Exhibit 99.3

THIRD QUARTER 2022 Fixed Income Supplemental The Hub Hillcrest Market San Diego, CA Mellody Farm Chicago, IL Village at La Floresta Los Angeles, CA The Field at Commonwealth Washington, D.C. Prestonbrook Crossing Dallas, TX East San Marco Jacksonville, FL Regency Centers.

Highlights Third Quarter 2022 Reported Nareit FFO of $1.01 per diluted share and Core Operating Earnings of $0.94 per diluted share for the third quarter Raised 2022 Nareit FFO guidance to a range of $4.00 to $4.03 per diluted share Raised 2022 Core Operating Earnings guidance to a range of $3.75 to $3.78 per diluted share, representing a 7% year-over-year increase at the midpoint excluding prior year collections Increased Same Property NOI excluding lease termination fees and prior year collections by 2.6% during the third quarter over the same period a year ago Increased Same Property percent leased by 20 basis points sequentially to 94.7%, and Same Property small shop percent leased by 40 basis points sequentially to 91.4% Executed quarterly volume of 2.3 million square feet of comparable new and renewal leases during the third quarter at a blended cash rent spread of +7.0% Net project costs for Regency’s in-process development and redevelopment projects were approximately $398 million as of September 30, 2022 Achieved pro-rata net debt-to-operating EBITDAre of 5.0x as of September 30, 2022 In September, Moody’s Investors Service affirmed its Baa1 senior unsecured debt rating for Regency and revised its outlook from stable to positive Subsequent to quarter end, on October 12, 2022, completed the acquisition of East Meadow Plaza in East Meadow, NY at a gross purchase price of $30 million at Regency’s share Subsequent to quarter end, on November 2, 2022, Regency’s Board of Directors (the “Board”) declared a quarterly cash dividend on the Company’s common stock of $0.65 per share, an increase of 4% from the prior quarterly dividend 2

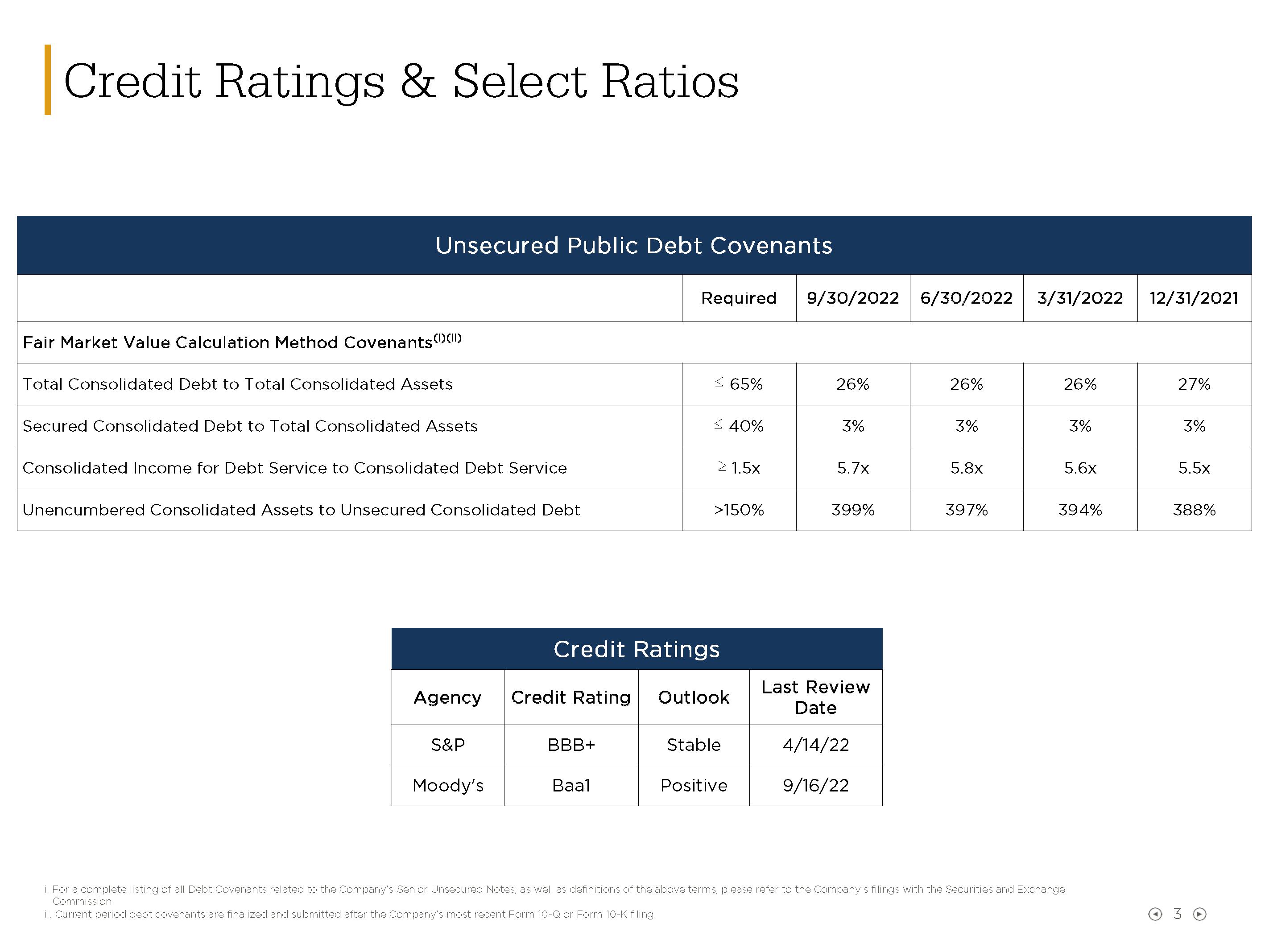

Credit Ratings & Select Ratios Credit Ratings Agency Credit Rating Outlook Last Review Date S&P BBB+ Stable 4/14/22 Moody's Baa1 Positive 9/16/22 i. For a complete listing of all Debt Covenants related to the Company’s Senior Unsecured Notes, as well as definitions of the above terms, please refer to the Company’s filings with the Securities and Exchange Commission. ii. Current period debt covenants are finalized and submitted after the Company’s most recent Form 10-Q or Form 10-K filing. 3 Unsecured Public Debt Covenants Required 9/30/2022 6/30/2022 3/31/2022 12/31/2021 Fair Market Value Calculation Method Covenants(i)(ii) Total Consolidated Debt to Total Consolidated Assets ≤ 65% 26% 26% 26% 27% Secured Consolidated Debt to Total Consolidated Assets ≤ 40% 3% 3% 3% 3% Consolidated Income for Debt Service to Consolidated Debt Service ≥ 1.5x 5.7x 5.8x 5.6x 5.5x Unencumbered Consolidated Assets to Unsecured Consolidated Debt >150% 399% 397% 394% 388%

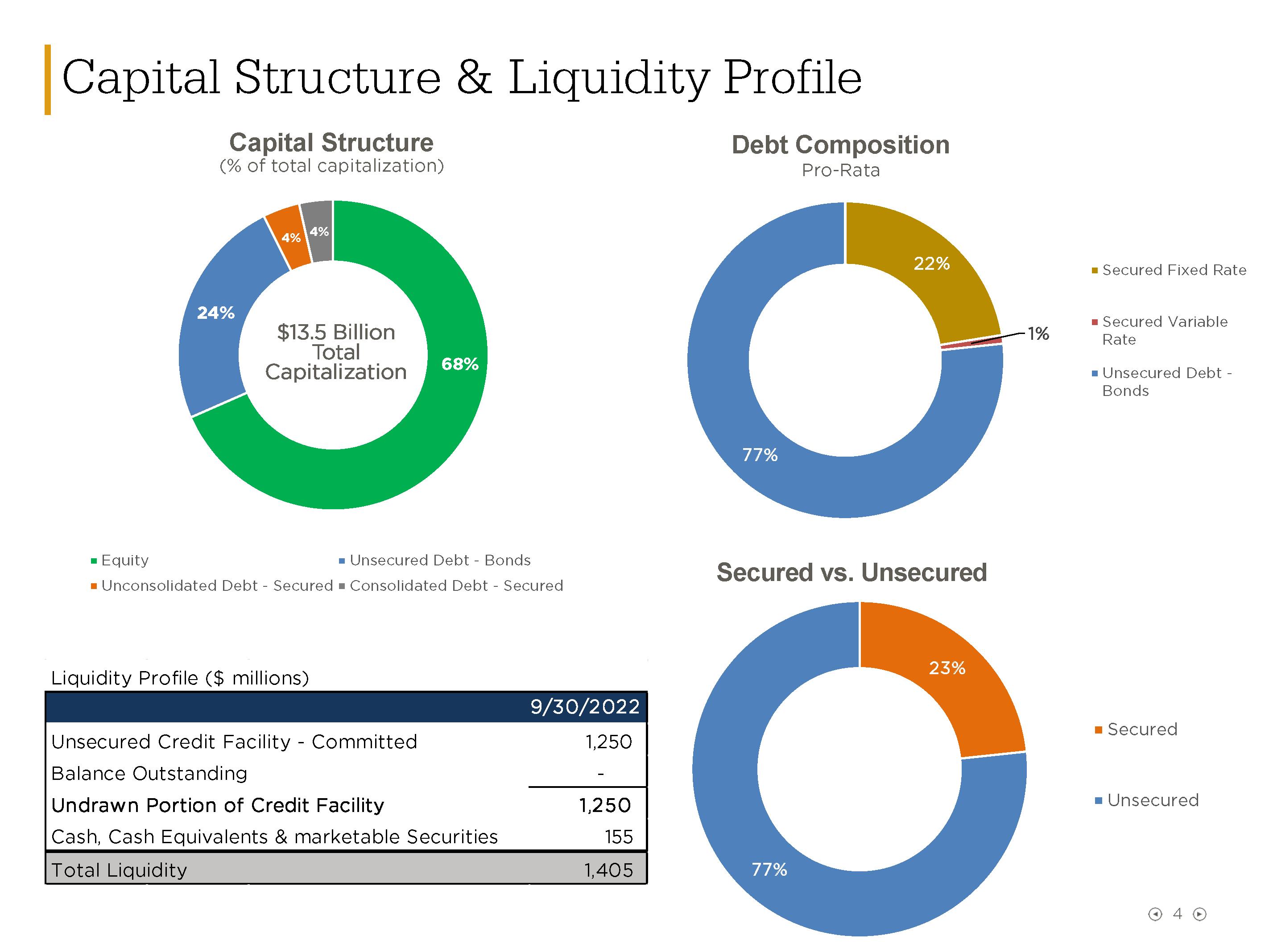

Capital Structure & Liquidity Profile Capital Structure (% of total capitalization) Debt Composition Pro-Rata Secured vs. Unsecured 4 $13.5 Billion Total Capitalization 68% 24% 4% 4% Equity Unsecured Debt - Bonds Unconsolidated Debt - Secured Consolidated Debt - Secured 22% 1% 77% Secured Fixed Rate Secured Variable Rate Unsecured Debt - Bonds 23% 77% Secured Unsecured Liquidity Profile ($ millions) Unsecured Credit Facility - Committed 1,250 Balance Outstanding - Undrawn Portion of Credit Facility 1,250 Cash, Cash Equivalents & marketable Securities 155 Total Liquidity 1,405

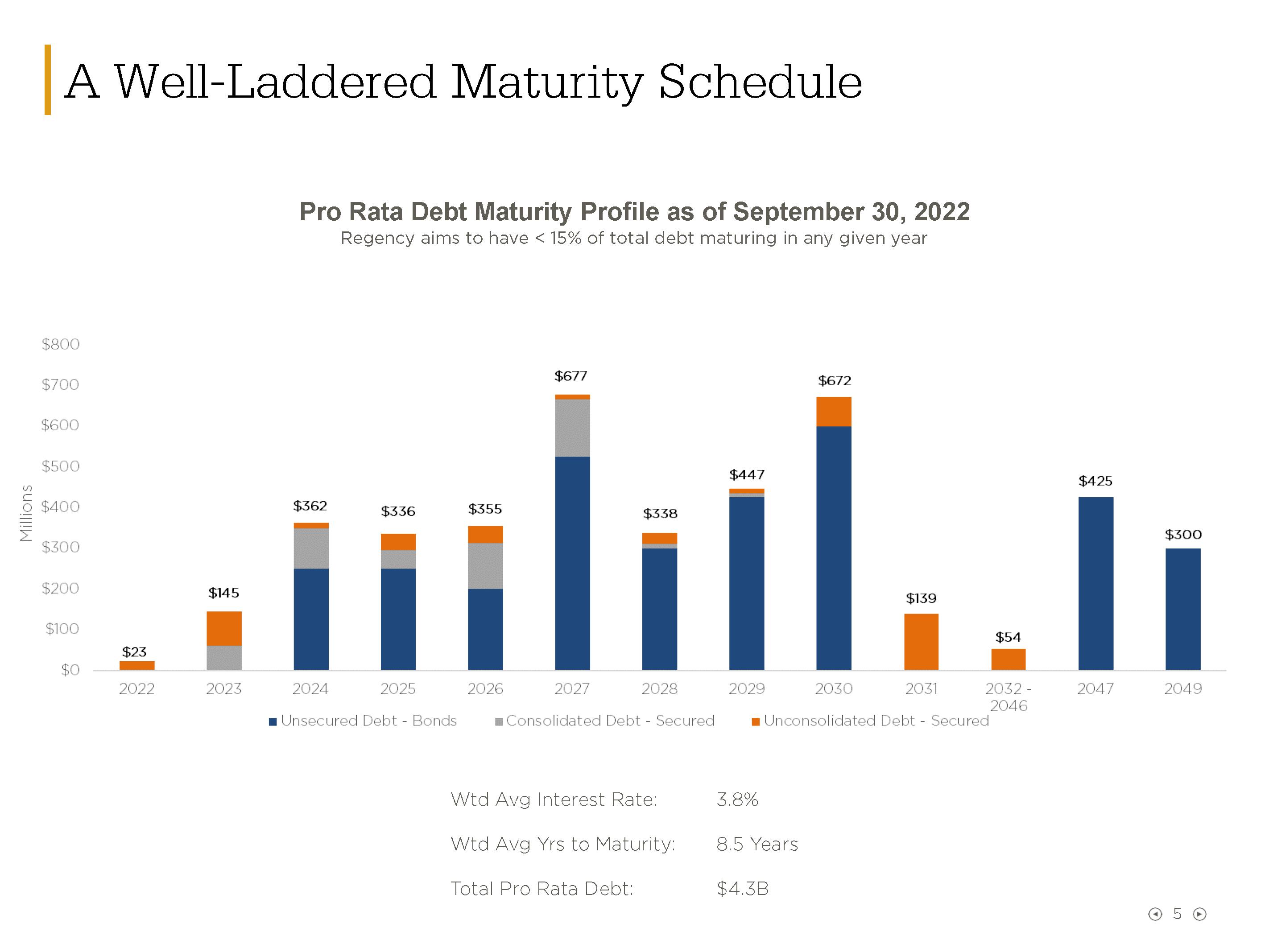

A Well-Laddered Maturity Schedule Pro Rata Debt Maturity Profile as of September 30, 2022 Regency aims to have < 15% of total debt maturing in any given year Wtd Avg Interest Rate: 3.8% Wtd Avg Yrs to Maturity: 8.5 Years Total Pro Rata Debt: $4.3B 5 $23 2022 $124 2023 $362 2024 $336 2025 $355 2026 $677 2027 $338 2028 $447 2029 $672 2030 $139 2031 $54 2032 2046 $425 2047 $300 2049 Unsecured Debt - Bonds Consolidated Debt - Secured Unconsolidated Debt - Secured

Follow us Third Quarter 2022 Earnings Conference Call Friday, November 4th, 2022 Time: 10:00 AM ET Dial#: 877-407-0789 or 201 689-8562 Webcast: investors.regencycenters.com Contact Information: Christy McElroy Senior Vice President, Capital Markets 904-598-7616 ChristyMcElroy@RegencyCenters.com Forward-Looking Statements Certain statements in this document regarding anticipated financial, business, legal or other outcomes including business and market conditions, outlook and other similar statements relating to Regency’s future events, developments, or financial or operational performance or results, are “forward-looking statements” made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. These forward-looking statements are identified by the use of words such as “may,” “will,” “should,” “expect,” “estimate,” “believe,” “intend,” “forecast,” “anticipate,” “guidance,” and other similar language. However, the absence of these or similar words or expressions does not mean a statement is not forward-looking. While we believe these forward-looking statements are reasonable when made, forward-looking statements are not guarantees of future performance or events and undue reliance should not be placed on these statements. Although we believe the expectations reflected in any forwardlooking statements are based on reasonable assumptions, we can give no assurance these expectations will be attained, and it is possible actual results may differ materially from those indicated by these forward-looking statements due to a variety of risks and uncertainties. Our operations are subject to a number of risks and uncertainties including, but not limited to, those Risk factors described in our SEC filings. When considering an investment in our securities, you should carefully read and consider these risks, together with all other information in our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and our other filings and submissions to the SEC. If any of the events described in the risk factors actually occur, our business, financial condition or operating results, as well as the market price of our securities, could be materially adversely affected. Forwardlooking statements are only as of the date they are made, and Regency undertakes no duty to update its forward-looking statements except as required by law. These risks and events include, without limitation: Risk Factors Relating to Current Economic Conditions Rising interest rates, as we have seen in 2022, may adversely affect the cost of and our ability to borrow, the valuation of our real estate, and our stock price. Current economic conditions and challenges may adversely impact our tenants, and, therefore, our ability to lease space and the level of rent we may be able to charge. Risks Related to Pandemics or other Health Crises Pandemics or other health crises, such as the COVID-19 pandemic, may adversely affect our tenants’ financial condition, the profitability of our properties, and our access to the capital markets and could have a material adverse effect on our business, results of operations, cash flows and financial condition. Risk Factors Related to Operating Retail-Based Shopping Centers Economic and market conditions may adversely affect the retail industry and consequently reduce our revenues and cash flow, and increase our operating expenses. Shifts in retail trends, sales, and delivery methods between brick and mortar stores, e-commerce, home delivery, and curbside pickup may adversely impact our revenues and cash flows. Changing economic and retail market conditions in geographic areas where our properties are concentrated may reduce our revenues and cash flow. In addition, labor challenges and supply delays and shortages due to a variety of macroeconomic factors, including inflationary pressures, could affect the retail industry. Our success depends on the continued presence and success of our “anchor” tenants. A significant percentage of our revenues are derived from smaller “shop space” tenants and our net income may be adversely impacted if our smaller shop tenants are not successful. We may be unable to collect balances due from tenants in bankruptcy. Many of our costs and expenses associated with operating our properties may remain constant or increase, even if our lease income decreases. Compliance with the Americans with Disabilities Act and fire, safety and other regulations may have a negative effect on us. Risk Factors Related to Real Estate Investments Our real estate assets may decline in value and be subject to impairment losses which may reduce our net income. We face risks associated with development, redevelopment and expansion of properties. We face risks associated with the development of mixed-use commercial properties. We face risks associated with the acquisition of properties. We may be unable to sell properties when desired because of market conditions. Changes in tax laws could impact our acquisition or disposition of real estate. Risk Factors Related to the Environment Affecting Our Properties Climate change may adversely impact our properties directly, and may lead to additional compliance obligations and costs as well as additional taxes and fees. Geographic concentration of our properties makes our business more vulnerable to natural disasters, severe weather conditions and climate change. Costs of environmental remediation may impact our financial performance and reduce our cash flow. Risk Factors Related to Corporate Matters An increased focus on metrics and reporting relating to environmental, social, and governance (“ESG”) factors may impose additional costs and expose us to new risks. An uninsured loss or a loss that exceeds the insurance coverage on our properties may subject us to loss of capital and revenue on those properties. Failure to attract and retain key personnel may adversely affect our business and operations. The unauthorized access, use, theft or destruction of tenant or employee personal, financial or other data or of Regency’s proprietary or confidential information stored in our information systems or by third parties on our behalf could impact our reputation and brand and expose us to potential liability and loss of revenues. Risk Factors Related to Our Partnerships and Joint Ventures We do not have voting control over all of the properties owned in our co-investment partnerships and joint ventures, so we are unable to ensure that our objectives will be pursued. The termination of our partnerships may adversely affect our cash flow, operating results, and our ability to make distributions to stock and unit holders. Risk Factors Related to Funding Strategies and Capital Structure Our ability to sell properties and fund acquisitions and developments may be adversely impacted by higher market capitalization rates and lower NOI at our properties which may dilute earnings. We depend on external sources of capital, which may not be available in the future on favorable terms or at all. Our debt financing may adversely affect our business and financial condition. Covenants in our debt agreements may restrict our operating activities and adversely affect our financial condition. Increases in interest rates would cause our borrowing costs to rise and negatively impact our results of operations. Hedging activity may expose us to risks, including the risks that a counterparty will not perform and that the hedge will not yield the economic benefits we anticipate, which may adversely affect us. The interest rates on our Unsecured Credit facilities as well as on our variable rate mortgages and interest rate swaps might change based on changes to the method in which LIBOR or its replacement rate is determined. Risk Factors Related to the Market Price for Our Securities Changes in economic and market conditions may adversely affect the market price of our securities. There is no assurance that we will continue to pay dividends at historical rates. Risk Factors Relating to the Company’s Qualification as a REIT If the Company fails to qualify as a REIT for federal income tax purposes, it would be subject to federal income tax at regular corporate rates. Dividends paid by REITs generally do not qualify for reduced tax rates. Certain foreign stockholders may be subject to U.S. federal income tax on gain recognized on a disposition of our common stock if we do not qualify as a “domestically controlled” REIT. Legislative or other actions affecting REITs may have a negative effect on us. Complying with REIT requirements may limit our ability to hedge effectively and may cause us to incur tax liabilities. Risk Factors Related to the Company’s Common Stock Restrictions on the ownership of the Company’s capital stock to preserve its REIT status may delay or prevent a change in control. The issuance of the Company's capital stock may delay or prevent a change in control. Ownership in the Company may be diluted in the future. Non-GAAP disclosure We believe these non-GAAP measures provide useful information to our Board of Directors, management and investors regarding certain trends relating to our financial condition and results of operations. Our management uses these non-GAAP measures to compare our performance to that of prior periods for trend analyses, purposes of determining management incentive compensation and budgeting, forecasting and planning purposes. We do not consider non-GAAP measures an alternative to financial measures determined in accordance with GAAP, rather they supplement GAAP measures by providing additional information we believe to be useful to our shareholders. The principal limitation of these non-GAAP financial measures is they may exclude significant expense and income items that are required by GAAP to be recognized in our consolidated financial statements. In addition, they reflect the exercise of management’s judgment about which expense and income items are excluded or included in determining these non-GAAP financial measures. In order to compensate for these limitations, reconciliations of the non-GAAP financial measures we use to their most directly comparable GAAP measures are provided. Non-GAAP financial measures should not be relied upon in evaluating the financial condition, results of operations or future prospects of the Company. Nareit FFO is a commonly used measure of REIT performance, which the National Association of Real Estate Investment Trusts (“Nareit”) defines as net income, computed in accordance with GAAP, excluding gains on sale and impairments of real estate, net of tax, plus depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. Regency computes Nareit FFO for all periods presented in accordance with Nareit's definition. Since Nareit FFO excludes depreciation and amortization and gains on sales and impairments of real estate, it provides a performance measure that, when compared year over year, reflects the impact on operations from trends in occupancy rates, rental rates, operating costs, acquisition and development activities, and financing costs. This provides a perspective of the Company’s financial performance not immediately apparent from net income determined in accordance with GAAP. Thus, Nareit FFO is a supplemental non-GAAP financial measure of the Company's operating performance, which does not represent cash generated from operating activities in accordance with GAAP; and, therefore, should not be considered a substitute measure of cash flows from operations. The Company provides a reconciliation of Net Income Attributable to Common Stockholders to Nareit FFO. Core Operating Earnings is an additional performance measure that excludes from Nareit FFO: (i) transaction related income or expenses (ii) gains or losses from the early extinguishment of debt; (iii) certain non-cash components of earnings derived from above and below market rent amortization, straight-line rents, and amortization of mark-to- market of debt adjustments; and (iv) other amounts as they occur. The Company provides a reconciliation of Net Income to Nareit FFO to Core Operating Earnings. 6