equal to the number of LLC Interests held by such Continuing Equity Owners, for nominal consideration; |

• | we will issue 7,692,308 shares of our Class A common stock to the purchasers in this offering (or 8,846,154 shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock) in exchange for net proceeds of approximately $139.5 million (or approximately $160.4 million if the underwriters exercise in full their option to purchase additional shares of Class A common stock) based upon an assumed initial public offering price of $19.50 per share (which is the midpoint of the estimated price range set forth on the cover page of this prospectus), less the underwriting discount; |

• | we will use the net proceeds from this offering (i) to purchase 6,410,257 newly issued LLC Interests for approximately $116.3 million directly from Smith Douglas Holdings LLC at the initial public offering price less the underwriting discount; and (ii) to purchase 1,282,051 LLC Interests from the Continuing Equity Owners on a pro rata basis for $23.2 million in aggregate (or 2,435,897 LLC Interests for $44.2 million in aggregate if the underwriters exercise in full their option to purchase additional shares of Class A common stock) at a price per unit equal to the initial public offering price per share of Class A common stock in this offering less the underwriting discount; |

• | Smith Douglas Holdings LLC intends to use the net proceeds from the sale of LLC Interests to Smith Douglas Homes Corp. (i) to repay approximately $71.0 million of borrowings outstanding under the Existing Credit Facility as part of the Refinancing, (ii) to redeem all outstanding Class C Units and Class D Units of Smith Douglas Holdings LLC at par in aggregate for $2.6 million, (ii) to repay $1.2 million in notes payable to certain related parties, and (iv) if any remain, for general corporate purposes as described under “Use of proceeds” and “Certain relationships and related person transactions”; and |

• | Smith Douglas Homes Corp. will enter into (i) the Registration Rights Agreement with certain of the Continuing Equity Owners and (ii) the Tax Receivable Agreement with Smith Douglas Holdings LLC and the Continuing Equity Owners. For a description of the terms of the Registration Rights Agreement and the Tax Receivable Agreement, see “Certain relationships and related person transactions.” |

• | Smith Douglas Homes Corp. will be a holding company and its principal asset will consist of LLC Interests it acquires directly from Smith Douglas Holdings LLC and from each Continuing Equity Owner; |

• | Smith Douglas Homes Corp. will be the sole managing member of Smith Douglas Holdings LLC and will control the business and affairs of Smith Douglas Holdings LLC; |

• | Smith Douglas Homes Corp. will own, directly or indirectly, 7,692,308 LLC Interests of Smith Douglas Holdings LLC, representing approximately 15.0% of the economic interest in Smith Douglas Holdings LLC (or 8,846,154 LLC Interests, representing approximately 17.3% of the economic interest in Smith Douglas Holdings LLC if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

• | the Continuing Equity Owners will own (i) 43,589,743 LLC Interests of Smith Douglas Holdings LLC, representing approximately 85.0% of the economic interest in Smith Douglas Holdings LLC (or 42,435,897 LLC Interests, representing approximately 82.7% of the economic interest in Smith Douglas Holdings LLC if the underwriters exercise in full their option to purchase additional shares of Class A common stock) and (ii) 43,589,743 shares of Class B common stock of Smith Douglas Homes Corp., representing approximately 98.3% of the combined voting power of all of Smith Douglas Homes Corp.’s common stock (or 42,435,897 shares of Class B common stock of Smith Douglas Homes Corp., representing approximately 98.0% if the underwriters exercise in full their option to purchase additional shares of Class A common stock); and |

• | the purchasers in this offering will own (i) 7,692,308 shares of Class A common stock of Smith Douglas Homes Corp. (or 8,846,154 shares of Class A common stock of Smith Douglas Homes Corp. if the underwriters exercise in full their option to purchase additional shares of Class A common stock), representing approximately 1.7% of the combined voting power of all of Smith Douglas Homes Corp.’s common stock and approximately 100% of the economic interest in Smith Douglas Homes Corp. (or approximately 2.0% of the combined voting power and approximately 100% of the economic interest if the underwriters exercise in full their option to purchase additional shares of Class A common stock), and (ii) through Smith Douglas Homes Corp.’s ownership of LLC Interests, indirectly will hold approximately 15.0% of the economic interest in Smith Douglas Holdings LLC (or approximately 17.3% of the economic interest in Smith Douglas Holdings LLC if the underwriters exercise in full their option to purchase additional shares of Class A common stock). |

(1) | Includes Founder Fund and GSB Holdings. |

• | of Smith Douglas Holdings LLC on a historical basis; and |

• | of Smith Douglas Homes Corp. and its subsidiaries, pro forma for the Transactions, including the sale of the shares of Class A common stock in this offering at an assumed initial public offering price of $19.50 per share (which is the midpoint of the estimated price range set forth on the cover page of this prospectus), after deducting the underwriting discount, and the application of the net proceeds therefrom as described under “Use of proceeds,” including the Refinancing. |

As of September 30, 2023 (in thousands, except per share and share amounts) | | | Smith Douglas Holdings LLC Historical | | | Smith Douglas Homes Corp. Pro Forma(1) |

Cash and cash equivalents | | | $10,440 | | | $51,938 |

Debt(2) | | | $76,000 | | | $5,000 |

Total members’ equity | | | 187,784 | | | — |

Stockholders’ equity | | | — | | | |

Class A common stock, par value $0.0001 per share; no shares authorized, issued and outstanding, actual; 250,000,000 shares authorized, 7,692,308 shares issued and outstanding, Smith Douglas Homes Corp. pro forma | | | — | | | 1 |

Class B common stock, par value $0.0001 per share; no shares authorized, issued and outstanding, actual; 100,000,000 shares authorized, 43,589,743 shares issued and outstanding, Smith Douglas Homes Corp. pro forma | | | — | | | 7 |

Preferred stock $0.0001 par value per share, no shares authorized, issued and outstanding, actual; 10,000,000 authorized, no shares issued and outstanding, pro forma | | | — | | | — |

Additional paid-in-capital | | | — | | | 44,529 |

Equity attributable to Smith Douglas Homes Corp. | | | — | | | 44,537 |

Non-controlling interest attributable to Smith Douglas LLC | | | — | | | 252,329 |

Total stockholders’ and members’ equity | | | 187,784 | | | 296,866 |

Total capitalization | | | $263,784 | | | $301,866 |

(1) | A $1.00 increase (decrease) in the assumed initial public offering price of $19.50 per share, which is the midpoint of the price range listed on the cover page of this prospectus, would increase (decrease) the pro forma amount of each of cash and cash equivalents, additional paid-in capital, total stockholders’ equity, and total capitalization by approximately $7.2 million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions. |

(2) | As of September 30, 2023, we had $71.0 million of borrowings outstanding under the Existing Credit Facility and $5.0 million outstanding under the three-year promissory note payable to the seller of the Devon Street Homes Acquisition. The Existing Credit Facility is a $175.0 million unsecured revolving credit facility, which includes a $25.0 million accordion feature, subject to additional commitments, and provides that up to $10.0 million may be used for letters of credit. Concurrently with, and conditioned upon, the closing of this offering, we intend to enter into the Amended Credit Facility and, as part of the Refinancing, pay down $71.0 million outstanding under our Existing Credit Facility. For a further description of our Existing Credit Facility, see “Management’s discussion and analysis of financial condition and results of operations—Liquidity and capital resources—Existing Credit Facility” and “Use of proceeds.” |

Assumed initial public offering price per share | | | | | $19.50 | |

Pro forma net tangible book value as of September 30, 2023 before this offering | | | $3.82 | | | |

Increase per share attributable to new investors in this offering | | | $1.65 | | | |

Pro forma net tangible book value per share after this offering | | | | | 5.47 | |

Dilution per share to new Class A common stock investors in this offering | | | | | $14.03 |

(in thousands) | | | Shares Purchased | | | Total Consideration | | | Average Price Per Share | ||||||

| | Number | | | Percent | | | Amount | | | Percent | | ||||

Continuing Equity Owners | | | 43,590 | | | 85.0% | | | $5,773 | | | 3.7% | | | $0.13 |

New public investors | | | 7,692 | | | 15.0% | | | 150,000 | | | 96.3% | | | $19.50 |

Total | | | 51,282 | | | 100% | | | $155,773 | | | 100% | | | $3.04 |

• | the percentage of shares of Class A common stock held by the Continuing Equity Owners will decrease to approximately 82.7% of the total number of shares of our Class A common stock outstanding after this offering; and |

• | the number of shares of Class A common stock held by new investors in this offering will increase to 8,846,154, or approximately 17.3% of the total number of shares of our Class A common stock outstanding after this offering. |

• | The acquisition of Devon Street Homes on July 31, 2023 (the “Acquisition Date”), for a purchase price of approximately $82.9 million funded by $2.9 million of cash on hand, $72.0 million of draws on our Existing Credit Facility, $5.0 million from the issuance of a three-year promissory note payable to the seller, and approximately $3.0 million of contingent consideration to the seller. We do not intend to use the proceeds from this offering for the payment of any outstanding amounts under the APA that may be paid pursuant to the contingent consideration. |

• | the amendment and restatement of the existing limited liability company agreement of Smith Douglas Holdings LLC, which will become effective prior to the consummation of this offering, to, among other things, (i) appoint Smith Douglas Homes Corp. as the sole managing member of Smith Douglas Holdings LLC upon its acquisition of LLC Interests in connection with this offering and (ii) provide certain redemption rights to the Continuing Equity Owners; |

• | the amendment and restatement of Smith Douglas Homes Corp’s certificate of incorporation to, among other things, provide (i) for Class A common stock, with each share of our Class A common stock entitling its holder to one vote per share on all matters presented to our stockholders generally and (ii) for Class B common stock, with each share of our Class B common stock entitling its holder to ten votes per share on all matters presented to our stockholders generally prior to the Sunset Date and from and after the occurrence of the Sunset Date each share of our Class B common stock will entitle its holder to one vote per share on all matters presented to our stockholders generally, and that shares of our Class B common stock may only be held by the Continuing Equity Owners and their respective permitted transferees as described in “Description of capital stock—Common stock—Class B common stock;” |

• | the issuance of 43,589,743 shares of our Class B common stock to the Continuing Equity Owners, which is equal to the number of LLC Interests held by such Continuing Equity Owners, for nominal consideration; and |

• | the entrance into the Tax Receivable Agreement with Smith Douglas Holdings LLC and the Continuing Equity Owners that will provide for the payment by Smith Douglas Homes Corp. to the Continuing Equity Owners of 85% of the amount of tax benefits, if any, that Smith Douglas Homes Corp. actually realizes (or in some circumstances is deemed to realize) related to certain Basis Adjustments, Section 704(c) Allocations, and payments made under the Tax Receivable Agreement. See “Certain relationships and related person transactions—Tax Receivable Agreement” for a description of the Tax Receivable Agreement. |

• | issuance of 7,692,308 shares of our Class A common stock to the purchasers in this offering (or 8,846,154 shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock) in exchange for net proceeds of approximately $139.5 million (or approximately $160.4 million if the underwriters exercise in full their option to purchase additional shares of Class A common stock) based upon an assumed initial public offering price of $19.50 per share (which is the midpoint of the estimated price range set forth on the cover page of this prospectus), less the underwriting discount; |

• | use of the net proceeds from this offering (i) to purchase 6,410,257 newly issued LLC Interests for approximately $116.3 million directly from Smith Douglas Holdings LLC at a price per unit equal to the initial public offering |

• | the use by Smith Douglas Holdings LLC of the proceeds from the sale of its LLC Interests to us to repay existing indebtedness under our Existing Credit Facility, to redeem all outstanding Class C Units and Class D Units of Smith Douglas Holdings LLC at par aggregating $2.6 million, repay $1.2 million in notes payable to certain related parties and the remainder, if any, for general corporate purposes, as described under “Use of Proceeds” and “Certain relationships and related person transactions;” |

• | the purchase of LLC Interests from the Continuing Equity Owners will reduce their ownership interest from 44,871,794 LLC Interests to 43,589,743; |

• | recognition of the obligation under the Tax Receivable Agreement triggered by the purchase of LLC Interests from each of the Continuing Equity Owners discussed above, and related set-up of deferred tax assets on the Tax Receivable Agreement and on the basis difference associated with the purchase of LLC Interests from each of the Continuing Equity Owners; and |

• | the grant of restricted stock unit awards pursuant to the 2024 Plan to certain of our directors and employees upon completion of this offering with an aggregate grant date fair value of approximately $9.2 million, which awards will cover 472,820 shares of our Class A common stock based on the initial public offering price of 19.50 per share, of which 165,128 shares of our Class A common stock (subject to awards with an aggregate grant date fair value of $3.2 million) will vest in full upon the one-year anniversary of the closing date of this offering, and 307,692 shares of our Class A common stock (subject to an award with a grant date fair value of $6.0 million) will vest in six equal installments on each of the first six anniversaries of the closing date of this offering, in each case subject to the applicable grantee's continued employment or service (as applicable) through the applicable vesting date, and further subject to accelerated vesting upon certain qualifying terminations of employment or service (as applicable) that occur following a change in control (as further described under the caption “Executive compensation—Narrative to summary compensation table—Equity compensation—IPO equity awards”). |

• | Smith Douglas Homes Corp. Other than the inception balance sheet dated as of June 20, 2023 and the interim financial statements dated as of September 30, 2023, the historical financial information of Smith Douglas Homes Corp. has not been included in this prospectus as it is a newly incorporated entity and has had no business transactions or activities to date, besides our initial capitalization. |

• | Smith Douglas Holdings LLC. Because Smith Douglas Homes Corp. will have no interest in any operations other than those of Smith Douglas Holdings LLC, the historical financial information included in this prospectus is that of Smith Douglas Holdings LLC. |

| | | Smith Douglas Holdings LLC historical | | | Reorganization and offering adjustments | | | Notes | | | Smith Douglas Homes Corp. pro forma | |

Assets: | | | | | | | | | ||||

Cash and cash equivalents | | | $10,440 | | | $7 | | | (a) | | | $51,938 |

| | | | | 139,500 | | | (b) | | | |||

| | | | | (23,250) | | | (d) | | | |||

| | | | | (71,000) | | | (f) | | | |||

| | | | | (1,159) | | | (g) | | | |||

| | | | | (2,600) | | | (h) | | | |||

Real estate inventory | | | 220,734 | | | — | | | | | 220,734 | |

Deposits on real estate under option or contract | | | 46,713 | | | — | | | | | 46,713 | |

Real estate not owned | | | 18,333 | | | — | | | | | 18,333 | |

Property and equipment, net | | | 1,656 | | | — | | | | | 1,656 | |

Other assets | | | 15,135 | | | (1,689) | | | (c) | | | 13,446 |

Deferred tax asset | | | — | | | 4,856 | | | (i) | | | 6,166 |

| | | | | 1,310 | | | (i) | | | |||

Goodwill | | | 16,465 | | | | | | | 16,465 | ||

Total assets | | | $329,476 | | | $45,975 | | | | | $375,451 | |

Liabilities and members’ equity: | | | | | | | | | ||||

Liabilities: | | | | | | | | | ||||

Accounts payable | | | $16,428 | | | $— | | | | | $16,428 | |

Customer deposits | | | 9,543 | | | — | | | | | 9,543 | |

Notes payable | | | 76,000 | | | (71,000) | | | (f) | | | 5,000 |

Liabilities related to real estate not owned | | | 18,333 | | | — | | | | | 18,333 | |

Accrued expenses and other liabilities | | | 21,388 | | | (1,159) | | | (g) | | | 24,040 |

| | | | | 3,811 | | | (c) | | | |||

Tax Receivable Agreement liability | | | — | | | 5,241 | | | (i) | | | 5,241 |

Total liabilities | | | 141,692 | | | (63,107) | | | | | 78,585 | |

Members’ equity: | | | | | | | | | ||||

Class A Units | | | 185,184 | | | (161,934) | | | (a) | | | — |

| | | | (23,250) | | | (d) | | | ||||

Class C Units | | | 2,000 | | | (2,000) | | | (h) | | | — |

Class D Units | | | 600 | | | (600) | | | (h) | | | — |

Stockholders’ equity: | | | | | | | | | — | |||

Class A common stock | | | | | 1 | | | (b) | | | 1 | |

Class B common stock | | | | | 7 | | | (a) | | | 7 | |

Additional paid-in-capital | | | | | 161,934 | | | (a) | | | 44,529 | |

| | | | | 139,499 | | | (b) | | | |||

| | | | | (5,500) | | | (c) | | | |||

| | | | | 925 | | | (i) | | | |||

| | | | | (252,329) | | | (e) | | | |||

Total stockholders’ equity attributable to Smith Douglas Homes Corp. | | | 187,784 | | | (143,247) | | | | | 44,537 | |

Non-controlling interest attributable to Smith Douglas Holdings LLC | | | — | | | 252,329 | | | (e) | | | 252,329 |

Total members’/partners’/ stockholders’ equity | | | 187,784 | | | 109,082 | | | | | 296,866 | |

Total liabilities and equity | | | $329,476 | | | $45,975 | | | | | $375,451 |

| | | Smith Douglas Holdings LLC historical | | | Devon Street Homes, L.P. historical for the seven months ended July 31, 2023 | | | Transaction accounting adjustments (Acquisition of Devon Street Homes) | | | Notes | | | Smith Douglas Holdings LLC Pro forma for Devon Street Homes | | | Reorganization and offering adjustments | | | Notes | | | Smith Douglas Homes Corp. pro forma | |

Home closing revenue | | | $547,304 | | | $47,287 | | | $ | | | | | $594,591 | | | $ | | | | | $594,591 | ||

Cost of home closings | | | 388,983 | | | 36,799 | | | 354 | | | (aa) | | | 426,136 | | | | | | | 426,136 | ||

Home closing gross profit | | | 158,321 | | | 10,488 | | | (354) | | | | | 168,455 | | | | | | | 168,455 | |||

Selling, general, and administrative costs | | | 64,901 | | | 4,183 | | | 1,547 | | | (bb) | | | 70,631 | | | 750 | | | (ee) | | | 71,381 |

Equity in income from unconsolidated entities | | | (658) | | | — | | | | | | | (658) | | | | | | | (658) | ||||

Interest expense | | | 795 | | | 726 | | | 3,902 | | | (cc) | | | 5,423 | | | (4,615) | | | (ff) | | | 808 |

Other income, net | | | (217) | | | (133) | | | 137 | | | (dd) | | | (213) | | | | | | | (213) | ||

Income before income taxes | | | 93,500 | | | $5,712 | | | (5,940) | | | | | 93,272 | | | 3,865 | | | | | 97,137 | ||

Provisions for income taxes | | | — | | | 59 | | | | | | | 59 | | | 3,584 | | | (gg) | | | 3,643 | ||

Net income | | | $93,500 | | | $5,653 | | | $(5,940) | | | | | $93,213 | | | $281 | | | | | $93,494 | ||

Net income attributable to non-controlling interest | | | | | | | | | | | | | 79,470 | | | (hh) | | | 79,470 | |||||

Net income attributable to Smith Douglas Homes Corp. | | | $ | | | $ | | | $ | | | | | $ | | | $ | | | | | $14,024 | ||

Pro forma per share data: | | | | | | | | | | | | | | | | | ||||||||

Pro forma net income per share | | | | | | | | | | | | | | | | | ||||||||

Basic and diluted | | | | | | | | | | | | | | | (ii) | | | $1.77 | ||||||

Pro forma weighted average shares used to compute pro forma net income per share | | | | | | | | | | | | | | | | | ||||||||

Basic and diluted | | | | | | | | | | | | | | | (ii) | | | $7,908,718 |

| | | Smith Douglas Holdings LLC historical | | | Devon Street Homes, L.P. historical | | | Transaction accounting adjustments (Acquisition of Devon Street Homes) | | | Notes | | | Smith Douglas Holdings LLC Pro forma for Devon Street Homes | | | Reorganization and offering adjustments | | | Notes | | | Smith Douglas Homes Corp. pro forma | |

Home closing revenue | | | $755,353 | | | $107,888 | | | $ | | | | | $863,241 | | | $ | | | | | $863,241 | ||

Cost of home closings | | | 532,599 | | | 80,390 | | | 4,252 | | | (aa) | | | 617,241 | | | | | | | 617,241 | ||

Home closing gross profit | | | 222,754 | | | 27,498 | | | (4,252) | | | | | 246,000 | | | | | | | 246,000 | |||

Selling, general, and administrative costs | | | 83,269 | | | 7,640 | | | 2,063 | | | (bb) | | | 92,972 | | | 4,220 | | | (ee) | | | 97,192 |

Equity in income from unconsolidated entities | | | (1,120) | | | — | | | | | | | (1,120) | | | | | | | (1,120) | ||||

Interest expense | | | 734 | | | 460 | | | 5,687 | | | (cc) | | | 6,881 | | | (5,865) | | | (ff) | | | 1,016 |

Other income, net | | | (573) | | | (117) | | | 217 | | | (dd) | | | (473) | | | | | | | (473) | ||

Income before income taxes | | | 140,444 | | | 19,515 | | | (12,219) | | | | | 147,740 | | | 1,645 | | | | | 149,385 | ||

Provisions for income taxes | | | — | | | 193 | | | | | | | 193 | | | 5,409 | | | (gg) | | | 5,602 | ||

Net income | | | $140,444 | | | $19,322 | | | $(12,219) | | | | | $147,547 | | | $(3,764) | | | | | $143,783 | ||

Net income attributable to non-controlling interest | | | | | | | | | | | | | 122,216 | | | (hh) | | | 122,216 | |||||

Net income attributable to Smith Douglas Homes Corp. | | | $ | | | $ | | | $ | | | | | $ | | | $ | | | | | $21,567 | ||

Pro forma per share data: | | | | | | | | | | | | | | | | | ||||||||

Pro forma net income per share | | | | | | | | | | | | | | | | | ||||||||

Basic and diluted | | | | | | | | | | | | | | | (ii) | | | $2.80 | ||||||

Pro forma weighted average shares used to compute pro forma net income per share | | | | | | | | | | | | | | | | | ||||||||

Basic and diluted | | | | | | | | | | | | | | | (ii) | | | $7,692,308 |

Cash consideration(1) | | | $74,868 |

Promissory note payable | | | 5,000 |

Contingent consideration(2) | | | 3,000 |

Total estimated consideration to be paid | | | $82,868 |

(1) | The cash consideration is funded by $2.9 million of cash on hand and $72.0 million of draws on our Existing Credit Facility. |

(2) | The contingent consideration represents management’s preliminary estimate of the fair value of the future payment to be made to the former owner of Devon Street Homes under the terms of the Gross Margin Earnout feature included in the executed APA for the Devon Street Homes Acquisition. Per the terms of the Gross Margin Earnout feature, the seller is entitled to receive a one time payment in the first quarter of 2025 based on the newly established Houston division’s gross margin (as defined) for the year ending December 31, 2024. The payout will be determined in accordance with the Gross Margin Calculation Payout Grid and ranges from a minimum of zero to a maximum of $5.0 million. |

Real estate inventory | | | $60,216 |

Deposits on real estate under option or contract | | | 7,193 |

Property and equipment, net | | | 69 |

Goodwill | | | 16,465 |

Other assets | | | 324 |

Accounts payable | | | (857) |

Customer deposits | | | (181) |

Accrued expenses and other liabilities | | | (361) |

Fair value of consideration transferred | | | $82,868 |

(a) | Reflects the net effect on cash and cash equivalents and stockholders’ equity of the issuance of shares of Class B common stock to the Continuing Equity Owners, which is equal to the number of LLC Interests held by such Continuing Equity Owners at the time of such issuance of Class B common stock, for nominal consideration. |

(b) | Reflects the net effect on cash and cash equivalents and stockholders’ equity of the receipt of offering proceeds to us of $139.5 million, based on the sale of 7,692,308 shares of Class A common stock (or 8,846,154 shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock) at the initial public offering price of $19.50 per share (which is the midpoint of the estimated price range set forth on the cover pages of this prospectus), after deducting the estimated underwriting discount. See “Use of proceeds.” |

(c) | Reflects the expenses incurred in connection with the Transactions, including this offering, that Smith Douglas Holdings LLC will bear or reimburse to Smith Douglas Homes Corp. |

(d) | Reflects the purchase of 1,282,051 LLC Interests from the Continuing Equity Owners on a pro rata basis for $23.2 million in aggregate (or 2,435,897 LLC Interests from the Continuing Equity Owners for $44.2 million in aggregate if the underwriters exercise in full their option to purchase additional shares of Class A common stock) at a price per unit equal to the initial public offering price per share of Class A common stock in this offering less the underwriting discount. |

(e) | Upon completion of the Transactions, we will become the sole managing member of Smith Douglas Holdings LLC. Although we will have a minority economic interest in Smith Douglas Holdings LLC, we will have the sole voting interest in, and control of the management of, Smith Douglas Holdings LLC. As a result, we will consolidate the financial results of Smith Douglas Holdings LLC and will report a non-controlling interest related to the interests in Smith Douglas Holdings LLC held by the Continuing Equity Holders in our consolidated balance sheet. Immediately following the Transactions, the economic interests held by the noncontrolling interest will be approximately 85.0%. If the underwriters were to exercise their option to purchase additional shares of our Class A common stock in full, the economic interests held by the noncontrolling interest would be approximately 82.7%. |

(f) | Reflects repayment of all outstanding borrowings under our Existing Credit Facility on September 30, 2023, as if the Offering had occurred on that date. See “Use of proceeds.” |

(g) | Reflects a decrease in cash and cash equivalents and accrued expenses and other liabilities for the repayment of approximately $1.2 million in notes payable to related parties as if it occurred on September 30, 2023. See “Use of proceeds.” |

(h) | Reflects a decrease in cash and cash equivalents and members' equity for repurchases of 2,000 Class C Units and 600 Class D Units as if they occurred on September 30, 2023. See “Use of proceeds.” |

(i) | Reflects adjustments for deferred tax assets and obligations under the Tax Receivable Agreement triggered by the purchase of LLC Interests from each of the Continuing Equity Owners, as described in greater detail under “Our organizational structure” and “Certain relationships and related person transactions—Tax Receivable Agreement,” in connection with the completion of this offering. The pro forma adjustments reflect the following: |

• | Estimated deferred tax benefit of approximately $4.9 million recognized for the tax benefit of the difference in basis between reporting under generally accepted accounting principles and income tax reporting purposes associated with the purchase of LLC Interests from each of the Continuing Equity Owners. In connection with this purchase, we intend to make an IRC 754 election, which will allow us to succeed to the aggregate historical tax basis of the LLC Interests. The total tax benefit from such historical tax basis, including any increases thereto as a result of the Transactions, will primarily be amortized over 15 years pursuant to Section 197 of the U.S. Internal Revenue Code of 1986, as amended (the “Code”), subject to further allocation adjustments to be made at the time of preparation of our tax returns. |

• | Estimated deferred tax benefit of $1.3 million associated with the obligation under the Tax Receivable Agreement. |

• | Corresponding liability under the Tax Receivable Agreement triggered by the purchase of LLC Interests from each of the Continuing Equity Owners of $5.2 million representing 85.0% of the amount of tax benefits that Smith Douglas Homes Corp. expects to realize related to certain tax basis adjustments and payments made under the Tax Receivable Agreement. |

• | Credit to Additional paid-in capital associated with the deferred tax assets ($4.9 million and $1.3 million) reduced by a charge for the obligation under the Tax Receivable Agreement of $5.2 million, for a total net credit of $0.9 million. |

(aa) | Reflects an increase in cost of home closings due to the $8.5 million fair value adjustment of real estate inventory completed and under construction as of January 1, 2022. This adjustment is being relieved into cost of home closings on a ratable basis over an estimated 48 months, with half of the adjustment relieved in the first 12 months and the remaining half relieved in the following 36 months. |